Financial Decision Making: Roast Ltd. Performance Evaluation

VerifiedAdded on 2023/01/17

|17

|4671

|67

Report

AI Summary

This report provides a detailed financial analysis of Roast Ltd., focusing on its performance within the UK coffee industry. It examines the company's financial statements, including the profit and loss statement, balance sheet, and cash flow statement, to evaluate its profitability, liquidity, and financial position. The analysis incorporates ratio analysis, such as gross profit margin, operating profit margin, net profit ratio, current ratio, quick ratio, and debt-to-equity ratio, to assess the company's operational efficiency and financial health. Furthermore, the report explores investment appraisal techniques to assess the potential acquisition of Roast Ltd. by Starbucks. The conclusion suggests that Starbucks should acquire Roast Ltd. based on its positive financial performance, and market growth potential. The report also provides an overview of the UK coffee industry, its challenges, and opportunities, including the impact of Brexit on the sector.

Financial Decision

Making

Making

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

EXECUTIVE SUMMARY.............................................................................................................3

MAIN BODY...................................................................................................................................3

PART 1 – Industry Overview..........................................................................................................3

PART 2 – Business Performance Analysis......................................................................................5

2.1 Statement of Profits & Loss...................................................................................................5

2.2 Statement of Financial Position.............................................................................................7

2.3 Statement of Cash Flows ......................................................................................................9

PART 3 – Investment Appraisal ...................................................................................................10

3.1.a Management Forecast.......................................................................................................10

3.1.b Investment Appraisal Techniques.....................................................................................10

3.2 Sources of Finance...............................................................................................................11

......................................................................................................................................................13

REFERENCES .............................................................................................................................14

APPENDIX ...................................................................................................................................16

EXECUTIVE SUMMARY.............................................................................................................3

MAIN BODY...................................................................................................................................3

PART 1 – Industry Overview..........................................................................................................3

PART 2 – Business Performance Analysis......................................................................................5

2.1 Statement of Profits & Loss...................................................................................................5

2.2 Statement of Financial Position.............................................................................................7

2.3 Statement of Cash Flows ......................................................................................................9

PART 3 – Investment Appraisal ...................................................................................................10

3.1.a Management Forecast.......................................................................................................10

3.1.b Investment Appraisal Techniques.....................................................................................10

3.2 Sources of Finance...............................................................................................................11

......................................................................................................................................................13

REFERENCES .............................................................................................................................14

APPENDIX ...................................................................................................................................16

EXECUTIVE SUMMARY

This report summarised that Coffee industry of UK perform well or contribute in the

economy through generating revenue. Main purpose of this study is to evaluate the financial

performance of Roast Ltd. On the basis of the results, it has been recommend that Starbucks of

UK should acquisition Roast Ltd. All the financial statements such as Profit & Loss, Balance

sheet and cash flows critically analysed or evaluate the overall performance of the company. In

addition, with the help of various appraisal techniques for the investment helps in evaluating and

making effective decision regarding acquisition of Roast Ltd by Starbucks.

MAIN BODY

PART 1 – Industry Overview

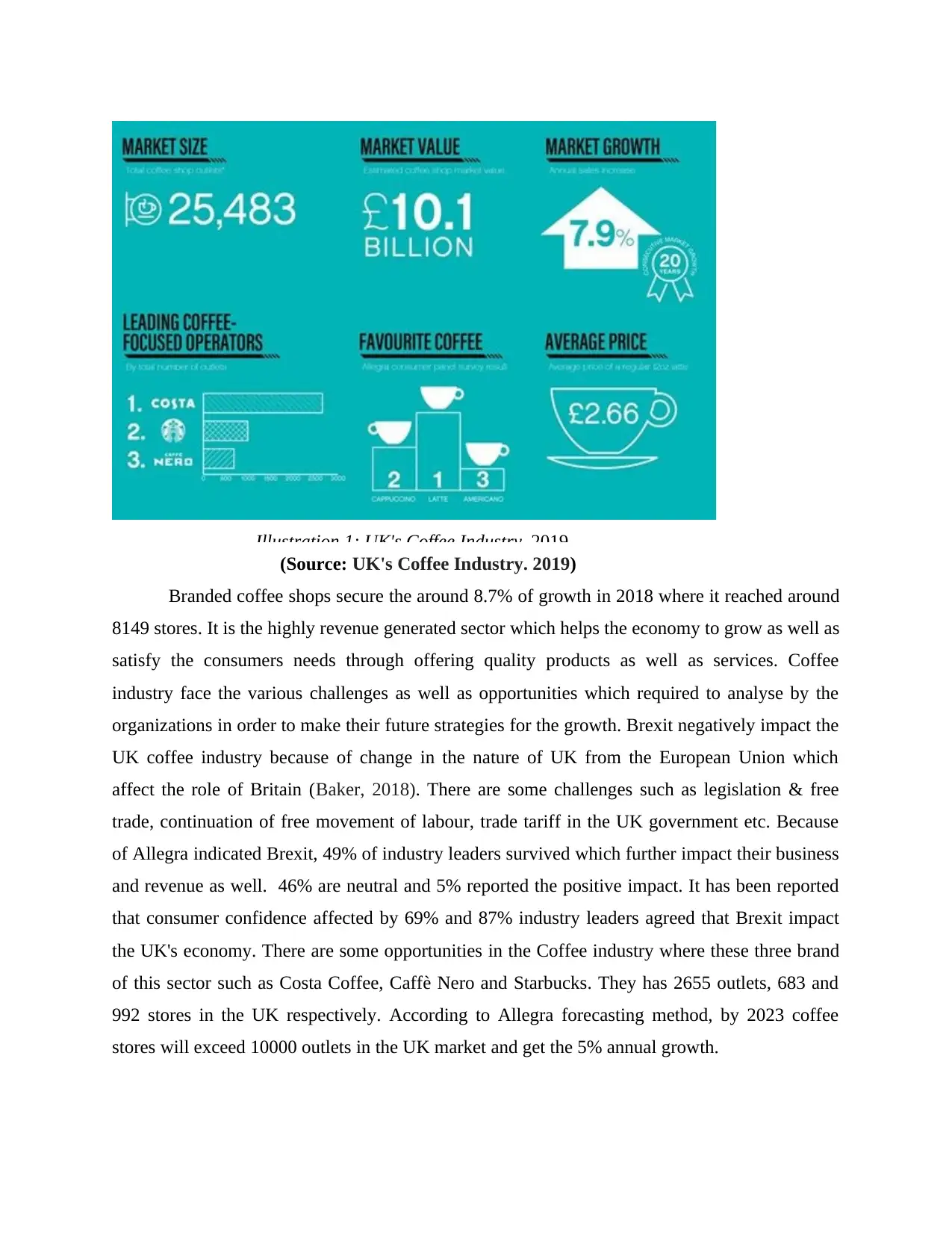

In the Coffee industry, coffee is the second most traded product around $ 20 billion

revenue this industry generate as well as they produce 210,325 jobs in the UK. This sector

achieve the 20 years continuous sustainable growth where it grow around 7.9% for the period of

2018. Almost £ 10.1 billion coffee shop open in the UK and market size around 25,483 and

average price of regular coffee is £ 2.66. There are some leading coffee operators such as Costa,

Nero and Starbucks (UK's Coffee Industry, 2019). One of the favourite coffee products are

LATTE which is on top and second most demanded is CAPPUCCINO and third one is

AMARICANO.

This report summarised that Coffee industry of UK perform well or contribute in the

economy through generating revenue. Main purpose of this study is to evaluate the financial

performance of Roast Ltd. On the basis of the results, it has been recommend that Starbucks of

UK should acquisition Roast Ltd. All the financial statements such as Profit & Loss, Balance

sheet and cash flows critically analysed or evaluate the overall performance of the company. In

addition, with the help of various appraisal techniques for the investment helps in evaluating and

making effective decision regarding acquisition of Roast Ltd by Starbucks.

MAIN BODY

PART 1 – Industry Overview

In the Coffee industry, coffee is the second most traded product around $ 20 billion

revenue this industry generate as well as they produce 210,325 jobs in the UK. This sector

achieve the 20 years continuous sustainable growth where it grow around 7.9% for the period of

2018. Almost £ 10.1 billion coffee shop open in the UK and market size around 25,483 and

average price of regular coffee is £ 2.66. There are some leading coffee operators such as Costa,

Nero and Starbucks (UK's Coffee Industry, 2019). One of the favourite coffee products are

LATTE which is on top and second most demanded is CAPPUCCINO and third one is

AMARICANO.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Illustration 1: UK's Coffee Industry, 2019.

(Source: UK's Coffee Industry. 2019)

Branded coffee shops secure the around 8.7% of growth in 2018 where it reached around

8149 stores. It is the highly revenue generated sector which helps the economy to grow as well as

satisfy the consumers needs through offering quality products as well as services. Coffee

industry face the various challenges as well as opportunities which required to analyse by the

organizations in order to make their future strategies for the growth. Brexit negatively impact the

UK coffee industry because of change in the nature of UK from the European Union which

affect the role of Britain (Baker, 2018). There are some challenges such as legislation & free

trade, continuation of free movement of labour, trade tariff in the UK government etc. Because

of Allegra indicated Brexit, 49% of industry leaders survived which further impact their business

and revenue as well. 46% are neutral and 5% reported the positive impact. It has been reported

that consumer confidence affected by 69% and 87% industry leaders agreed that Brexit impact

the UK's economy. There are some opportunities in the Coffee industry where these three brand

of this sector such as Costa Coffee, Caffè Nero and Starbucks. They has 2655 outlets, 683 and

992 stores in the UK respectively. According to Allegra forecasting method, by 2023 coffee

stores will exceed 10000 outlets in the UK market and get the 5% annual growth.

(Source: UK's Coffee Industry. 2019)

Branded coffee shops secure the around 8.7% of growth in 2018 where it reached around

8149 stores. It is the highly revenue generated sector which helps the economy to grow as well as

satisfy the consumers needs through offering quality products as well as services. Coffee

industry face the various challenges as well as opportunities which required to analyse by the

organizations in order to make their future strategies for the growth. Brexit negatively impact the

UK coffee industry because of change in the nature of UK from the European Union which

affect the role of Britain (Baker, 2018). There are some challenges such as legislation & free

trade, continuation of free movement of labour, trade tariff in the UK government etc. Because

of Allegra indicated Brexit, 49% of industry leaders survived which further impact their business

and revenue as well. 46% are neutral and 5% reported the positive impact. It has been reported

that consumer confidence affected by 69% and 87% industry leaders agreed that Brexit impact

the UK's economy. There are some opportunities in the Coffee industry where these three brand

of this sector such as Costa Coffee, Caffè Nero and Starbucks. They has 2655 outlets, 683 and

992 stores in the UK respectively. According to Allegra forecasting method, by 2023 coffee

stores will exceed 10000 outlets in the UK market and get the 5% annual growth.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

PART 2 – Business Performance Analysis

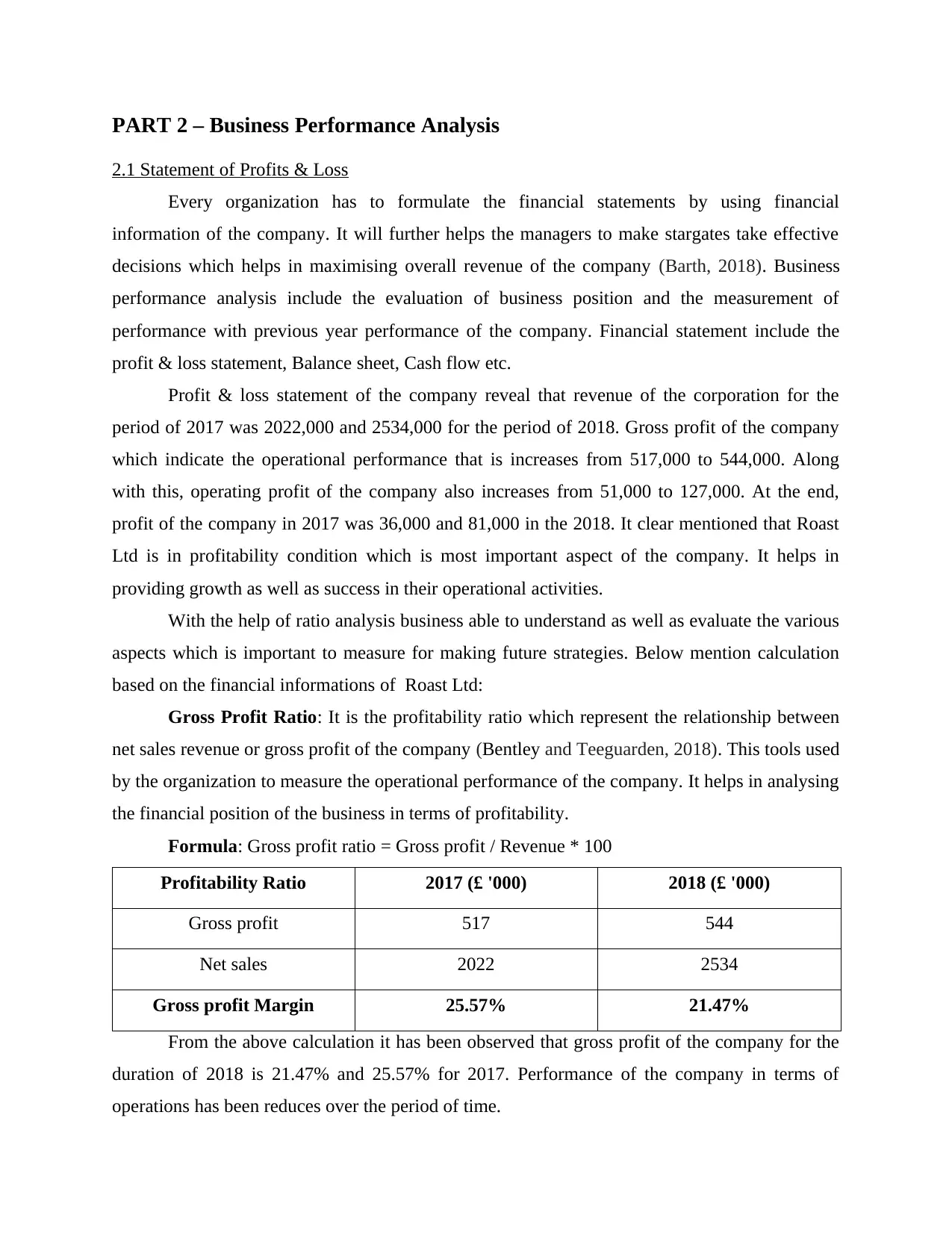

2.1 Statement of Profits & Loss

Every organization has to formulate the financial statements by using financial

information of the company. It will further helps the managers to make stargates take effective

decisions which helps in maximising overall revenue of the company (Barth, 2018). Business

performance analysis include the evaluation of business position and the measurement of

performance with previous year performance of the company. Financial statement include the

profit & loss statement, Balance sheet, Cash flow etc.

Profit & loss statement of the company reveal that revenue of the corporation for the

period of 2017 was 2022,000 and 2534,000 for the period of 2018. Gross profit of the company

which indicate the operational performance that is increases from 517,000 to 544,000. Along

with this, operating profit of the company also increases from 51,000 to 127,000. At the end,

profit of the company in 2017 was 36,000 and 81,000 in the 2018. It clear mentioned that Roast

Ltd is in profitability condition which is most important aspect of the company. It helps in

providing growth as well as success in their operational activities.

With the help of ratio analysis business able to understand as well as evaluate the various

aspects which is important to measure for making future strategies. Below mention calculation

based on the financial informations of Roast Ltd:

Gross Profit Ratio: It is the profitability ratio which represent the relationship between

net sales revenue or gross profit of the company (Bentley and Teeguarden, 2018). This tools used

by the organization to measure the operational performance of the company. It helps in analysing

the financial position of the business in terms of profitability.

Formula: Gross profit ratio = Gross profit / Revenue * 100

Profitability Ratio 2017 (£ '000) 2018 (£ '000)

Gross profit 517 544

Net sales 2022 2534

Gross profit Margin 25.57% 21.47%

From the above calculation it has been observed that gross profit of the company for the

duration of 2018 is 21.47% and 25.57% for 2017. Performance of the company in terms of

operations has been reduces over the period of time.

2.1 Statement of Profits & Loss

Every organization has to formulate the financial statements by using financial

information of the company. It will further helps the managers to make stargates take effective

decisions which helps in maximising overall revenue of the company (Barth, 2018). Business

performance analysis include the evaluation of business position and the measurement of

performance with previous year performance of the company. Financial statement include the

profit & loss statement, Balance sheet, Cash flow etc.

Profit & loss statement of the company reveal that revenue of the corporation for the

period of 2017 was 2022,000 and 2534,000 for the period of 2018. Gross profit of the company

which indicate the operational performance that is increases from 517,000 to 544,000. Along

with this, operating profit of the company also increases from 51,000 to 127,000. At the end,

profit of the company in 2017 was 36,000 and 81,000 in the 2018. It clear mentioned that Roast

Ltd is in profitability condition which is most important aspect of the company. It helps in

providing growth as well as success in their operational activities.

With the help of ratio analysis business able to understand as well as evaluate the various

aspects which is important to measure for making future strategies. Below mention calculation

based on the financial informations of Roast Ltd:

Gross Profit Ratio: It is the profitability ratio which represent the relationship between

net sales revenue or gross profit of the company (Bentley and Teeguarden, 2018). This tools used

by the organization to measure the operational performance of the company. It helps in analysing

the financial position of the business in terms of profitability.

Formula: Gross profit ratio = Gross profit / Revenue * 100

Profitability Ratio 2017 (£ '000) 2018 (£ '000)

Gross profit 517 544

Net sales 2022 2534

Gross profit Margin 25.57% 21.47%

From the above calculation it has been observed that gross profit of the company for the

duration of 2018 is 21.47% and 25.57% for 2017. Performance of the company in terms of

operations has been reduces over the period of time.

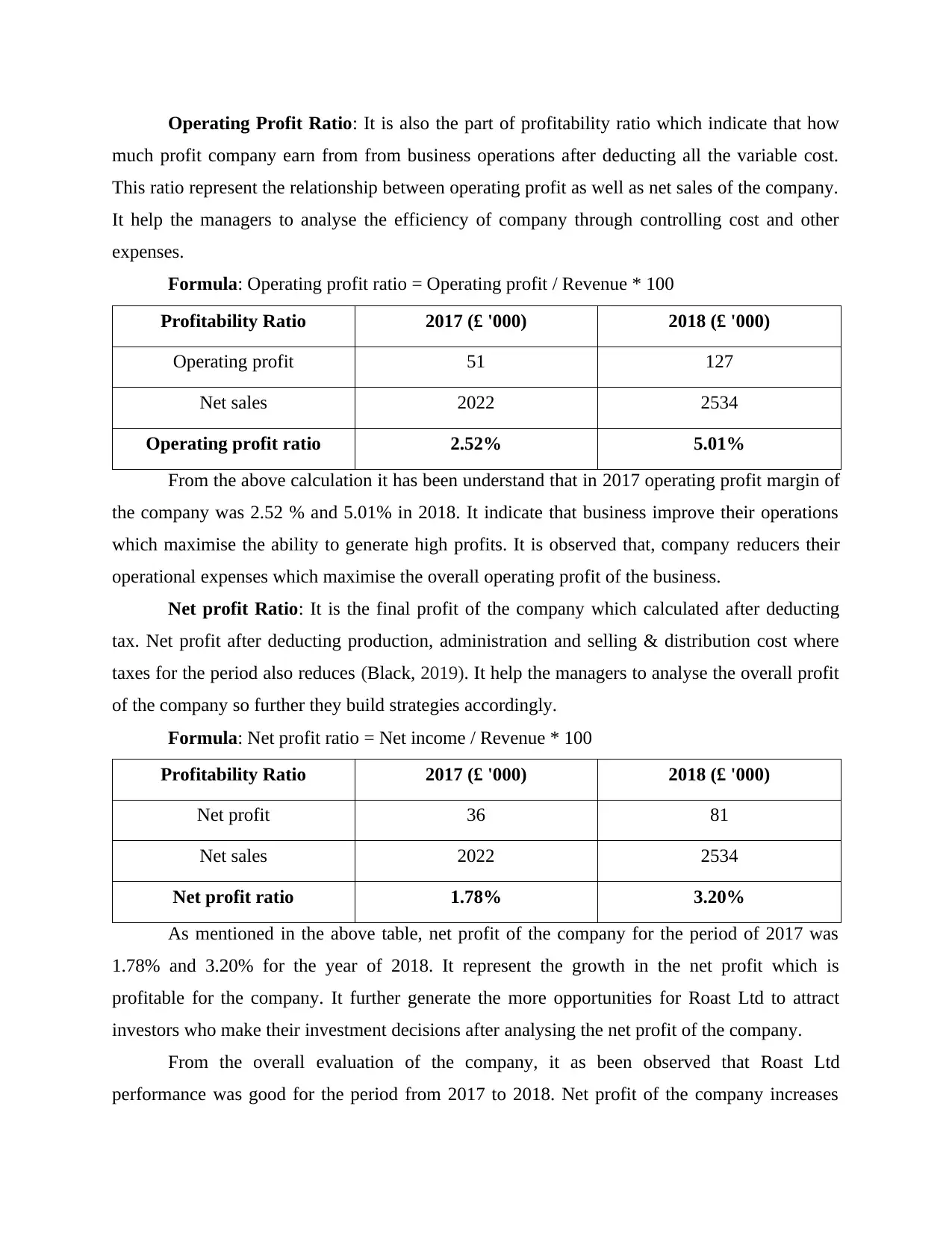

Operating Profit Ratio: It is also the part of profitability ratio which indicate that how

much profit company earn from from business operations after deducting all the variable cost.

This ratio represent the relationship between operating profit as well as net sales of the company.

It help the managers to analyse the efficiency of company through controlling cost and other

expenses.

Formula: Operating profit ratio = Operating profit / Revenue * 100

Profitability Ratio 2017 (£ '000) 2018 (£ '000)

Operating profit 51 127

Net sales 2022 2534

Operating profit ratio 2.52% 5.01%

From the above calculation it has been understand that in 2017 operating profit margin of

the company was 2.52 % and 5.01% in 2018. It indicate that business improve their operations

which maximise the ability to generate high profits. It is observed that, company reducers their

operational expenses which maximise the overall operating profit of the business.

Net profit Ratio: It is the final profit of the company which calculated after deducting

tax. Net profit after deducting production, administration and selling & distribution cost where

taxes for the period also reduces (Black, 2019). It help the managers to analyse the overall profit

of the company so further they build strategies accordingly.

Formula: Net profit ratio = Net income / Revenue * 100

Profitability Ratio 2017 (£ '000) 2018 (£ '000)

Net profit 36 81

Net sales 2022 2534

Net profit ratio 1.78% 3.20%

As mentioned in the above table, net profit of the company for the period of 2017 was

1.78% and 3.20% for the year of 2018. It represent the growth in the net profit which is

profitable for the company. It further generate the more opportunities for Roast Ltd to attract

investors who make their investment decisions after analysing the net profit of the company.

From the overall evaluation of the company, it as been observed that Roast Ltd

performance was good for the period from 2017 to 2018. Net profit of the company increases

much profit company earn from from business operations after deducting all the variable cost.

This ratio represent the relationship between operating profit as well as net sales of the company.

It help the managers to analyse the efficiency of company through controlling cost and other

expenses.

Formula: Operating profit ratio = Operating profit / Revenue * 100

Profitability Ratio 2017 (£ '000) 2018 (£ '000)

Operating profit 51 127

Net sales 2022 2534

Operating profit ratio 2.52% 5.01%

From the above calculation it has been understand that in 2017 operating profit margin of

the company was 2.52 % and 5.01% in 2018. It indicate that business improve their operations

which maximise the ability to generate high profits. It is observed that, company reducers their

operational expenses which maximise the overall operating profit of the business.

Net profit Ratio: It is the final profit of the company which calculated after deducting

tax. Net profit after deducting production, administration and selling & distribution cost where

taxes for the period also reduces (Black, 2019). It help the managers to analyse the overall profit

of the company so further they build strategies accordingly.

Formula: Net profit ratio = Net income / Revenue * 100

Profitability Ratio 2017 (£ '000) 2018 (£ '000)

Net profit 36 81

Net sales 2022 2534

Net profit ratio 1.78% 3.20%

As mentioned in the above table, net profit of the company for the period of 2017 was

1.78% and 3.20% for the year of 2018. It represent the growth in the net profit which is

profitable for the company. It further generate the more opportunities for Roast Ltd to attract

investors who make their investment decisions after analysing the net profit of the company.

From the overall evaluation of the company, it as been observed that Roast Ltd

performance was good for the period from 2017 to 2018. Net profit of the company increases

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

which is beneficial and it further provide the market growth. After evaluating income statement

of Roast Ltd, it is recommended that Starbucks should acquire the company which provide future

growth and helps in expanding their market share in the UK market.

2.2 Statement of Financial Position

Statement of financial position also called balance sheet which help the owner to evaluate

the performance as well as position of their business in terms of assets or liabilities of the

company (Chen, 2018). This statement represent net worth which further beneficial for the

shareholders of the company to evaluate the overall performance of the business. On the basis it,

investors make their decisions for the future investment.

On the basis of balance sheet of Roast Ltd, it has been noted that total assets of the

company for the period of 2017 was 1017,000 and for 2018 it was 1443,000. current assets are

447,000 for the duration of 2018 and previously it was 347,000. On the other hand, non- current

assets of the company in 2017 was 670,000 and in 2018 it was reported 996,000. Total equity of

the company in the period of 2017 was 779,000 and they get hike in 2018 and remain 860,000.

Current liability also increases for the period of 2017 to 2018 from 138,000 to 308,000. it

increases because company take bank overdraft in 2018 that is 73,000. In the long term

borrowing get they huge hike from 100,000 to 275,000 from 2017 to 2018 period. Below

mention calculation based on the financial information of balance sheet and it will represented

below:

Current Ratio: It is the liquidity ratio which is important to calculate in order to analyse

the overall liquidity of the company to perform operational activities. It represent the relationship

between current assets or current liability of the company (Dinçer and Yüksel, 2018).

Corporation has to ensure that business has two time of current assets in order to pay off their

obligation.

Formula: Current Ratio = Current assets / Current liabilities

Liquidity Ratio 2017 (£ '000) 2018 (£ '000)

Current Assets 347 447

Current Liabilities 138 308

Current Ratio 2.51 times 1.45 times

of Roast Ltd, it is recommended that Starbucks should acquire the company which provide future

growth and helps in expanding their market share in the UK market.

2.2 Statement of Financial Position

Statement of financial position also called balance sheet which help the owner to evaluate

the performance as well as position of their business in terms of assets or liabilities of the

company (Chen, 2018). This statement represent net worth which further beneficial for the

shareholders of the company to evaluate the overall performance of the business. On the basis it,

investors make their decisions for the future investment.

On the basis of balance sheet of Roast Ltd, it has been noted that total assets of the

company for the period of 2017 was 1017,000 and for 2018 it was 1443,000. current assets are

447,000 for the duration of 2018 and previously it was 347,000. On the other hand, non- current

assets of the company in 2017 was 670,000 and in 2018 it was reported 996,000. Total equity of

the company in the period of 2017 was 779,000 and they get hike in 2018 and remain 860,000.

Current liability also increases for the period of 2017 to 2018 from 138,000 to 308,000. it

increases because company take bank overdraft in 2018 that is 73,000. In the long term

borrowing get they huge hike from 100,000 to 275,000 from 2017 to 2018 period. Below

mention calculation based on the financial information of balance sheet and it will represented

below:

Current Ratio: It is the liquidity ratio which is important to calculate in order to analyse

the overall liquidity of the company to perform operational activities. It represent the relationship

between current assets or current liability of the company (Dinçer and Yüksel, 2018).

Corporation has to ensure that business has two time of current assets in order to pay off their

obligation.

Formula: Current Ratio = Current assets / Current liabilities

Liquidity Ratio 2017 (£ '000) 2018 (£ '000)

Current Assets 347 447

Current Liabilities 138 308

Current Ratio 2.51 times 1.45 times

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

From the above calculation it has been observed current ratio of the company for the

period of 2017 was more than two times in comparison to 2018. Liquidity of the company

decreases from 2.51 times to 1.45 in the duration of 2017 to 2018. Roast Ltd lost their flexibility

as well as liquidity which is very essential to meet their short term obligations.

Quick Ratio: This ratio indicate the short term liquidity position of the company which

helps in meeting short term obligations by using most liquidating assets. It also called acid test

ratio which provide the quick results or able the business to pay off their urgent liabilities.

Corporation has to maintain the one of one ratio of assets and liability. It exclude the inventory

of the business because it will take almost one year to generate cash from raw materiel.

Formula: Quick ratio = ( Current assets – Inventory ) / Current liability

Liquidity Ratio 2017 (£ '000) 2018 (£ '000)

Quick Assets 227 (347 - 120) 148 (447 – 299)

Current liability 138 308

Quick ratio 1.64 Times 0.48 Times

Above calculation indicate that quick ratio for the period of 2017 was 1.64 times and for

2018 it was 0.48 times. Both years unable to meet the ideal ratio that is 1:1 which means they

should maintain at least same level of quick assets to pay off their current liabilities. Company

reduce their liquidity that is not beneficial for the company.

Debt to Equity Ratio: It is financial ratio which indicate that in which proportion debt or

equity used to finance the assets of the company. It shows the relationship between total dent or

total equity of the organizations (Dinçer, Yüksel and Şenel, 2018). Ideal ratio is 1 to 10.5 so

corporate should maintain this proportion for the effective results of the company.

Formula: Debt Equity ratio = Total liability / Total shareholder's equity

Financial ratio 2017 (£ '000) 2018 (£ '000)

Debts 238 583

Equity 779 860

Debt to Equity Ratio 0.3055 0.6779

period of 2017 was more than two times in comparison to 2018. Liquidity of the company

decreases from 2.51 times to 1.45 in the duration of 2017 to 2018. Roast Ltd lost their flexibility

as well as liquidity which is very essential to meet their short term obligations.

Quick Ratio: This ratio indicate the short term liquidity position of the company which

helps in meeting short term obligations by using most liquidating assets. It also called acid test

ratio which provide the quick results or able the business to pay off their urgent liabilities.

Corporation has to maintain the one of one ratio of assets and liability. It exclude the inventory

of the business because it will take almost one year to generate cash from raw materiel.

Formula: Quick ratio = ( Current assets – Inventory ) / Current liability

Liquidity Ratio 2017 (£ '000) 2018 (£ '000)

Quick Assets 227 (347 - 120) 148 (447 – 299)

Current liability 138 308

Quick ratio 1.64 Times 0.48 Times

Above calculation indicate that quick ratio for the period of 2017 was 1.64 times and for

2018 it was 0.48 times. Both years unable to meet the ideal ratio that is 1:1 which means they

should maintain at least same level of quick assets to pay off their current liabilities. Company

reduce their liquidity that is not beneficial for the company.

Debt to Equity Ratio: It is financial ratio which indicate that in which proportion debt or

equity used to finance the assets of the company. It shows the relationship between total dent or

total equity of the organizations (Dinçer, Yüksel and Şenel, 2018). Ideal ratio is 1 to 10.5 so

corporate should maintain this proportion for the effective results of the company.

Formula: Debt Equity ratio = Total liability / Total shareholder's equity

Financial ratio 2017 (£ '000) 2018 (£ '000)

Debts 238 583

Equity 779 860

Debt to Equity Ratio 0.3055 0.6779

Above table indicate that debt to equity ratio increases from 0.30 to 0.67 for the period of

2017 to 2018. It represent the long-term liquidity as well as financial position which increased

and clearly mentioned in the figures.

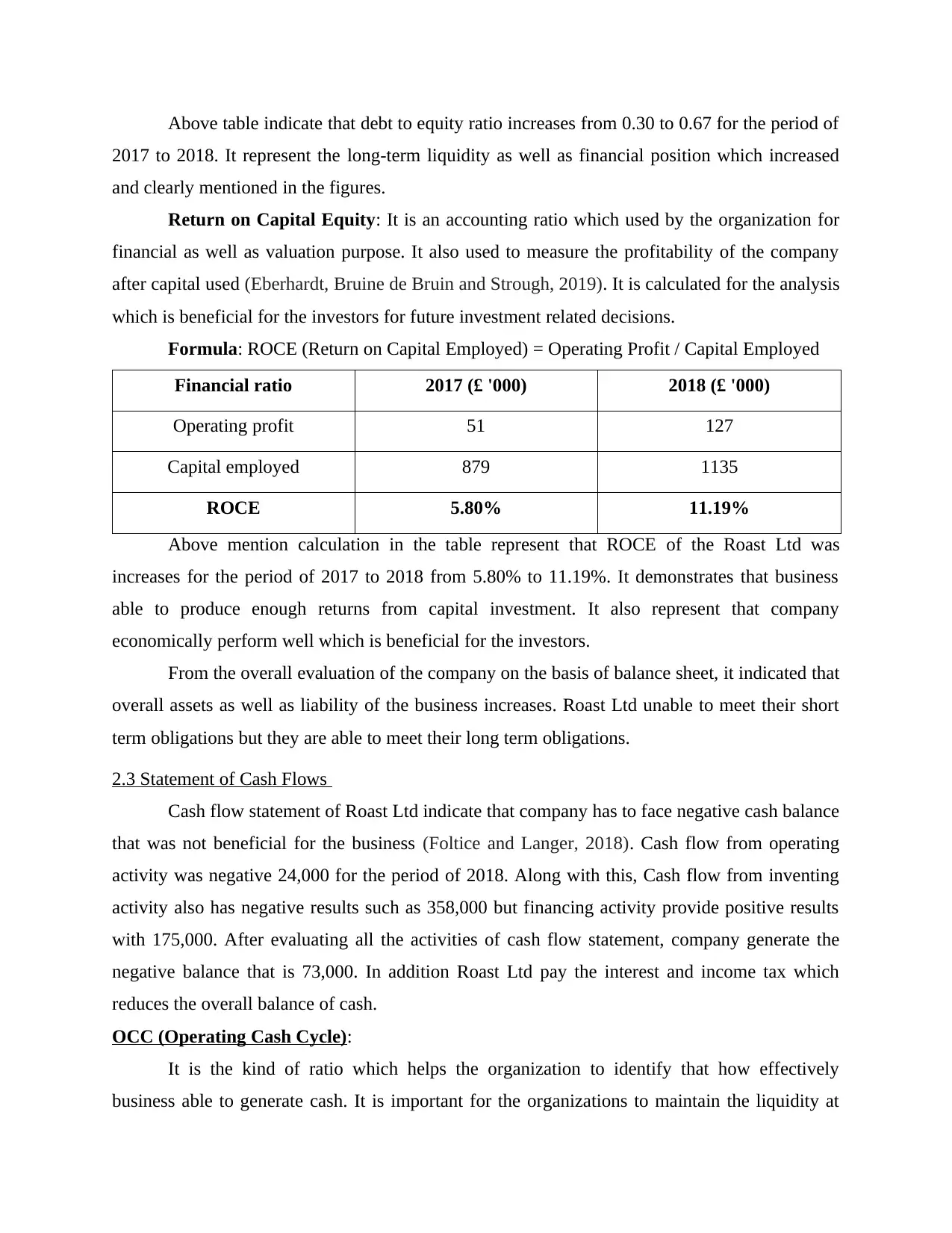

Return on Capital Equity: It is an accounting ratio which used by the organization for

financial as well as valuation purpose. It also used to measure the profitability of the company

after capital used (Eberhardt, Bruine de Bruin and Strough, 2019). It is calculated for the analysis

which is beneficial for the investors for future investment related decisions.

Formula: ROCE (Return on Capital Employed) = Operating Profit / Capital Employed

Financial ratio 2017 (£ '000) 2018 (£ '000)

Operating profit 51 127

Capital employed 879 1135

ROCE 5.80% 11.19%

Above mention calculation in the table represent that ROCE of the Roast Ltd was

increases for the period of 2017 to 2018 from 5.80% to 11.19%. It demonstrates that business

able to produce enough returns from capital investment. It also represent that company

economically perform well which is beneficial for the investors.

From the overall evaluation of the company on the basis of balance sheet, it indicated that

overall assets as well as liability of the business increases. Roast Ltd unable to meet their short

term obligations but they are able to meet their long term obligations.

2.3 Statement of Cash Flows

Cash flow statement of Roast Ltd indicate that company has to face negative cash balance

that was not beneficial for the business (Foltice and Langer, 2018). Cash flow from operating

activity was negative 24,000 for the period of 2018. Along with this, Cash flow from inventing

activity also has negative results such as 358,000 but financing activity provide positive results

with 175,000. After evaluating all the activities of cash flow statement, company generate the

negative balance that is 73,000. In addition Roast Ltd pay the interest and income tax which

reduces the overall balance of cash.

OCC (Operating Cash Cycle):

It is the kind of ratio which helps the organization to identify that how effectively

business able to generate cash. It is important for the organizations to maintain the liquidity at

2017 to 2018. It represent the long-term liquidity as well as financial position which increased

and clearly mentioned in the figures.

Return on Capital Equity: It is an accounting ratio which used by the organization for

financial as well as valuation purpose. It also used to measure the profitability of the company

after capital used (Eberhardt, Bruine de Bruin and Strough, 2019). It is calculated for the analysis

which is beneficial for the investors for future investment related decisions.

Formula: ROCE (Return on Capital Employed) = Operating Profit / Capital Employed

Financial ratio 2017 (£ '000) 2018 (£ '000)

Operating profit 51 127

Capital employed 879 1135

ROCE 5.80% 11.19%

Above mention calculation in the table represent that ROCE of the Roast Ltd was

increases for the period of 2017 to 2018 from 5.80% to 11.19%. It demonstrates that business

able to produce enough returns from capital investment. It also represent that company

economically perform well which is beneficial for the investors.

From the overall evaluation of the company on the basis of balance sheet, it indicated that

overall assets as well as liability of the business increases. Roast Ltd unable to meet their short

term obligations but they are able to meet their long term obligations.

2.3 Statement of Cash Flows

Cash flow statement of Roast Ltd indicate that company has to face negative cash balance

that was not beneficial for the business (Foltice and Langer, 2018). Cash flow from operating

activity was negative 24,000 for the period of 2018. Along with this, Cash flow from inventing

activity also has negative results such as 358,000 but financing activity provide positive results

with 175,000. After evaluating all the activities of cash flow statement, company generate the

negative balance that is 73,000. In addition Roast Ltd pay the interest and income tax which

reduces the overall balance of cash.

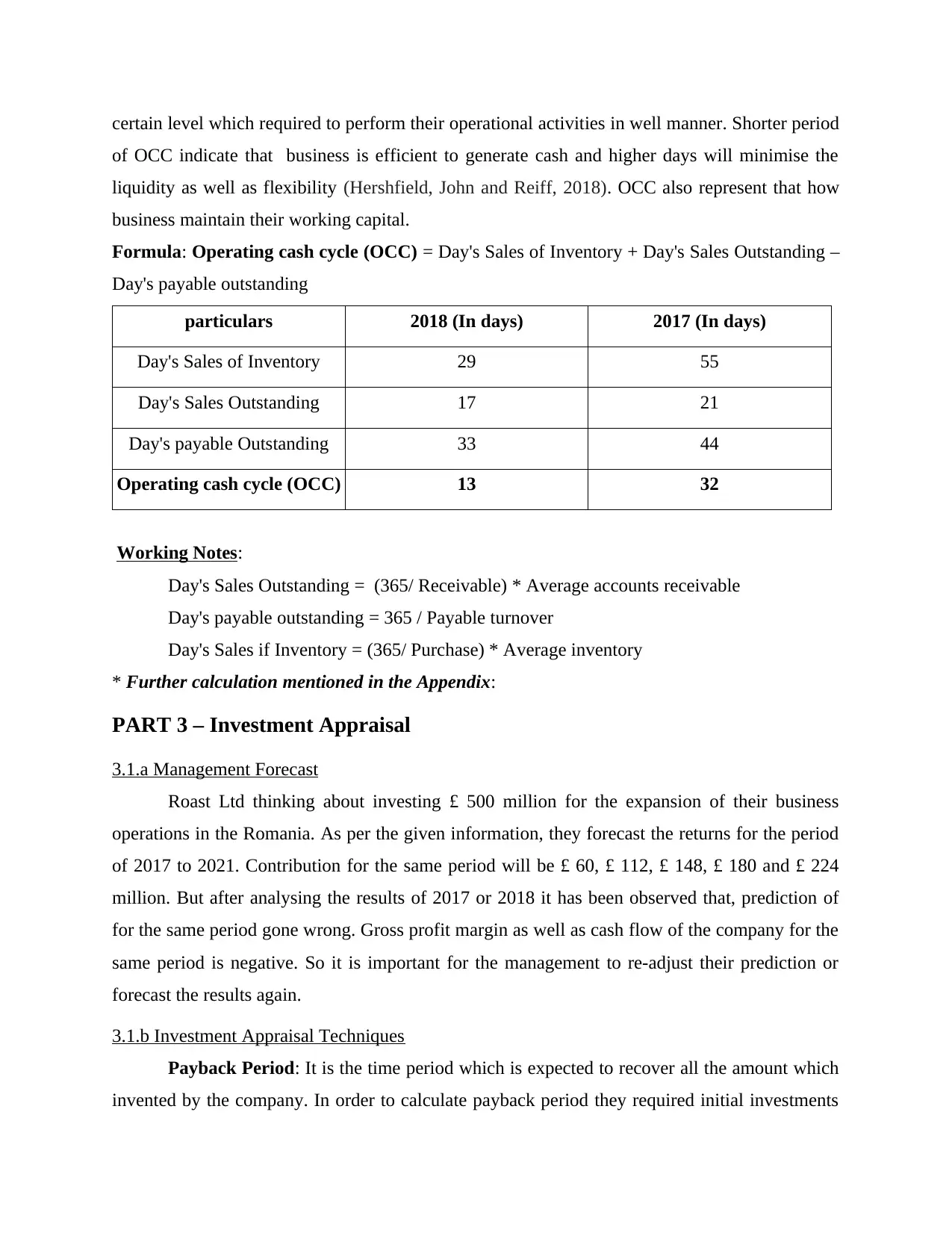

OCC (Operating Cash Cycle):

It is the kind of ratio which helps the organization to identify that how effectively

business able to generate cash. It is important for the organizations to maintain the liquidity at

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

certain level which required to perform their operational activities in well manner. Shorter period

of OCC indicate that business is efficient to generate cash and higher days will minimise the

liquidity as well as flexibility (Hershfield, John and Reiff, 2018). OCC also represent that how

business maintain their working capital.

Formula: Operating cash cycle (OCC) = Day's Sales of Inventory + Day's Sales Outstanding –

Day's payable outstanding

particulars 2018 (In days) 2017 (In days)

Day's Sales of Inventory 29 55

Day's Sales Outstanding 17 21

Day's payable Outstanding 33 44

Operating cash cycle (OCC) 13 32

Working Notes:

Day's Sales Outstanding = (365/ Receivable) * Average accounts receivable

Day's payable outstanding = 365 / Payable turnover

Day's Sales if Inventory = (365/ Purchase) * Average inventory

* Further calculation mentioned in the Appendix:

PART 3 – Investment Appraisal

3.1.a Management Forecast

Roast Ltd thinking about investing £ 500 million for the expansion of their business

operations in the Romania. As per the given information, they forecast the returns for the period

of 2017 to 2021. Contribution for the same period will be £ 60, £ 112, £ 148, £ 180 and £ 224

million. But after analysing the results of 2017 or 2018 it has been observed that, prediction of

for the same period gone wrong. Gross profit margin as well as cash flow of the company for the

same period is negative. So it is important for the management to re-adjust their prediction or

forecast the results again.

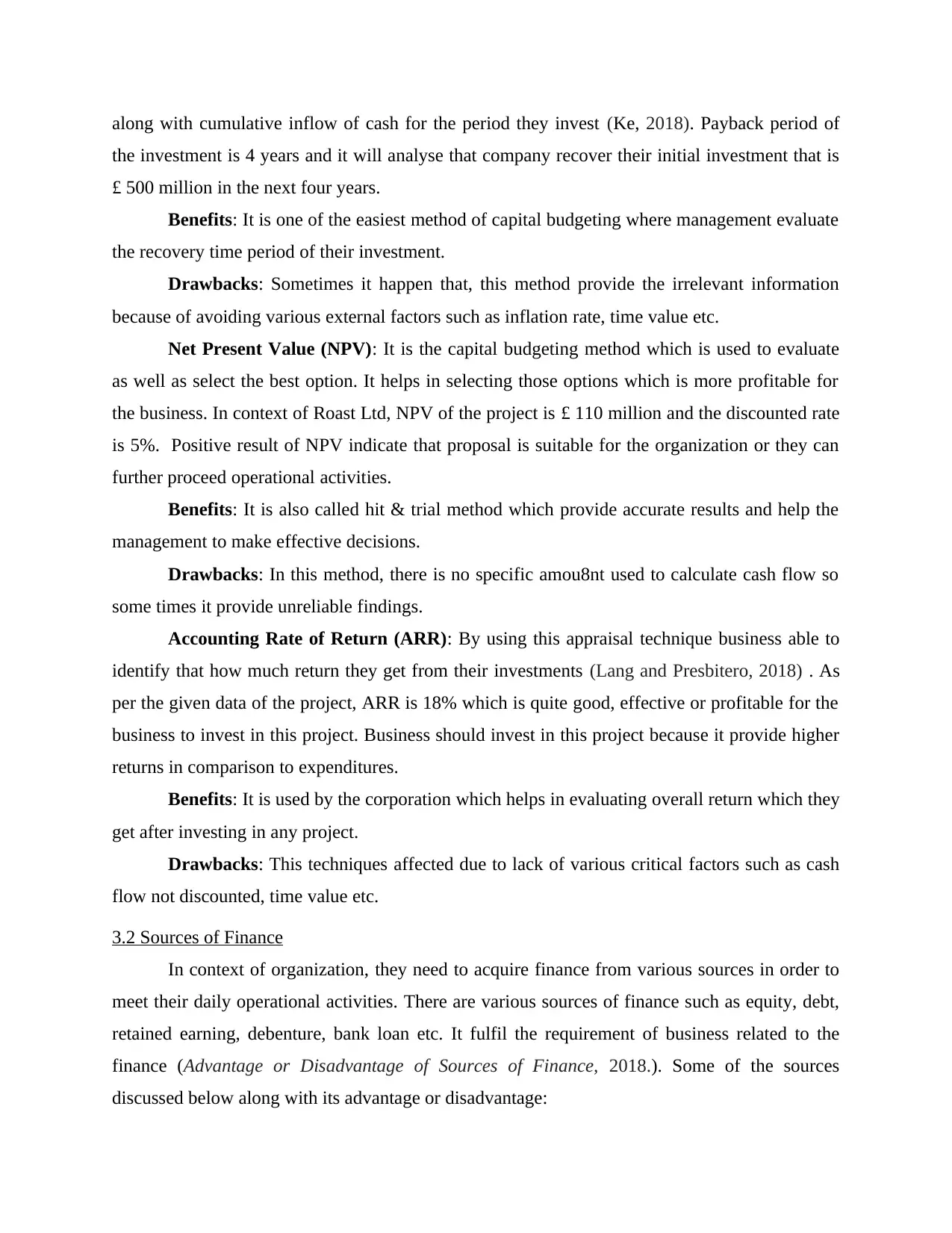

3.1.b Investment Appraisal Techniques

Payback Period: It is the time period which is expected to recover all the amount which

invented by the company. In order to calculate payback period they required initial investments

of OCC indicate that business is efficient to generate cash and higher days will minimise the

liquidity as well as flexibility (Hershfield, John and Reiff, 2018). OCC also represent that how

business maintain their working capital.

Formula: Operating cash cycle (OCC) = Day's Sales of Inventory + Day's Sales Outstanding –

Day's payable outstanding

particulars 2018 (In days) 2017 (In days)

Day's Sales of Inventory 29 55

Day's Sales Outstanding 17 21

Day's payable Outstanding 33 44

Operating cash cycle (OCC) 13 32

Working Notes:

Day's Sales Outstanding = (365/ Receivable) * Average accounts receivable

Day's payable outstanding = 365 / Payable turnover

Day's Sales if Inventory = (365/ Purchase) * Average inventory

* Further calculation mentioned in the Appendix:

PART 3 – Investment Appraisal

3.1.a Management Forecast

Roast Ltd thinking about investing £ 500 million for the expansion of their business

operations in the Romania. As per the given information, they forecast the returns for the period

of 2017 to 2021. Contribution for the same period will be £ 60, £ 112, £ 148, £ 180 and £ 224

million. But after analysing the results of 2017 or 2018 it has been observed that, prediction of

for the same period gone wrong. Gross profit margin as well as cash flow of the company for the

same period is negative. So it is important for the management to re-adjust their prediction or

forecast the results again.

3.1.b Investment Appraisal Techniques

Payback Period: It is the time period which is expected to recover all the amount which

invented by the company. In order to calculate payback period they required initial investments

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

along with cumulative inflow of cash for the period they invest (Ke, 2018). Payback period of

the investment is 4 years and it will analyse that company recover their initial investment that is

£ 500 million in the next four years.

Benefits: It is one of the easiest method of capital budgeting where management evaluate

the recovery time period of their investment.

Drawbacks: Sometimes it happen that, this method provide the irrelevant information

because of avoiding various external factors such as inflation rate, time value etc.

Net Present Value (NPV): It is the capital budgeting method which is used to evaluate

as well as select the best option. It helps in selecting those options which is more profitable for

the business. In context of Roast Ltd, NPV of the project is £ 110 million and the discounted rate

is 5%. Positive result of NPV indicate that proposal is suitable for the organization or they can

further proceed operational activities.

Benefits: It is also called hit & trial method which provide accurate results and help the

management to make effective decisions.

Drawbacks: In this method, there is no specific amou8nt used to calculate cash flow so

some times it provide unreliable findings.

Accounting Rate of Return (ARR): By using this appraisal technique business able to

identify that how much return they get from their investments (Lang and Presbitero, 2018) . As

per the given data of the project, ARR is 18% which is quite good, effective or profitable for the

business to invest in this project. Business should invest in this project because it provide higher

returns in comparison to expenditures.

Benefits: It is used by the corporation which helps in evaluating overall return which they

get after investing in any project.

Drawbacks: This techniques affected due to lack of various critical factors such as cash

flow not discounted, time value etc.

3.2 Sources of Finance

In context of organization, they need to acquire finance from various sources in order to

meet their daily operational activities. There are various sources of finance such as equity, debt,

retained earning, debenture, bank loan etc. It fulfil the requirement of business related to the

finance (Advantage or Disadvantage of Sources of Finance, 2018.). Some of the sources

discussed below along with its advantage or disadvantage:

the investment is 4 years and it will analyse that company recover their initial investment that is

£ 500 million in the next four years.

Benefits: It is one of the easiest method of capital budgeting where management evaluate

the recovery time period of their investment.

Drawbacks: Sometimes it happen that, this method provide the irrelevant information

because of avoiding various external factors such as inflation rate, time value etc.

Net Present Value (NPV): It is the capital budgeting method which is used to evaluate

as well as select the best option. It helps in selecting those options which is more profitable for

the business. In context of Roast Ltd, NPV of the project is £ 110 million and the discounted rate

is 5%. Positive result of NPV indicate that proposal is suitable for the organization or they can

further proceed operational activities.

Benefits: It is also called hit & trial method which provide accurate results and help the

management to make effective decisions.

Drawbacks: In this method, there is no specific amou8nt used to calculate cash flow so

some times it provide unreliable findings.

Accounting Rate of Return (ARR): By using this appraisal technique business able to

identify that how much return they get from their investments (Lang and Presbitero, 2018) . As

per the given data of the project, ARR is 18% which is quite good, effective or profitable for the

business to invest in this project. Business should invest in this project because it provide higher

returns in comparison to expenditures.

Benefits: It is used by the corporation which helps in evaluating overall return which they

get after investing in any project.

Drawbacks: This techniques affected due to lack of various critical factors such as cash

flow not discounted, time value etc.

3.2 Sources of Finance

In context of organization, they need to acquire finance from various sources in order to

meet their daily operational activities. There are various sources of finance such as equity, debt,

retained earning, debenture, bank loan etc. It fulfil the requirement of business related to the

finance (Advantage or Disadvantage of Sources of Finance, 2018.). Some of the sources

discussed below along with its advantage or disadvantage:

Back Loan:

It is one the most common as well as flexible source of finance which select by the

organizations to satisfy their financial needs. Bank provide loan on lower rate of interest which is

suitable as well as affordable for the corporation(Loibl, 2018) . They provide the loan on the

basis of their credit score which is based on their financial records and brand value of the

company. They offer long term as well as short term finances and charge interest rate

accordingly. For the operational expansion of Roast Ltd, management required the huge amount

of funding so they can prefer the bank but after analysing its advantage or disadvantage which

mentioned below:

Advantage:

Back does not want the ownership in the organization and there was no more obligations

on the landers after pay off the amount of loan.

Leaders have options to take loan for the different time period select the interest rate

which is not changed for the entire loan life (Nigam, Srivastava and Banwet, 2018) .

It is the simplest or easy way to get funds or fulfil their needs regarding finances which

make them able to perform their daily basis operational activities.

Business get the finance against the securities which they have to offer and the loan value

also based on the value of security the deposit.

Disadvantage:

Organization unable to obtain loan if they does not have sustainable financial records of

their business.

Higher the value of loan have higher interest rate which lenders have to pay which is the

biggest disadvantage of this source.

Sometimes it happen that, business unable to obtain the enough finance which make

business able to meet their needs regarding operations. If any case, business unable to pay their loan in given time period than they have to pay

additional charges for that which make loan more costly.

Retained Earnings:

It is the proportion of profit which is not distributed among the shareholders but it can be

used in the future for the business activity (Northwood and Rhine, 2018). It is one of the most

important sources of finance that used by the organizations for fixed as well as working capital

It is one the most common as well as flexible source of finance which select by the

organizations to satisfy their financial needs. Bank provide loan on lower rate of interest which is

suitable as well as affordable for the corporation(Loibl, 2018) . They provide the loan on the

basis of their credit score which is based on their financial records and brand value of the

company. They offer long term as well as short term finances and charge interest rate

accordingly. For the operational expansion of Roast Ltd, management required the huge amount

of funding so they can prefer the bank but after analysing its advantage or disadvantage which

mentioned below:

Advantage:

Back does not want the ownership in the organization and there was no more obligations

on the landers after pay off the amount of loan.

Leaders have options to take loan for the different time period select the interest rate

which is not changed for the entire loan life (Nigam, Srivastava and Banwet, 2018) .

It is the simplest or easy way to get funds or fulfil their needs regarding finances which

make them able to perform their daily basis operational activities.

Business get the finance against the securities which they have to offer and the loan value

also based on the value of security the deposit.

Disadvantage:

Organization unable to obtain loan if they does not have sustainable financial records of

their business.

Higher the value of loan have higher interest rate which lenders have to pay which is the

biggest disadvantage of this source.

Sometimes it happen that, business unable to obtain the enough finance which make

business able to meet their needs regarding operations. If any case, business unable to pay their loan in given time period than they have to pay

additional charges for that which make loan more costly.

Retained Earnings:

It is the proportion of profit which is not distributed among the shareholders but it can be

used in the future for the business activity (Northwood and Rhine, 2018). It is one of the most

important sources of finance that used by the organizations for fixed as well as working capital

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.