Financial Decision Making: X Firm's Capital Structure Analysis Report

VerifiedAdded on 2021/01/02

|15

|1919

|165

Report

AI Summary

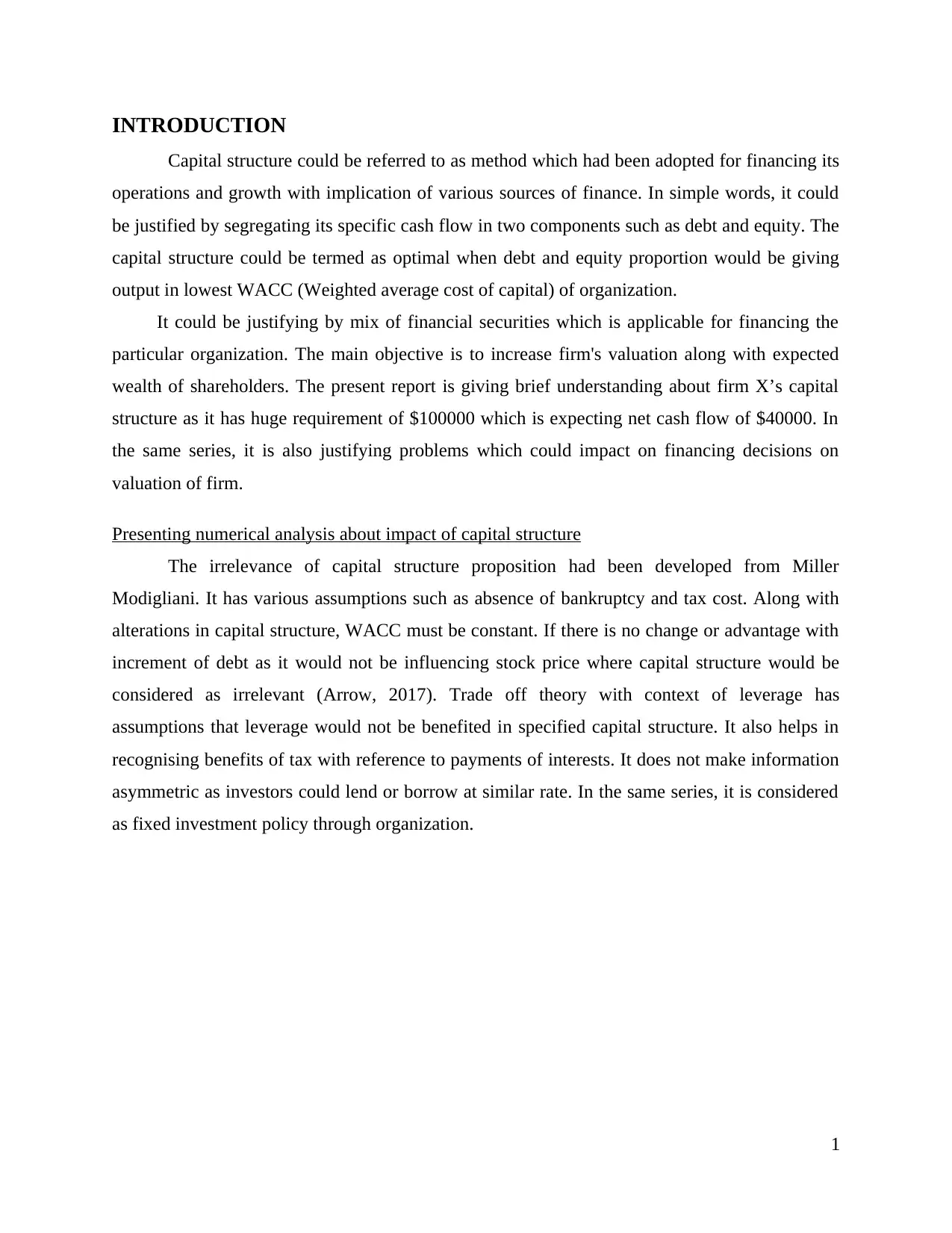

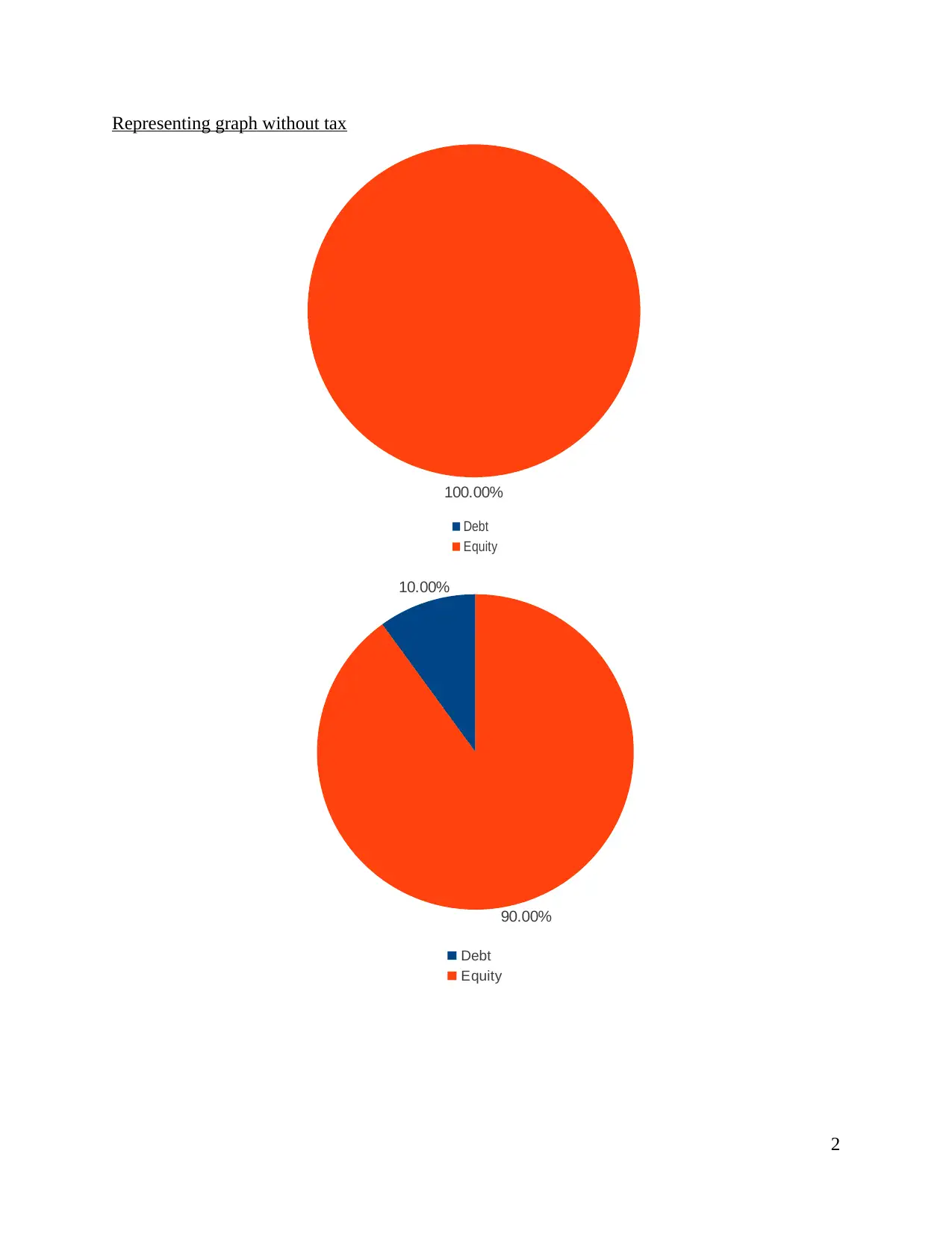

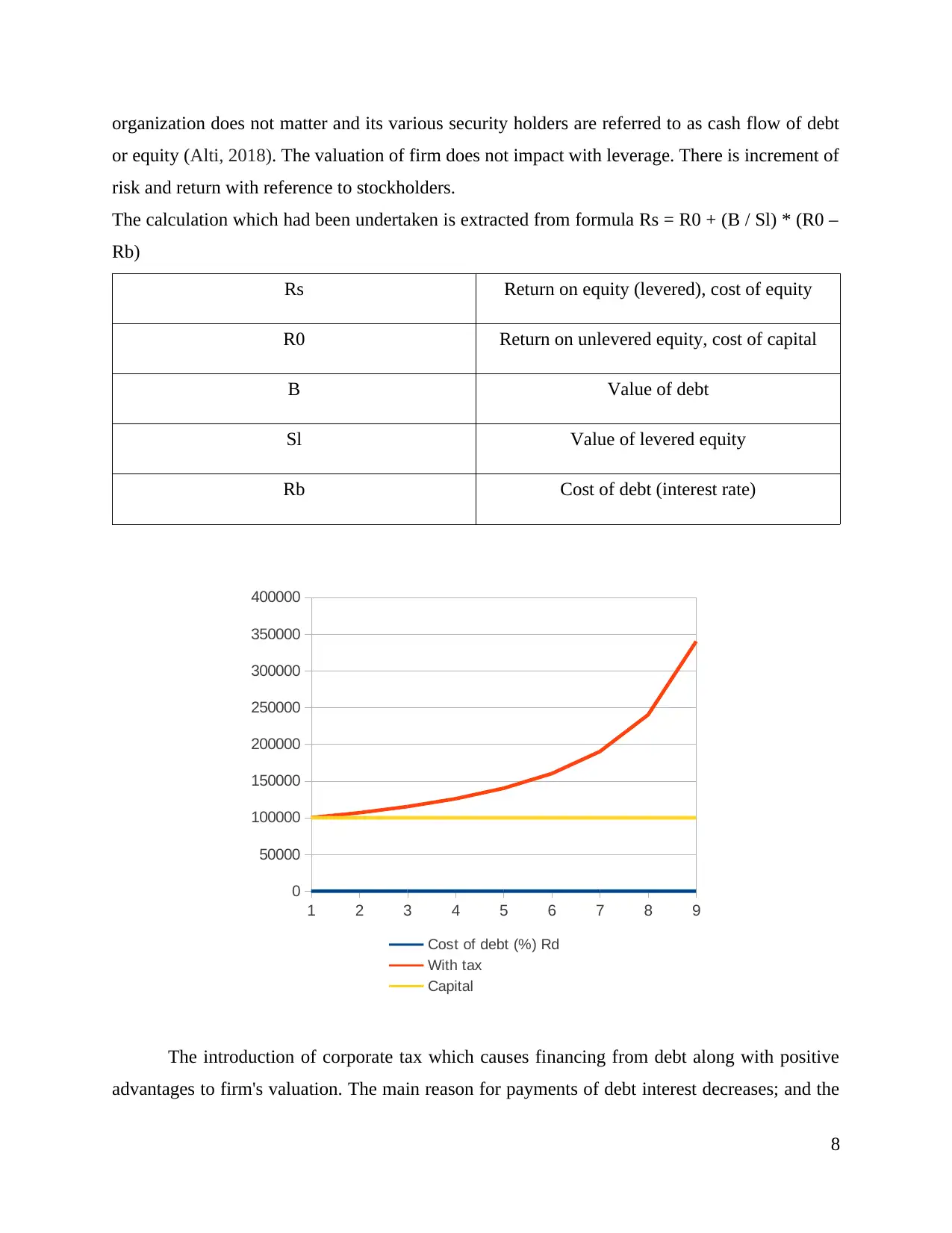

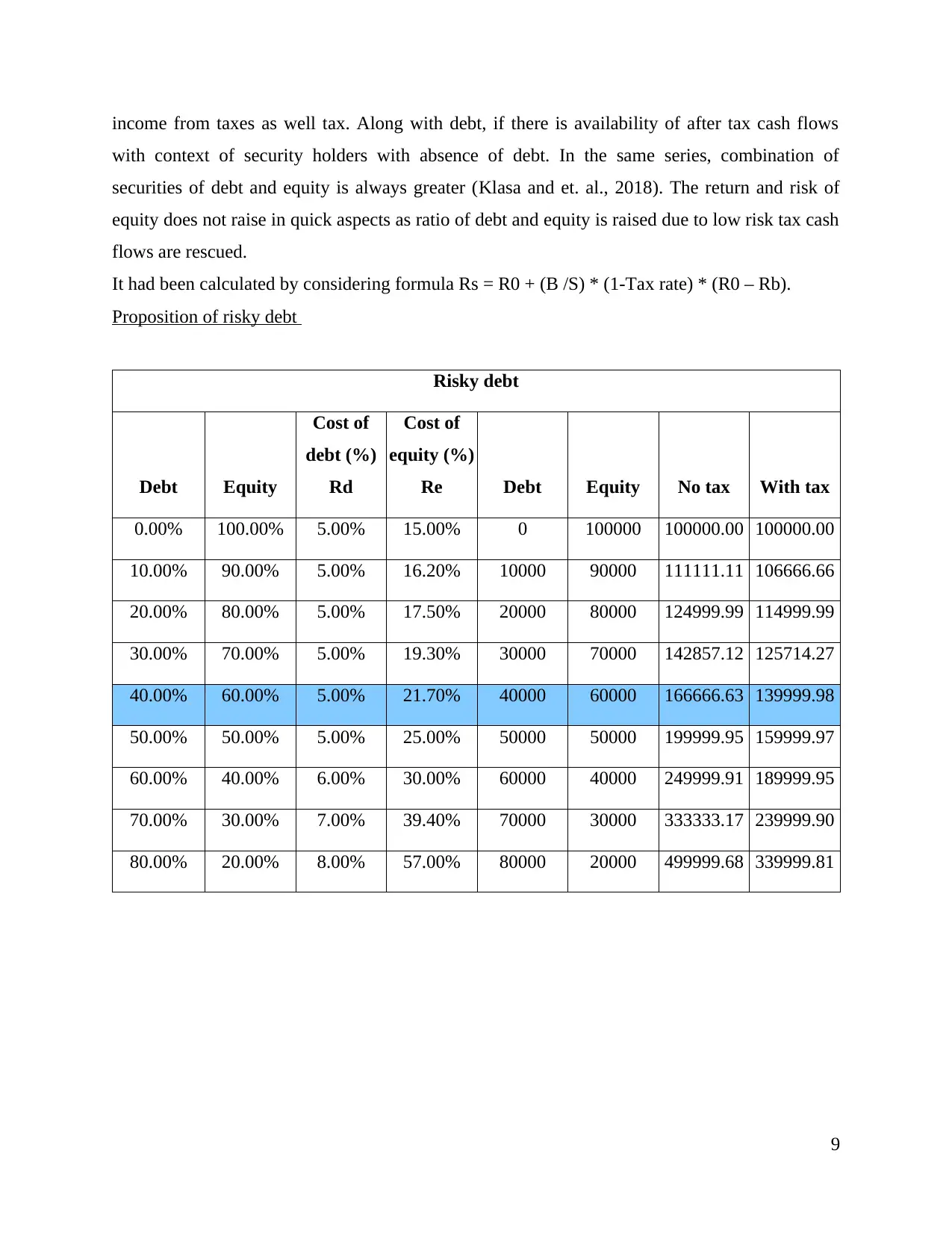

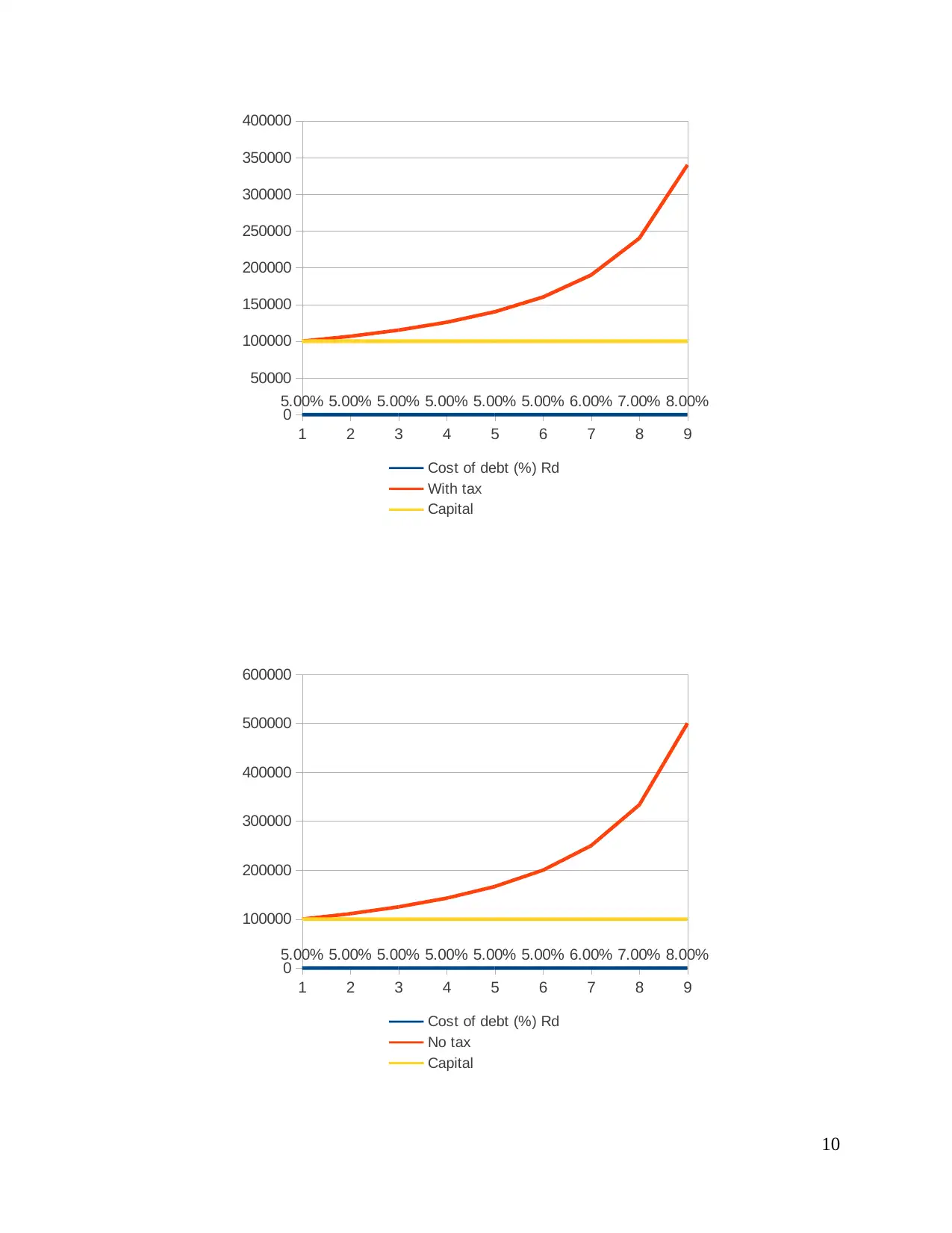

This report provides a comprehensive analysis of capital structure and its impact on financial decision-making and firm valuation. It begins with an introduction to capital structure, defining its components and the goal of optimizing it for the lowest Weighted Average Cost of Capital (WACC). The report then presents a numerical analysis of the impact of capital structure, including scenarios with and without tax, and explores the propositions of risk-free and risky debt. It examines the valuation of a hypothetical firm, 'X', under different debt-equity ratios and interest rates. The report also investigates the problems that can impact the financing decisions of the firm, such as agency and signaling effects, and their influence on firm value. The conclusion summarizes the findings, emphasizing the optimal capital structure and the importance of considering factors like corporate tax and risk when making financial decisions. The report utilizes tables and graphs to illustrate its points, and references relevant literature to support its analysis.

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.