Financial Analysis and Decision Making Report: Roast Ltd & Starbucks

VerifiedAdded on 2023/01/18

|17

|4772

|37

Report

AI Summary

This report presents a comprehensive analysis of the financial decision-making process, focusing on the evaluation of Roast Ltd's financial position. It begins with an industry review of the UK coffee market, highlighting market trends and key players. The main body delves into Roast Ltd's business performance, analyzing its profit and loss account, statement of financial position, and cash flow statement using ratio analysis to assess profitability, liquidity, and solvency. The report further examines investment appraisal methods and potential sources of finance, recommending that Starbucks acquire Roast Ltd based on its strong financial standing and market potential. The analysis covers gross profit, operating profit, and net profit ratios, along with current, quick, and debt-equity ratios to provide a comprehensive financial overview, making it a valuable resource for understanding financial analysis and decision-making in a real-world business context.

Financial Decision

Making

Making

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

EXECUTIVE SUMMARY ............................................................................................................3

MAIN BODY...................................................................................................................................3

Part 1 – Industry Review..................................................................................................................3

Part 2 – Business performance analysis...........................................................................................4

2.1 Statement of profit and loss account......................................................................................4

2.2 Statement of financial position..............................................................................................6

2.3 Statement of cash flow...........................................................................................................8

Part 3 – Investment appraisal and source of finance........................................................................9

3.1 Investment Appraisal.............................................................................................................9

3.2 Source of finance.................................................................................................................11

REFERENCES .............................................................................................................................13

APPENDIX....................................................................................................................................15

EXECUTIVE SUMMARY ............................................................................................................3

MAIN BODY...................................................................................................................................3

Part 1 – Industry Review..................................................................................................................3

Part 2 – Business performance analysis...........................................................................................4

2.1 Statement of profit and loss account......................................................................................4

2.2 Statement of financial position..............................................................................................6

2.3 Statement of cash flow...........................................................................................................8

Part 3 – Investment appraisal and source of finance........................................................................9

3.1 Investment Appraisal.............................................................................................................9

3.2 Source of finance.................................................................................................................11

REFERENCES .............................................................................................................................13

APPENDIX....................................................................................................................................15

EXECUTIVE SUMMARY

This report is based on financial decisions which taken by the top management to

evaluate the financial position of the company and make their decisions accordingly (Brown-

Liburd, Issa and Lombardi, 2015). Most of the issues related to the shareholder's equity,

liabilities and issuing bonds which further useful in achieving organizational goals & objectives.

Management focus on financial issues in order to minimise the risk or make them able to survive

in the market for longer period. With the help of ratio analysis or capital budgeting method

managers of Starbucks able to make their decisions regarding acquiring Roast Ltd or not. It

further helps in analysing that company have enough liquidity or not to perform their daily basis

operational activities. After all the analysis of financial statement of the company, it has been

recommended that Starbucks should acquire Roast Ltd because its financial position is good

which help them to capture market share.

MAIN BODY

Part 1 – Industry Review

In the UK market there are similar type of consumers who love tea as well as coffee

because on the basis of survey it was found that every four adults out of five prefer coffee. Retail

sales of coffee reached around 69 million kg in 2019 which is increases around 8% from 2014.

because of inflation or trend in the culture provide 17% growth that is around £ 1.27 billion

(Growth in UK's Coffee market, 2019). Currently, coffee dominate the 65% share of the UK

market which included variety such as ground coffee, beans etc. UK's retailer or wholesaler

target the young age group because they have more craze in comparison to older group.

Coffee industry generate around £ 6 billion revenues in 2019 where number of business

continues raise and reached at 16199. Coffee industry face the huge growth from 2014 to 2019

duration and that is 6.1% which provide the approx. 101,034 employment. Figures of coffee

industry increases because of huge demand in the consumers (Trend in UK's Coffee Industry,

2019). Over the five years, industry revenue is expected to grow around annual rate of 4.8%. it

includes the current growth which is 1.9% and expected to reach £6.6 billion.

Key players of Coffee industry are Costa Ltd, Pret A Manger Ltd, Starbucks or Caffe

Nero Group Holdings Ltd. These are the biggest player of the coffee market which increase the

competitors but along with this, they also face various challenges which impact the production as

This report is based on financial decisions which taken by the top management to

evaluate the financial position of the company and make their decisions accordingly (Brown-

Liburd, Issa and Lombardi, 2015). Most of the issues related to the shareholder's equity,

liabilities and issuing bonds which further useful in achieving organizational goals & objectives.

Management focus on financial issues in order to minimise the risk or make them able to survive

in the market for longer period. With the help of ratio analysis or capital budgeting method

managers of Starbucks able to make their decisions regarding acquiring Roast Ltd or not. It

further helps in analysing that company have enough liquidity or not to perform their daily basis

operational activities. After all the analysis of financial statement of the company, it has been

recommended that Starbucks should acquire Roast Ltd because its financial position is good

which help them to capture market share.

MAIN BODY

Part 1 – Industry Review

In the UK market there are similar type of consumers who love tea as well as coffee

because on the basis of survey it was found that every four adults out of five prefer coffee. Retail

sales of coffee reached around 69 million kg in 2019 which is increases around 8% from 2014.

because of inflation or trend in the culture provide 17% growth that is around £ 1.27 billion

(Growth in UK's Coffee market, 2019). Currently, coffee dominate the 65% share of the UK

market which included variety such as ground coffee, beans etc. UK's retailer or wholesaler

target the young age group because they have more craze in comparison to older group.

Coffee industry generate around £ 6 billion revenues in 2019 where number of business

continues raise and reached at 16199. Coffee industry face the huge growth from 2014 to 2019

duration and that is 6.1% which provide the approx. 101,034 employment. Figures of coffee

industry increases because of huge demand in the consumers (Trend in UK's Coffee Industry,

2019). Over the five years, industry revenue is expected to grow around annual rate of 4.8%. it

includes the current growth which is 1.9% and expected to reach £6.6 billion.

Key players of Coffee industry are Costa Ltd, Pret A Manger Ltd, Starbucks or Caffe

Nero Group Holdings Ltd. These are the biggest player of the coffee market which increase the

competitors but along with this, they also face various challenges which impact the production as

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

well as probability. Coffee industry of UK face the various opportunities such as Coffee is the

growing segment of European market because majority of people prefer to buy cheap

mainstream coffee. Along with this, they ready to pay high price for the high quality Coffee.

Increase in the interest in the coffee will maximise the number of coffee shops, roasters, small

brands and then it create the value of big competitors as well. Global demand for the coffee

increases around 2.5 % every year. On the other hand, change in the climate will impact the

agriculture which affect the coffee production. Increase in the temperature generate lower

altitude farms that is not suitable for coffee plants. Because of pest & diseases. they decrease the

yields & quality of coffee.

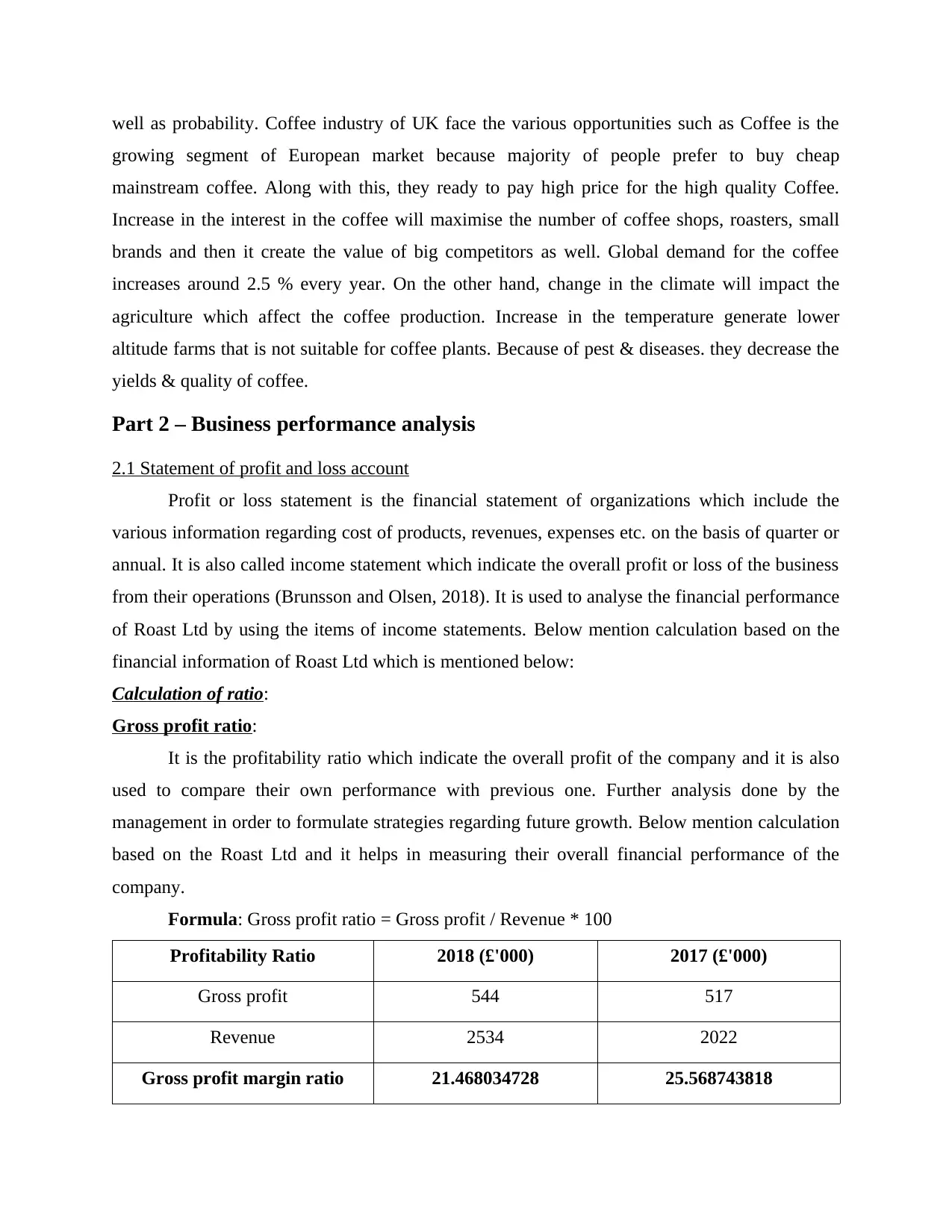

Part 2 – Business performance analysis

2.1 Statement of profit and loss account

Profit or loss statement is the financial statement of organizations which include the

various information regarding cost of products, revenues, expenses etc. on the basis of quarter or

annual. It is also called income statement which indicate the overall profit or loss of the business

from their operations (Brunsson and Olsen, 2018). It is used to analyse the financial performance

of Roast Ltd by using the items of income statements. Below mention calculation based on the

financial information of Roast Ltd which is mentioned below:

Calculation of ratio:

Gross profit ratio:

It is the profitability ratio which indicate the overall profit of the company and it is also

used to compare their own performance with previous one. Further analysis done by the

management in order to formulate strategies regarding future growth. Below mention calculation

based on the Roast Ltd and it helps in measuring their overall financial performance of the

company.

Formula: Gross profit ratio = Gross profit / Revenue * 100

Profitability Ratio 2018 (£'000) 2017 (£'000)

Gross profit 544 517

Revenue 2534 2022

Gross profit margin ratio 21.468034728 25.568743818

growing segment of European market because majority of people prefer to buy cheap

mainstream coffee. Along with this, they ready to pay high price for the high quality Coffee.

Increase in the interest in the coffee will maximise the number of coffee shops, roasters, small

brands and then it create the value of big competitors as well. Global demand for the coffee

increases around 2.5 % every year. On the other hand, change in the climate will impact the

agriculture which affect the coffee production. Increase in the temperature generate lower

altitude farms that is not suitable for coffee plants. Because of pest & diseases. they decrease the

yields & quality of coffee.

Part 2 – Business performance analysis

2.1 Statement of profit and loss account

Profit or loss statement is the financial statement of organizations which include the

various information regarding cost of products, revenues, expenses etc. on the basis of quarter or

annual. It is also called income statement which indicate the overall profit or loss of the business

from their operations (Brunsson and Olsen, 2018). It is used to analyse the financial performance

of Roast Ltd by using the items of income statements. Below mention calculation based on the

financial information of Roast Ltd which is mentioned below:

Calculation of ratio:

Gross profit ratio:

It is the profitability ratio which indicate the overall profit of the company and it is also

used to compare their own performance with previous one. Further analysis done by the

management in order to formulate strategies regarding future growth. Below mention calculation

based on the Roast Ltd and it helps in measuring their overall financial performance of the

company.

Formula: Gross profit ratio = Gross profit / Revenue * 100

Profitability Ratio 2018 (£'000) 2017 (£'000)

Gross profit 544 517

Revenue 2534 2022

Gross profit margin ratio 21.468034728 25.568743818

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

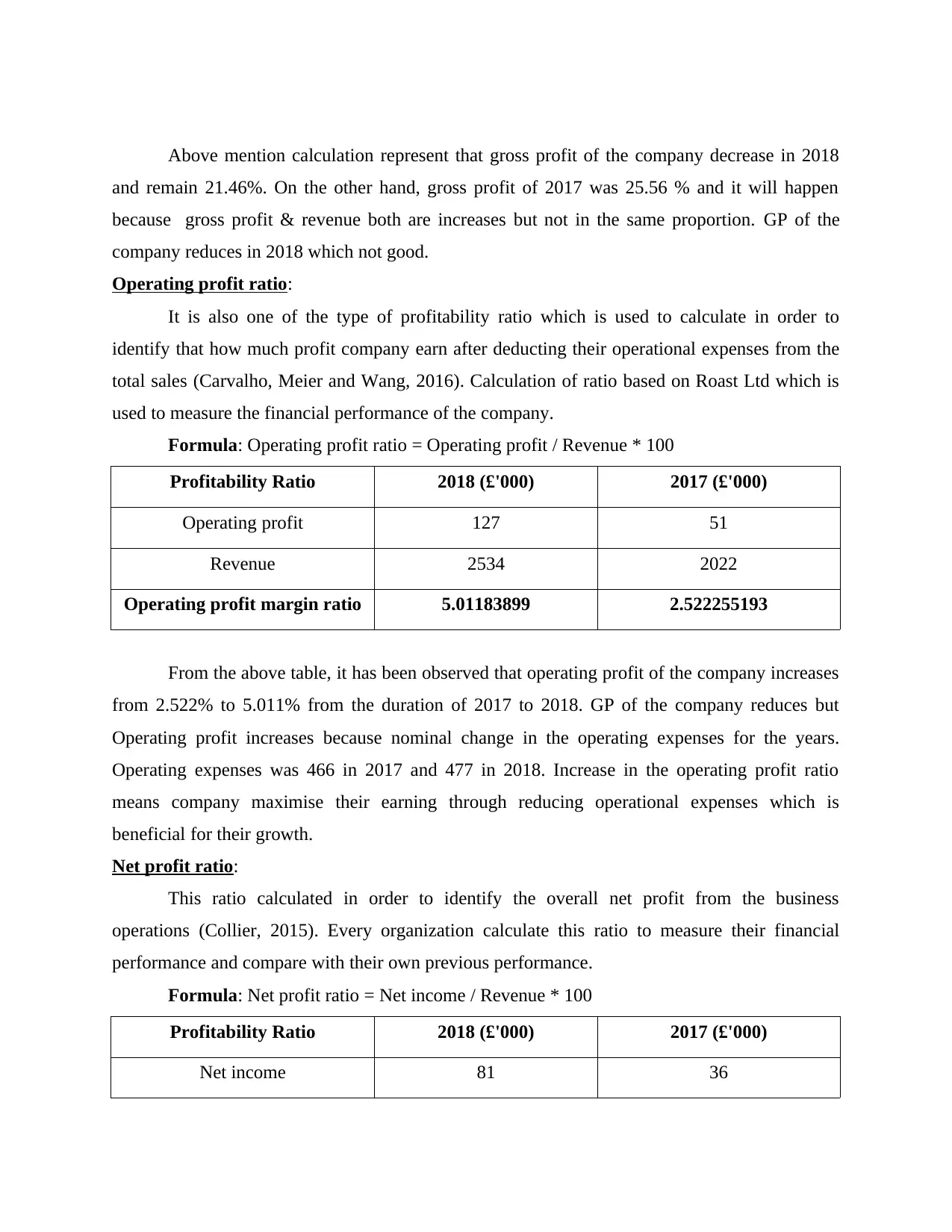

Above mention calculation represent that gross profit of the company decrease in 2018

and remain 21.46%. On the other hand, gross profit of 2017 was 25.56 % and it will happen

because gross profit & revenue both are increases but not in the same proportion. GP of the

company reduces in 2018 which not good.

Operating profit ratio:

It is also one of the type of profitability ratio which is used to calculate in order to

identify that how much profit company earn after deducting their operational expenses from the

total sales (Carvalho, Meier and Wang, 2016). Calculation of ratio based on Roast Ltd which is

used to measure the financial performance of the company.

Formula: Operating profit ratio = Operating profit / Revenue * 100

Profitability Ratio 2018 (£'000) 2017 (£'000)

Operating profit 127 51

Revenue 2534 2022

Operating profit margin ratio 5.01183899 2.522255193

From the above table, it has been observed that operating profit of the company increases

from 2.522% to 5.011% from the duration of 2017 to 2018. GP of the company reduces but

Operating profit increases because nominal change in the operating expenses for the years.

Operating expenses was 466 in 2017 and 477 in 2018. Increase in the operating profit ratio

means company maximise their earning through reducing operational expenses which is

beneficial for their growth.

Net profit ratio:

This ratio calculated in order to identify the overall net profit from the business

operations (Collier, 2015). Every organization calculate this ratio to measure their financial

performance and compare with their own previous performance.

Formula: Net profit ratio = Net income / Revenue * 100

Profitability Ratio 2018 (£'000) 2017 (£'000)

Net income 81 36

and remain 21.46%. On the other hand, gross profit of 2017 was 25.56 % and it will happen

because gross profit & revenue both are increases but not in the same proportion. GP of the

company reduces in 2018 which not good.

Operating profit ratio:

It is also one of the type of profitability ratio which is used to calculate in order to

identify that how much profit company earn after deducting their operational expenses from the

total sales (Carvalho, Meier and Wang, 2016). Calculation of ratio based on Roast Ltd which is

used to measure the financial performance of the company.

Formula: Operating profit ratio = Operating profit / Revenue * 100

Profitability Ratio 2018 (£'000) 2017 (£'000)

Operating profit 127 51

Revenue 2534 2022

Operating profit margin ratio 5.01183899 2.522255193

From the above table, it has been observed that operating profit of the company increases

from 2.522% to 5.011% from the duration of 2017 to 2018. GP of the company reduces but

Operating profit increases because nominal change in the operating expenses for the years.

Operating expenses was 466 in 2017 and 477 in 2018. Increase in the operating profit ratio

means company maximise their earning through reducing operational expenses which is

beneficial for their growth.

Net profit ratio:

This ratio calculated in order to identify the overall net profit from the business

operations (Collier, 2015). Every organization calculate this ratio to measure their financial

performance and compare with their own previous performance.

Formula: Net profit ratio = Net income / Revenue * 100

Profitability Ratio 2018 (£'000) 2017 (£'000)

Net income 81 36

Revenue 2534 2022

Net profit margin ratio 3.19652723 1.78041543

With the help of above calculation, it has been observed that net profit of the company

increases from 1.78% to 3.19% from the duration of 2017 to 2018. In a year, sales increases as

well as net income also increases which help the Roast Ltd to maximise their profitability. It help

the organization to maximise their revenue which further influence the external parties such as

investors or shareholders to invest in their business. With the help of these ratios a person make

their financial decisions regarding future decisions.

From the overall analysis of financial performance of Roast Ltd on the basis of profit and

loss statement of the company. Overall performance of Roast Ltd is good and it was clearly

indicated with the help of ratio analysis which used to major the performance of company in

terms of profitability (Hoffmann and Post, 2014). Gross profit of the company increases from

2017 to 2018 that is 517 to 544 but the proportion was not the same in comparison to total sales

that's why gross profit margin ratio decreases and remain 21.46% in 2018.

Operating profit of Roast Ltd was 51 in 2017 and 127 in 2018, it will provide the overall

profit which is beneficial for the company. GP ratio of the company decline but Operating profit

margin ratio increases from 2.522% to 5.011% in the period of 2017 and 2018 respectively.

Along with this, net profit of the company also increases from 36 to 81 in the duration of 2017 to

2018. With the help of ratio analysis, management will make decision in order to enhance their

productivity as well as profitability.

It has been critically evaluated that financial performance of Roast Ltd is good due to

increase in the net profit margin which indicate the profitability of the company. It means,

organization is profit making which grow in the market. On the basis of profit and loss statement,

Starbucks can acquire this company because it is profit making or have popularity in the UK

market.

2.2 Statement of financial position

Financial position of the company evaluated with the help of balance sheet which include

the assets or liabilities of the company. It include various items which required to measure the

liquidity as well as financial performance of the company (Kingsford-Smith and Dixon, 2015).

Net profit margin ratio 3.19652723 1.78041543

With the help of above calculation, it has been observed that net profit of the company

increases from 1.78% to 3.19% from the duration of 2017 to 2018. In a year, sales increases as

well as net income also increases which help the Roast Ltd to maximise their profitability. It help

the organization to maximise their revenue which further influence the external parties such as

investors or shareholders to invest in their business. With the help of these ratios a person make

their financial decisions regarding future decisions.

From the overall analysis of financial performance of Roast Ltd on the basis of profit and

loss statement of the company. Overall performance of Roast Ltd is good and it was clearly

indicated with the help of ratio analysis which used to major the performance of company in

terms of profitability (Hoffmann and Post, 2014). Gross profit of the company increases from

2017 to 2018 that is 517 to 544 but the proportion was not the same in comparison to total sales

that's why gross profit margin ratio decreases and remain 21.46% in 2018.

Operating profit of Roast Ltd was 51 in 2017 and 127 in 2018, it will provide the overall

profit which is beneficial for the company. GP ratio of the company decline but Operating profit

margin ratio increases from 2.522% to 5.011% in the period of 2017 and 2018 respectively.

Along with this, net profit of the company also increases from 36 to 81 in the duration of 2017 to

2018. With the help of ratio analysis, management will make decision in order to enhance their

productivity as well as profitability.

It has been critically evaluated that financial performance of Roast Ltd is good due to

increase in the net profit margin which indicate the profitability of the company. It means,

organization is profit making which grow in the market. On the basis of profit and loss statement,

Starbucks can acquire this company because it is profit making or have popularity in the UK

market.

2.2 Statement of financial position

Financial position of the company evaluated with the help of balance sheet which include

the assets or liabilities of the company. It include various items which required to measure the

liquidity as well as financial performance of the company (Kingsford-Smith and Dixon, 2015).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

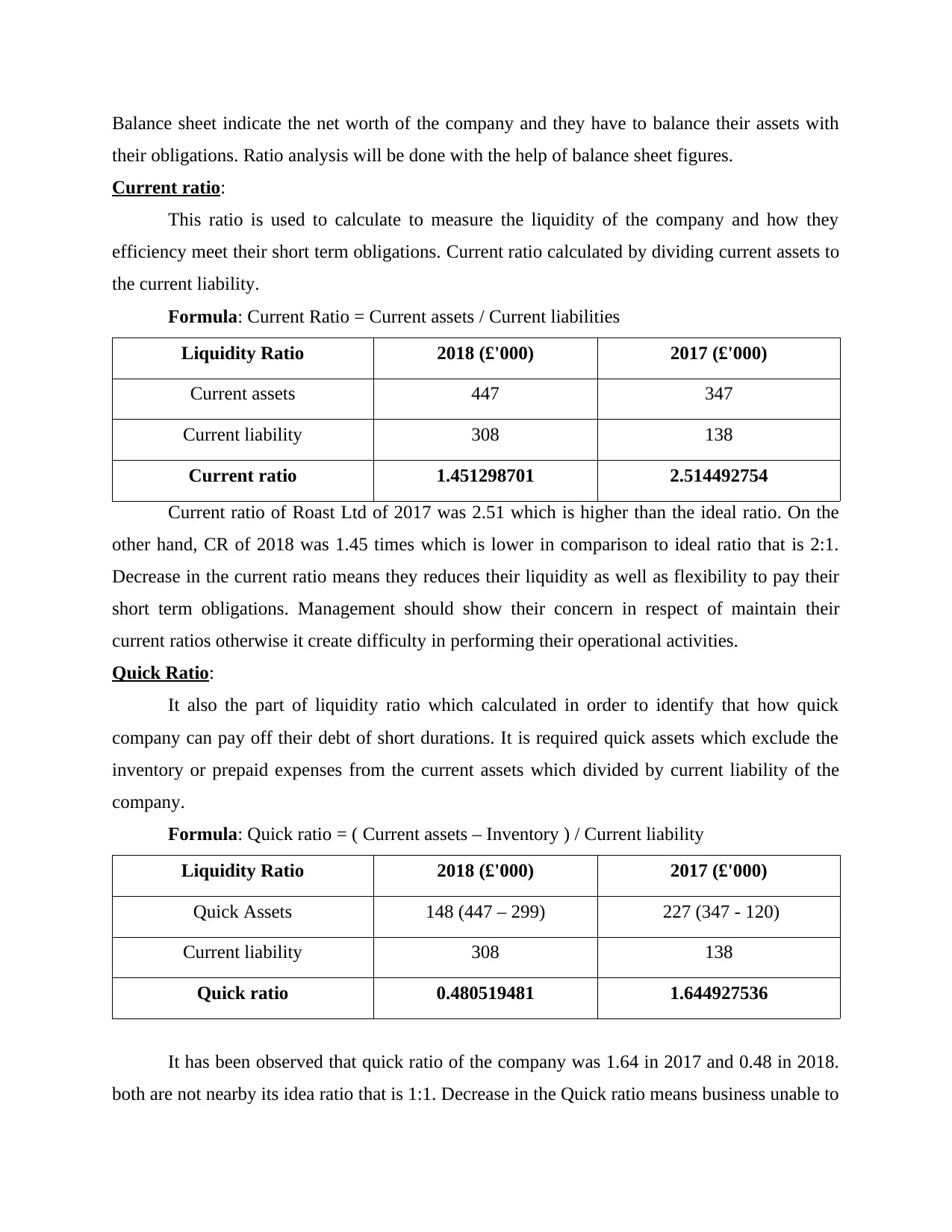

Balance sheet indicate the net worth of the company and they have to balance their assets with

their obligations. Ratio analysis will be done with the help of balance sheet figures.

Current ratio:

This ratio is used to calculate to measure the liquidity of the company and how they

efficiency meet their short term obligations. Current ratio calculated by dividing current assets to

the current liability.

Formula: Current Ratio = Current assets / Current liabilities

Liquidity Ratio 2018 (£'000) 2017 (£'000)

Current assets 447 347

Current liability 308 138

Current ratio 1.451298701 2.514492754

Current ratio of Roast Ltd of 2017 was 2.51 which is higher than the ideal ratio. On the

other hand, CR of 2018 was 1.45 times which is lower in comparison to ideal ratio that is 2:1.

Decrease in the current ratio means they reduces their liquidity as well as flexibility to pay their

short term obligations. Management should show their concern in respect of maintain their

current ratios otherwise it create difficulty in performing their operational activities.

Quick Ratio:

It also the part of liquidity ratio which calculated in order to identify that how quick

company can pay off their debt of short durations. It is required quick assets which exclude the

inventory or prepaid expenses from the current assets which divided by current liability of the

company.

Formula: Quick ratio = ( Current assets – Inventory ) / Current liability

Liquidity Ratio 2018 (£'000) 2017 (£'000)

Quick Assets 148 (447 – 299) 227 (347 - 120)

Current liability 308 138

Quick ratio 0.480519481 1.644927536

It has been observed that quick ratio of the company was 1.64 in 2017 and 0.48 in 2018.

both are not nearby its idea ratio that is 1:1. Decrease in the Quick ratio means business unable to

their obligations. Ratio analysis will be done with the help of balance sheet figures.

Current ratio:

This ratio is used to calculate to measure the liquidity of the company and how they

efficiency meet their short term obligations. Current ratio calculated by dividing current assets to

the current liability.

Formula: Current Ratio = Current assets / Current liabilities

Liquidity Ratio 2018 (£'000) 2017 (£'000)

Current assets 447 347

Current liability 308 138

Current ratio 1.451298701 2.514492754

Current ratio of Roast Ltd of 2017 was 2.51 which is higher than the ideal ratio. On the

other hand, CR of 2018 was 1.45 times which is lower in comparison to ideal ratio that is 2:1.

Decrease in the current ratio means they reduces their liquidity as well as flexibility to pay their

short term obligations. Management should show their concern in respect of maintain their

current ratios otherwise it create difficulty in performing their operational activities.

Quick Ratio:

It also the part of liquidity ratio which calculated in order to identify that how quick

company can pay off their debt of short durations. It is required quick assets which exclude the

inventory or prepaid expenses from the current assets which divided by current liability of the

company.

Formula: Quick ratio = ( Current assets – Inventory ) / Current liability

Liquidity Ratio 2018 (£'000) 2017 (£'000)

Quick Assets 148 (447 – 299) 227 (347 - 120)

Current liability 308 138

Quick ratio 0.480519481 1.644927536

It has been observed that quick ratio of the company was 1.64 in 2017 and 0.48 in 2018.

both are not nearby its idea ratio that is 1:1. Decrease in the Quick ratio means business unable to

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

meet their obligations because of lack of liquidity to pay. Company need to pay attention and

improve their liquidity position.

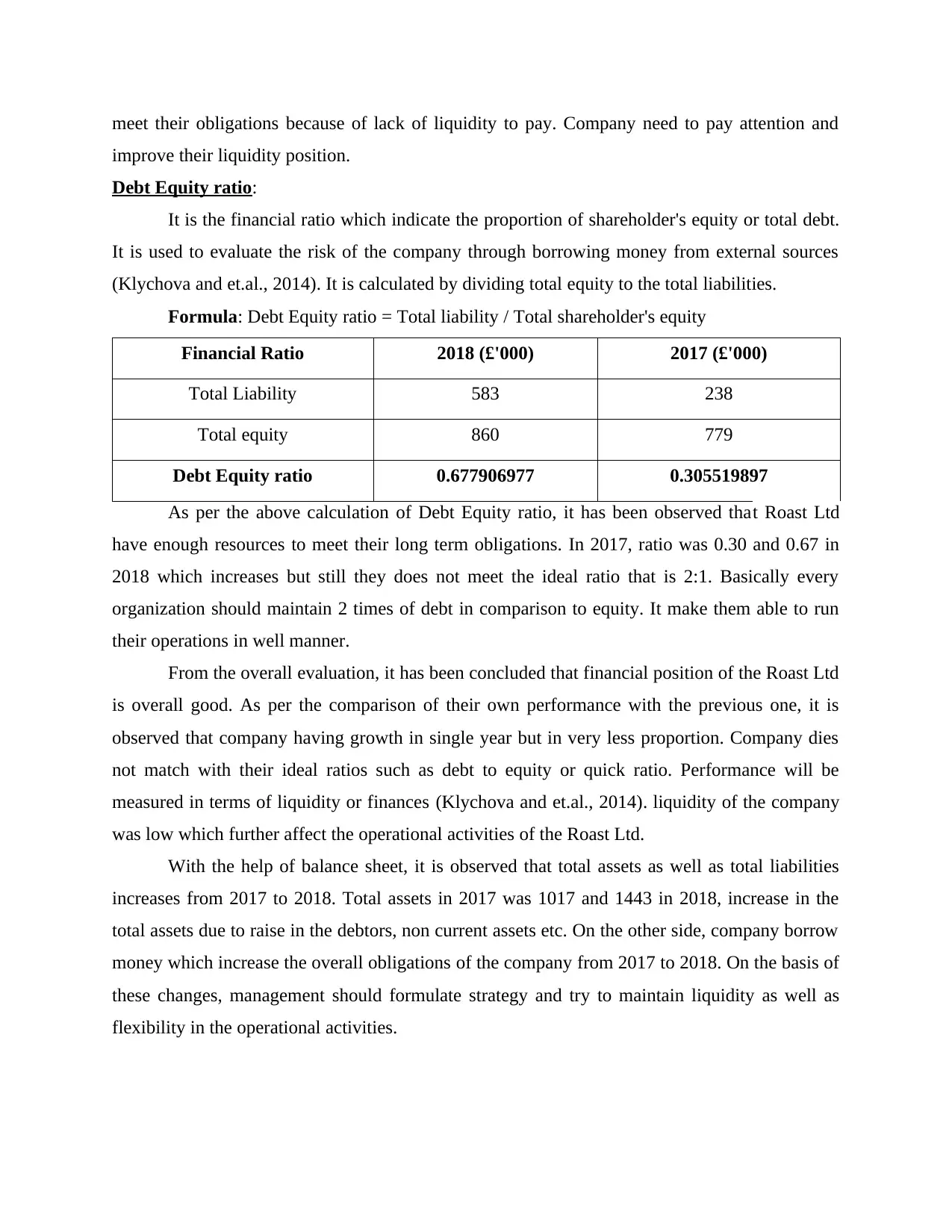

Debt Equity ratio:

It is the financial ratio which indicate the proportion of shareholder's equity or total debt.

It is used to evaluate the risk of the company through borrowing money from external sources

(Klychova and et.al., 2014). It is calculated by dividing total equity to the total liabilities.

Formula: Debt Equity ratio = Total liability / Total shareholder's equity

Financial Ratio 2018 (£'000) 2017 (£'000)

Total Liability 583 238

Total equity 860 779

Debt Equity ratio 0.677906977 0.305519897

As per the above calculation of Debt Equity ratio, it has been observed that Roast Ltd

have enough resources to meet their long term obligations. In 2017, ratio was 0.30 and 0.67 in

2018 which increases but still they does not meet the ideal ratio that is 2:1. Basically every

organization should maintain 2 times of debt in comparison to equity. It make them able to run

their operations in well manner.

From the overall evaluation, it has been concluded that financial position of the Roast Ltd

is overall good. As per the comparison of their own performance with the previous one, it is

observed that company having growth in single year but in very less proportion. Company dies

not match with their ideal ratios such as debt to equity or quick ratio. Performance will be

measured in terms of liquidity or finances (Klychova and et.al., 2014). liquidity of the company

was low which further affect the operational activities of the Roast Ltd.

With the help of balance sheet, it is observed that total assets as well as total liabilities

increases from 2017 to 2018. Total assets in 2017 was 1017 and 1443 in 2018, increase in the

total assets due to raise in the debtors, non current assets etc. On the other side, company borrow

money which increase the overall obligations of the company from 2017 to 2018. On the basis of

these changes, management should formulate strategy and try to maintain liquidity as well as

flexibility in the operational activities.

improve their liquidity position.

Debt Equity ratio:

It is the financial ratio which indicate the proportion of shareholder's equity or total debt.

It is used to evaluate the risk of the company through borrowing money from external sources

(Klychova and et.al., 2014). It is calculated by dividing total equity to the total liabilities.

Formula: Debt Equity ratio = Total liability / Total shareholder's equity

Financial Ratio 2018 (£'000) 2017 (£'000)

Total Liability 583 238

Total equity 860 779

Debt Equity ratio 0.677906977 0.305519897

As per the above calculation of Debt Equity ratio, it has been observed that Roast Ltd

have enough resources to meet their long term obligations. In 2017, ratio was 0.30 and 0.67 in

2018 which increases but still they does not meet the ideal ratio that is 2:1. Basically every

organization should maintain 2 times of debt in comparison to equity. It make them able to run

their operations in well manner.

From the overall evaluation, it has been concluded that financial position of the Roast Ltd

is overall good. As per the comparison of their own performance with the previous one, it is

observed that company having growth in single year but in very less proportion. Company dies

not match with their ideal ratios such as debt to equity or quick ratio. Performance will be

measured in terms of liquidity or finances (Klychova and et.al., 2014). liquidity of the company

was low which further affect the operational activities of the Roast Ltd.

With the help of balance sheet, it is observed that total assets as well as total liabilities

increases from 2017 to 2018. Total assets in 2017 was 1017 and 1443 in 2018, increase in the

total assets due to raise in the debtors, non current assets etc. On the other side, company borrow

money which increase the overall obligations of the company from 2017 to 2018. On the basis of

these changes, management should formulate strategy and try to maintain liquidity as well as

flexibility in the operational activities.

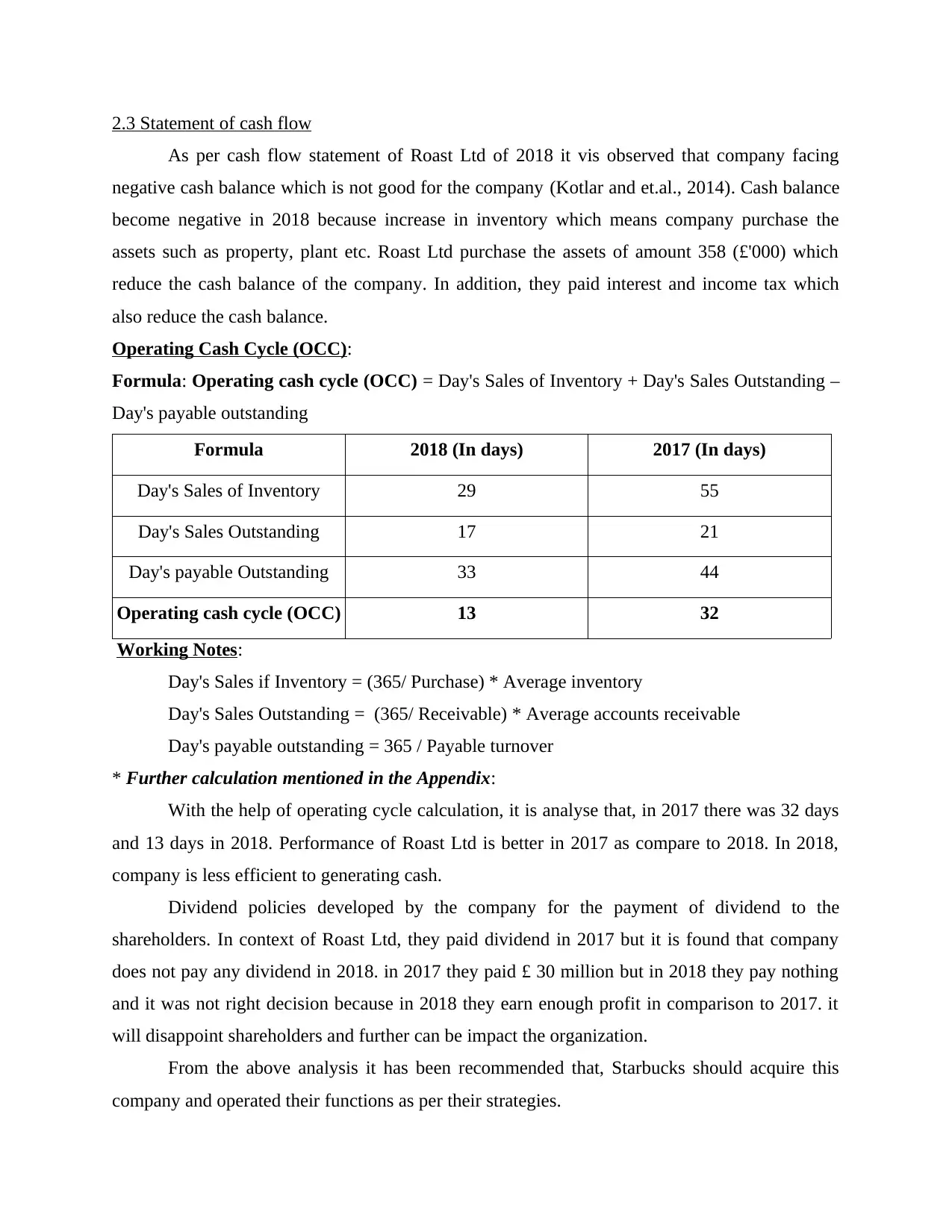

2.3 Statement of cash flow

As per cash flow statement of Roast Ltd of 2018 it vis observed that company facing

negative cash balance which is not good for the company (Kotlar and et.al., 2014). Cash balance

become negative in 2018 because increase in inventory which means company purchase the

assets such as property, plant etc. Roast Ltd purchase the assets of amount 358 (£'000) which

reduce the cash balance of the company. In addition, they paid interest and income tax which

also reduce the cash balance.

Operating Cash Cycle (OCC):

Formula: Operating cash cycle (OCC) = Day's Sales of Inventory + Day's Sales Outstanding –

Day's payable outstanding

Formula 2018 (In days) 2017 (In days)

Day's Sales of Inventory 29 55

Day's Sales Outstanding 17 21

Day's payable Outstanding 33 44

Operating cash cycle (OCC) 13 32

Working Notes:

Day's Sales if Inventory = (365/ Purchase) * Average inventory

Day's Sales Outstanding = (365/ Receivable) * Average accounts receivable

Day's payable outstanding = 365 / Payable turnover

* Further calculation mentioned in the Appendix:

With the help of operating cycle calculation, it is analyse that, in 2017 there was 32 days

and 13 days in 2018. Performance of Roast Ltd is better in 2017 as compare to 2018. In 2018,

company is less efficient to generating cash.

Dividend policies developed by the company for the payment of dividend to the

shareholders. In context of Roast Ltd, they paid dividend in 2017 but it is found that company

does not pay any dividend in 2018. in 2017 they paid £ 30 million but in 2018 they pay nothing

and it was not right decision because in 2018 they earn enough profit in comparison to 2017. it

will disappoint shareholders and further can be impact the organization.

From the above analysis it has been recommended that, Starbucks should acquire this

company and operated their functions as per their strategies.

As per cash flow statement of Roast Ltd of 2018 it vis observed that company facing

negative cash balance which is not good for the company (Kotlar and et.al., 2014). Cash balance

become negative in 2018 because increase in inventory which means company purchase the

assets such as property, plant etc. Roast Ltd purchase the assets of amount 358 (£'000) which

reduce the cash balance of the company. In addition, they paid interest and income tax which

also reduce the cash balance.

Operating Cash Cycle (OCC):

Formula: Operating cash cycle (OCC) = Day's Sales of Inventory + Day's Sales Outstanding –

Day's payable outstanding

Formula 2018 (In days) 2017 (In days)

Day's Sales of Inventory 29 55

Day's Sales Outstanding 17 21

Day's payable Outstanding 33 44

Operating cash cycle (OCC) 13 32

Working Notes:

Day's Sales if Inventory = (365/ Purchase) * Average inventory

Day's Sales Outstanding = (365/ Receivable) * Average accounts receivable

Day's payable outstanding = 365 / Payable turnover

* Further calculation mentioned in the Appendix:

With the help of operating cycle calculation, it is analyse that, in 2017 there was 32 days

and 13 days in 2018. Performance of Roast Ltd is better in 2017 as compare to 2018. In 2018,

company is less efficient to generating cash.

Dividend policies developed by the company for the payment of dividend to the

shareholders. In context of Roast Ltd, they paid dividend in 2017 but it is found that company

does not pay any dividend in 2018. in 2017 they paid £ 30 million but in 2018 they pay nothing

and it was not right decision because in 2018 they earn enough profit in comparison to 2017. it

will disappoint shareholders and further can be impact the organization.

From the above analysis it has been recommended that, Starbucks should acquire this

company and operated their functions as per their strategies.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Part 3 – Investment appraisal and source of finance

3.1 Investment Appraisal

Management forecast: Forecasting is the process of managing future activities where

they make decisions for future on the basis of previous projection (Petersen, Kushwaha and

Kumar, 2015). In context of Roast Ltd, company make decision to invest £ 500 million for the

expansion of their operation in Romania. Company forecast the figures from 2017 to 2021

where cash outflow from this project will be £62, £112, £148, £180 and £224. managers of Roast

Ltd expected to increase their revenue over the years. But they have to make sure that in the

initial stage they have to expect less because there are various complications company face due

to in favourable circumstances. Initial investment of the Roast Ltd company is £ 500 million and

they estimate the revenue of £ 300 million, £ 560 million, £ 740 million, £ 900 million and £

1120 million for the next five years respectively.

UK market already face the various challenges in respect of change in climate which

impact the production of coffee. So they need to analyse the weather condition of Romania and

select the suitable time which is beneficial to produce. Along with this, they need to identify the

interest of Romania's citizens regarding coffee. If they interested or prefer to consume coffee

then it is suitable expansion for the company.

Investment appraisal technique:

Payback Period: It is the time period which required to recover the initial investment in

the project. Lower the period is beneficial for the company because high payback period take

longer time to recover. Before making any investments they need to evaluate the duration and

select the best alternative for future investment. In context of Roast Ltd, for the expansion of

their operation in Romania they invest £ 500 million which estimated to recover in next five

years along with huge revenue. Payback period of this project will be 4 it means Roast Ltd can

recover their cost in 4 years and further it provides the more benefits. This technique has some

benefits as well as drawbacks which mentioned below:

Benefits: It is the simplest method of capital budgeting techniques which helps the

organizations to choose the best alternative for the investment.

Drawbacks: Most of the time it happen that final outcome is irrelevant due to ignorance

of some factors such as time value of money, inflation etc.

3.1 Investment Appraisal

Management forecast: Forecasting is the process of managing future activities where

they make decisions for future on the basis of previous projection (Petersen, Kushwaha and

Kumar, 2015). In context of Roast Ltd, company make decision to invest £ 500 million for the

expansion of their operation in Romania. Company forecast the figures from 2017 to 2021

where cash outflow from this project will be £62, £112, £148, £180 and £224. managers of Roast

Ltd expected to increase their revenue over the years. But they have to make sure that in the

initial stage they have to expect less because there are various complications company face due

to in favourable circumstances. Initial investment of the Roast Ltd company is £ 500 million and

they estimate the revenue of £ 300 million, £ 560 million, £ 740 million, £ 900 million and £

1120 million for the next five years respectively.

UK market already face the various challenges in respect of change in climate which

impact the production of coffee. So they need to analyse the weather condition of Romania and

select the suitable time which is beneficial to produce. Along with this, they need to identify the

interest of Romania's citizens regarding coffee. If they interested or prefer to consume coffee

then it is suitable expansion for the company.

Investment appraisal technique:

Payback Period: It is the time period which required to recover the initial investment in

the project. Lower the period is beneficial for the company because high payback period take

longer time to recover. Before making any investments they need to evaluate the duration and

select the best alternative for future investment. In context of Roast Ltd, for the expansion of

their operation in Romania they invest £ 500 million which estimated to recover in next five

years along with huge revenue. Payback period of this project will be 4 it means Roast Ltd can

recover their cost in 4 years and further it provides the more benefits. This technique has some

benefits as well as drawbacks which mentioned below:

Benefits: It is the simplest method of capital budgeting techniques which helps the

organizations to choose the best alternative for the investment.

Drawbacks: Most of the time it happen that final outcome is irrelevant due to ignorance

of some factors such as time value of money, inflation etc.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Accounting Rate of Return: It is the financial ratio where organizations evaluate the

accounting rate of return for the specific project. Under this method, percentage value represent

the return of their investments (Shepherd, Williams and Patzelt, 2015). So in multiple options,

business select the higher return project for the investment. In context of Roast Ltd, accounting

rate of return of the company will be 18% which is good in figures. With the help of investment

appraisal technique, management able to evaluate that expansion of any project is beneficial or

not. This project is look beneficial because it provides 18% accounting rate of return which is

good.

Benefits: This method is beneficial for the organizations because they able to measure

the profitability of each project and make their decisions accordingly.

Drawbacks: It exclude the critical factors such as time value of their investment and

considered cash flows which was not discounted.

Net Present Value: This capital budgeting method implement of the range of cash flows

which generated at different time period. It is used for investment planning where they have to

analyse the profitability of each project. Management of Roast Ltd required to evaluate that net

present value of the project which is £ 110 million. Company use the 5% cost of capital for the

evaluation of this project.

Benefits: It is the most accurate technique which provide the effective outcomes and here

cash flows are discounted.

Drawbacks: It is totally based on the assumption where they guessing cost of capital as

well as cash flow of project.

With the help of investment appraisal technique business able to forecast which help

them to make decision for further expansion. Managers of Roast Ltd evaluate that, with the help

of £ 500 million initial investment company able to recover their cost in 4 years. Along with this,

net present value of the company will be £ 110 million and accounting rate of return is 18%.

Expansion decision of Roast Ltd was right because as per appraisal technique company

get the enough revenue as well as they perform well in order to achieve their business goals &

objectives.

3.2 Source of finance

There are different types of sources of finance that utilise by the organisation to receive

fund to conduct different types of activities in the business (Sunder, 2016). In the context of the

accounting rate of return for the specific project. Under this method, percentage value represent

the return of their investments (Shepherd, Williams and Patzelt, 2015). So in multiple options,

business select the higher return project for the investment. In context of Roast Ltd, accounting

rate of return of the company will be 18% which is good in figures. With the help of investment

appraisal technique, management able to evaluate that expansion of any project is beneficial or

not. This project is look beneficial because it provides 18% accounting rate of return which is

good.

Benefits: This method is beneficial for the organizations because they able to measure

the profitability of each project and make their decisions accordingly.

Drawbacks: It exclude the critical factors such as time value of their investment and

considered cash flows which was not discounted.

Net Present Value: This capital budgeting method implement of the range of cash flows

which generated at different time period. It is used for investment planning where they have to

analyse the profitability of each project. Management of Roast Ltd required to evaluate that net

present value of the project which is £ 110 million. Company use the 5% cost of capital for the

evaluation of this project.

Benefits: It is the most accurate technique which provide the effective outcomes and here

cash flows are discounted.

Drawbacks: It is totally based on the assumption where they guessing cost of capital as

well as cash flow of project.

With the help of investment appraisal technique business able to forecast which help

them to make decision for further expansion. Managers of Roast Ltd evaluate that, with the help

of £ 500 million initial investment company able to recover their cost in 4 years. Along with this,

net present value of the company will be £ 110 million and accounting rate of return is 18%.

Expansion decision of Roast Ltd was right because as per appraisal technique company

get the enough revenue as well as they perform well in order to achieve their business goals &

objectives.

3.2 Source of finance

There are different types of sources of finance that utilise by the organisation to receive

fund to conduct different types of activities in the business (Sunder, 2016). In the context of the

Roast Ltd can expand to their business on big level so for this required to more fund that invest

in the business and prepare budget how to increase business and invest money in right things.

There are two source of finance which mentioned below:

Banks: It is one of the major sources of the fund that use by most of the organisation to

get money. To get money from this source required to give in deposit something because in case

of not paid money in particular time so take that particular thing. Most of the companies select

that particular sources because company get in lower interest on amount of fund that provide

effective outcomes as effective finance cost. The particulate sources of fund provided by the

bank on the basis of credit score and brand image. The bank provide fund in both manner long

term and short and according to that charge interest amount. The Roast Ltd wants to expand the

business activities at big level so for this required to fund. The cafe disclose their annual reports

which include the various financial statements which make them able to provide credit score and

take loan from banks. This source of fund have some benefits and drawbacks that discussed

below:

Advantages: The main benefit of this sources that it provides loan at cheap interest and

provide safety of public wealth (Valentine and Hollingworth, 2015).

Disadvantages: It is limited sources and provide amount according to credit score if

company have not good score so they don't get amount of loan.

Business angles: It is type of the source of the fund which is selected by the organisation

of fund. In this company take decisions for wealthy individual and make investment in business

venture. These individual helps to organisation to take appropriate financial decision and guide

as financial assistance. The aim purpose of the business angles to supports to entrepreneurship

individual succeed with particular business idea due to invest the own money in right business

and generate more money (Zietlow and et.al., 2018). The Roast Ltd wants to generate more

profit so they are investing their amount in business venture where they get huge money and use

in further activities. There are discussed different advantages and disadvantages of this sources

such as:

Advantages: There is company get amount without any interest and beneficial due to

individual make invest according to their interest.

Disadvantages: Many times company does not find out healthy business angle that

provide right suggestion regarding to business.

in the business and prepare budget how to increase business and invest money in right things.

There are two source of finance which mentioned below:

Banks: It is one of the major sources of the fund that use by most of the organisation to

get money. To get money from this source required to give in deposit something because in case

of not paid money in particular time so take that particular thing. Most of the companies select

that particular sources because company get in lower interest on amount of fund that provide

effective outcomes as effective finance cost. The particulate sources of fund provided by the

bank on the basis of credit score and brand image. The bank provide fund in both manner long

term and short and according to that charge interest amount. The Roast Ltd wants to expand the

business activities at big level so for this required to fund. The cafe disclose their annual reports

which include the various financial statements which make them able to provide credit score and

take loan from banks. This source of fund have some benefits and drawbacks that discussed

below:

Advantages: The main benefit of this sources that it provides loan at cheap interest and

provide safety of public wealth (Valentine and Hollingworth, 2015).

Disadvantages: It is limited sources and provide amount according to credit score if

company have not good score so they don't get amount of loan.

Business angles: It is type of the source of the fund which is selected by the organisation

of fund. In this company take decisions for wealthy individual and make investment in business

venture. These individual helps to organisation to take appropriate financial decision and guide

as financial assistance. The aim purpose of the business angles to supports to entrepreneurship

individual succeed with particular business idea due to invest the own money in right business

and generate more money (Zietlow and et.al., 2018). The Roast Ltd wants to generate more

profit so they are investing their amount in business venture where they get huge money and use

in further activities. There are discussed different advantages and disadvantages of this sources

such as:

Advantages: There is company get amount without any interest and beneficial due to

individual make invest according to their interest.

Disadvantages: Many times company does not find out healthy business angle that

provide right suggestion regarding to business.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.