[SOLVED] Financial Analysis of Harvey Homes Plc.

VerifiedAdded on 2020/09/03

|23

|5220

|56

AI Summary

The assignment involves a comprehensive financial analysis of Harvey Homes Plc., including calculation of key ratios such as debt ratio, quick ratio, current ratio, days inventory outstanding (DIO), days sales outstanding (DSO), and days payable outstanding (DPO). It also compares the company's gross profit and net sales, operating profits and revenue, cash conversion cycle, and cash flow from operating, investing, and financing activities. The analysis provides a detailed understanding of the company's financial performance and position.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

FINANCIAL DECISION

MAKING

MAKING

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

EXECUTIVE SUMMARY.............................................................................................................1

PART 1............................................................................................................................................1

Analysing the statement of profit or loss................................................................................1

Financial position analysis.....................................................................................................5

Analysis of cash flow statement.............................................................................................9

Market Segment Analysis.....................................................................................................10

PART 2: INVESTMENT APPRAISAL........................................................................................12

Management forecast ...........................................................................................................12

Techniques of investment appraisal ....................................................................................12

Payback period ................................................................................................................12

Accounting/Average rate of return (ARR) .....................................................................13

Net present value..................................................................................................................13

Non-financial factors ...........................................................................................................14

APPENDIX....................................................................................................................................18

EXECUTIVE SUMMARY.............................................................................................................1

PART 1............................................................................................................................................1

Analysing the statement of profit or loss................................................................................1

Financial position analysis.....................................................................................................5

Analysis of cash flow statement.............................................................................................9

Market Segment Analysis.....................................................................................................10

PART 2: INVESTMENT APPRAISAL........................................................................................12

Management forecast ...........................................................................................................12

Techniques of investment appraisal ....................................................................................12

Payback period ................................................................................................................12

Accounting/Average rate of return (ARR) .....................................................................13

Net present value..................................................................................................................13

Non-financial factors ...........................................................................................................14

APPENDIX....................................................................................................................................18

Illustration Index

Illustration 1: Comparison of gross profit and net sales..................................................................2

Illustration 2: Comparison of operating profits and revenue..........................................................3

Illustration 3: Comparison of operating profits and capital employed............................................4

Illustration 4: Current ratio of Harvey Homes Plc...........................................................................6

Illustration 5: Quick ratio of Harvey Homes Plc.............................................................................7

Illustration 6: Debt ratio of the Harvey Homes Plc.........................................................................8

Illustration 7: Cash flow from operating, investing and financing activities...................................9

Illustration 8: Comparison of Cash Conversion Cycle..................................................................10

Illustration 9: Comparison of the company's different segments..................................................11

Index of Tables

Table 1: Ratio analysis for profit and loss statement.....................................................................18

Table 2: Calculation of Capital employed.....................................................................................18

Table 3: Cash flow from operating, investing and financing activities.........................................19

Table 4: Calculation of DIO, DSO and DPO.................................................................................19

Illustration 1: Comparison of gross profit and net sales..................................................................2

Illustration 2: Comparison of operating profits and revenue..........................................................3

Illustration 3: Comparison of operating profits and capital employed............................................4

Illustration 4: Current ratio of Harvey Homes Plc...........................................................................6

Illustration 5: Quick ratio of Harvey Homes Plc.............................................................................7

Illustration 6: Debt ratio of the Harvey Homes Plc.........................................................................8

Illustration 7: Cash flow from operating, investing and financing activities...................................9

Illustration 8: Comparison of Cash Conversion Cycle..................................................................10

Illustration 9: Comparison of the company's different segments..................................................11

Index of Tables

Table 1: Ratio analysis for profit and loss statement.....................................................................18

Table 2: Calculation of Capital employed.....................................................................................18

Table 3: Cash flow from operating, investing and financing activities.........................................19

Table 4: Calculation of DIO, DSO and DPO.................................................................................19

EXECUTIVE SUMMARY

Analysing the financial statements of the entity helps in better decision making. It is

helpful in comparative analysis of sales, profits, assets etc (Allen, Larson and Sloan, 2013).

Harvey homes is a company which is involved in creating quality homes. Ratio analysis

technique have been used to analyse the financial statement of the company. Capital

budgeting technique have been used to assess that whether the project will prove to be

profitable for the company or not. The key findings suggest that current ratio of the company

is on higher side as compared to the ideal one which shows that the entity is not optimally

utilizing its resources available with it. Further, it has taken long term loan for 150 million in

order to meet its expenses as Harvey is not generating much operating cash in order to meet

out its needs. Midlands in not generating high revenues where the entity is advised to

improve its product mix and marketing strategy for better profits in near future. Moreover,

some financial and non-financial factors have been discussed which the enterprise should

consider while expanding in other country.

PART 1

Analysing the statement of profit or loss

Gross margin ratio

1

Analysing the financial statements of the entity helps in better decision making. It is

helpful in comparative analysis of sales, profits, assets etc (Allen, Larson and Sloan, 2013).

Harvey homes is a company which is involved in creating quality homes. Ratio analysis

technique have been used to analyse the financial statement of the company. Capital

budgeting technique have been used to assess that whether the project will prove to be

profitable for the company or not. The key findings suggest that current ratio of the company

is on higher side as compared to the ideal one which shows that the entity is not optimally

utilizing its resources available with it. Further, it has taken long term loan for 150 million in

order to meet its expenses as Harvey is not generating much operating cash in order to meet

out its needs. Midlands in not generating high revenues where the entity is advised to

improve its product mix and marketing strategy for better profits in near future. Moreover,

some financial and non-financial factors have been discussed which the enterprise should

consider while expanding in other country.

PART 1

Analysing the statement of profit or loss

Gross margin ratio

1

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

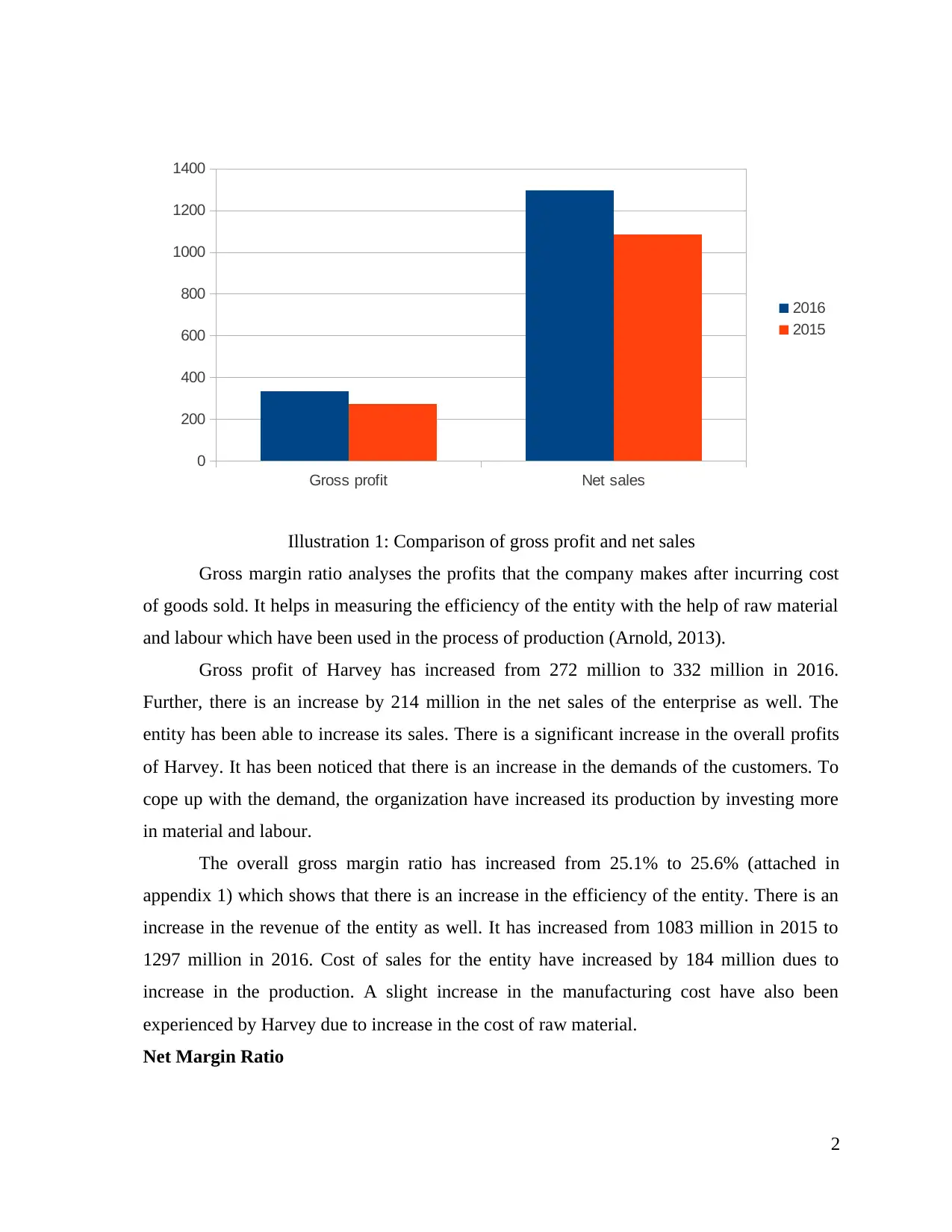

Gross margin ratio analyses the profits that the company makes after incurring cost

of goods sold. It helps in measuring the efficiency of the entity with the help of raw material

and labour which have been used in the process of production (Arnold, 2013).

Gross profit of Harvey has increased from 272 million to 332 million in 2016.

Further, there is an increase by 214 million in the net sales of the enterprise as well. The

entity has been able to increase its sales. There is a significant increase in the overall profits

of Harvey. It has been noticed that there is an increase in the demands of the customers. To

cope up with the demand, the organization have increased its production by investing more

in material and labour.

The overall gross margin ratio has increased from 25.1% to 25.6% (attached in

appendix 1) which shows that there is an increase in the efficiency of the entity. There is an

increase in the revenue of the entity as well. It has increased from 1083 million in 2015 to

1297 million in 2016. Cost of sales for the entity have increased by 184 million dues to

increase in the production. A slight increase in the manufacturing cost have also been

experienced by Harvey due to increase in the cost of raw material.

Net Margin Ratio

2

Gross profit Net sales

0

200

400

600

800

1000

1200

1400

2016

2015

Illustration 1: Comparison of gross profit and net sales

of goods sold. It helps in measuring the efficiency of the entity with the help of raw material

and labour which have been used in the process of production (Arnold, 2013).

Gross profit of Harvey has increased from 272 million to 332 million in 2016.

Further, there is an increase by 214 million in the net sales of the enterprise as well. The

entity has been able to increase its sales. There is a significant increase in the overall profits

of Harvey. It has been noticed that there is an increase in the demands of the customers. To

cope up with the demand, the organization have increased its production by investing more

in material and labour.

The overall gross margin ratio has increased from 25.1% to 25.6% (attached in

appendix 1) which shows that there is an increase in the efficiency of the entity. There is an

increase in the revenue of the entity as well. It has increased from 1083 million in 2015 to

1297 million in 2016. Cost of sales for the entity have increased by 184 million dues to

increase in the production. A slight increase in the manufacturing cost have also been

experienced by Harvey due to increase in the cost of raw material.

Net Margin Ratio

2

Gross profit Net sales

0

200

400

600

800

1000

1200

1400

2016

2015

Illustration 1: Comparison of gross profit and net sales

Operating profits Revenue

0

200

400

600

800

1000

1200

1400

2016

2015

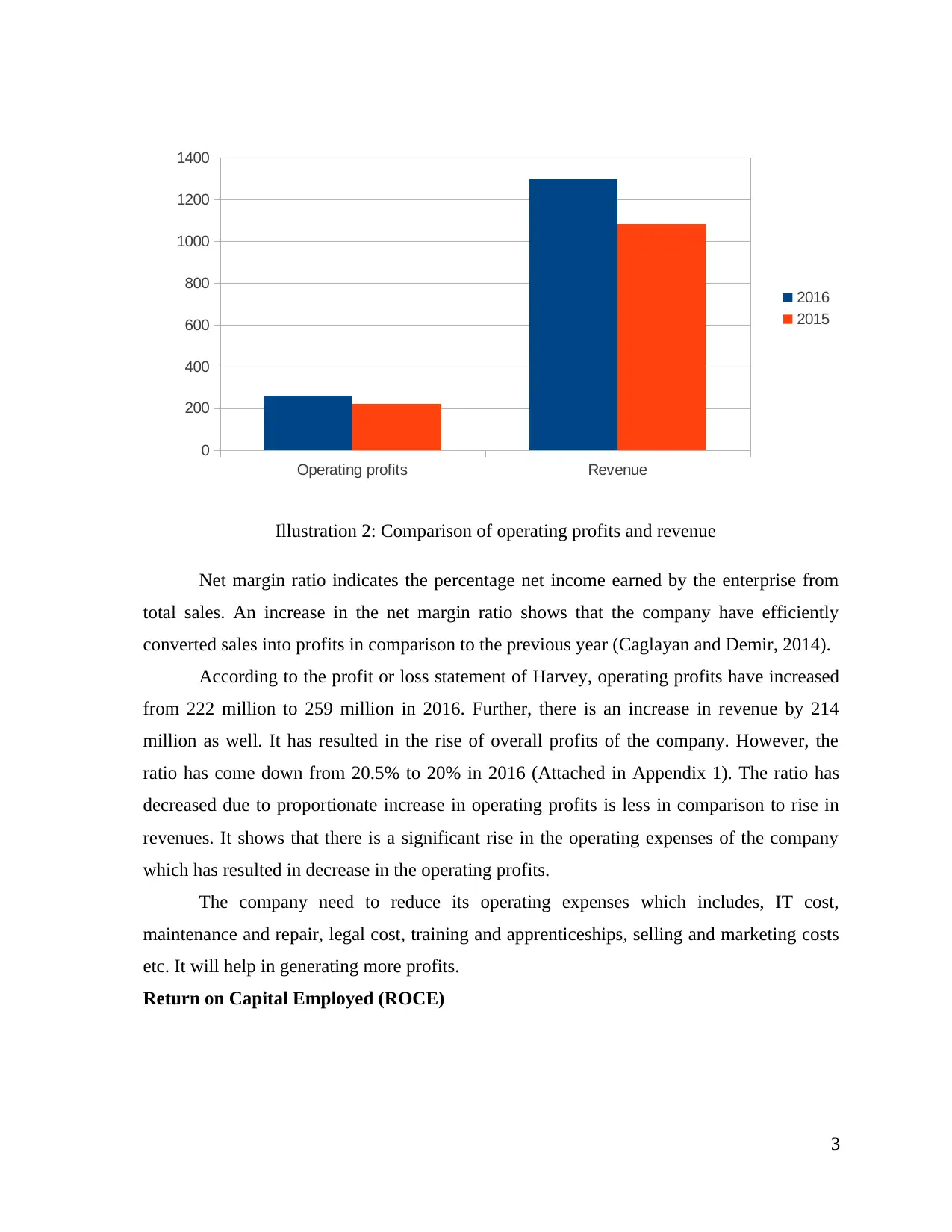

Illustration 2: Comparison of operating profits and revenue

Net margin ratio indicates the percentage net income earned by the enterprise from

total sales. An increase in the net margin ratio shows that the company have efficiently

converted sales into profits in comparison to the previous year (Caglayan and Demir, 2014).

According to the profit or loss statement of Harvey, operating profits have increased

from 222 million to 259 million in 2016. Further, there is an increase in revenue by 214

million as well. It has resulted in the rise of overall profits of the company. However, the

ratio has come down from 20.5% to 20% in 2016 (Attached in Appendix 1). The ratio has

decreased due to proportionate increase in operating profits is less in comparison to rise in

revenues. It shows that there is a significant rise in the operating expenses of the company

which has resulted in decrease in the operating profits.

The company need to reduce its operating expenses which includes, IT cost,

maintenance and repair, legal cost, training and apprenticeships, selling and marketing costs

etc. It will help in generating more profits.

Return on Capital Employed (ROCE)

3

0

200

400

600

800

1000

1200

1400

2016

2015

Illustration 2: Comparison of operating profits and revenue

Net margin ratio indicates the percentage net income earned by the enterprise from

total sales. An increase in the net margin ratio shows that the company have efficiently

converted sales into profits in comparison to the previous year (Caglayan and Demir, 2014).

According to the profit or loss statement of Harvey, operating profits have increased

from 222 million to 259 million in 2016. Further, there is an increase in revenue by 214

million as well. It has resulted in the rise of overall profits of the company. However, the

ratio has come down from 20.5% to 20% in 2016 (Attached in Appendix 1). The ratio has

decreased due to proportionate increase in operating profits is less in comparison to rise in

revenues. It shows that there is a significant rise in the operating expenses of the company

which has resulted in decrease in the operating profits.

The company need to reduce its operating expenses which includes, IT cost,

maintenance and repair, legal cost, training and apprenticeships, selling and marketing costs

etc. It will help in generating more profits.

Return on Capital Employed (ROCE)

3

Operating profits Capital employed

0

200

400

600

800

1000

1200

1400

1600

2016

2015

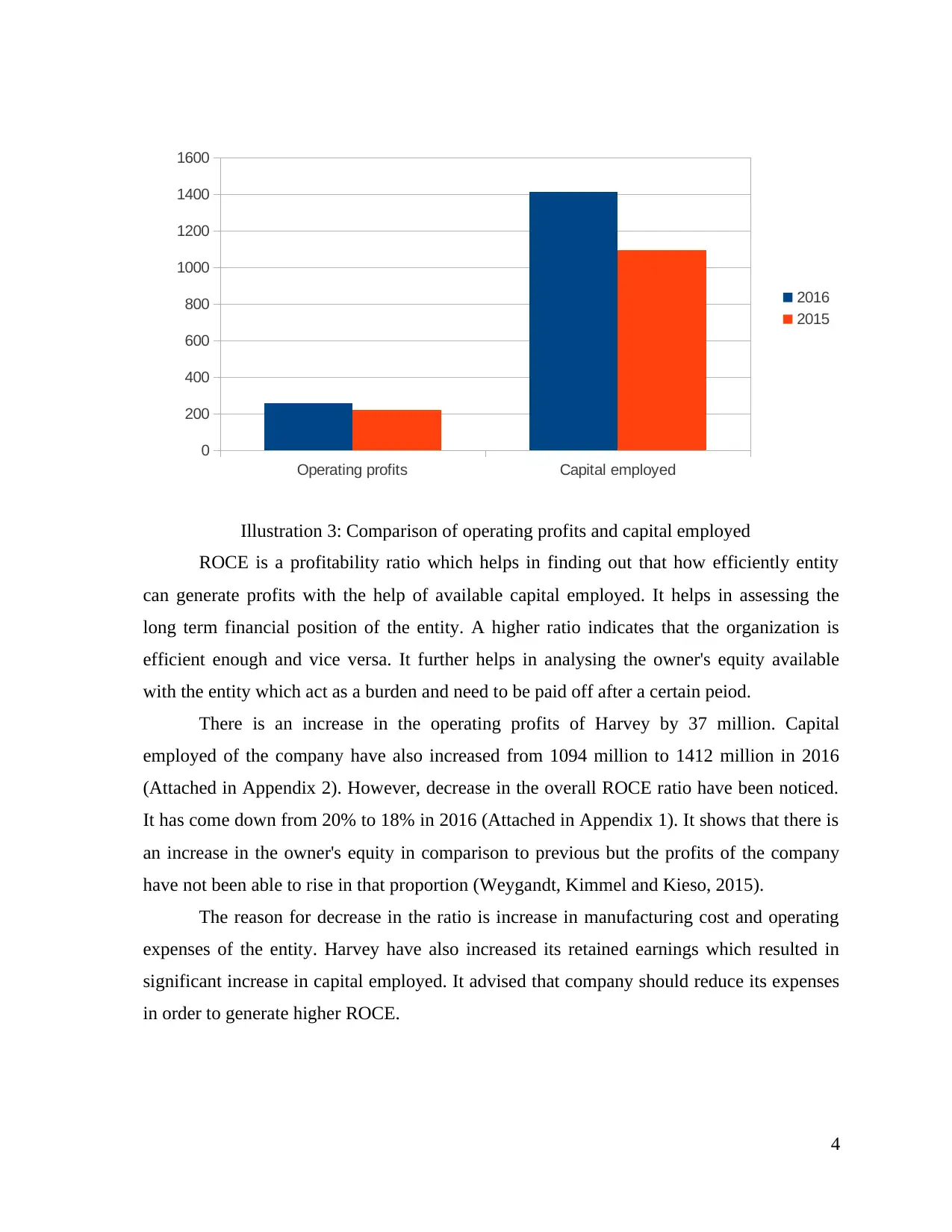

Illustration 3: Comparison of operating profits and capital employed

ROCE is a profitability ratio which helps in finding out that how efficiently entity

can generate profits with the help of available capital employed. It helps in assessing the

long term financial position of the entity. A higher ratio indicates that the organization is

efficient enough and vice versa. It further helps in analysing the owner's equity available

with the entity which act as a burden and need to be paid off after a certain peiod.

There is an increase in the operating profits of Harvey by 37 million. Capital

employed of the company have also increased from 1094 million to 1412 million in 2016

(Attached in Appendix 2). However, decrease in the overall ROCE ratio have been noticed.

It has come down from 20% to 18% in 2016 (Attached in Appendix 1). It shows that there is

an increase in the owner's equity in comparison to previous but the profits of the company

have not been able to rise in that proportion (Weygandt, Kimmel and Kieso, 2015).

The reason for decrease in the ratio is increase in manufacturing cost and operating

expenses of the entity. Harvey have also increased its retained earnings which resulted in

significant increase in capital employed. It advised that company should reduce its expenses

in order to generate higher ROCE.

4

0

200

400

600

800

1000

1200

1400

1600

2016

2015

Illustration 3: Comparison of operating profits and capital employed

ROCE is a profitability ratio which helps in finding out that how efficiently entity

can generate profits with the help of available capital employed. It helps in assessing the

long term financial position of the entity. A higher ratio indicates that the organization is

efficient enough and vice versa. It further helps in analysing the owner's equity available

with the entity which act as a burden and need to be paid off after a certain peiod.

There is an increase in the operating profits of Harvey by 37 million. Capital

employed of the company have also increased from 1094 million to 1412 million in 2016

(Attached in Appendix 2). However, decrease in the overall ROCE ratio have been noticed.

It has come down from 20% to 18% in 2016 (Attached in Appendix 1). It shows that there is

an increase in the owner's equity in comparison to previous but the profits of the company

have not been able to rise in that proportion (Weygandt, Kimmel and Kieso, 2015).

The reason for decrease in the ratio is increase in manufacturing cost and operating

expenses of the entity. Harvey have also increased its retained earnings which resulted in

significant increase in capital employed. It advised that company should reduce its expenses

in order to generate higher ROCE.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Financial position analysis

The financial position of the company is calculated of the basis of their assets and

liabilities as well as it also includes shareholders equity. To understand the value if the

venture, different investor looks at the organisation's financial position. It can be analysed by

evaluating the different financial ratio of the company. It is the mathematical comparison of

the financial statement categories and accounts. It helps the company's different stakeholders

such as their creditors, shareholders, investors, customers, suppliers as well as it helps the

organisation manage their company internally that how the business is performing and where

it need improvements. Financial ratios are the tool which is used to find the business

standing and if it is compared to past years, the firm can able to know that they are at the

growing stage or not (Caglayan and Demir, 2014). Different financial ratios are as follows:

Liquidity ratio

It helps the organisation to find that they are able to pay their both current liabilities

and their long-term liabilities which has further become the current liabilities. These ratios

communicate the cash level of the venture and how they can turn their recentre assets to pay

of their liabilities. It shows the ability of the organisation to easily convert their assets into

cash. It includes different ratio, that are as follows:

Current ratio: It shows the ability of the company to pay the current liabilities from their

current assets. Quick assets are that which is converted into cash within the 90 working days

such as cash, cash equivalents, marketable securities and short run investments. Formula for

calculating the current ratio is current assets by current liabilities.

Current ratio of Harvey Homes Plc

For 2015

1500+ 39+ 56/ 60+ 471+ 19 = 1595/500 = 3.19 :1

For 2016

1808+36+135/ 44+566+24 = 1979/634 = 2.9 :1

5

The financial position of the company is calculated of the basis of their assets and

liabilities as well as it also includes shareholders equity. To understand the value if the

venture, different investor looks at the organisation's financial position. It can be analysed by

evaluating the different financial ratio of the company. It is the mathematical comparison of

the financial statement categories and accounts. It helps the company's different stakeholders

such as their creditors, shareholders, investors, customers, suppliers as well as it helps the

organisation manage their company internally that how the business is performing and where

it need improvements. Financial ratios are the tool which is used to find the business

standing and if it is compared to past years, the firm can able to know that they are at the

growing stage or not (Caglayan and Demir, 2014). Different financial ratios are as follows:

Liquidity ratio

It helps the organisation to find that they are able to pay their both current liabilities

and their long-term liabilities which has further become the current liabilities. These ratios

communicate the cash level of the venture and how they can turn their recentre assets to pay

of their liabilities. It shows the ability of the organisation to easily convert their assets into

cash. It includes different ratio, that are as follows:

Current ratio: It shows the ability of the company to pay the current liabilities from their

current assets. Quick assets are that which is converted into cash within the 90 working days

such as cash, cash equivalents, marketable securities and short run investments. Formula for

calculating the current ratio is current assets by current liabilities.

Current ratio of Harvey Homes Plc

For 2015

1500+ 39+ 56/ 60+ 471+ 19 = 1595/500 = 3.19 :1

For 2016

1808+36+135/ 44+566+24 = 1979/634 = 2.9 :1

5

1 2

2.75

2.8

2.85

2.9

2.95

3

3.05

3.1

3.15

Current ratio

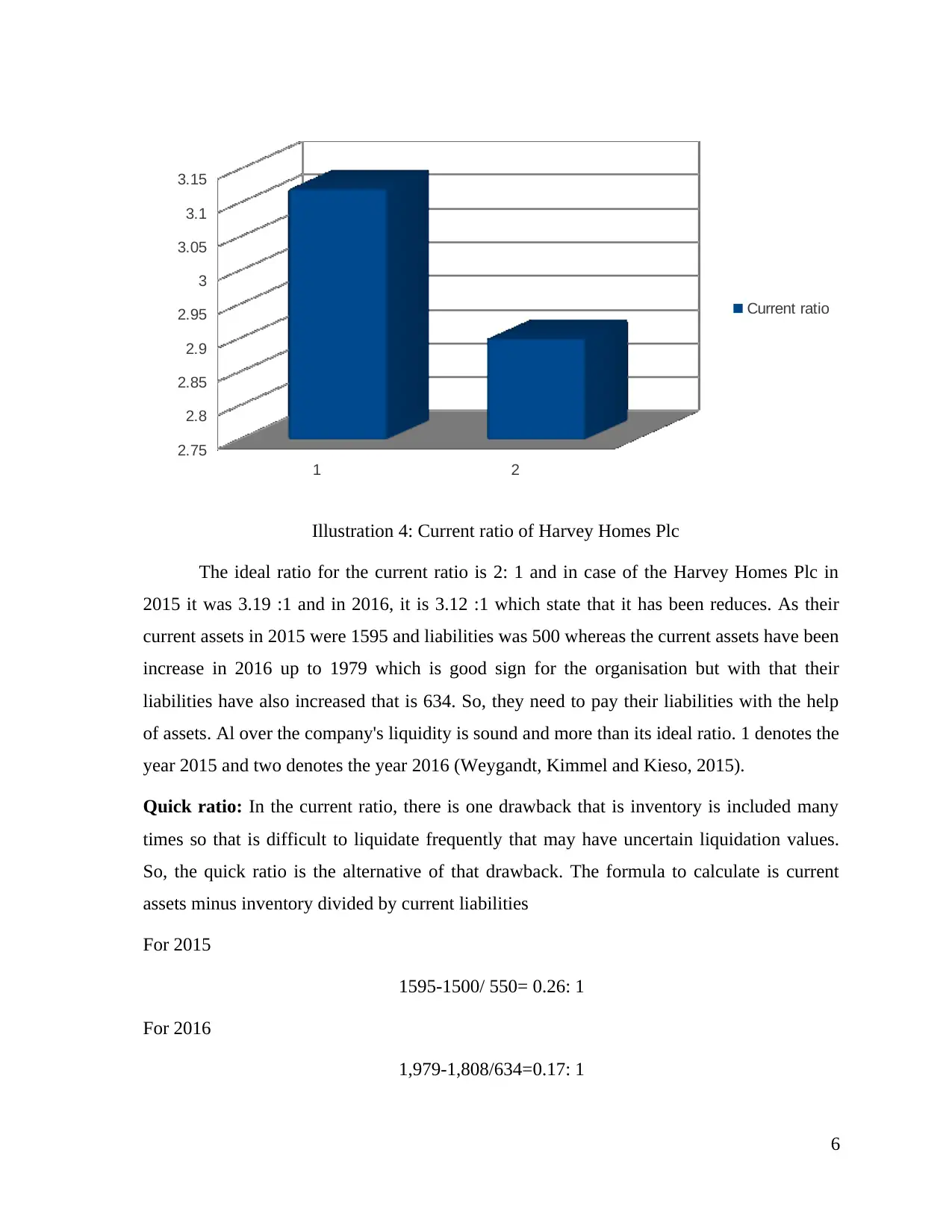

Illustration 4: Current ratio of Harvey Homes Plc

The ideal ratio for the current ratio is 2: 1 and in case of the Harvey Homes Plc in

2015 it was 3.19 :1 and in 2016, it is 3.12 :1 which state that it has been reduces. As their

current assets in 2015 were 1595 and liabilities was 500 whereas the current assets have been

increase in 2016 up to 1979 which is good sign for the organisation but with that their

liabilities have also increased that is 634. So, they need to pay their liabilities with the help

of assets. Al over the company's liquidity is sound and more than its ideal ratio. 1 denotes the

year 2015 and two denotes the year 2016 (Weygandt, Kimmel and Kieso, 2015).

Quick ratio: In the current ratio, there is one drawback that is inventory is included many

times so that is difficult to liquidate frequently that may have uncertain liquidation values.

So, the quick ratio is the alternative of that drawback. The formula to calculate is current

assets minus inventory divided by current liabilities

For 2015

1595-1500/ 550= 0.26: 1

For 2016

1,979-1,808/634=0.17: 1

6

2.75

2.8

2.85

2.9

2.95

3

3.05

3.1

3.15

Current ratio

Illustration 4: Current ratio of Harvey Homes Plc

The ideal ratio for the current ratio is 2: 1 and in case of the Harvey Homes Plc in

2015 it was 3.19 :1 and in 2016, it is 3.12 :1 which state that it has been reduces. As their

current assets in 2015 were 1595 and liabilities was 500 whereas the current assets have been

increase in 2016 up to 1979 which is good sign for the organisation but with that their

liabilities have also increased that is 634. So, they need to pay their liabilities with the help

of assets. Al over the company's liquidity is sound and more than its ideal ratio. 1 denotes the

year 2015 and two denotes the year 2016 (Weygandt, Kimmel and Kieso, 2015).

Quick ratio: In the current ratio, there is one drawback that is inventory is included many

times so that is difficult to liquidate frequently that may have uncertain liquidation values.

So, the quick ratio is the alternative of that drawback. The formula to calculate is current

assets minus inventory divided by current liabilities

For 2015

1595-1500/ 550= 0.26: 1

For 2016

1,979-1,808/634=0.17: 1

6

1 2

0

0.05

0.1

0.15

0.2

0.25

0.3

Quick ratio

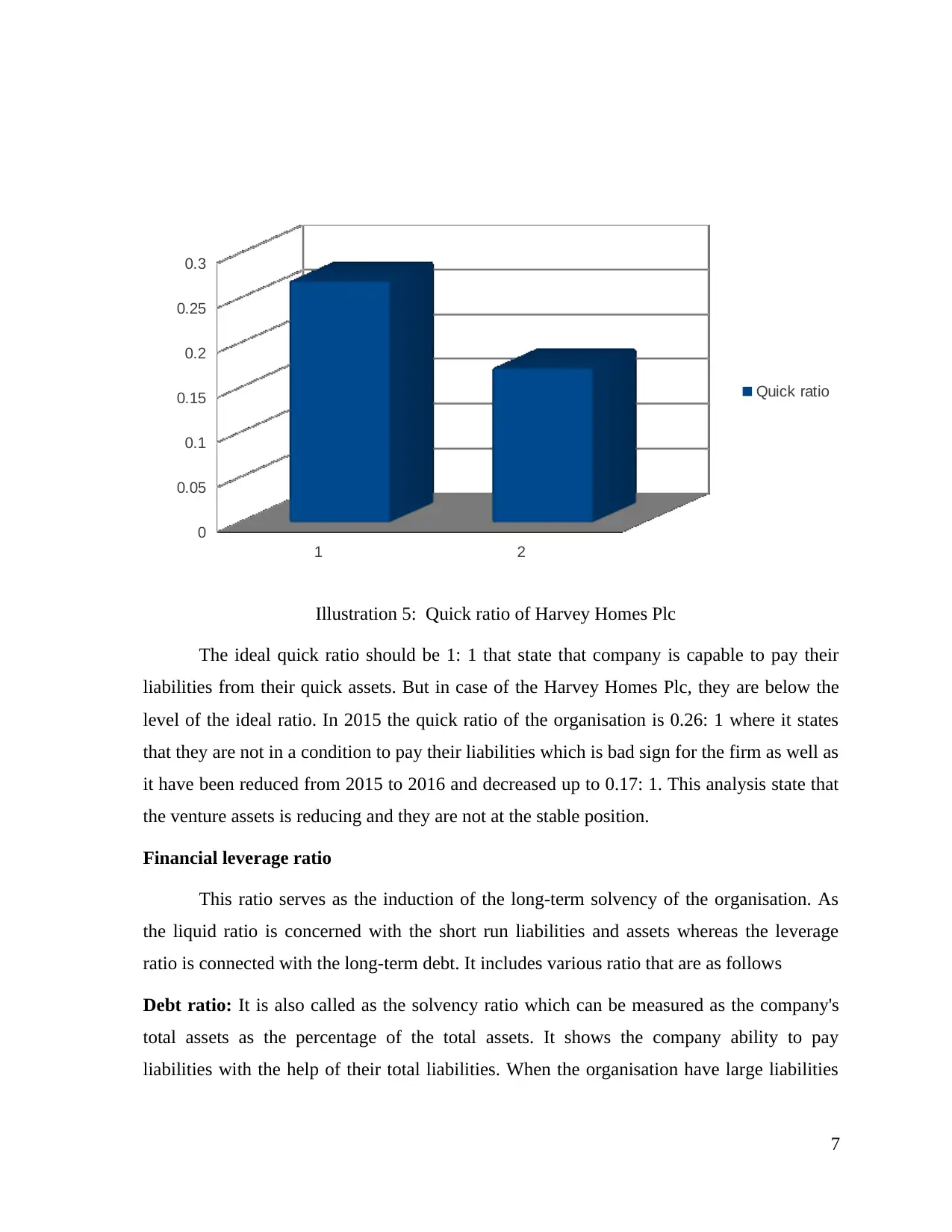

Illustration 5: Quick ratio of Harvey Homes Plc

The ideal quick ratio should be 1: 1 that state that company is capable to pay their

liabilities from their quick assets. But in case of the Harvey Homes Plc, they are below the

level of the ideal ratio. In 2015 the quick ratio of the organisation is 0.26: 1 where it states

that they are not in a condition to pay their liabilities which is bad sign for the firm as well as

it have been reduced from 2015 to 2016 and decreased up to 0.17: 1. This analysis state that

the venture assets is reducing and they are not at the stable position.

Financial leverage ratio

This ratio serves as the induction of the long-term solvency of the organisation. As

the liquid ratio is concerned with the short run liabilities and assets whereas the leverage

ratio is connected with the long-term debt. It includes various ratio that are as follows

Debt ratio: It is also called as the solvency ratio which can be measured as the company's

total assets as the percentage of the total assets. It shows the company ability to pay

liabilities with the help of their total liabilities. When the organisation have large liabilities

7

0

0.05

0.1

0.15

0.2

0.25

0.3

Quick ratio

Illustration 5: Quick ratio of Harvey Homes Plc

The ideal quick ratio should be 1: 1 that state that company is capable to pay their

liabilities from their quick assets. But in case of the Harvey Homes Plc, they are below the

level of the ideal ratio. In 2015 the quick ratio of the organisation is 0.26: 1 where it states

that they are not in a condition to pay their liabilities which is bad sign for the firm as well as

it have been reduced from 2015 to 2016 and decreased up to 0.17: 1. This analysis state that

the venture assets is reducing and they are not at the stable position.

Financial leverage ratio

This ratio serves as the induction of the long-term solvency of the organisation. As

the liquid ratio is concerned with the short run liabilities and assets whereas the leverage

ratio is connected with the long-term debt. It includes various ratio that are as follows

Debt ratio: It is also called as the solvency ratio which can be measured as the company's

total assets as the percentage of the total assets. It shows the company ability to pay

liabilities with the help of their total liabilities. When the organisation have large liabilities

7

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

over their assets that states that the company is at risk stage, it is calculated as the total debt/

total liabilities (Arnold, 2013).

Debt ratio of the Harvey Homes Plc

2015

1,644/795= 2.06: 1

2016

2046 /1,029= 1.98: 1

1 2

1.94

1.96

1.98

2

2.02

2.04

2.06

2.08

Debt ratio

Illustration 6: Debt ratio of the Harvey Homes Plc

For any organisation, the debt ratio should be 2: 1 which state that the company is at

the stable stage to pay their total liabilities from their assets. If the company have 2: 1 ratio

for the debt, then they have double assets to pay their single liabilities. In the case of the

Harvey Homes Plc in 2015 the ratio was 2.06: 1 so that ratio communicate that the company

is able to pay their liabilities with their assets and in the year 2016 the ratio was 1.98: 1

which has been decreases. In 2016 the assets have been increases from 1,644 to 2046 which

is good sign for the company but with that the liabilities are also increasing from 795 to

8

total liabilities (Arnold, 2013).

Debt ratio of the Harvey Homes Plc

2015

1,644/795= 2.06: 1

2016

2046 /1,029= 1.98: 1

1 2

1.94

1.96

1.98

2

2.02

2.04

2.06

2.08

Debt ratio

Illustration 6: Debt ratio of the Harvey Homes Plc

For any organisation, the debt ratio should be 2: 1 which state that the company is at

the stable stage to pay their total liabilities from their assets. If the company have 2: 1 ratio

for the debt, then they have double assets to pay their single liabilities. In the case of the

Harvey Homes Plc in 2015 the ratio was 2.06: 1 so that ratio communicate that the company

is able to pay their liabilities with their assets and in the year 2016 the ratio was 1.98: 1

which has been decreases. In 2016 the assets have been increases from 1,644 to 2046 which

is good sign for the company but with that the liabilities are also increasing from 795 to

8

1,029. So, they need to make that organisation such sound that the can able to increase their

assets so that they can able to pay increasing liabilities.

Analysis of cash flow statement

Cash flow from operating activities

Cash flow from investing activities

Cash flow from financing activities

-50

0

50

100

150

200

Cash flows

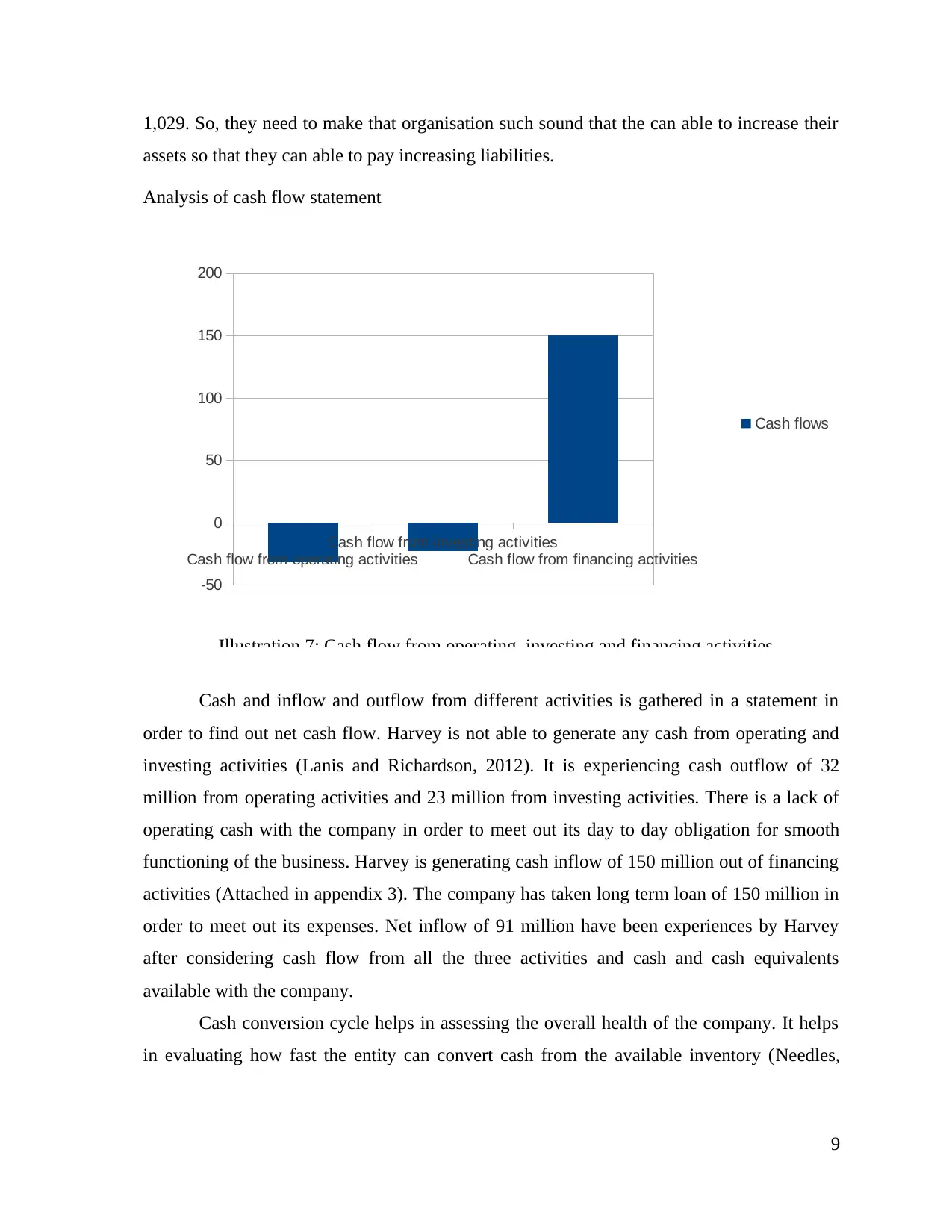

Illustration 7: Cash flow from operating, investing and financing activities

Cash and inflow and outflow from different activities is gathered in a statement in

order to find out net cash flow. Harvey is not able to generate any cash from operating and

investing activities (Lanis and Richardson, 2012). It is experiencing cash outflow of 32

million from operating activities and 23 million from investing activities. There is a lack of

operating cash with the company in order to meet out its day to day obligation for smooth

functioning of the business. Harvey is generating cash inflow of 150 million out of financing

activities (Attached in appendix 3). The company has taken long term loan of 150 million in

order to meet out its expenses. Net inflow of 91 million have been experiences by Harvey

after considering cash flow from all the three activities and cash and cash equivalents

available with the company.

Cash conversion cycle helps in assessing the overall health of the company. It helps

in evaluating how fast the entity can convert cash from the available inventory (Needles,

9

assets so that they can able to pay increasing liabilities.

Analysis of cash flow statement

Cash flow from operating activities

Cash flow from investing activities

Cash flow from financing activities

-50

0

50

100

150

200

Cash flows

Illustration 7: Cash flow from operating, investing and financing activities

Cash and inflow and outflow from different activities is gathered in a statement in

order to find out net cash flow. Harvey is not able to generate any cash from operating and

investing activities (Lanis and Richardson, 2012). It is experiencing cash outflow of 32

million from operating activities and 23 million from investing activities. There is a lack of

operating cash with the company in order to meet out its day to day obligation for smooth

functioning of the business. Harvey is generating cash inflow of 150 million out of financing

activities (Attached in appendix 3). The company has taken long term loan of 150 million in

order to meet out its expenses. Net inflow of 91 million have been experiences by Harvey

after considering cash flow from all the three activities and cash and cash equivalents

available with the company.

Cash conversion cycle helps in assessing the overall health of the company. It helps

in evaluating how fast the entity can convert cash from the available inventory (Needles,

9

Powers and Crosson, 2013). The formula used to calculate cash conversion cycle is as

follows:

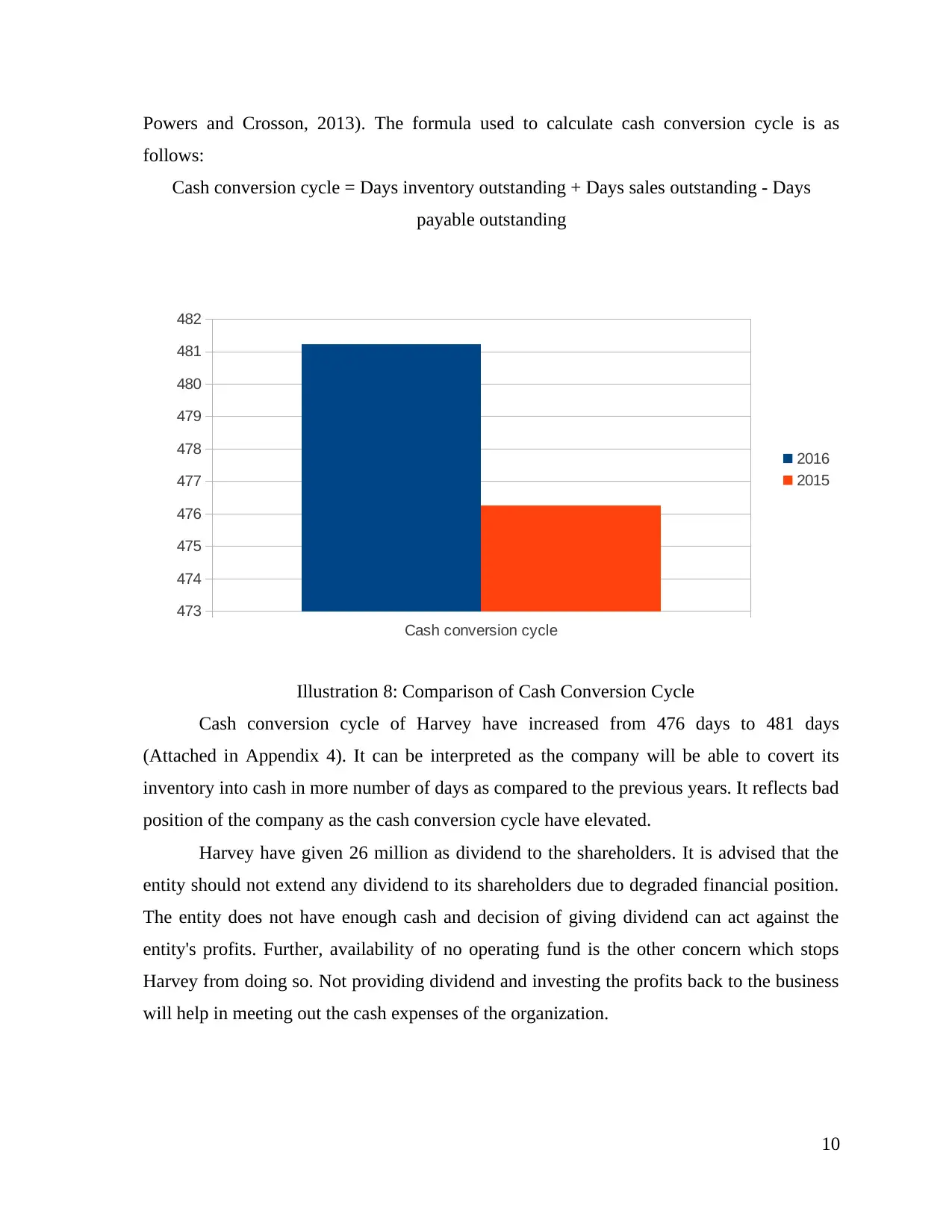

Cash conversion cycle = Days inventory outstanding + Days sales outstanding - Days

payable outstanding

Cash conversion cycle

473

474

475

476

477

478

479

480

481

482

2016

2015

Illustration 8: Comparison of Cash Conversion Cycle

Cash conversion cycle of Harvey have increased from 476 days to 481 days

(Attached in Appendix 4). It can be interpreted as the company will be able to covert its

inventory into cash in more number of days as compared to the previous years. It reflects bad

position of the company as the cash conversion cycle have elevated.

Harvey have given 26 million as dividend to the shareholders. It is advised that the

entity should not extend any dividend to its shareholders due to degraded financial position.

The entity does not have enough cash and decision of giving dividend can act against the

entity's profits. Further, availability of no operating fund is the other concern which stops

Harvey from doing so. Not providing dividend and investing the profits back to the business

will help in meeting out the cash expenses of the organization.

10

follows:

Cash conversion cycle = Days inventory outstanding + Days sales outstanding - Days

payable outstanding

Cash conversion cycle

473

474

475

476

477

478

479

480

481

482

2016

2015

Illustration 8: Comparison of Cash Conversion Cycle

Cash conversion cycle of Harvey have increased from 476 days to 481 days

(Attached in Appendix 4). It can be interpreted as the company will be able to covert its

inventory into cash in more number of days as compared to the previous years. It reflects bad

position of the company as the cash conversion cycle have elevated.

Harvey have given 26 million as dividend to the shareholders. It is advised that the

entity should not extend any dividend to its shareholders due to degraded financial position.

The entity does not have enough cash and decision of giving dividend can act against the

entity's profits. Further, availability of no operating fund is the other concern which stops

Harvey from doing so. Not providing dividend and investing the profits back to the business

will help in meeting out the cash expenses of the organization.

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

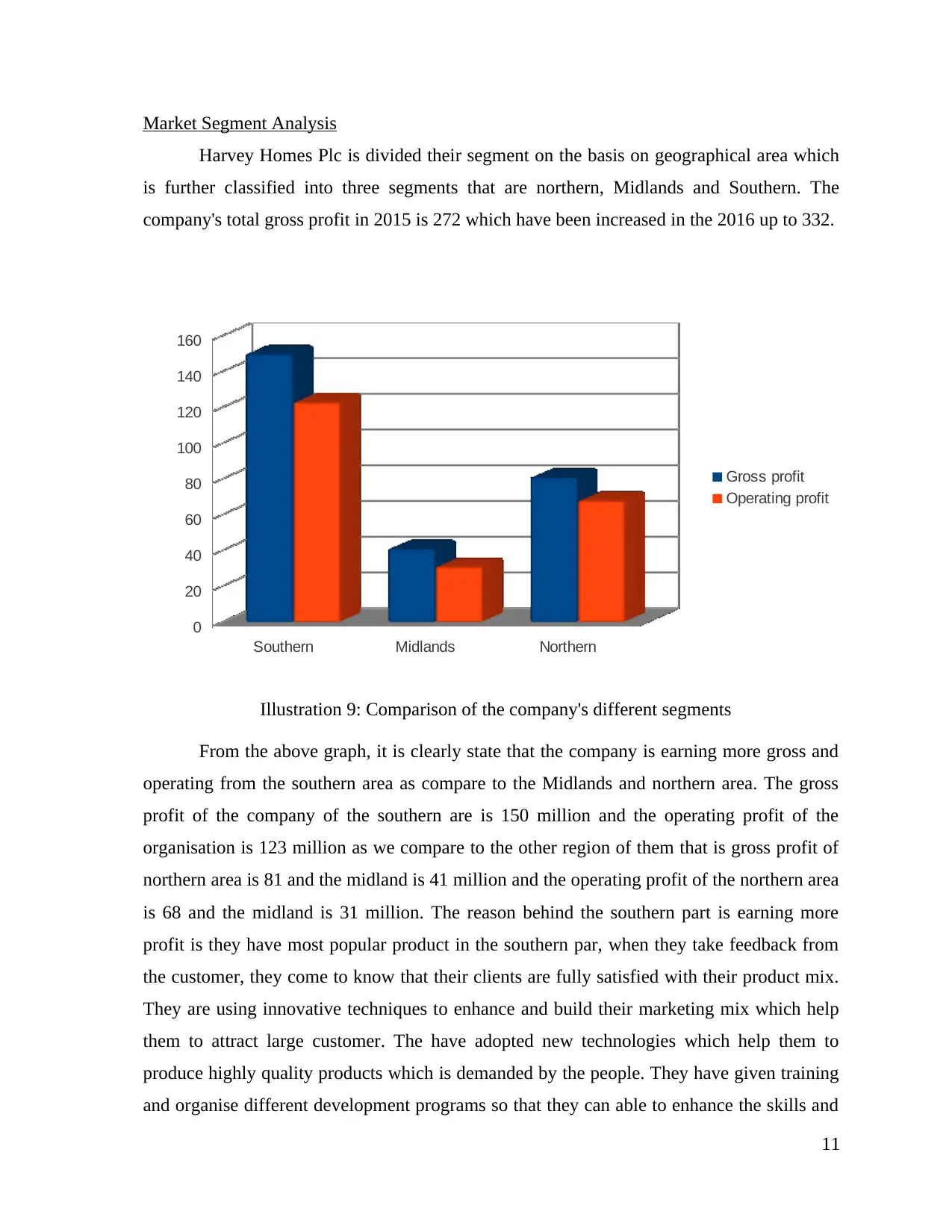

Market Segment Analysis

Harvey Homes Plc is divided their segment on the basis on geographical area which

is further classified into three segments that are northern, Midlands and Southern. The

company's total gross profit in 2015 is 272 which have been increased in the 2016 up to 332.

Southern Midlands Northern

0

20

40

60

80

100

120

140

160

Gross profit

Operating profit

Illustration 9: Comparison of the company's different segments

From the above graph, it is clearly state that the company is earning more gross and

operating from the southern area as compare to the Midlands and northern area. The gross

profit of the company of the southern are is 150 million and the operating profit of the

organisation is 123 million as we compare to the other region of them that is gross profit of

northern area is 81 and the midland is 41 million and the operating profit of the northern area

is 68 and the midland is 31 million. The reason behind the southern part is earning more

profit is they have most popular product in the southern par, when they take feedback from

the customer, they come to know that their clients are fully satisfied with their product mix.

They are using innovative techniques to enhance and build their marketing mix which help

them to attract large customer. The have adopted new technologies which help them to

produce highly quality products which is demanded by the people. They have given training

and organise different development programs so that they can able to enhance the skills and

11

Harvey Homes Plc is divided their segment on the basis on geographical area which

is further classified into three segments that are northern, Midlands and Southern. The

company's total gross profit in 2015 is 272 which have been increased in the 2016 up to 332.

Southern Midlands Northern

0

20

40

60

80

100

120

140

160

Gross profit

Operating profit

Illustration 9: Comparison of the company's different segments

From the above graph, it is clearly state that the company is earning more gross and

operating from the southern area as compare to the Midlands and northern area. The gross

profit of the company of the southern are is 150 million and the operating profit of the

organisation is 123 million as we compare to the other region of them that is gross profit of

northern area is 81 and the midland is 41 million and the operating profit of the northern area

is 68 and the midland is 31 million. The reason behind the southern part is earning more

profit is they have most popular product in the southern par, when they take feedback from

the customer, they come to know that their clients are fully satisfied with their product mix.

They are using innovative techniques to enhance and build their marketing mix which help

them to attract large customer. The have adopted new technologies which help them to

produce highly quality products which is demanded by the people. They have given training

and organise different development programs so that they can able to enhance the skills and

11

knowledge of the employee which helps them to fulfil the customer orders on time and serve

best experience than their competitors. The organisation should also adopt these all

techniques in all the areas so that they can improve their profits in all the areas.

PART 2: INVESTMENT APPRAISAL

Management forecast

Harvey Homes Plc is planning to acquire Midlands Market at an investment £500

million. Firm’s managers had presented a 5-year forecast. In the first year, revenue has been

projected to £300m which is expected to grow up to £360m (+20%), £432m (+20%), £518m

(+19.91%) and £648m (+25.10%) respectively. The forecasts looked achievable because as

managers decided to offer high- quality apartments and houses made through the use of

latest construction techniques will maximize overall market demand. Besides this, inflation

will lead to increase prices and maximize revenues. However, on the other side, due to

inflation, material prices will also be increase as a result, variable cost projection shows an

expected growth from £222m to £266m (+19.82%), £320m (+20.30%), £389m (+21.56%)

and £486m (+24.94%) respectively. The forecasts clearly present that executives have

considered several market components i.e. possible fluctuations in demand, offering prices,

technological advancement and cost volatility also, still, in the current era, sudden changes in

both the micro and macro business environment are the possible risks which can challenge

managerial forecasts. For instance, shortage of material can lead to high prices above

assumptions, competitors’ actions can also influence the market demand and affect the

quality of forecasts.

Techniques of investment appraisal

Payback period

Payback period provides useful information to the investor that what time a project is

expected to take to recover its initial outlay. The Midland project expected to take lengthy

period of 4.5 year just before 6 months to the completion of estimated life. The reasons is

initially, although the net cash flow demonstrates growing trend but at decreasing YOY

percetage growth as it got increased from £78m to £94m (+20.51%), £112m (+19.15%) and

129m (+15.18%) whilst finally it depicted an impressive growth of 25.58% to £162m. No-

doubt, the method helps investor in undertaking investment in project with lower PP, still,

12

best experience than their competitors. The organisation should also adopt these all

techniques in all the areas so that they can improve their profits in all the areas.

PART 2: INVESTMENT APPRAISAL

Management forecast

Harvey Homes Plc is planning to acquire Midlands Market at an investment £500

million. Firm’s managers had presented a 5-year forecast. In the first year, revenue has been

projected to £300m which is expected to grow up to £360m (+20%), £432m (+20%), £518m

(+19.91%) and £648m (+25.10%) respectively. The forecasts looked achievable because as

managers decided to offer high- quality apartments and houses made through the use of

latest construction techniques will maximize overall market demand. Besides this, inflation

will lead to increase prices and maximize revenues. However, on the other side, due to

inflation, material prices will also be increase as a result, variable cost projection shows an

expected growth from £222m to £266m (+19.82%), £320m (+20.30%), £389m (+21.56%)

and £486m (+24.94%) respectively. The forecasts clearly present that executives have

considered several market components i.e. possible fluctuations in demand, offering prices,

technological advancement and cost volatility also, still, in the current era, sudden changes in

both the micro and macro business environment are the possible risks which can challenge

managerial forecasts. For instance, shortage of material can lead to high prices above

assumptions, competitors’ actions can also influence the market demand and affect the

quality of forecasts.

Techniques of investment appraisal

Payback period

Payback period provides useful information to the investor that what time a project is

expected to take to recover its initial outlay. The Midland project expected to take lengthy

period of 4.5 year just before 6 months to the completion of estimated life. The reasons is

initially, although the net cash flow demonstrates growing trend but at decreasing YOY

percetage growth as it got increased from £78m to £94m (+20.51%), £112m (+19.15%) and

129m (+15.18%) whilst finally it depicted an impressive growth of 25.58% to £162m. No-

doubt, the method helps investor in undertaking investment in project with lower PP, still,

12

many academics & professionals criticized the method just because of its failure to not give

value to the currency’s time value (Avery, Flaherty, and Rhee, 2011). Besides this, another

criticism of the technique is that it also avoids cash flow that occurred after the recovery of

beginning investment. In contrast, some studies favour the method because it is very easy

way to determine the time length of recovery of initial cost to manage investment risk.

Accounting/Average rate of return (ARR)

ARR method is based on conventional accounting because it uses accrual concepts to

examine investment project worthiness. The method provides an idea that what percentage

of return does Harvey Homes Plc can collect on their capital invested. The acquisition of

Midland is expected to generate an annual return of 6% that exceeded the standard criteria

decided by the manager of 5% that encourage managers to accept the project. Undoubtedly,

it is a good way to examine the investment project considering return; still, the main

drawback is that it does not consider timing and also the cash flow variations (Echanis and

Kester, 2016). It considers profits after deducting depreciation which does not result in

actual cash outflow, thus, mislead investors. Considering its shortcoming, it is better to reach

to any decisions taking into account ARR only.

Net present value

NPV is widely used technique in the field of investment appraisal for the successful

financial decisions because it accounted for time value of currency using current rate of

interest at which Midland acquisition project is financed. For the given scenario, at 3% cost

of capital, NPV is determined to £22m at profitability Index of 4% that exceeded the

standard criteria of 3.5% set by the managers. As the method considers risk therefore, it is

considered really suitable and appropriate technique of capital budgeting and suggests

Harvey Homes to undertake investment of the current project. In contrast, academicians

contended that using a same rate for overall project life is not justifiable (Shibata and

Nishihara, 2015). Besides this, change in interest rate also affects the NPV outcome because

high rate results in less NPV or vice-versa which the method does not accounted. In addition,

at the global level, FOREX rate, corporation tax rate also has an influence over the result.

Although, the method has several drawbacks, still, among all the above techniques, it is

highly suitable; therefore, it is better to recommend the firm to invest required capital to

acquire Midland division so as to gain favourable return (Li and Trutnevyte, 2017).

13

value to the currency’s time value (Avery, Flaherty, and Rhee, 2011). Besides this, another

criticism of the technique is that it also avoids cash flow that occurred after the recovery of

beginning investment. In contrast, some studies favour the method because it is very easy

way to determine the time length of recovery of initial cost to manage investment risk.

Accounting/Average rate of return (ARR)

ARR method is based on conventional accounting because it uses accrual concepts to

examine investment project worthiness. The method provides an idea that what percentage

of return does Harvey Homes Plc can collect on their capital invested. The acquisition of

Midland is expected to generate an annual return of 6% that exceeded the standard criteria

decided by the manager of 5% that encourage managers to accept the project. Undoubtedly,

it is a good way to examine the investment project considering return; still, the main

drawback is that it does not consider timing and also the cash flow variations (Echanis and

Kester, 2016). It considers profits after deducting depreciation which does not result in

actual cash outflow, thus, mislead investors. Considering its shortcoming, it is better to reach

to any decisions taking into account ARR only.

Net present value

NPV is widely used technique in the field of investment appraisal for the successful

financial decisions because it accounted for time value of currency using current rate of

interest at which Midland acquisition project is financed. For the given scenario, at 3% cost

of capital, NPV is determined to £22m at profitability Index of 4% that exceeded the

standard criteria of 3.5% set by the managers. As the method considers risk therefore, it is

considered really suitable and appropriate technique of capital budgeting and suggests

Harvey Homes to undertake investment of the current project. In contrast, academicians

contended that using a same rate for overall project life is not justifiable (Shibata and

Nishihara, 2015). Besides this, change in interest rate also affects the NPV outcome because

high rate results in less NPV or vice-versa which the method does not accounted. In addition,

at the global level, FOREX rate, corporation tax rate also has an influence over the result.

Although, the method has several drawbacks, still, among all the above techniques, it is

highly suitable; therefore, it is better to recommend the firm to invest required capital to

acquire Midland division so as to gain favourable return (Li and Trutnevyte, 2017).

13

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Finance sources

Scenario presented that firm is looking for an additional investment in the France

which requires an initial outlay of £400m, hence, company requires sufficient amount of

capital to finance the project. There are following sources available through which, capital

can be gathered, enumerated hereunder:

Share issue: Firm can decide to go to public by issuing equity shares and collect

capital from the public subscription for acquiring stake in the company. No mandatory

obligation to pay a fixed rate of dividend at specified time is the key advantage of this

method, still, considering actual corporate world, it seems essential to distribute some

proportion of return as dividend to encourage investors to hold their equity or buy also (Sabri

and et.al., 2015). However, in contrast, absence of tax shields & transfer of stake are the

downfall sides of share issue.

Bank borrowings: In every nation, financial institutions provide monetary assistance

in the way of giving loan to the required party. Harvey Homes Plc can apply for bank loan

and in return, as per the schedule of payment, it will have to pay timely instalments inclusive

of interest. Although, business has to manage funds for the repayment, still, they can get tax

deductions to the amount of interest paid to the lender. In despite of this, business control is

not diverted to the debt providers and they have no voting power to participate in board

decisions (Peirson and et.al., 2014).

Retained earnings: Every business does not distribute all of its earning among

shareholders as dividend and keep some proportion in their hand so as to finance future

projects. Harvey Homes Plc can utilize its cumulative return of previous years and invest it

for undertaking investment in France without any financial and legal obligation.

Considering all the above sources, it is better to suggest the firm to incorporate a

mixture of all these financial sources to finance its new project. Debt must be used for

getting tax benefits whereas equity is suggested to use because of absence of mandatory

dividend payment and retained earning has no obligation. Firm must combine these financial

sources in a debt to equity ratio of 0.50:1 to manage risk appropriately.

14

Scenario presented that firm is looking for an additional investment in the France

which requires an initial outlay of £400m, hence, company requires sufficient amount of

capital to finance the project. There are following sources available through which, capital

can be gathered, enumerated hereunder:

Share issue: Firm can decide to go to public by issuing equity shares and collect

capital from the public subscription for acquiring stake in the company. No mandatory

obligation to pay a fixed rate of dividend at specified time is the key advantage of this

method, still, considering actual corporate world, it seems essential to distribute some

proportion of return as dividend to encourage investors to hold their equity or buy also (Sabri

and et.al., 2015). However, in contrast, absence of tax shields & transfer of stake are the

downfall sides of share issue.

Bank borrowings: In every nation, financial institutions provide monetary assistance

in the way of giving loan to the required party. Harvey Homes Plc can apply for bank loan

and in return, as per the schedule of payment, it will have to pay timely instalments inclusive

of interest. Although, business has to manage funds for the repayment, still, they can get tax

deductions to the amount of interest paid to the lender. In despite of this, business control is

not diverted to the debt providers and they have no voting power to participate in board

decisions (Peirson and et.al., 2014).

Retained earnings: Every business does not distribute all of its earning among

shareholders as dividend and keep some proportion in their hand so as to finance future

projects. Harvey Homes Plc can utilize its cumulative return of previous years and invest it

for undertaking investment in France without any financial and legal obligation.

Considering all the above sources, it is better to suggest the firm to incorporate a

mixture of all these financial sources to finance its new project. Debt must be used for

getting tax benefits whereas equity is suggested to use because of absence of mandatory

dividend payment and retained earning has no obligation. Firm must combine these financial

sources in a debt to equity ratio of 0.50:1 to manage risk appropriately.

14

Non-financial factors

Respective Directors

Harvey Homes Plc

10th August 2017

Subject: Qualitative factors in capital budgeting decisions

Investment appraisal techniques only help for the quantitative analysis, whereas, in the

corporate field, there are multitudes of qualitative components which must be looked before

undertaking a capital investment. For the France project, Harvey Homes Plc must examine

legislations and regulative framework prevailing in the country for delivering quality apartment

and homes to the public. Besides this, currently, people are demanding homes made with

modernised technologies with unique infrastructure, therefore, technical availability also must be

examined before undertaking investment in France (Non-Financial Factors for Investment

Appraisal, 2012). In addition, experienced & competent workforce availability must be looked to

carry out regular functions and competitors’ actions, product quality and technologies used

should be examined for running successful operations.

15

Respective Directors

Harvey Homes Plc

10th August 2017

Subject: Qualitative factors in capital budgeting decisions

Investment appraisal techniques only help for the quantitative analysis, whereas, in the

corporate field, there are multitudes of qualitative components which must be looked before

undertaking a capital investment. For the France project, Harvey Homes Plc must examine

legislations and regulative framework prevailing in the country for delivering quality apartment

and homes to the public. Besides this, currently, people are demanding homes made with

modernised technologies with unique infrastructure, therefore, technical availability also must be

examined before undertaking investment in France (Non-Financial Factors for Investment

Appraisal, 2012). In addition, experienced & competent workforce availability must be looked to

carry out regular functions and competitors’ actions, product quality and technologies used

should be examined for running successful operations.

15

REFERENCES

Books and Journal

Allen, E. J., Larson, C. R. and Sloan, R. G., 2013. Accrual reversals, earnings and stock

returns. Journal of Accounting and Economics. 56(1). pp.113-129.

Arnold, G., 2013. Corporate financial management. Pearson Higher Ed.

Caglayan, M. and Demir, F., 2014. Firm productivity, exchange rate movements, sources of

finance, and export orientation. World Development. 54. pp.204-219.

Lanis, R. and Richardson, G., 2012. Corporate social responsibility and tax aggressiveness: An

empirical analysis. Journal of Accounting and Public Policy. 31(1). pp.86-108.

Needles, B. E., Powers, M. and Crosson, S. V., 2013. Principles of accounting. Cengage

Learning.

Weygandt, J. J., Kimmel, P. D. and Kieso, D. E., 2015. Financial & Managerial Accounting.

John Wiley & Sons.

Peirson, G. and et.al., 2014. Business finance. McGraw-Hill Education Australia.

Shibata, T. and Nishihara, M., 2015. Investment timing, debt structure, and financing

constraints. European Journal of Operational Research. 241(2). pp. 513-526.

Sabri, M. F. and et.al., 2015. Financial literacy, financial Management practices, and retirement

confidence among Women working in government Agencies: A mediation model. The

Journal of Developing Areas. 49(6). pp. 405-412.

Echanis, E. S. and Kester, G. W., 2016. Capital Budgeting Practices of Listed Philippine

Firms. Philippine Management Review. 7(1). pp. 16-28.

AVERY, A.E., FLAHERTY, S.M.V. and RHEE, M., 2011. Fortifying the Payback Period

Method for Alternative Cash Flow Patterns. Journal of Financial and Economic

Practice. 11(2). pp. 1-9.

Li, F. G. and Trutnevyte, E., 2017. Investment appraisal of cost-optimal and near-optimal

pathways for the UK electricity sector transition to 2050. Applied Energy. 189. pp.89-109.

Online

16

Books and Journal

Allen, E. J., Larson, C. R. and Sloan, R. G., 2013. Accrual reversals, earnings and stock

returns. Journal of Accounting and Economics. 56(1). pp.113-129.

Arnold, G., 2013. Corporate financial management. Pearson Higher Ed.

Caglayan, M. and Demir, F., 2014. Firm productivity, exchange rate movements, sources of

finance, and export orientation. World Development. 54. pp.204-219.

Lanis, R. and Richardson, G., 2012. Corporate social responsibility and tax aggressiveness: An

empirical analysis. Journal of Accounting and Public Policy. 31(1). pp.86-108.

Needles, B. E., Powers, M. and Crosson, S. V., 2013. Principles of accounting. Cengage

Learning.

Weygandt, J. J., Kimmel, P. D. and Kieso, D. E., 2015. Financial & Managerial Accounting.

John Wiley & Sons.

Peirson, G. and et.al., 2014. Business finance. McGraw-Hill Education Australia.

Shibata, T. and Nishihara, M., 2015. Investment timing, debt structure, and financing

constraints. European Journal of Operational Research. 241(2). pp. 513-526.

Sabri, M. F. and et.al., 2015. Financial literacy, financial Management practices, and retirement

confidence among Women working in government Agencies: A mediation model. The

Journal of Developing Areas. 49(6). pp. 405-412.

Echanis, E. S. and Kester, G. W., 2016. Capital Budgeting Practices of Listed Philippine

Firms. Philippine Management Review. 7(1). pp. 16-28.

AVERY, A.E., FLAHERTY, S.M.V. and RHEE, M., 2011. Fortifying the Payback Period

Method for Alternative Cash Flow Patterns. Journal of Financial and Economic

Practice. 11(2). pp. 1-9.

Li, F. G. and Trutnevyte, E., 2017. Investment appraisal of cost-optimal and near-optimal

pathways for the UK electricity sector transition to 2050. Applied Energy. 189. pp.89-109.

Online

16

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Non-Financial Factors for Investment Appraisal. 2012. [Online]. Available through: <

https://www.nibusinessinfo.co.uk/content/non-financial-factors-investment-appraisal>.

[Accessed on 10th August 2017].

17

https://www.nibusinessinfo.co.uk/content/non-financial-factors-investment-appraisal>.

[Accessed on 10th August 2017].

17

APPENDIX

Appendix 1:

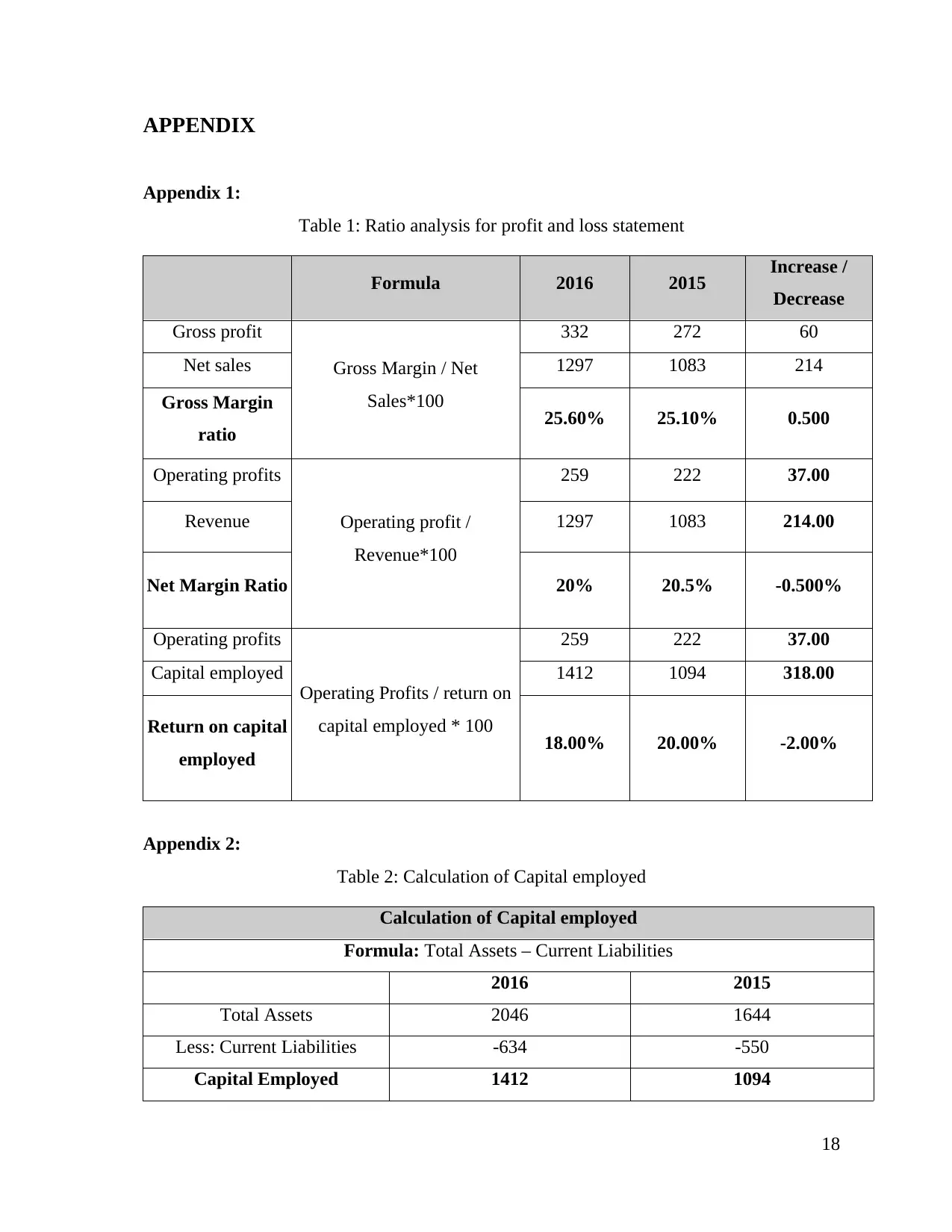

Table 1: Ratio analysis for profit and loss statement

Formula 2016 2015 Increase /

Decrease

Gross profit

Gross Margin / Net

Sales*100

332 272 60

Net sales 1297 1083 214

Gross Margin

ratio 25.60% 25.10% 0.500

Operating profits

Operating profit /

Revenue*100

259 222 37.00

Revenue 1297 1083 214.00

Net Margin Ratio 20% 20.5% -0.500%

Operating profits

Operating Profits / return on

capital employed * 100

259 222 37.00

Capital employed 1412 1094 318.00

Return on capital

employed 18.00% 20.00% -2.00%

Appendix 2:

Table 2: Calculation of Capital employed

Calculation of Capital employed

Formula: Total Assets – Current Liabilities

2016 2015

Total Assets 2046 1644

Less: Current Liabilities -634 -550

Capital Employed 1412 1094

18

Appendix 1:

Table 1: Ratio analysis for profit and loss statement

Formula 2016 2015 Increase /

Decrease

Gross profit

Gross Margin / Net

Sales*100

332 272 60

Net sales 1297 1083 214

Gross Margin

ratio 25.60% 25.10% 0.500

Operating profits

Operating profit /

Revenue*100

259 222 37.00

Revenue 1297 1083 214.00

Net Margin Ratio 20% 20.5% -0.500%

Operating profits

Operating Profits / return on

capital employed * 100

259 222 37.00

Capital employed 1412 1094 318.00

Return on capital

employed 18.00% 20.00% -2.00%

Appendix 2:

Table 2: Calculation of Capital employed

Calculation of Capital employed

Formula: Total Assets – Current Liabilities

2016 2015

Total Assets 2046 1644

Less: Current Liabilities -634 -550

Capital Employed 1412 1094

18

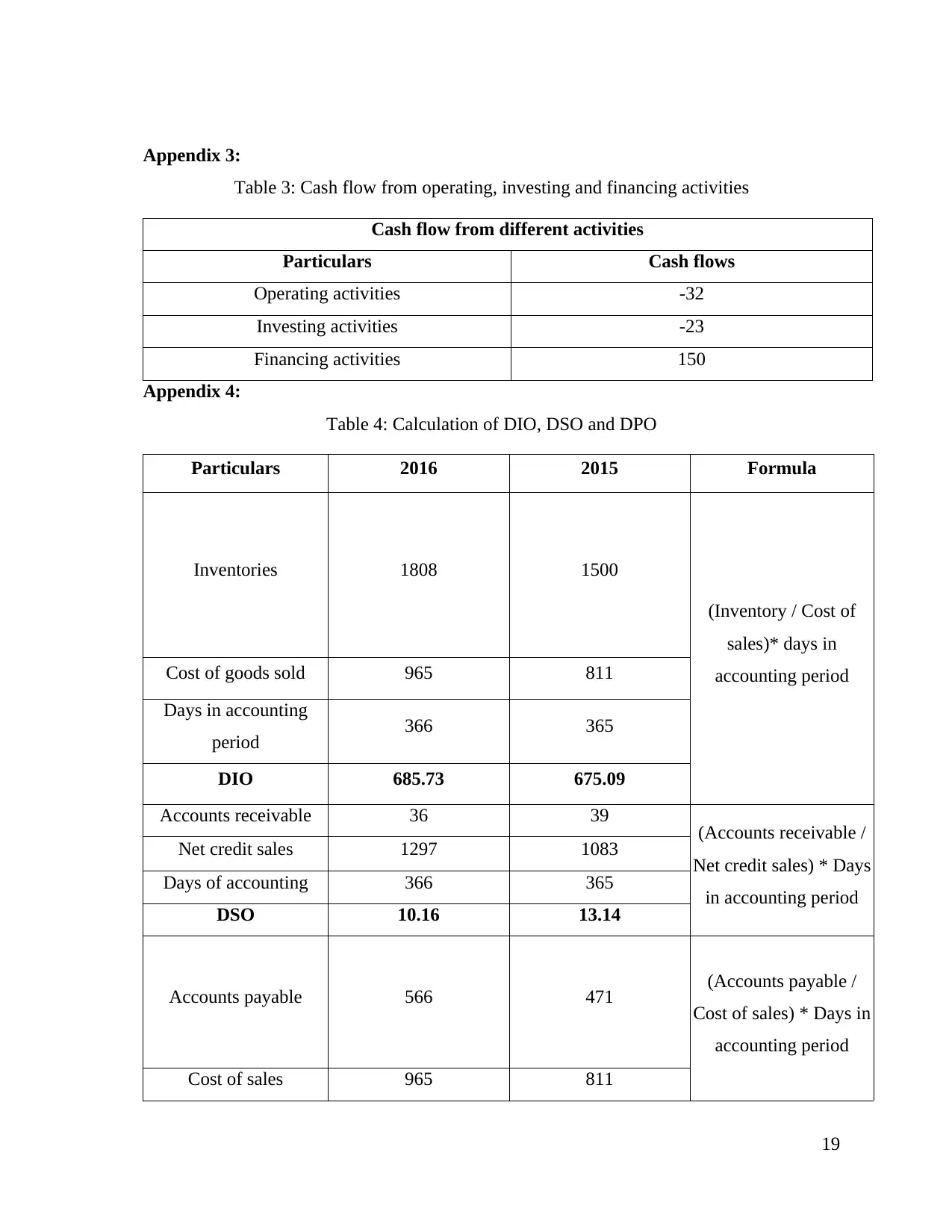

Appendix 3:

Table 3: Cash flow from operating, investing and financing activities

Cash flow from different activities

Particulars Cash flows

Operating activities -32

Investing activities -23

Financing activities 150

Appendix 4:

Table 4: Calculation of DIO, DSO and DPO

Particulars 2016 2015 Formula

Inventories 1808 1500

(Inventory / Cost of

sales)* days in

accounting periodCost of goods sold 965 811

Days in accounting

period 366 365

DIO 685.73 675.09

Accounts receivable 36 39 (Accounts receivable /

Net credit sales) * Days

in accounting period

Net credit sales 1297 1083

Days of accounting 366 365

DSO 10.16 13.14

Accounts payable 566 471 (Accounts payable /

Cost of sales) * Days in

accounting period

Cost of sales 965 811

19

Table 3: Cash flow from operating, investing and financing activities

Cash flow from different activities

Particulars Cash flows

Operating activities -32

Investing activities -23

Financing activities 150

Appendix 4:

Table 4: Calculation of DIO, DSO and DPO

Particulars 2016 2015 Formula

Inventories 1808 1500

(Inventory / Cost of

sales)* days in

accounting periodCost of goods sold 965 811

Days in accounting

period 366 365

DIO 685.73 675.09

Accounts receivable 36 39 (Accounts receivable /

Net credit sales) * Days

in accounting period

Net credit sales 1297 1083

Days of accounting 366 365

DSO 10.16 13.14

Accounts payable 566 471 (Accounts payable /

Cost of sales) * Days in

accounting period

Cost of sales 965 811

19

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

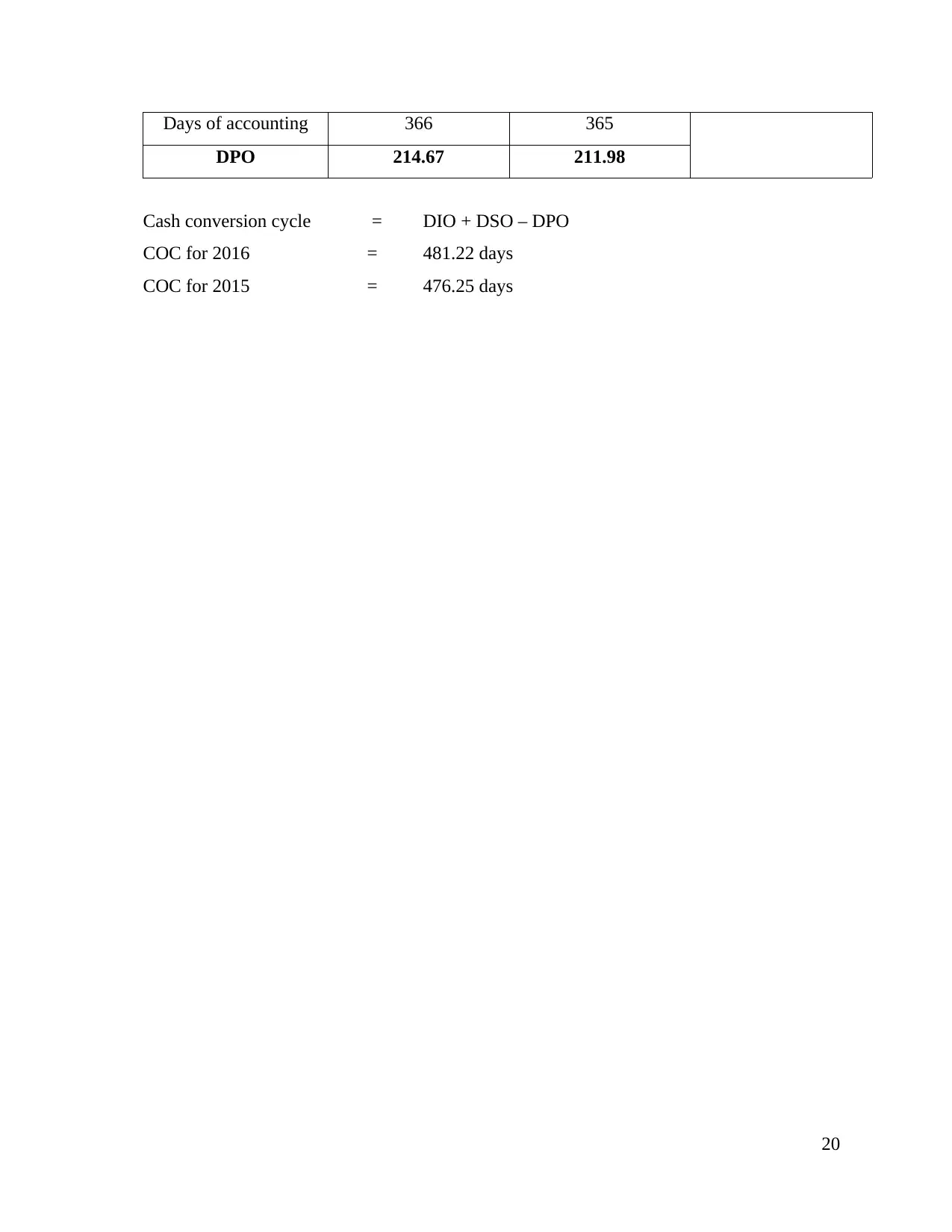

Days of accounting 366 365

DPO 214.67 211.98

Cash conversion cycle = DIO + DSO – DPO

COC for 2016 = 481.22 days

COC for 2015 = 476.25 days

20

DPO 214.67 211.98

Cash conversion cycle = DIO + DSO – DPO

COC for 2016 = 481.22 days

COC for 2015 = 476.25 days

20

1 out of 23

Related Documents

![[PDF] Harvey Company Financial Analysis](/_next/image/?url=https%3A%2F%2Fdesklib.com%2Fmedia%2Fimages%2Fvy%2F7c46e52b2ed44dc28c4d7f598dd6c910.jpg&w=256&q=75)

![[FULL ACCESS] Financial Analysis and Market Segmentation](/_next/image/?url=https%3A%2F%2Fdesklib.com%2Fmedia%2Fimages%2Fqf%2Fca1b2367267248f99b66462acf21e250.jpg&w=256&q=75)

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.