Financial Decision Making: Importance of Accounting and Finance Functions in SKANSKA Plc

VerifiedAdded on 2023/06/17

|13

|3924

|451

AI Summary

This report discusses the importance of accounting and finance functions in SKANSKA Plc and evaluates their duties and roles. It also covers the calculation of financial ratios and analyzes the performance of the company.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

FINANCIAL DECISION

MAKING

MAKING

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

Implication of management accounting techniques within SKANSKA Plc for decision making

.....................................................................................................................................................3

Critical evaluation of significance of Accounting and finance function.....................................4

Significance of accounting and finance functions......................................................................4

Duties of accounting & finance within SKANSKA PLC...........................................................6

Roles of Accounting & finance within SKANSKA PLC...........................................................6

TASK 2............................................................................................................................................7

Calculation of financial ratios.....................................................................................................7

Comment on the performance of SKANSKA Plc mentioning possible causes, reasons and

effects for change........................................................................................................................8

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................12

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

Implication of management accounting techniques within SKANSKA Plc for decision making

.....................................................................................................................................................3

Critical evaluation of significance of Accounting and finance function.....................................4

Significance of accounting and finance functions......................................................................4

Duties of accounting & finance within SKANSKA PLC...........................................................6

Roles of Accounting & finance within SKANSKA PLC...........................................................6

TASK 2............................................................................................................................................7

Calculation of financial ratios.....................................................................................................7

Comment on the performance of SKANSKA Plc mentioning possible causes, reasons and

effects for change........................................................................................................................8

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................12

INTRODUCTION

The financial decision-making is one of the crucial decisions made by the finance

manager of the company. The decision is about the financing mix of the organization. This report

is basically based on the SKANSKA Plc which contain two tasks. In the first task, the report will

discuss the importance of accounting and finance function. Further, the report will also critically

evaluate the importance of accounting and finance duties and roles in SKANSKA Plc using the

appropriate examples. In addition, the second task of the report will cover the calculation of

financial ratios of SKANSKA Plc using the financial statement of the company. In the

continuous, the report will interpretate and analyse the performance of the company on the basis

of the ratio results (Agbo and Nwankwo, 2018). Lastly, the report will state whether the investors

need to invest £1 million in the SKANSKA company or not.

TASK 1

Implication of management accounting techniques within SKANSKA Plc for decision making

The various management accounting techniques that is available to the company with the

help of which they can plan, control and make decision regarding business operations and

finance are as follows:

Variance analysis: This is a technique which state the difference or gap between the

actual and standard income and expenses. With the implication of this technique the

management of the SKANSKA Plc improve their budgets estimations for upcoming year.

For example, the company able to identify and manage the key areas which leads to more

gap (Akhtaruzzaman, Berg and Hajzler, 2017).

Break-even analysis: The break-even analysis of the products helps the company in

identifying the sales point whether they will neither earn profit nor they will incur any

loss. For example, with the implication of this technique, SKANSKA company able to

identify each product margin of safety and on this basis make decision regarding

continuation or dropping of that product line. This helps the company in maintaining its

profitability.

Investment appraisal technique: This is also known as capital budgeting technique

which helps the company in identifying the best and profitable projects out of the

The financial decision-making is one of the crucial decisions made by the finance

manager of the company. The decision is about the financing mix of the organization. This report

is basically based on the SKANSKA Plc which contain two tasks. In the first task, the report will

discuss the importance of accounting and finance function. Further, the report will also critically

evaluate the importance of accounting and finance duties and roles in SKANSKA Plc using the

appropriate examples. In addition, the second task of the report will cover the calculation of

financial ratios of SKANSKA Plc using the financial statement of the company. In the

continuous, the report will interpretate and analyse the performance of the company on the basis

of the ratio results (Agbo and Nwankwo, 2018). Lastly, the report will state whether the investors

need to invest £1 million in the SKANSKA company or not.

TASK 1

Implication of management accounting techniques within SKANSKA Plc for decision making

The various management accounting techniques that is available to the company with the

help of which they can plan, control and make decision regarding business operations and

finance are as follows:

Variance analysis: This is a technique which state the difference or gap between the

actual and standard income and expenses. With the implication of this technique the

management of the SKANSKA Plc improve their budgets estimations for upcoming year.

For example, the company able to identify and manage the key areas which leads to more

gap (Akhtaruzzaman, Berg and Hajzler, 2017).

Break-even analysis: The break-even analysis of the products helps the company in

identifying the sales point whether they will neither earn profit nor they will incur any

loss. For example, with the implication of this technique, SKANSKA company able to

identify each product margin of safety and on this basis make decision regarding

continuation or dropping of that product line. This helps the company in maintaining its

profitability.

Investment appraisal technique: This is also known as capital budgeting technique

which helps the company in identifying the best and profitable projects out of the

alternative projects. For example, if the SKANSKA Plc wants to invest its fund in the

projects than they can use Net Present Value method of appraisal to select one out of

many. The impact of which the company can achieve its higher returns objectives from

such investment appraisal (Anjum, 2021).

Critical evaluation of significance of Accounting and finance function

Both finance & accounting are of great importance while managing the any concern in order to

achieve financial goals and objectives of the business. In order to handle money with care, these

functions are necessary to be performed. It aids in effective management of business income and

expenses, assessing and controlling flow money, accordingly, directing business operations to

move towards the achievement of desired objectives (Kokina and Blanchette, 2019). The

accountant and financial manager or director are those who by performing these functions able to

frame financial strategy for the business, so that end goals and objectives can be met in the

desired manner and at the right time.

Accounting function is concerned with keeping accurate record of all the financial

transaction that took place during the course of a business and accordingly create journal, ledger

and trial balance, on the basis of which financial statements are prepared at the end of the period

which is required by the law and various internal and external parties to the business. In other

words, accounting function aims to communicate great sort of financial information to the

stakeholders, owners, managers and investors at large of the business which in turn helps these

parties of the business in making decision for the future related to their association with the

business (Brooks and Oikonomou, 2018). For instance, stakeholders utilises financial

information to assess the financial standing of the business to decide upon whether to continue

their association with the business or not. Investors specially needed such financial information

before making any new or additional investment in SKANSKA plc. to evaluate its financial

performance. It is the duty of the accounting or financial manager to ensure that whatever

information has been communicated is being understood by the concerned party in a required

manner. Therefore, accounting and financial information must be presented in a manner that

experts could get benefited out of it.

Significance of accounting and finance functions

Helps in the evaluation of business performance: The records generated by accounting function

reflects the outcome of business operations with the help of which financial position of the

projects than they can use Net Present Value method of appraisal to select one out of

many. The impact of which the company can achieve its higher returns objectives from

such investment appraisal (Anjum, 2021).

Critical evaluation of significance of Accounting and finance function

Both finance & accounting are of great importance while managing the any concern in order to

achieve financial goals and objectives of the business. In order to handle money with care, these

functions are necessary to be performed. It aids in effective management of business income and

expenses, assessing and controlling flow money, accordingly, directing business operations to

move towards the achievement of desired objectives (Kokina and Blanchette, 2019). The

accountant and financial manager or director are those who by performing these functions able to

frame financial strategy for the business, so that end goals and objectives can be met in the

desired manner and at the right time.

Accounting function is concerned with keeping accurate record of all the financial

transaction that took place during the course of a business and accordingly create journal, ledger

and trial balance, on the basis of which financial statements are prepared at the end of the period

which is required by the law and various internal and external parties to the business. In other

words, accounting function aims to communicate great sort of financial information to the

stakeholders, owners, managers and investors at large of the business which in turn helps these

parties of the business in making decision for the future related to their association with the

business (Brooks and Oikonomou, 2018). For instance, stakeholders utilises financial

information to assess the financial standing of the business to decide upon whether to continue

their association with the business or not. Investors specially needed such financial information

before making any new or additional investment in SKANSKA plc. to evaluate its financial

performance. It is the duty of the accounting or financial manager to ensure that whatever

information has been communicated is being understood by the concerned party in a required

manner. Therefore, accounting and financial information must be presented in a manner that

experts could get benefited out of it.

Significance of accounting and finance functions

Helps in the evaluation of business performance: The records generated by accounting function

reflects the outcome of business operations with the help of which financial position of the

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

business can be determined easily, so that understanding can be developed about what is going

on in the business in financial terms. Also, with the data available of various financial years can

be used for establishing comparison between current data & previous data in order to budget

future perspectives of the business appropriately along with determining the performance trends

of the business (Bebbington and Unerman, 2018). This accordingly helps in determining whether

the financial circumstances of the business has improved or worsened in comparison to previous

years.

Statutory compliance can be ensured: When appropriate processes and systems of accounting

are present, it is helpful in complying with the statutory requirements, so that various issues and

problems that could arise due to non – compliance can be avoided to a large extent. Also,

meeting liabilities of both short term and long term can be facilitated through maintaining

appropriate record of each accounts associated with SKANSKA plc. For example, if the

creditor’s payment is outstanding on particular day can be easily determined through creditor’s

ledger.

Preparation of budget and making future projections: Forecasting and budgeting both are

known as either maker or destroyer of the business and to accomplish these tasks of forecasting

and budgeting successfully, financial records play a vital role (Kornberger, Pflueger and

Mouritsen, 2017). Business trends can be identified through historical data and on the basis of

which various future projections are made by financial manager or director with the aims of

keeping up the business profitable. The utility and value of financial data gets enhanced when it

has been generated through an appropriate accounting processes.

Helps in making investment decisions: With the help of finance function, where to make

investment can be determined as this function provide useful insights of which investment will

generate how much liquidity or return and for how much time. Accordingly, allocation of capital

can be done towards long term assets in the most profitable manner.

Helps in making financing decisions: Such decisions are meant for identify the sources from

which funds needed business operations can be acquired. It also determines the time when the

funds will be needed along with the amount of funds required. How much proportion of debt and

equity should be included in the overall capital is the concern of this function as it affects the

firm’s value and shareholder’s wealth. Therefore, maximisation of shareholder’s wealth and

minimisation of business’s risks can be ensured through finance function. For example, whether

on in the business in financial terms. Also, with the data available of various financial years can

be used for establishing comparison between current data & previous data in order to budget

future perspectives of the business appropriately along with determining the performance trends

of the business (Bebbington and Unerman, 2018). This accordingly helps in determining whether

the financial circumstances of the business has improved or worsened in comparison to previous

years.

Statutory compliance can be ensured: When appropriate processes and systems of accounting

are present, it is helpful in complying with the statutory requirements, so that various issues and

problems that could arise due to non – compliance can be avoided to a large extent. Also,

meeting liabilities of both short term and long term can be facilitated through maintaining

appropriate record of each accounts associated with SKANSKA plc. For example, if the

creditor’s payment is outstanding on particular day can be easily determined through creditor’s

ledger.

Preparation of budget and making future projections: Forecasting and budgeting both are

known as either maker or destroyer of the business and to accomplish these tasks of forecasting

and budgeting successfully, financial records play a vital role (Kornberger, Pflueger and

Mouritsen, 2017). Business trends can be identified through historical data and on the basis of

which various future projections are made by financial manager or director with the aims of

keeping up the business profitable. The utility and value of financial data gets enhanced when it

has been generated through an appropriate accounting processes.

Helps in making investment decisions: With the help of finance function, where to make

investment can be determined as this function provide useful insights of which investment will

generate how much liquidity or return and for how much time. Accordingly, allocation of capital

can be done towards long term assets in the most profitable manner.

Helps in making financing decisions: Such decisions are meant for identify the sources from

which funds needed business operations can be acquired. It also determines the time when the

funds will be needed along with the amount of funds required. How much proportion of debt and

equity should be included in the overall capital is the concern of this function as it affects the

firm’s value and shareholder’s wealth. Therefore, maximisation of shareholder’s wealth and

minimisation of business’s risks can be ensured through finance function. For example, whether

to use more of equity or debt in the capital structure and how much the proportion of both these

components would cost to the business & and affects its value is being decided through

performing finance function.

Helps in making decisions related to distribution of profits: Dividend decision taken by the

financial manager is concerned about how much of the earnings of the SKANSKA plc. should be

distributed among shareholders and how much should be retained with the company can be

decided through finance function only. For example, dividend pay - out ratio can be determined

by finance manager by understanding the stability of SKANSKA plc. in generating revenues and

profits and liquidity position of the company, so that future course of action of the company

could not get hampered.

Duties of accounting & finance within SKANSKA PLC.

The finance & accounting department of SKANSKA plc. has the following duties to perform:

It is the duty of the financial accountant of SKANSKA plc. to record all the financial

transaction associated with the company on a regular basis (Scase and Goffee, 2017).

Financial accountant has the duty to prepare income & expenditure reports on a monthly

basis and provides the same to the financial manager of SKANSKA plc. to carry out their

duty of making decisions and preparing budgets accordingly.

Financial accountant has the duty of collecting as much data as possible, so that future

estimations can be in an effective manner. Similarly, financial manager is responsible for

advising on how much funding will be needed for the particular project on the basis of

their own estimations.

At last, Key Performance Indicators of the business must be created by financial manager

and analysed from time to time to ensure that the business is moving in the desired

direction.

For example, financial manager of SKANSKA is responsible for conducting internal audit on a

monthly basis to identify any discrepancies in the company’s financial results as against its

financial goals.

Roles of Accounting & finance within SKANSKA PLC.

The role played by accounting and finance department of SKANSKA plc. Is very noticeable

where it facilitates the following:

components would cost to the business & and affects its value is being decided through

performing finance function.

Helps in making decisions related to distribution of profits: Dividend decision taken by the

financial manager is concerned about how much of the earnings of the SKANSKA plc. should be

distributed among shareholders and how much should be retained with the company can be

decided through finance function only. For example, dividend pay - out ratio can be determined

by finance manager by understanding the stability of SKANSKA plc. in generating revenues and

profits and liquidity position of the company, so that future course of action of the company

could not get hampered.

Duties of accounting & finance within SKANSKA PLC.

The finance & accounting department of SKANSKA plc. has the following duties to perform:

It is the duty of the financial accountant of SKANSKA plc. to record all the financial

transaction associated with the company on a regular basis (Scase and Goffee, 2017).

Financial accountant has the duty to prepare income & expenditure reports on a monthly

basis and provides the same to the financial manager of SKANSKA plc. to carry out their

duty of making decisions and preparing budgets accordingly.

Financial accountant has the duty of collecting as much data as possible, so that future

estimations can be in an effective manner. Similarly, financial manager is responsible for

advising on how much funding will be needed for the particular project on the basis of

their own estimations.

At last, Key Performance Indicators of the business must be created by financial manager

and analysed from time to time to ensure that the business is moving in the desired

direction.

For example, financial manager of SKANSKA is responsible for conducting internal audit on a

monthly basis to identify any discrepancies in the company’s financial results as against its

financial goals.

Roles of Accounting & finance within SKANSKA PLC.

The role played by accounting and finance department of SKANSKA plc. Is very noticeable

where it facilitates the following:

Recording of company's income and expenses to arrive at the year end financial

performance of the company (Mai and et.al., 2019).

System accountant facilitates analysis of financial information needs of the company by

undertaking review of the existing accounting system.

Monthly processing of payroll is what the task of financial accountant.

Financial manager undertake to prepare budgets for every upcoming period and

accordingly identify variances occuring between planned and actual performance to avoid

any discrepancies in overall performance by taking corrective measures immediately or at

the right time. In this way, they ensures that the SKANSKA plc. is moving on the right

track.

TASK 2

Calculation of financial ratios

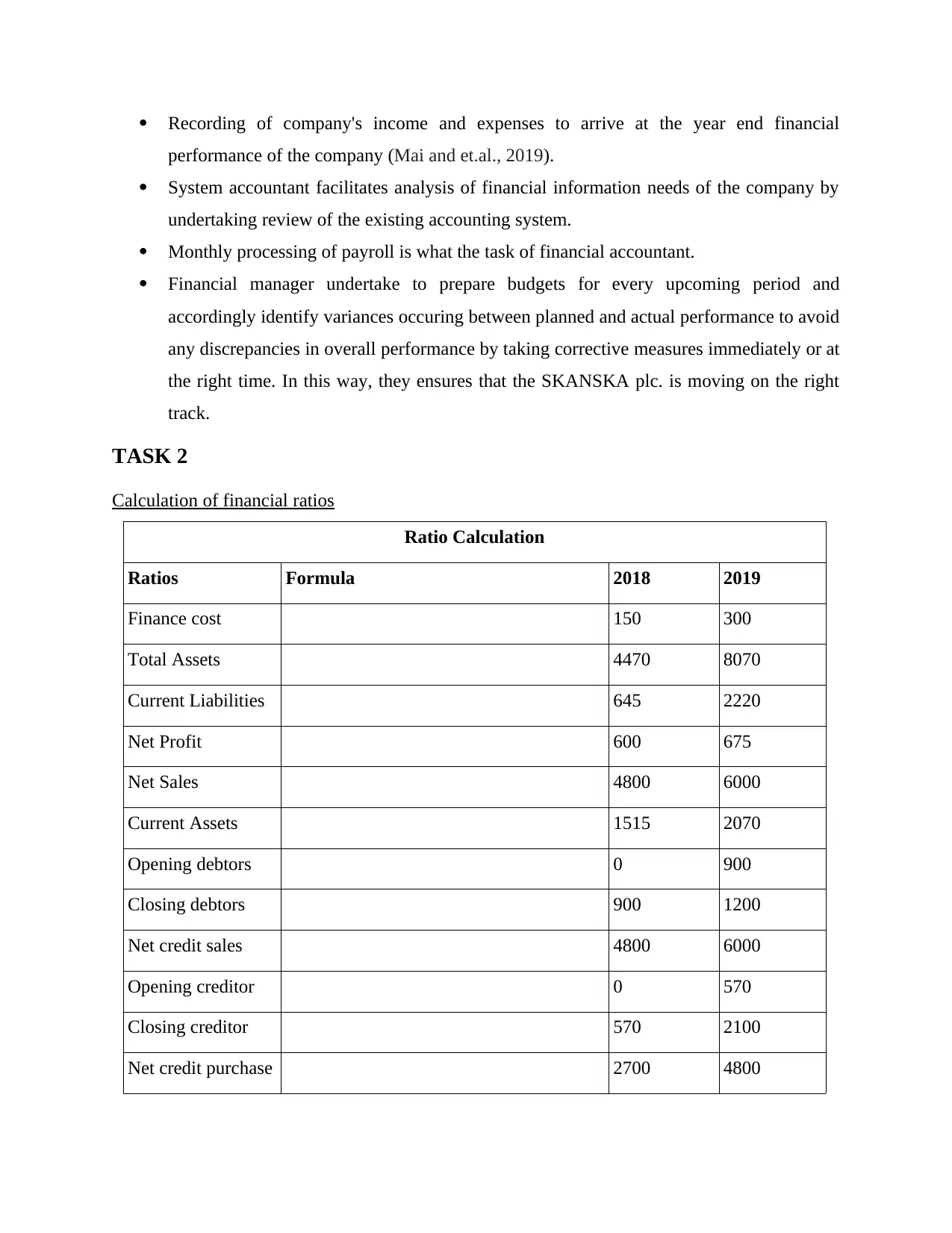

Ratio Calculation

Ratios Formula 2018 2019

Finance cost 150 300

Total Assets 4470 8070

Current Liabilities 645 2220

Net Profit 600 675

Net Sales 4800 6000

Current Assets 1515 2070

Opening debtors 0 900

Closing debtors 900 1200

Net credit sales 4800 6000

Opening creditor 0 570

Closing creditor 570 2100

Net credit purchase 2700 4800

performance of the company (Mai and et.al., 2019).

System accountant facilitates analysis of financial information needs of the company by

undertaking review of the existing accounting system.

Monthly processing of payroll is what the task of financial accountant.

Financial manager undertake to prepare budgets for every upcoming period and

accordingly identify variances occuring between planned and actual performance to avoid

any discrepancies in overall performance by taking corrective measures immediately or at

the right time. In this way, they ensures that the SKANSKA plc. is moving on the right

track.

TASK 2

Calculation of financial ratios

Ratio Calculation

Ratios Formula 2018 2019

Finance cost 150 300

Total Assets 4470 8070

Current Liabilities 645 2220

Net Profit 600 675

Net Sales 4800 6000

Current Assets 1515 2070

Opening debtors 0 900

Closing debtors 900 1200

Net credit sales 4800 6000

Opening creditor 0 570

Closing creditor 570 2100

Net credit purchase 2700 4800

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

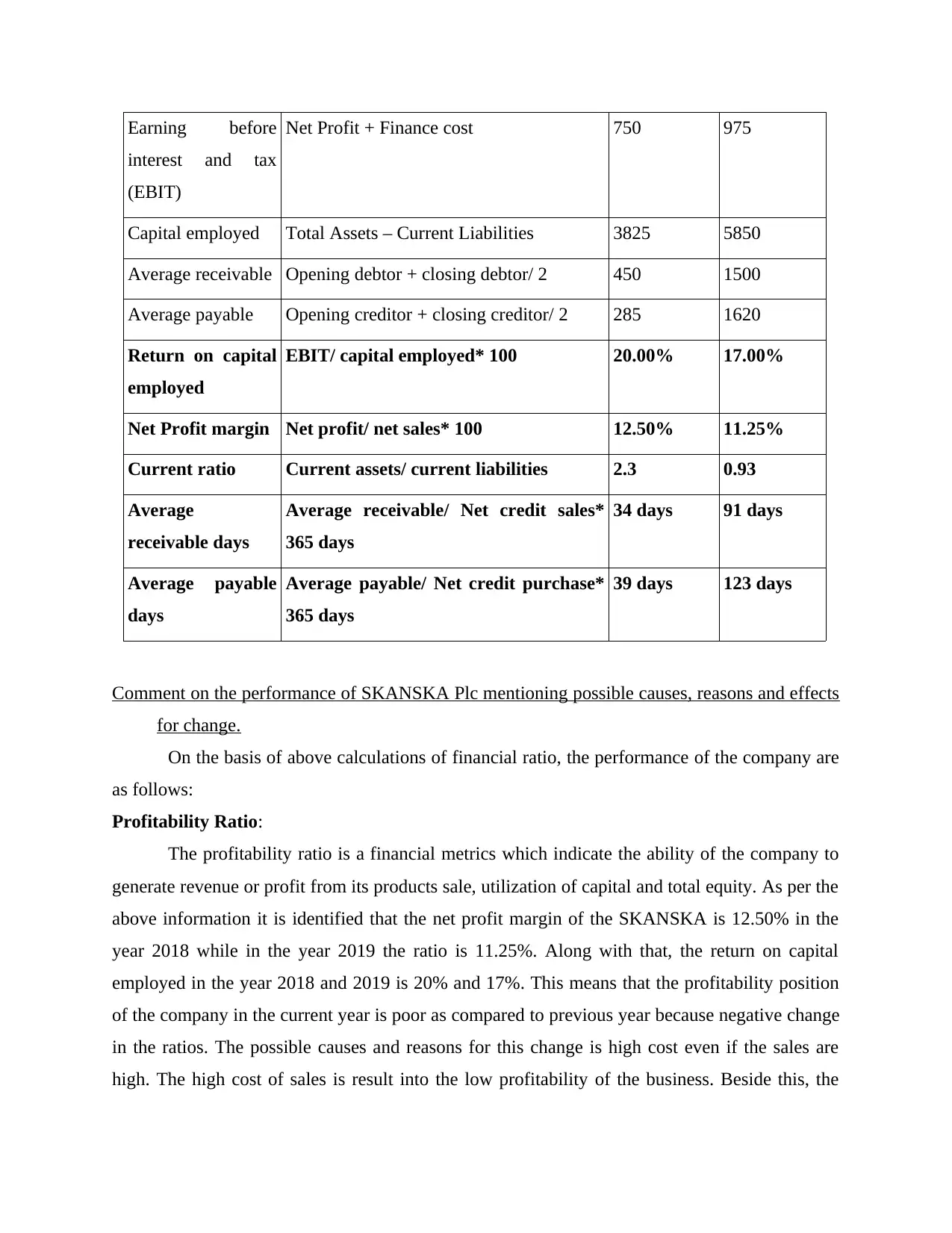

Earning before

interest and tax

(EBIT)

Net Profit + Finance cost 750 975

Capital employed Total Assets – Current Liabilities 3825 5850

Average receivable Opening debtor + closing debtor/ 2 450 1500

Average payable Opening creditor + closing creditor/ 2 285 1620

Return on capital

employed

EBIT/ capital employed* 100 20.00% 17.00%

Net Profit margin Net profit/ net sales* 100 12.50% 11.25%

Current ratio Current assets/ current liabilities 2.3 0.93

Average

receivable days

Average receivable/ Net credit sales*

365 days

34 days 91 days

Average payable

days

Average payable/ Net credit purchase*

365 days

39 days 123 days

Comment on the performance of SKANSKA Plc mentioning possible causes, reasons and effects

for change.

On the basis of above calculations of financial ratio, the performance of the company are

as follows:

Profitability Ratio:

The profitability ratio is a financial metrics which indicate the ability of the company to

generate revenue or profit from its products sale, utilization of capital and total equity. As per the

above information it is identified that the net profit margin of the SKANSKA is 12.50% in the

year 2018 while in the year 2019 the ratio is 11.25%. Along with that, the return on capital

employed in the year 2018 and 2019 is 20% and 17%. This means that the profitability position

of the company in the current year is poor as compared to previous year because negative change

in the ratios. The possible causes and reasons for this change is high cost even if the sales are

high. The high cost of sales is result into the low profitability of the business. Beside this, the

interest and tax

(EBIT)

Net Profit + Finance cost 750 975

Capital employed Total Assets – Current Liabilities 3825 5850

Average receivable Opening debtor + closing debtor/ 2 450 1500

Average payable Opening creditor + closing creditor/ 2 285 1620

Return on capital

employed

EBIT/ capital employed* 100 20.00% 17.00%

Net Profit margin Net profit/ net sales* 100 12.50% 11.25%

Current ratio Current assets/ current liabilities 2.3 0.93

Average

receivable days

Average receivable/ Net credit sales*

365 days

34 days 91 days

Average payable

days

Average payable/ Net credit purchase*

365 days

39 days 123 days

Comment on the performance of SKANSKA Plc mentioning possible causes, reasons and effects

for change.

On the basis of above calculations of financial ratio, the performance of the company are

as follows:

Profitability Ratio:

The profitability ratio is a financial metrics which indicate the ability of the company to

generate revenue or profit from its products sale, utilization of capital and total equity. As per the

above information it is identified that the net profit margin of the SKANSKA is 12.50% in the

year 2018 while in the year 2019 the ratio is 11.25%. Along with that, the return on capital

employed in the year 2018 and 2019 is 20% and 17%. This means that the profitability position

of the company in the current year is poor as compared to previous year because negative change

in the ratios. The possible causes and reasons for this change is high cost even if the sales are

high. The high cost of sales is result into the low profitability of the business. Beside this, the

poor management of the company is also one of the reasons behind the poor profitability

(Battiston and et.al., 2021). The effect of such change over the investors is that they unable to get

high returns and on the company is that they unable to keep their investors happy and satisfied.

Liquidity Ratio:

The liquidity ratio is also one of the significant part of the financial ratio which state the

ability of the company to pay of its current liabilities. The payment must be done with the use of

amount generated from current assets. This ratio includes current ratio (CR). The CR of

SKANSKA Plc in the year 2018 is 2.3 while in the year 2019 it has reduced to 0.93. This is a

negative change in the ratio which indicate that company are unable to manage its current assets

and liabilities. The reason and causes behind this might be that the company are holding outdated

inventories within the warehouse which further increases their holding cost. Further, the reason

of such change is also because of the late payment receivables from trade debtors. This change

majorly affects the performance of the SKASKA Plc because they are unable to maintain a

relation with its customer as well as its creditors (Bradbury and Scott, 2021). However, investors

of the company do not use the liquidity ratio for their decision-making thus it does not affect

them. In order to improve this, it is advisable to the company that they have to switch from the

short-term debt to the long-term debt.

Efficiency Ratio:

The efficiency ratio of the company basically states its ability to use and manage the

current and fixed assets of the company. This includes the average receivable days which state

the ability of the company to receive the payment from its debtors and customers. The average

receivable days also known as debtors’ collection period of the SKANSKA Plc in the year 2018

is 34 days while in the year 2019 91 days. This indicates that previously company receives its

debtors’ dues in 34 days but now they require 91 days to get its payment from the trade

receivables. The reason behind such change is that the company is poor credit policy

management of the business. The decrease in the cash sales and increase in the credit sales of the

products are also one of the causes behind the high collection days. This change has affected

only on the debtors and company but it does not put the effect on the investors. The poor and low

collection period badly affects the operating cycle of the business and the impact of which whole

(Battiston and et.al., 2021). The effect of such change over the investors is that they unable to get

high returns and on the company is that they unable to keep their investors happy and satisfied.

Liquidity Ratio:

The liquidity ratio is also one of the significant part of the financial ratio which state the

ability of the company to pay of its current liabilities. The payment must be done with the use of

amount generated from current assets. This ratio includes current ratio (CR). The CR of

SKANSKA Plc in the year 2018 is 2.3 while in the year 2019 it has reduced to 0.93. This is a

negative change in the ratio which indicate that company are unable to manage its current assets

and liabilities. The reason and causes behind this might be that the company are holding outdated

inventories within the warehouse which further increases their holding cost. Further, the reason

of such change is also because of the late payment receivables from trade debtors. This change

majorly affects the performance of the SKASKA Plc because they are unable to maintain a

relation with its customer as well as its creditors (Bradbury and Scott, 2021). However, investors

of the company do not use the liquidity ratio for their decision-making thus it does not affect

them. In order to improve this, it is advisable to the company that they have to switch from the

short-term debt to the long-term debt.

Efficiency Ratio:

The efficiency ratio of the company basically states its ability to use and manage the

current and fixed assets of the company. This includes the average receivable days which state

the ability of the company to receive the payment from its debtors and customers. The average

receivable days also known as debtors’ collection period of the SKANSKA Plc in the year 2018

is 34 days while in the year 2019 91 days. This indicates that previously company receives its

debtors’ dues in 34 days but now they require 91 days to get its payment from the trade

receivables. The reason behind such change is that the company is poor credit policy

management of the business. The decrease in the cash sales and increase in the credit sales of the

products are also one of the causes behind the high collection days. This change has affected

only on the debtors and company but it does not put the effect on the investors. The poor and low

collection period badly affects the operating cycle of the business and the impact of which whole

cash management get dissolved (Brooks and Oikonomou, 2018). Thus, it is advisable to the

company that they have to improve the same for which they need to provide the discounts to its

debtors on its early payment. Further, the credit policy is only allowable to the loyal customers of

the company only.

Short-term Solvency Ratio:

The short-term solvency ratio of the company indicates that the ability of the company to

meet its short-term obligation such as business loan, creditors etc. This ratio involves the average

payment ratio and this ratio of SKANSKA Plc in the year 2018 is 39 days while in the year 2019

is 123 days. This means that now the company is paying its creditors late which indicate poor

credibility and solvency of the business. The possible causes of such negative change of ratio is

that the company are unable to receive its payment from customer on time thus they also unable

to pay the payment to its creditors on time. The effect of this over the company is that their credit

worthiness is highly affected and further the creditors will never allow to supply the raw material

to company at credit terms (Bui, 2021). That's why it is advisable to the company that they have

to improve its creditors payment period. For this, they can acquire long-term loan to pay its

creditors on time if the liability gets increases.

Recommendation to Investors of SKANSKA Plc.

On the basis of above calculation and interpretation of financial ratios of SKANSKA Plc,

it is identified that the overall performance of the company in the year 2019 is poorer than the

performance of the company in the year 2018. On this basis, it can be clearly identified and state

that investment of the £1 million in the SKANSKA company is not profitable for the investors at

all. It is because the profit and earnings of the company as comparison or percentage of its sales

are decreasing even though the sales of the company are increasing. The investors of the

company basically analyse the risk attached with the business before making the decision

regarding the investment. It is because any wrong decision may lead to heavy loss to the

company which may also be financial. Further, it is also advisable to the company that such

negative change and poor performance is because of the Covid-19 and lock-down (Cockcroft and

Russell, 2018). After this situation, it might be possible that the company will definitely recover

company that they have to improve the same for which they need to provide the discounts to its

debtors on its early payment. Further, the credit policy is only allowable to the loyal customers of

the company only.

Short-term Solvency Ratio:

The short-term solvency ratio of the company indicates that the ability of the company to

meet its short-term obligation such as business loan, creditors etc. This ratio involves the average

payment ratio and this ratio of SKANSKA Plc in the year 2018 is 39 days while in the year 2019

is 123 days. This means that now the company is paying its creditors late which indicate poor

credibility and solvency of the business. The possible causes of such negative change of ratio is

that the company are unable to receive its payment from customer on time thus they also unable

to pay the payment to its creditors on time. The effect of this over the company is that their credit

worthiness is highly affected and further the creditors will never allow to supply the raw material

to company at credit terms (Bui, 2021). That's why it is advisable to the company that they have

to improve its creditors payment period. For this, they can acquire long-term loan to pay its

creditors on time if the liability gets increases.

Recommendation to Investors of SKANSKA Plc.

On the basis of above calculation and interpretation of financial ratios of SKANSKA Plc,

it is identified that the overall performance of the company in the year 2019 is poorer than the

performance of the company in the year 2018. On this basis, it can be clearly identified and state

that investment of the £1 million in the SKANSKA company is not profitable for the investors at

all. It is because the profit and earnings of the company as comparison or percentage of its sales

are decreasing even though the sales of the company are increasing. The investors of the

company basically analyse the risk attached with the business before making the decision

regarding the investment. It is because any wrong decision may lead to heavy loss to the

company which may also be financial. Further, it is also advisable to the company that such

negative change and poor performance is because of the Covid-19 and lock-down (Cockcroft and

Russell, 2018). After this situation, it might be possible that the company will definitely recover

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

its position and earn high profit. So, investors can invest part of the amount of £1 million in the

company.

CONCLUSION

The report has concluded the function, duty and roles of the accounting and finance team

within the SKANSKA Plc. The report has also concluded the importance of accounting and

finance within the company and how they help the company in achieving their goals and

objectives. Further, this report has also calculated the five ratios such as return on capital

employed, net profit margin, current ratio, average receivable days and average payable days.

The report has also commented on the performance of SKANSKA using the result of the

financial ratio. The comment also includes the reason, causes and effect of negative as well as

positive change in the ratio. This report has also concluded that the performance of the company

in the current year is poor as compared to the previous year which might be because of the

Covid-19 situation and lock-down. The report has also concluded the management accounting

techniques which help the company in their decision-making process along with the planning

and controlling. Lastly, the report has stated that investment of £1 million is profitable for the

investors of the company or not.

company.

CONCLUSION

The report has concluded the function, duty and roles of the accounting and finance team

within the SKANSKA Plc. The report has also concluded the importance of accounting and

finance within the company and how they help the company in achieving their goals and

objectives. Further, this report has also calculated the five ratios such as return on capital

employed, net profit margin, current ratio, average receivable days and average payable days.

The report has also commented on the performance of SKANSKA using the result of the

financial ratio. The comment also includes the reason, causes and effect of negative as well as

positive change in the ratio. This report has also concluded that the performance of the company

in the current year is poor as compared to the previous year which might be because of the

Covid-19 situation and lock-down. The report has also concluded the management accounting

techniques which help the company in their decision-making process along with the planning

and controlling. Lastly, the report has stated that investment of £1 million is profitable for the

investors of the company or not.

REFERENCES

Books and Journals

Agbo, E. I. and Nwankwo, S. N. P., 2018. Impact of Average Payments Period on the Return on

Assets of Quoted Insurance Companies in Nigeria. European Journal of Business and

Management. 10(28). pp.25-34.

Akhtaruzzaman, M., Berg, N. and Hajzler, C., 2017. Expropriation risk and FDI in developing

countries: Does return of capital dominate return on capital?. European Journal of

Political Economy. 49. pp.84-107.

Anjum, S., 2021. Job Selection Priorities of Accounting and Finance Graduates: An Empirical

Evidence from Pakistan. Business, Management and Economics Research. 7(2). pp.27-38.

Battiston, S. and et.al., 2021. Accounting for finance is key for climate mitigation

pathways. Science. 372(6545). pp.918-920.

Bradbury, M. E. and Scott, T., 2021. What accounting standards were the cause of enforcement

actions following IFRS adoption?. Accounting & Finance. 61. pp.2247-2268.

Brooks, C. and Oikonomou, I., 2018. The effects of environmental, social and governance

disclosures and performance on firm value: A review of the literature in accounting and

finance. The British Accounting Review. 50(1). pp.1-15.

Bui, B., 2021. A critical examination of the use of research templates in accounting and

finance. Accounting & Finance. 61(2). pp.2671-2696.

Cockcroft, S. and Russell, M., 2018. Big data opportunities for accounting and finance practice

and research. Australian Accounting Review. 28(3). pp.323-333.

ElShaabany, M. M., 2021. Does Accounting and Finance Courses Enable Soft Skill Learning? A

Mediation Study. World Journal of Education. 11(1). pp.42-50.

Kokina, J. and Blanchette, S., 2019. Early evidence of digital labor in accounting: Innovation

with Robotic Process Automation. International Journal of Accounting Information

Systems. 35. p.100431.

Brooks, C. and Oikonomou, I., 2018. The effects of environmental, social and governance

disclosures and performance on firm value: A review of the literature in accounting and

finance. The British Accounting Review. 50(1). pp.1-15.

Books and Journals

Agbo, E. I. and Nwankwo, S. N. P., 2018. Impact of Average Payments Period on the Return on

Assets of Quoted Insurance Companies in Nigeria. European Journal of Business and

Management. 10(28). pp.25-34.

Akhtaruzzaman, M., Berg, N. and Hajzler, C., 2017. Expropriation risk and FDI in developing

countries: Does return of capital dominate return on capital?. European Journal of

Political Economy. 49. pp.84-107.

Anjum, S., 2021. Job Selection Priorities of Accounting and Finance Graduates: An Empirical

Evidence from Pakistan. Business, Management and Economics Research. 7(2). pp.27-38.

Battiston, S. and et.al., 2021. Accounting for finance is key for climate mitigation

pathways. Science. 372(6545). pp.918-920.

Bradbury, M. E. and Scott, T., 2021. What accounting standards were the cause of enforcement

actions following IFRS adoption?. Accounting & Finance. 61. pp.2247-2268.

Brooks, C. and Oikonomou, I., 2018. The effects of environmental, social and governance

disclosures and performance on firm value: A review of the literature in accounting and

finance. The British Accounting Review. 50(1). pp.1-15.

Bui, B., 2021. A critical examination of the use of research templates in accounting and

finance. Accounting & Finance. 61(2). pp.2671-2696.

Cockcroft, S. and Russell, M., 2018. Big data opportunities for accounting and finance practice

and research. Australian Accounting Review. 28(3). pp.323-333.

ElShaabany, M. M., 2021. Does Accounting and Finance Courses Enable Soft Skill Learning? A

Mediation Study. World Journal of Education. 11(1). pp.42-50.

Kokina, J. and Blanchette, S., 2019. Early evidence of digital labor in accounting: Innovation

with Robotic Process Automation. International Journal of Accounting Information

Systems. 35. p.100431.

Brooks, C. and Oikonomou, I., 2018. The effects of environmental, social and governance

disclosures and performance on firm value: A review of the literature in accounting and

finance. The British Accounting Review. 50(1). pp.1-15.

Bebbington, J. and Unerman, J., 2018. Achieving the United Nations Sustainable Development

Goals: an enabling role for accounting research. Accounting, Auditing & Accountability

Journal.

Kornberger, M., Pflueger, D. and Mouritsen, J., 2017. Evaluative infrastructures: Accounting

for platform organization. Accounting, Organizations and Society. 60. pp.79-95.

Scase, R. and Goffee, R., 2017. Reluctant Managers (Routledge Revivals): Their Work and

Lifestyles. Routledge.

Mai, F. and et.al., 2019. Deep learning models for bankruptcy prediction using textual

disclosures. European journal of operational research. 274(2). pp.743-758.

Goals: an enabling role for accounting research. Accounting, Auditing & Accountability

Journal.

Kornberger, M., Pflueger, D. and Mouritsen, J., 2017. Evaluative infrastructures: Accounting

for platform organization. Accounting, Organizations and Society. 60. pp.79-95.

Scase, R. and Goffee, R., 2017. Reluctant Managers (Routledge Revivals): Their Work and

Lifestyles. Routledge.

Mai, F. and et.al., 2019. Deep learning models for bankruptcy prediction using textual

disclosures. European journal of operational research. 274(2). pp.743-758.

1 out of 13

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.