Financial Decision Making INTRODUCTION 3 TASK 13 Evaluation of the role of accounting and finance: 6 Interpretation and Analysis of financial ratios: 7

VerifiedAdded on 2021/02/19

|11

|3669

|262

AI Summary

Financial Decision Making INTRODUCTION 3 TASK 13 Evaluation of the role of accounting and finance: 3 TASK 26 Calculation of the ratios to analyse company performance: 6 Interpretation and analysis of financial ratios:7 CONCLUSION 10 Interpretation 10 REFERENCES 11 INTRODUCTION Financial decision making implies to systematic and organised set of activity concerned with choosing most appropriate and efficient alternative among different alternative course of action related to managing fiscal operation. Report provides explanation about various elements like terms, structure of financial statements and application in

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Financial

Decision Making

Decision Making

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

Evaluation of the role of accounting and finance:.......................................................................3

TASK 2............................................................................................................................................6

Calculation of the ratios to analyse company performance:........................................................6

Interpretation and analysis of financial ratios:.............................................................................7

CONCLUSION..............................................................................................................................10

......................................................................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

Evaluation of the role of accounting and finance:.......................................................................3

TASK 2............................................................................................................................................6

Calculation of the ratios to analyse company performance:........................................................6

Interpretation and analysis of financial ratios:.............................................................................7

CONCLUSION..............................................................................................................................10

......................................................................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION

Financial decision making implies to systematic and organised set of activity concerned

with choosing most appropriate and efficient alternative among different alternative course of

action related to fiscal operation. Basic objective or motto of it is to bring and choose new or

innovative steps in order to attain business objective, vision and mission (Ball, 2013). Report

provides explanation about various elements like terms, structure of financial statements and

application in planning, controlling and decision making of techniques of management

accounting in context of Camden Limited. It is United kingdom's top supplier and manufacturer

of uPVC windows and doors. Report also contains workings of ratios along with relevance to

different users and duty of accounting and finance in business entity regarding decision-making

and reporting in context of ALPHA Limited, UK's manufacturing company.

TASK 1

Evaluation of the role of accounting and finance:

Overview of company:

In UK, Camden Limited is most famous supplier and provider of uPVC doorway,

entrance and windows. Company provides customised designs of windows and entrance

according to customers choice. Company has main head office in Antrim, Northern Ireland and

managing its business across the UK through it. Company is renowned for their

uncompanionable designs and range of windows, entrance doors. It has reached in this position

due to experience of approx 36 years and unique product quality in industry. It design and

provide products which are long lasting and complies with security norms (Camden Group.

2019). Recently company made funding in recycling of uPVC products and offer recycling of its

old products. Company with its unique ideas and innovation giving tuff competition in uPVC

industry. It has product range which are substitute of normal demanding products with changing

environment and climate. It is supplying products for domestic and commercial use in UK.

Structure of and terms used within the financial statements:

Financial statements majorly combines income statements or profit or loss accounts,

balance sheet or statement of financial position and change in equity or shareholder's fund, cash

flow statement etc. Structure of balance sheet includes owner's equity, liabilities and all assets.

Balances shown in balance sheet is value of all liabilities and assets as on fix specified date.

Financial decision making implies to systematic and organised set of activity concerned

with choosing most appropriate and efficient alternative among different alternative course of

action related to fiscal operation. Basic objective or motto of it is to bring and choose new or

innovative steps in order to attain business objective, vision and mission (Ball, 2013). Report

provides explanation about various elements like terms, structure of financial statements and

application in planning, controlling and decision making of techniques of management

accounting in context of Camden Limited. It is United kingdom's top supplier and manufacturer

of uPVC windows and doors. Report also contains workings of ratios along with relevance to

different users and duty of accounting and finance in business entity regarding decision-making

and reporting in context of ALPHA Limited, UK's manufacturing company.

TASK 1

Evaluation of the role of accounting and finance:

Overview of company:

In UK, Camden Limited is most famous supplier and provider of uPVC doorway,

entrance and windows. Company provides customised designs of windows and entrance

according to customers choice. Company has main head office in Antrim, Northern Ireland and

managing its business across the UK through it. Company is renowned for their

uncompanionable designs and range of windows, entrance doors. It has reached in this position

due to experience of approx 36 years and unique product quality in industry. It design and

provide products which are long lasting and complies with security norms (Camden Group.

2019). Recently company made funding in recycling of uPVC products and offer recycling of its

old products. Company with its unique ideas and innovation giving tuff competition in uPVC

industry. It has product range which are substitute of normal demanding products with changing

environment and climate. It is supplying products for domestic and commercial use in UK.

Structure of and terms used within the financial statements:

Financial statements majorly combines income statements or profit or loss accounts,

balance sheet or statement of financial position and change in equity or shareholder's fund, cash

flow statement etc. Structure of balance sheet includes owner's equity, liabilities and all assets.

Balances shown in balance sheet is value of all liabilities and assets as on fix specified date.

Shareholder's fund or owner's equity includes capital, reserves and current year profit. Liabilities

are further divided in current liabilities and non current liabilities. Assets are also classified as

non current assets i.e. tangible assets, fictitious assets etc. and current assets i.e. inventory, cash

and cash equivalents etc. Structure of income statements comprises net turnover, cost of goods

sold, gross income, direct and indirect expenses and net income. Income statements combine

both trading account and profit & loss account (Bryer, 2013). In trading account part gross profit

calculation is shown. Gross profit is computed by adjusting opening and closing inventory, and

deducting direct expenses from total amount of sales. Where as in net profit part all indirect

expenses and incomes are exhibited. Net profit is computed by deducting all indirect expenses

from indirect incomes. Indirect expense and income are those gain and expense which are not

directly related to core business activities of business activity.

Role of management accounting techniques:

Management accounting contains most valuable functions which facilitates management

by rendering information or aggregations to managing employees/officials in trade enterprise

assisting them in taking judgements and decisions. The whole of process and concerned activities

of management accounting focuses towards use of specific relevant tools and techniques that to

bring smoothness in process of controlling, decision-making and planning. Here major aim of

company officials is to provide effectiveness and make vital improvement in company's key

practices. In large companies like Camden LTD accountants or managerial personnels using

different techniques to achieve desired efficiencies company's operations and practises. It also

assist in systematic allocation and assignment of monetary and fiscal resources to increase and

attain accountability. Techniques are adopted by companies set guidance and policies for

conducing trade and management practices. financial planning, cash flow statements, analysis of

financial statements, fund flow statements etc. are most widely accepted management accounting

techniques. There multi-purpose techniques which are necessary for complete development of

and to provide efficiency in internal and external processes. Following is a discussion on various

techniques management applies under management accounting:

Financial Planning: It simply implies to set of specific tasks and functions that are

conducted by companies to project findings, estimate capitals and asses the need of

capital requirement while considering competitive factors. It helps to create financial

polices and guidelines regarding procurement, investment & application and management

are further divided in current liabilities and non current liabilities. Assets are also classified as

non current assets i.e. tangible assets, fictitious assets etc. and current assets i.e. inventory, cash

and cash equivalents etc. Structure of income statements comprises net turnover, cost of goods

sold, gross income, direct and indirect expenses and net income. Income statements combine

both trading account and profit & loss account (Bryer, 2013). In trading account part gross profit

calculation is shown. Gross profit is computed by adjusting opening and closing inventory, and

deducting direct expenses from total amount of sales. Where as in net profit part all indirect

expenses and incomes are exhibited. Net profit is computed by deducting all indirect expenses

from indirect incomes. Indirect expense and income are those gain and expense which are not

directly related to core business activities of business activity.

Role of management accounting techniques:

Management accounting contains most valuable functions which facilitates management

by rendering information or aggregations to managing employees/officials in trade enterprise

assisting them in taking judgements and decisions. The whole of process and concerned activities

of management accounting focuses towards use of specific relevant tools and techniques that to

bring smoothness in process of controlling, decision-making and planning. Here major aim of

company officials is to provide effectiveness and make vital improvement in company's key

practices. In large companies like Camden LTD accountants or managerial personnels using

different techniques to achieve desired efficiencies company's operations and practises. It also

assist in systematic allocation and assignment of monetary and fiscal resources to increase and

attain accountability. Techniques are adopted by companies set guidance and policies for

conducing trade and management practices. financial planning, cash flow statements, analysis of

financial statements, fund flow statements etc. are most widely accepted management accounting

techniques. There multi-purpose techniques which are necessary for complete development of

and to provide efficiency in internal and external processes. Following is a discussion on various

techniques management applies under management accounting:

Financial Planning: It simply implies to set of specific tasks and functions that are

conducted by companies to project findings, estimate capitals and asses the need of

capital requirement while considering competitive factors. It helps to create financial

polices and guidelines regarding procurement, investment & application and management

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

of amount of funds gathered through various sources within a business entity. Managers

in Camden Limited managers also using financial planning to develop a systems that

warn about level and adequateness of short and long term capital or funds to take quick

investment decisions. It provide easiness in planning process and developing a controlled

web to manage finance and funding tasks (Chiang, Nouri and Samanta, 2014). On the

basis of company's existing performance and funding structure, managerial personnels

conduct analysis and estimate funds requirement. It ascertain impact of funding sources

and ensures that long term funds are utilised for the long term purpose.

Analysis of financial statements: It is core method which is used by almost all

corporate entities to evaluate results and performance over a specific time period

applying financial statement and related sources. Financial statements generally includes

balance sheet, statement of income, change in shareholder's fund statement etc. All of

them covers and presents numerous aspects of entity. For instance balance sheet exhibits

book value of company's assets and liabilities as on period ended date whereas income

statement presents actual gross and net profitability condition. A detailed analysis of

these can help managers in planning and decision making as financial statement shows

true facts on performance. Camden LTD reports financial statements and its analysis on

annually basis which is used by users and management for decision making. Company

performs such analysis to explore the potential opportunities, funding sources, factors

harming company's performance and determining possible or contingent obligations.

Financial statement facilitates a comparative analysis of figures and values of more than

one year, an recognisance of weakness of company.

Historical Cost Accounting: It is a technique applied by managers and accountants to

record various assets of company at historical costs in statement of financial position.

Historical cost referred as basic initial price paid at the time of acquisition of assets. This

technique emphasises on theory that assets specially tangible fixed assets are required to

be presented at cost price paid on purchase and other expenses which are necessary for

used of asset, instead of market price (Hope, Thomas and Vyas, 2013). This approach

help to enhance the creditability of financial statement as it help to presents more reliable

data. However not all assets are recorded at historical price for example marketable

securities are not recorded at historical price. It is more biased free approach as value can

in Camden Limited managers also using financial planning to develop a systems that

warn about level and adequateness of short and long term capital or funds to take quick

investment decisions. It provide easiness in planning process and developing a controlled

web to manage finance and funding tasks (Chiang, Nouri and Samanta, 2014). On the

basis of company's existing performance and funding structure, managerial personnels

conduct analysis and estimate funds requirement. It ascertain impact of funding sources

and ensures that long term funds are utilised for the long term purpose.

Analysis of financial statements: It is core method which is used by almost all

corporate entities to evaluate results and performance over a specific time period

applying financial statement and related sources. Financial statements generally includes

balance sheet, statement of income, change in shareholder's fund statement etc. All of

them covers and presents numerous aspects of entity. For instance balance sheet exhibits

book value of company's assets and liabilities as on period ended date whereas income

statement presents actual gross and net profitability condition. A detailed analysis of

these can help managers in planning and decision making as financial statement shows

true facts on performance. Camden LTD reports financial statements and its analysis on

annually basis which is used by users and management for decision making. Company

performs such analysis to explore the potential opportunities, funding sources, factors

harming company's performance and determining possible or contingent obligations.

Financial statement facilitates a comparative analysis of figures and values of more than

one year, an recognisance of weakness of company.

Historical Cost Accounting: It is a technique applied by managers and accountants to

record various assets of company at historical costs in statement of financial position.

Historical cost referred as basic initial price paid at the time of acquisition of assets. This

technique emphasises on theory that assets specially tangible fixed assets are required to

be presented at cost price paid on purchase and other expenses which are necessary for

used of asset, instead of market price (Hope, Thomas and Vyas, 2013). This approach

help to enhance the creditability of financial statement as it help to presents more reliable

data. However not all assets are recorded at historical price for example marketable

securities are not recorded at historical price. It is more biased free approach as value can

be easily verified through supporting documents. It can help to control the effective

utilisation of assets for business context. Management can also take decisions and

develop plans related to takeover and acquisition of assets.

Budgetary Control: Almost all business enterprise projects expenses and incomes, and

prepares different budgets on the basis of its different objectives and goals. Main

objective of farming various budgets is to develop processes and to create control over all

budgetary activities of company, so budget and budgetary controls are closely associated

with each other. Budgetary control includes processes related to forecasting values and

monitor the usage and fluctuation of funds (Zeff, Van der Wel and Camfferman, 2016).

Camden LTD applying budgetary control to control funds, do planning of utilisation of

funds and take budgetary decisions. It also provides complete comparative analysis of

different aspects of budgets to facilitate quick and effective decision-making. It help to

define planning as budgets prepared under it on the basis of effective plans. It control

costs and minimise costs by eliminating excessive wastages within company which leads

to maximisation of overall profits.

TASK 2

Calculation of the ratios to analyse company performance:

Ratios 2018 2017

ROCE or Return On Capital

Employed :

= (Operating Profit /Capital

Employed) *100

here, Capital Employed = Total

Assets – External liabilities.

= 412 / 2925 * 100

= 14.10%

= 375 / 1912.50 *100

= 19.60%

Net Profit Margin:

= Net Profit / Sale * 100

= 262.50 / 3000 * 100

= 8.75 %

= 300/ 2400 * 100

= 12.5 %

Current Ratio:

= Current Assets / Current

Liability

= 1035 / 1110

= 0.93

= 757.50 / 322.50

= 2.34

utilisation of assets for business context. Management can also take decisions and

develop plans related to takeover and acquisition of assets.

Budgetary Control: Almost all business enterprise projects expenses and incomes, and

prepares different budgets on the basis of its different objectives and goals. Main

objective of farming various budgets is to develop processes and to create control over all

budgetary activities of company, so budget and budgetary controls are closely associated

with each other. Budgetary control includes processes related to forecasting values and

monitor the usage and fluctuation of funds (Zeff, Van der Wel and Camfferman, 2016).

Camden LTD applying budgetary control to control funds, do planning of utilisation of

funds and take budgetary decisions. It also provides complete comparative analysis of

different aspects of budgets to facilitate quick and effective decision-making. It help to

define planning as budgets prepared under it on the basis of effective plans. It control

costs and minimise costs by eliminating excessive wastages within company which leads

to maximisation of overall profits.

TASK 2

Calculation of the ratios to analyse company performance:

Ratios 2018 2017

ROCE or Return On Capital

Employed :

= (Operating Profit /Capital

Employed) *100

here, Capital Employed = Total

Assets – External liabilities.

= 412 / 2925 * 100

= 14.10%

= 375 / 1912.50 *100

= 19.60%

Net Profit Margin:

= Net Profit / Sale * 100

= 262.50 / 3000 * 100

= 8.75 %

= 300/ 2400 * 100

= 12.5 %

Current Ratio:

= Current Assets / Current

Liability

= 1035 / 1110

= 0.93

= 757.50 / 322.50

= 2.34

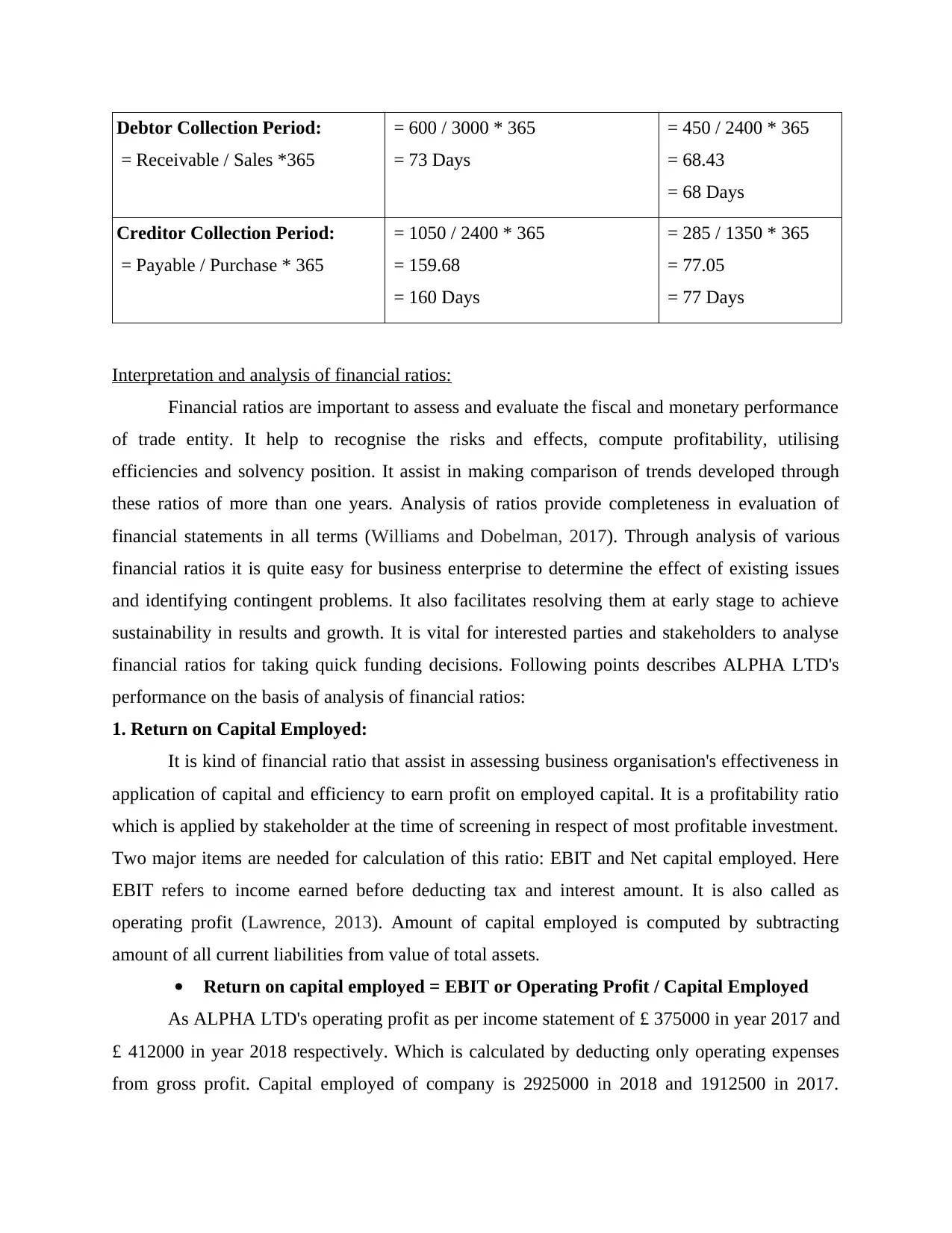

Debtor Collection Period:

= Receivable / Sales *365

= 600 / 3000 * 365

= 73 Days

= 450 / 2400 * 365

= 68.43

= 68 Days

Creditor Collection Period:

= Payable / Purchase * 365

= 1050 / 2400 * 365

= 159.68

= 160 Days

= 285 / 1350 * 365

= 77.05

= 77 Days

Interpretation and analysis of financial ratios:

Financial ratios are important to assess and evaluate the fiscal and monetary performance

of trade entity. It help to recognise the risks and effects, compute profitability, utilising

efficiencies and solvency position. It assist in making comparison of trends developed through

these ratios of more than one years. Analysis of ratios provide completeness in evaluation of

financial statements in all terms (Williams and Dobelman, 2017). Through analysis of various

financial ratios it is quite easy for business enterprise to determine the effect of existing issues

and identifying contingent problems. It also facilitates resolving them at early stage to achieve

sustainability in results and growth. It is vital for interested parties and stakeholders to analyse

financial ratios for taking quick funding decisions. Following points describes ALPHA LTD's

performance on the basis of analysis of financial ratios:

1. Return on Capital Employed:

It is kind of financial ratio that assist in assessing business organisation's effectiveness in

application of capital and efficiency to earn profit on employed capital. It is a profitability ratio

which is applied by stakeholder at the time of screening in respect of most profitable investment.

Two major items are needed for calculation of this ratio: EBIT and Net capital employed. Here

EBIT refers to income earned before deducting tax and interest amount. It is also called as

operating profit (Lawrence, 2013). Amount of capital employed is computed by subtracting

amount of all current liabilities from value of total assets.

Return on capital employed = EBIT or Operating Profit / Capital Employed

As ALPHA LTD's operating profit as per income statement of £ 375000 in year 2017 and

£ 412000 in year 2018 respectively. Which is calculated by deducting only operating expenses

from gross profit. Capital employed of company is 2925000 in 2018 and 1912500 in 2017.

= Receivable / Sales *365

= 600 / 3000 * 365

= 73 Days

= 450 / 2400 * 365

= 68.43

= 68 Days

Creditor Collection Period:

= Payable / Purchase * 365

= 1050 / 2400 * 365

= 159.68

= 160 Days

= 285 / 1350 * 365

= 77.05

= 77 Days

Interpretation and analysis of financial ratios:

Financial ratios are important to assess and evaluate the fiscal and monetary performance

of trade entity. It help to recognise the risks and effects, compute profitability, utilising

efficiencies and solvency position. It assist in making comparison of trends developed through

these ratios of more than one years. Analysis of ratios provide completeness in evaluation of

financial statements in all terms (Williams and Dobelman, 2017). Through analysis of various

financial ratios it is quite easy for business enterprise to determine the effect of existing issues

and identifying contingent problems. It also facilitates resolving them at early stage to achieve

sustainability in results and growth. It is vital for interested parties and stakeholders to analyse

financial ratios for taking quick funding decisions. Following points describes ALPHA LTD's

performance on the basis of analysis of financial ratios:

1. Return on Capital Employed:

It is kind of financial ratio that assist in assessing business organisation's effectiveness in

application of capital and efficiency to earn profit on employed capital. It is a profitability ratio

which is applied by stakeholder at the time of screening in respect of most profitable investment.

Two major items are needed for calculation of this ratio: EBIT and Net capital employed. Here

EBIT refers to income earned before deducting tax and interest amount. It is also called as

operating profit (Lawrence, 2013). Amount of capital employed is computed by subtracting

amount of all current liabilities from value of total assets.

Return on capital employed = EBIT or Operating Profit / Capital Employed

As ALPHA LTD's operating profit as per income statement of £ 375000 in year 2017 and

£ 412000 in year 2018 respectively. Which is calculated by deducting only operating expenses

from gross profit. Capital employed of company is 2925000 in 2018 and 1912500 in 2017.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Which is calculated as total assets less all current liabilities. So company's return on capital

employed is 14.10% and 19.60% in year 2018 and 2017 respectively. A decline in this ratio

indicating decrease in profit generation efficiency from capital engaged. Company can improve

this ratio by enhancing its operating profits, controlling its operating expenses and reducing

capital employed. It is most considerable ratio from investors point of view as they analyse this

ratio before making investment.

2. Net profit margin:

It is the revenue remaining after deducting all operating expenses, interests, taxes and

preferred stock dividends. All these elements are deducted from company's total revenue to

calculate net profit margin. It is the ratio of net profits to revenue for a firm . Net profit margin is

expressed in percentage form but for the ease can be represented in decimal form also. It

illustrates that how much of each pound in revenue collected by a company converts into profit.

It is one of the most key determinant of company's financial health. By keeping a track on

increase and decrease in its net profit margin a company can analyse whether current strategies

are beneficial or can forecast profits based on earnings (Lisowsky and Minnis, 2018). It is

helpful to the investors in assessing a company's position whether it is able to generate revenue

from its sales and whether the operating costs and overhead costs are being checked. Some key

factors which determines as to what is a good net profit margin are industry specifics, expansion

goals of the firm, longevity and size. Alpha Ltd. Had net profit margin of 12.5% in year 2017

whereas it had 8.75% in the year 2018 which shows that its ratio decreased in year 2018

compared to year 2017 which is a bad sign for the company. Alpha Ltd. Can increase its net

profit margin by reducing additional expenses which do not form part of core activities, by

cutting down underperforming products and services, By increasing products, value to the

customers and services, and at times increasing prices which although can be a harsh decision

but is required for business survival.

3. Current ratio:

It is a liquidity ratio which measures a firm's ability to meet its short term liabilities with

its current assets. It is an important ratio because it determines firms liability arising in upcoming

year. It alerts the firm to attain sufficient liquidity to meet its short upcoming liabilities. Current

assets like cash, cash equivalents, marketable securities form part of current ratio calculation

because they can be easily converted to cash in quick time. Companies with large base of current

employed is 14.10% and 19.60% in year 2018 and 2017 respectively. A decline in this ratio

indicating decrease in profit generation efficiency from capital engaged. Company can improve

this ratio by enhancing its operating profits, controlling its operating expenses and reducing

capital employed. It is most considerable ratio from investors point of view as they analyse this

ratio before making investment.

2. Net profit margin:

It is the revenue remaining after deducting all operating expenses, interests, taxes and

preferred stock dividends. All these elements are deducted from company's total revenue to

calculate net profit margin. It is the ratio of net profits to revenue for a firm . Net profit margin is

expressed in percentage form but for the ease can be represented in decimal form also. It

illustrates that how much of each pound in revenue collected by a company converts into profit.

It is one of the most key determinant of company's financial health. By keeping a track on

increase and decrease in its net profit margin a company can analyse whether current strategies

are beneficial or can forecast profits based on earnings (Lisowsky and Minnis, 2018). It is

helpful to the investors in assessing a company's position whether it is able to generate revenue

from its sales and whether the operating costs and overhead costs are being checked. Some key

factors which determines as to what is a good net profit margin are industry specifics, expansion

goals of the firm, longevity and size. Alpha Ltd. Had net profit margin of 12.5% in year 2017

whereas it had 8.75% in the year 2018 which shows that its ratio decreased in year 2018

compared to year 2017 which is a bad sign for the company. Alpha Ltd. Can increase its net

profit margin by reducing additional expenses which do not form part of core activities, by

cutting down underperforming products and services, By increasing products, value to the

customers and services, and at times increasing prices which although can be a harsh decision

but is required for business survival.

3. Current ratio:

It is a liquidity ratio which measures a firm's ability to meet its short term liabilities with

its current assets. It is an important ratio because it determines firms liability arising in upcoming

year. It alerts the firm to attain sufficient liquidity to meet its short upcoming liabilities. Current

assets like cash, cash equivalents, marketable securities form part of current ratio calculation

because they can be easily converted to cash in quick time. Companies with large base of current

assets will be easily able to pay off current liabilities when they fall due without the need to sell

important long term assets. It is a simple ratio calculated by dividing current assets with current

liabilities (Mio, 2016). The ideal current ratio for any business is 2:1. More the current ratio

more will be the liquidity hence more beneficial for the firm. That means a current ratio of 4:1

would means current assets are 4 times liquid to current liabilities. Alpha Ltd. Had a current ratio

of 2.34 in year 2017 and 0.93 in the year 2018 which shows that the it had more liquidity in year

2017 and became highly illiquid in the year 2018. Alpha Ltd. Can improve its current ratio by

introducing measures to faster conversion of debtors or account receivable, by paying of existing

current liabilities, by cutting off unproductive assets, by raising capital from the shareholders to

meet its funding requirements to pay off its debt, and lastly by sweeping bank accounts.

3. Debtor Collection Period:

It is ratio that provides period or days account debtors takes to pay company.

Adequateness of cash to meet current obligations can be easily ensured by using this ratio. It

helps to recognize the debtors that in the near future may be insolvent. By early detection of

prospective insolvent debtors, the company can monitor its quantity of bed loans and dubious

provisions. Credit policies within a business organisation can be effectively formulated by

managers with help of this ratio (Omar, Johari and Smith, 2017). To operate day to day business

functions company needs to assess this ratio. It is calculated by dividing the average amount to

be received from trade receivables or balance of debtors by the credit sales. The obtained

amount is multiplied total days to get result in number of days.

Company Alpha Ltd has trade receivable amounting 450000 in year 2017 and 600000 in

2018. Sales of company in year 2017 is 2400000 and in 2018 it is 3000000, here in calculation of

ratio total sales is assumed to be credit sales. Company's average collection period in 2018 is 73

days which was 68 days in year 2017. Here a decline in average collection period is recorded

which point out that Alpha Ltd's company's effectiveness to gather amounts from its debtors

decreased and company may face insufficiency of liquid cash to operate its activities in near

future. Company can improve this ratio by reducing credit sales and by optimising credit period

given to its debtors.

4. Creditors Collection Period: It is kind of financial ratio which exhibits days average

company is taking to pay its creditors and accounts payables. Here creditors includes vendors,

key suppliers, other companies providing short term credits. The ratio is calculated quarterly or

important long term assets. It is a simple ratio calculated by dividing current assets with current

liabilities (Mio, 2016). The ideal current ratio for any business is 2:1. More the current ratio

more will be the liquidity hence more beneficial for the firm. That means a current ratio of 4:1

would means current assets are 4 times liquid to current liabilities. Alpha Ltd. Had a current ratio

of 2.34 in year 2017 and 0.93 in the year 2018 which shows that the it had more liquidity in year

2017 and became highly illiquid in the year 2018. Alpha Ltd. Can improve its current ratio by

introducing measures to faster conversion of debtors or account receivable, by paying of existing

current liabilities, by cutting off unproductive assets, by raising capital from the shareholders to

meet its funding requirements to pay off its debt, and lastly by sweeping bank accounts.

3. Debtor Collection Period:

It is ratio that provides period or days account debtors takes to pay company.

Adequateness of cash to meet current obligations can be easily ensured by using this ratio. It

helps to recognize the debtors that in the near future may be insolvent. By early detection of

prospective insolvent debtors, the company can monitor its quantity of bed loans and dubious

provisions. Credit policies within a business organisation can be effectively formulated by

managers with help of this ratio (Omar, Johari and Smith, 2017). To operate day to day business

functions company needs to assess this ratio. It is calculated by dividing the average amount to

be received from trade receivables or balance of debtors by the credit sales. The obtained

amount is multiplied total days to get result in number of days.

Company Alpha Ltd has trade receivable amounting 450000 in year 2017 and 600000 in

2018. Sales of company in year 2017 is 2400000 and in 2018 it is 3000000, here in calculation of

ratio total sales is assumed to be credit sales. Company's average collection period in 2018 is 73

days which was 68 days in year 2017. Here a decline in average collection period is recorded

which point out that Alpha Ltd's company's effectiveness to gather amounts from its debtors

decreased and company may face insufficiency of liquid cash to operate its activities in near

future. Company can improve this ratio by reducing credit sales and by optimising credit period

given to its debtors.

4. Creditors Collection Period: It is kind of financial ratio which exhibits days average

company is taking to pay its creditors and accounts payables. Here creditors includes vendors,

key suppliers, other companies providing short term credits. The ratio is calculated quarterly or

annually and shows how well the money outflows of the company are managed (Tang, Chen and

Lin, 2016). Company having higher creditor collection period takes more time for payment of its

various bills. It represent company's performance in liquidity term. It point outs the decreasing

decreasing efficiency or inability to pay its creditors. Credit term provided by creditors also

affected by results of this ratio.

Alpha Ltd has reported trade payable amounting 285000 and 1050000 in year 2017 and

2018 respectively. Company's purchase amount is 2400000 and 1350000 in year 2018 and 2017

respectively. Here all purchases are assumed to be on credit. Company's average payable period

is 160 days in 2018 which was 77 days. There is an increase recorded in average payable period

which indicates that company is ability to make payments to its different trade payable has been

decreased.

CONCLUSION

It has been founded from the above study that financial decision making is a vital task for

a business organisation as it determines the future course of action. In establishing a structure for

effective decision making, ratio analysis and interpretation of financial statement is significant.

In practical world to provide effectiveness in process of effective financial decision-making,

managerial personnels conducts analysis of financial statements, structure, ratios and other

financial aspects.

Lin, 2016). Company having higher creditor collection period takes more time for payment of its

various bills. It represent company's performance in liquidity term. It point outs the decreasing

decreasing efficiency or inability to pay its creditors. Credit term provided by creditors also

affected by results of this ratio.

Alpha Ltd has reported trade payable amounting 285000 and 1050000 in year 2017 and

2018 respectively. Company's purchase amount is 2400000 and 1350000 in year 2018 and 2017

respectively. Here all purchases are assumed to be on credit. Company's average payable period

is 160 days in 2018 which was 77 days. There is an increase recorded in average payable period

which indicates that company is ability to make payments to its different trade payable has been

decreased.

CONCLUSION

It has been founded from the above study that financial decision making is a vital task for

a business organisation as it determines the future course of action. In establishing a structure for

effective decision making, ratio analysis and interpretation of financial statement is significant.

In practical world to provide effectiveness in process of effective financial decision-making,

managerial personnels conducts analysis of financial statements, structure, ratios and other

financial aspects.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

REFERENCES

Books and Journals:

Ball, R., 2013. Accounting informs investors and earnings management is rife: Two

questionable beliefs. Accounting Horizons. 27(4). pp.847-853.

Bryer, R., 2013. Americanism and financial accounting theory–Part 2: The ‘modern business

enterprise’, America's transition to capitalism, and the genesis of management

accounting. Critical Perspectives on Accounting. 24(4-5). pp.273-318.

Chiang, B., Nouri, H. and Samanta, S., 2014. The effects of different teaching approaches in

introductory financial accounting. Accounting Education. 23(1). pp.42-53.

Hope, O. K., Thomas, W. B. and Vyas, D., 2013. Financial reporting quality of US private and

public firms. The Accounting Review. 88(5). pp.1715-1742.

Lawrence, A., 2013. Individual investors and financial disclosure. Journal of Accounting and

Economics. 56(1). pp.130-147.

Lisowsky, P. and Minnis, M., 2018. The Silent majority: Private US firms and financial reporting

choices. Chicago Booth Research Paper, (14-01).

Mio, C. ed., 2016. Integrated reporting: A new accounting disclosure. Springer.

Omar, N., Johari, Z. A. and Smith, M., 2017. Predicting fraudulent financial reporting using

artificial neural network. Journal of Financial Crime. 24(2). pp.362-387.

Tang, Q., Chen, H. and Lin, Z., 2016. How to measure country-level financial reporting quality?.

Journal of Financial Reporting and Accounting. 14(2). pp.230-265.

Williams, E. E. and Dobelman, J. A., 2017. Financial statement analysis. World Scientific Book

Chapters, pp.109-169.

Zeff, S. A., Van der Wel, F. and Camfferman, C., 2016. Company financial reporting: A

historical and comparative study of the Dutch regulatory process. Routledge.

Online

Camden Group. 2019 [Online] Available Through. <https://www.camdengroup.co.uk/about>

Books and Journals:

Ball, R., 2013. Accounting informs investors and earnings management is rife: Two

questionable beliefs. Accounting Horizons. 27(4). pp.847-853.

Bryer, R., 2013. Americanism and financial accounting theory–Part 2: The ‘modern business

enterprise’, America's transition to capitalism, and the genesis of management

accounting. Critical Perspectives on Accounting. 24(4-5). pp.273-318.

Chiang, B., Nouri, H. and Samanta, S., 2014. The effects of different teaching approaches in

introductory financial accounting. Accounting Education. 23(1). pp.42-53.

Hope, O. K., Thomas, W. B. and Vyas, D., 2013. Financial reporting quality of US private and

public firms. The Accounting Review. 88(5). pp.1715-1742.

Lawrence, A., 2013. Individual investors and financial disclosure. Journal of Accounting and

Economics. 56(1). pp.130-147.

Lisowsky, P. and Minnis, M., 2018. The Silent majority: Private US firms and financial reporting

choices. Chicago Booth Research Paper, (14-01).

Mio, C. ed., 2016. Integrated reporting: A new accounting disclosure. Springer.

Omar, N., Johari, Z. A. and Smith, M., 2017. Predicting fraudulent financial reporting using

artificial neural network. Journal of Financial Crime. 24(2). pp.362-387.

Tang, Q., Chen, H. and Lin, Z., 2016. How to measure country-level financial reporting quality?.

Journal of Financial Reporting and Accounting. 14(2). pp.230-265.

Williams, E. E. and Dobelman, J. A., 2017. Financial statement analysis. World Scientific Book

Chapters, pp.109-169.

Zeff, S. A., Van der Wel, F. and Camfferman, C., 2016. Company financial reporting: A

historical and comparative study of the Dutch regulatory process. Routledge.

Online

Camden Group. 2019 [Online] Available Through. <https://www.camdengroup.co.uk/about>

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.