Role of Accounting and Finance Departments in Tesco: Financial Decision Making

VerifiedAdded on 2023/06/10

|12

|4103

|132

AI Summary

This report explains the role of accounting and finance departments in Tesco and the utility of financial ratios to the company as well as the potential investors. Various ratios are calculated and on the basis of such calculations, valued interpretations are drawn to form a basis for the decision making regarding investment for the potential investors’ perspective.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Financial Decision Making

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

INTRODUCTION...........................................................................................................................3

MAIN BODY..................................................................................................................................3

TASK 1............................................................................................................................................3

Role of Accounting and Finance Departments............................................................................3

TASK – 2.........................................................................................................................................6

CONCLUSION..............................................................................................................................10

REFERENCES................................................................................................................................1

INTRODUCTION...........................................................................................................................3

MAIN BODY..................................................................................................................................3

TASK 1............................................................................................................................................3

Role of Accounting and Finance Departments............................................................................3

TASK – 2.........................................................................................................................................6

CONCLUSION..............................................................................................................................10

REFERENCES................................................................................................................................1

INTRODUCTION

Every entity needs to have accounting and financing department to be able to manage the

functions regarding both the departments efficiently and distribute the work load evenly on the

work force as both the departments are equally complicated and required personnel to manage.

Therefore, the following report explains the role of accounting and finance departments in Tesco.

Also, the following report explains the utility of financial ratios to the company as well as the

potential investors. Thus, various ratios are calculated and on the basis of such calculations,

valued interpretations are drawn to form a basis for the decision making regarding investment for

the potential investors’ perspective.

MAIN BODY

TASK 1

Role of Accounting and Finance Departments

1. Accounting:

a) Financial accounting function: The foremost role of accounting in the organization is to

prepare the key financial statements. There are three key or fundamental financial

statements that are prepared during accounting in a business organization like Tesco.

These statements namely are balance sheet, income statement and cash flow statement. It

is role of accounting to prepare in statements following accounting concepts and

conventions (Al-Wattar, Almagtome and Al-Shafeay, 2019). The statements prepared are

very essential for the users of the information that these depicts. The role of accounting is

to identify, classify, record, summarize the financial information for the purpose of

making it available to various stakeholders.

b) Management accounting function: Another role of accounting is to do accounting for the

management of the company. Management of Tesco requires reporting of the financial

aspects of the company to make vital decisions in order to direct the activities of the

company. Management of the company is responsible for giving directions to the efforts

of the employees and managers working with the company for accomplishing the goals

of the company (Gonçalves and Gaio, 2021). The role of accounting is to provide or

highlight the essential information for enabling the management take necessary decisions

over the financial and non-financial aspects of the company. This role very crucial as the

decisions of the top management are based on this particular role of accounting. The role

Every entity needs to have accounting and financing department to be able to manage the

functions regarding both the departments efficiently and distribute the work load evenly on the

work force as both the departments are equally complicated and required personnel to manage.

Therefore, the following report explains the role of accounting and finance departments in Tesco.

Also, the following report explains the utility of financial ratios to the company as well as the

potential investors. Thus, various ratios are calculated and on the basis of such calculations,

valued interpretations are drawn to form a basis for the decision making regarding investment for

the potential investors’ perspective.

MAIN BODY

TASK 1

Role of Accounting and Finance Departments

1. Accounting:

a) Financial accounting function: The foremost role of accounting in the organization is to

prepare the key financial statements. There are three key or fundamental financial

statements that are prepared during accounting in a business organization like Tesco.

These statements namely are balance sheet, income statement and cash flow statement. It

is role of accounting to prepare in statements following accounting concepts and

conventions (Al-Wattar, Almagtome and Al-Shafeay, 2019). The statements prepared are

very essential for the users of the information that these depicts. The role of accounting is

to identify, classify, record, summarize the financial information for the purpose of

making it available to various stakeholders.

b) Management accounting function: Another role of accounting is to do accounting for the

management of the company. Management of Tesco requires reporting of the financial

aspects of the company to make vital decisions in order to direct the activities of the

company. Management of the company is responsible for giving directions to the efforts

of the employees and managers working with the company for accomplishing the goals

of the company (Gonçalves and Gaio, 2021). The role of accounting is to provide or

highlight the essential information for enabling the management take necessary decisions

over the financial and non-financial aspects of the company. This role very crucial as the

decisions of the top management are based on this particular role of accounting. The role

is also useful in the planning process of the company. With this the company’s

management is able to identify the early symptoms of the issues that might occur and

impose its consequences over the management of the business. Strategies of the company

are formulated on the basis of the results that management accounting proposes.

c) Tax function: This role of accounting is responsible for taking care of the taxation aspect

of Tesco. It is ensured that all the rules concerned with accounting are duly taken into

consideration while accounting statements are being prepared for Tesco. There are two

aspects of tax transactions. The outcome is either tax assets or liabilities of tax being

created in the books of Tesco (Ascani, Ciccola and Chiucchi, 2021). Taxing in

accounting is originally derived from the code of internal revenue. The tax related figures

in the books of company (income statement) may happen to appear contradictory to that

represented by the tax accounting. This contradictory figures being represented are a

result of fact that there are delays and preponed decisions being made as per the rules for

tax. As per the legal point of view of a company the tax accounting is very crucial.

d) Auditing function: Gathering the information that were prepared through accounting in

the form of financial statements as per the financial accounting role the auditing function

role of accounting is executed. The statements that are prepared are verified in this role. It

is ensured that the prepared statements are capable of correctly and fairly depicting the

financial position of Tesco. Audit role of accounting is further bifurcated into two types

one is internal audit and second is external audit. Internal audit is done for checking the

capability of Tesco in maintaining its efficiency in operations that it performs (Moll and

Yigitbasioglu, 2019). Also the ability of firm is judged on the basis of its management of

accounting processes while it does so in accordance with the rules and regulations that

are recognised as a standard. Internal audit is conducted by Tesco from time to time to

make sure that strictness is being implied within the firm while following of the

administrative fundamentals. Also the utmost accuracy is ensured in the financial reports.

The independent verifications of the financial statements prepared by a company is

termed as external audit. This type of audit is conducted for the statutory determinations.

It is mandated by the compulsory provisions and legal system of the country.

2. Finance:

management is able to identify the early symptoms of the issues that might occur and

impose its consequences over the management of the business. Strategies of the company

are formulated on the basis of the results that management accounting proposes.

c) Tax function: This role of accounting is responsible for taking care of the taxation aspect

of Tesco. It is ensured that all the rules concerned with accounting are duly taken into

consideration while accounting statements are being prepared for Tesco. There are two

aspects of tax transactions. The outcome is either tax assets or liabilities of tax being

created in the books of Tesco (Ascani, Ciccola and Chiucchi, 2021). Taxing in

accounting is originally derived from the code of internal revenue. The tax related figures

in the books of company (income statement) may happen to appear contradictory to that

represented by the tax accounting. This contradictory figures being represented are a

result of fact that there are delays and preponed decisions being made as per the rules for

tax. As per the legal point of view of a company the tax accounting is very crucial.

d) Auditing function: Gathering the information that were prepared through accounting in

the form of financial statements as per the financial accounting role the auditing function

role of accounting is executed. The statements that are prepared are verified in this role. It

is ensured that the prepared statements are capable of correctly and fairly depicting the

financial position of Tesco. Audit role of accounting is further bifurcated into two types

one is internal audit and second is external audit. Internal audit is done for checking the

capability of Tesco in maintaining its efficiency in operations that it performs (Moll and

Yigitbasioglu, 2019). Also the ability of firm is judged on the basis of its management of

accounting processes while it does so in accordance with the rules and regulations that

are recognised as a standard. Internal audit is conducted by Tesco from time to time to

make sure that strictness is being implied within the firm while following of the

administrative fundamentals. Also the utmost accuracy is ensured in the financial reports.

The independent verifications of the financial statements prepared by a company is

termed as external audit. This type of audit is conducted for the statutory determinations.

It is mandated by the compulsory provisions and legal system of the country.

2. Finance:

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

a) Investment Function: The role of finance department in an organization is to perform the

investment function. Basically investment function of finance department is concerned

with taking of decision over the investment opportunities that a firm has. It may happen

that there are various alternates that are available to a firm for investment but not all

alternates are equally profitable. And a firm also cannot invest in each alternate provided

that the available resources with the firm are limited.

b) Financing Function: Merely defining the objectives and goals of the entity is not enough.

For the effective achievement of such objectives and goals, an entity requires optimum

funds to fuel the operations so as to work towards such goals. Such a tedious task of

arranging funds for the operations of the entity comes under the financing function

(Barbopoulos, Danbolt and Alexakis, 2018). Now, such funds shall be arranged on terms

and conditions which are favourable to the entity and the cost of which the entity can bear

and be profitable after that. Such financing will involve short term and long term funds of

Tesco. Such financing can be availed through various sources like own shares, bank

loans, own debentures, overdrafts of bank, commercial papers, etc. It is the responsibility

of the finance manager to avail funds from the sources which will result in the minimum

finance cost to be incurred.

c) Dividend Function: Dividend means distribution of the surplus profits of the company

among the shareholders. So, dividend function is responsible for the decisions regarding

quantum of dividend, timing of dividend, source of dividend, etc. Now, a company may

or may not declare dividend in the case of surplus profits (Dividend. 2022.). It is the

decision of the management whether to declare the dividend or not. An optimum

dividend pay-out ratio needs to be calculated to manage the surplus funds so as to earn

optimum amount of return on the surplus not distributed to the shareholders (Kilincarslan

and Ozdemir, 2018). So, Tesco’s management will be deciding whether to declare the

dividend or not and when it is declared then how much to be declared.

d) Working capital function: Working capital is the capital required to fuel the daily

operations of the entity including short term obligations (Gonçalves, Gaio and Robles,

2018). Enough working capital means the entity is able to maintain and keep running its

daily operations like payment to its employees, payment to its suppliers and meeting

other obligations like payment of taxes, payment of finance costs (What Is Working

investment function. Basically investment function of finance department is concerned

with taking of decision over the investment opportunities that a firm has. It may happen

that there are various alternates that are available to a firm for investment but not all

alternates are equally profitable. And a firm also cannot invest in each alternate provided

that the available resources with the firm are limited.

b) Financing Function: Merely defining the objectives and goals of the entity is not enough.

For the effective achievement of such objectives and goals, an entity requires optimum

funds to fuel the operations so as to work towards such goals. Such a tedious task of

arranging funds for the operations of the entity comes under the financing function

(Barbopoulos, Danbolt and Alexakis, 2018). Now, such funds shall be arranged on terms

and conditions which are favourable to the entity and the cost of which the entity can bear

and be profitable after that. Such financing will involve short term and long term funds of

Tesco. Such financing can be availed through various sources like own shares, bank

loans, own debentures, overdrafts of bank, commercial papers, etc. It is the responsibility

of the finance manager to avail funds from the sources which will result in the minimum

finance cost to be incurred.

c) Dividend Function: Dividend means distribution of the surplus profits of the company

among the shareholders. So, dividend function is responsible for the decisions regarding

quantum of dividend, timing of dividend, source of dividend, etc. Now, a company may

or may not declare dividend in the case of surplus profits (Dividend. 2022.). It is the

decision of the management whether to declare the dividend or not. An optimum

dividend pay-out ratio needs to be calculated to manage the surplus funds so as to earn

optimum amount of return on the surplus not distributed to the shareholders (Kilincarslan

and Ozdemir, 2018). So, Tesco’s management will be deciding whether to declare the

dividend or not and when it is declared then how much to be declared.

d) Working capital function: Working capital is the capital required to fuel the daily

operations of the entity including short term obligations (Gonçalves, Gaio and Robles,

2018). Enough working capital means the entity is able to maintain and keep running its

daily operations like payment to its employees, payment to its suppliers and meeting

other obligations like payment of taxes, payment of finance costs (What Is Working

Capital? How to Calculate and Why It’s Important. 2022.). Here, Tesco will have to

manage its working capital efficiently to be able to keep the business running smoothly

without any hindrance to the daily operations (Tingbani and et.al., 2020). It will be

needing working capital for the purchase of its raw material, payment to its creditors for

such purchase of raw material, payment to other creditors for other daily operations,

payment of salaries and wages to employees and labour, payment of taxes and finance

costs to the government and lenders.

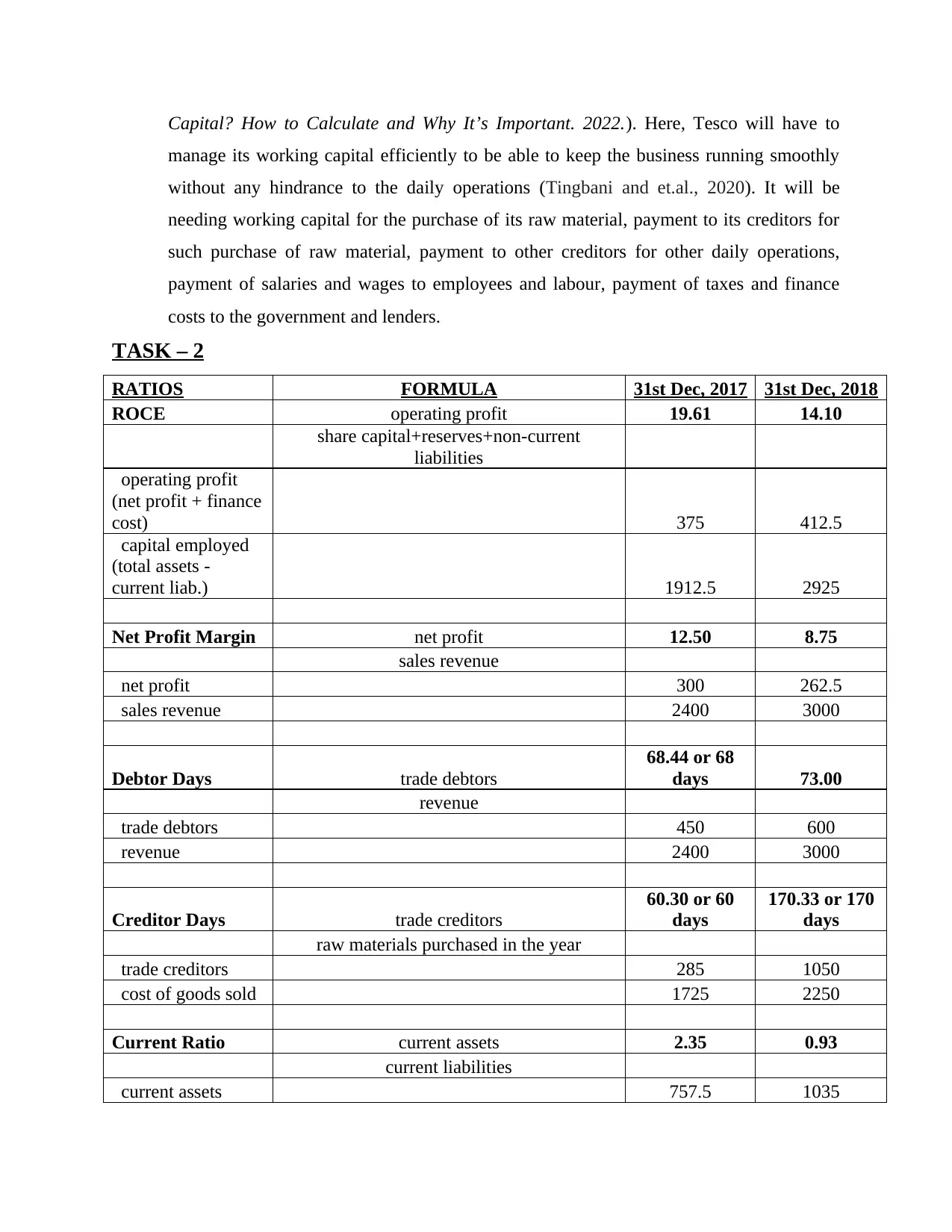

TASK – 2

RATIOS FORMULA 31st Dec, 2017 31st Dec, 2018

ROCE operating profit 19.61 14.10

share capital+reserves+non-current

liabilities

operating profit

(net profit + finance

cost) 375 412.5

capital employed

(total assets -

current liab.) 1912.5 2925

Net Profit Margin net profit 12.50 8.75

sales revenue

net profit 300 262.5

sales revenue 2400 3000

Debtor Days trade debtors

68.44 or 68

days 73.00

revenue

trade debtors 450 600

revenue 2400 3000

Creditor Days trade creditors

60.30 or 60

days

170.33 or 170

days

raw materials purchased in the year

trade creditors 285 1050

cost of goods sold 1725 2250

Current Ratio current assets 2.35 0.93

current liabilities

current assets 757.5 1035

manage its working capital efficiently to be able to keep the business running smoothly

without any hindrance to the daily operations (Tingbani and et.al., 2020). It will be

needing working capital for the purchase of its raw material, payment to its creditors for

such purchase of raw material, payment to other creditors for other daily operations,

payment of salaries and wages to employees and labour, payment of taxes and finance

costs to the government and lenders.

TASK – 2

RATIOS FORMULA 31st Dec, 2017 31st Dec, 2018

ROCE operating profit 19.61 14.10

share capital+reserves+non-current

liabilities

operating profit

(net profit + finance

cost) 375 412.5

capital employed

(total assets -

current liab.) 1912.5 2925

Net Profit Margin net profit 12.50 8.75

sales revenue

net profit 300 262.5

sales revenue 2400 3000

Debtor Days trade debtors

68.44 or 68

days 73.00

revenue

trade debtors 450 600

revenue 2400 3000

Creditor Days trade creditors

60.30 or 60

days

170.33 or 170

days

raw materials purchased in the year

trade creditors 285 1050

cost of goods sold 1725 2250

Current Ratio current assets 2.35 0.93

current liabilities

current assets 757.5 1035

current liabilities 322.5 1110

Analysing the above accounting ratios, the following inferences can be drawn regarding the

performance of Alpha Limited and the relevant change in the position of the company from 31st

December, 2017 to 31st December, 2018:

1. Return on Capital Employed –

Without going technical, the return on capital employed is a type of profitability ratio

which simply means how much percentage of return does a company is able to plough out of

the capital invested in the company. Such capital invested or capital employed can be

calculated in two ways – either deduct current liabilities from total assets which has been

done in the above calculation or add share capital, reserves & surplus and non-current

liabilities. Capital employed is owner's money invested in the business and how much a

business owner is able to earn out of its capital invested is shown by return on capital

employed (Firnanti and Karmudiandri, 2020).

As can be seen in the above table, Alpha Limited is performing unfavourably as the

return on capital employed is decreasing in the current year i.e., 31st December, 2018 from

the previous year i.e., 31st December, 2017. Figuratively, return on capital employed

decreased from 19.61% to 14.10%. Clear reason for such fall is steep hike in the capital

invested by the owner. But it shall be noted that such hike in capital invested is due to 10%

loan notes which doubled in the current year and thus capital employed shows a steep hike.

2. Net Profit Margin –

It is a type of profitability ratio that is calculated for getting insights of the profit earning

capability of the company (Madushanka and Jathurika, 2018). The net profit margin of Alpha

Ltd. indicates the ability of the company for profits in terms of part of revenue sales the

company is able to have in hand after it make payments for its variable and other overheads

in the percentage. The ratio is computed by the formula net profit divided by sales revenue

result multiplied by 100. As per the computations the net profit margin of Alpha Ltd. for the

previous year is 12.50 % which reduced to 8.75 % in the current year.

The reasons for lowering down of the profitability of the company is that even after

increase in the sales being experienced by the company the net profit generation did not

increase. Cost of sales of the company along with the finance cost are the main reason behind

Analysing the above accounting ratios, the following inferences can be drawn regarding the

performance of Alpha Limited and the relevant change in the position of the company from 31st

December, 2017 to 31st December, 2018:

1. Return on Capital Employed –

Without going technical, the return on capital employed is a type of profitability ratio

which simply means how much percentage of return does a company is able to plough out of

the capital invested in the company. Such capital invested or capital employed can be

calculated in two ways – either deduct current liabilities from total assets which has been

done in the above calculation or add share capital, reserves & surplus and non-current

liabilities. Capital employed is owner's money invested in the business and how much a

business owner is able to earn out of its capital invested is shown by return on capital

employed (Firnanti and Karmudiandri, 2020).

As can be seen in the above table, Alpha Limited is performing unfavourably as the

return on capital employed is decreasing in the current year i.e., 31st December, 2018 from

the previous year i.e., 31st December, 2017. Figuratively, return on capital employed

decreased from 19.61% to 14.10%. Clear reason for such fall is steep hike in the capital

invested by the owner. But it shall be noted that such hike in capital invested is due to 10%

loan notes which doubled in the current year and thus capital employed shows a steep hike.

2. Net Profit Margin –

It is a type of profitability ratio that is calculated for getting insights of the profit earning

capability of the company (Madushanka and Jathurika, 2018). The net profit margin of Alpha

Ltd. indicates the ability of the company for profits in terms of part of revenue sales the

company is able to have in hand after it make payments for its variable and other overheads

in the percentage. The ratio is computed by the formula net profit divided by sales revenue

result multiplied by 100. As per the computations the net profit margin of Alpha Ltd. for the

previous year is 12.50 % which reduced to 8.75 % in the current year.

The reasons for lowering down of the profitability of the company is that even after

increase in the sales being experienced by the company the net profit generation did not

increase. Cost of sales of the company along with the finance cost are the main reason behind

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

this change (Net Profit Margin, 2022). To improve the situation company can further aim at

increasing the sales through advertising. Cheaper ways to advertise must be adopted by the

company so the decision does not lead to creation of increase level of tension over the

increase in the expenses of the company. In addition to the this the company should review

its production process so that the wasteful or activities that are not required can be eliminated

in order to reduce the expenses of the company. Further the raw materials used by the

company should be either changed or purchased from some supplier other than the existing

supplier of the company so that materials can be accessed at cheaper rates.

3. Average Receivable Days / Debtors Collection Period –

Average receivable days also called as debtors collection period as the name suggests can

be defined as the number of days averagely an entity takes to collect its trade debts from its

debtors mainly, its customers (Manullang and et.al., 2020). Naturally, the lesser will be the

number of days of the collection period the better it will be because the entity will have

liquidity in its hand and meeting day to day expenditures of running the business will become

easier as compared to when the entity has very high collection period i.e., it takes numerous

days to collect its trade debts. In this case, meeting day to day expenditures of running the

business will be a tedious task along with the loss of interest income it would’ve earned on

such collection.

Now, it can be seen that Alpha Limited’s average collection period is increasing in the

current year i.e., on 31st December, 2018 as compared to the previous year i.e., on 31st

December, 2017 from 68.44 days or 68 days to 73 days. Although increase is merely of 5

days but it an unfavourable indication entity shall exercise control on such aspect because if

not controlled more increase in the long run will affect the entity adversely. Now to cope

with such increase in the average collection period, various measures can be devised like

strict adherence to the credit policies to avoid delays in collection, to set up a dedicated task

force for sole purpose of collection of debts, making available discounts on early payments

by the debtors to realize the collection faster, charging of interest on the late payments by the

debtors on trade debts to avoid delay in collection, etc.

4. Average Payable Days / Creditors Payment Period –

Average payable days also called as creditors collection period as the name suggests can

be defined as the number of days averagely an entity takes to pay its trade credits to the

increasing the sales through advertising. Cheaper ways to advertise must be adopted by the

company so the decision does not lead to creation of increase level of tension over the

increase in the expenses of the company. In addition to the this the company should review

its production process so that the wasteful or activities that are not required can be eliminated

in order to reduce the expenses of the company. Further the raw materials used by the

company should be either changed or purchased from some supplier other than the existing

supplier of the company so that materials can be accessed at cheaper rates.

3. Average Receivable Days / Debtors Collection Period –

Average receivable days also called as debtors collection period as the name suggests can

be defined as the number of days averagely an entity takes to collect its trade debts from its

debtors mainly, its customers (Manullang and et.al., 2020). Naturally, the lesser will be the

number of days of the collection period the better it will be because the entity will have

liquidity in its hand and meeting day to day expenditures of running the business will become

easier as compared to when the entity has very high collection period i.e., it takes numerous

days to collect its trade debts. In this case, meeting day to day expenditures of running the

business will be a tedious task along with the loss of interest income it would’ve earned on

such collection.

Now, it can be seen that Alpha Limited’s average collection period is increasing in the

current year i.e., on 31st December, 2018 as compared to the previous year i.e., on 31st

December, 2017 from 68.44 days or 68 days to 73 days. Although increase is merely of 5

days but it an unfavourable indication entity shall exercise control on such aspect because if

not controlled more increase in the long run will affect the entity adversely. Now to cope

with such increase in the average collection period, various measures can be devised like

strict adherence to the credit policies to avoid delays in collection, to set up a dedicated task

force for sole purpose of collection of debts, making available discounts on early payments

by the debtors to realize the collection faster, charging of interest on the late payments by the

debtors on trade debts to avoid delay in collection, etc.

4. Average Payable Days / Creditors Payment Period –

Average payable days also called as creditors collection period as the name suggests can

be defined as the number of days averagely an entity takes to pay its trade credits to the

creditors mainly, its vendors. Naturally, lesser will be the number of payable days the better

will be the liquidity position of the business. Although more time available to the entity for

the payment to the creditors the better it will be but it leads to degradation of the credit image

of the entity in the market that it always takes more time to meet its trade credit obligations

as compared to other entities in the market (Tenney and Kalenkoski, 2019). Late payments

will lead to degraded goodwill and also charging of interest on such late payments or even

legal action if any. It can also be said that it is ethical to pay its due on time specially when

the vendors or creditors are small businesses to allow them to manage their own cash flows

as well.

In the above calculation of the ratios it can be seen that average payable days of Alpha

Limited is increasing in the current year i.e., 31st December, 2018 as compared to the

previous year i.e., 31st December, 2017 from 60.30 days or 60 days to 170.33 days or 170

days (Yuliarti and Diyani, 2018). This is a serious concern as the increase is highly adverse

and this clearly shows the issue of liquidity of the Alpha Limited which can be further proven

by the analysis of current ratio which is decreasing in the current year and is below 1. Alpha

limited needs to implement serious measures to improve the payable days and manage the

liquidity of the entity in an efficient manner.

5. Current Ratio –

Current ratio is a type of liquidity ratio which shows the liquidity position of the entity to

meet its current obligations and whether the entity is able to meet its trade credit obligations

on time. A higher current ratio shows an efficient liquidity position of the entity and lower

current ratio shows that entity will have trouble meeting its trade credit obligations. Current

obligations here mean the obligations which are due to be paid within a year (Charitou and

et.al., 2018). An ideal current ratio is considered to be somewhere between 1 to 3 and the

ratio anywhere less than 1 is a serious concern because it shows that current assets are not

enough to meet the current liability obligations.

In the above calculation of the ratios it can be seen that current ratio of Alpha Limited is

decreasing in the current year i.e., year ended 31st December, 2018 as compared to the

previous year i.e., year ended 31st December, 2017 from 2.35 to 0.93. Now, the ratio in the

current ratio is less than 1 which is a serious concern as discussed earlier and the adverse

impact of this can be seen on the abnormal increase in the creditors payment period form 60

will be the liquidity position of the business. Although more time available to the entity for

the payment to the creditors the better it will be but it leads to degradation of the credit image

of the entity in the market that it always takes more time to meet its trade credit obligations

as compared to other entities in the market (Tenney and Kalenkoski, 2019). Late payments

will lead to degraded goodwill and also charging of interest on such late payments or even

legal action if any. It can also be said that it is ethical to pay its due on time specially when

the vendors or creditors are small businesses to allow them to manage their own cash flows

as well.

In the above calculation of the ratios it can be seen that average payable days of Alpha

Limited is increasing in the current year i.e., 31st December, 2018 as compared to the

previous year i.e., 31st December, 2017 from 60.30 days or 60 days to 170.33 days or 170

days (Yuliarti and Diyani, 2018). This is a serious concern as the increase is highly adverse

and this clearly shows the issue of liquidity of the Alpha Limited which can be further proven

by the analysis of current ratio which is decreasing in the current year and is below 1. Alpha

limited needs to implement serious measures to improve the payable days and manage the

liquidity of the entity in an efficient manner.

5. Current Ratio –

Current ratio is a type of liquidity ratio which shows the liquidity position of the entity to

meet its current obligations and whether the entity is able to meet its trade credit obligations

on time. A higher current ratio shows an efficient liquidity position of the entity and lower

current ratio shows that entity will have trouble meeting its trade credit obligations. Current

obligations here mean the obligations which are due to be paid within a year (Charitou and

et.al., 2018). An ideal current ratio is considered to be somewhere between 1 to 3 and the

ratio anywhere less than 1 is a serious concern because it shows that current assets are not

enough to meet the current liability obligations.

In the above calculation of the ratios it can be seen that current ratio of Alpha Limited is

decreasing in the current year i.e., year ended 31st December, 2018 as compared to the

previous year i.e., year ended 31st December, 2017 from 2.35 to 0.93. Now, the ratio in the

current ratio is less than 1 which is a serious concern as discussed earlier and the adverse

impact of this can be seen on the abnormal increase in the creditors payment period form 60

days to 170 days which clearly shows liquidity issues in the entity. Corrective measure needs

to be taken immediately to avoid the decrease of current ratio consistently as it can hamper

the day to day working of the entity in the long run (Kumsta and Vivian, 2020). Further,

Alpha limited also needs to evaluate the ratio with respect to the other competitors and

industry averages for a better understanding on the current position of the entity at the current

numbers.

Referring to the above calculations of the various ratios of Alpha Limited and further

interpretation of each of the above ratios calculated in detail it can be analysed that none of the

ratios shows a favourable indication regarding the performance of the business. All the ratios are

adverse namely –

1. Return on capital employed is decreasing in the current year which shows poor management

of funds invested in the entity by the owner and the management.

2. Net profit margin for the current year is also decreasing in the current year which again

shows poor management of revenues generated in the year.

3. Debtor days are increasing in the current year which shows delay in the collection of trade

debts and thus hindering liquidity of the entity.

4. Creditor days are increasing significantly in the current year which shows weak liquidity to

meet its trade credit obligations.

5. Current ratio has fallen below 1 in the current year which shows inability to meet the current

obligations through its current assets.

Therefore, it is not advisable to invest in such a company for the potential investors as the

performance of the company is not favourable at all.

CONCLUSION

It can be concluded that accounting and finance departments of every entity plays an

important role in their functioning which includes various functions like financial accounting

function, management accounting function, investment function, financing function, etc. Also,

the above report contains analysis of various financial ratios namely – return on capital

employed, net profit margin, debtor period, creditor period and current ratio depending on which

the decision regarding investment by the potential investors will be taken and also the

performance of the Alpha Limited will be judged.

to be taken immediately to avoid the decrease of current ratio consistently as it can hamper

the day to day working of the entity in the long run (Kumsta and Vivian, 2020). Further,

Alpha limited also needs to evaluate the ratio with respect to the other competitors and

industry averages for a better understanding on the current position of the entity at the current

numbers.

Referring to the above calculations of the various ratios of Alpha Limited and further

interpretation of each of the above ratios calculated in detail it can be analysed that none of the

ratios shows a favourable indication regarding the performance of the business. All the ratios are

adverse namely –

1. Return on capital employed is decreasing in the current year which shows poor management

of funds invested in the entity by the owner and the management.

2. Net profit margin for the current year is also decreasing in the current year which again

shows poor management of revenues generated in the year.

3. Debtor days are increasing in the current year which shows delay in the collection of trade

debts and thus hindering liquidity of the entity.

4. Creditor days are increasing significantly in the current year which shows weak liquidity to

meet its trade credit obligations.

5. Current ratio has fallen below 1 in the current year which shows inability to meet the current

obligations through its current assets.

Therefore, it is not advisable to invest in such a company for the potential investors as the

performance of the company is not favourable at all.

CONCLUSION

It can be concluded that accounting and finance departments of every entity plays an

important role in their functioning which includes various functions like financial accounting

function, management accounting function, investment function, financing function, etc. Also,

the above report contains analysis of various financial ratios namely – return on capital

employed, net profit margin, debtor period, creditor period and current ratio depending on which

the decision regarding investment by the potential investors will be taken and also the

performance of the Alpha Limited will be judged.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

REFERENCES

Books and Journals

Al-Wattar, Y. M. A., Almagtome, A. H. and Al-Shafeay, K. M., 2019. The role of integrating

hotel sustainability reporting practices into an Accounting Information System to enhance

Hotel Financial Performance: Evidence from Iraq. African Journal of Hospitality,

Tourism and Leisure. 8(5). pp.1-16.

Ascani, I., Ciccola, R. and Chiucchi, M. S., 2021. A structured literature review about the role of

management accountants in sustainability accounting and reporting. Sustainability. 13(4).

p.2357.

Barbopoulos, L. G., Danbolt, J. and Alexakis, D., 2018. The role of earnout financing on the

valuation effects of global diversification. Journal of International Business

Studies. 49(5). pp.523-551.

Charitou, A. and et.al., 2018. Non-GAAP earnings disclosures on the face of the income

statement by UK firms: The effect on market liquidity. The International Journal of

Accounting. 53(3). pp.183-202.

Firnanti, F. and Karmudiandri, A., 2020. Corporate governance and financial ratios effect on

audit report Lag. Firnanti. F. pp.15-21.

Gonçalves, T. and Gaio, C., 2021. The role of management accounting systems in global value

strategies. Journal of Business Research. 124. pp.603-609.

Gonçalves, T., Gaio, C. and Robles, F., 2018. The impact of Working Capital Management on

firm profitability in different economic cycles: Evidence from the United

Kingdom. Economics and Business Letters. 7(2). pp.70-75.

Kilincarslan, E. and Ozdemir, O., 2018. Institutional investment horizon and dividend policy: An

empirical study of UK firms. Finance research letters. 24. pp.291-300.

Kumsta, R. and Vivian, A., 2020. The financial strength anomaly in the UK: information

uncertainty or liquidity? The European Journal of Finance. 26(10). pp.925-957.

Madushanka, K. H. I. and Jathurika, M., 2018. The impact of liquidity ratios on

profitability. International Research Journal of Advanced Engineering and Science. 3(4).

pp.157-161.

Manullang, A. E. A. and et.al., 2020. The Significance of Accounts Receivable Turnover, Debt

to Equity Ratio, Current Ratio to The Probability of Manufacturing

Companies. International Journal of Social Science and Business. 4(3). pp.464-471.

Moll, J. and Yigitbasioglu, O., 2019. The role of internet-related technologies in shaping the

work of accountants: New directions for accounting research. The British Accounting

Review. 51(6). p.100833.

Tenney, J. A. and Kalenkoski, C. M., 2019. Financial ratios and financial satisfaction: Exploring

associations between objective and subjective measures of financial well-being among

older Americans. Journal of Financial Counseling and Planning. 30(2). pp.231-243.

Tingbani, I. and et.al., 2020. Working capital management and financial performance of UK

listed firms: a contingency approach. International Journal of Banking, Accounting and

Finance. 11(2). pp.173-201.

Yuliarti, A. and Diyani, L. A., 2018. The effect of firm size, financial ratios and cash flow on

stock return. The Indonesian Accounting Review. 8(2). pp.226-240.

1

Books and Journals

Al-Wattar, Y. M. A., Almagtome, A. H. and Al-Shafeay, K. M., 2019. The role of integrating

hotel sustainability reporting practices into an Accounting Information System to enhance

Hotel Financial Performance: Evidence from Iraq. African Journal of Hospitality,

Tourism and Leisure. 8(5). pp.1-16.

Ascani, I., Ciccola, R. and Chiucchi, M. S., 2021. A structured literature review about the role of

management accountants in sustainability accounting and reporting. Sustainability. 13(4).

p.2357.

Barbopoulos, L. G., Danbolt, J. and Alexakis, D., 2018. The role of earnout financing on the

valuation effects of global diversification. Journal of International Business

Studies. 49(5). pp.523-551.

Charitou, A. and et.al., 2018. Non-GAAP earnings disclosures on the face of the income

statement by UK firms: The effect on market liquidity. The International Journal of

Accounting. 53(3). pp.183-202.

Firnanti, F. and Karmudiandri, A., 2020. Corporate governance and financial ratios effect on

audit report Lag. Firnanti. F. pp.15-21.

Gonçalves, T. and Gaio, C., 2021. The role of management accounting systems in global value

strategies. Journal of Business Research. 124. pp.603-609.

Gonçalves, T., Gaio, C. and Robles, F., 2018. The impact of Working Capital Management on

firm profitability in different economic cycles: Evidence from the United

Kingdom. Economics and Business Letters. 7(2). pp.70-75.

Kilincarslan, E. and Ozdemir, O., 2018. Institutional investment horizon and dividend policy: An

empirical study of UK firms. Finance research letters. 24. pp.291-300.

Kumsta, R. and Vivian, A., 2020. The financial strength anomaly in the UK: information

uncertainty or liquidity? The European Journal of Finance. 26(10). pp.925-957.

Madushanka, K. H. I. and Jathurika, M., 2018. The impact of liquidity ratios on

profitability. International Research Journal of Advanced Engineering and Science. 3(4).

pp.157-161.

Manullang, A. E. A. and et.al., 2020. The Significance of Accounts Receivable Turnover, Debt

to Equity Ratio, Current Ratio to The Probability of Manufacturing

Companies. International Journal of Social Science and Business. 4(3). pp.464-471.

Moll, J. and Yigitbasioglu, O., 2019. The role of internet-related technologies in shaping the

work of accountants: New directions for accounting research. The British Accounting

Review. 51(6). p.100833.

Tenney, J. A. and Kalenkoski, C. M., 2019. Financial ratios and financial satisfaction: Exploring

associations between objective and subjective measures of financial well-being among

older Americans. Journal of Financial Counseling and Planning. 30(2). pp.231-243.

Tingbani, I. and et.al., 2020. Working capital management and financial performance of UK

listed firms: a contingency approach. International Journal of Banking, Accounting and

Finance. 11(2). pp.173-201.

Yuliarti, A. and Diyani, L. A., 2018. The effect of firm size, financial ratios and cash flow on

stock return. The Indonesian Accounting Review. 8(2). pp.226-240.

1

Online

Dividend. 2022. [Online]. Available through:

<https://corporatefinanceinstitute.com/resources/knowledge/finance/dividend/>

Net Profit Margin. 2022. [Online]. Available through: <

https://corporatefinanceinstitute.com/resources/knowledge/finance/net-profit-margin-

formula/>

What Is Working Capital? How to Calculate and Why It’s Important. 2022. [Online]. Available

through: <https://www.netsuite.com/portal/resource/articles/financial-management/

working-capital.shtml#:~:text=Why%20Is%20Working%20Capital%20Important,runs

%20into%20cash%20flow%20challenges.>

2

Dividend. 2022. [Online]. Available through:

<https://corporatefinanceinstitute.com/resources/knowledge/finance/dividend/>

Net Profit Margin. 2022. [Online]. Available through: <

https://corporatefinanceinstitute.com/resources/knowledge/finance/net-profit-margin-

formula/>

What Is Working Capital? How to Calculate and Why It’s Important. 2022. [Online]. Available

through: <https://www.netsuite.com/portal/resource/articles/financial-management/

working-capital.shtml#:~:text=Why%20Is%20Working%20Capital%20Important,runs

%20into%20cash%20flow%20challenges.>

2

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.