BM414 Financial Decision Making: Accounting, Finance Roles & Alpha Ltd

VerifiedAdded on 2023/06/10

|13

|3645

|107

Report

AI Summary

This report critically evaluates the roles of accounting and finance departments within an organization, focusing on Unilever plc as an example. It defines accounting and finance functions, highlighting their importance in maintaining financial records, providing insights for decision-making, and ensuring timely fund provision. The report delves into the specific roles of the accounts department, including financial, management, tax, and auditing functions, and critically assesses their contributions. Furthermore, it examines the finance department's key functions, such as investment, financing, dividend, and working capital management. The report also includes a practical task involving the calculation and interpretation of financial ratios for Alpha Limited for the years 2017 and 2018, analyzing the company's profitability, efficiency, and liquidity. Desklib provides a platform to access similar solved assignments and resources for students.

FINANCIAL DECISION

MAKING

MAKING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

MAIN BODY..................................................................................................................................4

Critical evaluation of role of Accounts department.....................................................................4

Critical evaluation of role of Finance department.......................................................................6

TASK 2............................................................................................................................................7

Calculation of ratios for Alpha limited for two years (2017 and 2018)......................................7

Interpretation and analysis of performance.................................................................................9

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

Books and Journals....................................................................................................................12

INTRODUCTION...........................................................................................................................3

MAIN BODY..................................................................................................................................4

Critical evaluation of role of Accounts department.....................................................................4

Critical evaluation of role of Finance department.......................................................................6

TASK 2............................................................................................................................................7

Calculation of ratios for Alpha limited for two years (2017 and 2018)......................................7

Interpretation and analysis of performance.................................................................................9

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

Books and Journals....................................................................................................................12

INTRODUCTION

This report is based on Unilever plc, which is popularly known as a British MNC dealing in

consumer goods and headquartered in London, United Kingdom. The company was founded in

1929 and has accessibility across 190 countries of the world.

Definition of Accounting and finance department

Accounting can be defined as the process involving identification, classification, summarization

and recording of day to day transactions concerning operations of the business in order to reveal

financial outcome at the end of the accounting period (AlDabbagh, 2020).

On the other hand, as per the definition given by Limbäck and Yahya (2021), finance function

performed by the accounting and finance department is the art of money management by making

investment with assurance that acquired funds have been allocated to several asset classes, so

that maximum returns could be generated for the investors or shareholders of the business.

Importance of accounting and finance department

Accounting function performed by accounting and finance department of Unilever is

considered to be of great importance because it allows for keeping systematic record of

its financial information generated as a result of day to day business activities. When the

financial records are up to date, the users of such records such as managers, investors,

creditors, etc. could establish effective comparison between the financial performance of

current period against the financial performance of previous years (Al Sawafi and et.al.,

2022).

The significance of finance department goes beyond the task of bookkeeping. This

department within a concern like Unilever facilitates the provision of useful insights

while making decision that have a great impact over the business in the future.

Furthermore, with respect to Unilever, the timely and adequate provision of funds for

fulfilling the requirements of business operations are ensured by finance department.

Also, collection from debtors and payments to suppliers must be done on time is ensured

by financial department within Unilever. This department is also responsible for

coordinating the monitoring of expenditures and income.

This report is based on Unilever plc, which is popularly known as a British MNC dealing in

consumer goods and headquartered in London, United Kingdom. The company was founded in

1929 and has accessibility across 190 countries of the world.

Definition of Accounting and finance department

Accounting can be defined as the process involving identification, classification, summarization

and recording of day to day transactions concerning operations of the business in order to reveal

financial outcome at the end of the accounting period (AlDabbagh, 2020).

On the other hand, as per the definition given by Limbäck and Yahya (2021), finance function

performed by the accounting and finance department is the art of money management by making

investment with assurance that acquired funds have been allocated to several asset classes, so

that maximum returns could be generated for the investors or shareholders of the business.

Importance of accounting and finance department

Accounting function performed by accounting and finance department of Unilever is

considered to be of great importance because it allows for keeping systematic record of

its financial information generated as a result of day to day business activities. When the

financial records are up to date, the users of such records such as managers, investors,

creditors, etc. could establish effective comparison between the financial performance of

current period against the financial performance of previous years (Al Sawafi and et.al.,

2022).

The significance of finance department goes beyond the task of bookkeeping. This

department within a concern like Unilever facilitates the provision of useful insights

while making decision that have a great impact over the business in the future.

Furthermore, with respect to Unilever, the timely and adequate provision of funds for

fulfilling the requirements of business operations are ensured by finance department.

Also, collection from debtors and payments to suppliers must be done on time is ensured

by financial department within Unilever. This department is also responsible for

coordinating the monitoring of expenditures and income.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

MAIN BODY

Critical evaluation of role of Accounts department

The main role of accounting department is to perform bookkeeping of day to day

business transactions. The collection and storage of financial information with respect to

transaction taking place within the organization is what the role of accounting department. The

following are the major functions or role that accounts department within Unilever performs:

Financial accounting: It refers to the utilization of accounting transaction in order to prepare

financial statements for the given period which indicates the financial performance and position

of Unilever at the end of the period. The tasks performed under this function of accounting

involves identification, classification, summarization and recording of financial transactions in

order to prepared final accounts such as income statement, balance sheet and cash flow statement

at the end of the period (Almasria and et.al., 2021). By evaluating the financial statement of past

years against the financial statements of current year, historical analysis can be established in

order to determine positive and negative deviation in financial performance and position of the

business. Therefore, there are several benefits that Unilever enjoys as a result of performing

financial accounting such as maintainance of financial records of the business in systematic

manner, determination of financial performance and position of the business through preparing

financial statements at the end of the period and establishing control over various financial

aspects of the business.

Management accounting: This accounting type is concerned with observing the financial

performance of the business along with identifying ways to improve the organisation’s overall

financial health. In such a system, the management is provided with the financial information

and resources, assisting the management in decision making process. Managers can use such

information in planning, identifying problem areas, formulating policies, and controlling. Several

techniques that accounting department uses while performing the function of management

accounting involves ratio analysis, budgeting, standard costing, marginal costing, etc. There are

many advantages accrue to Unilever as a result of performing management accounting such as

assistance in financial planning, enhancement and improvement in efficiency and

communication of useful insights to managers for making decisions pertaining to the nearest

future. However, management accounting is solely depending on financial and cost accounting

Critical evaluation of role of Accounts department

The main role of accounting department is to perform bookkeeping of day to day

business transactions. The collection and storage of financial information with respect to

transaction taking place within the organization is what the role of accounting department. The

following are the major functions or role that accounts department within Unilever performs:

Financial accounting: It refers to the utilization of accounting transaction in order to prepare

financial statements for the given period which indicates the financial performance and position

of Unilever at the end of the period. The tasks performed under this function of accounting

involves identification, classification, summarization and recording of financial transactions in

order to prepared final accounts such as income statement, balance sheet and cash flow statement

at the end of the period (Almasria and et.al., 2021). By evaluating the financial statement of past

years against the financial statements of current year, historical analysis can be established in

order to determine positive and negative deviation in financial performance and position of the

business. Therefore, there are several benefits that Unilever enjoys as a result of performing

financial accounting such as maintainance of financial records of the business in systematic

manner, determination of financial performance and position of the business through preparing

financial statements at the end of the period and establishing control over various financial

aspects of the business.

Management accounting: This accounting type is concerned with observing the financial

performance of the business along with identifying ways to improve the organisation’s overall

financial health. In such a system, the management is provided with the financial information

and resources, assisting the management in decision making process. Managers can use such

information in planning, identifying problem areas, formulating policies, and controlling. Several

techniques that accounting department uses while performing the function of management

accounting involves ratio analysis, budgeting, standard costing, marginal costing, etc. There are

many advantages accrue to Unilever as a result of performing management accounting such as

assistance in financial planning, enhancement and improvement in efficiency and

communication of useful insights to managers for making decisions pertaining to the nearest

future. However, management accounting is solely depending on financial and cost accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

and in case of no availability of reliable and appropriate records through these accounting

functions, it would leads to negative impact over the function of management accounting and

thus reduces its effectiveness.

Various components of management accounting are product costing and pricing, analysis of cash

flow, inventory analysis, analysis of production, analysis of financial leverage, accounts

receivables/payables management, budgeting, forecasting and trend analysis (Al Sawafi and

et.al., 2022).

Utilizing the financial information and resources, the management prepares internal management

reports which serves as the basis of carrying out almost all the departmental functions like

production, marketing, human resources etc. In short, management accounting is the key to all

decision making in an organisation.

Tax function: This type of accounting is concerned with accounting methods for preparing the

tax returns and statements for tax compliance. Objective of tax accounting is finding out the

taxable profit by adjusting the accounting profit i.e. the profit arrived through accounting

principles. All adjustments and workings are included in tax return, and these statements are

required for tax audit. In case when the taxable profit is more than the accounting profit, it results

in deferred tax asset, meaning the extra amount paid as tax shall be realized in the coming years.

In case the taxable profit is less than the accounting profit, deferred tax liability arises i.e. the

shortfall in tax paid is payable in coming years. Tax planning refers to methods and strategies in

order to minimize the tax outgo lawfully by capitalizing on available exemptions, deductions and

benefits. Strategies of tax analysis include analyzing post tax returns and making affordable

commitments.

Auditing function: Auditing refers to the examination of books of accounts, independently

undertaken, in order to determine the accuracy of the financial statements. It can be performed

internally by the management, or externally by an independent authority (Bialowolski, Cwynar

and Weziak-Bialowolska, 2020). This ensures that the inspection/examination is performed in a

fair manner. It is performed to ensure that the books of accounts present a true picture of the

financial performance and position of the organisation. Public listed firms are statutorily required

to get their financial statements audited by an independent auditor before they are published.

There are three types of audits-internal, external and government audits. Internal audits are

functions, it would leads to negative impact over the function of management accounting and

thus reduces its effectiveness.

Various components of management accounting are product costing and pricing, analysis of cash

flow, inventory analysis, analysis of production, analysis of financial leverage, accounts

receivables/payables management, budgeting, forecasting and trend analysis (Al Sawafi and

et.al., 2022).

Utilizing the financial information and resources, the management prepares internal management

reports which serves as the basis of carrying out almost all the departmental functions like

production, marketing, human resources etc. In short, management accounting is the key to all

decision making in an organisation.

Tax function: This type of accounting is concerned with accounting methods for preparing the

tax returns and statements for tax compliance. Objective of tax accounting is finding out the

taxable profit by adjusting the accounting profit i.e. the profit arrived through accounting

principles. All adjustments and workings are included in tax return, and these statements are

required for tax audit. In case when the taxable profit is more than the accounting profit, it results

in deferred tax asset, meaning the extra amount paid as tax shall be realized in the coming years.

In case the taxable profit is less than the accounting profit, deferred tax liability arises i.e. the

shortfall in tax paid is payable in coming years. Tax planning refers to methods and strategies in

order to minimize the tax outgo lawfully by capitalizing on available exemptions, deductions and

benefits. Strategies of tax analysis include analyzing post tax returns and making affordable

commitments.

Auditing function: Auditing refers to the examination of books of accounts, independently

undertaken, in order to determine the accuracy of the financial statements. It can be performed

internally by the management, or externally by an independent authority (Bialowolski, Cwynar

and Weziak-Bialowolska, 2020). This ensures that the inspection/examination is performed in a

fair manner. It is performed to ensure that the books of accounts present a true picture of the

financial performance and position of the organisation. Public listed firms are statutorily required

to get their financial statements audited by an independent auditor before they are published.

There are three types of audits-internal, external and government audits. Internal audits are

performed by the employees of the organisation for management use. External audit is the one

performed by an independent authority and hence provides an clear and unbiased opinion, in

contrast with internal audit. Government audits ensure that the financial statements are prepared

to report accurate taxable income and tax returns are verified.

Critical evaluation of role of Finance department

The finance department is mainly concerned with reduction of financing cost, ensuring

availability of enough funds and establishing effective planning and controlling for the purpose

of procurement and utilization of funds. The four major functions performed by finance

department are as follows:

Investment function: Under this function of finance department, managers within Unilever

decides upon how much amount is available for investment both for the long term and short -

term purposes (Limbäck and Yahya, 2021). For the long-term investment, capital is committed

for a longer period in fixed assets of the business and accordingly, these decisions have a great

impact over financial pursuits & performance of Unilever. The investment function facilitates

efficient utilization and allocation of capital through committing procured funds to several long-

term assets and other profitable activities of a concern.

Financing function: This function involves obtaining funds from external and internal sources

of finance by keeping in mind the costs associated with it. Under this function, several activities

are performed such as determination of sources & application of finance in order to make sure

that enough funds are available as and when required. Also, it is determined that from which

sources funds should be procured by keeping in mind the cost and risk factor associated with it.

For instance, equity capital is considered as a less risky source of capital while debt capital is

considered as a highly risky source of capital because both interest payment and capital

repayment is obligatory on the part of borrower. Therefore, financial planning and capital

structuring is the core of financing function performed by finance department of the company.

Also, raising funds and its effective allocation, effective use of funds through establishing

budgetary and non – budgetary control are important functions of finance department within

Unilever.

Dividend function: This function of finance department is concerned with deciding upon how

much dividend should be distributed among shareholders out of the profit generated in a year and

performed by an independent authority and hence provides an clear and unbiased opinion, in

contrast with internal audit. Government audits ensure that the financial statements are prepared

to report accurate taxable income and tax returns are verified.

Critical evaluation of role of Finance department

The finance department is mainly concerned with reduction of financing cost, ensuring

availability of enough funds and establishing effective planning and controlling for the purpose

of procurement and utilization of funds. The four major functions performed by finance

department are as follows:

Investment function: Under this function of finance department, managers within Unilever

decides upon how much amount is available for investment both for the long term and short -

term purposes (Limbäck and Yahya, 2021). For the long-term investment, capital is committed

for a longer period in fixed assets of the business and accordingly, these decisions have a great

impact over financial pursuits & performance of Unilever. The investment function facilitates

efficient utilization and allocation of capital through committing procured funds to several long-

term assets and other profitable activities of a concern.

Financing function: This function involves obtaining funds from external and internal sources

of finance by keeping in mind the costs associated with it. Under this function, several activities

are performed such as determination of sources & application of finance in order to make sure

that enough funds are available as and when required. Also, it is determined that from which

sources funds should be procured by keeping in mind the cost and risk factor associated with it.

For instance, equity capital is considered as a less risky source of capital while debt capital is

considered as a highly risky source of capital because both interest payment and capital

repayment is obligatory on the part of borrower. Therefore, financial planning and capital

structuring is the core of financing function performed by finance department of the company.

Also, raising funds and its effective allocation, effective use of funds through establishing

budgetary and non – budgetary control are important functions of finance department within

Unilever.

Dividend function: This function of finance department is concerned with deciding upon how

much dividend should be distributed among shareholders out of the profit generated in a year and

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

how much profit should be retained with the business for financing future prospects (Green,

Greene and Orsini, 2018). While deciding upon the amount of profit to be distributed among the

shareholders of the company, several factors are taken into account which involves stability of

earnings of the company, growth opportunities for a concern, cash flows or liquidity position of

the business, preferences of the shareholders and legal constraints restricting or encouraging the

payment of dividends. Therefore, this function is largely based on the earnings of Unilever and

the financial managers within all concerns are responsible for devising optimum policy related to

dividend distribution that should ensure maximization of value of the firm in the market. This is

done through determining optimum dividend payout ratio and the decision pertaining to dividend

must be taken by keeping in mind the overall objective of shareholder’s wealth maximization.

Working capital function: Working capital is that capital which indicates the amount invested

in current assets which is meant for meeting the requirements of day to day operations of a

business. Current assets provide liquidity to a concern like Unilever because it can be converted

into cash in a very short notice of no more than a year. Therefore, it is the duty of the finance

department to determine the working capital requirements of the business and make

arrangements for the same through investing required amount of capital in current assets.

Working capital requirements are determined by taking into account several factors such as

nature of business, scale of operations, seasonal factors, business and production cycle,

operational efficiency and credit policies of the business (Amos, Au-Yong and Musa, 2021).

This function must be performed with great care because both over and under estimation of

working capital requirement is dangerous for the business where former leads to idle capital

generating no profits while the latter leads to failure of the business. This is because, lack of

working capital would directly affect the day to day operations of the business.

TASK 2

Calculation of ratios for Alpha limited for two years (2017 and 2018)

Particulars Formula 31st December 2017 31st December 2018

Revenue

from sales

2400 3000

Net profit 300 262.5

Greene and Orsini, 2018). While deciding upon the amount of profit to be distributed among the

shareholders of the company, several factors are taken into account which involves stability of

earnings of the company, growth opportunities for a concern, cash flows or liquidity position of

the business, preferences of the shareholders and legal constraints restricting or encouraging the

payment of dividends. Therefore, this function is largely based on the earnings of Unilever and

the financial managers within all concerns are responsible for devising optimum policy related to

dividend distribution that should ensure maximization of value of the firm in the market. This is

done through determining optimum dividend payout ratio and the decision pertaining to dividend

must be taken by keeping in mind the overall objective of shareholder’s wealth maximization.

Working capital function: Working capital is that capital which indicates the amount invested

in current assets which is meant for meeting the requirements of day to day operations of a

business. Current assets provide liquidity to a concern like Unilever because it can be converted

into cash in a very short notice of no more than a year. Therefore, it is the duty of the finance

department to determine the working capital requirements of the business and make

arrangements for the same through investing required amount of capital in current assets.

Working capital requirements are determined by taking into account several factors such as

nature of business, scale of operations, seasonal factors, business and production cycle,

operational efficiency and credit policies of the business (Amos, Au-Yong and Musa, 2021).

This function must be performed with great care because both over and under estimation of

working capital requirement is dangerous for the business where former leads to idle capital

generating no profits while the latter leads to failure of the business. This is because, lack of

working capital would directly affect the day to day operations of the business.

TASK 2

Calculation of ratios for Alpha limited for two years (2017 and 2018)

Particulars Formula 31st December 2017 31st December 2018

Revenue

from sales

2400 3000

Net profit 300 262.5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

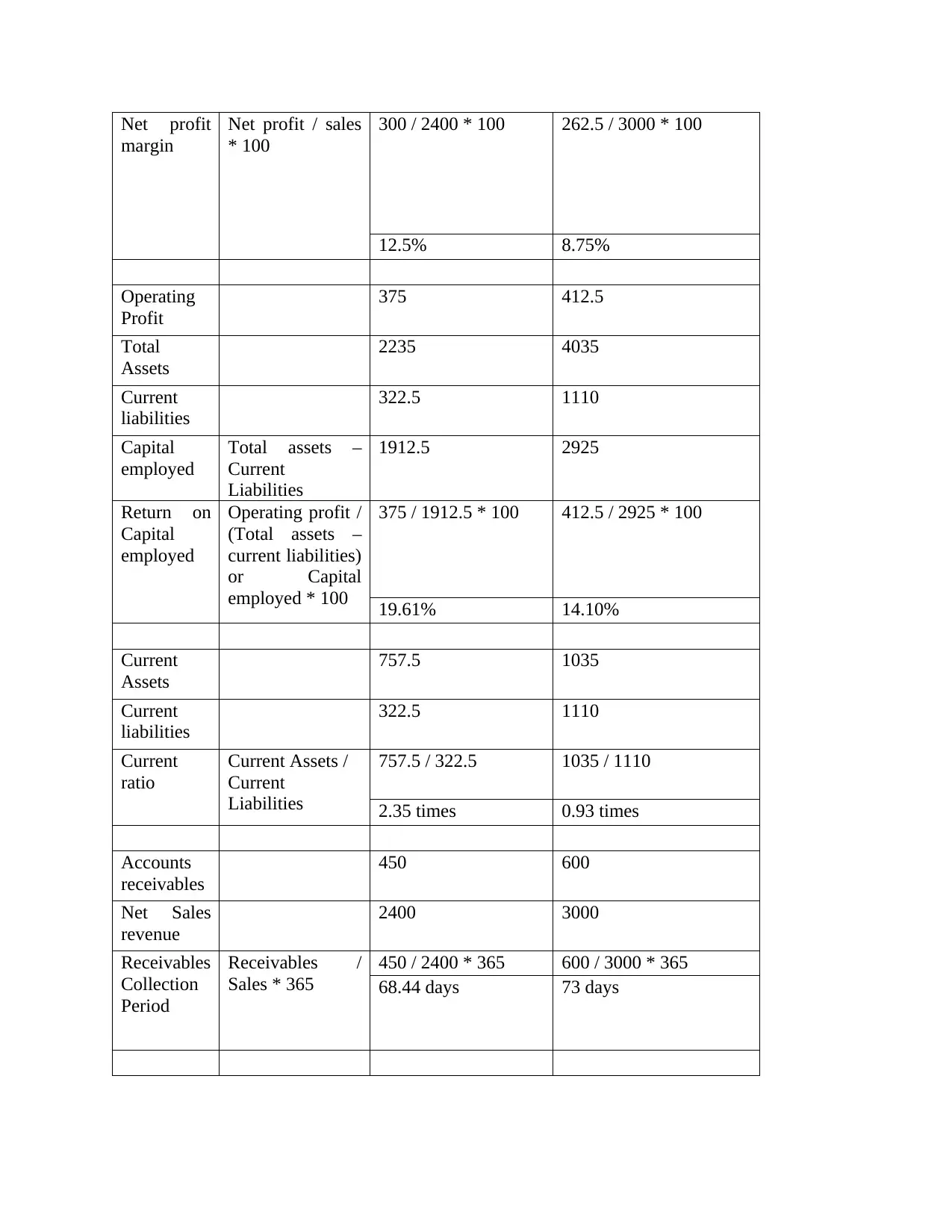

Net profit

margin

Net profit / sales

* 100

300 / 2400 * 100 262.5 / 3000 * 100

12.5% 8.75%

Operating

Profit

375 412.5

Total

Assets

2235 4035

Current

liabilities

322.5 1110

Capital

employed

Total assets –

Current

Liabilities

1912.5 2925

Return on

Capital

employed

Operating profit /

(Total assets –

current liabilities)

or Capital

employed * 100

375 / 1912.5 * 100 412.5 / 2925 * 100

19.61% 14.10%

Current

Assets

757.5 1035

Current

liabilities

322.5 1110

Current

ratio

Current Assets /

Current

Liabilities

757.5 / 322.5 1035 / 1110

2.35 times 0.93 times

Accounts

receivables

450 600

Net Sales

revenue

2400 3000

Receivables

Collection

Period

Receivables /

Sales * 365

450 / 2400 * 365 600 / 3000 * 365

68.44 days 73 days

margin

Net profit / sales

* 100

300 / 2400 * 100 262.5 / 3000 * 100

12.5% 8.75%

Operating

Profit

375 412.5

Total

Assets

2235 4035

Current

liabilities

322.5 1110

Capital

employed

Total assets –

Current

Liabilities

1912.5 2925

Return on

Capital

employed

Operating profit /

(Total assets –

current liabilities)

or Capital

employed * 100

375 / 1912.5 * 100 412.5 / 2925 * 100

19.61% 14.10%

Current

Assets

757.5 1035

Current

liabilities

322.5 1110

Current

ratio

Current Assets /

Current

Liabilities

757.5 / 322.5 1035 / 1110

2.35 times 0.93 times

Accounts

receivables

450 600

Net Sales

revenue

2400 3000

Receivables

Collection

Period

Receivables /

Sales * 365

450 / 2400 * 365 600 / 3000 * 365

68.44 days 73 days

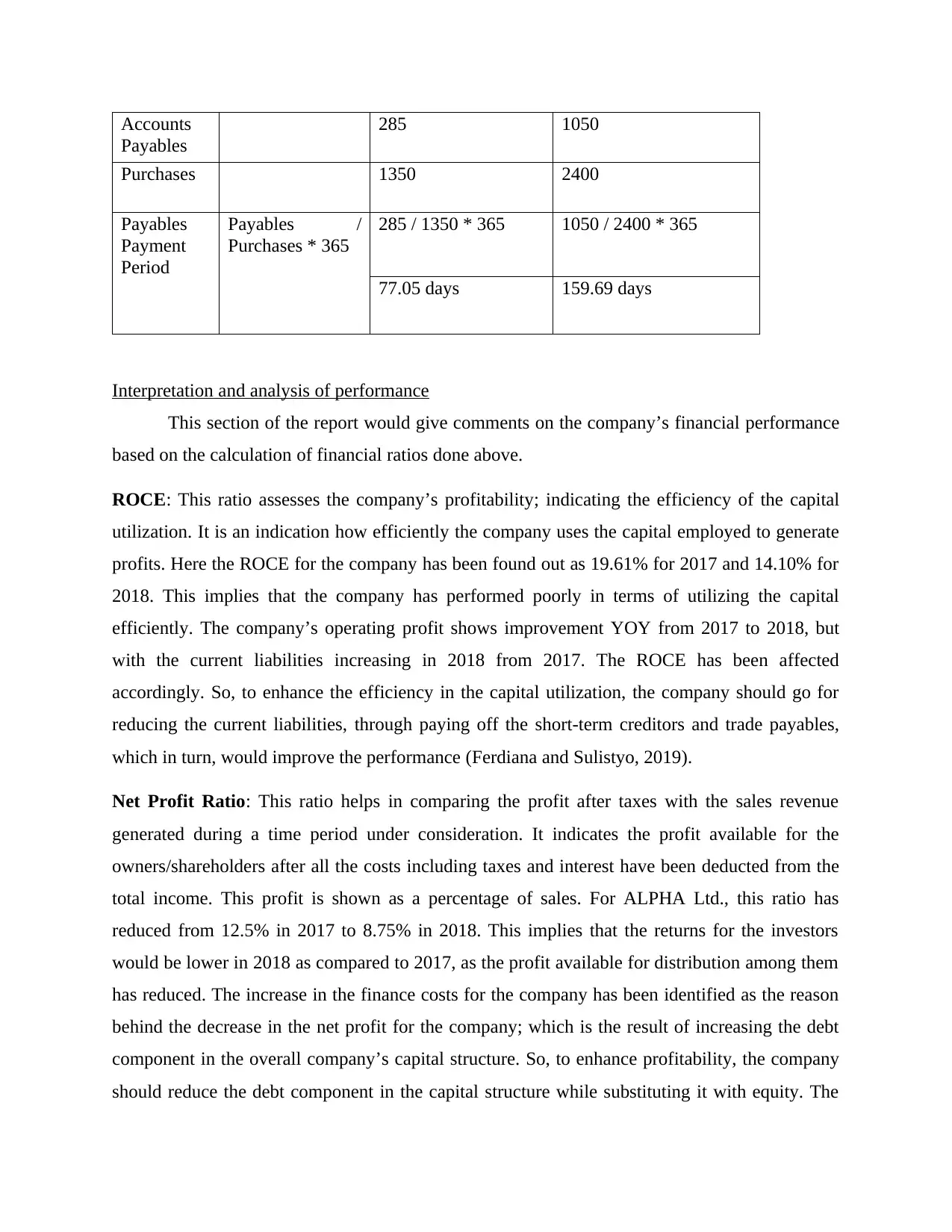

Accounts

Payables

285 1050

Purchases 1350 2400

Payables

Payment

Period

Payables /

Purchases * 365

285 / 1350 * 365 1050 / 2400 * 365

77.05 days 159.69 days

Interpretation and analysis of performance

This section of the report would give comments on the company’s financial performance

based on the calculation of financial ratios done above.

ROCE: This ratio assesses the company’s profitability; indicating the efficiency of the capital

utilization. It is an indication how efficiently the company uses the capital employed to generate

profits. Here the ROCE for the company has been found out as 19.61% for 2017 and 14.10% for

2018. This implies that the company has performed poorly in terms of utilizing the capital

efficiently. The company’s operating profit shows improvement YOY from 2017 to 2018, but

with the current liabilities increasing in 2018 from 2017. The ROCE has been affected

accordingly. So, to enhance the efficiency in the capital utilization, the company should go for

reducing the current liabilities, through paying off the short-term creditors and trade payables,

which in turn, would improve the performance (Ferdiana and Sulistyo, 2019).

Net Profit Ratio: This ratio helps in comparing the profit after taxes with the sales revenue

generated during a time period under consideration. It indicates the profit available for the

owners/shareholders after all the costs including taxes and interest have been deducted from the

total income. This profit is shown as a percentage of sales. For ALPHA Ltd., this ratio has

reduced from 12.5% in 2017 to 8.75% in 2018. This implies that the returns for the investors

would be lower in 2018 as compared to 2017, as the profit available for distribution among them

has reduced. The increase in the finance costs for the company has been identified as the reason

behind the decrease in the net profit for the company; which is the result of increasing the debt

component in the overall company’s capital structure. So, to enhance profitability, the company

should reduce the debt component in the capital structure while substituting it with equity. The

Payables

285 1050

Purchases 1350 2400

Payables

Payment

Period

Payables /

Purchases * 365

285 / 1350 * 365 1050 / 2400 * 365

77.05 days 159.69 days

Interpretation and analysis of performance

This section of the report would give comments on the company’s financial performance

based on the calculation of financial ratios done above.

ROCE: This ratio assesses the company’s profitability; indicating the efficiency of the capital

utilization. It is an indication how efficiently the company uses the capital employed to generate

profits. Here the ROCE for the company has been found out as 19.61% for 2017 and 14.10% for

2018. This implies that the company has performed poorly in terms of utilizing the capital

efficiently. The company’s operating profit shows improvement YOY from 2017 to 2018, but

with the current liabilities increasing in 2018 from 2017. The ROCE has been affected

accordingly. So, to enhance the efficiency in the capital utilization, the company should go for

reducing the current liabilities, through paying off the short-term creditors and trade payables,

which in turn, would improve the performance (Ferdiana and Sulistyo, 2019).

Net Profit Ratio: This ratio helps in comparing the profit after taxes with the sales revenue

generated during a time period under consideration. It indicates the profit available for the

owners/shareholders after all the costs including taxes and interest have been deducted from the

total income. This profit is shown as a percentage of sales. For ALPHA Ltd., this ratio has

reduced from 12.5% in 2017 to 8.75% in 2018. This implies that the returns for the investors

would be lower in 2018 as compared to 2017, as the profit available for distribution among them

has reduced. The increase in the finance costs for the company has been identified as the reason

behind the decrease in the net profit for the company; which is the result of increasing the debt

component in the overall company’s capital structure. So, to enhance profitability, the company

should reduce the debt component in the capital structure while substituting it with equity. The

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

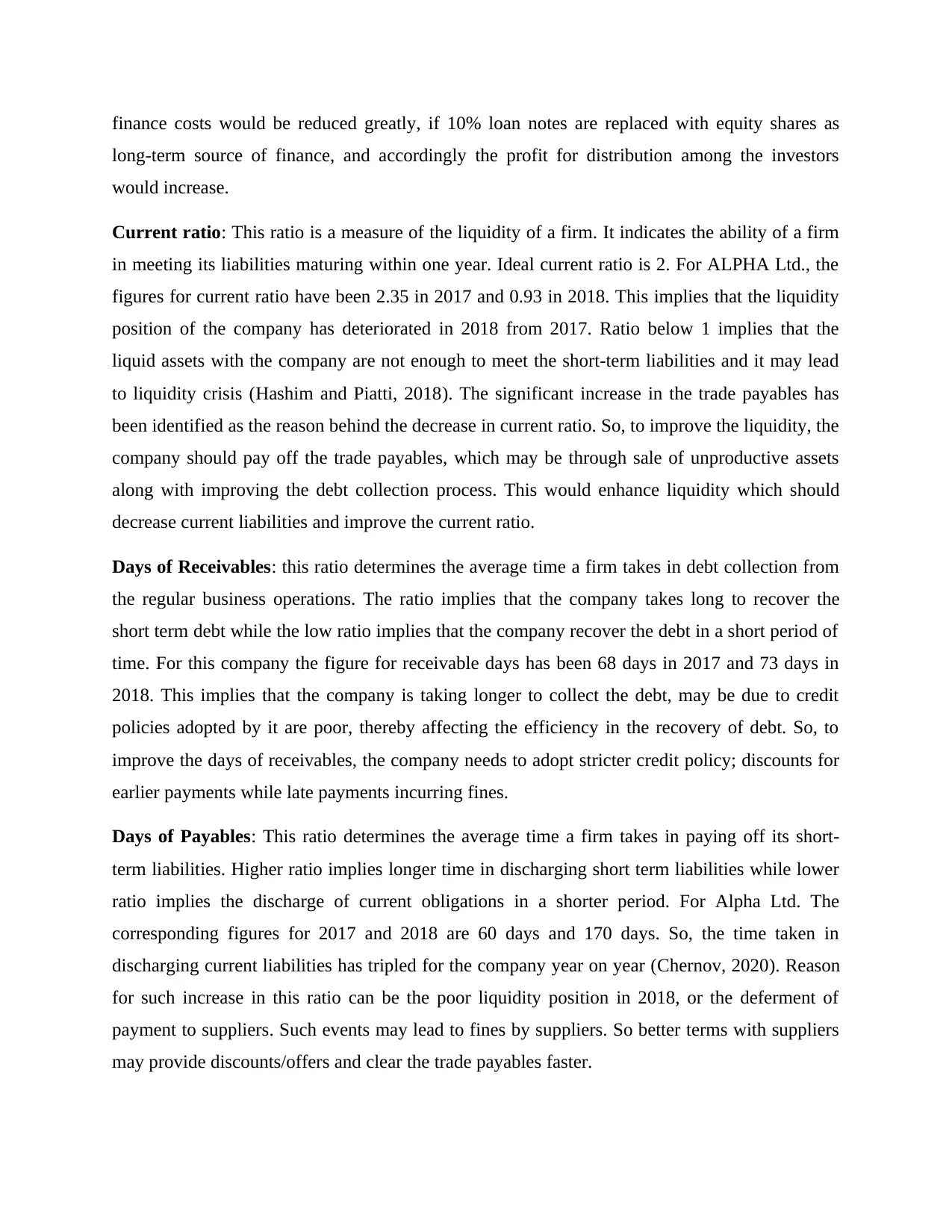

finance costs would be reduced greatly, if 10% loan notes are replaced with equity shares as

long-term source of finance, and accordingly the profit for distribution among the investors

would increase.

Current ratio: This ratio is a measure of the liquidity of a firm. It indicates the ability of a firm

in meeting its liabilities maturing within one year. Ideal current ratio is 2. For ALPHA Ltd., the

figures for current ratio have been 2.35 in 2017 and 0.93 in 2018. This implies that the liquidity

position of the company has deteriorated in 2018 from 2017. Ratio below 1 implies that the

liquid assets with the company are not enough to meet the short-term liabilities and it may lead

to liquidity crisis (Hashim and Piatti, 2018). The significant increase in the trade payables has

been identified as the reason behind the decrease in current ratio. So, to improve the liquidity, the

company should pay off the trade payables, which may be through sale of unproductive assets

along with improving the debt collection process. This would enhance liquidity which should

decrease current liabilities and improve the current ratio.

Days of Receivables: this ratio determines the average time a firm takes in debt collection from

the regular business operations. The ratio implies that the company takes long to recover the

short term debt while the low ratio implies that the company recover the debt in a short period of

time. For this company the figure for receivable days has been 68 days in 2017 and 73 days in

2018. This implies that the company is taking longer to collect the debt, may be due to credit

policies adopted by it are poor, thereby affecting the efficiency in the recovery of debt. So, to

improve the days of receivables, the company needs to adopt stricter credit policy; discounts for

earlier payments while late payments incurring fines.

Days of Payables: This ratio determines the average time a firm takes in paying off its short-

term liabilities. Higher ratio implies longer time in discharging short term liabilities while lower

ratio implies the discharge of current obligations in a shorter period. For Alpha Ltd. The

corresponding figures for 2017 and 2018 are 60 days and 170 days. So, the time taken in

discharging current liabilities has tripled for the company year on year (Chernov, 2020). Reason

for such increase in this ratio can be the poor liquidity position in 2018, or the deferment of

payment to suppliers. Such events may lead to fines by suppliers. So better terms with suppliers

may provide discounts/offers and clear the trade payables faster.

long-term source of finance, and accordingly the profit for distribution among the investors

would increase.

Current ratio: This ratio is a measure of the liquidity of a firm. It indicates the ability of a firm

in meeting its liabilities maturing within one year. Ideal current ratio is 2. For ALPHA Ltd., the

figures for current ratio have been 2.35 in 2017 and 0.93 in 2018. This implies that the liquidity

position of the company has deteriorated in 2018 from 2017. Ratio below 1 implies that the

liquid assets with the company are not enough to meet the short-term liabilities and it may lead

to liquidity crisis (Hashim and Piatti, 2018). The significant increase in the trade payables has

been identified as the reason behind the decrease in current ratio. So, to improve the liquidity, the

company should pay off the trade payables, which may be through sale of unproductive assets

along with improving the debt collection process. This would enhance liquidity which should

decrease current liabilities and improve the current ratio.

Days of Receivables: this ratio determines the average time a firm takes in debt collection from

the regular business operations. The ratio implies that the company takes long to recover the

short term debt while the low ratio implies that the company recover the debt in a short period of

time. For this company the figure for receivable days has been 68 days in 2017 and 73 days in

2018. This implies that the company is taking longer to collect the debt, may be due to credit

policies adopted by it are poor, thereby affecting the efficiency in the recovery of debt. So, to

improve the days of receivables, the company needs to adopt stricter credit policy; discounts for

earlier payments while late payments incurring fines.

Days of Payables: This ratio determines the average time a firm takes in paying off its short-

term liabilities. Higher ratio implies longer time in discharging short term liabilities while lower

ratio implies the discharge of current obligations in a shorter period. For Alpha Ltd. The

corresponding figures for 2017 and 2018 are 60 days and 170 days. So, the time taken in

discharging current liabilities has tripled for the company year on year (Chernov, 2020). Reason

for such increase in this ratio can be the poor liquidity position in 2018, or the deferment of

payment to suppliers. Such events may lead to fines by suppliers. So better terms with suppliers

may provide discounts/offers and clear the trade payables faster.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CONCLUSION

From the above report, it has been concluded that the performance of ALPHA limited as

indicates by its financial statements and ratios calculated has deteriorated in 2018 as against the

performance 2017 in terms of efficiency, liquidity and profitability as well. So, it would be

suggested to ALPHA limited that it should go reframing the policies associated with its financial

and credit activities which could improvise its performance in terms of liquidity, efficiency and

profitability. Furthermore, it has been identified that there are several roles performed by

accounting and finance department of every concern. For instance, accounting department is

responsible for performing financial accounting, management accounting, taxation function and

auditing function while finance department is responsible for taking and implementing the

decision pertaining to investment, financing, dividend and working capital management related

activities of the business.

From the above report, it has been concluded that the performance of ALPHA limited as

indicates by its financial statements and ratios calculated has deteriorated in 2018 as against the

performance 2017 in terms of efficiency, liquidity and profitability as well. So, it would be

suggested to ALPHA limited that it should go reframing the policies associated with its financial

and credit activities which could improvise its performance in terms of liquidity, efficiency and

profitability. Furthermore, it has been identified that there are several roles performed by

accounting and finance department of every concern. For instance, accounting department is

responsible for performing financial accounting, management accounting, taxation function and

auditing function while finance department is responsible for taking and implementing the

decision pertaining to investment, financing, dividend and working capital management related

activities of the business.

REFERENCES

Books and Journals

AlDabbagh, L. M., 2020. The Role of Sustainability Accounting Reporting in Assessing the

Environmental Performance of the Health Sector By applying to the Directorate of

Nineveh Health. Tikrit Journal of Administration and Economics Sciences, 16(Special

Issue part 1).

Al Sawafi, A. A. K. and et.al., 2022. THE ROLE OF MANAGERIAL ACCOUNTING IN

MAKING THE PRICING DECISION. World Bulletin of Management and Law, 7, pp.1-

11.

Almasria, N., and et.al., 2021. The role of accounting information systems in enhancing the

quality of external audit procedures. Journal of management Information and Decision

Sciences, 24(7), pp.1-23.

Limbäck, I. and Yahya, S. S., 2021. The Extent of Customer Data: A study of creating value

from customer data for the finance department.

Green, R., Greene, D. and Orsini, J., 2018. the CFO's role in accelerating systemwide

performance improvement: Finance leaders can leverage their operational expertise to

serve as catalysts for comprehensive performance improvement--a systematic approach

to increasing overall value. Healthcare Financial Management, 72(6), pp.48-54.

Amos, D., Au-Yong, C. P. and Musa, Z. N., 2021. The mediating effects of finance on the

performance of hospital facilities management services. Journal of Building

Engineering, 34, p.101899.

Ferdiana, R. and Sulistyo, S., 2019. The role of information technology usage on startup

financial management and taxation. Procedia Computer Science, 161, pp.1308-1315.

Hashim, A. and Piatti, M., 2018. Lessons from reforming financial management information

systems: a review of the evidence. World Bank Policy Research Working Paper, (8312).

Chernov, V. A., 2020. Implementation of Digital Technologies in Financial

Management. Ekonomika regiona, (1), p.283.

Books and Journals

AlDabbagh, L. M., 2020. The Role of Sustainability Accounting Reporting in Assessing the

Environmental Performance of the Health Sector By applying to the Directorate of

Nineveh Health. Tikrit Journal of Administration and Economics Sciences, 16(Special

Issue part 1).

Al Sawafi, A. A. K. and et.al., 2022. THE ROLE OF MANAGERIAL ACCOUNTING IN

MAKING THE PRICING DECISION. World Bulletin of Management and Law, 7, pp.1-

11.

Almasria, N., and et.al., 2021. The role of accounting information systems in enhancing the

quality of external audit procedures. Journal of management Information and Decision

Sciences, 24(7), pp.1-23.

Limbäck, I. and Yahya, S. S., 2021. The Extent of Customer Data: A study of creating value

from customer data for the finance department.

Green, R., Greene, D. and Orsini, J., 2018. the CFO's role in accelerating systemwide

performance improvement: Finance leaders can leverage their operational expertise to

serve as catalysts for comprehensive performance improvement--a systematic approach

to increasing overall value. Healthcare Financial Management, 72(6), pp.48-54.

Amos, D., Au-Yong, C. P. and Musa, Z. N., 2021. The mediating effects of finance on the

performance of hospital facilities management services. Journal of Building

Engineering, 34, p.101899.

Ferdiana, R. and Sulistyo, S., 2019. The role of information technology usage on startup

financial management and taxation. Procedia Computer Science, 161, pp.1308-1315.

Hashim, A. and Piatti, M., 2018. Lessons from reforming financial management information

systems: a review of the evidence. World Bank Policy Research Working Paper, (8312).

Chernov, V. A., 2020. Implementation of Digital Technologies in Financial

Management. Ekonomika regiona, (1), p.283.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.