Financial Analysis and Investment Appraisal for ABC Consulting LLP

VerifiedAdded on 2020/12/29

|20

|4779

|73

Report

AI Summary

This report presents a financial analysis of ABC Consulting LLP, focusing on its performance and potential for expansion. It examines the company's financial statements, including the Statement of Profit or Loss, Statement of Financial Position, and Statement of Cash Flows, to assess profitability, liquidity, and cash flow management. The analysis includes key financial ratios such as gross profit margin, net profit ratio, current ratio, and return on assets. Furthermore, the report applies investment appraisal techniques to evaluate the feasibility of expansion into the Australian market and discusses the sources of finance and non-financial factors influencing the firm's operations. The analysis reveals a decrease in profitability in the recent financial year, prompting recommendations for cost control. The report also provides a segmental analysis of the UK and US markets, highlighting performance differences and areas for improvement. Overall, the report provides a comprehensive overview of ABC Consulting LLP's financial health and strategic considerations for future growth.

FINANCIAL DECISION

MAKING

MAKING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

EXECUTIVE SUMMARY

Decision-making particularly in financial perspective is for any company. Present report

deals with ABC Consulting LLP which is engaged in providing financial services. It is planning

to expand in Eastern market as it has established its position and profits that can be attained.

Seeking this, it can be summarized that financial statements have been analysed and company

needs to perform well because profitability has decreased. Moreover, it is performing good in the

US market. Investment appraisal techniques are applied for making analysis whether investment

would be feasible in Australian market or not. Furthermore, sources of finance and non-financial

factors are also explained with regards to firm's nature of operations.

Decision-making particularly in financial perspective is for any company. Present report

deals with ABC Consulting LLP which is engaged in providing financial services. It is planning

to expand in Eastern market as it has established its position and profits that can be attained.

Seeking this, it can be summarized that financial statements have been analysed and company

needs to perform well because profitability has decreased. Moreover, it is performing good in the

US market. Investment appraisal techniques are applied for making analysis whether investment

would be feasible in Australian market or not. Furthermore, sources of finance and non-financial

factors are also explained with regards to firm's nature of operations.

TABLE OF CONTENTS

PART 1- Business Performance Analysis.......................................................................................1

Statement of Profit or Loss (SPL)..........................................................................................1

Statement of Financial Position (SFP)...................................................................................2

Statement of Cash Flows........................................................................................................4

Segmental Analysis................................................................................................................6

PART 2- Investment Appraisal........................................................................................................7

CONCLUSION................................................................................................................................7

REFERENCES................................................................................................................................8

PART 1- Business Performance Analysis.......................................................................................1

Statement of Profit or Loss (SPL)..........................................................................................1

Statement of Financial Position (SFP)...................................................................................2

Statement of Cash Flows........................................................................................................4

Segmental Analysis................................................................................................................6

PART 2- Investment Appraisal........................................................................................................7

CONCLUSION................................................................................................................................7

REFERENCES................................................................................................................................8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

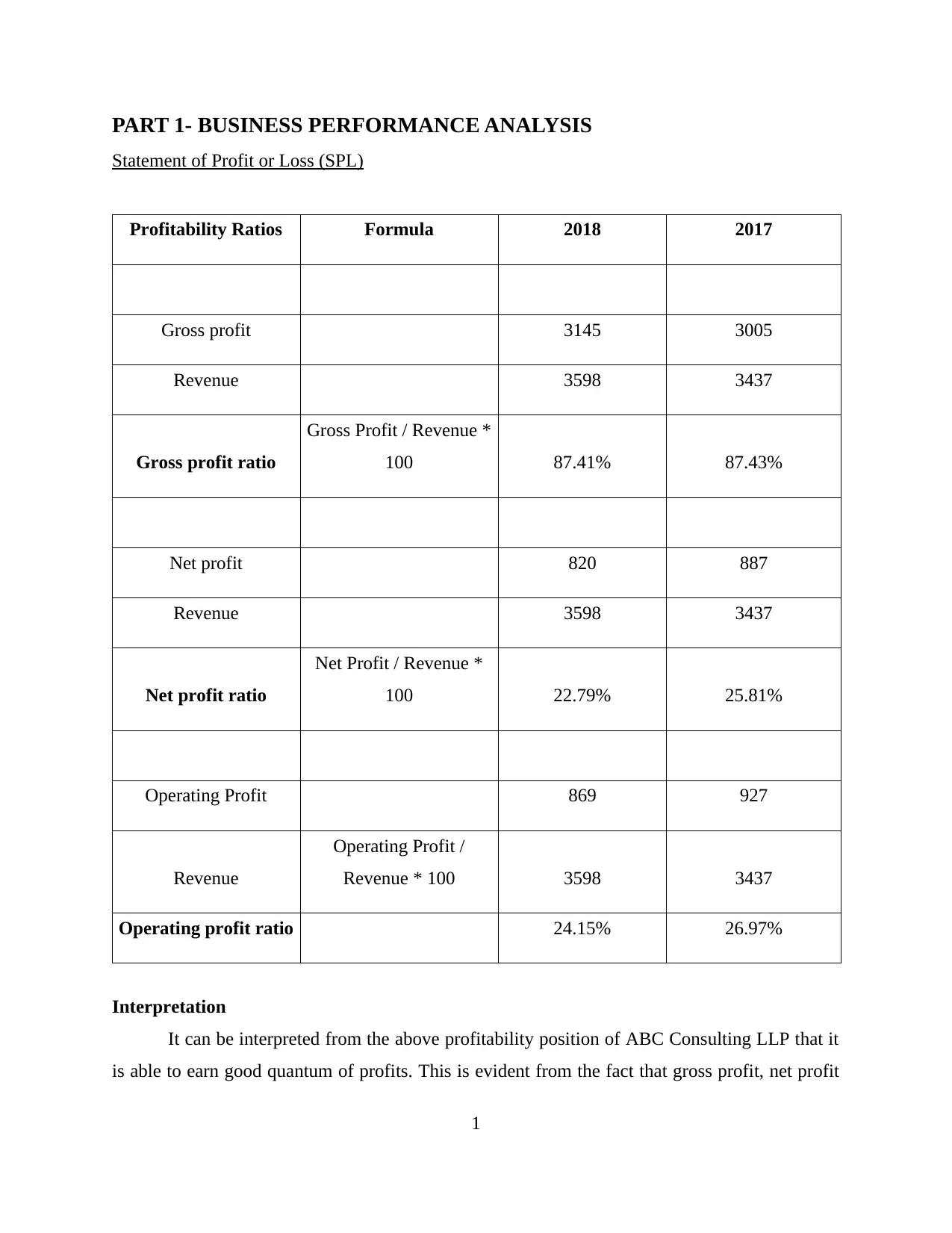

PART 1- BUSINESS PERFORMANCE ANALYSIS

Statement of Profit or Loss (SPL)

Profitability Ratios Formula 2018 2017

Gross profit 3145 3005

Revenue 3598 3437

Gross profit ratio

Gross Profit / Revenue *

100 87.41% 87.43%

Net profit 820 887

Revenue 3598 3437

Net profit ratio

Net Profit / Revenue *

100 22.79% 25.81%

Operating Profit 869 927

Revenue

Operating Profit /

Revenue * 100 3598 3437

Operating profit ratio 24.15% 26.97%

Interpretation

It can be interpreted from the above profitability position of ABC Consulting LLP that it

is able to earn good quantum of profits. This is evident from the fact that gross profit, net profit

1

Statement of Profit or Loss (SPL)

Profitability Ratios Formula 2018 2017

Gross profit 3145 3005

Revenue 3598 3437

Gross profit ratio

Gross Profit / Revenue *

100 87.41% 87.43%

Net profit 820 887

Revenue 3598 3437

Net profit ratio

Net Profit / Revenue *

100 22.79% 25.81%

Operating Profit 869 927

Revenue

Operating Profit /

Revenue * 100 3598 3437

Operating profit ratio 24.15% 26.97%

Interpretation

It can be interpreted from the above profitability position of ABC Consulting LLP that it

is able to earn good quantum of profits. This is evident from the fact that gross profit, net profit

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

and operating profit have been favourable over the past couple of years. The firm should be

profitable enough by which it may be easily expanded in the new market. It is expected to

expand in the Eastern European market and it requires that profits should be maximised in the

best possible manner by initiating overall expenses and gain desired revenue quite effectually.

By seeking the gross profit ratio, ABC Consulting LLP had earned 87.43 % in the

financial year of 2017. While, in the next year, it went down to 87.41 % which clearly shows

organization is maximising sales by eradicating expenditure up to a high extent. In relation to

this, sales in 2017 were 3437 while it reached to 3598 in 2018. This means that sales have

increased recently.

On the other hand, operating profit ratio is being calculated for the past two years. It can

be analysed that operating profit has been decreased in 2018 as compared to 2017. This may be

seen from operating profit of 927 in 2017 and 869 in next period. Hence, ratio was 26.97 % in

2017 and decreased to 24.15 % indicating difference of 2.82 % which is much reduced.

It is advised that ABC Consulting LLP should control operating expenses particularly

that are least important for maximising profits. Furthermore, net profit ratio is also computed that

shows income left after charging or deducting all operating and non-operating expenses. In

simple words, residue is achieved after reducing expenditures of company (Charitou, Karamanou

and Kopita, 2017).

It can be said that firm had accomplished net profit of 25.81 % in 2017 which reduced to

22.79 % implying significant margin. Main reason behind such decrease in profits is that overall

costs are more as compared to sales which has minimised net profit. It is recommended to ABC

Consulting LLP regarding incurring of unwanted expenses to improve profit in the best possible

manner. It can be analysed that company has been performing well but in the recent financial

year, profitability position has been somewhat decreased as margins have gone down. Hence, it

should focus on decreasing its expenses in order to maximise returns in effectual manner.

Statement of Financial Position (SFP)

Financial Ratios Formula 2018 2017

Liquidity ratios

2

profitable enough by which it may be easily expanded in the new market. It is expected to

expand in the Eastern European market and it requires that profits should be maximised in the

best possible manner by initiating overall expenses and gain desired revenue quite effectually.

By seeking the gross profit ratio, ABC Consulting LLP had earned 87.43 % in the

financial year of 2017. While, in the next year, it went down to 87.41 % which clearly shows

organization is maximising sales by eradicating expenditure up to a high extent. In relation to

this, sales in 2017 were 3437 while it reached to 3598 in 2018. This means that sales have

increased recently.

On the other hand, operating profit ratio is being calculated for the past two years. It can

be analysed that operating profit has been decreased in 2018 as compared to 2017. This may be

seen from operating profit of 927 in 2017 and 869 in next period. Hence, ratio was 26.97 % in

2017 and decreased to 24.15 % indicating difference of 2.82 % which is much reduced.

It is advised that ABC Consulting LLP should control operating expenses particularly

that are least important for maximising profits. Furthermore, net profit ratio is also computed that

shows income left after charging or deducting all operating and non-operating expenses. In

simple words, residue is achieved after reducing expenditures of company (Charitou, Karamanou

and Kopita, 2017).

It can be said that firm had accomplished net profit of 25.81 % in 2017 which reduced to

22.79 % implying significant margin. Main reason behind such decrease in profits is that overall

costs are more as compared to sales which has minimised net profit. It is recommended to ABC

Consulting LLP regarding incurring of unwanted expenses to improve profit in the best possible

manner. It can be analysed that company has been performing well but in the recent financial

year, profitability position has been somewhat decreased as margins have gone down. Hence, it

should focus on decreasing its expenses in order to maximise returns in effectual manner.

Statement of Financial Position (SFP)

Financial Ratios Formula 2018 2017

Liquidity ratios

2

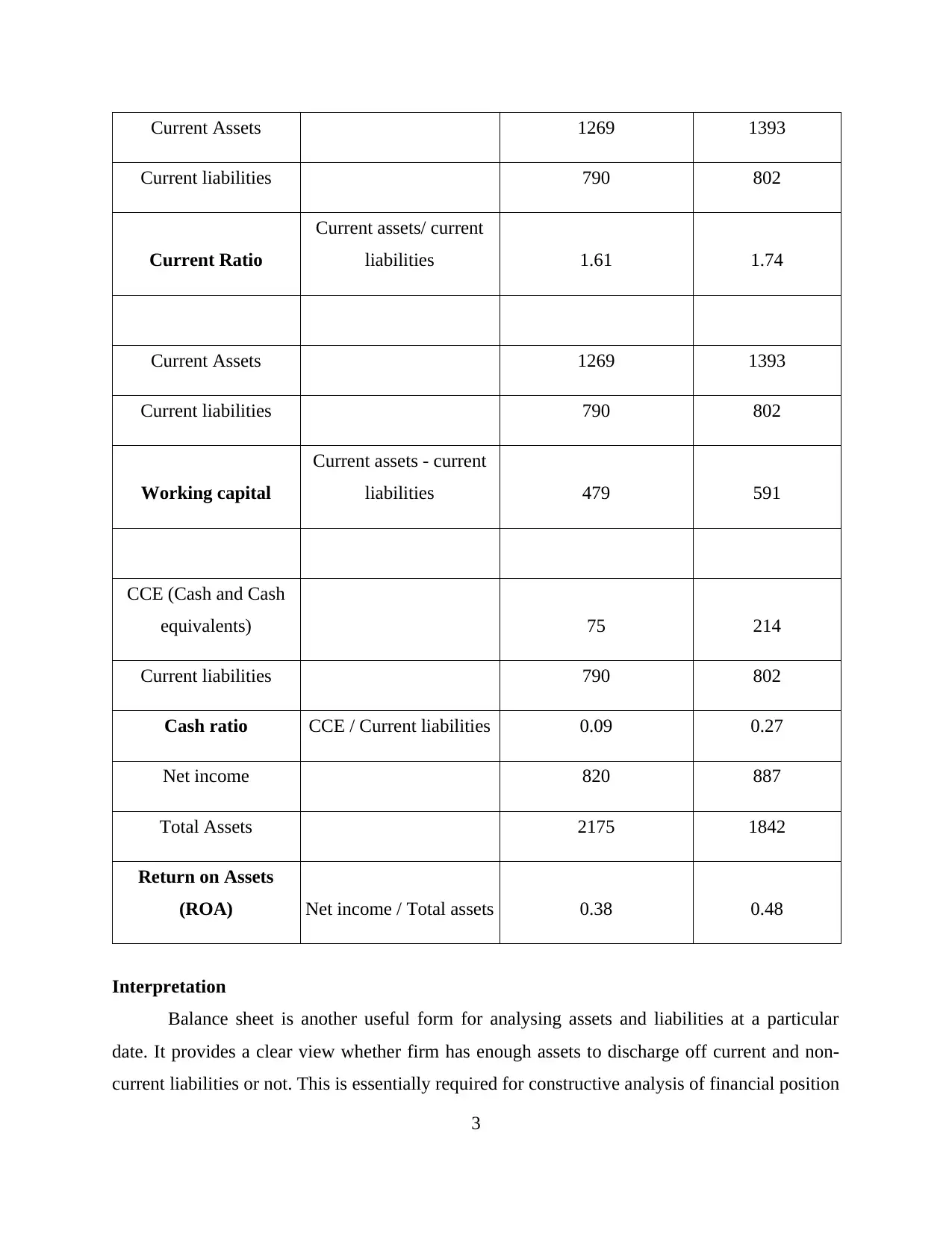

Current Assets 1269 1393

Current liabilities 790 802

Current Ratio

Current assets/ current

liabilities 1.61 1.74

Current Assets 1269 1393

Current liabilities 790 802

Working capital

Current assets - current

liabilities 479 591

CCE (Cash and Cash

equivalents) 75 214

Current liabilities 790 802

Cash ratio CCE / Current liabilities 0.09 0.27

Net income 820 887

Total Assets 2175 1842

Return on Assets

(ROA) Net income / Total assets 0.38 0.48

Interpretation

Balance sheet is another useful form for analysing assets and liabilities at a particular

date. It provides a clear view whether firm has enough assets to discharge off current and non-

current liabilities or not. This is essentially required for constructive analysis of financial position

3

Current liabilities 790 802

Current Ratio

Current assets/ current

liabilities 1.61 1.74

Current Assets 1269 1393

Current liabilities 790 802

Working capital

Current assets - current

liabilities 479 591

CCE (Cash and Cash

equivalents) 75 214

Current liabilities 790 802

Cash ratio CCE / Current liabilities 0.09 0.27

Net income 820 887

Total Assets 2175 1842

Return on Assets

(ROA) Net income / Total assets 0.38 0.48

Interpretation

Balance sheet is another useful form for analysing assets and liabilities at a particular

date. It provides a clear view whether firm has enough assets to discharge off current and non-

current liabilities or not. This is essentially required for constructive analysis of financial position

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

of company in an effectual manner. Firm has purchased PPE in 2018 which is more than

purchased in previous year. It means that investment is made by company in non-current assets.

By implementation of ratio analysis, liquidity ratio has been computed i.e. current ratio. It

can be analysed that total current assets in 2017 were 1393 which decreased to 1269 in 2018.

Current liabilities were 802 and 790 in 2017 and 2018 respectively. By applying formula, current

ratio comes to 1.74 and 1.61 in both years. In addition to this, ideal standard ratio guided by

market experts is around 2:1. However, it can be seen that the current ratio is decreased in 2018

in comparison to 2017. This means that organization will face difficulties in paying off liabilities

lapsing within time of one year.

Working capital is also calculated by subtracting current liabilities from current assets. It

can be interpreted that working capital in 2017 was 591 which decreased in the next year to 479.

This clearly implies that company has less amount of current assets for discharging current

liabilities in the business. Moreover, it is required that organization should pay-off liabilities in

effectual way which can be achieved only by enhancing working capital with much ease.

However, firm has enough quantum of total assets in 2018 amounting to 2175 while it was 1842

in 2017. Furthermore, firm will have to increase its working capital so that it may be able to

improve upon its position and also requirements of day-to-day basis that can be met quite

effectually.

Moreover, ABC Consulting LLP has enough non-current assets which have been

analysed by seeking financial statement i.e. balance sheet. It can be derived from the same that

PPE (Property, Plant and Equipment) were 370 in 2017 which increased in further year to 827

signifying that firm has made investment in the fixed assets (Gordon and et. al., 2017).

On the other side, current assets include trade receivables and cash. With relation to

receivables ratio, figures in 2017 were 1179 and it increased to 1194 in the next. While, cash has

been reduced up to an extent as figure was 214 in 2017 and reached to 75 in the last year.

Moreover, ROA is also calculated which implies that how much profit is being generated

by company by utilising its assets. The ratio in 2017 was 0.48 while it decreased to 0.38 in 2018.

Higher the ratio, better for the company. However, it can be seen that ratio has been reduced in

4

purchased in previous year. It means that investment is made by company in non-current assets.

By implementation of ratio analysis, liquidity ratio has been computed i.e. current ratio. It

can be analysed that total current assets in 2017 were 1393 which decreased to 1269 in 2018.

Current liabilities were 802 and 790 in 2017 and 2018 respectively. By applying formula, current

ratio comes to 1.74 and 1.61 in both years. In addition to this, ideal standard ratio guided by

market experts is around 2:1. However, it can be seen that the current ratio is decreased in 2018

in comparison to 2017. This means that organization will face difficulties in paying off liabilities

lapsing within time of one year.

Working capital is also calculated by subtracting current liabilities from current assets. It

can be interpreted that working capital in 2017 was 591 which decreased in the next year to 479.

This clearly implies that company has less amount of current assets for discharging current

liabilities in the business. Moreover, it is required that organization should pay-off liabilities in

effectual way which can be achieved only by enhancing working capital with much ease.

However, firm has enough quantum of total assets in 2018 amounting to 2175 while it was 1842

in 2017. Furthermore, firm will have to increase its working capital so that it may be able to

improve upon its position and also requirements of day-to-day basis that can be met quite

effectually.

Moreover, ABC Consulting LLP has enough non-current assets which have been

analysed by seeking financial statement i.e. balance sheet. It can be derived from the same that

PPE (Property, Plant and Equipment) were 370 in 2017 which increased in further year to 827

signifying that firm has made investment in the fixed assets (Gordon and et. al., 2017).

On the other side, current assets include trade receivables and cash. With relation to

receivables ratio, figures in 2017 were 1179 and it increased to 1194 in the next. While, cash has

been reduced up to an extent as figure was 214 in 2017 and reached to 75 in the last year.

Moreover, ROA is also calculated which implies that how much profit is being generated

by company by utilising its assets. The ratio in 2017 was 0.48 while it decreased to 0.38 in 2018.

Higher the ratio, better for the company. However, it can be seen that ratio has been reduced in

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

the past year which implies that firm is not adequately using its assets for generating higher

amount of profits.

Statement of Cash Flows

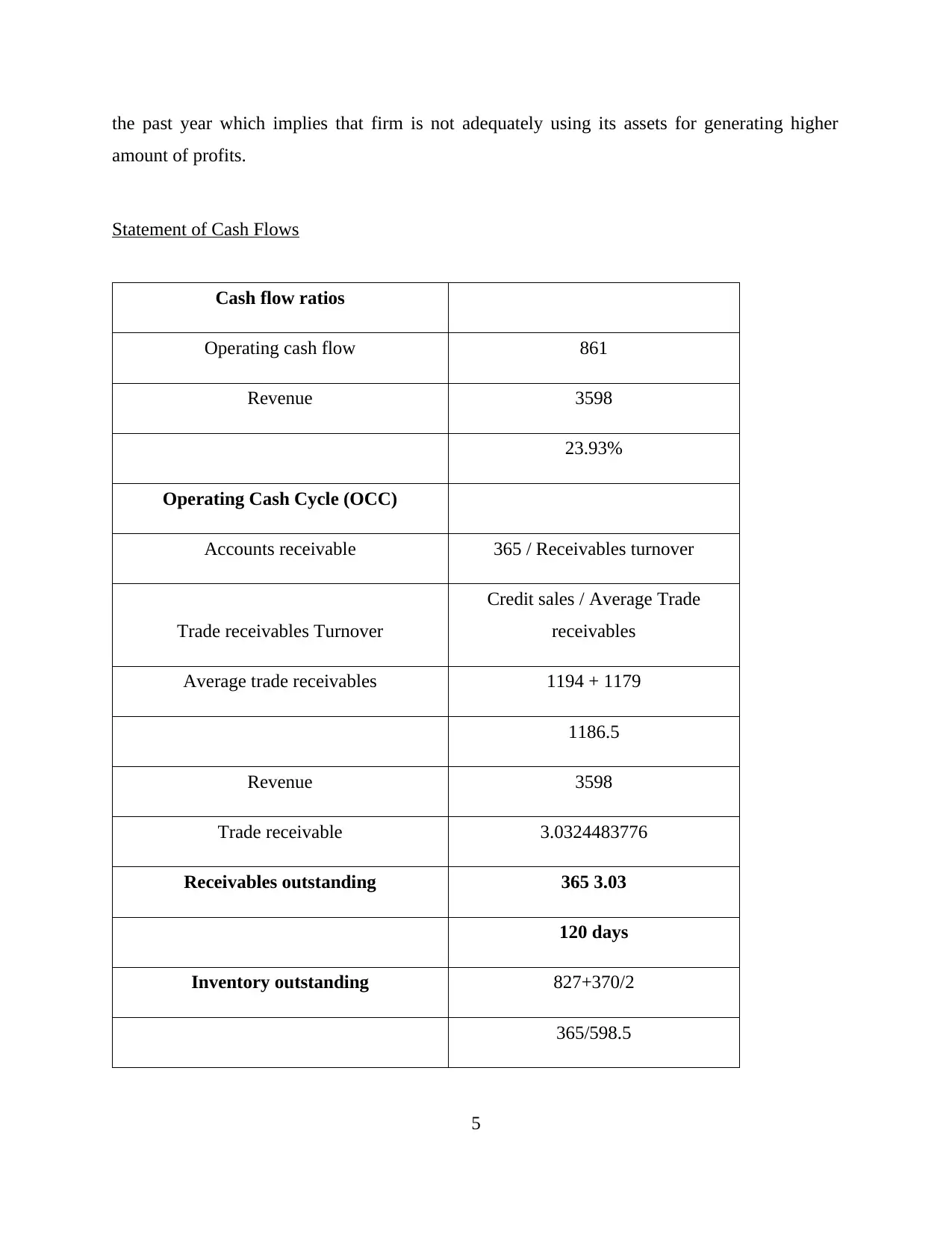

Cash flow ratios

Operating cash flow 861

Revenue 3598

23.93%

Operating Cash Cycle (OCC)

Accounts receivable 365 / Receivables turnover

Trade receivables Turnover

Credit sales / Average Trade

receivables

Average trade receivables 1194 + 1179

1186.5

Revenue 3598

Trade receivable 3.0324483776

Receivables outstanding 365 3.03

120 days

Inventory outstanding 827+370/2

365/598.5

5

amount of profits.

Statement of Cash Flows

Cash flow ratios

Operating cash flow 861

Revenue 3598

23.93%

Operating Cash Cycle (OCC)

Accounts receivable 365 / Receivables turnover

Trade receivables Turnover

Credit sales / Average Trade

receivables

Average trade receivables 1194 + 1179

1186.5

Revenue 3598

Trade receivable 3.0324483776

Receivables outstanding 365 3.03

120 days

Inventory outstanding 827+370/2

365/598.5

5

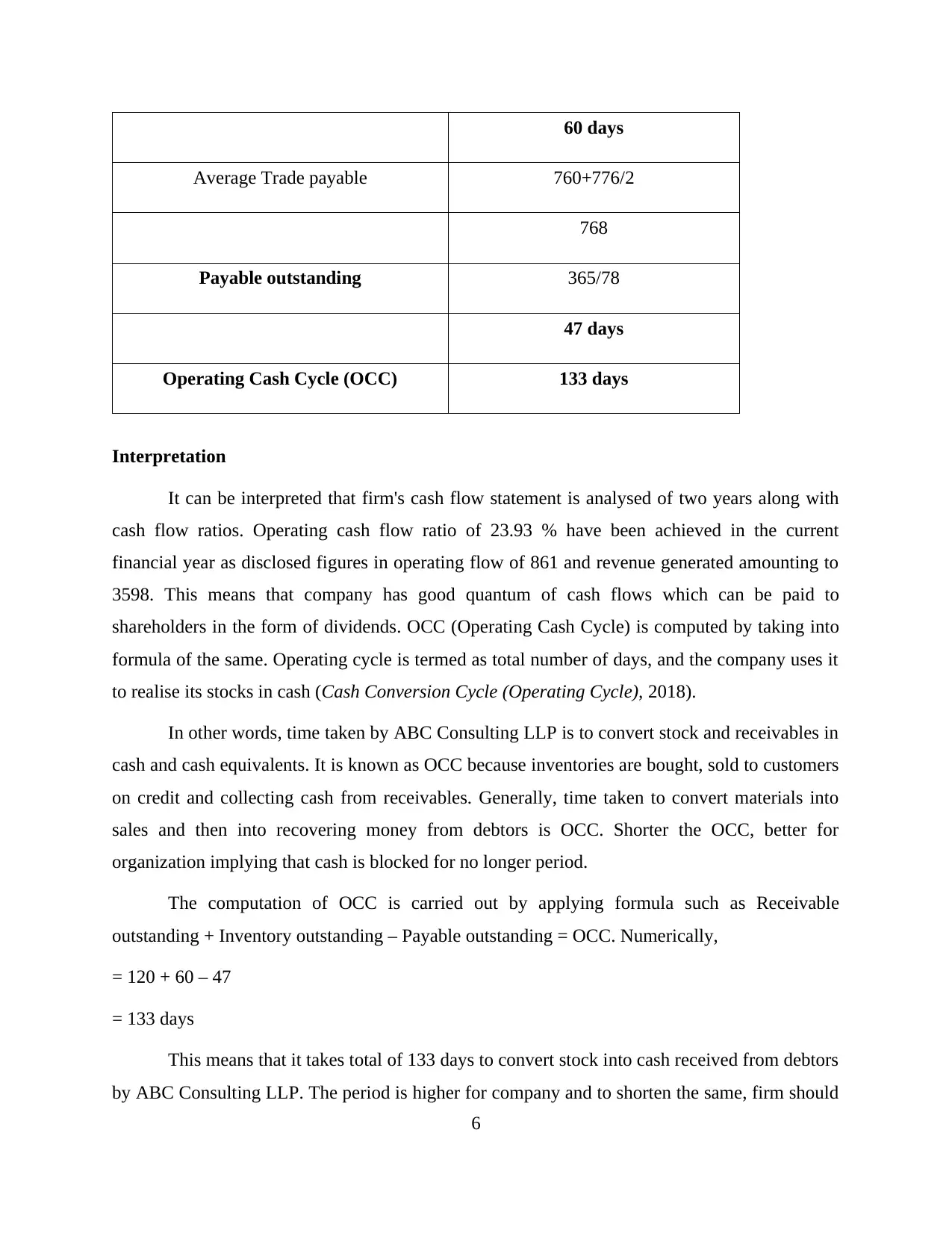

60 days

Average Trade payable 760+776/2

768

Payable outstanding 365/78

47 days

Operating Cash Cycle (OCC) 133 days

Interpretation

It can be interpreted that firm's cash flow statement is analysed of two years along with

cash flow ratios. Operating cash flow ratio of 23.93 % have been achieved in the current

financial year as disclosed figures in operating flow of 861 and revenue generated amounting to

3598. This means that company has good quantum of cash flows which can be paid to

shareholders in the form of dividends. OCC (Operating Cash Cycle) is computed by taking into

formula of the same. Operating cycle is termed as total number of days, and the company uses it

to realise its stocks in cash (Cash Conversion Cycle (Operating Cycle), 2018).

In other words, time taken by ABC Consulting LLP is to convert stock and receivables in

cash and cash equivalents. It is known as OCC because inventories are bought, sold to customers

on credit and collecting cash from receivables. Generally, time taken to convert materials into

sales and then into recovering money from debtors is OCC. Shorter the OCC, better for

organization implying that cash is blocked for no longer period.

The computation of OCC is carried out by applying formula such as Receivable

outstanding + Inventory outstanding – Payable outstanding = OCC. Numerically,

= 120 + 60 – 47

= 133 days

This means that it takes total of 133 days to convert stock into cash received from debtors

by ABC Consulting LLP. The period is higher for company and to shorten the same, firm should

6

Average Trade payable 760+776/2

768

Payable outstanding 365/78

47 days

Operating Cash Cycle (OCC) 133 days

Interpretation

It can be interpreted that firm's cash flow statement is analysed of two years along with

cash flow ratios. Operating cash flow ratio of 23.93 % have been achieved in the current

financial year as disclosed figures in operating flow of 861 and revenue generated amounting to

3598. This means that company has good quantum of cash flows which can be paid to

shareholders in the form of dividends. OCC (Operating Cash Cycle) is computed by taking into

formula of the same. Operating cycle is termed as total number of days, and the company uses it

to realise its stocks in cash (Cash Conversion Cycle (Operating Cycle), 2018).

In other words, time taken by ABC Consulting LLP is to convert stock and receivables in

cash and cash equivalents. It is known as OCC because inventories are bought, sold to customers

on credit and collecting cash from receivables. Generally, time taken to convert materials into

sales and then into recovering money from debtors is OCC. Shorter the OCC, better for

organization implying that cash is blocked for no longer period.

The computation of OCC is carried out by applying formula such as Receivable

outstanding + Inventory outstanding – Payable outstanding = OCC. Numerically,

= 120 + 60 – 47

= 133 days

This means that it takes total of 133 days to convert stock into cash received from debtors

by ABC Consulting LLP. The period is higher for company and to shorten the same, firm should

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

use inventories in quick manner and also it should apply strict credit policies so that cash can be

collected from debtors with much ease.

On the other hand, firm has made payments to members (partners) amounting to 668 in

2017 while, in next year, it has paid 551 to partners' capital account. The payment has been

reduced despite of good opening balance of 447 in 2018. However, profit for the year is

minimised amounting to 820 which was 887 in 2017. This is the reason for making less payment

to members which is feasible and appropriate as profits are decreased (Yang and et. al., 2018).

Segmental Analysis

UK-

It can be analysed from the above figures that net revenue has been increased in

comparison to 2017. Figure was 2207 in 2017 which got increased to 2251. However, operating

expenses have maximised leading to affect operating profits of company up to a major extent. It

can be analysed that operating expenditures were 1522 and 1674 in past consecutive years. Staff

costs are maximised as well by 33 in comparison to previous year. This means that UK's segment

ratios are calculated of gross profit margin was 45.58 % in 2017 while, increased to 45.18 % in

2018. This shows that margin has decreased in the current year. Operating margin was 33.53 %

signifying that company has initiated good control over operational expenditures. But ratio

reached to 25.63 % in 2018 having much difference as compared to previous year. It means that

UK segment is not performing adequately (Gitman, Juchau and Flanagan, 2015).

US-

The segmental analysis of US market is also being carried out showing whether firm is

earning profits in optimum way or not. Revenue was 324 in 2017 which increased to 553 in 2018

showing that ABC Consulting LLP is making good sales in US. Expenses and disbursements in

2018 was 49 which was 56 in the previous year. This shows that expenses have been reduced

quite effectually. Moreover, net revenue is much more in 2018 and is just double of previous

period.

Deducting operational expenses, the operating profit of 179 is achieved which was

negative in the earlier year. Seeking this, ratios of US segment are computed which are in favour

of firm. Operating margin was -7.84 % in 2017 increased to 35.52 % in 2018 implying

organization has generated good operating income leading to maximum profit. On the other

7

collected from debtors with much ease.

On the other hand, firm has made payments to members (partners) amounting to 668 in

2017 while, in next year, it has paid 551 to partners' capital account. The payment has been

reduced despite of good opening balance of 447 in 2018. However, profit for the year is

minimised amounting to 820 which was 887 in 2017. This is the reason for making less payment

to members which is feasible and appropriate as profits are decreased (Yang and et. al., 2018).

Segmental Analysis

UK-

It can be analysed from the above figures that net revenue has been increased in

comparison to 2017. Figure was 2207 in 2017 which got increased to 2251. However, operating

expenses have maximised leading to affect operating profits of company up to a major extent. It

can be analysed that operating expenditures were 1522 and 1674 in past consecutive years. Staff

costs are maximised as well by 33 in comparison to previous year. This means that UK's segment

ratios are calculated of gross profit margin was 45.58 % in 2017 while, increased to 45.18 % in

2018. This shows that margin has decreased in the current year. Operating margin was 33.53 %

signifying that company has initiated good control over operational expenditures. But ratio

reached to 25.63 % in 2018 having much difference as compared to previous year. It means that

UK segment is not performing adequately (Gitman, Juchau and Flanagan, 2015).

US-

The segmental analysis of US market is also being carried out showing whether firm is

earning profits in optimum way or not. Revenue was 324 in 2017 which increased to 553 in 2018

showing that ABC Consulting LLP is making good sales in US. Expenses and disbursements in

2018 was 49 which was 56 in the previous year. This shows that expenses have been reduced

quite effectually. Moreover, net revenue is much more in 2018 and is just double of previous

period.

Deducting operational expenses, the operating profit of 179 is achieved which was

negative in the earlier year. Seeking this, ratios of US segment are computed which are in favour

of firm. Operating margin was -7.84 % in 2017 increased to 35.52 % in 2018 implying

organization has generated good operating income leading to maximum profit. On the other

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

hand, gross margin was 32.84 % and 58.13 in 2017 and 2018 respectively. This clearly shows

that ABC Consulting LLP is earning higher profits in US market as major earnings are

accumulated from this that only leads profitability for company.

8

that ABC Consulting LLP is earning higher profits in US market as major earnings are

accumulated from this that only leads profitability for company.

8

Australia-

It can be interpreted that Australian market is also equally important for the company in

achieving profits in excess (Wu, Chen and Olson, 2014). The figures show that this segment is

not much profitable for it. This is evident from the fact because revenue was 648 in 2017 which

decreased to 516 in 2018 stating sales have gone down.

Expenses and disbursements have also increased affecting operating profit quite badly. It

was 208 in 2017 that reduced to 113. Staff costs are maximised as well which is shown by

figures. In relation to this, gross margin was 70.57 % in 2017 which decreased to 55.13 %.

Similarly, operating margin was 39.25 % in 2017 and reached failure in the next year to 28.97 %.

By considering segmental analysis, it can be interpreted that firm is better performing in US

market as profitability ratios are higher.

PART 2- INVESTMENT APPRAISAL

With the present investment, appraisal information by the Financial Director, management can

forecast about the future return of the new project planned.

Management Forecast

Exhibit 3:

1

It can be interpreted that Australian market is also equally important for the company in

achieving profits in excess (Wu, Chen and Olson, 2014). The figures show that this segment is

not much profitable for it. This is evident from the fact because revenue was 648 in 2017 which

decreased to 516 in 2018 stating sales have gone down.

Expenses and disbursements have also increased affecting operating profit quite badly. It

was 208 in 2017 that reduced to 113. Staff costs are maximised as well which is shown by

figures. In relation to this, gross margin was 70.57 % in 2017 which decreased to 55.13 %.

Similarly, operating margin was 39.25 % in 2017 and reached failure in the next year to 28.97 %.

By considering segmental analysis, it can be interpreted that firm is better performing in US

market as profitability ratios are higher.

PART 2- INVESTMENT APPRAISAL

With the present investment, appraisal information by the Financial Director, management can

forecast about the future return of the new project planned.

Management Forecast

Exhibit 3:

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.