Financial Decision Making: Ratio Analysis of Alpha Ltd's Performance

VerifiedAdded on 2023/01/11

|8

|1838

|35

Report

AI Summary

This report presents a financial analysis of Alpha Ltd, focusing on key financial ratios to assess the company's performance. The analysis includes the calculation and interpretation of Return on Capital Employed (ROCE), net profit margin, current ratio, debtors collection period, and creditors coll...

FINANCIAL DECISION

MAKING

MAKING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

TABLE OF CONTENTS..............................................................................................................2

INTRODUCTION...........................................................................................................................3

Calculation of ratios....................................................................................................................3

Performance of the ratios............................................................................................................5

CONCLUSION................................................................................................................................7

REFERENCES................................................................................................................................8

TABLE OF CONTENTS..............................................................................................................2

INTRODUCTION...........................................................................................................................3

Calculation of ratios....................................................................................................................3

Performance of the ratios............................................................................................................5

CONCLUSION................................................................................................................................7

REFERENCES................................................................................................................................8

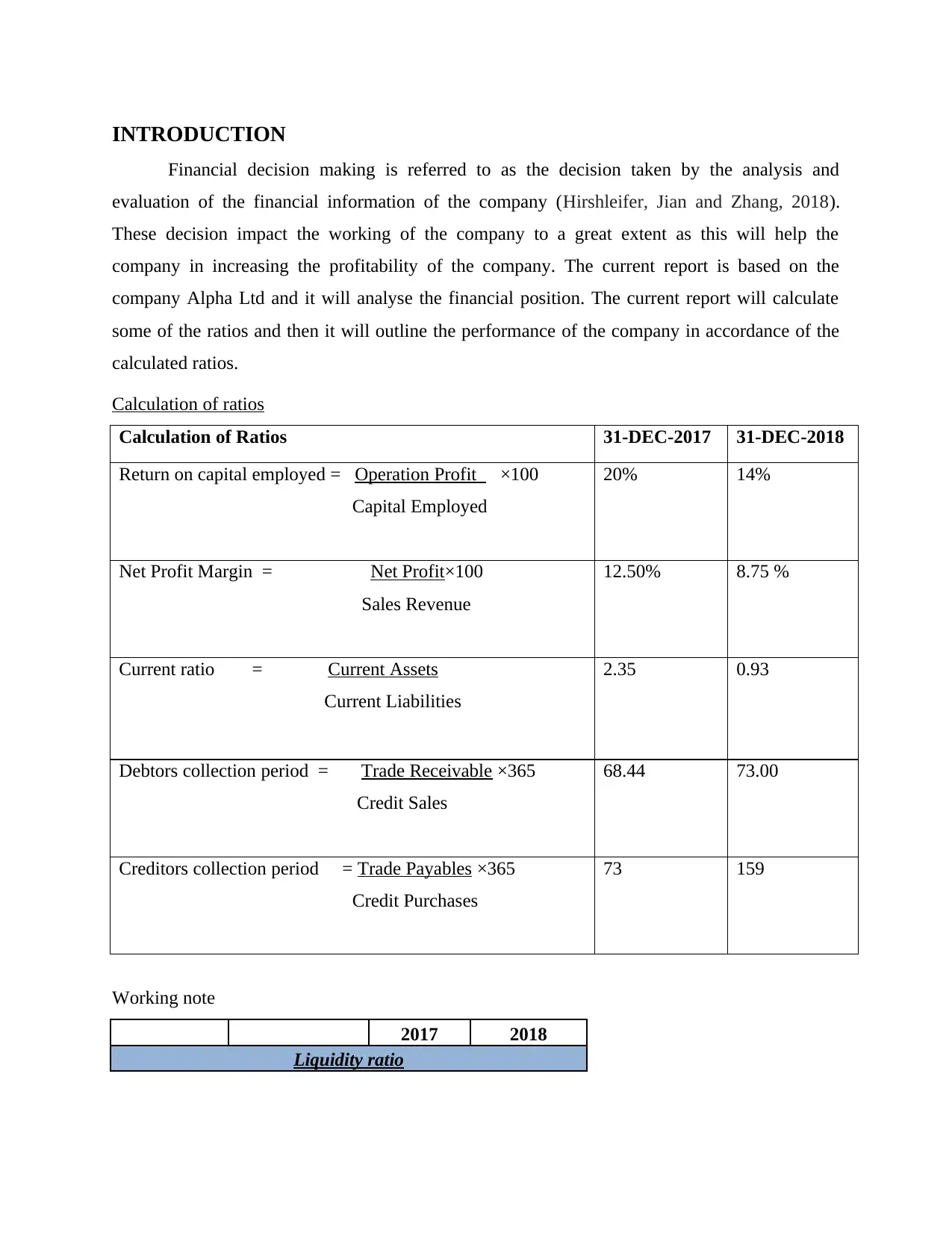

INTRODUCTION

Financial decision making is referred to as the decision taken by the analysis and

evaluation of the financial information of the company (Hirshleifer, Jian and Zhang, 2018).

These decision impact the working of the company to a great extent as this will help the

company in increasing the profitability of the company. The current report is based on the

company Alpha Ltd and it will analyse the financial position. The current report will calculate

some of the ratios and then it will outline the performance of the company in accordance of the

calculated ratios.

Calculation of ratios

Calculation of Ratios 31-DEC-2017 31-DEC-2018

Return on capital employed = Operation Profit ×100

Capital Employed

20% 14%

Net Profit Margin = Net Profit×100

Sales Revenue

12.50% 8.75 %

Current ratio = Current Assets

Current Liabilities

2.35 0.93

Debtors collection period = Trade Receivable ×365

Credit Sales

68.44 73.00

Creditors collection period = Trade Payables ×365

Credit Purchases

73 159

Working note

2017 2018

Liquidity ratio

Financial decision making is referred to as the decision taken by the analysis and

evaluation of the financial information of the company (Hirshleifer, Jian and Zhang, 2018).

These decision impact the working of the company to a great extent as this will help the

company in increasing the profitability of the company. The current report is based on the

company Alpha Ltd and it will analyse the financial position. The current report will calculate

some of the ratios and then it will outline the performance of the company in accordance of the

calculated ratios.

Calculation of ratios

Calculation of Ratios 31-DEC-2017 31-DEC-2018

Return on capital employed = Operation Profit ×100

Capital Employed

20% 14%

Net Profit Margin = Net Profit×100

Sales Revenue

12.50% 8.75 %

Current ratio = Current Assets

Current Liabilities

2.35 0.93

Debtors collection period = Trade Receivable ×365

Credit Sales

68.44 73.00

Creditors collection period = Trade Payables ×365

Credit Purchases

73 159

Working note

2017 2018

Liquidity ratio

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

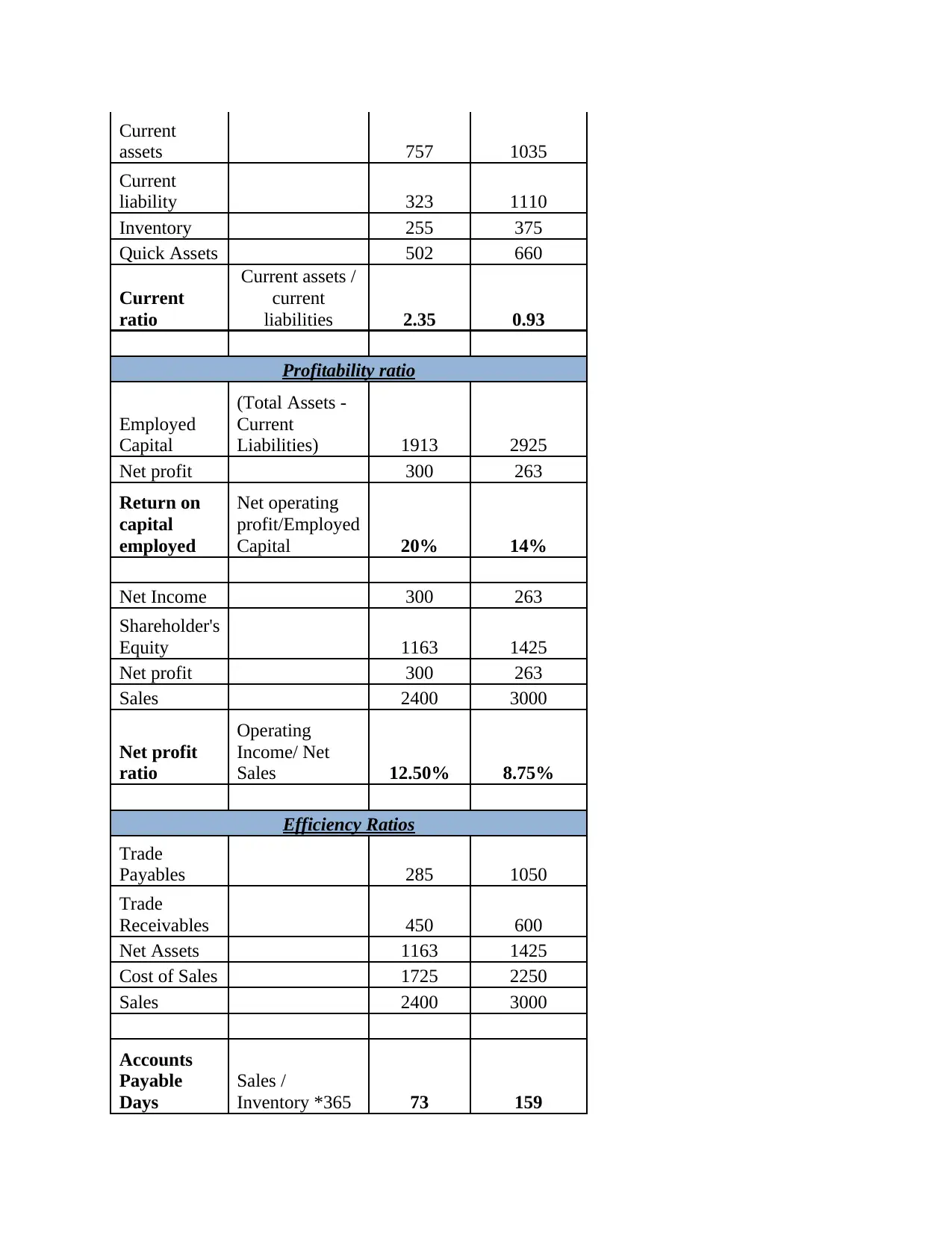

Current

assets 757 1035

Current

liability 323 1110

Inventory 255 375

Quick Assets 502 660

Current

ratio

Current assets /

current

liabilities 2.35 0.93

Profitability ratio

Employed

Capital

(Total Assets -

Current

Liabilities) 1913 2925

Net profit 300 263

Return on

capital

employed

Net operating

profit/Employed

Capital 20% 14%

Net Income 300 263

Shareholder's

Equity 1163 1425

Net profit 300 263

Sales 2400 3000

Net profit

ratio

Operating

Income/ Net

Sales 12.50% 8.75%

Efficiency Ratios

Trade

Payables 285 1050

Trade

Receivables 450 600

Net Assets 1163 1425

Cost of Sales 1725 2250

Sales 2400 3000

Accounts

Payable

Days

Sales /

Inventory *365 73 159

assets 757 1035

Current

liability 323 1110

Inventory 255 375

Quick Assets 502 660

Current

ratio

Current assets /

current

liabilities 2.35 0.93

Profitability ratio

Employed

Capital

(Total Assets -

Current

Liabilities) 1913 2925

Net profit 300 263

Return on

capital

employed

Net operating

profit/Employed

Capital 20% 14%

Net Income 300 263

Shareholder's

Equity 1163 1425

Net profit 300 263

Sales 2400 3000

Net profit

ratio

Operating

Income/ Net

Sales 12.50% 8.75%

Efficiency Ratios

Trade

Payables 285 1050

Trade

Receivables 450 600

Net Assets 1163 1425

Cost of Sales 1725 2250

Sales 2400 3000

Accounts

Payable

Days

Sales /

Inventory *365 73 159

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

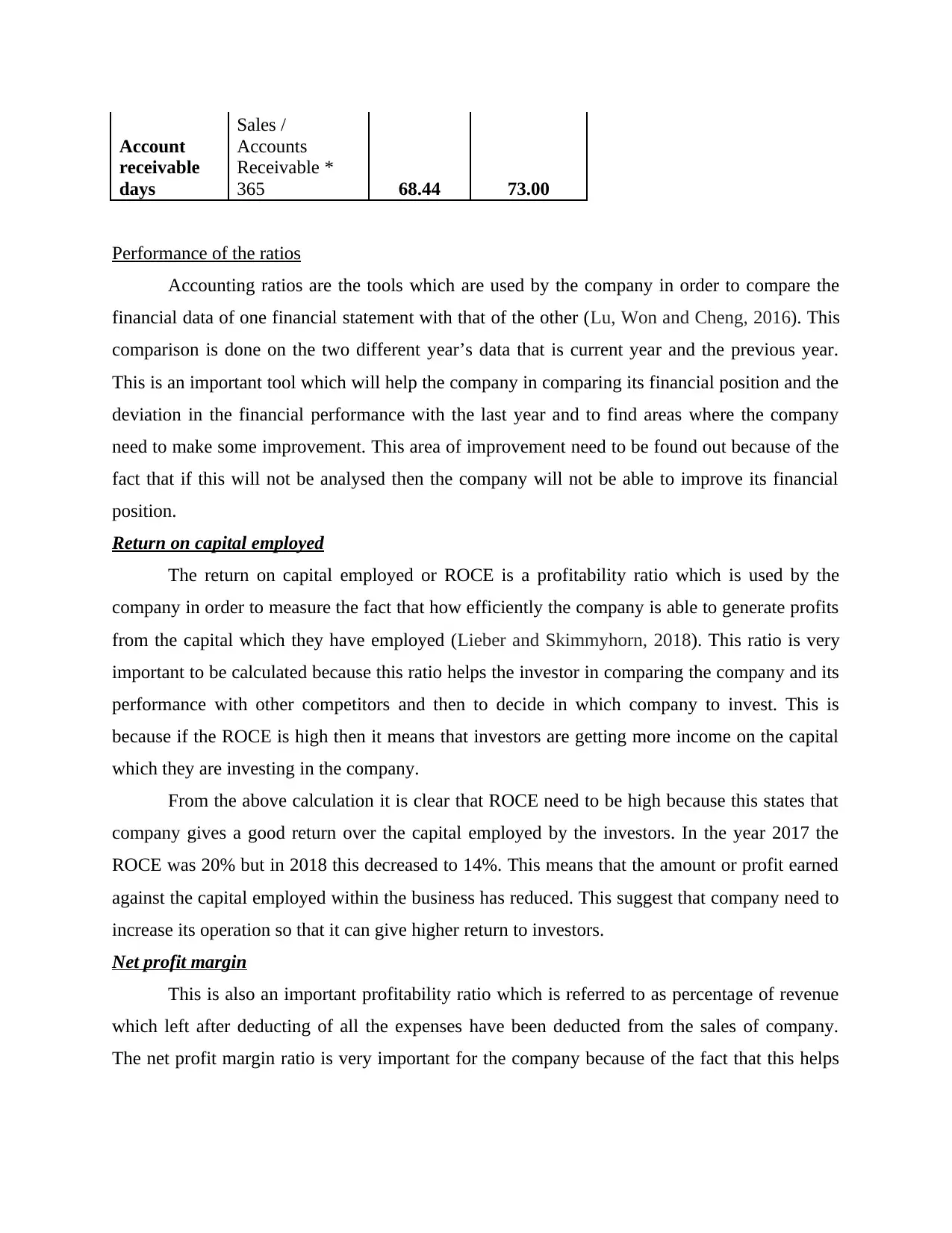

Account

receivable

days

Sales /

Accounts

Receivable *

365 68.44 73.00

Performance of the ratios

Accounting ratios are the tools which are used by the company in order to compare the

financial data of one financial statement with that of the other (Lu, Won and Cheng, 2016). This

comparison is done on the two different year’s data that is current year and the previous year.

This is an important tool which will help the company in comparing its financial position and the

deviation in the financial performance with the last year and to find areas where the company

need to make some improvement. This area of improvement need to be found out because of the

fact that if this will not be analysed then the company will not be able to improve its financial

position.

Return on capital employed

The return on capital employed or ROCE is a profitability ratio which is used by the

company in order to measure the fact that how efficiently the company is able to generate profits

from the capital which they have employed (Lieber and Skimmyhorn, 2018). This ratio is very

important to be calculated because this ratio helps the investor in comparing the company and its

performance with other competitors and then to decide in which company to invest. This is

because if the ROCE is high then it means that investors are getting more income on the capital

which they are investing in the company.

From the above calculation it is clear that ROCE need to be high because this states that

company gives a good return over the capital employed by the investors. In the year 2017 the

ROCE was 20% but in 2018 this decreased to 14%. This means that the amount or profit earned

against the capital employed within the business has reduced. This suggest that company need to

increase its operation so that it can give higher return to investors.

Net profit margin

This is also an important profitability ratio which is referred to as percentage of revenue

which left after deducting of all the expenses have been deducted from the sales of company.

The net profit margin ratio is very important for the company because of the fact that this helps

receivable

days

Sales /

Accounts

Receivable *

365 68.44 73.00

Performance of the ratios

Accounting ratios are the tools which are used by the company in order to compare the

financial data of one financial statement with that of the other (Lu, Won and Cheng, 2016). This

comparison is done on the two different year’s data that is current year and the previous year.

This is an important tool which will help the company in comparing its financial position and the

deviation in the financial performance with the last year and to find areas where the company

need to make some improvement. This area of improvement need to be found out because of the

fact that if this will not be analysed then the company will not be able to improve its financial

position.

Return on capital employed

The return on capital employed or ROCE is a profitability ratio which is used by the

company in order to measure the fact that how efficiently the company is able to generate profits

from the capital which they have employed (Lieber and Skimmyhorn, 2018). This ratio is very

important to be calculated because this ratio helps the investor in comparing the company and its

performance with other competitors and then to decide in which company to invest. This is

because if the ROCE is high then it means that investors are getting more income on the capital

which they are investing in the company.

From the above calculation it is clear that ROCE need to be high because this states that

company gives a good return over the capital employed by the investors. In the year 2017 the

ROCE was 20% but in 2018 this decreased to 14%. This means that the amount or profit earned

against the capital employed within the business has reduced. This suggest that company need to

increase its operation so that it can give higher return to investors.

Net profit margin

This is also an important profitability ratio which is referred to as percentage of revenue

which left after deducting of all the expenses have been deducted from the sales of company.

The net profit margin ratio is very important for the company because of the fact that this helps

the company in measuring overall success of the company. The higher profit margin suggests

that business is using right pricing strategies and this help company in increasing high profit.

In case of Alpha Ltd and calculation of the net profit margin it was observed that the

profitability of the company in 2017 was good as the net profit ratio was 12.50%. But this was

not in case of 2018 as in this the profit margin reduced to 8.75% and this means that the profit

earning capacity of the company reduced by 3.75% and this is not a good position. This states

that company need to take measures in improving the sales of company and this can be done

with many different steps and measures.

Current ratio

Current ratio is referred to as the liquidity ratio which is helpful for the company in

measuring the ability of the company to pay its current liabilities with the cash being made from

the current asset (Kim, Gutter and Spangler, 2017). The current ratio measurement is important

for the company because this outline the capacity of company to meet its short term liabilities

with the given current asset and cash for a period of financial year. This is calculated by

deducting the current liabilities from the current assets of the companies.

From the assessment and evaluation of the above calculation and its interpretation it is

clear that if the current ratio of the company is good then it means that company is in position of

paying of the current liabilities with their current asset only. This is in case of year 2017 wherein

the current ratio is 2.35 this means that the current assets are 2.35 times more than the current

liabilities. On the contrary in the year 2018 the current ratio decreased to 0.93 and this states that

the company has only 0.93 times the current asset more than the current liabilities. If the

liabilities are more than the company had to take loans from other people to pay off their current

liabilities.

Average collection period/ debtor collection period

The average collection period is referred to as a ratio which is calculated as the average

of the balance of account receivable by the total credit sales for a period of financial year. This is

the most important ratio for the company who rely majorly on the credit sales and the receivables

(Valaskova, Bartosova and Kubala, 2019). The major importance of this ratio for the company is

that these ratios help the company in predicting the time in which the company is able to recover

all its payment.

that business is using right pricing strategies and this help company in increasing high profit.

In case of Alpha Ltd and calculation of the net profit margin it was observed that the

profitability of the company in 2017 was good as the net profit ratio was 12.50%. But this was

not in case of 2018 as in this the profit margin reduced to 8.75% and this means that the profit

earning capacity of the company reduced by 3.75% and this is not a good position. This states

that company need to take measures in improving the sales of company and this can be done

with many different steps and measures.

Current ratio

Current ratio is referred to as the liquidity ratio which is helpful for the company in

measuring the ability of the company to pay its current liabilities with the cash being made from

the current asset (Kim, Gutter and Spangler, 2017). The current ratio measurement is important

for the company because this outline the capacity of company to meet its short term liabilities

with the given current asset and cash for a period of financial year. This is calculated by

deducting the current liabilities from the current assets of the companies.

From the assessment and evaluation of the above calculation and its interpretation it is

clear that if the current ratio of the company is good then it means that company is in position of

paying of the current liabilities with their current asset only. This is in case of year 2017 wherein

the current ratio is 2.35 this means that the current assets are 2.35 times more than the current

liabilities. On the contrary in the year 2018 the current ratio decreased to 0.93 and this states that

the company has only 0.93 times the current asset more than the current liabilities. If the

liabilities are more than the company had to take loans from other people to pay off their current

liabilities.

Average collection period/ debtor collection period

The average collection period is referred to as a ratio which is calculated as the average

of the balance of account receivable by the total credit sales for a period of financial year. This is

the most important ratio for the company who rely majorly on the credit sales and the receivables

(Valaskova, Bartosova and Kubala, 2019). The major importance of this ratio for the company is

that these ratios help the company in predicting the time in which the company is able to recover

all its payment.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

At time of calculation and its interpretation it was seen that the debtor collection period in

2017 was 68.44 but in 2018 it was 73.00. This data suggest that in the year 2017 the speed of

collecting the receivables was fast as compared to the period of 2018. But in the year 2018 it

increased to 73 which means that the speed or the time taken in receiving the due amount

reduced by 4.56 times. Hence, the performance of Alpha ltd reduced as now the company is able

to recover its money at a slow pace. Also, it is suggested to the company that as they are not able

to recover the more amount so they must stop the credit sales. This is because if credit sales will

not be done then no money needs to be recovered by the company.

Average payable days/ creditors collection period

This is an efficiency ratio which helps the company in calculating the average payment

which the company has to do for all the credit purchases they have made during the financial

period (Greenberg and Hershfield, 2019). Also, known as creditor turnover ratio this indicates

the time involved during the credit sales which is make the current liabilities outstanding fir the

company and this need to be paid. This ratio is important as this indicates the time when the

company is able to pay off all its debts and is in pure liquid position.

With help of calculation of the average payable days it was seen that in 2017 this was 70

but in the year 2018 it was 159. This suggest that in the year 2017 it was good but in the year

2018 it increased drastically which is not at all good for the company. Having this higher

collection period in 2018 suggest that the company is not able to pay off its current asset on time

and in proper manner that is full. Also, this higher number of creditor collection period suggests

that the company is not having proper communication with the consumer and because of this the

sales of company is reducing and for this the company need to take loans from other to run and

operate the business. Hence, because of this the profitability of the company reduces.

CONCLUSION

In the end it is summarised that the calculation and analysis o f the ratios is very essential

for the company in taking the financial decision. This is because the ratios help the company in

analysing the fact that where the company need to improve and this help the company in talking

the decision for the betterment of the company.

2017 was 68.44 but in 2018 it was 73.00. This data suggest that in the year 2017 the speed of

collecting the receivables was fast as compared to the period of 2018. But in the year 2018 it

increased to 73 which means that the speed or the time taken in receiving the due amount

reduced by 4.56 times. Hence, the performance of Alpha ltd reduced as now the company is able

to recover its money at a slow pace. Also, it is suggested to the company that as they are not able

to recover the more amount so they must stop the credit sales. This is because if credit sales will

not be done then no money needs to be recovered by the company.

Average payable days/ creditors collection period

This is an efficiency ratio which helps the company in calculating the average payment

which the company has to do for all the credit purchases they have made during the financial

period (Greenberg and Hershfield, 2019). Also, known as creditor turnover ratio this indicates

the time involved during the credit sales which is make the current liabilities outstanding fir the

company and this need to be paid. This ratio is important as this indicates the time when the

company is able to pay off all its debts and is in pure liquid position.

With help of calculation of the average payable days it was seen that in 2017 this was 70

but in the year 2018 it was 159. This suggest that in the year 2017 it was good but in the year

2018 it increased drastically which is not at all good for the company. Having this higher

collection period in 2018 suggest that the company is not able to pay off its current asset on time

and in proper manner that is full. Also, this higher number of creditor collection period suggests

that the company is not having proper communication with the consumer and because of this the

sales of company is reducing and for this the company need to take loans from other to run and

operate the business. Hence, because of this the profitability of the company reduces.

CONCLUSION

In the end it is summarised that the calculation and analysis o f the ratios is very essential

for the company in taking the financial decision. This is because the ratios help the company in

analysing the fact that where the company need to improve and this help the company in talking

the decision for the betterment of the company.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals

Greenberg, A.E. and Hershfield, H.E., 2019. Financial decision making. Consumer Psychology

Review. 2(1). pp.17-29.

Hirshleifer, D., Jian, M. and Zhang, H., 2018. Superstition and financial decision

making. Management Science. 64(1). pp.235-252.

Kim, J., Gutter, M.S. and Spangler, T., 2017. Review of family financial decision making:

Suggestions for future research and implications for financial education. Journal of

Financial Counseling and Planning. 28(2). pp.253-267.

Lieber, E.M. and Skimmyhorn, W., 2018. Peer effects in financial decision-making. Journal of

Public Economics. 163. pp.37-59.

Lu, Q., Won, J. and Cheng, J.C., 2016. A financial decision making framework for construction

projects based on 5D Building Information Modeling (BIM). International Journal of

Project Management. 34(1). pp.3-21.

Valaskova, K., Bartosova, V. and Kubala, P., 2019. Behavioural Aspects of the Financial

Decision-Making. Organizacija. 52(1).

Books and Journals

Greenberg, A.E. and Hershfield, H.E., 2019. Financial decision making. Consumer Psychology

Review. 2(1). pp.17-29.

Hirshleifer, D., Jian, M. and Zhang, H., 2018. Superstition and financial decision

making. Management Science. 64(1). pp.235-252.

Kim, J., Gutter, M.S. and Spangler, T., 2017. Review of family financial decision making:

Suggestions for future research and implications for financial education. Journal of

Financial Counseling and Planning. 28(2). pp.253-267.

Lieber, E.M. and Skimmyhorn, W., 2018. Peer effects in financial decision-making. Journal of

Public Economics. 163. pp.37-59.

Lu, Q., Won, J. and Cheng, J.C., 2016. A financial decision making framework for construction

projects based on 5D Building Information Modeling (BIM). International Journal of

Project Management. 34(1). pp.3-21.

Valaskova, K., Bartosova, V. and Kubala, P., 2019. Behavioural Aspects of the Financial

Decision-Making. Organizacija. 52(1).

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.