Financial Resources and Decisions for Sweet Island Restaurant

VerifiedAdded on 2020/01/21

|17

|5565

|227

Report

AI Summary

This report provides a comprehensive analysis of financial resources and decisions for Sweet Island Restaurant. It begins by examining internal and external sources of finance, including the implications of each source and their suitability for the restaurant's needs, particularly for expansion. The report then delves into the cost of different financing options, the importance of financial planning, and the information required by various decision-makers. It also explores the impact of financing choices on financial statements. Furthermore, the report analyzes budgets, calculates unit costs, and evaluates the viability of investment projects using investment appraisal techniques. Finally, it covers financial statements, different types of accounts, and the calculation of various financial ratios to assess the financial position of Sweet Island Restaurant and compare it with another restaurant. The report aims to provide a holistic view of financial management within the context of a restaurant business.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

MANGING FINANCIAL

RESOURCES AND

DECISIONS

RESOURCES AND

DECISIONS

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

INTRODUCTION ..........................................................................................................................1

TASK 1............................................................................................................................................1

1.1 Internal and external sources of finance available with the business to raise its capital.......1

1.2 Implications of various sources of finance............................................................................2

1.3 Appropriate sources of finance for Sweet Island Restaurant to requirement for cash..........3

TASK 2............................................................................................................................................4

2.1 Cost of different sources of finance for Sweet Island Restaurant.........................................4

2.2 Importance of financial planning for Sweet Island Restaurant.............................................5

2.3 Information needed by different decision maker of Sweet Island Restaurant.....................5

2.4 Impact of sources of finance identified on the financial statements of Sweet Island

Restaurant....................................................................................................................................6

TASK 3............................................................................................................................................7

3.1 Analyze of the budgets in order to make appropriate decisions...........................................7

3.2 Calculation of Unit cost and its relevant pricing decisions...................................................8

3.3 Viability of the two projects using investment appraisal techniques....................................8

TASK 4............................................................................................................................................9

4.1 Financial statements..............................................................................................................9

4.2 Different types of accounts prepared by different organization..........................................10

4.3 Calculation of various ratio.................................................................................................10

Conclusion.....................................................................................................................................13

References......................................................................................................................................13

INTRODUCTION ..........................................................................................................................1

TASK 1............................................................................................................................................1

1.1 Internal and external sources of finance available with the business to raise its capital.......1

1.2 Implications of various sources of finance............................................................................2

1.3 Appropriate sources of finance for Sweet Island Restaurant to requirement for cash..........3

TASK 2............................................................................................................................................4

2.1 Cost of different sources of finance for Sweet Island Restaurant.........................................4

2.2 Importance of financial planning for Sweet Island Restaurant.............................................5

2.3 Information needed by different decision maker of Sweet Island Restaurant.....................5

2.4 Impact of sources of finance identified on the financial statements of Sweet Island

Restaurant....................................................................................................................................6

TASK 3............................................................................................................................................7

3.1 Analyze of the budgets in order to make appropriate decisions...........................................7

3.2 Calculation of Unit cost and its relevant pricing decisions...................................................8

3.3 Viability of the two projects using investment appraisal techniques....................................8

TASK 4............................................................................................................................................9

4.1 Financial statements..............................................................................................................9

4.2 Different types of accounts prepared by different organization..........................................10

4.3 Calculation of various ratio.................................................................................................10

Conclusion.....................................................................................................................................13

References......................................................................................................................................13

INTRODUCTION

Finance is the science that identifies the management of funds, investments, banking,

credit and assets and liabilities made by company. In other words, it can be said that finance is

the management of all activities that take place in the organization on cash and credit terms.

Finance consists of financial system and financial instruments. The following report is going to

interpret about various internal and external sources of finance which company can undertake in

order to meet its long term, medium term and short term requirements of funds.

In this report, importance of financial planning for Sweet Menu Restaurant is discussed.

Along with that, impact of various sources of finance on financial statements is explained. In

addition to this, budget of Blue Island Restaurant is going to be analysed in order to find out

company’s position. Unit cost of firm is calculated as well. In this, various different types of

financial statements used by different types of business are also discussed. At last, in this report,

various ratios related to profitability, solvency, etc. are calculated in order to compare the

financial position of Sweet Menu Restaurant and Blue Island Restaurant.

TASK 1

1.1 Internal and external sources of finance available with the business to raise its capital

Internal sources of finance:

Sale of Stock: - This is one of the methods which are used by company to generate cash

by selling out the available assets. Cash generated by selling the stock is used by the firm

for financing the capital needs. This method can be used by the organization to meet its

both short and long term requirement of cash. But it mainly depends on the type of assets

sold.

Retained profits: - It is one of the easiest methods which can be used by company to

meet its urgent requirement of funds. This is a type of liquid cash which is kept as a

reserve by the firm for future use. Retained profit is collected by deducting a small

amount of profit margin that is earned by company every year (Beaver, McNichols and

Rhie, 2005).

External sources of finance:

Share capital: - This is the source of finance in which company issues new shares or

raises the price of existing shares in order to raise the funds to meet its long term

3

Finance is the science that identifies the management of funds, investments, banking,

credit and assets and liabilities made by company. In other words, it can be said that finance is

the management of all activities that take place in the organization on cash and credit terms.

Finance consists of financial system and financial instruments. The following report is going to

interpret about various internal and external sources of finance which company can undertake in

order to meet its long term, medium term and short term requirements of funds.

In this report, importance of financial planning for Sweet Menu Restaurant is discussed.

Along with that, impact of various sources of finance on financial statements is explained. In

addition to this, budget of Blue Island Restaurant is going to be analysed in order to find out

company’s position. Unit cost of firm is calculated as well. In this, various different types of

financial statements used by different types of business are also discussed. At last, in this report,

various ratios related to profitability, solvency, etc. are calculated in order to compare the

financial position of Sweet Menu Restaurant and Blue Island Restaurant.

TASK 1

1.1 Internal and external sources of finance available with the business to raise its capital

Internal sources of finance:

Sale of Stock: - This is one of the methods which are used by company to generate cash

by selling out the available assets. Cash generated by selling the stock is used by the firm

for financing the capital needs. This method can be used by the organization to meet its

both short and long term requirement of cash. But it mainly depends on the type of assets

sold.

Retained profits: - It is one of the easiest methods which can be used by company to

meet its urgent requirement of funds. This is a type of liquid cash which is kept as a

reserve by the firm for future use. Retained profit is collected by deducting a small

amount of profit margin that is earned by company every year (Beaver, McNichols and

Rhie, 2005).

External sources of finance:

Share capital: - This is the source of finance in which company issues new shares or

raises the price of existing shares in order to raise the funds to meet its long term

3

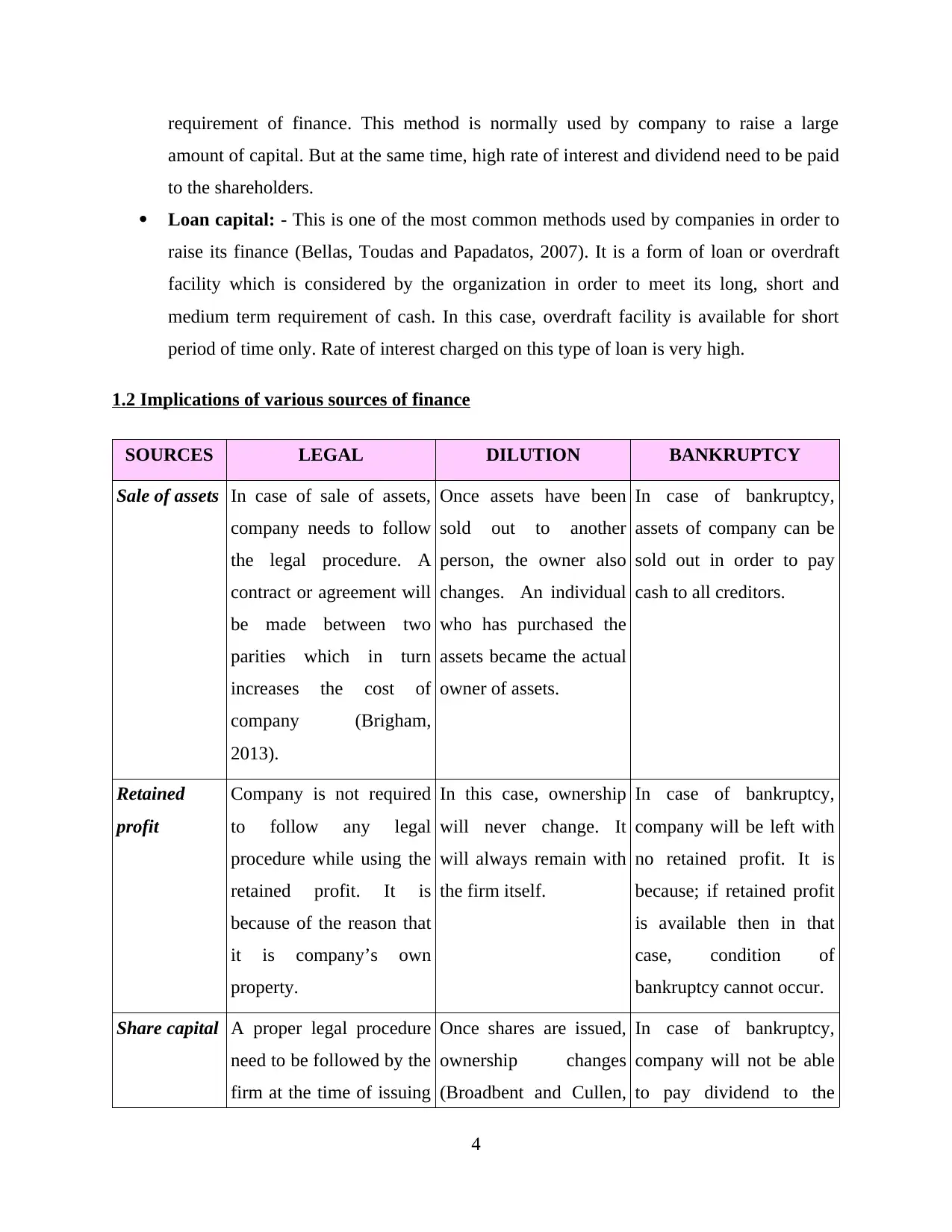

requirement of finance. This method is normally used by company to raise a large

amount of capital. But at the same time, high rate of interest and dividend need to be paid

to the shareholders.

Loan capital: - This is one of the most common methods used by companies in order to

raise its finance (Bellas, Toudas and Papadatos, 2007). It is a form of loan or overdraft

facility which is considered by the organization in order to meet its long, short and

medium term requirement of cash. In this case, overdraft facility is available for short

period of time only. Rate of interest charged on this type of loan is very high.

1.2 Implications of various sources of finance

SOURCES LEGAL DILUTION BANKRUPTCY

Sale of assets In case of sale of assets,

company needs to follow

the legal procedure. A

contract or agreement will

be made between two

parities which in turn

increases the cost of

company (Brigham,

2013).

Once assets have been

sold out to another

person, the owner also

changes. An individual

who has purchased the

assets became the actual

owner of assets.

In case of bankruptcy,

assets of company can be

sold out in order to pay

cash to all creditors.

Retained

profit

Company is not required

to follow any legal

procedure while using the

retained profit. It is

because of the reason that

it is company’s own

property.

In this case, ownership

will never change. It

will always remain with

the firm itself.

In case of bankruptcy,

company will be left with

no retained profit. It is

because; if retained profit

is available then in that

case, condition of

bankruptcy cannot occur.

Share capital A proper legal procedure

need to be followed by the

firm at the time of issuing

Once shares are issued,

ownership changes

(Broadbent and Cullen,

In case of bankruptcy,

company will not be able

to pay dividend to the

4

amount of capital. But at the same time, high rate of interest and dividend need to be paid

to the shareholders.

Loan capital: - This is one of the most common methods used by companies in order to

raise its finance (Bellas, Toudas and Papadatos, 2007). It is a form of loan or overdraft

facility which is considered by the organization in order to meet its long, short and

medium term requirement of cash. In this case, overdraft facility is available for short

period of time only. Rate of interest charged on this type of loan is very high.

1.2 Implications of various sources of finance

SOURCES LEGAL DILUTION BANKRUPTCY

Sale of assets In case of sale of assets,

company needs to follow

the legal procedure. A

contract or agreement will

be made between two

parities which in turn

increases the cost of

company (Brigham,

2013).

Once assets have been

sold out to another

person, the owner also

changes. An individual

who has purchased the

assets became the actual

owner of assets.

In case of bankruptcy,

assets of company can be

sold out in order to pay

cash to all creditors.

Retained

profit

Company is not required

to follow any legal

procedure while using the

retained profit. It is

because of the reason that

it is company’s own

property.

In this case, ownership

will never change. It

will always remain with

the firm itself.

In case of bankruptcy,

company will be left with

no retained profit. It is

because; if retained profit

is available then in that

case, condition of

bankruptcy cannot occur.

Share capital A proper legal procedure

need to be followed by the

firm at the time of issuing

Once shares are issued,

ownership changes

(Broadbent and Cullen,

In case of bankruptcy,

company will not be able

to pay dividend to the

4

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

shares. This in turn

increases the cost of

company.

2012). Those individuals

who hold the equity

shares are given with the

right to vote in the

decision making process

of organization.

shareholders.

Loan capital In this case also, company

needs to follow a legal

procedure in order to avail

loan from the bank. At the

same time, firm also needs

to provide collateral

security to the bank. This

in turn increases the cost

of organization because

company need to pay high

rate of interest.

Ownership of the

amount withdraws by

company from bank as a

loan changes. Company

is now liable to use the

fund collected from

bank in any manner.

In case of bankruptcy,

bank will sell out the

collateral security

provided by the firm in

order to recover the

amount paid to company

(Butters, 2004).

1.3 Appropriate sources of finance for Sweet Island Restaurant to requirement for cash.

There are various sources of finance that are available with company to meet its short and

long term requirement of cash. But the most appropriate source which will aid the Sweet Island

Restaurant to meet its requirement of £3,00,000 to £5,00,000 in order to expand its business by

opening new branches are as follows:-

If Sweet Island Restaurant wants to raise its capital by using the internal sources of finance

then in that case, company can move on by selling assets. Similarly, if firm wants to raise its

finance by using external sources then it can move on with the share capital.

SOURCES ADVANTAGES DISADVANTAGES SUITABILITY

Sale of assets Finance can be

generated without

Loss can be faced by company

at the time of sale of assets.

For purchasing new

assets or for expanding

5

increases the cost of

company.

2012). Those individuals

who hold the equity

shares are given with the

right to vote in the

decision making process

of organization.

shareholders.

Loan capital In this case also, company

needs to follow a legal

procedure in order to avail

loan from the bank. At the

same time, firm also needs

to provide collateral

security to the bank. This

in turn increases the cost

of organization because

company need to pay high

rate of interest.

Ownership of the

amount withdraws by

company from bank as a

loan changes. Company

is now liable to use the

fund collected from

bank in any manner.

In case of bankruptcy,

bank will sell out the

collateral security

provided by the firm in

order to recover the

amount paid to company

(Butters, 2004).

1.3 Appropriate sources of finance for Sweet Island Restaurant to requirement for cash.

There are various sources of finance that are available with company to meet its short and

long term requirement of cash. But the most appropriate source which will aid the Sweet Island

Restaurant to meet its requirement of £3,00,000 to £5,00,000 in order to expand its business by

opening new branches are as follows:-

If Sweet Island Restaurant wants to raise its capital by using the internal sources of finance

then in that case, company can move on by selling assets. Similarly, if firm wants to raise its

finance by using external sources then it can move on with the share capital.

SOURCES ADVANTAGES DISADVANTAGES SUITABILITY

Sale of assets Finance can be

generated without

Loss can be faced by company

at the time of sale of assets.

For purchasing new

assets or for expanding

5

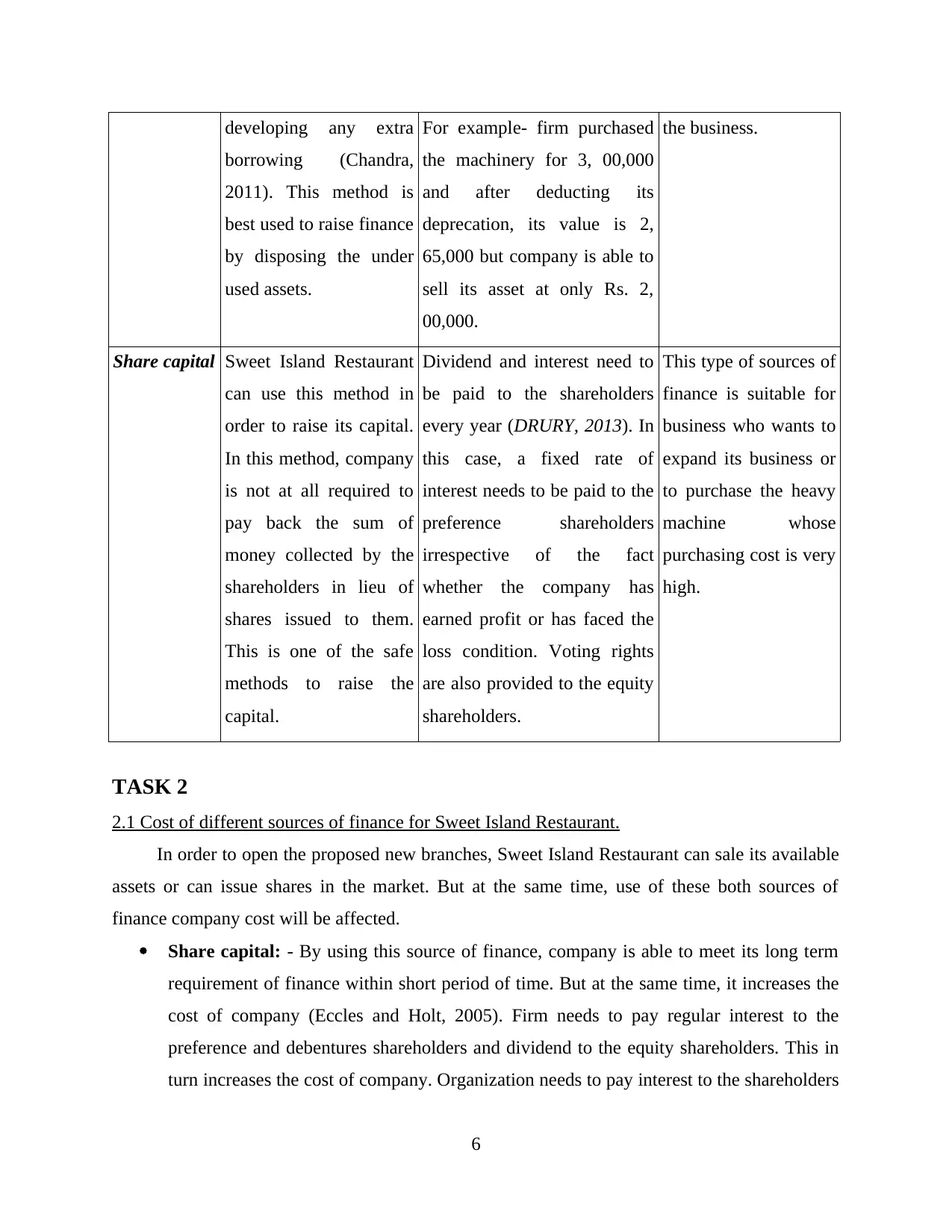

developing any extra

borrowing (Chandra,

2011). This method is

best used to raise finance

by disposing the under

used assets.

For example- firm purchased

the machinery for 3, 00,000

and after deducting its

deprecation, its value is 2,

65,000 but company is able to

sell its asset at only Rs. 2,

00,000.

the business.

Share capital Sweet Island Restaurant

can use this method in

order to raise its capital.

In this method, company

is not at all required to

pay back the sum of

money collected by the

shareholders in lieu of

shares issued to them.

This is one of the safe

methods to raise the

capital.

Dividend and interest need to

be paid to the shareholders

every year (DRURY, 2013). In

this case, a fixed rate of

interest needs to be paid to the

preference shareholders

irrespective of the fact

whether the company has

earned profit or has faced the

loss condition. Voting rights

are also provided to the equity

shareholders.

This type of sources of

finance is suitable for

business who wants to

expand its business or

to purchase the heavy

machine whose

purchasing cost is very

high.

TASK 2

2.1 Cost of different sources of finance for Sweet Island Restaurant.

In order to open the proposed new branches, Sweet Island Restaurant can sale its available

assets or can issue shares in the market. But at the same time, use of these both sources of

finance company cost will be affected.

Share capital: - By using this source of finance, company is able to meet its long term

requirement of finance within short period of time. But at the same time, it increases the

cost of company (Eccles and Holt, 2005). Firm needs to pay regular interest to the

preference and debentures shareholders and dividend to the equity shareholders. This in

turn increases the cost of company. Organization needs to pay interest to the shareholders

6

borrowing (Chandra,

2011). This method is

best used to raise finance

by disposing the under

used assets.

For example- firm purchased

the machinery for 3, 00,000

and after deducting its

deprecation, its value is 2,

65,000 but company is able to

sell its asset at only Rs. 2,

00,000.

the business.

Share capital Sweet Island Restaurant

can use this method in

order to raise its capital.

In this method, company

is not at all required to

pay back the sum of

money collected by the

shareholders in lieu of

shares issued to them.

This is one of the safe

methods to raise the

capital.

Dividend and interest need to

be paid to the shareholders

every year (DRURY, 2013). In

this case, a fixed rate of

interest needs to be paid to the

preference shareholders

irrespective of the fact

whether the company has

earned profit or has faced the

loss condition. Voting rights

are also provided to the equity

shareholders.

This type of sources of

finance is suitable for

business who wants to

expand its business or

to purchase the heavy

machine whose

purchasing cost is very

high.

TASK 2

2.1 Cost of different sources of finance for Sweet Island Restaurant.

In order to open the proposed new branches, Sweet Island Restaurant can sale its available

assets or can issue shares in the market. But at the same time, use of these both sources of

finance company cost will be affected.

Share capital: - By using this source of finance, company is able to meet its long term

requirement of finance within short period of time. But at the same time, it increases the

cost of company (Eccles and Holt, 2005). Firm needs to pay regular interest to the

preference and debentures shareholders and dividend to the equity shareholders. This in

turn increases the cost of company. Organization needs to pay interest to the shareholders

6

irrespective of the fact whether company is able to generate profit or not. At the same

time, enterprise also needs to provide voting rights to the equity shareholders. Therefore,

payment of interest and dividend will reduce the profit margin of company.

Sale of assets: - By using this source of finance, Sweet Island Restaurant will be able to

meet its both short term and long term requirement of finance. Requirement of cash

depends on the type of assets sold. But at the same time, it affects the cost of company

(Efendi, Srivastava and Swanson, 2007). Assets of the firm will be reduced. Company

can also face the loss if proper value of assets is not able to be availed. For example, firm

purchases the assets for £5, 00,000 whose value after deprecation was £4, 50,000 but sold

at £3, 50,000. Therefore, it can be said that company faces loss of £1, 00,000.

2.2 Importance of financial planning for Sweet Island Restaurant

Planning of all the financial activities in advance will prove to be very beneficial for the

Sweet Island Restaurant in the following manner.

Able to maintain the flow of funds from the restaurant: - Financial planning of all the

activities in advance will assist the Sweet Island Restaurant to maintain the inflow and

outflow of the funds from the organization (Hursti and Maula, 2007). It will also aid the

company to maintain the balance between inflow and outflow of the funds.

Able to achieve maximum utilisation of resources: - Financial planning by the Sweet

Island Restaurant will assist them to utilise the available resources to the full extent. This

in turn will aid the company to reduce the wastage of the resources.

Able to distribute finance properly to each and every department: - Proper financial

planning will assist the Sweet Island Restaurant to distribute the funds available with the

company in each and every department according to the requirement in the following

departments. This in turn will aid the company to avoid the condition of excess

availability of funds and low availability of funds.

Reduce uncertainty: - Financial planning will also help the Sweet Island Restaurant to

reduce the condition of uncertainty which could be faced by them at the time of change in

various internal and external environmental factors (Muradoglu and Harvey, 2012).

Avoid shocks and surprises: - Financial planning will aid the Sweet Island Restaurant to

avoid the condition of shocks and surprise which can be occurred due to sudden change

in the environment especially in the internal organization.

7

time, enterprise also needs to provide voting rights to the equity shareholders. Therefore,

payment of interest and dividend will reduce the profit margin of company.

Sale of assets: - By using this source of finance, Sweet Island Restaurant will be able to

meet its both short term and long term requirement of finance. Requirement of cash

depends on the type of assets sold. But at the same time, it affects the cost of company

(Efendi, Srivastava and Swanson, 2007). Assets of the firm will be reduced. Company

can also face the loss if proper value of assets is not able to be availed. For example, firm

purchases the assets for £5, 00,000 whose value after deprecation was £4, 50,000 but sold

at £3, 50,000. Therefore, it can be said that company faces loss of £1, 00,000.

2.2 Importance of financial planning for Sweet Island Restaurant

Planning of all the financial activities in advance will prove to be very beneficial for the

Sweet Island Restaurant in the following manner.

Able to maintain the flow of funds from the restaurant: - Financial planning of all the

activities in advance will assist the Sweet Island Restaurant to maintain the inflow and

outflow of the funds from the organization (Hursti and Maula, 2007). It will also aid the

company to maintain the balance between inflow and outflow of the funds.

Able to achieve maximum utilisation of resources: - Financial planning by the Sweet

Island Restaurant will assist them to utilise the available resources to the full extent. This

in turn will aid the company to reduce the wastage of the resources.

Able to distribute finance properly to each and every department: - Proper financial

planning will assist the Sweet Island Restaurant to distribute the funds available with the

company in each and every department according to the requirement in the following

departments. This in turn will aid the company to avoid the condition of excess

availability of funds and low availability of funds.

Reduce uncertainty: - Financial planning will also help the Sweet Island Restaurant to

reduce the condition of uncertainty which could be faced by them at the time of change in

various internal and external environmental factors (Muradoglu and Harvey, 2012).

Avoid shocks and surprises: - Financial planning will aid the Sweet Island Restaurant to

avoid the condition of shocks and surprise which can be occurred due to sudden change

in the environment especially in the internal organization.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2.3 Information needed by different decision maker of Sweet Island Restaurant

Different types of information needed by the stakeholders of the company are as follows:-

Shareholders: - shareholders are most valuable persons to the organization. They invest

their personal saving in the company in order to gain high rate of return on the investment

made. Therefore, in order to decide whether they should invest or not certain type of

information are required by them (Paramasivan, 2009). They need financial statements,

cash flow statement and income statements to decide whether company is growing or not

and whether they will be able to gain high return or not.

Suppliers: - Suppliers are the distributors of raw material to the company. They supply

goods to the company in order to develop the finished goods. Therefore, in order to

decide whether the suppliers should supply goods to the company or not they want

financial statements of the company. These suppliers simply want to see whether the

company is in a position to pay them for the goods supplied by them or not.

Managers: - Managers are the individual who work for the betterment of the company.

This decision maker requires all type of financial accounts and company audit report in

order to conclude the actual position of the company and to prepare various strategies

(Ryan, 2005).

Government:- Government is the another decision maker of the Sweet Island Restaurant

who wants different types of financial accounts and company audit report in order to

calculate the amount of tax need to be paid. At the same time they also want to see the

financial position of the company in order to grant permission on various matters.

Thus, these are some of the information which is required by the decision maker of Sweet

Island Restaurant in order to make various decisions.

2.4 Impact of sources of finance identified on the financial statements of Sweet Island Restaurant

Sale of assets: - Entry of sale of assets will be made at two sides in the balance sheet.

One it will be deducted from the asset that is sold out and secondly cash of the company

will increase.

Retained profit: - Entry of retained profit will be made in liability side of the balance

sheet under the head of Equities. Retained profit is calculated by the company after

paying dividend to the shareholders (Shahrokhi, 2008).

8

Different types of information needed by the stakeholders of the company are as follows:-

Shareholders: - shareholders are most valuable persons to the organization. They invest

their personal saving in the company in order to gain high rate of return on the investment

made. Therefore, in order to decide whether they should invest or not certain type of

information are required by them (Paramasivan, 2009). They need financial statements,

cash flow statement and income statements to decide whether company is growing or not

and whether they will be able to gain high return or not.

Suppliers: - Suppliers are the distributors of raw material to the company. They supply

goods to the company in order to develop the finished goods. Therefore, in order to

decide whether the suppliers should supply goods to the company or not they want

financial statements of the company. These suppliers simply want to see whether the

company is in a position to pay them for the goods supplied by them or not.

Managers: - Managers are the individual who work for the betterment of the company.

This decision maker requires all type of financial accounts and company audit report in

order to conclude the actual position of the company and to prepare various strategies

(Ryan, 2005).

Government:- Government is the another decision maker of the Sweet Island Restaurant

who wants different types of financial accounts and company audit report in order to

calculate the amount of tax need to be paid. At the same time they also want to see the

financial position of the company in order to grant permission on various matters.

Thus, these are some of the information which is required by the decision maker of Sweet

Island Restaurant in order to make various decisions.

2.4 Impact of sources of finance identified on the financial statements of Sweet Island Restaurant

Sale of assets: - Entry of sale of assets will be made at two sides in the balance sheet.

One it will be deducted from the asset that is sold out and secondly cash of the company

will increase.

Retained profit: - Entry of retained profit will be made in liability side of the balance

sheet under the head of Equities. Retained profit is calculated by the company after

paying dividend to the shareholders (Shahrokhi, 2008).

8

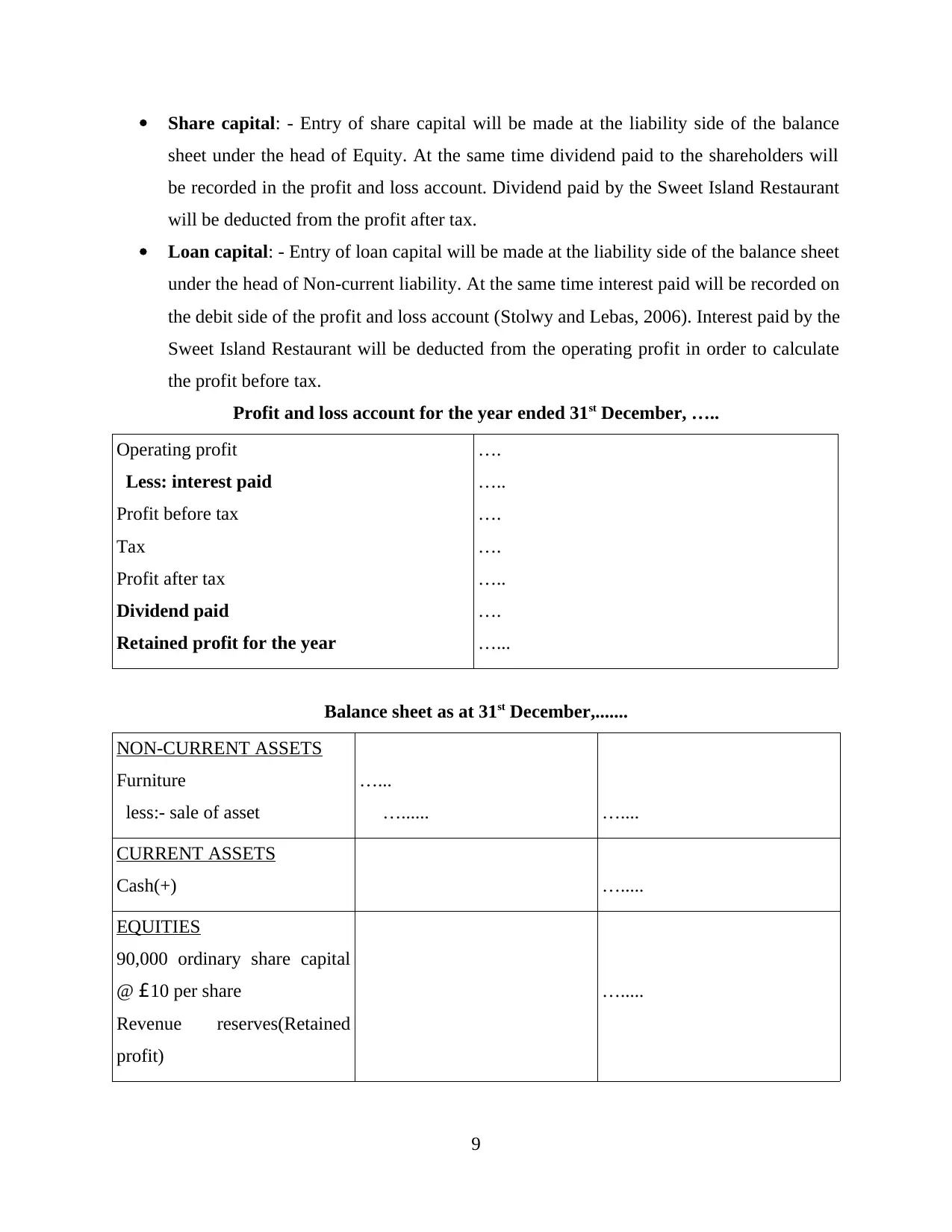

Share capital: - Entry of share capital will be made at the liability side of the balance

sheet under the head of Equity. At the same time dividend paid to the shareholders will

be recorded in the profit and loss account. Dividend paid by the Sweet Island Restaurant

will be deducted from the profit after tax.

Loan capital: - Entry of loan capital will be made at the liability side of the balance sheet

under the head of Non-current liability. At the same time interest paid will be recorded on

the debit side of the profit and loss account (Stolwy and Lebas, 2006). Interest paid by the

Sweet Island Restaurant will be deducted from the operating profit in order to calculate

the profit before tax.

Profit and loss account for the year ended 31st December, …..

Operating profit

Less: interest paid

Profit before tax

Tax

Profit after tax

Dividend paid

Retained profit for the year

….

…..

….

….

…..

….

…...

Balance sheet as at 31st December,.......

NON-CURRENT ASSETS

Furniture

less:- sale of asset

…...

…...... …....

CURRENT ASSETS

Cash(+) ….....

EQUITIES

90,000 ordinary share capital

@ £10 per share

Revenue reserves(Retained

profit)

….....

9

sheet under the head of Equity. At the same time dividend paid to the shareholders will

be recorded in the profit and loss account. Dividend paid by the Sweet Island Restaurant

will be deducted from the profit after tax.

Loan capital: - Entry of loan capital will be made at the liability side of the balance sheet

under the head of Non-current liability. At the same time interest paid will be recorded on

the debit side of the profit and loss account (Stolwy and Lebas, 2006). Interest paid by the

Sweet Island Restaurant will be deducted from the operating profit in order to calculate

the profit before tax.

Profit and loss account for the year ended 31st December, …..

Operating profit

Less: interest paid

Profit before tax

Tax

Profit after tax

Dividend paid

Retained profit for the year

….

…..

….

….

…..

….

…...

Balance sheet as at 31st December,.......

NON-CURRENT ASSETS

Furniture

less:- sale of asset

…...

…...... …....

CURRENT ASSETS

Cash(+) ….....

EQUITIES

90,000 ordinary share capital

@ £10 per share

Revenue reserves(Retained

profit)

….....

9

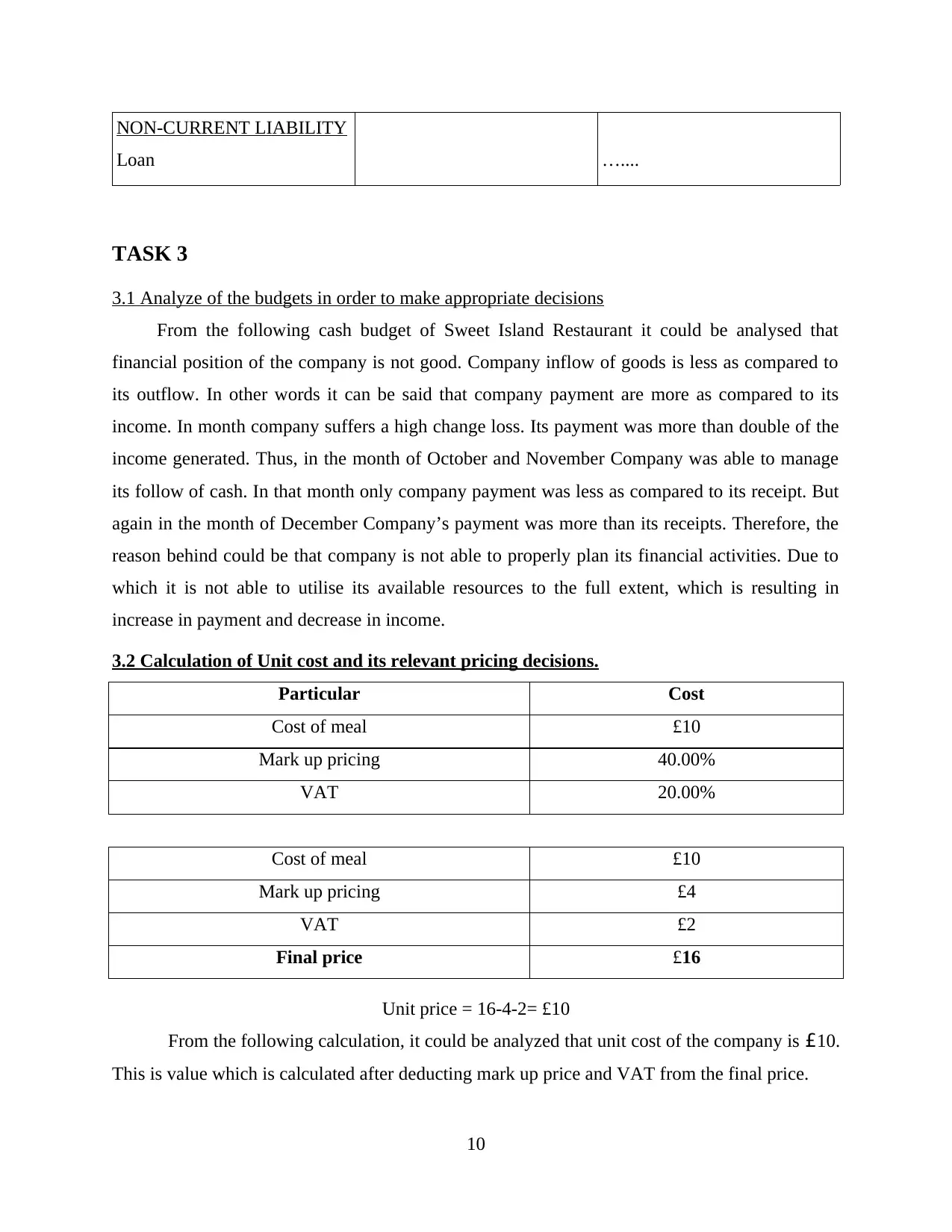

NON-CURRENT LIABILITY

Loan …....

TASK 3

3.1 Analyze of the budgets in order to make appropriate decisions

From the following cash budget of Sweet Island Restaurant it could be analysed that

financial position of the company is not good. Company inflow of goods is less as compared to

its outflow. In other words it can be said that company payment are more as compared to its

income. In month company suffers a high change loss. Its payment was more than double of the

income generated. Thus, in the month of October and November Company was able to manage

its follow of cash. In that month only company payment was less as compared to its receipt. But

again in the month of December Company’s payment was more than its receipts. Therefore, the

reason behind could be that company is not able to properly plan its financial activities. Due to

which it is not able to utilise its available resources to the full extent, which is resulting in

increase in payment and decrease in income.

3.2 Calculation of Unit cost and its relevant pricing decisions.

Particular Cost

Cost of meal £10

Mark up pricing 40.00%

VAT 20.00%

Cost of meal £10

Mark up pricing £4

VAT £2

Final price £16

Unit price = 16-4-2= £10

From the following calculation, it could be analyzed that unit cost of the company is £10.

This is value which is calculated after deducting mark up price and VAT from the final price.

10

Loan …....

TASK 3

3.1 Analyze of the budgets in order to make appropriate decisions

From the following cash budget of Sweet Island Restaurant it could be analysed that

financial position of the company is not good. Company inflow of goods is less as compared to

its outflow. In other words it can be said that company payment are more as compared to its

income. In month company suffers a high change loss. Its payment was more than double of the

income generated. Thus, in the month of October and November Company was able to manage

its follow of cash. In that month only company payment was less as compared to its receipt. But

again in the month of December Company’s payment was more than its receipts. Therefore, the

reason behind could be that company is not able to properly plan its financial activities. Due to

which it is not able to utilise its available resources to the full extent, which is resulting in

increase in payment and decrease in income.

3.2 Calculation of Unit cost and its relevant pricing decisions.

Particular Cost

Cost of meal £10

Mark up pricing 40.00%

VAT 20.00%

Cost of meal £10

Mark up pricing £4

VAT £2

Final price £16

Unit price = 16-4-2= £10

From the following calculation, it could be analyzed that unit cost of the company is £10.

This is value which is calculated after deducting mark up price and VAT from the final price.

10

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

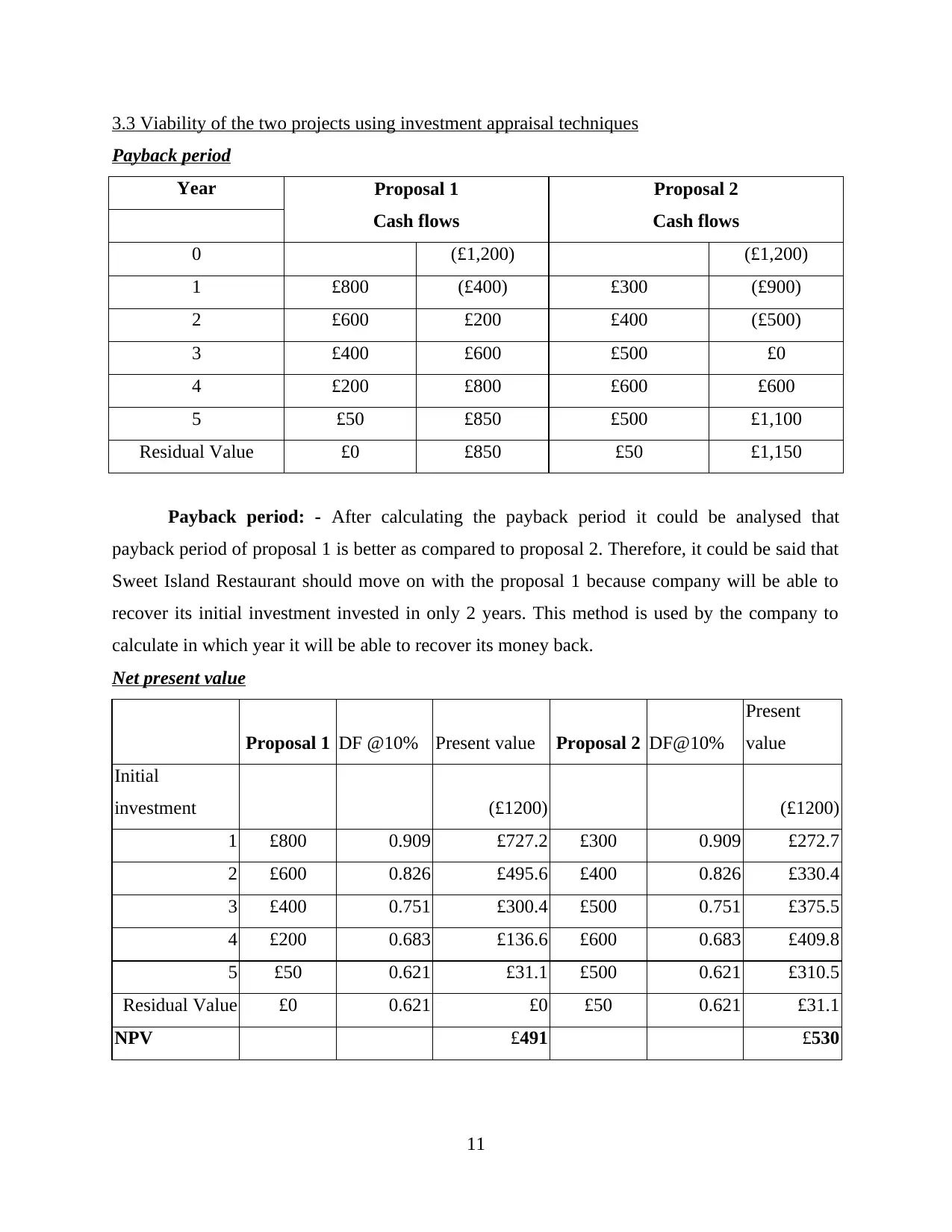

3.3 Viability of the two projects using investment appraisal techniques

Payback period

Year Proposal 1

Cash flows

Proposal 2

Cash flows

0 (£1,200) (£1,200)

1 £800 (£400) £300 (£900)

2 £600 £200 £400 (£500)

3 £400 £600 £500 £0

4 £200 £800 £600 £600

5 £50 £850 £500 £1,100

Residual Value £0 £850 £50 £1,150

Payback period: - After calculating the payback period it could be analysed that

payback period of proposal 1 is better as compared to proposal 2. Therefore, it could be said that

Sweet Island Restaurant should move on with the proposal 1 because company will be able to

recover its initial investment invested in only 2 years. This method is used by the company to

calculate in which year it will be able to recover its money back.

Net present value

Proposal 1 DF @10% Present value Proposal 2 DF@10%

Present

value

Initial

investment (£1200) (£1200)

1 £800 0.909 £727.2 £300 0.909 £272.7

2 £600 0.826 £495.6 £400 0.826 £330.4

3 £400 0.751 £300.4 £500 0.751 £375.5

4 £200 0.683 £136.6 £600 0.683 £409.8

5 £50 0.621 £31.1 £500 0.621 £310.5

Residual Value £0 0.621 £0 £50 0.621 £31.1

NPV £491 £530

11

Payback period

Year Proposal 1

Cash flows

Proposal 2

Cash flows

0 (£1,200) (£1,200)

1 £800 (£400) £300 (£900)

2 £600 £200 £400 (£500)

3 £400 £600 £500 £0

4 £200 £800 £600 £600

5 £50 £850 £500 £1,100

Residual Value £0 £850 £50 £1,150

Payback period: - After calculating the payback period it could be analysed that

payback period of proposal 1 is better as compared to proposal 2. Therefore, it could be said that

Sweet Island Restaurant should move on with the proposal 1 because company will be able to

recover its initial investment invested in only 2 years. This method is used by the company to

calculate in which year it will be able to recover its money back.

Net present value

Proposal 1 DF @10% Present value Proposal 2 DF@10%

Present

value

Initial

investment (£1200) (£1200)

1 £800 0.909 £727.2 £300 0.909 £272.7

2 £600 0.826 £495.6 £400 0.826 £330.4

3 £400 0.751 £300.4 £500 0.751 £375.5

4 £200 0.683 £136.6 £600 0.683 £409.8

5 £50 0.621 £31.1 £500 0.621 £310.5

Residual Value £0 0.621 £0 £50 0.621 £31.1

NPV £491 £530

11

Net present value: - This method is used by the company to calculate the cash flows by

considering the rate of discounted factors. From the following calculation it could be analysed

that net present value of proposal 2 is more as compared to proposal 1. Therefore, it could be

said that Sweet Island Restaurant should move on with proposal 2. Because proposal 2 will give

better return to the company on the amount invested.

TASK 4

4.1 Financial statements

Profit and loss account: - Profit and loss account includes all types of income and

expenditure made by the company at the end of the every financial year. These

statements are also used to calculate the net profit or net loss generate by the company.

These statements are used by different types of stakeholder like managers, employees,

government and so on (Thomas, 2008). They prefer these statements in order to calculate

the amount of tax need to be paid by the company and to form various strategies.

Balance sheet: - Balance sheet includes all types of asset available with the company and

the liabilities made by the company. Liabilities are recorded on the left hand side of the

balance sheet and assets are recorded on the right hand side. These statements are

prepared by the company in order to know the actual position of the company. These

statements are used by the manager (in order to develop various strategies) and

shareholders (in order to know the company's actual position). Increased in liabilities of

the company indicates that company position is not good.

Cash flow statements: - This statement indicates the flow of cash and cash equivalents

from within and outside the organization (Tulsian, 2002). These statements are divided

into three different types of activities that indicate the follow of cash. The activities are

operating activity, investment activities and financial activities. Therefore, these

statements are used by the shareholders, board of directors and investor in order to find

out the follow of cash from the organization. And at the same time it also helps to find

out the actual position of the company.

o 4.2 Different types of accounts prepared by different organization

Private organization: - This firm is the firm who’s all the operation and activities are

managed and controlled by the private individuals. In this type of organization there is no

12

considering the rate of discounted factors. From the following calculation it could be analysed

that net present value of proposal 2 is more as compared to proposal 1. Therefore, it could be

said that Sweet Island Restaurant should move on with proposal 2. Because proposal 2 will give

better return to the company on the amount invested.

TASK 4

4.1 Financial statements

Profit and loss account: - Profit and loss account includes all types of income and

expenditure made by the company at the end of the every financial year. These

statements are also used to calculate the net profit or net loss generate by the company.

These statements are used by different types of stakeholder like managers, employees,

government and so on (Thomas, 2008). They prefer these statements in order to calculate

the amount of tax need to be paid by the company and to form various strategies.

Balance sheet: - Balance sheet includes all types of asset available with the company and

the liabilities made by the company. Liabilities are recorded on the left hand side of the

balance sheet and assets are recorded on the right hand side. These statements are

prepared by the company in order to know the actual position of the company. These

statements are used by the manager (in order to develop various strategies) and

shareholders (in order to know the company's actual position). Increased in liabilities of

the company indicates that company position is not good.

Cash flow statements: - This statement indicates the flow of cash and cash equivalents

from within and outside the organization (Tulsian, 2002). These statements are divided

into three different types of activities that indicate the follow of cash. The activities are

operating activity, investment activities and financial activities. Therefore, these

statements are used by the shareholders, board of directors and investor in order to find

out the follow of cash from the organization. And at the same time it also helps to find

out the actual position of the company.

o 4.2 Different types of accounts prepared by different organization

Private organization: - This firm is the firm who’s all the operation and activities are

managed and controlled by the private individuals. In this type of organization there is no

12

government interference. These organizations are required to prepare all the financial

statements if this organization is listed on stock exchange (White, 2006). If size of the

firm is small than in that company can only prepare the income statements.

Public Organization: - these firms are the firms who are all the operations and activities

are controlled and managed by the government. These organization need to prepare all

the financial statements along with the company audit report. These organization need to

follow all the policies and norms imposed by the government.

Non-profit organization: - These organization work for the betterment of the society.

These organizations are also known as charitable institution. These organizations are

managed by the individual or a group of person (Sabău, 2013). Therefore, these

organization need to prepare only receipt and payment account. These organizations

record all its daily transaction in the form of journal only.

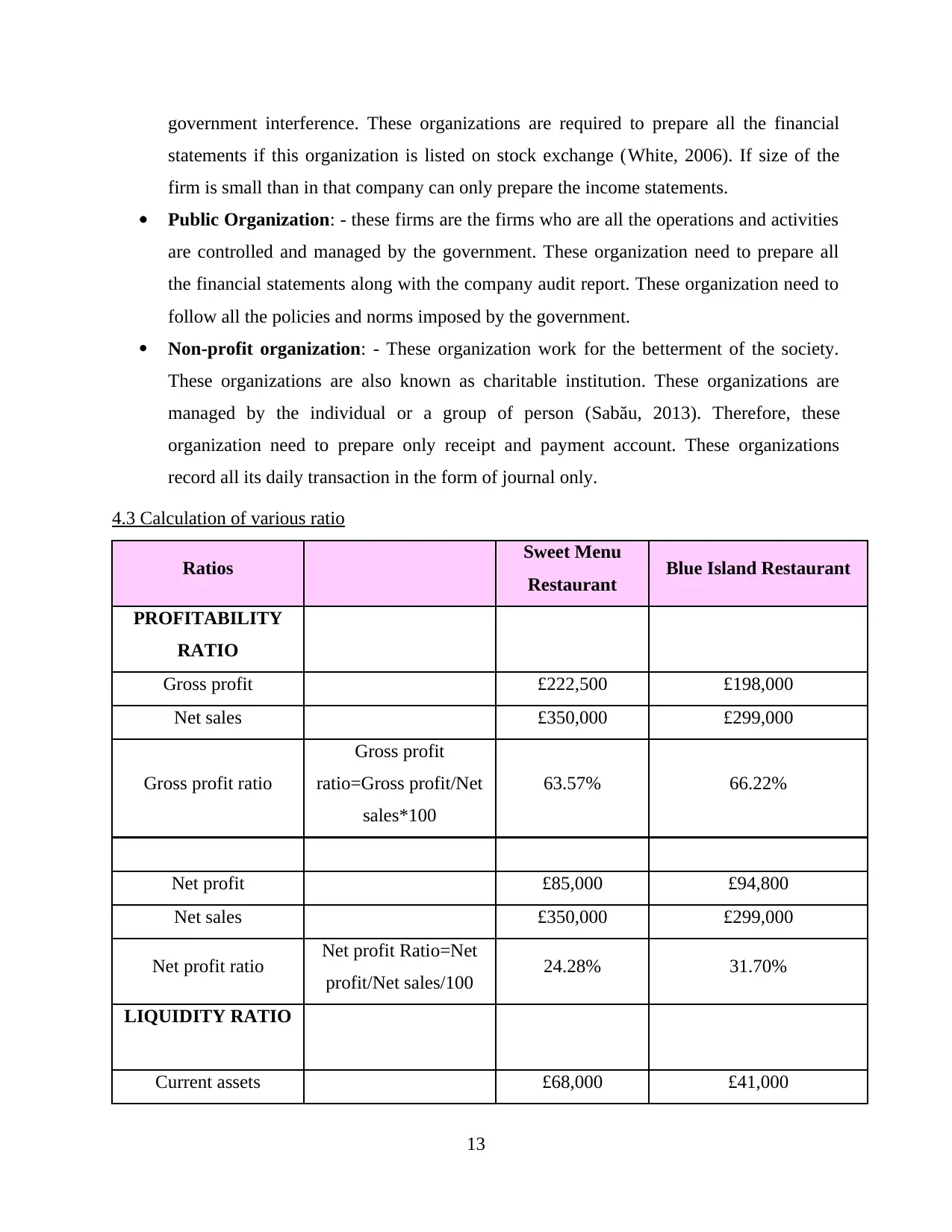

4.3 Calculation of various ratio

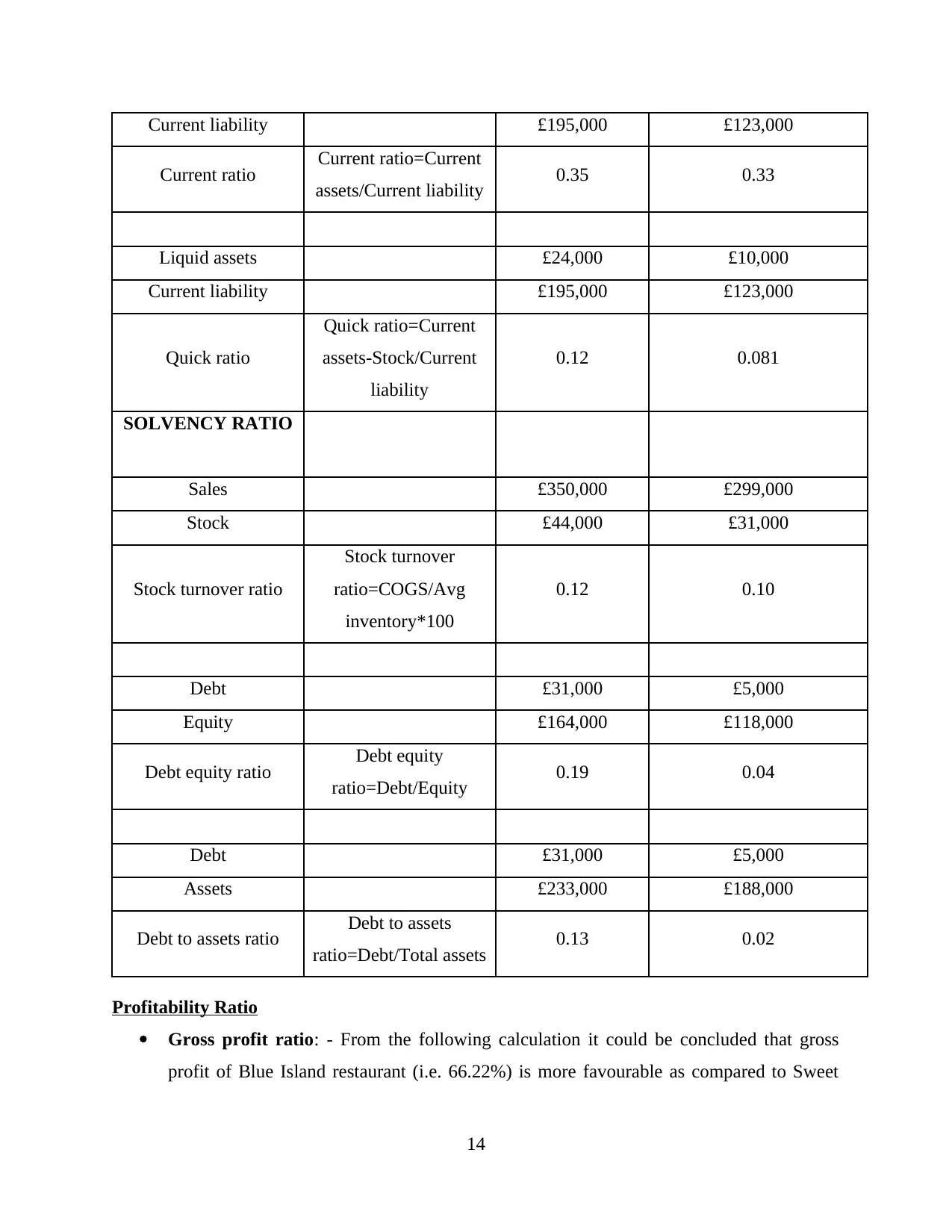

Ratios Sweet Menu

Restaurant Blue Island Restaurant

PROFITABILITY

RATIO

Gross profit £222,500 £198,000

Net sales £350,000 £299,000

Gross profit ratio

Gross profit

ratio=Gross profit/Net

sales*100

63.57% 66.22%

Net profit £85,000 £94,800

Net sales £350,000 £299,000

Net profit ratio Net profit Ratio=Net

profit/Net sales/100 24.28% 31.70%

LIQUIDITY RATIO

Current assets £68,000 £41,000

13

statements if this organization is listed on stock exchange (White, 2006). If size of the

firm is small than in that company can only prepare the income statements.

Public Organization: - these firms are the firms who are all the operations and activities

are controlled and managed by the government. These organization need to prepare all

the financial statements along with the company audit report. These organization need to

follow all the policies and norms imposed by the government.

Non-profit organization: - These organization work for the betterment of the society.

These organizations are also known as charitable institution. These organizations are

managed by the individual or a group of person (Sabău, 2013). Therefore, these

organization need to prepare only receipt and payment account. These organizations

record all its daily transaction in the form of journal only.

4.3 Calculation of various ratio

Ratios Sweet Menu

Restaurant Blue Island Restaurant

PROFITABILITY

RATIO

Gross profit £222,500 £198,000

Net sales £350,000 £299,000

Gross profit ratio

Gross profit

ratio=Gross profit/Net

sales*100

63.57% 66.22%

Net profit £85,000 £94,800

Net sales £350,000 £299,000

Net profit ratio Net profit Ratio=Net

profit/Net sales/100 24.28% 31.70%

LIQUIDITY RATIO

Current assets £68,000 £41,000

13

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Current liability £195,000 £123,000

Current ratio Current ratio=Current

assets/Current liability 0.35 0.33

Liquid assets £24,000 £10,000

Current liability £195,000 £123,000

Quick ratio

Quick ratio=Current

assets-Stock/Current

liability

0.12 0.081

SOLVENCY RATIO

Sales £350,000 £299,000

Stock £44,000 £31,000

Stock turnover ratio

Stock turnover

ratio=COGS/Avg

inventory*100

0.12 0.10

Debt £31,000 £5,000

Equity £164,000 £118,000

Debt equity ratio Debt equity

ratio=Debt/Equity 0.19 0.04

Debt £31,000 £5,000

Assets £233,000 £188,000

Debt to assets ratio Debt to assets

ratio=Debt/Total assets 0.13 0.02

Profitability Ratio

Gross profit ratio: - From the following calculation it could be concluded that gross

profit of Blue Island restaurant (i.e. 66.22%) is more favourable as compared to Sweet

14

Current ratio Current ratio=Current

assets/Current liability 0.35 0.33

Liquid assets £24,000 £10,000

Current liability £195,000 £123,000

Quick ratio

Quick ratio=Current

assets-Stock/Current

liability

0.12 0.081

SOLVENCY RATIO

Sales £350,000 £299,000

Stock £44,000 £31,000

Stock turnover ratio

Stock turnover

ratio=COGS/Avg

inventory*100

0.12 0.10

Debt £31,000 £5,000

Equity £164,000 £118,000

Debt equity ratio Debt equity

ratio=Debt/Equity 0.19 0.04

Debt £31,000 £5,000

Assets £233,000 £188,000

Debt to assets ratio Debt to assets

ratio=Debt/Total assets 0.13 0.02

Profitability Ratio

Gross profit ratio: - From the following calculation it could be concluded that gross

profit of Blue Island restaurant (i.e. 66.22%) is more favourable as compared to Sweet

14

Menu restaurant (i.e. 63.57%). The reason behind could be that company is able to reduce

the cost of its production.

Net profit ratio: - The following calculation shows that net profit ratio of Blue Island

restaurant (i.e.31.70%) is more than that of Sweet Menu restaurant (i.e. 24.28%). The

reason behind this could be that Blue Island Restaurant is effectively managing its

operational costs and cost of production. This in turn have direct impact on the

profitability of the company.

Liquidity Ratio

Current ratio: - Current ratio indicates the liquid cash available with the company.

Therefore, from the following comparison it could be concluded that capability of

meeting short term requirement of Sweet Menu Restaurant is better than that of Blue

Island Restaurant. This in turn also indicates that current liabilities of the company is

more that its current assets.

Quick ratio: - This ratio shows that liquidity of the organization including the current

assets and current liabilities but excluding the stock (Sources of finance. 2012).

Therefore, from the following comparison it could be concluded that Quick ratio of

Sweet Menu restaurant is higher than that of Blue Island restaurant. The reason behind

this could be that company is able to meet its short term obligations.

Solvency Ratio

Stock turnover ratio: - This ratio shows the efficiency of the company to crook its stock

into sales. Therefore, by comparing the both the company ratio it could concluded that

efficiency of changing the stock is better of Sweet Menu Restaurant as compared to Blue

Island restaurant.

Debt equity ratio: - higher debt equity ratio of Sweet Menu Restaurant indicates that

debt of the company is lower and investment made by the owner is high. Similarly, on the

other hand Blue Island Restaurant indicates that debt of the company of the company is

more as compared to the investment made by the owner.

Debt to assets ratio: - this ratio shows the proportion of debts over the total assets of the

company. Therefore, it can be concluded that ratio of Sweet Menu restaurant is better

than Blue Island restaurant.

15

the cost of its production.

Net profit ratio: - The following calculation shows that net profit ratio of Blue Island

restaurant (i.e.31.70%) is more than that of Sweet Menu restaurant (i.e. 24.28%). The

reason behind this could be that Blue Island Restaurant is effectively managing its

operational costs and cost of production. This in turn have direct impact on the

profitability of the company.

Liquidity Ratio

Current ratio: - Current ratio indicates the liquid cash available with the company.

Therefore, from the following comparison it could be concluded that capability of

meeting short term requirement of Sweet Menu Restaurant is better than that of Blue

Island Restaurant. This in turn also indicates that current liabilities of the company is

more that its current assets.

Quick ratio: - This ratio shows that liquidity of the organization including the current

assets and current liabilities but excluding the stock (Sources of finance. 2012).

Therefore, from the following comparison it could be concluded that Quick ratio of

Sweet Menu restaurant is higher than that of Blue Island restaurant. The reason behind

this could be that company is able to meet its short term obligations.

Solvency Ratio

Stock turnover ratio: - This ratio shows the efficiency of the company to crook its stock

into sales. Therefore, by comparing the both the company ratio it could concluded that

efficiency of changing the stock is better of Sweet Menu Restaurant as compared to Blue

Island restaurant.

Debt equity ratio: - higher debt equity ratio of Sweet Menu Restaurant indicates that

debt of the company is lower and investment made by the owner is high. Similarly, on the

other hand Blue Island Restaurant indicates that debt of the company of the company is

more as compared to the investment made by the owner.

Debt to assets ratio: - this ratio shows the proportion of debts over the total assets of the

company. Therefore, it can be concluded that ratio of Sweet Menu restaurant is better

than Blue Island restaurant.

15

Thus, after comparing the overall position of the both the companies it could be calculated

that market position of Sweet Menu Restaurant are more favourable than that of Blue Island

Restaurant.

CONCLUSION

The following report emphasis on the various sources of finance available with the

company. In these report appropriate sources of finance for the Blue Island Restaurant to expand

its business is concluded. In this importance of financial planning are also concluded. In this

report cash budget of the company is analyzed in order to find out its actual position. In this

various techniques are used in order to decide which proposal will be beneficial for the company.

In this report unit cost of the company is also calculated. At last, various profitability, solvency

and liquidity ratios are calculated in order to compare the financial position of both the

companies (i.e. Blue Island Restaurant and Sweet Menu Restaurant).

16

that market position of Sweet Menu Restaurant are more favourable than that of Blue Island

Restaurant.

CONCLUSION

The following report emphasis on the various sources of finance available with the

company. In these report appropriate sources of finance for the Blue Island Restaurant to expand

its business is concluded. In this importance of financial planning are also concluded. In this

report cash budget of the company is analyzed in order to find out its actual position. In this

various techniques are used in order to decide which proposal will be beneficial for the company.

In this report unit cost of the company is also calculated. At last, various profitability, solvency

and liquidity ratios are calculated in order to compare the financial position of both the

companies (i.e. Blue Island Restaurant and Sweet Menu Restaurant).

16

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

REFERENCES

Beaver, W. H., McNichols, M. F. and Rhie, J. W., 2005. Have financial statements become less

informative? Evidence from the ability of financial ratios to predict bankruptcy. Review

of Accounting Studies. 10(1). pp. 93-122.

Bellas, A., Toudas, K. and Papadatos, K., 2007. The consequences of applying International

Accounting Standards (IAS) to the financial statements of Greek companies. In 30th

Annual Congress of European Accounting Association, Lisbon-Portugal.

Brigham, E. ,2013. Financial Management: Theory and Practice. Cengage Learning.

Broadbent, M. and Cullen, J. 2012. Managing Financial Resources. Routledge.

Butters, J. 2004 .Managing finances for a fulfilled Canadian retirement. Leadership in Health

Services .17 (1). pp.12 – 18.

Chandra, P., 2011. Financial management. Tata McGraw-Hill Education.

DRURY, C.M., 2013. Management and cost accounting. Springer.

Eccles, T. and Holt, A., 2005. Financial statements and corporate accounts: the conceptual

framework. Property Management. 23(5). pp. 374-387.

Efendi, J., Srivastava, A. and Swanson, E. P., 2007. Why do corporate managers misstate

financial statements? The role of option compensation and other factors. Journal of

Financial Economics. 85(3). pp. 667-708.

Hursti, J. and Maula, M.V., 2007. Acquiring financial resources from foreign equity capital

markets: An examination of factors influencing foreign initial public offerings. Journal

of Business Venturing. 22(6). pp.833-851.

Muradoglu, G. and Harvey, N. 2012. Behavioural finance: the role of psychological factors in

financial decisions. Review of Behavioural Finance 4 (2). pp.68 – 80.

Paramasivan, C. 2009. Financial management. New age international.

Ryan, J.F., 2005. Institutional expenditures and student engagement: a role for financial

resources in enhancing student learning and development?. Research in higher

education. 46(2). pp.235-249.

Shahrokhi, M. 2008. E‐finance: status, innovations, resources and future challenges. Managerial

Finance . 34 (6). pp.365 – 398.

Stolwy, H. and Lebas, M., 2006. Financial Accounting and Reporting. Cengage Learning

Thomas, H.G., 2008, Managing Financial Resources. Open University Press .

Tulsian, C. P., 2002. Financial Accounting. Pearson Education India.

17

Beaver, W. H., McNichols, M. F. and Rhie, J. W., 2005. Have financial statements become less

informative? Evidence from the ability of financial ratios to predict bankruptcy. Review

of Accounting Studies. 10(1). pp. 93-122.

Bellas, A., Toudas, K. and Papadatos, K., 2007. The consequences of applying International

Accounting Standards (IAS) to the financial statements of Greek companies. In 30th

Annual Congress of European Accounting Association, Lisbon-Portugal.

Brigham, E. ,2013. Financial Management: Theory and Practice. Cengage Learning.

Broadbent, M. and Cullen, J. 2012. Managing Financial Resources. Routledge.

Butters, J. 2004 .Managing finances for a fulfilled Canadian retirement. Leadership in Health

Services .17 (1). pp.12 – 18.

Chandra, P., 2011. Financial management. Tata McGraw-Hill Education.

DRURY, C.M., 2013. Management and cost accounting. Springer.

Eccles, T. and Holt, A., 2005. Financial statements and corporate accounts: the conceptual

framework. Property Management. 23(5). pp. 374-387.

Efendi, J., Srivastava, A. and Swanson, E. P., 2007. Why do corporate managers misstate

financial statements? The role of option compensation and other factors. Journal of

Financial Economics. 85(3). pp. 667-708.

Hursti, J. and Maula, M.V., 2007. Acquiring financial resources from foreign equity capital

markets: An examination of factors influencing foreign initial public offerings. Journal

of Business Venturing. 22(6). pp.833-851.

Muradoglu, G. and Harvey, N. 2012. Behavioural finance: the role of psychological factors in

financial decisions. Review of Behavioural Finance 4 (2). pp.68 – 80.

Paramasivan, C. 2009. Financial management. New age international.

Ryan, J.F., 2005. Institutional expenditures and student engagement: a role for financial

resources in enhancing student learning and development?. Research in higher

education. 46(2). pp.235-249.

Shahrokhi, M. 2008. E‐finance: status, innovations, resources and future challenges. Managerial

Finance . 34 (6). pp.365 – 398.

Stolwy, H. and Lebas, M., 2006. Financial Accounting and Reporting. Cengage Learning

Thomas, H.G., 2008, Managing Financial Resources. Open University Press .

Tulsian, C. P., 2002. Financial Accounting. Pearson Education India.

17

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.