Managerial Economics Case Study: The 2008 GFC & UAE Banking Sector

VerifiedAdded on 2023/06/15

|23

|12514

|290

Case Study

AI Summary

This case study analyzes the impact of the 2008 Global Financial Crisis (GFC) on the banking sector in the United Arab Emirates (UAE), applying managerial economics concepts to understand the economic factors contributing to the crisis and its subsequent effects on UAE banks, the economic market, and employment within the banking sector. It aims to provide an in-depth understanding of how the GFC affected the UAE's banking system, including specific banks that were impacted, the broader economic consequences for the UAE, and the resulting effects on bank employees, such as terminations. The study follows a structured format, including an abstract, introduction, body, and conclusion, adhering to specific formatting guidelines (Times New Roman, 12pt font, 1.5 spacing) and APA style referencing, utilizing free online articles, journals, books, and websites as sources.

Journal of Islamic Accounting and Business Research

Financial development, Islamic finance and economic growth: evidence of the

UAE

Hajer Zarrouk, Teheni El Ghak, Elias Abu Al Haija,

Article information:

To cite this document:

Hajer Zarrouk, Teheni El Ghak, Elias Abu Al Haija, (2017) "Financial development, Islamic finance

and economic growth: evidence of the UAE", Journal of Islamic Accounting and Business Research,

Vol. 8 Issue: 1, pp.2-22, https://doi.org/10.1108/JIABR-05-2015-0020

Permanent link to this document:

https://doi.org/10.1108/JIABR-05-2015-0020

Downloaded on: 02 January 2018, At: 05:01 (PT)

References: this document contains references to 51 other documents.

To copy this document: permissions@emeraldinsight.com

The fulltext of this document has been downloaded 3140 times since 2017*

Users who downloaded this article also downloaded:

(2017),"Poverty alleviation through financing microenterprises with equity finance", Journal of

Islamic Accounting and Business Research, Vol. 8 Iss 1 pp. 87-99 <a href="https://doi.org/10.1108/

JIABR-07-2013-0022">https://doi.org/10.1108/JIABR-07-2013-0022</a>

(2015),"The global financial crisis and Islamic finance: a review of selected literature", Journal of

Islamic Accounting and Business Research, Vol. 6 Iss 1 pp. 94-106 <a href="https://doi.org/10.1108/

JIABR-03-2012-0015">https://doi.org/10.1108/JIABR-03-2012-0015</a>

Access to this document was granted through an Emerald subscription provided by emerald-

srm:393177 []

For Authors

If you would like to write for this, or any other Emerald publication, then please use our Emera

for Authors service information about how to choose which publication to write for and submis

guidelines are available for all. Please visit www.emeraldinsight.com/authors for more informa

About Emerald www.emeraldinsight.com

Emerald is a global publisher linking research and practice to the benefit of society. The compa

manages a portfolio of more than 290 journals and over 2,350 books and book series volumes

well as providing an extensive range of online products and additional customer resources and

services.

Emerald is both COUNTER 4 and TRANSFER compliant. The organization is a partner of the

Committee on Publication Ethics (COPE) and also works with Portico and the LOCKSS initiative for

digital archive preservation.

Downloaded by RMIT University Library At 05:01 02 January 2018 (PT)

Financial development, Islamic finance and economic growth: evidence of the

UAE

Hajer Zarrouk, Teheni El Ghak, Elias Abu Al Haija,

Article information:

To cite this document:

Hajer Zarrouk, Teheni El Ghak, Elias Abu Al Haija, (2017) "Financial development, Islamic finance

and economic growth: evidence of the UAE", Journal of Islamic Accounting and Business Research,

Vol. 8 Issue: 1, pp.2-22, https://doi.org/10.1108/JIABR-05-2015-0020

Permanent link to this document:

https://doi.org/10.1108/JIABR-05-2015-0020

Downloaded on: 02 January 2018, At: 05:01 (PT)

References: this document contains references to 51 other documents.

To copy this document: permissions@emeraldinsight.com

The fulltext of this document has been downloaded 3140 times since 2017*

Users who downloaded this article also downloaded:

(2017),"Poverty alleviation through financing microenterprises with equity finance", Journal of

Islamic Accounting and Business Research, Vol. 8 Iss 1 pp. 87-99 <a href="https://doi.org/10.1108/

JIABR-07-2013-0022">https://doi.org/10.1108/JIABR-07-2013-0022</a>

(2015),"The global financial crisis and Islamic finance: a review of selected literature", Journal of

Islamic Accounting and Business Research, Vol. 6 Iss 1 pp. 94-106 <a href="https://doi.org/10.1108/

JIABR-03-2012-0015">https://doi.org/10.1108/JIABR-03-2012-0015</a>

Access to this document was granted through an Emerald subscription provided by emerald-

srm:393177 []

For Authors

If you would like to write for this, or any other Emerald publication, then please use our Emera

for Authors service information about how to choose which publication to write for and submis

guidelines are available for all. Please visit www.emeraldinsight.com/authors for more informa

About Emerald www.emeraldinsight.com

Emerald is a global publisher linking research and practice to the benefit of society. The compa

manages a portfolio of more than 290 journals and over 2,350 books and book series volumes

well as providing an extensive range of online products and additional customer resources and

services.

Emerald is both COUNTER 4 and TRANSFER compliant. The organization is a partner of the

Committee on Publication Ethics (COPE) and also works with Portico and the LOCKSS initiative for

digital archive preservation.

Downloaded by RMIT University Library At 05:01 02 January 2018 (PT)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

*Related content and download information correct at time of download.

Downloaded by RMIT University Library At 05:01 02 January 2018 (PT)

Downloaded by RMIT University Library At 05:01 02 January 2018 (PT)

Financial development, Islamic

finance and economic growth:

evidence of the UAE

Hajer Zarrouk

Emirates College of Technology, Abu Dhabi, UAE and

PS2D, Faculty of Economics Sciences and Management,

University Tunis ElManar, Tunis, Tunisia

Teheni El Ghak

Faculty of Economic Sciences and Management of Tunis,

University of Tunis ElManar, Tunis, Tunisia, and

Elias Abu Al Haija

Department of Banking and Finance, Emirates College of Technology,

Abu Dhabi, UAE

Abstract

Purpose –Does Islamic finance affect economic growth? The empirical literature in this area seem

be in early stages and the results are often mixed and inconclusive.This paper aims to examine the

causality between financialdevelopmentin general,Islamic finance in particular and realeconomic

growth in the United Arab Emirates (UAE).

Design/methodology/approach –Using time series data from 1990 to 2012,a bivariate vector

autoregressive modelwas used to document the financialdevelopment-Islamic finance-growth causal

nexus and to forecast growth under various scenarios.A composite indicator,as a proxy for financial

development,was determined using a non-parametric approach:data envelopment analysis.

Findings –The direction of causality runs from financialdevelopment to economic growth and the

reverse causality does not drive this relationship; however, the real gross domestic product (GDP)

Islamic financial development with no reverse effect.Furthermore,the forecasting results indicate that

the past relation has been a proxy for the future where financial development leads to better prog

real economic activity.This will likely continue to stimulate the development of Islamic finance.

Research limitations/implications –Because the financial markets in the UAE were established in

2000,this study ignored Islamic bonds and equity product.The value of the Sukuk listed on Dubai’s

exchangesis around US$36.75bn (Thomson Reuters,2015),reinforcing Dubai’sposition as an

international center for Sukuk activity.Among the most important tools of the Islamic financial sector,

Sukuk deserves a closer empirical study.This can set the agenda for future work.

Practical implications –The financial sector appears to be one of the main drivers of real economi

activity.However,more effort in the area of Islamic finance is needed to promote Shari’ah-compliant

economic activities and thus better contribute toward making Dubai-UAE the capitalof the Islamic

economy.

Originality/value –A new indicator was used to evaluate the financialstrength ofthe UAE and

analyze its effect on economic development.In addition,as one of UAE’emirates,Dubaideclared its

The authors would like to thank participants at The 2015 An Islamic Perspective of Accountin

Finance,Economics and Management (IPAFEM)conference,University of Glasgow,UK, for their

comments and suggestions.The authors specially thank Dr Mohamed Sherif.The authors take

responsibility for any errors in the article.

The current issue and full text archive of this journal is available on Emerald Insight at:

www.emeraldinsight.com/1759-0817.htm

JIABR

8,1

2

Received 22 May 2015

Revised 2 October 2015

24 November 2015

6 January 2016

Accepted 6 January 2016

Journal of Islamic Accounting and

Business Research

Vol. 8 No. 1, 2017

pp. 2-22

© Emerald Publishing Limited

1759-0817

DOI 10.1108/JIABR-05-2015-0020

Downloaded by RMIT University Library At 05:01 02 January 2018 (PT)

finance and economic growth:

evidence of the UAE

Hajer Zarrouk

Emirates College of Technology, Abu Dhabi, UAE and

PS2D, Faculty of Economics Sciences and Management,

University Tunis ElManar, Tunis, Tunisia

Teheni El Ghak

Faculty of Economic Sciences and Management of Tunis,

University of Tunis ElManar, Tunis, Tunisia, and

Elias Abu Al Haija

Department of Banking and Finance, Emirates College of Technology,

Abu Dhabi, UAE

Abstract

Purpose –Does Islamic finance affect economic growth? The empirical literature in this area seem

be in early stages and the results are often mixed and inconclusive.This paper aims to examine the

causality between financialdevelopmentin general,Islamic finance in particular and realeconomic

growth in the United Arab Emirates (UAE).

Design/methodology/approach –Using time series data from 1990 to 2012,a bivariate vector

autoregressive modelwas used to document the financialdevelopment-Islamic finance-growth causal

nexus and to forecast growth under various scenarios.A composite indicator,as a proxy for financial

development,was determined using a non-parametric approach:data envelopment analysis.

Findings –The direction of causality runs from financialdevelopment to economic growth and the

reverse causality does not drive this relationship; however, the real gross domestic product (GDP)

Islamic financial development with no reverse effect.Furthermore,the forecasting results indicate that

the past relation has been a proxy for the future where financial development leads to better prog

real economic activity.This will likely continue to stimulate the development of Islamic finance.

Research limitations/implications –Because the financial markets in the UAE were established in

2000,this study ignored Islamic bonds and equity product.The value of the Sukuk listed on Dubai’s

exchangesis around US$36.75bn (Thomson Reuters,2015),reinforcing Dubai’sposition as an

international center for Sukuk activity.Among the most important tools of the Islamic financial sector,

Sukuk deserves a closer empirical study.This can set the agenda for future work.

Practical implications –The financial sector appears to be one of the main drivers of real economi

activity.However,more effort in the area of Islamic finance is needed to promote Shari’ah-compliant

economic activities and thus better contribute toward making Dubai-UAE the capitalof the Islamic

economy.

Originality/value –A new indicator was used to evaluate the financialstrength ofthe UAE and

analyze its effect on economic development.In addition,as one of UAE’emirates,Dubaideclared its

The authors would like to thank participants at The 2015 An Islamic Perspective of Accountin

Finance,Economics and Management (IPAFEM)conference,University of Glasgow,UK, for their

comments and suggestions.The authors specially thank Dr Mohamed Sherif.The authors take

responsibility for any errors in the article.

The current issue and full text archive of this journal is available on Emerald Insight at:

www.emeraldinsight.com/1759-0817.htm

JIABR

8,1

2

Received 22 May 2015

Revised 2 October 2015

24 November 2015

6 January 2016

Accepted 6 January 2016

Journal of Islamic Accounting and

Business Research

Vol. 8 No. 1, 2017

pp. 2-22

© Emerald Publishing Limited

1759-0817

DOI 10.1108/JIABR-05-2015-0020

Downloaded by RMIT University Library At 05:01 02 January 2018 (PT)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

vision in 2013 to become the “capital of the Islamic economy”,this study analyzed the finance,Islamic

finance and growth relations over the period 2013-2022.

Keywords Islamic finance, Data envelopment analysis, Growth, Financial development, UAE,

bVAR

Paper type Research paper

1. Introduction

Economists have been interested in the role of expansion of financial institutions in resource

allocation and so in economic growth. Most researchers agree on the importance of the role of

the financial sector in real economic growth,both at the national and international levels

(Demirgüç-Kunt et al., 2004; Love, 2003). The financial sector plays a promotional role if it is

able to channel financial resources toward the industries with good growth opportunities.

When the financial sector is more developed, more financial resources can be allocated into

productive realinvestment and more physicalcapitalgets formed,which willstimulate

economic growth.

In the past two decades, the Islamic financial industry has emerged through the world.

Global Islamic banking assets have been growing rapidly. According to the World Islamic

Banking Competitiveness Report 2014-2015,they attained a compounded annual growth

rate of around 17 per cent from 2009 to 2013.InternationalIslamic banking assets with

commercial banks were set to exceed US$778bn in 2014. In particular, six markets – Qatar,

Indonesia,SaudiArabia,Malaysia,the United Arab Emirates (UAE)and Turkey – are

heading toward touching US$1.8tn by 2019.The performance and relative stability of

Islamic financial institutions during the financial crisis that hit the world in 2008 increased

the demand for Shari’ah-compliant products, not only from financiers in the Middle East and

other Muslim countries, but also by investors around the world seeking Islamic investment

as a means of diversification.

How important is Islamic financialdevelopment for economic development? Several

theoretical studies have been undertaken in the different fields of Islamic banking. Most of

them indicate the superiority of the Islamic financial industry compared to the conventional

one in terms of stability and efficiency (Hasan and Dridi, 2010; Hanif et al., 2012; Mansor et al.,

2015).However,only few studies have searched for empirical evidence connecting Islamic

finance and economic growth.

Against this background, this study attempts to respond to the question:

Q1. Do financial development and Islamic finance stimulate the real economic activity of

the UAE?

In line with earlier studies,the presentstudy closely examines the causality between

financialdevelopment and economic activity,but with some differences.First,previous

studies generally considered a sample ofcountries,including the UAE.These studies

provided a higher degree of generalization and not an internalvalidity specific to each

country,thereby increasing the need forcountry-specific studies.To the bestof our

knowledge, studies in this area on the UAE are very few (Al-Malkawi et al., 2012; Tabash and

Dhankar, 2014).

Meanwhile, the UAE’s gross domestic product (GDP) in 2013 was US$396.24bn, making

it the world’s 27th largest economy. The contribution of the oil sector to the UAE’s GDP is

decreasing because the government is attempting to diversify its economy.The UAE has

embarked on an overalleconomic reform package thatincluded policy and structural

reforms in the financialsector.The role of Islamic finance,as a segment of the global

financial system,has also been a key focus in development policy discussions.Therefore,

3

Islamic finance

and economic

growth

Downloaded by RMIT University Library At 05:01 02 January 2018 (PT)

finance and growth relations over the period 2013-2022.

Keywords Islamic finance, Data envelopment analysis, Growth, Financial development, UAE,

bVAR

Paper type Research paper

1. Introduction

Economists have been interested in the role of expansion of financial institutions in resource

allocation and so in economic growth. Most researchers agree on the importance of the role of

the financial sector in real economic growth,both at the national and international levels

(Demirgüç-Kunt et al., 2004; Love, 2003). The financial sector plays a promotional role if it is

able to channel financial resources toward the industries with good growth opportunities.

When the financial sector is more developed, more financial resources can be allocated into

productive realinvestment and more physicalcapitalgets formed,which willstimulate

economic growth.

In the past two decades, the Islamic financial industry has emerged through the world.

Global Islamic banking assets have been growing rapidly. According to the World Islamic

Banking Competitiveness Report 2014-2015,they attained a compounded annual growth

rate of around 17 per cent from 2009 to 2013.InternationalIslamic banking assets with

commercial banks were set to exceed US$778bn in 2014. In particular, six markets – Qatar,

Indonesia,SaudiArabia,Malaysia,the United Arab Emirates (UAE)and Turkey – are

heading toward touching US$1.8tn by 2019.The performance and relative stability of

Islamic financial institutions during the financial crisis that hit the world in 2008 increased

the demand for Shari’ah-compliant products, not only from financiers in the Middle East and

other Muslim countries, but also by investors around the world seeking Islamic investment

as a means of diversification.

How important is Islamic financialdevelopment for economic development? Several

theoretical studies have been undertaken in the different fields of Islamic banking. Most of

them indicate the superiority of the Islamic financial industry compared to the conventional

one in terms of stability and efficiency (Hasan and Dridi, 2010; Hanif et al., 2012; Mansor et al.,

2015).However,only few studies have searched for empirical evidence connecting Islamic

finance and economic growth.

Against this background, this study attempts to respond to the question:

Q1. Do financial development and Islamic finance stimulate the real economic activity of

the UAE?

In line with earlier studies,the presentstudy closely examines the causality between

financialdevelopment and economic activity,but with some differences.First,previous

studies generally considered a sample ofcountries,including the UAE.These studies

provided a higher degree of generalization and not an internalvalidity specific to each

country,thereby increasing the need forcountry-specific studies.To the bestof our

knowledge, studies in this area on the UAE are very few (Al-Malkawi et al., 2012; Tabash and

Dhankar, 2014).

Meanwhile, the UAE’s gross domestic product (GDP) in 2013 was US$396.24bn, making

it the world’s 27th largest economy. The contribution of the oil sector to the UAE’s GDP is

decreasing because the government is attempting to diversify its economy.The UAE has

embarked on an overalleconomic reform package thatincluded policy and structural

reforms in the financialsector.The role of Islamic finance,as a segment of the global

financial system,has also been a key focus in development policy discussions.Therefore,

3

Islamic finance

and economic

growth

Downloaded by RMIT University Library At 05:01 02 January 2018 (PT)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

focusing on the UAE economy in this study is significant. Second, previous studies g

considered financialdevelopmentor Islamic financing.In contrast,the presentstudy

considers the role of financialdevelopment in generaland Islamic finance in particular.

Third,while most of the empirical research has focused on single indicators of finan

development, this study mainly focuses on a composite index used to evaluate the

strength of the UAE. Fourth, economic forecasting has always been a central conce

researchers and policy-makers. It helps to establish plans and formulate objectives

the past decade,the vector autoregressive model (VAR) has become the standard tool

predicting economic activity.This study projects historicalvalues of variables into the

future by using a VAR.

The rest of the paper is structured as follows: Section 2 presents the theoretical

whereby the relationship between financialdevelopment,Islamic finance and economic

growth is outlined. Section 3 describes the details of the data and the empirical app

in this study. Section 4 reports and analyzes the results. Section 5 contains the con

2. Theoretical and empirical framework

A brief overview is provided in this section to highlight the fact that Islamic financia

similar to the conventional one,performs broad functions that may influence saving and

investment decisions and hence could have implications for real economic growth.These

include the provision of external financing as described bySchumpeter (1912) – financial

institutions provide funding to entrepreneurs with good growth prospects.Any industry

with high growth opportunities will require a relatively large amount of outside fina

Thus, the banking sector is considered an engine of economic growth.

Gurley and Shaw (1955),Goldsmith (1969)and Hicks (1969)have argued that more

developed financialmarketspromoteeconomicgrowth by mobilizing savingsand

facilitating investment.Mobilization may involve multiple bilateralcontracts between

productive units raising capital and agents with surplus resources.To economize on the

costs associated with multiple bilateral contracts, pooling may occur through interm

where thousands of investors entrust their wealth to intermediaries that invest in h

of firms (Sirri and Tufano,1995).This takes place when mobilizers convince savers of the

soundness of the investments.

King and Levine (1993)emphasized the role offinancialinstitutions in overcoming

informationalproblems.Indeed,there are large costs associated with evaluating firms,

managers and market conditions before making investment decisions.Individualsavers

may not have the ability to collect and produce information on possible investment

will be averse to invest in industries having little reliable information. High informat

may keep capitalfrom flowing to its highest value use.Financialinstitutions producing

better information on firms will thereby find more promising investments, and indu

efficient allocation of capital and foster growth (Greenwood and Jovanovic, 1990).

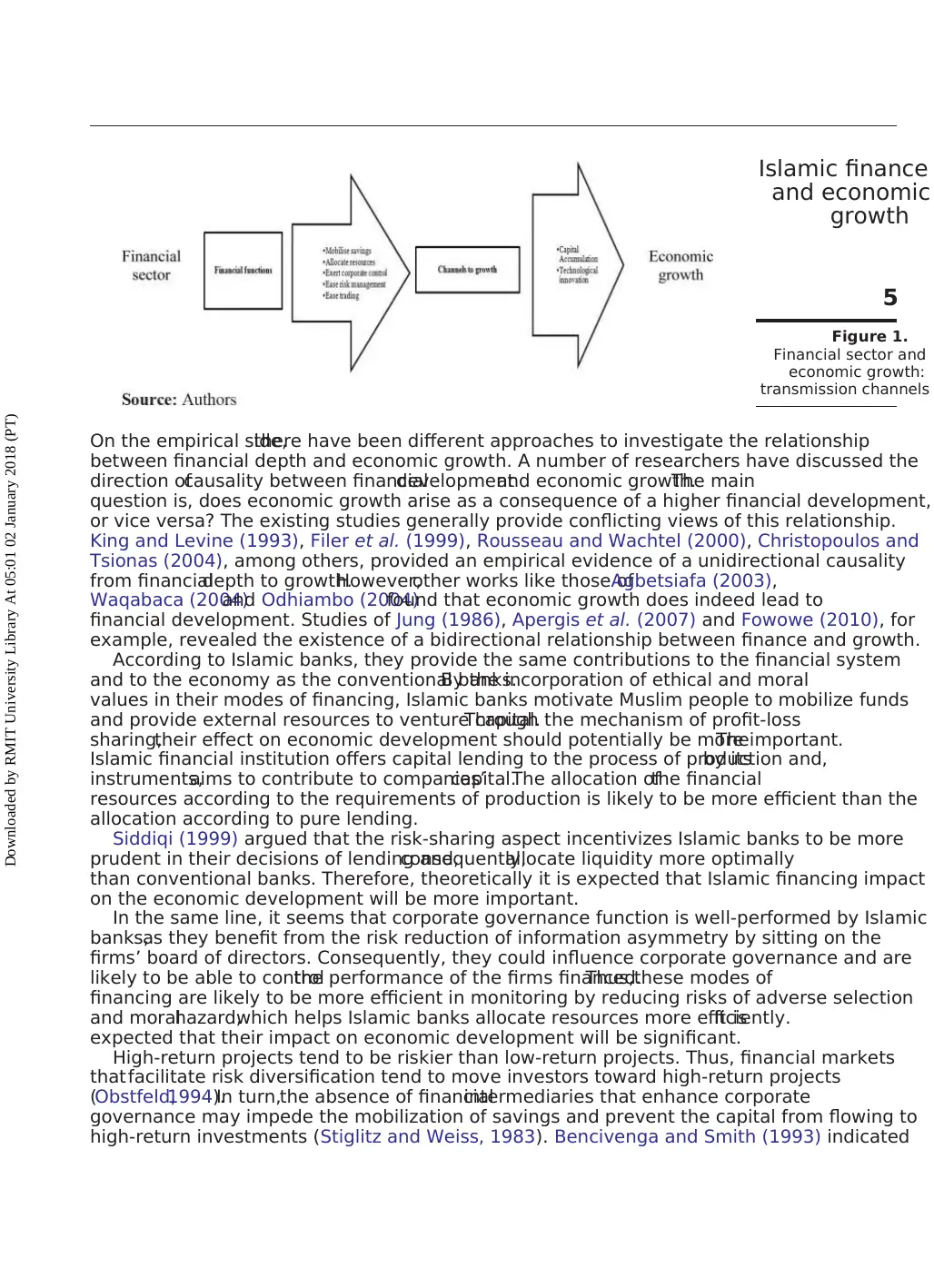

In this line of thinking, Levine (1997) stressed that market frictions like informati

transaction costs motivate the emergence of a well-developed financial sector whic

seen as well-offered financial services. Therefore, an increased financial service ma

economic growth through two main channels:capitalaccumulation and technological

innovation (Figure 1).

In addition,as suggested by Rajan and Zingales (1998),certain industries have a lag

between investment opportunities and cash flow.Industries with this inherent need for

externalfinance willrespond to growth opportunities in countries with well-developed

financial institutions.

JIABR

8,1

4

Downloaded by RMIT University Library At 05:01 02 January 2018 (PT)

considered financialdevelopmentor Islamic financing.In contrast,the presentstudy

considers the role of financialdevelopment in generaland Islamic finance in particular.

Third,while most of the empirical research has focused on single indicators of finan

development, this study mainly focuses on a composite index used to evaluate the

strength of the UAE. Fourth, economic forecasting has always been a central conce

researchers and policy-makers. It helps to establish plans and formulate objectives

the past decade,the vector autoregressive model (VAR) has become the standard tool

predicting economic activity.This study projects historicalvalues of variables into the

future by using a VAR.

The rest of the paper is structured as follows: Section 2 presents the theoretical

whereby the relationship between financialdevelopment,Islamic finance and economic

growth is outlined. Section 3 describes the details of the data and the empirical app

in this study. Section 4 reports and analyzes the results. Section 5 contains the con

2. Theoretical and empirical framework

A brief overview is provided in this section to highlight the fact that Islamic financia

similar to the conventional one,performs broad functions that may influence saving and

investment decisions and hence could have implications for real economic growth.These

include the provision of external financing as described bySchumpeter (1912) – financial

institutions provide funding to entrepreneurs with good growth prospects.Any industry

with high growth opportunities will require a relatively large amount of outside fina

Thus, the banking sector is considered an engine of economic growth.

Gurley and Shaw (1955),Goldsmith (1969)and Hicks (1969)have argued that more

developed financialmarketspromoteeconomicgrowth by mobilizing savingsand

facilitating investment.Mobilization may involve multiple bilateralcontracts between

productive units raising capital and agents with surplus resources.To economize on the

costs associated with multiple bilateral contracts, pooling may occur through interm

where thousands of investors entrust their wealth to intermediaries that invest in h

of firms (Sirri and Tufano,1995).This takes place when mobilizers convince savers of the

soundness of the investments.

King and Levine (1993)emphasized the role offinancialinstitutions in overcoming

informationalproblems.Indeed,there are large costs associated with evaluating firms,

managers and market conditions before making investment decisions.Individualsavers

may not have the ability to collect and produce information on possible investment

will be averse to invest in industries having little reliable information. High informat

may keep capitalfrom flowing to its highest value use.Financialinstitutions producing

better information on firms will thereby find more promising investments, and indu

efficient allocation of capital and foster growth (Greenwood and Jovanovic, 1990).

In this line of thinking, Levine (1997) stressed that market frictions like informati

transaction costs motivate the emergence of a well-developed financial sector whic

seen as well-offered financial services. Therefore, an increased financial service ma

economic growth through two main channels:capitalaccumulation and technological

innovation (Figure 1).

In addition,as suggested by Rajan and Zingales (1998),certain industries have a lag

between investment opportunities and cash flow.Industries with this inherent need for

externalfinance willrespond to growth opportunities in countries with well-developed

financial institutions.

JIABR

8,1

4

Downloaded by RMIT University Library At 05:01 02 January 2018 (PT)

On the empirical side,there have been different approaches to investigate the relationship

between financial depth and economic growth. A number of researchers have discussed the

direction ofcausality between financialdevelopmentand economic growth.The main

question is, does economic growth arise as a consequence of a higher financial development,

or vice versa? The existing studies generally provide conflicting views of this relationship.

King and Levine (1993), Filer et al. (1999), Rousseau and Wachtel (2000), Christopoulos and

Tsionas (2004), among others, provided an empirical evidence of a unidirectional causality

from financialdepth to growth.However,other works like those ofAgbetsiafa (2003),

Waqabaca (2004)and Odhiambo (2004)found that economic growth does indeed lead to

financial development. Studies of Jung (1986), Apergis et al. (2007) and Fowowe (2010), for

example, revealed the existence of a bidirectional relationship between finance and growth.

According to Islamic banks, they provide the same contributions to the financial system

and to the economy as the conventional banks.By the incorporation of ethical and moral

values in their modes of financing, Islamic banks motivate Muslim people to mobilize funds

and provide external resources to venture capital.Through the mechanism of profit-loss

sharing,their effect on economic development should potentially be more important.The

Islamic financial institution offers capital lending to the process of production and,by its

instruments,aims to contribute to companies’capital.The allocation ofthe financial

resources according to the requirements of production is likely to be more efficient than the

allocation according to pure lending.

Siddiqi (1999) argued that the risk-sharing aspect incentivizes Islamic banks to be more

prudent in their decisions of lending and,consequently,allocate liquidity more optimally

than conventional banks. Therefore, theoretically it is expected that Islamic financing impact

on the economic development will be more important.

In the same line, it seems that corporate governance function is well-performed by Islamic

banks,as they benefit from the risk reduction of information asymmetry by sitting on the

firms’ board of directors. Consequently, they could influence corporate governance and are

likely to be able to controlthe performance of the firms financed.Thus,these modes of

financing are likely to be more efficient in monitoring by reducing risks of adverse selection

and moralhazard,which helps Islamic banks allocate resources more efficiently.It is

expected that their impact on economic development will be significant.

High-return projects tend to be riskier than low-return projects. Thus, financial markets

thatfacilitate risk diversification tend to move investors toward high-return projects

(Obstfeld,1994).In turn,the absence of financialintermediaries that enhance corporate

governance may impede the mobilization of savings and prevent the capital from flowing to

high-return investments (Stiglitz and Weiss, 1983). Bencivenga and Smith (1993) indicated

Figure 1.

Financial sector and

economic growth:

transmission channels

5

Islamic finance

and economic

growth

Downloaded by RMIT University Library At 05:01 02 January 2018 (PT)

between financial depth and economic growth. A number of researchers have discussed the

direction ofcausality between financialdevelopmentand economic growth.The main

question is, does economic growth arise as a consequence of a higher financial development,

or vice versa? The existing studies generally provide conflicting views of this relationship.

King and Levine (1993), Filer et al. (1999), Rousseau and Wachtel (2000), Christopoulos and

Tsionas (2004), among others, provided an empirical evidence of a unidirectional causality

from financialdepth to growth.However,other works like those ofAgbetsiafa (2003),

Waqabaca (2004)and Odhiambo (2004)found that economic growth does indeed lead to

financial development. Studies of Jung (1986), Apergis et al. (2007) and Fowowe (2010), for

example, revealed the existence of a bidirectional relationship between finance and growth.

According to Islamic banks, they provide the same contributions to the financial system

and to the economy as the conventional banks.By the incorporation of ethical and moral

values in their modes of financing, Islamic banks motivate Muslim people to mobilize funds

and provide external resources to venture capital.Through the mechanism of profit-loss

sharing,their effect on economic development should potentially be more important.The

Islamic financial institution offers capital lending to the process of production and,by its

instruments,aims to contribute to companies’capital.The allocation ofthe financial

resources according to the requirements of production is likely to be more efficient than the

allocation according to pure lending.

Siddiqi (1999) argued that the risk-sharing aspect incentivizes Islamic banks to be more

prudent in their decisions of lending and,consequently,allocate liquidity more optimally

than conventional banks. Therefore, theoretically it is expected that Islamic financing impact

on the economic development will be more important.

In the same line, it seems that corporate governance function is well-performed by Islamic

banks,as they benefit from the risk reduction of information asymmetry by sitting on the

firms’ board of directors. Consequently, they could influence corporate governance and are

likely to be able to controlthe performance of the firms financed.Thus,these modes of

financing are likely to be more efficient in monitoring by reducing risks of adverse selection

and moralhazard,which helps Islamic banks allocate resources more efficiently.It is

expected that their impact on economic development will be significant.

High-return projects tend to be riskier than low-return projects. Thus, financial markets

thatfacilitate risk diversification tend to move investors toward high-return projects

(Obstfeld,1994).In turn,the absence of financialintermediaries that enhance corporate

governance may impede the mobilization of savings and prevent the capital from flowing to

high-return investments (Stiglitz and Weiss, 1983). Bencivenga and Smith (1993) indicated

Figure 1.

Financial sector and

economic growth:

transmission channels

5

Islamic finance

and economic

growth

Downloaded by RMIT University Library At 05:01 02 January 2018 (PT)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

that a well-functioning financial system improves corporate governance by econom

monitoring costs, reduces credit rationing and consequently stimulates productivity

accumulation and growth. Cˇihák and Hesse (2008) proved that the Islamic financial syste

less risky than the conventional system. By excluding the interest on the principal f

mechanism,Islamic banks preventall speculative activities related to the interestrate

expectations and thus reduce uncertainty.

Change in money flow will directly reflect on real activity by a change in the supp

demand of goods and services.The financing of Islamic banks through Musharakah and

Mudarabah is related to the real economic sphere. The time value of money is main

and other rates through the mechanism of profit and loss sharing are used. These fi

modes are likely to reduce risk and uncertainty,thereby helping Islamic banks to allocate

resources more efficiently.While inflation and interest rates are the basic motivation for

people to spend and circulate money in conventional economics, Islamic economy

methods to motivate people to circulate money and stimulate real investment. Peo

the Nisab, who pay Zakat of 2.5 per cent from their wealth to poor people, are mot

spend or invest money than to save it. The Prophet said that fund should be investe

it is eaten by Sadaqah. Thus, the received Zakat is also spent. Consequently, an inc

the demand increases the supply, and the prices are maintained at the same level

quantity produced increases.Real assets and money used only to exchange the resource

facilitate the growth of the Islamic economic system without inflation.

The empiricalstudieson Islamic financeconducted havemainly assessed the

performance and stability of Islamic financial institutions compared to conventional

(Hasan and Dridi,2010;Hanif et al.,2012;Arbi et al.,2014;Basov and Bhatti,2014;and

Mansor et al., 2015). There are few studies analyzing the relationship between Islam

and economic growth.Furqani and Mulyany (2009),for example,examined the dynamic

interactions between Islamic banking and the economic growth of Malaysia by usin

cointergration test and vector error correction model (VECM). They found that in th

run,only fixed investment caused the expansion of Islamic banks during 1997-1 thr

2005-4.However in the long run,there is evidence of a bi-directional relationship between

Islamic banks and fixed investment, and there is evidence to support that the incre

causes development of Islamic banking and not vice versa.Abduh and Chowdhury (2012)

analyzed the long run and dynamic relationship between Islamic banking developm

economic growth in the case of Bangladesh.The quarterly time-series data of economic

growth, total financing and total deposit of Islamic banks from Q1:2004 to Q2:2011

Applying cointergration and Granger’s causality,the study confirms a positive and

significant relationship between Islamic banks’ financing and economic growth in th

as well as in the short run. It implies that the development of Islamic banking is one

policies, which should be considered by the government to improve their income.

Severalcritics were highlighted by Goaied and Sassi(2010).They argued thatthe

empirical literature on the impact of Islamic finance on economic growth in Middle

and North African (MENA) countries is still in its early stages.In addition,they indicated

that a large number of empirical studies have used different types of econometric a

and a variety of indicators. The results are often mixed and inconclusive. Thus, the

attracts both academia and policy-makers to advance the knowledge in this area.

With respect to the case of the UAE,studies that tried to investigate the multi-faceted

relationship between financialdevelopment,Islamic finance and growth are very few.

Mosesov and Sahawneh (2005) examined the finance-growth nexus in the UAE.Based on

time series data (1973-2003), authors found no positive and/or significant evidence

that financialdevelopmenthad influenced the economic growth.However,the UAE

JIABR

8,1

6

Downloaded by RMIT University Library At 05:01 02 January 2018 (PT)

monitoring costs, reduces credit rationing and consequently stimulates productivity

accumulation and growth. Cˇihák and Hesse (2008) proved that the Islamic financial syste

less risky than the conventional system. By excluding the interest on the principal f

mechanism,Islamic banks preventall speculative activities related to the interestrate

expectations and thus reduce uncertainty.

Change in money flow will directly reflect on real activity by a change in the supp

demand of goods and services.The financing of Islamic banks through Musharakah and

Mudarabah is related to the real economic sphere. The time value of money is main

and other rates through the mechanism of profit and loss sharing are used. These fi

modes are likely to reduce risk and uncertainty,thereby helping Islamic banks to allocate

resources more efficiently.While inflation and interest rates are the basic motivation for

people to spend and circulate money in conventional economics, Islamic economy

methods to motivate people to circulate money and stimulate real investment. Peo

the Nisab, who pay Zakat of 2.5 per cent from their wealth to poor people, are mot

spend or invest money than to save it. The Prophet said that fund should be investe

it is eaten by Sadaqah. Thus, the received Zakat is also spent. Consequently, an inc

the demand increases the supply, and the prices are maintained at the same level

quantity produced increases.Real assets and money used only to exchange the resource

facilitate the growth of the Islamic economic system without inflation.

The empiricalstudieson Islamic financeconducted havemainly assessed the

performance and stability of Islamic financial institutions compared to conventional

(Hasan and Dridi,2010;Hanif et al.,2012;Arbi et al.,2014;Basov and Bhatti,2014;and

Mansor et al., 2015). There are few studies analyzing the relationship between Islam

and economic growth.Furqani and Mulyany (2009),for example,examined the dynamic

interactions between Islamic banking and the economic growth of Malaysia by usin

cointergration test and vector error correction model (VECM). They found that in th

run,only fixed investment caused the expansion of Islamic banks during 1997-1 thr

2005-4.However in the long run,there is evidence of a bi-directional relationship between

Islamic banks and fixed investment, and there is evidence to support that the incre

causes development of Islamic banking and not vice versa.Abduh and Chowdhury (2012)

analyzed the long run and dynamic relationship between Islamic banking developm

economic growth in the case of Bangladesh.The quarterly time-series data of economic

growth, total financing and total deposit of Islamic banks from Q1:2004 to Q2:2011

Applying cointergration and Granger’s causality,the study confirms a positive and

significant relationship between Islamic banks’ financing and economic growth in th

as well as in the short run. It implies that the development of Islamic banking is one

policies, which should be considered by the government to improve their income.

Severalcritics were highlighted by Goaied and Sassi(2010).They argued thatthe

empirical literature on the impact of Islamic finance on economic growth in Middle

and North African (MENA) countries is still in its early stages.In addition,they indicated

that a large number of empirical studies have used different types of econometric a

and a variety of indicators. The results are often mixed and inconclusive. Thus, the

attracts both academia and policy-makers to advance the knowledge in this area.

With respect to the case of the UAE,studies that tried to investigate the multi-faceted

relationship between financialdevelopment,Islamic finance and growth are very few.

Mosesov and Sahawneh (2005) examined the finance-growth nexus in the UAE.Based on

time series data (1973-2003), authors found no positive and/or significant evidence

that financialdevelopmenthad influenced the economic growth.However,the UAE

JIABR

8,1

6

Downloaded by RMIT University Library At 05:01 02 January 2018 (PT)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

economy is dependent on the world oilmarket prices.Such dependence may influence

financial development – economic growth nexus.

Also, Al-Malkawi et al. (2012) found that financial development and economic growth are

consistently and negatively correlated. The results display a bidirectional causality between

the two variables. These findings inform both the demand-following and the supply-leading

hypotheses for the UAE.

In a recent study,Tabash and Dhankar (2014), using time series data from 1990 to 2010,

revealed that there is a strong positive association between Islamic banks’ financing credited

to private sector and the GDP, Gross fixed capital formation and foreign direct investment

inflow (FDI). Their results indicate that a causal relationship happens only in one direction

from Islamic banks’financing to economic growth.Furthermore,the results show that

Islamic banks’ financing has contributed to the increase of investment and the attraction of

FDI in the long term and in a positive way in the UAE. However, a bi-directional relationship

was noted between Islamic Banks’ financing and FDI.

3. Data and methodology

3.1 Data

The present study examines the causalrelationship between financialdevelopment and

economic growth in the UAE using annual data from 1990 to 2012.

Three main sources are used: the World Bank’s World Development Indicators database,

IslamicBanks and FinancialInstitutionsInformation (IBIS)databaseand Financial

Development and Structure Dataset (2013) ofBeck et al. (2000)

Different indicators will proxy different aspects of the financial system and economic

development.In relation to the financialsystem,a number of variables are used which

include: domestic credit to private sector by banks as a percentage of GDP; domestic credit

provided by the financial sector as a percentage of GDP; and money and quasi-money as a

percentage of GDP.King and Levine (1993) believe that the rate of liquidity is a reliable

indicator of financial development. The two first indicators are used to assess the allocation

of financial assets and likely are more linked to economic growth through the channel of

financed investment. Total Islamic financial investment as a percentage of GDP is a proxy

for Islamic financial development.It discloses the sum of total outstanding amount of all

modes offinance (Murabaha,Mudarabah,Ijarah,Musharakah,Salam and Istisna),the

investment portfolio,the prepaid expenses and other receivable;and real GDP is used as

proxy for economic development.

The description and source of all variables of interest are presented inTable I.

Table I.

Variables description

Variables Description Notation Source

Level of economic

development

GDP per capita. Data are in constant

2005 local currency

R_GDP World Bank’s World Development

Indicators

Financial

deepening

Money and quasi-money (M2) as a

percentage of GDP

M2

Degree of financial

intermediation

Domestic credit provided by

financial sector as a percentage of

GDP

T_Credit

Degree of bank

development

Domestic credit to private sector

provided by banks as a percentage

of GDP

P_Credit Financial Development and Structure

Dataset (2013)

Beck et al. (2000)

Islamic bank

development

Total Islamic financial investment as

a percentage of GDP

Is_InvestIBIS data base

7

Islamic finance

and economic

growth

Downloaded by RMIT University Library At 05:01 02 January 2018 (PT)

financial development – economic growth nexus.

Also, Al-Malkawi et al. (2012) found that financial development and economic growth are

consistently and negatively correlated. The results display a bidirectional causality between

the two variables. These findings inform both the demand-following and the supply-leading

hypotheses for the UAE.

In a recent study,Tabash and Dhankar (2014), using time series data from 1990 to 2010,

revealed that there is a strong positive association between Islamic banks’ financing credited

to private sector and the GDP, Gross fixed capital formation and foreign direct investment

inflow (FDI). Their results indicate that a causal relationship happens only in one direction

from Islamic banks’financing to economic growth.Furthermore,the results show that

Islamic banks’ financing has contributed to the increase of investment and the attraction of

FDI in the long term and in a positive way in the UAE. However, a bi-directional relationship

was noted between Islamic Banks’ financing and FDI.

3. Data and methodology

3.1 Data

The present study examines the causalrelationship between financialdevelopment and

economic growth in the UAE using annual data from 1990 to 2012.

Three main sources are used: the World Bank’s World Development Indicators database,

IslamicBanks and FinancialInstitutionsInformation (IBIS)databaseand Financial

Development and Structure Dataset (2013) ofBeck et al. (2000)

Different indicators will proxy different aspects of the financial system and economic

development.In relation to the financialsystem,a number of variables are used which

include: domestic credit to private sector by banks as a percentage of GDP; domestic credit

provided by the financial sector as a percentage of GDP; and money and quasi-money as a

percentage of GDP.King and Levine (1993) believe that the rate of liquidity is a reliable

indicator of financial development. The two first indicators are used to assess the allocation

of financial assets and likely are more linked to economic growth through the channel of

financed investment. Total Islamic financial investment as a percentage of GDP is a proxy

for Islamic financial development.It discloses the sum of total outstanding amount of all

modes offinance (Murabaha,Mudarabah,Ijarah,Musharakah,Salam and Istisna),the

investment portfolio,the prepaid expenses and other receivable;and real GDP is used as

proxy for economic development.

The description and source of all variables of interest are presented inTable I.

Table I.

Variables description

Variables Description Notation Source

Level of economic

development

GDP per capita. Data are in constant

2005 local currency

R_GDP World Bank’s World Development

Indicators

Financial

deepening

Money and quasi-money (M2) as a

percentage of GDP

M2

Degree of financial

intermediation

Domestic credit provided by

financial sector as a percentage of

GDP

T_Credit

Degree of bank

development

Domestic credit to private sector

provided by banks as a percentage

of GDP

P_Credit Financial Development and Structure

Dataset (2013)

Beck et al. (2000)

Islamic bank

development

Total Islamic financial investment as

a percentage of GDP

Is_InvestIBIS data base

7

Islamic finance

and economic

growth

Downloaded by RMIT University Library At 05:01 02 January 2018 (PT)

3.2 Methodology

The methodology used to assess the relationship between financial development,Islamic

finance and economic growth is divided in three steps.First,to assess the effect of the

different dimensions included in the concept of financial development, the authors

a composite indicator determined with the non-parametric approach:data envelopment

analysis (DEA).This approach uses linear programming tools and defined a best pract

frontier that serves as a benchmark for estimating the performance of a given set o

Financial sector performance is represented by the distance to the best practice fro

weights for partial indicators are endogenously calculated in such a way that the di

minimized for every unit. More precisely, the authors present a variant of the DEA m

radial model without inputs (Lovell and Pastor, 1999). This approach is supposed to be ab

to direct all the partial indicators toward their maximum values. It is a DEA model d

toward the outputs,and only one input is a dummy equal to the unit for all the studied

decision making units (DMU)[1]. The purpose is to maximize the composite indicator give

the constraint of the partial indicators availability[2]. The DEA model is thus the fol

Max 兺i

vi Xi0 ⫽ CI 0

ST: 兺r

兺rYr0 ⫽ 1

兺i

vi Xij ⫺ 兺r

兺rYrj ⱕ 0 ∀j ⫽ 1… …N Normalization constraint

With N: number of studied DMU.

vi ⱖ 0 ∀i ⫽ 1… …p Non-negativity constraint

兺r ⱖ 0 ∀r ⫽ 1… …q

(1)

Vrj ⫽ 兺rYrj/ 兺 r⫽1

q 兺rYrj is the contribution of each partial indicator, as presented in the pre

section in the construction of composite indicator;

DMUj consumesamountXij of input i and producesamountY rj of outputr

(sub-indicators);

CI0 is a composite indicator (CI) for a given country. The authors obtain 0 ⱕ CI ⱕ 1

(expressed as a percentage) for each country j. A score close to 100 indicates a bet

financial sector performance;

i means sub-indicators;

Xi0 equal to unit;

vi is the weight of the ith indicator:The highest relative weights are assigned to the

sub-indicators for which the country j achieves the best relative financial sector per

in comparison to the other countries. The weights are not fixed a priori; the only re

in the formulation above is that they should be non-negative, which implies that th

non-decreasing function of the sub-indicators (non-negativity constraint).In the financial

composite index case, each sub-indicator/output i has the following interpretation:ij ⬎

Y ik, then country j has a more developed financial market than country k. The norm

constraint means that no country in the sample can achieve a value that is greater

under these weights.

The estimation of the composite indicators was carried out with the software EM

The second step involved the use of a bivariate vector autoregressive model (bV

analyze the long-term relationships between financial deepening and economic gro

first level of the bVAR study is to determine whether the series are stationary or noIn a

model, to ensure a correct evaluation, time series should be separated from all effe

JIABR

8,1

8

Downloaded by RMIT University Library At 05:01 02 January 2018 (PT)

The methodology used to assess the relationship between financial development,Islamic

finance and economic growth is divided in three steps.First,to assess the effect of the

different dimensions included in the concept of financial development, the authors

a composite indicator determined with the non-parametric approach:data envelopment

analysis (DEA).This approach uses linear programming tools and defined a best pract

frontier that serves as a benchmark for estimating the performance of a given set o

Financial sector performance is represented by the distance to the best practice fro

weights for partial indicators are endogenously calculated in such a way that the di

minimized for every unit. More precisely, the authors present a variant of the DEA m

radial model without inputs (Lovell and Pastor, 1999). This approach is supposed to be ab

to direct all the partial indicators toward their maximum values. It is a DEA model d

toward the outputs,and only one input is a dummy equal to the unit for all the studied

decision making units (DMU)[1]. The purpose is to maximize the composite indicator give

the constraint of the partial indicators availability[2]. The DEA model is thus the fol

Max 兺i

vi Xi0 ⫽ CI 0

ST: 兺r

兺rYr0 ⫽ 1

兺i

vi Xij ⫺ 兺r

兺rYrj ⱕ 0 ∀j ⫽ 1… …N Normalization constraint

With N: number of studied DMU.

vi ⱖ 0 ∀i ⫽ 1… …p Non-negativity constraint

兺r ⱖ 0 ∀r ⫽ 1… …q

(1)

Vrj ⫽ 兺rYrj/ 兺 r⫽1

q 兺rYrj is the contribution of each partial indicator, as presented in the pre

section in the construction of composite indicator;

DMUj consumesamountXij of input i and producesamountY rj of outputr

(sub-indicators);

CI0 is a composite indicator (CI) for a given country. The authors obtain 0 ⱕ CI ⱕ 1

(expressed as a percentage) for each country j. A score close to 100 indicates a bet

financial sector performance;

i means sub-indicators;

Xi0 equal to unit;

vi is the weight of the ith indicator:The highest relative weights are assigned to the

sub-indicators for which the country j achieves the best relative financial sector per

in comparison to the other countries. The weights are not fixed a priori; the only re

in the formulation above is that they should be non-negative, which implies that th

non-decreasing function of the sub-indicators (non-negativity constraint).In the financial

composite index case, each sub-indicator/output i has the following interpretation:ij ⬎

Y ik, then country j has a more developed financial market than country k. The norm

constraint means that no country in the sample can achieve a value that is greater

under these weights.

The estimation of the composite indicators was carried out with the software EM

The second step involved the use of a bivariate vector autoregressive model (bV

analyze the long-term relationships between financial deepening and economic gro

first level of the bVAR study is to determine whether the series are stationary or noIn a

model, to ensure a correct evaluation, time series should be separated from all effe

JIABR

8,1

8

Downloaded by RMIT University Library At 05:01 02 January 2018 (PT)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

series should be stationary.Thus,logarithms of time series were taken.The augmented

Dickey-Fuller [(1981)ADP] and Phillips and Perron [(1988)PP] tests were used.The lag

length of each variable is based on the minimum values of Schwarz information criterion

(SIC) statistics, and the max lag is four. The test equations include constant and trend as in

the following:

Lt ⫽ 兺 ⫹ t ⫹ 兺i⫽1

k⫺1

兺i⌬Lt⫺i ⫹ ␣Lt⫺1 ⫹ 兺t (2)

where,兺t i.i.d.N (0,兺兺

2) and L 兺 兺 R_GDP, P_Credit, M2, T_Credit, Is_Invest 兺 .The variables

are to be tested for non-stationary. The null hypothesis is the variable L contains unit root

and the alternative is the variable L is stationary (integrated of order 0, I(0)).

Then,Johansen cointergration test was applied to examine the long-term relationship

between financial development and economic growth. In this case, established numbers of

lag are very important.In this study,Akaike information criteria (AIC) were adopted for

selecting theoptimallag. In addition,in all models,stability testwas used and

auto-correlation tests to residuals were made.Models were generally stable and residuals

were not auto-correlated.And then,the Granger causality test was practiced to test the

causality between financialdevelopment,Islamic finance and economic growth.The

separate effect of Islamic bank development on real economic activity was distinguished.

The authors estimate the following regression equations:

Yt ⫽ ␥⫹ 兺i⫽1

k

␣iYt⫺i ⫹ 兺i⫽1

k

i Xt⫺i ⫹ 兺t (3)

Xt ⫽ 兺 ⫹ 兺i⫽1

k

␦iYt⫺i ⫹ 兺i⫽1

k

兺i Xt⫺i ⫹ 兺t (4)

where, Y ⫽ R_GDP and X 兺 兺 P_Credit, M2, T_Credit, Is_Invest 兺

兺t and 兺t are the respective intercepts and are white noise error terms,and k is the

maximum lag length used in each time series.

X Granger causes Y if thei coefficients are jointly significantly different from zero.

Similarly, Y Granger causes X if the␦i coefficients are jointly and significantly different from

zero.

Eviews software was used to test and analyze the results.

The third step was a VAR forecasting procedure to investigate a statistical association or

correlation pattern among variables,without imposing strong restrictions relating to the

structure of the economy, and then to use this information to predict likely future values for

each of the endogenous variables. The authors assumed that the relationship which existed

in the past between two variables will continue to exist in the future.Given that real GDP

forms part of every single model,the authors built the different VAR specifications by

permuting the candidate variables. All series were transformed with a natural logarithm to

improve their statisticalproperties and not seasonally adjusted,as seasonaladjustment

procedures generally apply two-sided filters and consequently,for any given point in the

past,give future information that was not available at the time of measurement.Enders

(1995) suggested that the lag lengths of the single VAR model are dynamically optimized

using the lowest values of AIC.

9

Islamic finance

and economic

growth

Downloaded by RMIT University Library At 05:01 02 January 2018 (PT)

Dickey-Fuller [(1981)ADP] and Phillips and Perron [(1988)PP] tests were used.The lag

length of each variable is based on the minimum values of Schwarz information criterion

(SIC) statistics, and the max lag is four. The test equations include constant and trend as in

the following:

Lt ⫽ 兺 ⫹ t ⫹ 兺i⫽1

k⫺1

兺i⌬Lt⫺i ⫹ ␣Lt⫺1 ⫹ 兺t (2)

where,兺t i.i.d.N (0,兺兺

2) and L 兺 兺 R_GDP, P_Credit, M2, T_Credit, Is_Invest 兺 .The variables

are to be tested for non-stationary. The null hypothesis is the variable L contains unit root

and the alternative is the variable L is stationary (integrated of order 0, I(0)).

Then,Johansen cointergration test was applied to examine the long-term relationship

between financial development and economic growth. In this case, established numbers of

lag are very important.In this study,Akaike information criteria (AIC) were adopted for

selecting theoptimallag. In addition,in all models,stability testwas used and

auto-correlation tests to residuals were made.Models were generally stable and residuals

were not auto-correlated.And then,the Granger causality test was practiced to test the

causality between financialdevelopment,Islamic finance and economic growth.The

separate effect of Islamic bank development on real economic activity was distinguished.

The authors estimate the following regression equations:

Yt ⫽ ␥⫹ 兺i⫽1

k

␣iYt⫺i ⫹ 兺i⫽1

k

i Xt⫺i ⫹ 兺t (3)

Xt ⫽ 兺 ⫹ 兺i⫽1

k

␦iYt⫺i ⫹ 兺i⫽1

k

兺i Xt⫺i ⫹ 兺t (4)

where, Y ⫽ R_GDP and X 兺 兺 P_Credit, M2, T_Credit, Is_Invest 兺

兺t and 兺t are the respective intercepts and are white noise error terms,and k is the

maximum lag length used in each time series.

X Granger causes Y if thei coefficients are jointly significantly different from zero.

Similarly, Y Granger causes X if the␦i coefficients are jointly and significantly different from

zero.

Eviews software was used to test and analyze the results.

The third step was a VAR forecasting procedure to investigate a statistical association or

correlation pattern among variables,without imposing strong restrictions relating to the

structure of the economy, and then to use this information to predict likely future values for

each of the endogenous variables. The authors assumed that the relationship which existed

in the past between two variables will continue to exist in the future.Given that real GDP

forms part of every single model,the authors built the different VAR specifications by

permuting the candidate variables. All series were transformed with a natural logarithm to

improve their statisticalproperties and not seasonally adjusted,as seasonaladjustment

procedures generally apply two-sided filters and consequently,for any given point in the

past,give future information that was not available at the time of measurement.Enders

(1995) suggested that the lag lengths of the single VAR model are dynamically optimized

using the lowest values of AIC.

9

Islamic finance

and economic

growth

Downloaded by RMIT University Library At 05:01 02 January 2018 (PT)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4. Empirical results and discussion

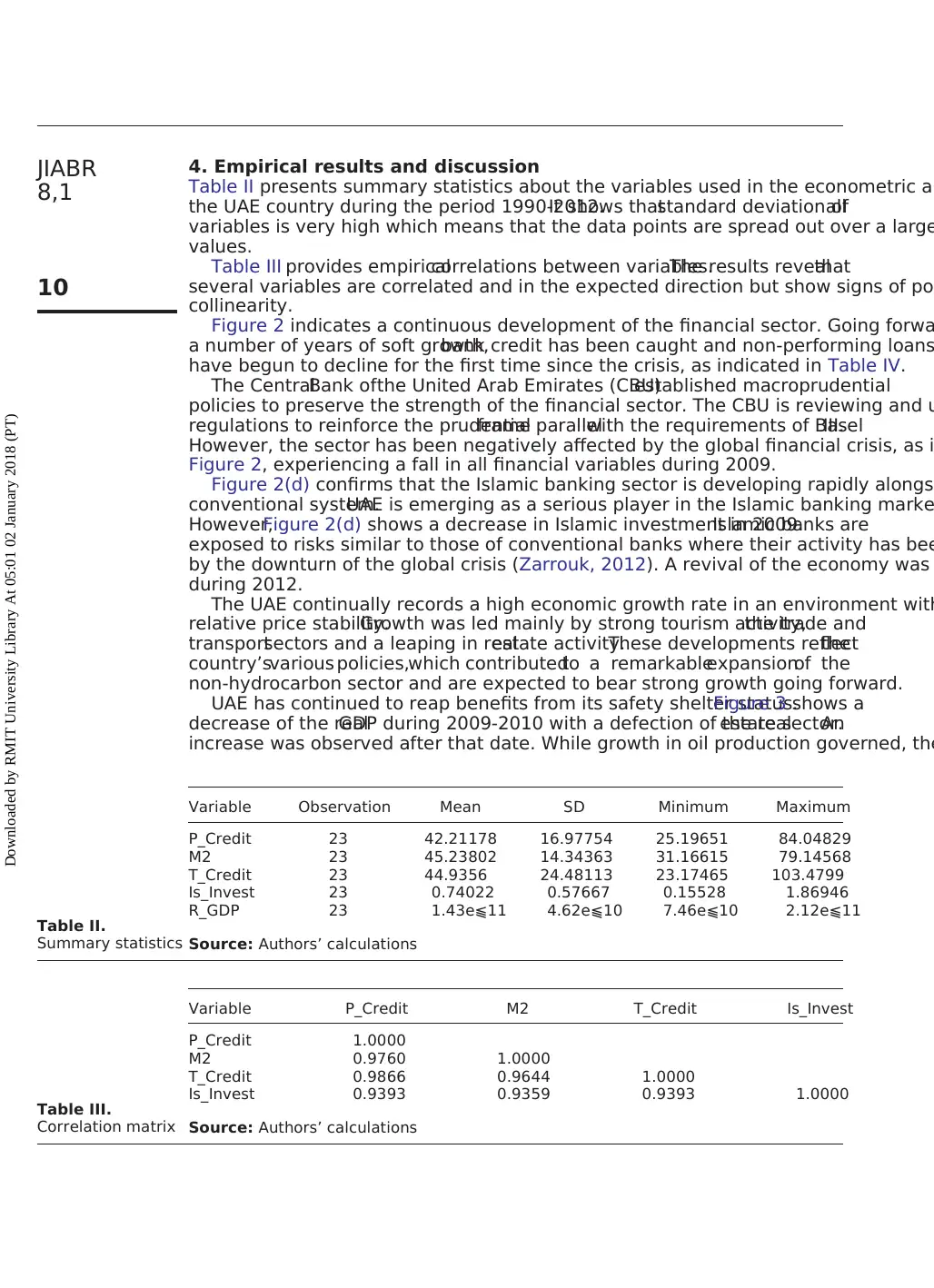

Table II presents summary statistics about the variables used in the econometric an

the UAE country during the period 1990-2012.It shows thatstandard deviation ofall

variables is very high which means that the data points are spread out over a large

values.

Table III provides empiricalcorrelations between variables.The results revealthat

several variables are correlated and in the expected direction but show signs of po

collinearity.

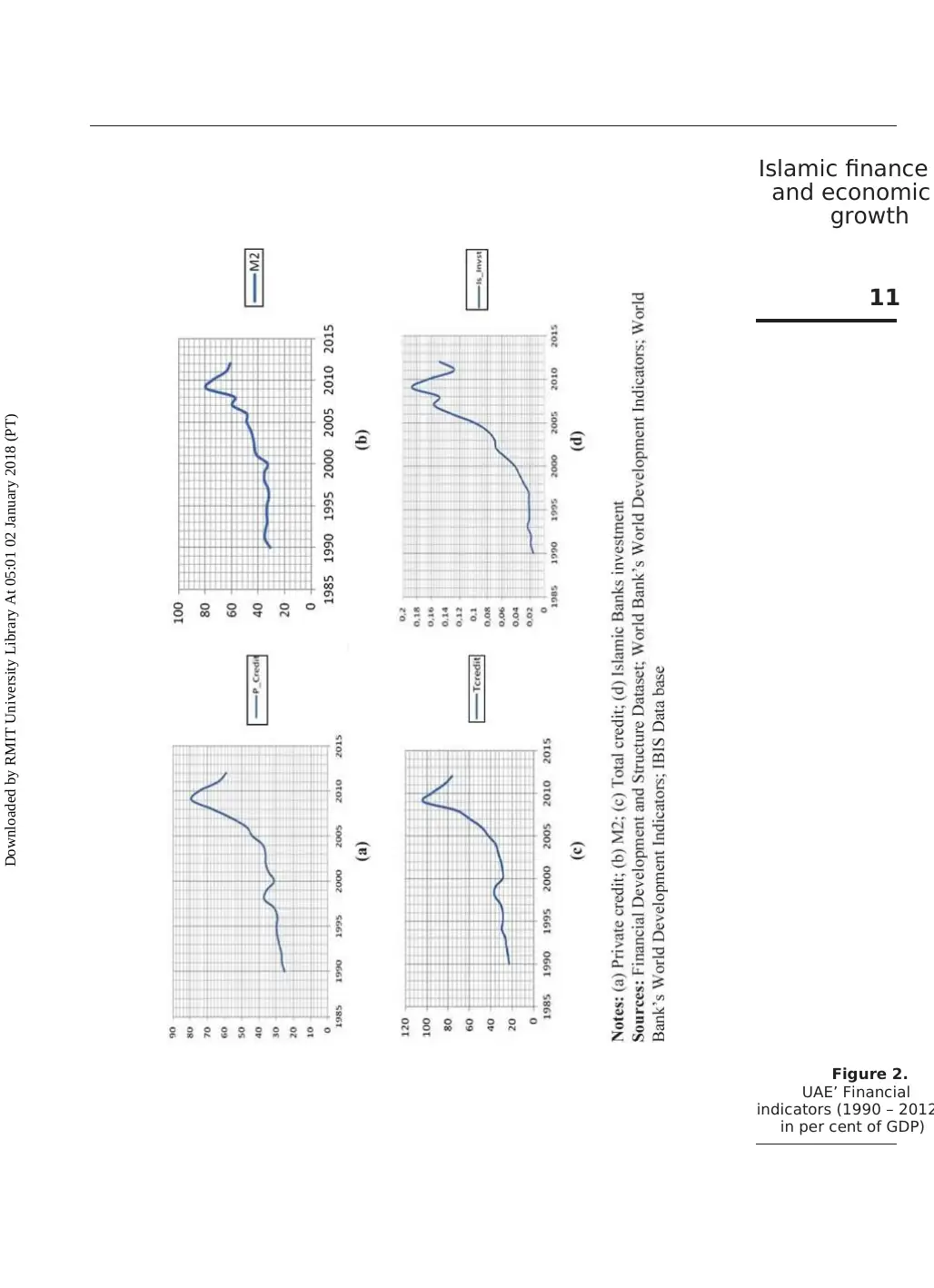

Figure 2 indicates a continuous development of the financial sector. Going forwa

a number of years of soft growth,bank credit has been caught and non-performing loans

have begun to decline for the first time since the crisis, as indicated in Table IV.

The CentralBank ofthe United Arab Emirates (CBU)established macroprudential

policies to preserve the strength of the financial sector. The CBU is reviewing and u

regulations to reinforce the prudentialframe parallelwith the requirements of BaselIII.

However, the sector has been negatively affected by the global financial crisis, as i

Figure 2, experiencing a fall in all financial variables during 2009.

Figure 2(d) confirms that the Islamic banking sector is developing rapidly alongs

conventional system.UAE is emerging as a serious player in the Islamic banking marke

However,Figure 2(d) shows a decrease in Islamic investment in 2009.Islamic banks are

exposed to risks similar to those of conventional banks where their activity has bee

by the downturn of the global crisis (Zarrouk, 2012). A revival of the economy was

during 2012.

The UAE continually records a high economic growth rate in an environment with

relative price stability.Growth was led mainly by strong tourism activity,the trade and

transportsectors and a leaping in realestate activity.These developments reflectthe

country’svarious policies,which contributedto a remarkableexpansionof the

non-hydrocarbon sector and are expected to bear strong growth going forward.

UAE has continued to reap benefits from its safety shelter status.Figure 3 shows a

decrease of the realGDP during 2009-2010 with a defection of the realestate sector.An

increase was observed after that date. While growth in oil production governed, the

Table II.

Summary statistics

Variable Observation Mean SD Minimum Maximum

P_Credit 23 42.21178 16.97754 25.19651 84.04829

M2 23 45.23802 14.34363 31.16615 79.14568

T_Credit 23 44.9356 24.48113 23.17465 103.4799

Is_Invest 23 0.74022 0.57667 0.15528 1.86946

R_GDP 23 1.43e⫹11 4.62e⫹10 7.46e⫹10 2.12e⫹11

Source: Authors’ calculations

Table III.

Correlation matrix

Variable P_Credit M2 T_Credit Is_Invest

P_Credit 1.0000

M2 0.9760 1.0000

T_Credit 0.9866 0.9644 1.0000

Is_Invest 0.9393 0.9359 0.9393 1.0000

Source: Authors’ calculations

JIABR

8,1

10

Downloaded by RMIT University Library At 05:01 02 January 2018 (PT)

Table II presents summary statistics about the variables used in the econometric an

the UAE country during the period 1990-2012.It shows thatstandard deviation ofall

variables is very high which means that the data points are spread out over a large

values.

Table III provides empiricalcorrelations between variables.The results revealthat

several variables are correlated and in the expected direction but show signs of po

collinearity.

Figure 2 indicates a continuous development of the financial sector. Going forwa

a number of years of soft growth,bank credit has been caught and non-performing loans

have begun to decline for the first time since the crisis, as indicated in Table IV.

The CentralBank ofthe United Arab Emirates (CBU)established macroprudential

policies to preserve the strength of the financial sector. The CBU is reviewing and u

regulations to reinforce the prudentialframe parallelwith the requirements of BaselIII.

However, the sector has been negatively affected by the global financial crisis, as i

Figure 2, experiencing a fall in all financial variables during 2009.

Figure 2(d) confirms that the Islamic banking sector is developing rapidly alongs

conventional system.UAE is emerging as a serious player in the Islamic banking marke

However,Figure 2(d) shows a decrease in Islamic investment in 2009.Islamic banks are

exposed to risks similar to those of conventional banks where their activity has bee

by the downturn of the global crisis (Zarrouk, 2012). A revival of the economy was

during 2012.

The UAE continually records a high economic growth rate in an environment with

relative price stability.Growth was led mainly by strong tourism activity,the trade and

transportsectors and a leaping in realestate activity.These developments reflectthe

country’svarious policies,which contributedto a remarkableexpansionof the

non-hydrocarbon sector and are expected to bear strong growth going forward.

UAE has continued to reap benefits from its safety shelter status.Figure 3 shows a

decrease of the realGDP during 2009-2010 with a defection of the realestate sector.An

increase was observed after that date. While growth in oil production governed, the

Table II.

Summary statistics

Variable Observation Mean SD Minimum Maximum

P_Credit 23 42.21178 16.97754 25.19651 84.04829

M2 23 45.23802 14.34363 31.16615 79.14568

T_Credit 23 44.9356 24.48113 23.17465 103.4799

Is_Invest 23 0.74022 0.57667 0.15528 1.86946

R_GDP 23 1.43e⫹11 4.62e⫹10 7.46e⫹10 2.12e⫹11

Source: Authors’ calculations

Table III.

Correlation matrix

Variable P_Credit M2 T_Credit Is_Invest

P_Credit 1.0000

M2 0.9760 1.0000

T_Credit 0.9866 0.9644 1.0000

Is_Invest 0.9393 0.9359 0.9393 1.0000

Source: Authors’ calculations

JIABR

8,1

10

Downloaded by RMIT University Library At 05:01 02 January 2018 (PT)

Figure 2.

UAE’ Financial

indicators (1990 – 2012

in per cent of GDP)

11

Islamic finance

and economic

growth

Downloaded by RMIT University Library At 05:01 02 January 2018 (PT)

UAE’ Financial

indicators (1990 – 2012

in per cent of GDP)

11

Islamic finance

and economic

growth

Downloaded by RMIT University Library At 05:01 02 January 2018 (PT)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 23

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.