Financial development, Islamic finance and economic growth: evidence of the UAE

Added on 2023-06-15

23 Pages12514 Words290 Views

Journal of Islamic Accounting and Business Research

Financial development, Islamic finance and economic growth: evidence of the

UAE

Hajer Zarrouk, Teheni El Ghak, Elias Abu Al Haija,

Article information:

To cite this document:

Hajer Zarrouk, Teheni El Ghak, Elias Abu Al Haija, (2017) "Financial development, Islamic finance

and economic growth: evidence of the UAE", Journal of Islamic Accounting and Business Research,

Vol. 8 Issue: 1, pp.2-22, https://doi.org/10.1108/JIABR-05-2015-0020

Permanent link to this document:

https://doi.org/10.1108/JIABR-05-2015-0020

Downloaded on: 02 January 2018, At: 05:01 (PT)

References: this document contains references to 51 other documents.

To copy this document: permissions@emeraldinsight.com

The fulltext of this document has been downloaded 3140 times since 2017*

Users who downloaded this article also downloaded:

(2017),"Poverty alleviation through financing microenterprises with equity finance", Journal of

Islamic Accounting and Business Research, Vol. 8 Iss 1 pp. 87-99 <a href="https://doi.org/10.1108/

JIABR-07-2013-0022">https://doi.org/10.1108/JIABR-07-2013-0022</a>

(2015),"The global financial crisis and Islamic finance: a review of selected literature", Journal of

Islamic Accounting and Business Research, Vol. 6 Iss 1 pp. 94-106 <a href="https://doi.org/10.1108/

JIABR-03-2012-0015">https://doi.org/10.1108/JIABR-03-2012-0015</a>

Access to this document was granted through an Emerald subscription provided by emerald-

srm:393177 []

For Authors

If you would like to write for this, or any other Emerald publication, then please use our Emerald

for Authors service information about how to choose which publication to write for and submission

guidelines are available for all. Please visit www.emeraldinsight.com/authors for more information.

About Emerald www.emeraldinsight.com

Emerald is a global publisher linking research and practice to the benefit of society. The company

manages a portfolio of more than 290 journals and over 2,350 books and book series volumes, as

well as providing an extensive range of online products and additional customer resources and

services.

Emerald is both COUNTER 4 and TRANSFER compliant. The organization is a partner of the

Committee on Publication Ethics (COPE) and also works with Portico and the LOCKSS initiative for

digital archive preservation.Downloaded by RMIT University Library At 05:01 02 January 2018 (PT)

Financial development, Islamic finance and economic growth: evidence of the

UAE

Hajer Zarrouk, Teheni El Ghak, Elias Abu Al Haija,

Article information:

To cite this document:

Hajer Zarrouk, Teheni El Ghak, Elias Abu Al Haija, (2017) "Financial development, Islamic finance

and economic growth: evidence of the UAE", Journal of Islamic Accounting and Business Research,

Vol. 8 Issue: 1, pp.2-22, https://doi.org/10.1108/JIABR-05-2015-0020

Permanent link to this document:

https://doi.org/10.1108/JIABR-05-2015-0020

Downloaded on: 02 January 2018, At: 05:01 (PT)

References: this document contains references to 51 other documents.

To copy this document: permissions@emeraldinsight.com

The fulltext of this document has been downloaded 3140 times since 2017*

Users who downloaded this article also downloaded:

(2017),"Poverty alleviation through financing microenterprises with equity finance", Journal of

Islamic Accounting and Business Research, Vol. 8 Iss 1 pp. 87-99 <a href="https://doi.org/10.1108/

JIABR-07-2013-0022">https://doi.org/10.1108/JIABR-07-2013-0022</a>

(2015),"The global financial crisis and Islamic finance: a review of selected literature", Journal of

Islamic Accounting and Business Research, Vol. 6 Iss 1 pp. 94-106 <a href="https://doi.org/10.1108/

JIABR-03-2012-0015">https://doi.org/10.1108/JIABR-03-2012-0015</a>

Access to this document was granted through an Emerald subscription provided by emerald-

srm:393177 []

For Authors

If you would like to write for this, or any other Emerald publication, then please use our Emerald

for Authors service information about how to choose which publication to write for and submission

guidelines are available for all. Please visit www.emeraldinsight.com/authors for more information.

About Emerald www.emeraldinsight.com

Emerald is a global publisher linking research and practice to the benefit of society. The company

manages a portfolio of more than 290 journals and over 2,350 books and book series volumes, as

well as providing an extensive range of online products and additional customer resources and

services.

Emerald is both COUNTER 4 and TRANSFER compliant. The organization is a partner of the

Committee on Publication Ethics (COPE) and also works with Portico and the LOCKSS initiative for

digital archive preservation.Downloaded by RMIT University Library At 05:01 02 January 2018 (PT)

*Related content and download information correct at time of download.Downloaded by RMIT University Library At 05:01 02 January 2018 (PT)

Financial development, Islamic

finance and economic growth:

evidence of the UAE

Hajer Zarrouk

Emirates College of Technology, Abu Dhabi, UAE and

PS2D, Faculty of Economics Sciences and Management,

University Tunis El Manar, Tunis, Tunisia

Teheni El Ghak

Faculty of Economic Sciences and Management of Tunis,

University of Tunis El Manar, Tunis, Tunisia, and

Elias Abu Al Haija

Department of Banking and Finance, Emirates College of Technology,

Abu Dhabi, UAE

Abstract

Purpose – Does Islamic finance affect economic growth? The empirical literature in this area seems to

be in early stages and the results are often mixed and inconclusive. This paper aims to examine the

causality between financial development in general, Islamic finance in particular and real economic

growth in the United Arab Emirates (UAE).

Design/methodology/approach – Using time series data from 1990 to 2012, a bivariate vector

autoregressive model was used to document the financial development-Islamic finance-growth causal

nexus and to forecast growth under various scenarios. A composite indicator, as a proxy for financial

development, was determined using a non-parametric approach: data envelopment analysis.

Findings – The direction of causality runs from financial development to economic growth and the

reverse causality does not drive this relationship; however, the real gross domestic product (GDP) causes

Islamic financial development with no reverse effect. Furthermore, the forecasting results indicate that

the past relation has been a proxy for the future where financial development leads to better progress in

real economic activity. This will likely continue to stimulate the development of Islamic finance.

Research limitations/implications – Because the financial markets in the UAE were established in

2000, this study ignored Islamic bonds and equity product. The value of the Sukuk listed on Dubai’s

exchanges is around US$36.75bn (Thomson Reuters, 2015), reinforcing Dubai’s position as an

international center for Sukuk activity. Among the most important tools of the Islamic financial sector,

Sukuk deserves a closer empirical study. This can set the agenda for future work.

Practical implications – The financial sector appears to be one of the main drivers of real economic

activity. However, more effort in the area of Islamic finance is needed to promote Shari’ah-compliant

economic activities and thus better contribute toward making Dubai-UAE the capital of the Islamic

economy.

Originality/value – A new indicator was used to evaluate the financial strength of the UAE and

analyze its effect on economic development. In addition, as one of UAE’ emirates, Dubai declared its

The authors would like to thank participants at The 2015 An Islamic Perspective of Accounting,

Finance, Economics and Management (IPAFEM) conference, University of Glasgow, UK, for their

comments and suggestions. The authors specially thank Dr Mohamed Sherif. The authors take

responsibility for any errors in the article.

The current issue and full text archive of this journal is available on Emerald Insight at:

www.emeraldinsight.com/1759-0817.htm

JIABR

8,1

2

Received 22 May 2015

Revised 2 October 2015

24 November 2015

6 January 2016

Accepted 6 January 2016

Journal of Islamic Accounting and

Business Research

Vol. 8 No. 1, 2017

pp. 2-22

© Emerald Publishing Limited

1759-0817

DOI 10.1108/JIABR-05-2015-0020Downloaded by RMIT University Library At 05:01 02 January 2018 (PT)

finance and economic growth:

evidence of the UAE

Hajer Zarrouk

Emirates College of Technology, Abu Dhabi, UAE and

PS2D, Faculty of Economics Sciences and Management,

University Tunis El Manar, Tunis, Tunisia

Teheni El Ghak

Faculty of Economic Sciences and Management of Tunis,

University of Tunis El Manar, Tunis, Tunisia, and

Elias Abu Al Haija

Department of Banking and Finance, Emirates College of Technology,

Abu Dhabi, UAE

Abstract

Purpose – Does Islamic finance affect economic growth? The empirical literature in this area seems to

be in early stages and the results are often mixed and inconclusive. This paper aims to examine the

causality between financial development in general, Islamic finance in particular and real economic

growth in the United Arab Emirates (UAE).

Design/methodology/approach – Using time series data from 1990 to 2012, a bivariate vector

autoregressive model was used to document the financial development-Islamic finance-growth causal

nexus and to forecast growth under various scenarios. A composite indicator, as a proxy for financial

development, was determined using a non-parametric approach: data envelopment analysis.

Findings – The direction of causality runs from financial development to economic growth and the

reverse causality does not drive this relationship; however, the real gross domestic product (GDP) causes

Islamic financial development with no reverse effect. Furthermore, the forecasting results indicate that

the past relation has been a proxy for the future where financial development leads to better progress in

real economic activity. This will likely continue to stimulate the development of Islamic finance.

Research limitations/implications – Because the financial markets in the UAE were established in

2000, this study ignored Islamic bonds and equity product. The value of the Sukuk listed on Dubai’s

exchanges is around US$36.75bn (Thomson Reuters, 2015), reinforcing Dubai’s position as an

international center for Sukuk activity. Among the most important tools of the Islamic financial sector,

Sukuk deserves a closer empirical study. This can set the agenda for future work.

Practical implications – The financial sector appears to be one of the main drivers of real economic

activity. However, more effort in the area of Islamic finance is needed to promote Shari’ah-compliant

economic activities and thus better contribute toward making Dubai-UAE the capital of the Islamic

economy.

Originality/value – A new indicator was used to evaluate the financial strength of the UAE and

analyze its effect on economic development. In addition, as one of UAE’ emirates, Dubai declared its

The authors would like to thank participants at The 2015 An Islamic Perspective of Accounting,

Finance, Economics and Management (IPAFEM) conference, University of Glasgow, UK, for their

comments and suggestions. The authors specially thank Dr Mohamed Sherif. The authors take

responsibility for any errors in the article.

The current issue and full text archive of this journal is available on Emerald Insight at:

www.emeraldinsight.com/1759-0817.htm

JIABR

8,1

2

Received 22 May 2015

Revised 2 October 2015

24 November 2015

6 January 2016

Accepted 6 January 2016

Journal of Islamic Accounting and

Business Research

Vol. 8 No. 1, 2017

pp. 2-22

© Emerald Publishing Limited

1759-0817

DOI 10.1108/JIABR-05-2015-0020Downloaded by RMIT University Library At 05:01 02 January 2018 (PT)

vision in 2013 to become the “capital of the Islamic economy”, this study analyzed the finance, Islamic

finance and growth relations over the period 2013-2022.

Keywords Islamic finance, Data envelopment analysis, Growth, Financial development, UAE,

bVAR

Paper type Research paper

1. Introduction

Economists have been interested in the role of expansion of financial institutions in resource

allocation and so in economic growth. Most researchers agree on the importance of the role of

the financial sector in real economic growth, both at the national and international levels

(Demirgüç-Kunt et al., 2004; Love, 2003). The financial sector plays a promotional role if it is

able to channel financial resources toward the industries with good growth opportunities.

When the financial sector is more developed, more financial resources can be allocated into

productive real investment and more physical capital gets formed, which will stimulate

economic growth.

In the past two decades, the Islamic financial industry has emerged through the world.

Global Islamic banking assets have been growing rapidly. According to the World Islamic

Banking Competitiveness Report 2014-2015, they attained a compounded annual growth

rate of around 17 per cent from 2009 to 2013. International Islamic banking assets with

commercial banks were set to exceed US$778bn in 2014. In particular, six markets – Qatar,

Indonesia, Saudi Arabia, Malaysia, the United Arab Emirates (UAE) and Turkey – are

heading toward touching US$1.8tn by 2019. The performance and relative stability of

Islamic financial institutions during the financial crisis that hit the world in 2008 increased

the demand for Shari’ah-compliant products, not only from financiers in the Middle East and

other Muslim countries, but also by investors around the world seeking Islamic investment

as a means of diversification.

How important is Islamic financial development for economic development? Several

theoretical studies have been undertaken in the different fields of Islamic banking. Most of

them indicate the superiority of the Islamic financial industry compared to the conventional

one in terms of stability and efficiency (Hasan and Dridi, 2010; Hanif et al., 2012; Mansor et al.,

2015). However, only few studies have searched for empirical evidence connecting Islamic

finance and economic growth.

Against this background, this study attempts to respond to the question:

Q1. Do financial development and Islamic finance stimulate the real economic activity of

the UAE?

In line with earlier studies, the present study closely examines the causality between

financial development and economic activity, but with some differences. First, previous

studies generally considered a sample of countries, including the UAE. These studies

provided a higher degree of generalization and not an internal validity specific to each

country, thereby increasing the need for country-specific studies. To the best of our

knowledge, studies in this area on the UAE are very few (Al-Malkawi et al., 2012; Tabash and

Dhankar, 2014).

Meanwhile, the UAE’s gross domestic product (GDP) in 2013 was US$396.24bn, making

it the world’s 27th largest economy. The contribution of the oil sector to the UAE’s GDP is

decreasing because the government is attempting to diversify its economy. The UAE has

embarked on an overall economic reform package that included policy and structural

reforms in the financial sector. The role of Islamic finance, as a segment of the global

financial system, has also been a key focus in development policy discussions. Therefore,

3

Islamic finance

and economic

growthDownloaded by RMIT University Library At 05:01 02 January 2018 (PT)

finance and growth relations over the period 2013-2022.

Keywords Islamic finance, Data envelopment analysis, Growth, Financial development, UAE,

bVAR

Paper type Research paper

1. Introduction

Economists have been interested in the role of expansion of financial institutions in resource

allocation and so in economic growth. Most researchers agree on the importance of the role of

the financial sector in real economic growth, both at the national and international levels

(Demirgüç-Kunt et al., 2004; Love, 2003). The financial sector plays a promotional role if it is

able to channel financial resources toward the industries with good growth opportunities.

When the financial sector is more developed, more financial resources can be allocated into

productive real investment and more physical capital gets formed, which will stimulate

economic growth.

In the past two decades, the Islamic financial industry has emerged through the world.

Global Islamic banking assets have been growing rapidly. According to the World Islamic

Banking Competitiveness Report 2014-2015, they attained a compounded annual growth

rate of around 17 per cent from 2009 to 2013. International Islamic banking assets with

commercial banks were set to exceed US$778bn in 2014. In particular, six markets – Qatar,

Indonesia, Saudi Arabia, Malaysia, the United Arab Emirates (UAE) and Turkey – are

heading toward touching US$1.8tn by 2019. The performance and relative stability of

Islamic financial institutions during the financial crisis that hit the world in 2008 increased

the demand for Shari’ah-compliant products, not only from financiers in the Middle East and

other Muslim countries, but also by investors around the world seeking Islamic investment

as a means of diversification.

How important is Islamic financial development for economic development? Several

theoretical studies have been undertaken in the different fields of Islamic banking. Most of

them indicate the superiority of the Islamic financial industry compared to the conventional

one in terms of stability and efficiency (Hasan and Dridi, 2010; Hanif et al., 2012; Mansor et al.,

2015). However, only few studies have searched for empirical evidence connecting Islamic

finance and economic growth.

Against this background, this study attempts to respond to the question:

Q1. Do financial development and Islamic finance stimulate the real economic activity of

the UAE?

In line with earlier studies, the present study closely examines the causality between

financial development and economic activity, but with some differences. First, previous

studies generally considered a sample of countries, including the UAE. These studies

provided a higher degree of generalization and not an internal validity specific to each

country, thereby increasing the need for country-specific studies. To the best of our

knowledge, studies in this area on the UAE are very few (Al-Malkawi et al., 2012; Tabash and

Dhankar, 2014).

Meanwhile, the UAE’s gross domestic product (GDP) in 2013 was US$396.24bn, making

it the world’s 27th largest economy. The contribution of the oil sector to the UAE’s GDP is

decreasing because the government is attempting to diversify its economy. The UAE has

embarked on an overall economic reform package that included policy and structural

reforms in the financial sector. The role of Islamic finance, as a segment of the global

financial system, has also been a key focus in development policy discussions. Therefore,

3

Islamic finance

and economic

growthDownloaded by RMIT University Library At 05:01 02 January 2018 (PT)

focusing on the UAE economy in this study is significant. Second, previous studies generally

considered financial development or Islamic financing. In contrast, the present study

considers the role of financial development in general and Islamic finance in particular.

Third, while most of the empirical research has focused on single indicators of financial

development, this study mainly focuses on a composite index used to evaluate the financial

strength of the UAE. Fourth, economic forecasting has always been a central concern among

researchers and policy-makers. It helps to establish plans and formulate objectives. During

the past decade, the vector autoregressive model (VAR) has become the standard tool for

predicting economic activity. This study projects historical values of variables into the

future by using a VAR.

The rest of the paper is structured as follows: Section 2 presents the theoretical framework

whereby the relationship between financial development, Islamic finance and economic

growth is outlined. Section 3 describes the details of the data and the empirical approach used

in this study. Section 4 reports and analyzes the results. Section 5 contains the conclusion.

2. Theoretical and empirical framework

A brief overview is provided in this section to highlight the fact that Islamic financial system,

similar to the conventional one, performs broad functions that may influence saving and

investment decisions and hence could have implications for real economic growth. These

include the provision of external financing as described by Schumpeter (1912) – financial

institutions provide funding to entrepreneurs with good growth prospects. Any industry

with high growth opportunities will require a relatively large amount of outside financing.

Thus, the banking sector is considered an engine of economic growth.

Gurley and Shaw (1955), Goldsmith (1969) and Hicks (1969) have argued that more

developed financial markets promote economic growth by mobilizing savings and

facilitating investment. Mobilization may involve multiple bilateral contracts between

productive units raising capital and agents with surplus resources. To economize on the

costs associated with multiple bilateral contracts, pooling may occur through intermediaries,

where thousands of investors entrust their wealth to intermediaries that invest in hundreds

of firms (Sirri and Tufano, 1995). This takes place when mobilizers convince savers of the

soundness of the investments.

King and Levine (1993) emphasized the role of financial institutions in overcoming

informational problems. Indeed, there are large costs associated with evaluating firms,

managers and market conditions before making investment decisions. Individual savers

may not have the ability to collect and produce information on possible investments. Savers

will be averse to invest in industries having little reliable information. High information costs

may keep capital from flowing to its highest value use. Financial institutions producing

better information on firms will thereby find more promising investments, and induce a more

efficient allocation of capital and foster growth (Greenwood and Jovanovic, 1990).

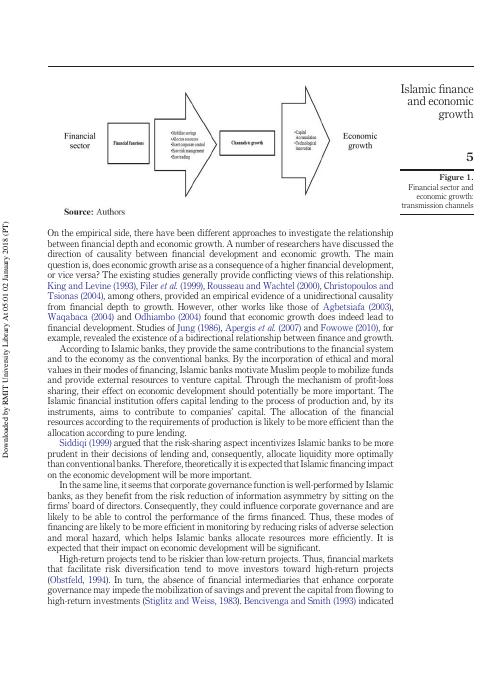

In this line of thinking, Levine (1997) stressed that market frictions like information and

transaction costs motivate the emergence of a well-developed financial sector which can be

seen as well-offered financial services. Therefore, an increased financial service may affect

economic growth through two main channels: capital accumulation and technological

innovation (Figure 1).

In addition, as suggested by Rajan and Zingales (1998), certain industries have a lag

between investment opportunities and cash flow. Industries with this inherent need for

external finance will respond to growth opportunities in countries with well-developed

financial institutions.

JIABR

8,1

4Downloaded by RMIT University Library At 05:01 02 January 2018 (PT)

considered financial development or Islamic financing. In contrast, the present study

considers the role of financial development in general and Islamic finance in particular.

Third, while most of the empirical research has focused on single indicators of financial

development, this study mainly focuses on a composite index used to evaluate the financial

strength of the UAE. Fourth, economic forecasting has always been a central concern among

researchers and policy-makers. It helps to establish plans and formulate objectives. During

the past decade, the vector autoregressive model (VAR) has become the standard tool for

predicting economic activity. This study projects historical values of variables into the

future by using a VAR.

The rest of the paper is structured as follows: Section 2 presents the theoretical framework

whereby the relationship between financial development, Islamic finance and economic

growth is outlined. Section 3 describes the details of the data and the empirical approach used

in this study. Section 4 reports and analyzes the results. Section 5 contains the conclusion.

2. Theoretical and empirical framework

A brief overview is provided in this section to highlight the fact that Islamic financial system,

similar to the conventional one, performs broad functions that may influence saving and

investment decisions and hence could have implications for real economic growth. These

include the provision of external financing as described by Schumpeter (1912) – financial

institutions provide funding to entrepreneurs with good growth prospects. Any industry

with high growth opportunities will require a relatively large amount of outside financing.

Thus, the banking sector is considered an engine of economic growth.

Gurley and Shaw (1955), Goldsmith (1969) and Hicks (1969) have argued that more

developed financial markets promote economic growth by mobilizing savings and

facilitating investment. Mobilization may involve multiple bilateral contracts between

productive units raising capital and agents with surplus resources. To economize on the

costs associated with multiple bilateral contracts, pooling may occur through intermediaries,

where thousands of investors entrust their wealth to intermediaries that invest in hundreds

of firms (Sirri and Tufano, 1995). This takes place when mobilizers convince savers of the

soundness of the investments.

King and Levine (1993) emphasized the role of financial institutions in overcoming

informational problems. Indeed, there are large costs associated with evaluating firms,

managers and market conditions before making investment decisions. Individual savers

may not have the ability to collect and produce information on possible investments. Savers

will be averse to invest in industries having little reliable information. High information costs

may keep capital from flowing to its highest value use. Financial institutions producing

better information on firms will thereby find more promising investments, and induce a more

efficient allocation of capital and foster growth (Greenwood and Jovanovic, 1990).

In this line of thinking, Levine (1997) stressed that market frictions like information and

transaction costs motivate the emergence of a well-developed financial sector which can be

seen as well-offered financial services. Therefore, an increased financial service may affect

economic growth through two main channels: capital accumulation and technological

innovation (Figure 1).

In addition, as suggested by Rajan and Zingales (1998), certain industries have a lag

between investment opportunities and cash flow. Industries with this inherent need for

external finance will respond to growth opportunities in countries with well-developed

financial institutions.

JIABR

8,1

4Downloaded by RMIT University Library At 05:01 02 January 2018 (PT)

On the empirical side, there have been different approaches to investigate the relationship

between financial depth and economic growth. A number of researchers have discussed the

direction of causality between financial development and economic growth. The main

question is, does economic growth arise as a consequence of a higher financial development,

or vice versa? The existing studies generally provide conflicting views of this relationship.

King and Levine (1993), Filer et al. (1999), Rousseau and Wachtel (2000), Christopoulos and

Tsionas (2004), among others, provided an empirical evidence of a unidirectional causality

from financial depth to growth. However, other works like those of Agbetsiafa (2003),

Waqabaca (2004) and Odhiambo (2004) found that economic growth does indeed lead to

financial development. Studies of Jung (1986), Apergis et al. (2007) and Fowowe (2010), for

example, revealed the existence of a bidirectional relationship between finance and growth.

According to Islamic banks, they provide the same contributions to the financial system

and to the economy as the conventional banks. By the incorporation of ethical and moral

values in their modes of financing, Islamic banks motivate Muslim people to mobilize funds

and provide external resources to venture capital. Through the mechanism of profit-loss

sharing, their effect on economic development should potentially be more important. The

Islamic financial institution offers capital lending to the process of production and, by its

instruments, aims to contribute to companies’ capital. The allocation of the financial

resources according to the requirements of production is likely to be more efficient than the

allocation according to pure lending.

Siddiqi (1999) argued that the risk-sharing aspect incentivizes Islamic banks to be more

prudent in their decisions of lending and, consequently, allocate liquidity more optimally

than conventional banks. Therefore, theoretically it is expected that Islamic financing impact

on the economic development will be more important.

In the same line, it seems that corporate governance function is well-performed by Islamic

banks, as they benefit from the risk reduction of information asymmetry by sitting on the

firms’ board of directors. Consequently, they could influence corporate governance and are

likely to be able to control the performance of the firms financed. Thus, these modes of

financing are likely to be more efficient in monitoring by reducing risks of adverse selection

and moral hazard, which helps Islamic banks allocate resources more efficiently. It is

expected that their impact on economic development will be significant.

High-return projects tend to be riskier than low-return projects. Thus, financial markets

that facilitate risk diversification tend to move investors toward high-return projects

(Obstfeld, 1994). In turn, the absence of financial intermediaries that enhance corporate

governance may impede the mobilization of savings and prevent the capital from flowing to

high-return investments (Stiglitz and Weiss, 1983). Bencivenga and Smith (1993) indicated

Figure 1.

Financial sector and

economic growth:

transmission channels

5

Islamic finance

and economic

growthDownloaded by RMIT University Library At 05:01 02 January 2018 (PT)

between financial depth and economic growth. A number of researchers have discussed the

direction of causality between financial development and economic growth. The main

question is, does economic growth arise as a consequence of a higher financial development,

or vice versa? The existing studies generally provide conflicting views of this relationship.

King and Levine (1993), Filer et al. (1999), Rousseau and Wachtel (2000), Christopoulos and

Tsionas (2004), among others, provided an empirical evidence of a unidirectional causality

from financial depth to growth. However, other works like those of Agbetsiafa (2003),

Waqabaca (2004) and Odhiambo (2004) found that economic growth does indeed lead to

financial development. Studies of Jung (1986), Apergis et al. (2007) and Fowowe (2010), for

example, revealed the existence of a bidirectional relationship between finance and growth.

According to Islamic banks, they provide the same contributions to the financial system

and to the economy as the conventional banks. By the incorporation of ethical and moral

values in their modes of financing, Islamic banks motivate Muslim people to mobilize funds

and provide external resources to venture capital. Through the mechanism of profit-loss

sharing, their effect on economic development should potentially be more important. The

Islamic financial institution offers capital lending to the process of production and, by its

instruments, aims to contribute to companies’ capital. The allocation of the financial

resources according to the requirements of production is likely to be more efficient than the

allocation according to pure lending.

Siddiqi (1999) argued that the risk-sharing aspect incentivizes Islamic banks to be more

prudent in their decisions of lending and, consequently, allocate liquidity more optimally

than conventional banks. Therefore, theoretically it is expected that Islamic financing impact

on the economic development will be more important.

In the same line, it seems that corporate governance function is well-performed by Islamic

banks, as they benefit from the risk reduction of information asymmetry by sitting on the

firms’ board of directors. Consequently, they could influence corporate governance and are

likely to be able to control the performance of the firms financed. Thus, these modes of

financing are likely to be more efficient in monitoring by reducing risks of adverse selection

and moral hazard, which helps Islamic banks allocate resources more efficiently. It is

expected that their impact on economic development will be significant.

High-return projects tend to be riskier than low-return projects. Thus, financial markets

that facilitate risk diversification tend to move investors toward high-return projects

(Obstfeld, 1994). In turn, the absence of financial intermediaries that enhance corporate

governance may impede the mobilization of savings and prevent the capital from flowing to

high-return investments (Stiglitz and Weiss, 1983). Bencivenga and Smith (1993) indicated

Figure 1.

Financial sector and

economic growth:

transmission channels

5

Islamic finance

and economic

growthDownloaded by RMIT University Library At 05:01 02 January 2018 (PT)

{kind=link}

End of preview

Want to access all the pages? Upload your documents or become a member.

Related Documents

Consumer Attitudes Toward Online Video Advertisementlg...

|16

|8133

|156

A Decision Making Model for Selecting Start-up Businesses in a Government Venture Capital Schemelg...

|23

|13976

|84