Financial Econometric Analysis: CAPM and Regression

Added on 2023-01-12

8 Pages1392 Words22 Views

Financial econometric

Contents

INTRODUCTION...........................................................................................................................1

MAIN BODY..................................................................................................................................1

CAPM..........................................................................................................................................1

Regression analysis......................................................................................................................2

CONCLUSION................................................................................................................................5

REFERENCES................................................................................................................................6

INTRODUCTION...........................................................................................................................1

MAIN BODY..................................................................................................................................1

CAPM..........................................................................................................................................1

Regression analysis......................................................................................................................2

CONCLUSION................................................................................................................................5

REFERENCES................................................................................................................................6

INTRODUCTION

Financial econometrics is the branch of economics in which is concerned with mathematical

methods (Chang, McAleer and Wang, 2018). In context of this concept, the panel data is a

combination of multi dimensional data which is recorded over a time. The main aim of this

report is to construct a data and then analyse it using appropriate regression analysis. For this

purpose, a panel data is created which has stock prices for 8 large scale companies. This data is

recorded over the period of two years. Furthermore, this data is used to run regression test using

SPSS so that theory of CAPM can be verified and regression results can be analysed.

MAIN BODY

CAPM

The panel data which has been used has stock prices of 8 countries which are Amazon,

AutoZone Inc., Hilton Worldwide Holdings Inc. (HLT), MGM Resorts International (MGM),

AT&T Inc. (T), Twitter, Inc. (TWTR), Verizon Communications Inc. (VZ) and The Interpublic

Group of Companies, Inc. Among all these companies, Amazon is considered as a dependent

variable in order to analyse the relationship between the prices of stocks of each company with

Amazon.

The theory of CAPM determines the relationship between systematic risk and expected

return (Ghosh, Jana and Sanyal, 2019). In this case, the stocks of Amazon can be considered as

systematic risk using which expected stock prices of all other companies can be gained. The

formula of CAPM is:

ERi=Rf+βi(ERm−Rf)

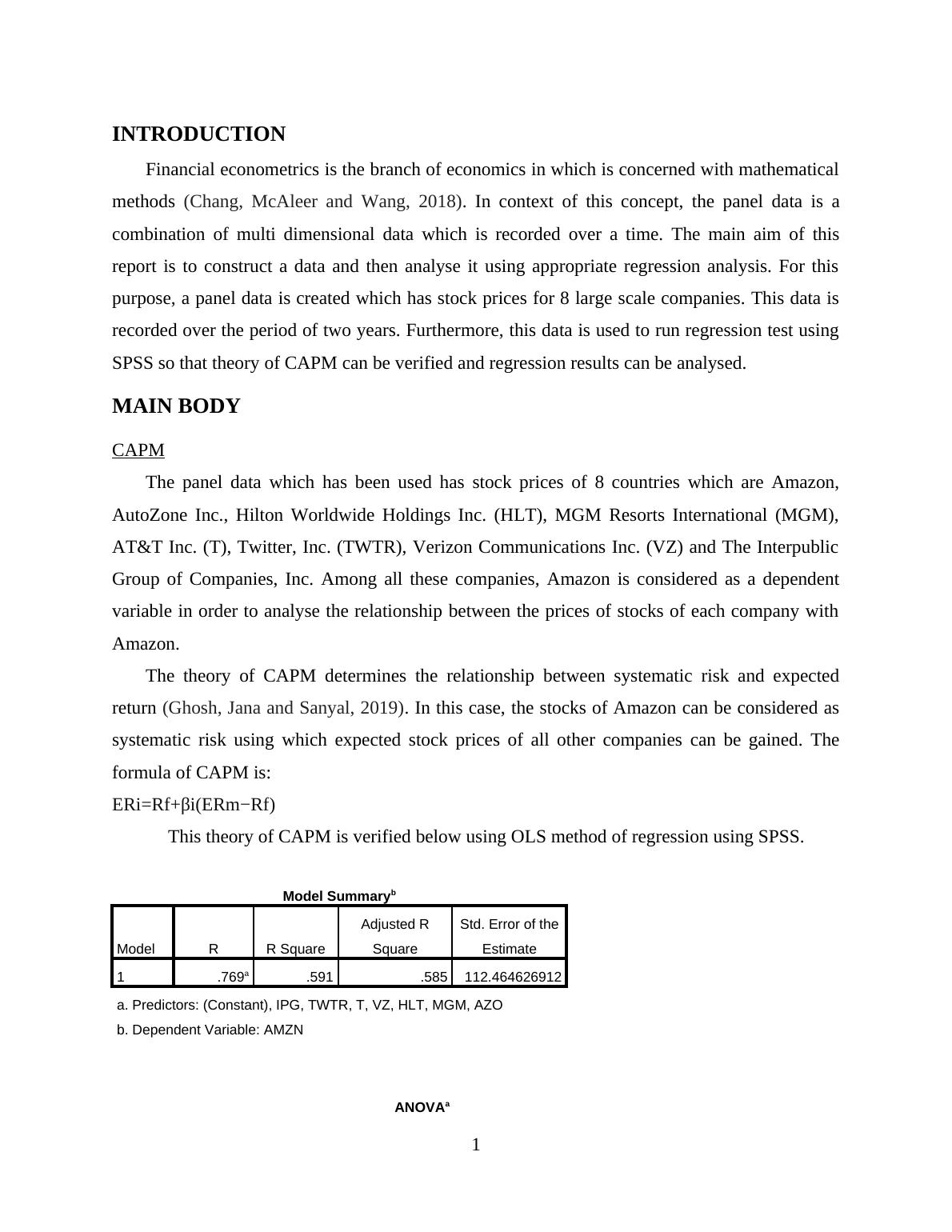

This theory of CAPM is verified below using OLS method of regression using SPSS.

Model Summaryb

Model R R Square

Adjusted R

Square

Std. Error of the

Estimate

1 .769a .591 .585 112.464626912

a. Predictors: (Constant), IPG, TWTR, T, VZ, HLT, MGM, AZO

b. Dependent Variable: AMZN

ANOVAa

1

Financial econometrics is the branch of economics in which is concerned with mathematical

methods (Chang, McAleer and Wang, 2018). In context of this concept, the panel data is a

combination of multi dimensional data which is recorded over a time. The main aim of this

report is to construct a data and then analyse it using appropriate regression analysis. For this

purpose, a panel data is created which has stock prices for 8 large scale companies. This data is

recorded over the period of two years. Furthermore, this data is used to run regression test using

SPSS so that theory of CAPM can be verified and regression results can be analysed.

MAIN BODY

CAPM

The panel data which has been used has stock prices of 8 countries which are Amazon,

AutoZone Inc., Hilton Worldwide Holdings Inc. (HLT), MGM Resorts International (MGM),

AT&T Inc. (T), Twitter, Inc. (TWTR), Verizon Communications Inc. (VZ) and The Interpublic

Group of Companies, Inc. Among all these companies, Amazon is considered as a dependent

variable in order to analyse the relationship between the prices of stocks of each company with

Amazon.

The theory of CAPM determines the relationship between systematic risk and expected

return (Ghosh, Jana and Sanyal, 2019). In this case, the stocks of Amazon can be considered as

systematic risk using which expected stock prices of all other companies can be gained. The

formula of CAPM is:

ERi=Rf+βi(ERm−Rf)

This theory of CAPM is verified below using OLS method of regression using SPSS.

Model Summaryb

Model R R Square

Adjusted R

Square

Std. Error of the

Estimate

1 .769a .591 .585 112.464626912

a. Predictors: (Constant), IPG, TWTR, T, VZ, HLT, MGM, AZO

b. Dependent Variable: AMZN

ANOVAa

1

End of preview

Want to access all the pages? Upload your documents or become a member.

Related Documents

Testing the CAPM Theory Using Time Series Regression Analysislg...

|18

|3072

|254

Data Analysis Project for Deskliblg...

|9

|2087

|218