Analysis of Working Capital Management

VerifiedAdded on 2020/10/22

|18

|5600

|218

AI Summary

The provided document is a solution to an assignment that analyzes the impact of working capital management on the operational functioning of industries. It discusses how effective working capital management can lead to improved performance and profitability. The assignment also reviews literature on working capital management, highlighting its significance in emerging economies. A meta title and description are generated for SEO purposes, along with a summary that provides an overview of the assignment's content.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

FINANCIAL ECONOMETRICS

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

1. Overview.................................................................................................................................1

2. Literature review.....................................................................................................................1

3. Outlining specification of the equation /model and stating hypotheses..................................4

4. Explaining variables, data, and data sources...........................................................................4

5. Producing estimated specification in standard format............................................................5

6. Analysing results of regression...............................................................................................8

7. RECOMMENDATIONS...........................................................................................................12

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

INTRODUCTION...........................................................................................................................1

1. Overview.................................................................................................................................1

2. Literature review.....................................................................................................................1

3. Outlining specification of the equation /model and stating hypotheses..................................4

4. Explaining variables, data, and data sources...........................................................................4

5. Producing estimated specification in standard format............................................................5

6. Analysing results of regression...............................................................................................8

7. RECOMMENDATIONS...........................................................................................................12

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

INTRODUCTION

Financial econometrics is very important concept for analysing dataset. The term implies

applying of statistical techniques to financial market data. It is quite useful as it provides vital

study with respect to capital markets, corporate finance, corporate governance, etc. Present report

deals with analysing relationship among the variables under study. The regression analysis is

presented and firm's performance is taken as dependent variable and working capital

management is taken as independent variable. In relation to this, 20 organizations which are

listed on FTSE 100 index is taken over the period of last 10 years’ performance. E views 10 is

used for running regression results and hypotheses is presented along with specification of model

is produced. ROA as dependent variable is taken. While, independent variables are inventory

turnover, payable period and receivable turnover are being for appropriate results. Regression

results are produced and recommendation will be made for future research.

1. Overview

Working capital management and profitability of firm both are interdependent factors

which are important for organisations. In present report, ROA of 20 companies that is Burberry,

Tesco, Sainsbury, Next, Morrisons, OCADO Group, Paddy Power Betfair, Easy Jet, British

American Tobacco, Coca-cola, Diageo, Imperial Brands, Just Eat, Kingfisher, Marks and

Spencers, Unilever, Whitebread, Carnival Corp & PLC, Intercontinentals Hotels Group, TUI

Group is taken as dependent variable and independent variables are inventory turnover, accounts

receivable and payable period having impact on overall profitability of firms.

2. Literature review

As per the views of Abor (2017), account receivables directly impact profitability as it is

dependent on convention of accounting which is applicable and affects recording of transaction

as activity of sale. In Statement of balance sheet it is stated as asset, if turnover is slow with

reference to receivables which can impact organization's bottom line. In the same series, if

money is owned to specific organization before sales, it could directly give effect on various

business parts. There are various things outlined if credit is extended. If revenue consists of

paying accounts receivable in slow format, then it will reflect cash flow along with capability of

organization for paying its vendors to meet its specific obligations along with credit financiers. It

provides outcome with context of business had incurred huge charges with reference to interest.

While, tax consideration might be due to revenue prior to account receivable collection.

1

Financial econometrics is very important concept for analysing dataset. The term implies

applying of statistical techniques to financial market data. It is quite useful as it provides vital

study with respect to capital markets, corporate finance, corporate governance, etc. Present report

deals with analysing relationship among the variables under study. The regression analysis is

presented and firm's performance is taken as dependent variable and working capital

management is taken as independent variable. In relation to this, 20 organizations which are

listed on FTSE 100 index is taken over the period of last 10 years’ performance. E views 10 is

used for running regression results and hypotheses is presented along with specification of model

is produced. ROA as dependent variable is taken. While, independent variables are inventory

turnover, payable period and receivable turnover are being for appropriate results. Regression

results are produced and recommendation will be made for future research.

1. Overview

Working capital management and profitability of firm both are interdependent factors

which are important for organisations. In present report, ROA of 20 companies that is Burberry,

Tesco, Sainsbury, Next, Morrisons, OCADO Group, Paddy Power Betfair, Easy Jet, British

American Tobacco, Coca-cola, Diageo, Imperial Brands, Just Eat, Kingfisher, Marks and

Spencers, Unilever, Whitebread, Carnival Corp & PLC, Intercontinentals Hotels Group, TUI

Group is taken as dependent variable and independent variables are inventory turnover, accounts

receivable and payable period having impact on overall profitability of firms.

2. Literature review

As per the views of Abor (2017), account receivables directly impact profitability as it is

dependent on convention of accounting which is applicable and affects recording of transaction

as activity of sale. In Statement of balance sheet it is stated as asset, if turnover is slow with

reference to receivables which can impact organization's bottom line. In the same series, if

money is owned to specific organization before sales, it could directly give effect on various

business parts. There are various things outlined if credit is extended. If revenue consists of

paying accounts receivable in slow format, then it will reflect cash flow along with capability of

organization for paying its vendors to meet its specific obligations along with credit financiers. It

provides outcome with context of business had incurred huge charges with reference to interest.

While, tax consideration might be due to revenue prior to account receivable collection.

1

In the same series, if cash flow is tight then organization might consider fewer inventory

in hand and it would hire staff for paying its vendors or for accomplishing product demands. It

would directly reflect time of delivery and its growth will be put on limit. Simultaneously, the

time spent with context of task of book keeping is monitored consistently as it balances bank

account for meeting obligations and to gain productivity of business. As per cash flows,

especially outflows should be made in accordance to production level of organization if engaged

in non-manufacturing sector. By properly initiating control over outflows, cash position can be

enhanced in a better way.

According to Afrifa and Padachi (2016), accounts payable might give positive impact on

profitability of organization, if best practices had been set with context of appropriate

management. Initially, if organization pay its bills on proper time it is considered as very simple

practice. If it is performed essentially then it would create trust among suppliers and then they

would try to offer different discounts which indirectly impacts profitability. In the same series, it

would be facilitating different account payable process with minimum staff and less paperwork.

It minimises various accounts and payable clerks. It directly soothes its management of accounts

payable and raises profitability by reducing personnel. In contrast to this, Bhatia and Srivastava

(2016) says that firm should emphasize on making quick payments so as to avail discounts from

suppliers. This is essentially required because cash remains blocked in production and if good

discount rate is not provided on faster payments, then it results into unnecessary cash outflows

without being beneficial to the company.

According to Afrifa (2016), inventory is considered as one of the major factor which

helps in raising profitability. The method in which inventory had been managed gives effect on

various level of profit with context of income statement. Especially, inventory turnover is

number of times stock had been utilised in specific duration as it provides directs link to

profitability. The stocks which are stated as obsolete are kept and had given low turnover which

reduce it sales as well. The inventory level had directly considered level of demand for ignoring

under or overstocking. If management of stock is in appropriate format, then it would maximise

its efficiency and profitability via its operations. However, Christopher (2016) says that

inventory is not replicated in quick manner, and therefore increment in holding costs gets

prevailed which is harmful for organization. Major part of cash is usually blocked in inventory

2

in hand and it would hire staff for paying its vendors or for accomplishing product demands. It

would directly reflect time of delivery and its growth will be put on limit. Simultaneously, the

time spent with context of task of book keeping is monitored consistently as it balances bank

account for meeting obligations and to gain productivity of business. As per cash flows,

especially outflows should be made in accordance to production level of organization if engaged

in non-manufacturing sector. By properly initiating control over outflows, cash position can be

enhanced in a better way.

According to Afrifa and Padachi (2016), accounts payable might give positive impact on

profitability of organization, if best practices had been set with context of appropriate

management. Initially, if organization pay its bills on proper time it is considered as very simple

practice. If it is performed essentially then it would create trust among suppliers and then they

would try to offer different discounts which indirectly impacts profitability. In the same series, it

would be facilitating different account payable process with minimum staff and less paperwork.

It minimises various accounts and payable clerks. It directly soothes its management of accounts

payable and raises profitability by reducing personnel. In contrast to this, Bhatia and Srivastava

(2016) says that firm should emphasize on making quick payments so as to avail discounts from

suppliers. This is essentially required because cash remains blocked in production and if good

discount rate is not provided on faster payments, then it results into unnecessary cash outflows

without being beneficial to the company.

According to Afrifa (2016), inventory is considered as one of the major factor which

helps in raising profitability. The method in which inventory had been managed gives effect on

various level of profit with context of income statement. Especially, inventory turnover is

number of times stock had been utilised in specific duration as it provides directs link to

profitability. The stocks which are stated as obsolete are kept and had given low turnover which

reduce it sales as well. The inventory level had directly considered level of demand for ignoring

under or overstocking. If management of stock is in appropriate format, then it would maximise

its efficiency and profitability via its operations. However, Christopher (2016) says that

inventory is not replicated in quick manner, and therefore increment in holding costs gets

prevailed which is harmful for organization. Major part of cash is usually blocked in inventory

2

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

and it is required that quick replenishment of the same should be done in order to accelerate

production.

As per the views of Charitou, Elfani and Lois (2016), Cash conversion cycle is replicated

as very important measure for effective working capital management of organization where most

important concern is of managing cash. Cash conversion cycle impacts association in positive

aspect along with return on equity and assets as it indicates that, it is not mandatory that cash

conversion cycle should be less. In the same series if organization is capable for selling inventory

and to collect its accounts receivable prior to repaying its payables as in this specific situation it

would be different. In contrast to this, Baker and Chapin (2018) says that cash conversion cycle

should be quick enough to derive efficiency of firm in converting stock purchases into cash

flows or not. In the same manner, positive cash conversion cycle is beneficial for company as it

provides clarity in receiving outstanding amount from credit customers in case of receivables. If

company is not able to collect due money, then, cash flows tend to be interrupted. Working

capital management is utmost vital in the company so that operational needs may be carried out

in a better way. This is essentially required that current liabilities may be effectively paid off

with those current assets in the best possible manner. Without the better working capital, firm

may lend into difficulty while meeting obligations within stipulated time. Current assets should

be in excess of current liabilities so that firm could meet with ease.

Cooke and et.al (2018) says pecking order theory is one of the important capital structure

theory which helps to choose sources of finance with respect to certain hierarchy. First

preference is given to internal financing in hierarchical way. If internal finance does not meet

requirements, then external funds are being attracted by management. Debt is issued for

generating funds, then when it is impossible to issue more debt, equity is the last resort or option

for attaining financing. This helps to effectively decrease WACC (Weighted Average Cost of

Capital) and changes in relation to capital structure. Control over firm is effectively maintained.

However, Sarma and Barua (2018) says that it does not take into consideration financial distress,

agency expenses, investment opportunity being available to actual capital structure. It also does

not take influences that is usually made because of application of various taxes.

As per the views of Singla, Sethi and Ahuja (2018), trade-off theory is used in capital

structure when organization chooses how much equity to be financed and of debt so that costs

3

production.

As per the views of Charitou, Elfani and Lois (2016), Cash conversion cycle is replicated

as very important measure for effective working capital management of organization where most

important concern is of managing cash. Cash conversion cycle impacts association in positive

aspect along with return on equity and assets as it indicates that, it is not mandatory that cash

conversion cycle should be less. In the same series if organization is capable for selling inventory

and to collect its accounts receivable prior to repaying its payables as in this specific situation it

would be different. In contrast to this, Baker and Chapin (2018) says that cash conversion cycle

should be quick enough to derive efficiency of firm in converting stock purchases into cash

flows or not. In the same manner, positive cash conversion cycle is beneficial for company as it

provides clarity in receiving outstanding amount from credit customers in case of receivables. If

company is not able to collect due money, then, cash flows tend to be interrupted. Working

capital management is utmost vital in the company so that operational needs may be carried out

in a better way. This is essentially required that current liabilities may be effectively paid off

with those current assets in the best possible manner. Without the better working capital, firm

may lend into difficulty while meeting obligations within stipulated time. Current assets should

be in excess of current liabilities so that firm could meet with ease.

Cooke and et.al (2018) says pecking order theory is one of the important capital structure

theory which helps to choose sources of finance with respect to certain hierarchy. First

preference is given to internal financing in hierarchical way. If internal finance does not meet

requirements, then external funds are being attracted by management. Debt is issued for

generating funds, then when it is impossible to issue more debt, equity is the last resort or option

for attaining financing. This helps to effectively decrease WACC (Weighted Average Cost of

Capital) and changes in relation to capital structure. Control over firm is effectively maintained.

However, Sarma and Barua (2018) says that it does not take into consideration financial distress,

agency expenses, investment opportunity being available to actual capital structure. It also does

not take influences that is usually made because of application of various taxes.

As per the views of Singla, Sethi and Ahuja (2018), trade-off theory is used in capital

structure when organization chooses how much equity to be financed and of debt so that costs

3

and benefits arriving out may be balanced. It is quite useful for company as it helps to make

balance between debt and equity. Financing with debt is useful because tax benefits are achieved.

Equity is good up to certain extent when company is performing well in the market and value of

shares are maximised. On the contrary, Oliveira and Handfield (2018) says that trade-off theory

is used to have optimal balance in capital structure. However, after certain time, cost of capital

can be minimised by maximising total debt but after that, cost of capital again increases leading

to riskiness for the firm. It is required that minimisation should be done so that company may be

able to attain trade-off between marginal costs and benefits in the best possible manner.

Moreover, firm is able to have better understanding about the performance in terms of optimum

capital structure (Clark. 2015).

3. Outlining specification of the equation /model and stating hypotheses

Hypotheses

H0: There is no significant difference between organization's performance and working capital

management

H1: There is significant difference between organization's performance and working capital

management

The specification of the estimate regression equation is as follows-

Y = β0 + β1 x1 + β2 x2

Method- In present regression equation, LS - Least Squares method is being taken for obtaining

result.

Sample- Last 10-year performance of 20 companies listed on FTSE 100 indexes are taken as a

sample for producing result in E views 10.

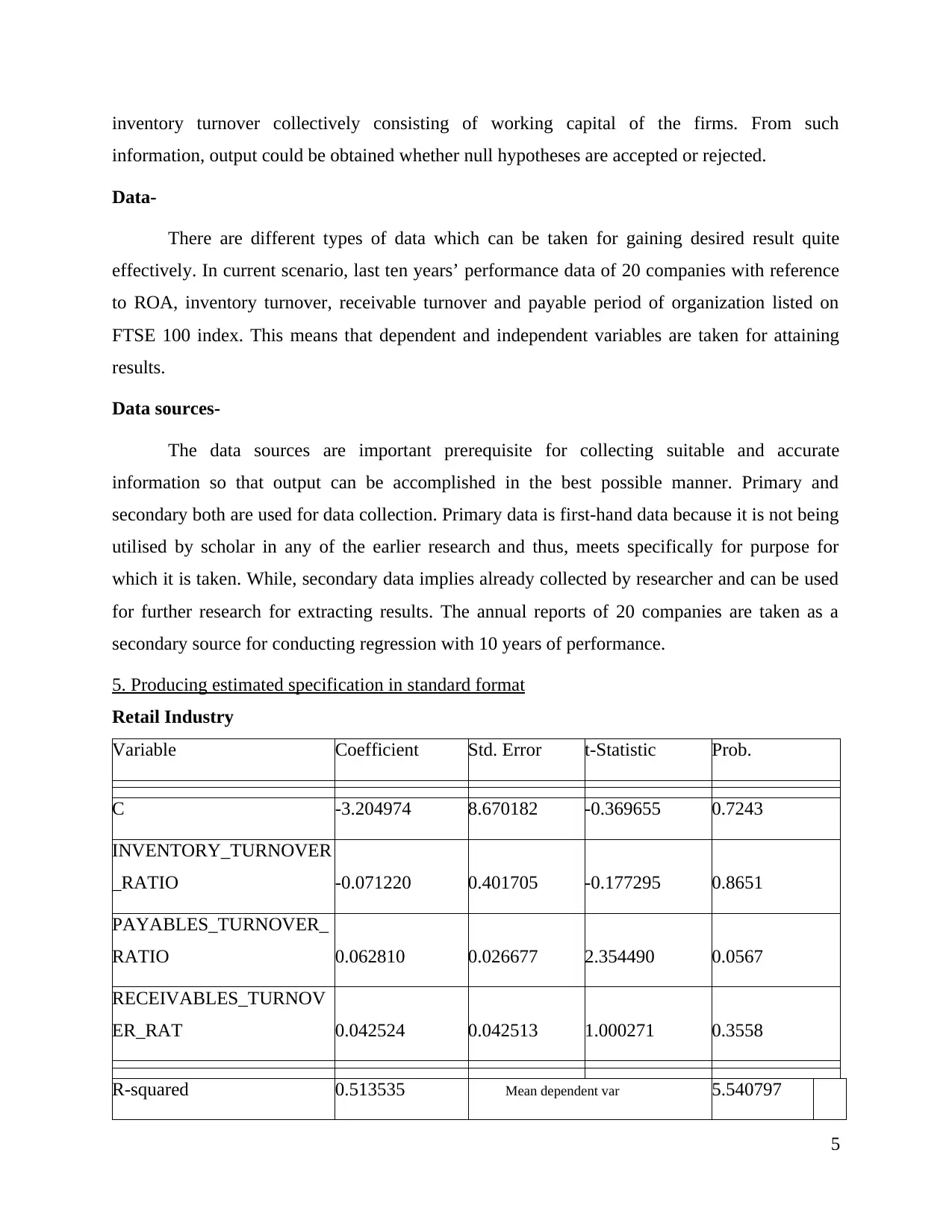

4. Explaining variables, data, and data sources

Variables-

There are various variables being taken in the regression model so as to effectively

produce result whether there is significant difference between organization's performance and

working capital management or not. Dependent and independent variables are taken to arrive at

conclusion. Dependent variable is ROA (Return On Assets) of 20 companies over a period of ten

years. On the other hand, independent variables are receivable turnover, payable period,

4

balance between debt and equity. Financing with debt is useful because tax benefits are achieved.

Equity is good up to certain extent when company is performing well in the market and value of

shares are maximised. On the contrary, Oliveira and Handfield (2018) says that trade-off theory

is used to have optimal balance in capital structure. However, after certain time, cost of capital

can be minimised by maximising total debt but after that, cost of capital again increases leading

to riskiness for the firm. It is required that minimisation should be done so that company may be

able to attain trade-off between marginal costs and benefits in the best possible manner.

Moreover, firm is able to have better understanding about the performance in terms of optimum

capital structure (Clark. 2015).

3. Outlining specification of the equation /model and stating hypotheses

Hypotheses

H0: There is no significant difference between organization's performance and working capital

management

H1: There is significant difference between organization's performance and working capital

management

The specification of the estimate regression equation is as follows-

Y = β0 + β1 x1 + β2 x2

Method- In present regression equation, LS - Least Squares method is being taken for obtaining

result.

Sample- Last 10-year performance of 20 companies listed on FTSE 100 indexes are taken as a

sample for producing result in E views 10.

4. Explaining variables, data, and data sources

Variables-

There are various variables being taken in the regression model so as to effectively

produce result whether there is significant difference between organization's performance and

working capital management or not. Dependent and independent variables are taken to arrive at

conclusion. Dependent variable is ROA (Return On Assets) of 20 companies over a period of ten

years. On the other hand, independent variables are receivable turnover, payable period,

4

inventory turnover collectively consisting of working capital of the firms. From such

information, output could be obtained whether null hypotheses are accepted or rejected.

Data-

There are different types of data which can be taken for gaining desired result quite

effectively. In current scenario, last ten years’ performance data of 20 companies with reference

to ROA, inventory turnover, receivable turnover and payable period of organization listed on

FTSE 100 index. This means that dependent and independent variables are taken for attaining

results.

Data sources-

The data sources are important prerequisite for collecting suitable and accurate

information so that output can be accomplished in the best possible manner. Primary and

secondary both are used for data collection. Primary data is first-hand data because it is not being

utilised by scholar in any of the earlier research and thus, meets specifically for purpose for

which it is taken. While, secondary data implies already collected by researcher and can be used

for further research for extracting results. The annual reports of 20 companies are taken as a

secondary source for conducting regression with 10 years of performance.

5. Producing estimated specification in standard format

Retail Industry

Variable Coefficient Std. Error t-Statistic Prob.

C -3.204974 8.670182 -0.369655 0.7243

INVENTORY_TURNOVER

_RATIO -0.071220 0.401705 -0.177295 0.8651

PAYABLES_TURNOVER_

RATIO 0.062810 0.026677 2.354490 0.0567

RECEIVABLES_TURNOV

ER_RAT 0.042524 0.042513 1.000271 0.3558

R-squared 0.513535 Mean dependent var 5.540797

5

information, output could be obtained whether null hypotheses are accepted or rejected.

Data-

There are different types of data which can be taken for gaining desired result quite

effectively. In current scenario, last ten years’ performance data of 20 companies with reference

to ROA, inventory turnover, receivable turnover and payable period of organization listed on

FTSE 100 index. This means that dependent and independent variables are taken for attaining

results.

Data sources-

The data sources are important prerequisite for collecting suitable and accurate

information so that output can be accomplished in the best possible manner. Primary and

secondary both are used for data collection. Primary data is first-hand data because it is not being

utilised by scholar in any of the earlier research and thus, meets specifically for purpose for

which it is taken. While, secondary data implies already collected by researcher and can be used

for further research for extracting results. The annual reports of 20 companies are taken as a

secondary source for conducting regression with 10 years of performance.

5. Producing estimated specification in standard format

Retail Industry

Variable Coefficient Std. Error t-Statistic Prob.

C -3.204974 8.670182 -0.369655 0.7243

INVENTORY_TURNOVER

_RATIO -0.071220 0.401705 -0.177295 0.8651

PAYABLES_TURNOVER_

RATIO 0.062810 0.026677 2.354490 0.0567

RECEIVABLES_TURNOV

ER_RAT 0.042524 0.042513 1.000271 0.3558

R-squared 0.513535 Mean dependent var 5.540797

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Adjusted R-squared 0.270303 S.D. dependent var 3.712652

S.E. of regression 3.171433 Akaike info criterion 5.435419

Sum squared resid 60.34793 Schwarz criterion 5.556453

Log likelihood -23.17709 Hannan-Quinn criter. 5.302645

F-statistic 2.111294 Durbin-Watson stat 2.100732

Prob(F-statistic) 0.200171

Dependent Variable: ROA

Method: Least Squares

Date: 08/27/18 Time: 17:05

Sample: 2008 2017

Included observations: 10

Variable Coefficient Std. Error t-Statistic Prob.

C 10.10942 17.52005 0.577020 0.5849

INVENTORY_TURNOVER_RATI

O -0.061758 0.247614 -0.249414 0.8114

RECEIVABLES_TURNOVER_RA

T -0.000677 0.003628 -0.186589 0.8581

PAYABLES_PERIOD 0.057754 0.052756 1.094747 0.3156

R-squared 0.171114 Mean dependent var 10.03240

Adjusted R-squared -0.243330 S.D. dependent var 2.650911

6

S.E. of regression 3.171433 Akaike info criterion 5.435419

Sum squared resid 60.34793 Schwarz criterion 5.556453

Log likelihood -23.17709 Hannan-Quinn criter. 5.302645

F-statistic 2.111294 Durbin-Watson stat 2.100732

Prob(F-statistic) 0.200171

Dependent Variable: ROA

Method: Least Squares

Date: 08/27/18 Time: 17:05

Sample: 2008 2017

Included observations: 10

Variable Coefficient Std. Error t-Statistic Prob.

C 10.10942 17.52005 0.577020 0.5849

INVENTORY_TURNOVER_RATI

O -0.061758 0.247614 -0.249414 0.8114

RECEIVABLES_TURNOVER_RA

T -0.000677 0.003628 -0.186589 0.8581

PAYABLES_PERIOD 0.057754 0.052756 1.094747 0.3156

R-squared 0.171114 Mean dependent var 10.03240

Adjusted R-squared -0.243330 S.D. dependent var 2.650911

6

S.E. of regression 2.955890 Akaike info criterion 5.294651

Sum squared resid 52.42372 Schwarz criterion 5.415685

Log likelihood -22.47326 Hannan-Quinn criter. 5.161877

F-statistic 0.412876 Durbin-Watson stat 2.486239

Prob(F-statistic) 0.750027

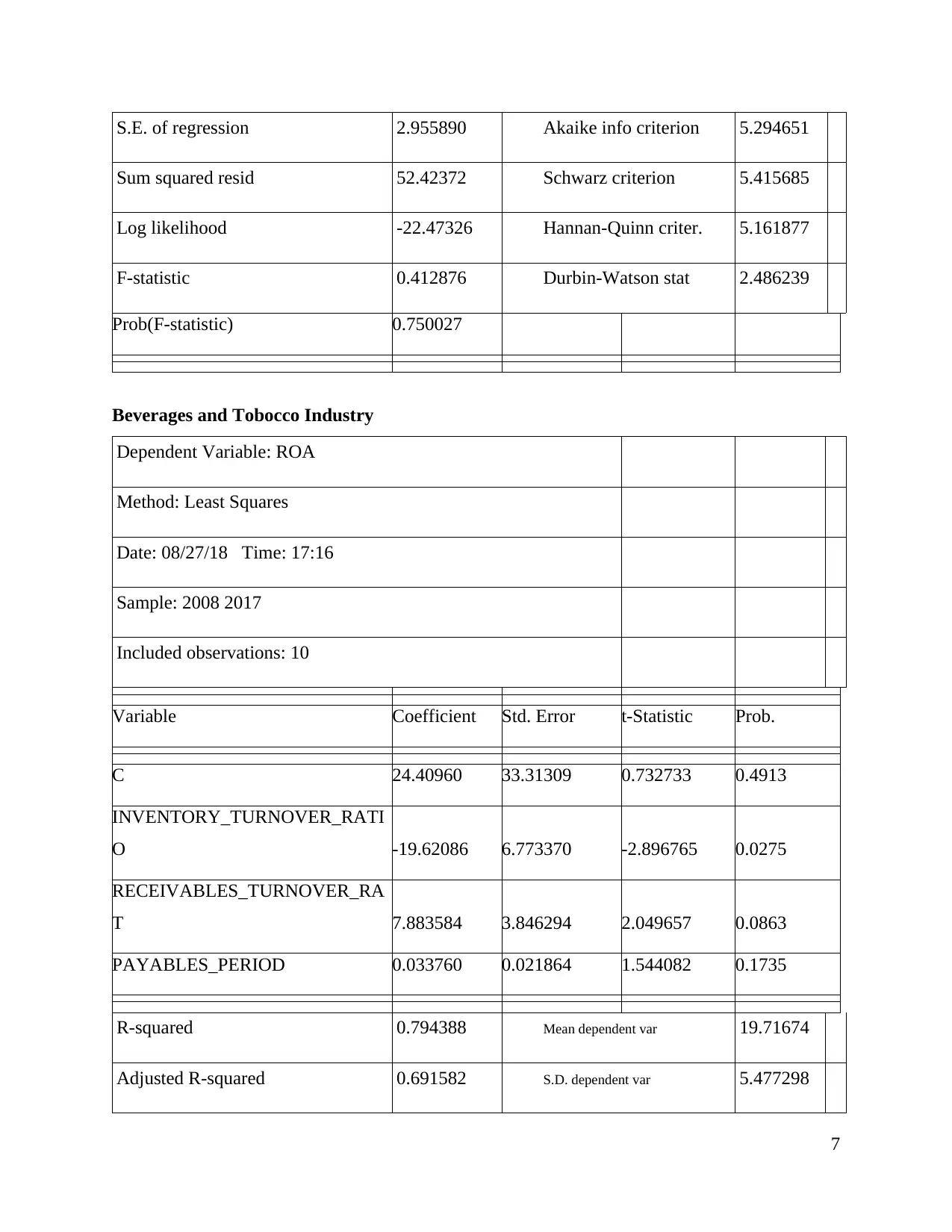

Beverages and Tobocco Industry

Dependent Variable: ROA

Method: Least Squares

Date: 08/27/18 Time: 17:16

Sample: 2008 2017

Included observations: 10

Variable Coefficient Std. Error t-Statistic Prob.

C 24.40960 33.31309 0.732733 0.4913

INVENTORY_TURNOVER_RATI

O -19.62086 6.773370 -2.896765 0.0275

RECEIVABLES_TURNOVER_RA

T 7.883584 3.846294 2.049657 0.0863

PAYABLES_PERIOD 0.033760 0.021864 1.544082 0.1735

R-squared 0.794388 Mean dependent var 19.71674

Adjusted R-squared 0.691582 S.D. dependent var 5.477298

7

Sum squared resid 52.42372 Schwarz criterion 5.415685

Log likelihood -22.47326 Hannan-Quinn criter. 5.161877

F-statistic 0.412876 Durbin-Watson stat 2.486239

Prob(F-statistic) 0.750027

Beverages and Tobocco Industry

Dependent Variable: ROA

Method: Least Squares

Date: 08/27/18 Time: 17:16

Sample: 2008 2017

Included observations: 10

Variable Coefficient Std. Error t-Statistic Prob.

C 24.40960 33.31309 0.732733 0.4913

INVENTORY_TURNOVER_RATI

O -19.62086 6.773370 -2.896765 0.0275

RECEIVABLES_TURNOVER_RA

T 7.883584 3.846294 2.049657 0.0863

PAYABLES_PERIOD 0.033760 0.021864 1.544082 0.1735

R-squared 0.794388 Mean dependent var 19.71674

Adjusted R-squared 0.691582 S.D. dependent var 5.477298

7

S.E. of regression 3.041839 Akaike info criterion 5.351976

Sum squared resid 55.51672 Schwarz criterion 5.473010

Log likelihood -22.75988 Hannan-Quinn criter. 5.219202

F-statistic 7.727058 Durbin-Watson stat 2.458019

Prob(F-statistic) 0.017483

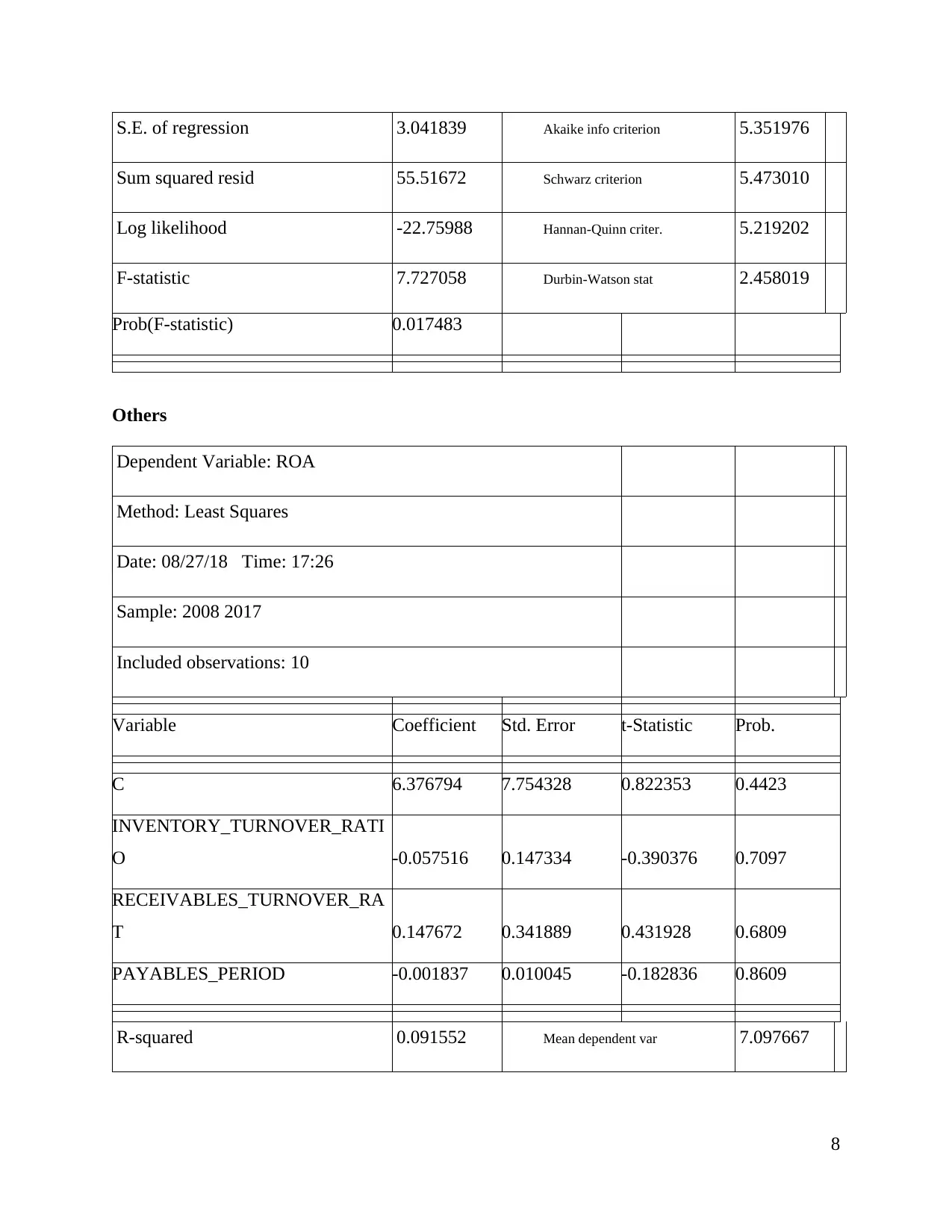

Others

Dependent Variable: ROA

Method: Least Squares

Date: 08/27/18 Time: 17:26

Sample: 2008 2017

Included observations: 10

Variable Coefficient Std. Error t-Statistic Prob.

C 6.376794 7.754328 0.822353 0.4423

INVENTORY_TURNOVER_RATI

O -0.057516 0.147334 -0.390376 0.7097

RECEIVABLES_TURNOVER_RA

T 0.147672 0.341889 0.431928 0.6809

PAYABLES_PERIOD -0.001837 0.010045 -0.182836 0.8609

R-squared 0.091552 Mean dependent var 7.097667

8

Sum squared resid 55.51672 Schwarz criterion 5.473010

Log likelihood -22.75988 Hannan-Quinn criter. 5.219202

F-statistic 7.727058 Durbin-Watson stat 2.458019

Prob(F-statistic) 0.017483

Others

Dependent Variable: ROA

Method: Least Squares

Date: 08/27/18 Time: 17:26

Sample: 2008 2017

Included observations: 10

Variable Coefficient Std. Error t-Statistic Prob.

C 6.376794 7.754328 0.822353 0.4423

INVENTORY_TURNOVER_RATI

O -0.057516 0.147334 -0.390376 0.7097

RECEIVABLES_TURNOVER_RA

T 0.147672 0.341889 0.431928 0.6809

PAYABLES_PERIOD -0.001837 0.010045 -0.182836 0.8609

R-squared 0.091552 Mean dependent var 7.097667

8

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Adjusted R-squared -0.362672 S.D. dependent var 1.460114

S.E. of regression 1.704443 Akaike info criterion 4.193529

Sum squared resid 17.43076 Schwarz criterion 4.314563

Log likelihood -16.96764 Hannan-Quinn criter. 4.060755

F-statistic 0.201556 Durbin-Watson stat 2.125073

Prob(F-statistic) 0.891686

6. Analysing results of regression

Retail Industry

Interpretation-

It can be interpreted from the above regression analysis that retail industry is highly

competitive so it needs to have efficient working capital. Payable period is highlighted in a

probability that it is 0.05 which is more than significance level and it shows that alternative

hypotheses is accepted and this implies that there is significant impact on ROA because of

payables and as a result, hypotheses tends to be true.

On the other hand, accounts receivable is 0.3558 which is less than acceptance criteria.

Moreover, inventory turnover calculated is 0.86 and it clearly signifies firm's profitability is not

dependent on accounts receivable and stock period. In case of retail industry, R square attained is

0.51353 which means that no strong relationship is found between company profitability and

working capital management. It signifies retail industry is moderately affected in terms of profits

with respect to net working capital. This is means that retail companies have moderate impact on

the profitability aspect.

Discussion-

There is consideration of three variables for assessing profitability of retail sector such as

return on assets, receivables turnover and payables period. These three variables are directly

impacting whole retail industry. The organisation which belongs to retail industry, highly relies

on managing its working capital as it is very important function for gaining profitability and for

9

S.E. of regression 1.704443 Akaike info criterion 4.193529

Sum squared resid 17.43076 Schwarz criterion 4.314563

Log likelihood -16.96764 Hannan-Quinn criter. 4.060755

F-statistic 0.201556 Durbin-Watson stat 2.125073

Prob(F-statistic) 0.891686

6. Analysing results of regression

Retail Industry

Interpretation-

It can be interpreted from the above regression analysis that retail industry is highly

competitive so it needs to have efficient working capital. Payable period is highlighted in a

probability that it is 0.05 which is more than significance level and it shows that alternative

hypotheses is accepted and this implies that there is significant impact on ROA because of

payables and as a result, hypotheses tends to be true.

On the other hand, accounts receivable is 0.3558 which is less than acceptance criteria.

Moreover, inventory turnover calculated is 0.86 and it clearly signifies firm's profitability is not

dependent on accounts receivable and stock period. In case of retail industry, R square attained is

0.51353 which means that no strong relationship is found between company profitability and

working capital management. It signifies retail industry is moderately affected in terms of profits

with respect to net working capital. This is means that retail companies have moderate impact on

the profitability aspect.

Discussion-

There is consideration of three variables for assessing profitability of retail sector such as

return on assets, receivables turnover and payables period. These three variables are directly

impacting whole retail industry. The organisation which belongs to retail industry, highly relies

on managing its working capital as it is very important function for gaining profitability and for

9

avoiding solvency. Return on assets of any organization helps in measuring efficiency of its

operations for producing profits via its assets, but initially it is giving impact on financing. In the

same series, it had reflected receivable turnover ratio which is measuring level of efficiency of

application of its assets via organization. There is articulation of payables period as it is one of

the major component of cash conversion cycle. Generally, it helps in measuring effectiveness of

management and duration in which cash can be converted into cash in hand.

Among these variables, payables period is very important as it is directly linked to

working capital. It is required to be managed properly else it leads to bankruptcy. The main

function of this variable is to measure duration of organization for repaying its invoices from its

trade creditors like suppliers. It signifies money which is owed for paying back in small duration.

In this scenario, the relationship among credit purchases and payments had been maintained. If

payables period is short, then it increases cash in hand which help in attaining huge returns

which can be invested in specific business. For the purpose of organization, it is considered as

very important for businesses to know fund level which could be invested in every component of

current assets. In the same series, it had direct relationship with organization's liquidity and

profitability.

Travel and Leisure Industry

Interpretation:

Considering the classical linear regression models for identifying outcomes and

presenting the profitable solutions to the issues which have been faced by organization in due

period. However, the above listed determination of the outcomes which are based on travel and

leisure industry have been addressed. Thus, on the basis of outcomes, it can be said that the

probability value is comparatively higher than 0.5 which indicate that there is a significant

difference between performance of organization and working capital management. Similarly, as

per various statistical analysis it has been demonstrated that R-square as 0.17, F-statistic as 0.41,

mean dependent variable as 10.03, standard deviation as 2.65, etc. Moreover, analysing such

outcomes on it can be assessed that, the changes in the working capital variables will affect

operational performance of the business. Thus, the variations incurred in current assets and

liabilities will have affect operational practices and variations.

Discussion:

10

operations for producing profits via its assets, but initially it is giving impact on financing. In the

same series, it had reflected receivable turnover ratio which is measuring level of efficiency of

application of its assets via organization. There is articulation of payables period as it is one of

the major component of cash conversion cycle. Generally, it helps in measuring effectiveness of

management and duration in which cash can be converted into cash in hand.

Among these variables, payables period is very important as it is directly linked to

working capital. It is required to be managed properly else it leads to bankruptcy. The main

function of this variable is to measure duration of organization for repaying its invoices from its

trade creditors like suppliers. It signifies money which is owed for paying back in small duration.

In this scenario, the relationship among credit purchases and payments had been maintained. If

payables period is short, then it increases cash in hand which help in attaining huge returns

which can be invested in specific business. For the purpose of organization, it is considered as

very important for businesses to know fund level which could be invested in every component of

current assets. In the same series, it had direct relationship with organization's liquidity and

profitability.

Travel and Leisure Industry

Interpretation:

Considering the classical linear regression models for identifying outcomes and

presenting the profitable solutions to the issues which have been faced by organization in due

period. However, the above listed determination of the outcomes which are based on travel and

leisure industry have been addressed. Thus, on the basis of outcomes, it can be said that the

probability value is comparatively higher than 0.5 which indicate that there is a significant

difference between performance of organization and working capital management. Similarly, as

per various statistical analysis it has been demonstrated that R-square as 0.17, F-statistic as 0.41,

mean dependent variable as 10.03, standard deviation as 2.65, etc. Moreover, analysing such

outcomes on it can be assessed that, the changes in the working capital variables will affect

operational performance of the business. Thus, the variations incurred in current assets and

liabilities will have affect operational practices and variations.

Discussion:

10

On the basis of above listed analysis and the various outcomes which have been

determined to have adequate operational solutions to issues in the study. There has been analysis

based on performance of 20 FTSE 100 listed organization with the motive of having proper

operational practices and control on each solution. However, 10 years of data has been gathered

and analysed to evaluate concrete solutions to the issues. Considering the outcomes derived from

analysis of retail industry on which measurement is had been done based on inventory turnover

ratio, payables period and receivable turnover ratio.

As per demonstrating outcome on which it can be said that, probability in most variables

turns out to be more than 0.5 in all ratio which implies that there will be acceptance to the

alternative hypothesis and rejection to the null hypothesis. It states that, there is a significant

difference between organization's performance and working capital management. Therefore, it is

required that businesses in travel and leisure industry to initiate control on its current assets and

liabilities for better execution and operational control on practices.

In relation to beverages and tobacco industries the outcome is comparatively higher than

the idle 0.5 probability. Thus, it determined that, there is no significant difference between

organization's profitability and working capital management. In addition, there will be impact on

the profitability and operational performance of the industries as there is need to have control on

working capital of business. They balance between amount of short term debts and assets on

favourable instinct. Similarly, there is need to have administration on the short-term solvency of

entity.

As per ascertaining the other industries, the probability outcomes have been determined

in analysis of statistical test. Thus, there are mixed reviews over the results which will be

presented as per concrete solution to the issues. The probability of various outcomes is less than

0.5 of value which represents that, there is no significant difference between organization's

performance and working capital management While considering the other outcomes which

determines the p value more than 0.5. Thus, such outcomes demonstrate that, there is a

significant difference between firm's performance and working capital management. Moreover, it

is necessary that there is need to have effective control on the operational efficiency and gains of

the business. In addition, the changes in working capital amount will have impact on operational

performance and practices of the industry. Thus, there is requirement of making better control on

the debts as well as liquid asset of firm.

11

determined to have adequate operational solutions to issues in the study. There has been analysis

based on performance of 20 FTSE 100 listed organization with the motive of having proper

operational practices and control on each solution. However, 10 years of data has been gathered

and analysed to evaluate concrete solutions to the issues. Considering the outcomes derived from

analysis of retail industry on which measurement is had been done based on inventory turnover

ratio, payables period and receivable turnover ratio.

As per demonstrating outcome on which it can be said that, probability in most variables

turns out to be more than 0.5 in all ratio which implies that there will be acceptance to the

alternative hypothesis and rejection to the null hypothesis. It states that, there is a significant

difference between organization's performance and working capital management. Therefore, it is

required that businesses in travel and leisure industry to initiate control on its current assets and

liabilities for better execution and operational control on practices.

In relation to beverages and tobacco industries the outcome is comparatively higher than

the idle 0.5 probability. Thus, it determined that, there is no significant difference between

organization's profitability and working capital management. In addition, there will be impact on

the profitability and operational performance of the industries as there is need to have control on

working capital of business. They balance between amount of short term debts and assets on

favourable instinct. Similarly, there is need to have administration on the short-term solvency of

entity.

As per ascertaining the other industries, the probability outcomes have been determined

in analysis of statistical test. Thus, there are mixed reviews over the results which will be

presented as per concrete solution to the issues. The probability of various outcomes is less than

0.5 of value which represents that, there is no significant difference between organization's

performance and working capital management While considering the other outcomes which

determines the p value more than 0.5. Thus, such outcomes demonstrate that, there is a

significant difference between firm's performance and working capital management. Moreover, it

is necessary that there is need to have effective control on the operational efficiency and gains of

the business. In addition, the changes in working capital amount will have impact on operational

performance and practices of the industry. Thus, there is requirement of making better control on

the debts as well as liquid asset of firm.

11

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Beverages and Tobacco Industry

Interpretation-

It can be interpreted that Beverages and Tobacco industry is affected by inventory

turnover up to certain extent. It is evident from fact that probability attained is 0.0275 which is

more than significant level showing clearly firm's position in terms of profitability is much

affected by working capital management particularly inventory which is crucial element as

production is done of beverages and tobacco. Apart from this, receivable turnover is 0.08 and

payable period turns out to be 0.17 implying beverage sector's profits have direct dependency on

working capital used for meeting out daily operational activities in the best possible manner.

This means that working capital should be managed properly for enlarging profits.

Discussion-

The working capital in beverages and tobacco industry is taken in consideration to

analyse whether profits are largely affected or not. R squared turns out to be 0.79 which signifies

net income which gets much impacted because of working capital. It is a production sector in

which efficiency of working capital must be efficiently operated so that no interruptions may

prevail. F-statistic is 0.01, Mean dependent variable is 19.71674 which represents that there is

some sort of relationship between regression equations and hypotheses in this industry.

Moreover, receivable and payable turnover ratio is moderate which means that main impact on

profits is of inventory. Hence, stock should be replenishing quickly so as to attain desired level

of production and thus, profits could be increased with ease.

Others

Interpretation-

It can be analysed from above chart that other sector is also attaining good amount of

profits and helping UK economy to maximise growth in a better way. Past ten years of data of

companies shows positive growth. The output clearly implies that working capital management

has moderate impact on the profitability position of company. Inventory turnover turns out to be

0.70, while receivable is 0.68 and payable is 0.86 which shows that industry is moderately

affected by working capital management. It is required that current assets should be managed

properly so that liabilities can be met with much ease. This is mainly needed because operational

activities can be enhanced and production could be met leading to have enormous profits.

12

Interpretation-

It can be interpreted that Beverages and Tobacco industry is affected by inventory

turnover up to certain extent. It is evident from fact that probability attained is 0.0275 which is

more than significant level showing clearly firm's position in terms of profitability is much

affected by working capital management particularly inventory which is crucial element as

production is done of beverages and tobacco. Apart from this, receivable turnover is 0.08 and

payable period turns out to be 0.17 implying beverage sector's profits have direct dependency on

working capital used for meeting out daily operational activities in the best possible manner.

This means that working capital should be managed properly for enlarging profits.

Discussion-

The working capital in beverages and tobacco industry is taken in consideration to

analyse whether profits are largely affected or not. R squared turns out to be 0.79 which signifies

net income which gets much impacted because of working capital. It is a production sector in

which efficiency of working capital must be efficiently operated so that no interruptions may

prevail. F-statistic is 0.01, Mean dependent variable is 19.71674 which represents that there is

some sort of relationship between regression equations and hypotheses in this industry.

Moreover, receivable and payable turnover ratio is moderate which means that main impact on

profits is of inventory. Hence, stock should be replenishing quickly so as to attain desired level

of production and thus, profits could be increased with ease.

Others

Interpretation-

It can be analysed from above chart that other sector is also attaining good amount of

profits and helping UK economy to maximise growth in a better way. Past ten years of data of

companies shows positive growth. The output clearly implies that working capital management

has moderate impact on the profitability position of company. Inventory turnover turns out to be

0.70, while receivable is 0.68 and payable is 0.86 which shows that industry is moderately

affected by working capital management. It is required that current assets should be managed

properly so that liabilities can be met with much ease. This is mainly needed because operational

activities can be enhanced and production could be met leading to have enormous profits.

12

Discussion-

The working capital management is derived by taking into account inventory turnover,

receivable turnover and payable period. R squared value is 0.091552 and probability F-statistic is

0.891686 which means that industry is required to take into consideration working capital so that

it will be able to attain efficiency in operational tasks in an effective manner. Moreover, it is

required that companies need to replenish stocks efficiently, to make timely payments to

suppliers so as to accomplish discounts on quicker payments. On the other hand, it is required

that credit allowed to customers such as debtors should be approached to make timely payments

within credit period because, cash conversion cycle needs to be balanced and financing

requirements are met accordingly. Moreover, industry has mean dependent variable amounting

to 7.097667 and it implies that sector is contributing to economic growth quite effectually.

7. RECOMMENDATIONS

According to this data analysis, working capital such as payables period, return on asset,

receivable and inventory turnover ratio have been used for assessing profitability level. It had

been analysed that retail industry got impacted from its payables as it is directly affecting its

financials and growth. It is also referred as creditors payment period which is very important

source for financing on short term aspect usually from businesses which are small and lost

capability for attaining funds via bank and financial institutions. With context of retail industry,

suppliers before granting period of credit always considers credit worthiness of company. The

capability of organization had been examined via supplier for repaying its raw materials.

In this analysis, profitability is referred as very significant factor for considering and

examining credit worthiness of particular business along with retail industry. It had retained huge

impact from its payables period as business is capable for investing through significant amount

which is returned to business. It would be directly indicating about continuity of business for

long term aspect. In the same series, it had interpreted analysis of travel and leisure industry in

which alternative hypothesis is accepted. It could be stated that working capital impacts

profitability of company up to certain extent.

According to this specific analysis, it had been recommended that retail industry must be

able to maintain its payable period which gives major impact on working capital. If working

capital is strong then it would be considered as positive aspect with reference to growth and

13

The working capital management is derived by taking into account inventory turnover,

receivable turnover and payable period. R squared value is 0.091552 and probability F-statistic is

0.891686 which means that industry is required to take into consideration working capital so that

it will be able to attain efficiency in operational tasks in an effective manner. Moreover, it is

required that companies need to replenish stocks efficiently, to make timely payments to

suppliers so as to accomplish discounts on quicker payments. On the other hand, it is required

that credit allowed to customers such as debtors should be approached to make timely payments

within credit period because, cash conversion cycle needs to be balanced and financing

requirements are met accordingly. Moreover, industry has mean dependent variable amounting

to 7.097667 and it implies that sector is contributing to economic growth quite effectually.

7. RECOMMENDATIONS

According to this data analysis, working capital such as payables period, return on asset,

receivable and inventory turnover ratio have been used for assessing profitability level. It had

been analysed that retail industry got impacted from its payables as it is directly affecting its

financials and growth. It is also referred as creditors payment period which is very important

source for financing on short term aspect usually from businesses which are small and lost

capability for attaining funds via bank and financial institutions. With context of retail industry,

suppliers before granting period of credit always considers credit worthiness of company. The

capability of organization had been examined via supplier for repaying its raw materials.

In this analysis, profitability is referred as very significant factor for considering and

examining credit worthiness of particular business along with retail industry. It had retained huge

impact from its payables period as business is capable for investing through significant amount

which is returned to business. It would be directly indicating about continuity of business for

long term aspect. In the same series, it had interpreted analysis of travel and leisure industry in

which alternative hypothesis is accepted. It could be stated that working capital impacts

profitability of company up to certain extent.

According to this specific analysis, it had been recommended that retail industry must be

able to maintain its payable period which gives major impact on working capital. If working

capital is strong then it would be considered as positive aspect with reference to growth and

13

profitability. In the same series, except these variable company should be capable to keep perfect

balance on debt and equity as its ideal ratio is 40:60 which should be followed. Further, various

organizations are struggling on inventory, as it is necessary that investment in inventory should

be made judiciously else profits gets decline. The credit policies of organization enable major

impact on volume of goods which are sold. The longer credit period had been grant then it would

encourage sales along with profit. Along with these factors, there are various external factors

which gives impact on profitability of organization such as market share, cost of production,

rivalry competition, economic growth, product life cycle, brand image and exchange rate. It had

been recommended that to manage working capital, payables period or cash conversion cycle in

efficient aspect. It helps in satisfying requirements of short term financial of any specific

business entity.

CONCLUSION

On the basis of above report it can be concluded that working capital has major impact on

profitability of company. It basically denotes the changes in the short-term solvency of business.

The current liabilities, assets determine the short-term solvency of the business. Thus,

appropriate execution and administration of the financial issues will be resolved for making

qualitative control in each activity. Along with this, analysis based on 20 industries operating on

different segmentation have been addressed and analysed. It demonstrated that there is a

significant difference between organization's performance and working capital management.

Thus, the impacts of changes in working capital outcomes will affect the operational functioning

of the industries on short-term basis. Operational administration will be beneficial for enhancing

the performance of industry on most satisfactory stage.

14

balance on debt and equity as its ideal ratio is 40:60 which should be followed. Further, various

organizations are struggling on inventory, as it is necessary that investment in inventory should

be made judiciously else profits gets decline. The credit policies of organization enable major

impact on volume of goods which are sold. The longer credit period had been grant then it would

encourage sales along with profit. Along with these factors, there are various external factors

which gives impact on profitability of organization such as market share, cost of production,

rivalry competition, economic growth, product life cycle, brand image and exchange rate. It had

been recommended that to manage working capital, payables period or cash conversion cycle in

efficient aspect. It helps in satisfying requirements of short term financial of any specific

business entity.

CONCLUSION

On the basis of above report it can be concluded that working capital has major impact on

profitability of company. It basically denotes the changes in the short-term solvency of business.

The current liabilities, assets determine the short-term solvency of the business. Thus,

appropriate execution and administration of the financial issues will be resolved for making

qualitative control in each activity. Along with this, analysis based on 20 industries operating on

different segmentation have been addressed and analysed. It demonstrated that there is a

significant difference between organization's performance and working capital management.

Thus, the impacts of changes in working capital outcomes will affect the operational functioning

of the industries on short-term basis. Operational administration will be beneficial for enhancing

the performance of industry on most satisfactory stage.

14

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

REFERENCES

Books and Journals

Abor, J. Y., 2017. Working Capital Management. In Entrepreneurial Finance for MSMEs (pp.

225-255). Palgrave Macmillan, Cham.

Afrifa, G. A. and Padachi, K., 2016. Working capital level influence on SME

profitability. Journal of Small Business and Enterprise Development. 23(1). pp.44-63.

Afrifa, G. A., 2016. Net working capital, cash flow and performance of UK SMEs. Review of

Accounting and Finance.15(1). pp.21-44.

Baker, S. and Chapin III, F. S., 2018. Going beyond" it depends:" the role of context in shaping

participation in natural resource management. Ecology and Society. 23(1).

Bhatia, S. and Srivastava, A., 2016. Working capital management and firm performance in

emerging economies: evidence from India. Management and Labour Studies. 41(2). pp.71-

87.

Charitou, M. S., Elfani, M. and Lois, P., 2016. The Effect of Working Capital Management On

Firm's Profitability: Empirical Evidence from an Emerging Market. Journal of Business &

Economics Research (Online). 14(3). p.111.

Christopher, M., 2016. Logistics & supply chain management. Pearson UK.

Cooke, F. L., Wood, G., Wang, M. and Veen, A., 2018. How far has international HRM

travelled? A systematic review of literature on multinational corporations (2000–

2014). Human Resource Management Review.

Oliveira, M.P.V.D. and Handfield, R., 2018. Analytical foundations for development of real-time

supply chain capabilities. International Journal of Production Research. pp.1-19.

Sarma, A. and Barua, P., 2018. Challenges of Human Resource Management in Hospitals and

their probable solutions: A study based on review of literature. Journal of Management in

Practice. 3(1).

Singla, A., Sethi, A.P.S. and Ahuja, I. S., 2018. An empirical examination of critical barriers in

transitions between technology push and demand pull strategies in manufacturing

organizations. World Journal of Science, Technology and Sustainable Development.

15

Books and Journals

Abor, J. Y., 2017. Working Capital Management. In Entrepreneurial Finance for MSMEs (pp.

225-255). Palgrave Macmillan, Cham.

Afrifa, G. A. and Padachi, K., 2016. Working capital level influence on SME

profitability. Journal of Small Business and Enterprise Development. 23(1). pp.44-63.

Afrifa, G. A., 2016. Net working capital, cash flow and performance of UK SMEs. Review of

Accounting and Finance.15(1). pp.21-44.

Baker, S. and Chapin III, F. S., 2018. Going beyond" it depends:" the role of context in shaping

participation in natural resource management. Ecology and Society. 23(1).

Bhatia, S. and Srivastava, A., 2016. Working capital management and firm performance in

emerging economies: evidence from India. Management and Labour Studies. 41(2). pp.71-

87.

Charitou, M. S., Elfani, M. and Lois, P., 2016. The Effect of Working Capital Management On

Firm's Profitability: Empirical Evidence from an Emerging Market. Journal of Business &

Economics Research (Online). 14(3). p.111.

Christopher, M., 2016. Logistics & supply chain management. Pearson UK.

Cooke, F. L., Wood, G., Wang, M. and Veen, A., 2018. How far has international HRM

travelled? A systematic review of literature on multinational corporations (2000–

2014). Human Resource Management Review.

Oliveira, M.P.V.D. and Handfield, R., 2018. Analytical foundations for development of real-time

supply chain capabilities. International Journal of Production Research. pp.1-19.

Sarma, A. and Barua, P., 2018. Challenges of Human Resource Management in Hospitals and

their probable solutions: A study based on review of literature. Journal of Management in

Practice. 3(1).

Singla, A., Sethi, A.P.S. and Ahuja, I. S., 2018. An empirical examination of critical barriers in

transitions between technology push and demand pull strategies in manufacturing

organizations. World Journal of Science, Technology and Sustainable Development.

15

ONLINE

Clark. 2015. Trade-off and Pecking-order Theories. [Online]. Available Through:

<http://elijahclark.com/trade-off-and-pecking-order-theories/>

16

Clark. 2015. Trade-off and Pecking-order Theories. [Online]. Available Through:

<http://elijahclark.com/trade-off-and-pecking-order-theories/>

16

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.