Corporate Performance Report: Financial Analysis of Rio Tinto Plc

VerifiedAdded on 2023/05/28

|20

|6033

|192

Report

AI Summary

This report presents a financial evaluation of Rio Tinto, focusing on its corporate performance to guide investment decisions for the Arden Fund. The analysis utilizes ratio analysis to assess profitability, liquidity, leverage, and efficiency over a period of time. The report includes an introduction, a detailed explanation of financial statement analysis, and the factors influencing investment decisions. The analysis covers profitability, liquidity, financial leverage, and efficiency ratios, using financial data from 2013 to 2017. The report identifies potential risks and issues within the company, and concludes with recommendations for investors. The report also includes an analysis of the financial report using corporate accounting principles, and a reflective statement commenting on the effectiveness of the analysis process. The report is well-referenced and provides a comprehensive overview of Rio Tinto's financial performance, including the identification of key strengths, weaknesses, and potential risks.

1

Corporate Performance Report of Rio Tinto

Corporate Performance Report of Rio Tinto

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2

Executive Summary

The present report is developed for carrying out financial evaluation of Rio Tinto to

determine its prospects of future growth and development. This is mainly carried out for guiding

the decision of Arden Fund investors who want to invest in the company. As such, the report has

incorporated the use of ratio analysis for determining the profitability, liquidity, leverage and

earning potential of the company to identify the potential risk and issues in advance. It has been

identified through the use of financial analysis that there is significant risk of generating good

profits for the shareholders within the company. Thus, it has been recommended to the investors

for analyzing the future performance of the company for the coming period of time before

investing within the company.

Executive Summary

The present report is developed for carrying out financial evaluation of Rio Tinto to

determine its prospects of future growth and development. This is mainly carried out for guiding

the decision of Arden Fund investors who want to invest in the company. As such, the report has

incorporated the use of ratio analysis for determining the profitability, liquidity, leverage and

earning potential of the company to identify the potential risk and issues in advance. It has been

identified through the use of financial analysis that there is significant risk of generating good

profits for the shareholders within the company. Thus, it has been recommended to the investors

for analyzing the future performance of the company for the coming period of time before

investing within the company.

3

Contents

Executive Summary.........................................................................................................................2

1.0: Answer 1: Financial Report of Rio Tinto.................................................................................4

2.0: Introduction.............................................................................................................................4

3.0: Understanding the meaning of the financial statement analysis...............................................4

4.0: Factors that influences the making of investment decision......................................................4

5.0: Analysis of financial statements of Rio Tinto..........................................................................5

5.1: Ratio Analysis...........................................................................................................................5

Financial Data of Rio Tinto.............................................................................................................5

Profitability Analysis.......................................................................................................................6

Liquidity Analysis...........................................................................................................................8

Financial Leverage Analysis............................................................................................................9

Efficiency Analysis........................................................................................................................11

5.2: Earnings Analysis...................................................................................................................12

6.0: Potential Risks or Potential Issues..........................................................................................12

7.0: Conclusion..............................................................................................................................13

8.0: Solution 2: Analysis of financial report produced in question 1 through using corporate

accounting principles.....................................................................................................................14

9.0: Solution 3: Reflective Statement Commenting on the Effectiveness of the Process from

Questions 1 and 2...........................................................................................................................16

10.0: References............................................................................................................................18

Contents

Executive Summary.........................................................................................................................2

1.0: Answer 1: Financial Report of Rio Tinto.................................................................................4

2.0: Introduction.............................................................................................................................4

3.0: Understanding the meaning of the financial statement analysis...............................................4

4.0: Factors that influences the making of investment decision......................................................4

5.0: Analysis of financial statements of Rio Tinto..........................................................................5

5.1: Ratio Analysis...........................................................................................................................5

Financial Data of Rio Tinto.............................................................................................................5

Profitability Analysis.......................................................................................................................6

Liquidity Analysis...........................................................................................................................8

Financial Leverage Analysis............................................................................................................9

Efficiency Analysis........................................................................................................................11

5.2: Earnings Analysis...................................................................................................................12

6.0: Potential Risks or Potential Issues..........................................................................................12

7.0: Conclusion..............................................................................................................................13

8.0: Solution 2: Analysis of financial report produced in question 1 through using corporate

accounting principles.....................................................................................................................14

9.0: Solution 3: Reflective Statement Commenting on the Effectiveness of the Process from

Questions 1 and 2...........................................................................................................................16

10.0: References............................................................................................................................18

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4

1.0: Answer 1: Financial Report of Rio Tinto

2.0: Introduction

The analysis of internal and external performance of a firm is very important for

assessing its present and future potential of growth. This forms the basis for decision-making

process of investors for their investment decisions. In this context, the present report is

developed for assessing the internal as well as external performance of Rio Tinto, an Australian

multinational metals and mining company established in the year 1873 and headquartered within

the UK. This is mainly done for guiding the decision-making process of Arden Fund, a collection

of ethical investors interested in buying a significant volume of shares in Rio Tinto Plc. The

external performance of the firm is evaluated in the report through the use of financial analysis

that is through the technique of ratio analysis. The internal performance is evaluated by assessing

the effectiveness of its internal processes as analyzed on the basis of the results of its financial

analysis.

3.0: Understanding the meaning of the financial statement analysis

The financial statements can be defined as the summary of the operating, financing and

investment activities of a business. The financial statement analysis can be described as the

process of reviewing and analyzing the financial performance of a company through evaluation

of its financial reports. It intends to examine the past and current financial data for assessing its

present and future growth potential. The most important benefit of financial statement analysis is

to provide idea to the investors for guiding their investment decisions by prediction of a

company future financial performance. The main type of financial statements that are developed

by a business entity for disclosing the financial performances to the external stakeholders are

equity statement, income statement, balance sheet and statement of cash flow. Equity statement

reflects the part of the value of a firm that is owned by the creditors whereas income statement

reflects a summary of the revenue and expenses. Balance sheet depicts the summary of assets,

liabilities and equity while cash flow statement depicts the summary of cash flows over a period

of time. The analysis of all these financial statement determines a firm internal strength and

weakness and established its future strategic direction by developing of possible measures to

overcome its weakness.

4.0: Factors that influences the making of investment decision

Financial ratio analysis can be regarded as the most important tool for financial analysis

that guides the decision-making process of investors. Ratio analysis proves to be most

appropriate for evaluation of the various aspects of a company’s performance that are, efficiency,

liquidly, profitability and solvency. The Arden Fund Investors through the use of technique of

1.0: Answer 1: Financial Report of Rio Tinto

2.0: Introduction

The analysis of internal and external performance of a firm is very important for

assessing its present and future potential of growth. This forms the basis for decision-making

process of investors for their investment decisions. In this context, the present report is

developed for assessing the internal as well as external performance of Rio Tinto, an Australian

multinational metals and mining company established in the year 1873 and headquartered within

the UK. This is mainly done for guiding the decision-making process of Arden Fund, a collection

of ethical investors interested in buying a significant volume of shares in Rio Tinto Plc. The

external performance of the firm is evaluated in the report through the use of financial analysis

that is through the technique of ratio analysis. The internal performance is evaluated by assessing

the effectiveness of its internal processes as analyzed on the basis of the results of its financial

analysis.

3.0: Understanding the meaning of the financial statement analysis

The financial statements can be defined as the summary of the operating, financing and

investment activities of a business. The financial statement analysis can be described as the

process of reviewing and analyzing the financial performance of a company through evaluation

of its financial reports. It intends to examine the past and current financial data for assessing its

present and future growth potential. The most important benefit of financial statement analysis is

to provide idea to the investors for guiding their investment decisions by prediction of a

company future financial performance. The main type of financial statements that are developed

by a business entity for disclosing the financial performances to the external stakeholders are

equity statement, income statement, balance sheet and statement of cash flow. Equity statement

reflects the part of the value of a firm that is owned by the creditors whereas income statement

reflects a summary of the revenue and expenses. Balance sheet depicts the summary of assets,

liabilities and equity while cash flow statement depicts the summary of cash flows over a period

of time. The analysis of all these financial statement determines a firm internal strength and

weakness and established its future strategic direction by developing of possible measures to

overcome its weakness.

4.0: Factors that influences the making of investment decision

Financial ratio analysis can be regarded as the most important tool for financial analysis

that guides the decision-making process of investors. Ratio analysis proves to be most

appropriate for evaluation of the various aspects of a company’s performance that are, efficiency,

liquidly, profitability and solvency. The Arden Fund Investors through the use of technique of

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5

financial ratio analysis can adequately evaluate its operating financial performance that will help

in assessing its potential of future growth and development. In addition to this, investors can

adequately analyze the market value of firm securities with the use of earning analysis. Earning

analysis can be carried out by evaluation of the earning per share of a firm that given a depiction

of its market worth by measuring its operating earnings. As such, Arden Fund investors can

analyze the EPS of Rio Tinto before making the investment decision.

5.0: Analysis of financial statements of Rio Tinto

5.1: Ratio Analysis

Ratio analysis is regarded as the most important accounting tool used to perform the

financial analysis. All the required information that is needed to be processed is primarily

gathered from the financial statements of the selected company. Ratio is referred to the

mathematical relationship two main quantities from the financial statement of the company.

Through use of ratios, investors can have information about the five major aspects of the

financial performance mainly return on investment, liquidity, efficiency, profitability, and capital

structure or financial leverage.

Importance of Ratio Analysis

Ratios are one of the most important tools that were used in finance and that almost every

business does and by calculating these ratios, it is easy to express an opinion about the

performance of particular enterprise.

We can use ratio analysis to tell us whether the business is –

• Profitable

• Has enough money to pay its debts

• Could be paying its employees higher wages, remuneration or so on

• Is able to pay its taxes

• Is using its assets efficiently or not

• Has a sufficient amount of fund to meet their daily obligations (Brigham and Michael,

2013)

Types of Ratios

• Profitability Analysis

• Liquidity Analysis

• Efficiency Analysis

• Financial Leverage Analysis

financial ratio analysis can adequately evaluate its operating financial performance that will help

in assessing its potential of future growth and development. In addition to this, investors can

adequately analyze the market value of firm securities with the use of earning analysis. Earning

analysis can be carried out by evaluation of the earning per share of a firm that given a depiction

of its market worth by measuring its operating earnings. As such, Arden Fund investors can

analyze the EPS of Rio Tinto before making the investment decision.

5.0: Analysis of financial statements of Rio Tinto

5.1: Ratio Analysis

Ratio analysis is regarded as the most important accounting tool used to perform the

financial analysis. All the required information that is needed to be processed is primarily

gathered from the financial statements of the selected company. Ratio is referred to the

mathematical relationship two main quantities from the financial statement of the company.

Through use of ratios, investors can have information about the five major aspects of the

financial performance mainly return on investment, liquidity, efficiency, profitability, and capital

structure or financial leverage.

Importance of Ratio Analysis

Ratios are one of the most important tools that were used in finance and that almost every

business does and by calculating these ratios, it is easy to express an opinion about the

performance of particular enterprise.

We can use ratio analysis to tell us whether the business is –

• Profitable

• Has enough money to pay its debts

• Could be paying its employees higher wages, remuneration or so on

• Is able to pay its taxes

• Is using its assets efficiently or not

• Has a sufficient amount of fund to meet their daily obligations (Brigham and Michael,

2013)

Types of Ratios

• Profitability Analysis

• Liquidity Analysis

• Efficiency Analysis

• Financial Leverage Analysis

6

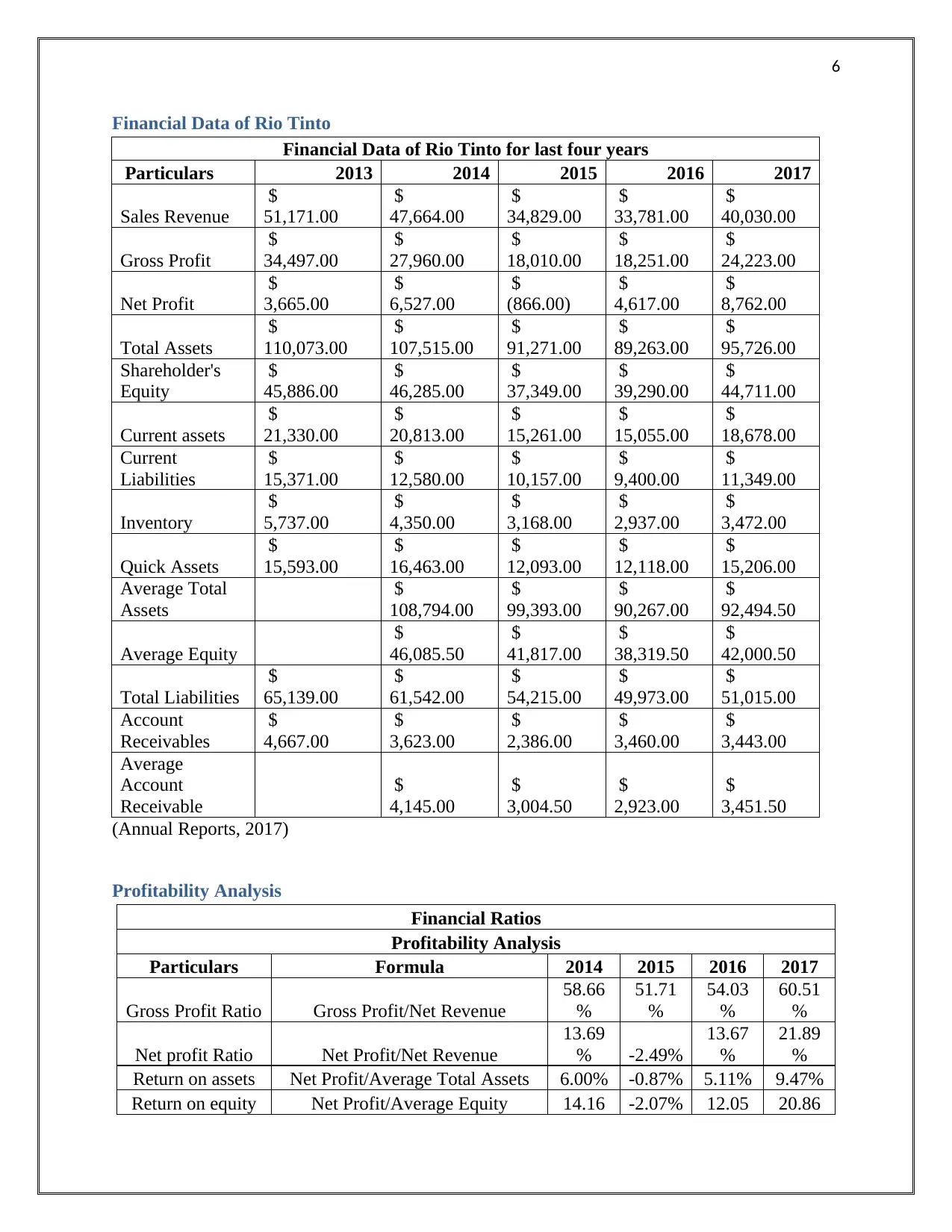

Financial Data of Rio Tinto

Financial Data of Rio Tinto for last four years

Particulars 2013 2014 2015 2016 2017

Sales Revenue

$

51,171.00

$

47,664.00

$

34,829.00

$

33,781.00

$

40,030.00

Gross Profit

$

34,497.00

$

27,960.00

$

18,010.00

$

18,251.00

$

24,223.00

Net Profit

$

3,665.00

$

6,527.00

$

(866.00)

$

4,617.00

$

8,762.00

Total Assets

$

110,073.00

$

107,515.00

$

91,271.00

$

89,263.00

$

95,726.00

Shareholder's

Equity

$

45,886.00

$

46,285.00

$

37,349.00

$

39,290.00

$

44,711.00

Current assets

$

21,330.00

$

20,813.00

$

15,261.00

$

15,055.00

$

18,678.00

Current

Liabilities

$

15,371.00

$

12,580.00

$

10,157.00

$

9,400.00

$

11,349.00

Inventory

$

5,737.00

$

4,350.00

$

3,168.00

$

2,937.00

$

3,472.00

Quick Assets

$

15,593.00

$

16,463.00

$

12,093.00

$

12,118.00

$

15,206.00

Average Total

Assets

$

108,794.00

$

99,393.00

$

90,267.00

$

92,494.50

Average Equity

$

46,085.50

$

41,817.00

$

38,319.50

$

42,000.50

Total Liabilities

$

65,139.00

$

61,542.00

$

54,215.00

$

49,973.00

$

51,015.00

Account

Receivables

$

4,667.00

$

3,623.00

$

2,386.00

$

3,460.00

$

3,443.00

Average

Account

Receivable

$

4,145.00

$

3,004.50

$

2,923.00

$

3,451.50

(Annual Reports, 2017)

Profitability Analysis

Financial Ratios

Profitability Analysis

Particulars Formula 2014 2015 2016 2017

Gross Profit Ratio Gross Profit/Net Revenue

58.66

%

51.71

%

54.03

%

60.51

%

Net profit Ratio Net Profit/Net Revenue

13.69

% -2.49%

13.67

%

21.89

%

Return on assets Net Profit/Average Total Assets 6.00% -0.87% 5.11% 9.47%

Return on equity Net Profit/Average Equity 14.16 -2.07% 12.05 20.86

Financial Data of Rio Tinto

Financial Data of Rio Tinto for last four years

Particulars 2013 2014 2015 2016 2017

Sales Revenue

$

51,171.00

$

47,664.00

$

34,829.00

$

33,781.00

$

40,030.00

Gross Profit

$

34,497.00

$

27,960.00

$

18,010.00

$

18,251.00

$

24,223.00

Net Profit

$

3,665.00

$

6,527.00

$

(866.00)

$

4,617.00

$

8,762.00

Total Assets

$

110,073.00

$

107,515.00

$

91,271.00

$

89,263.00

$

95,726.00

Shareholder's

Equity

$

45,886.00

$

46,285.00

$

37,349.00

$

39,290.00

$

44,711.00

Current assets

$

21,330.00

$

20,813.00

$

15,261.00

$

15,055.00

$

18,678.00

Current

Liabilities

$

15,371.00

$

12,580.00

$

10,157.00

$

9,400.00

$

11,349.00

Inventory

$

5,737.00

$

4,350.00

$

3,168.00

$

2,937.00

$

3,472.00

Quick Assets

$

15,593.00

$

16,463.00

$

12,093.00

$

12,118.00

$

15,206.00

Average Total

Assets

$

108,794.00

$

99,393.00

$

90,267.00

$

92,494.50

Average Equity

$

46,085.50

$

41,817.00

$

38,319.50

$

42,000.50

Total Liabilities

$

65,139.00

$

61,542.00

$

54,215.00

$

49,973.00

$

51,015.00

Account

Receivables

$

4,667.00

$

3,623.00

$

2,386.00

$

3,460.00

$

3,443.00

Average

Account

Receivable

$

4,145.00

$

3,004.50

$

2,923.00

$

3,451.50

(Annual Reports, 2017)

Profitability Analysis

Financial Ratios

Profitability Analysis

Particulars Formula 2014 2015 2016 2017

Gross Profit Ratio Gross Profit/Net Revenue

58.66

%

51.71

%

54.03

%

60.51

%

Net profit Ratio Net Profit/Net Revenue

13.69

% -2.49%

13.67

%

21.89

%

Return on assets Net Profit/Average Total Assets 6.00% -0.87% 5.11% 9.47%

Return on equity Net Profit/Average Equity 14.16 -2.07% 12.05 20.86

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7

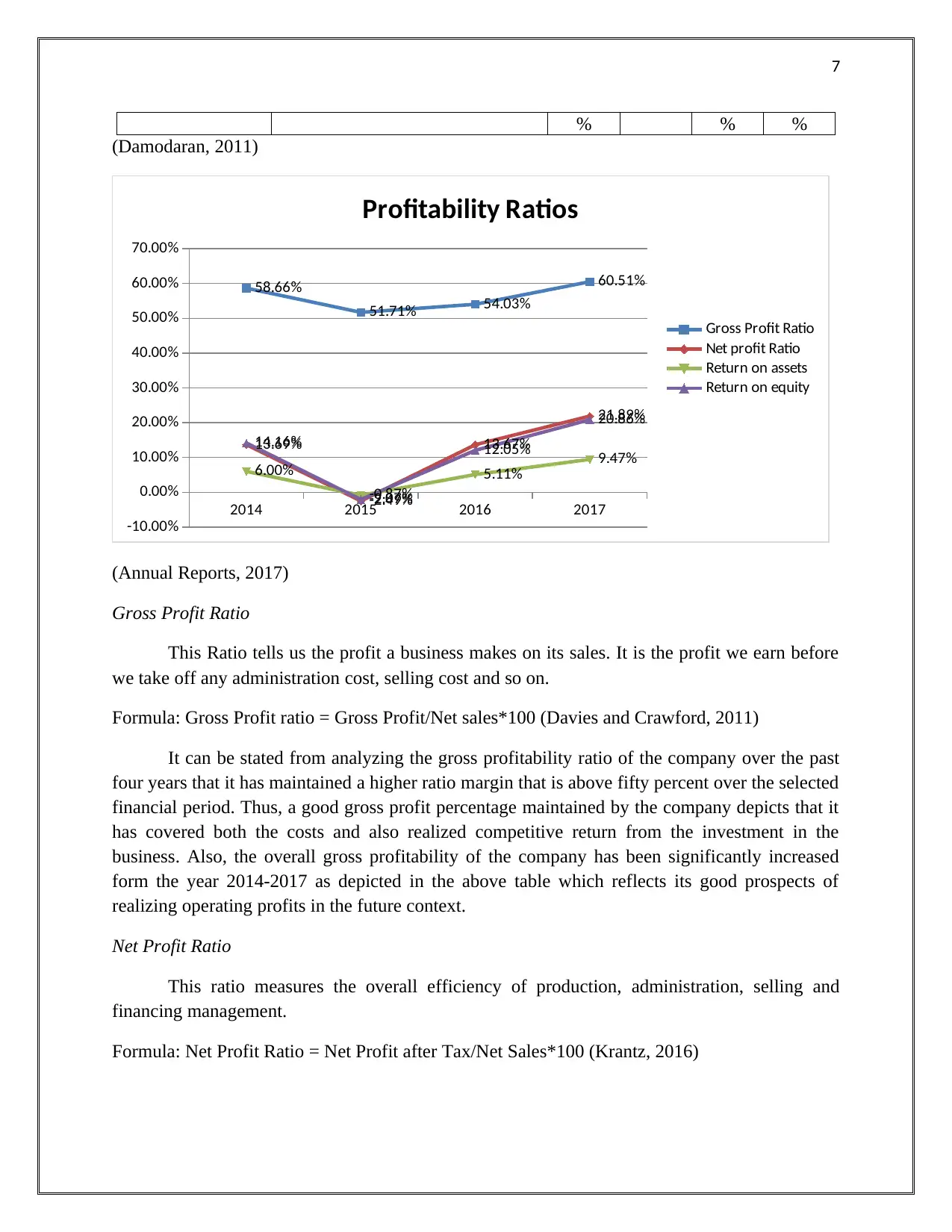

% % %

(Damodaran, 2011)

2014 2015 2016 2017

-10.00%

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

70.00%

58.66%

51.71% 54.03%

60.51%

13.69%

-2.49%

13.67%

21.89%

6.00%

-0.87%

5.11% 9.47%

14.16%

-2.07%

12.05%

20.86%

Profitability Ratios

Gross Profit Ratio

Net profit Ratio

Return on assets

Return on equity

(Annual Reports, 2017)

Gross Profit Ratio

This Ratio tells us the profit a business makes on its sales. It is the profit we earn before

we take off any administration cost, selling cost and so on.

Formula: Gross Profit ratio = Gross Profit/Net sales*100 (Davies and Crawford, 2011)

It can be stated from analyzing the gross profitability ratio of the company over the past

four years that it has maintained a higher ratio margin that is above fifty percent over the selected

financial period. Thus, a good gross profit percentage maintained by the company depicts that it

has covered both the costs and also realized competitive return from the investment in the

business. Also, the overall gross profitability of the company has been significantly increased

form the year 2014-2017 as depicted in the above table which reflects its good prospects of

realizing operating profits in the future context.

Net Profit Ratio

This ratio measures the overall efficiency of production, administration, selling and

financing management.

Formula: Net Profit Ratio = Net Profit after Tax/Net Sales*100 (Krantz, 2016)

% % %

(Damodaran, 2011)

2014 2015 2016 2017

-10.00%

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

70.00%

58.66%

51.71% 54.03%

60.51%

13.69%

-2.49%

13.67%

21.89%

6.00%

-0.87%

5.11% 9.47%

14.16%

-2.07%

12.05%

20.86%

Profitability Ratios

Gross Profit Ratio

Net profit Ratio

Return on assets

Return on equity

(Annual Reports, 2017)

Gross Profit Ratio

This Ratio tells us the profit a business makes on its sales. It is the profit we earn before

we take off any administration cost, selling cost and so on.

Formula: Gross Profit ratio = Gross Profit/Net sales*100 (Davies and Crawford, 2011)

It can be stated from analyzing the gross profitability ratio of the company over the past

four years that it has maintained a higher ratio margin that is above fifty percent over the selected

financial period. Thus, a good gross profit percentage maintained by the company depicts that it

has covered both the costs and also realized competitive return from the investment in the

business. Also, the overall gross profitability of the company has been significantly increased

form the year 2014-2017 as depicted in the above table which reflects its good prospects of

realizing operating profits in the future context.

Net Profit Ratio

This ratio measures the overall efficiency of production, administration, selling and

financing management.

Formula: Net Profit Ratio = Net Profit after Tax/Net Sales*100 (Krantz, 2016)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8

The after-tax profits realized to net sales has depicted an increasing trend from the year

2014-2017 which depicts that its efficiency to meet the cost of production and financing has been

improved reflecting its good financial position. However, it has been reflected from the table that

the ratio for the year 2015 reflects a negative trend depicting that it has suffered loss in the

respective financial year. The ratio has then reflected an increasing trend till the year 2017

reflecting that it has improved its ability to meet the operating expenses which consequently lead

to increase in its sales revenue.

Return on Assets (ROA)

This ratio actually measures the profitability of the investments in the firm.

Formula: Return on Assets = Net Profit after Tax/Total Assets*100 (Madura, 2014)

The return on assets of the company has depicted an increasing trend from the year 2014-

2017 reflecting the improvement in its ability to gain returns on the investment. The company

ROA has been negative in the year 2015 indicating that it has incurred losses on its investment

but has then improved its ability to realize returns on its investments as the ratio has depicted an

increasing trend from the year 2015-2017.

Return on Equity (ROE)

It measures the profitability of a business in relation to the equity invested by its

shareholders.

Formula: ROE=Net Income/Shareholder equity (Moles and Kidwekk, 2011)

The ROE has reflected an increasing trend from the year 2014-2017 as depicted in the

above table. The ratio has depicted a negative trend in the year 2015 which means that it has

earned loss on its equity investment. However, the company has then improved its ROE but it

has depicted a financial risk present within the company for the shareholders as its ROE is below

10% as analyzed for the last four years.

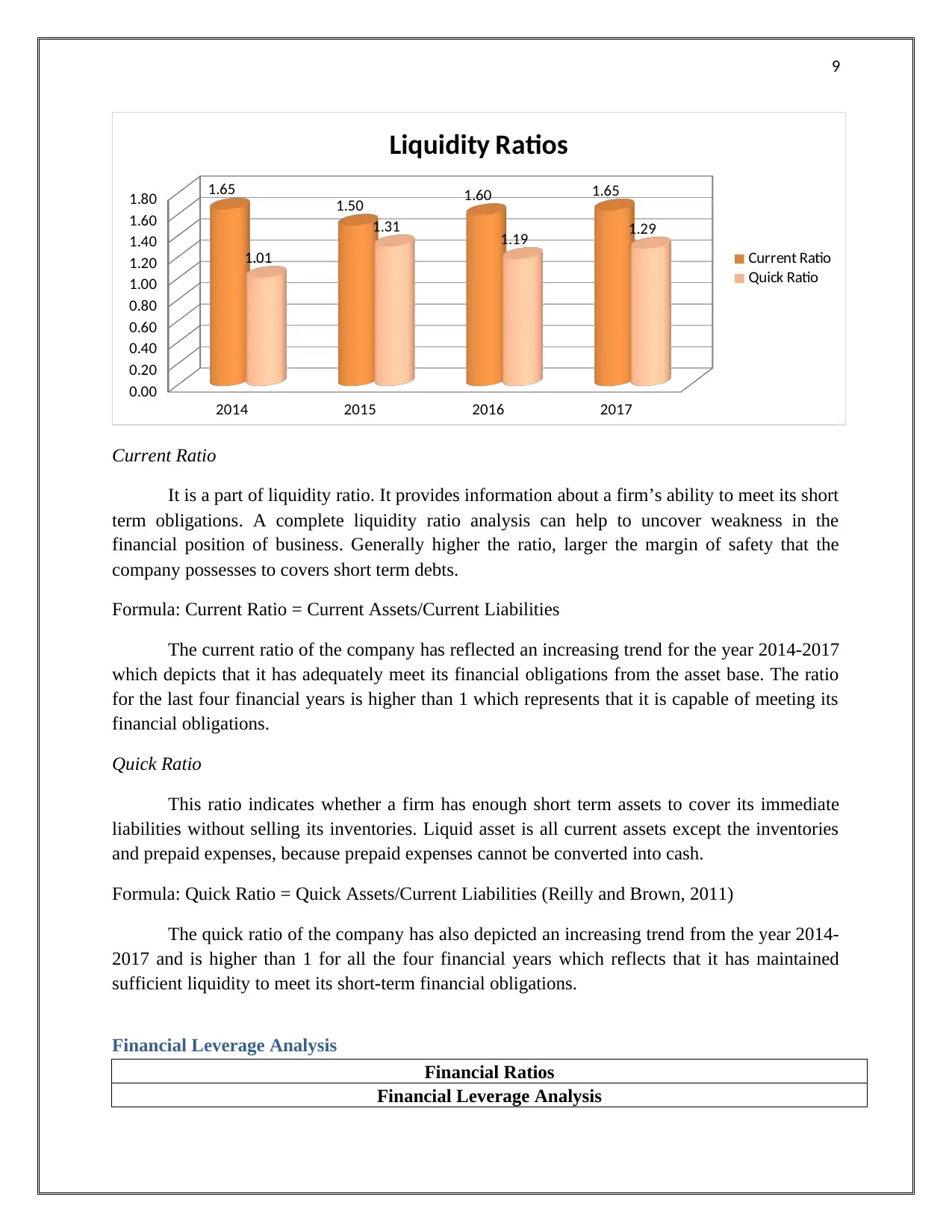

Liquidity Analysis

Financial Ratios

Liquidity Analysis

Particulars Formula 2014 2015 2016 2017

Current Ratio Current Assets/Current Liabilities 1.65 1.50 1.60 1.65

Quick Ratio Quick Assets/Current Liabilities 1.01 1.31 1.19 1.29

(Annual Reports, 2017)

The after-tax profits realized to net sales has depicted an increasing trend from the year

2014-2017 which depicts that its efficiency to meet the cost of production and financing has been

improved reflecting its good financial position. However, it has been reflected from the table that

the ratio for the year 2015 reflects a negative trend depicting that it has suffered loss in the

respective financial year. The ratio has then reflected an increasing trend till the year 2017

reflecting that it has improved its ability to meet the operating expenses which consequently lead

to increase in its sales revenue.

Return on Assets (ROA)

This ratio actually measures the profitability of the investments in the firm.

Formula: Return on Assets = Net Profit after Tax/Total Assets*100 (Madura, 2014)

The return on assets of the company has depicted an increasing trend from the year 2014-

2017 reflecting the improvement in its ability to gain returns on the investment. The company

ROA has been negative in the year 2015 indicating that it has incurred losses on its investment

but has then improved its ability to realize returns on its investments as the ratio has depicted an

increasing trend from the year 2015-2017.

Return on Equity (ROE)

It measures the profitability of a business in relation to the equity invested by its

shareholders.

Formula: ROE=Net Income/Shareholder equity (Moles and Kidwekk, 2011)

The ROE has reflected an increasing trend from the year 2014-2017 as depicted in the

above table. The ratio has depicted a negative trend in the year 2015 which means that it has

earned loss on its equity investment. However, the company has then improved its ROE but it

has depicted a financial risk present within the company for the shareholders as its ROE is below

10% as analyzed for the last four years.

Liquidity Analysis

Financial Ratios

Liquidity Analysis

Particulars Formula 2014 2015 2016 2017

Current Ratio Current Assets/Current Liabilities 1.65 1.50 1.60 1.65

Quick Ratio Quick Assets/Current Liabilities 1.01 1.31 1.19 1.29

(Annual Reports, 2017)

9

2014 2015 2016 2017

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

1.60

1.80 1.65

1.50 1.60 1.65

1.01

1.31 1.19 1.29

Liquidity Ratios

Current Ratio

Quick Ratio

Current Ratio

It is a part of liquidity ratio. It provides information about a firm’s ability to meet its short

term obligations. A complete liquidity ratio analysis can help to uncover weakness in the

financial position of business. Generally higher the ratio, larger the margin of safety that the

company possesses to covers short term debts.

Formula: Current Ratio = Current Assets/Current Liabilities

The current ratio of the company has reflected an increasing trend for the year 2014-2017

which depicts that it has adequately meet its financial obligations from the asset base. The ratio

for the last four financial years is higher than 1 which represents that it is capable of meeting its

financial obligations.

Quick Ratio

This ratio indicates whether a firm has enough short term assets to cover its immediate

liabilities without selling its inventories. Liquid asset is all current assets except the inventories

and prepaid expenses, because prepaid expenses cannot be converted into cash.

Formula: Quick Ratio = Quick Assets/Current Liabilities (Reilly and Brown, 2011)

The quick ratio of the company has also depicted an increasing trend from the year 2014-

2017 and is higher than 1 for all the four financial years which reflects that it has maintained

sufficient liquidity to meet its short-term financial obligations.

Financial Leverage Analysis

Financial Ratios

Financial Leverage Analysis

2014 2015 2016 2017

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

1.60

1.80 1.65

1.50 1.60 1.65

1.01

1.31 1.19 1.29

Liquidity Ratios

Current Ratio

Quick Ratio

Current Ratio

It is a part of liquidity ratio. It provides information about a firm’s ability to meet its short

term obligations. A complete liquidity ratio analysis can help to uncover weakness in the

financial position of business. Generally higher the ratio, larger the margin of safety that the

company possesses to covers short term debts.

Formula: Current Ratio = Current Assets/Current Liabilities

The current ratio of the company has reflected an increasing trend for the year 2014-2017

which depicts that it has adequately meet its financial obligations from the asset base. The ratio

for the last four financial years is higher than 1 which represents that it is capable of meeting its

financial obligations.

Quick Ratio

This ratio indicates whether a firm has enough short term assets to cover its immediate

liabilities without selling its inventories. Liquid asset is all current assets except the inventories

and prepaid expenses, because prepaid expenses cannot be converted into cash.

Formula: Quick Ratio = Quick Assets/Current Liabilities (Reilly and Brown, 2011)

The quick ratio of the company has also depicted an increasing trend from the year 2014-

2017 and is higher than 1 for all the four financial years which reflects that it has maintained

sufficient liquidity to meet its short-term financial obligations.

Financial Leverage Analysis

Financial Ratios

Financial Leverage Analysis

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10

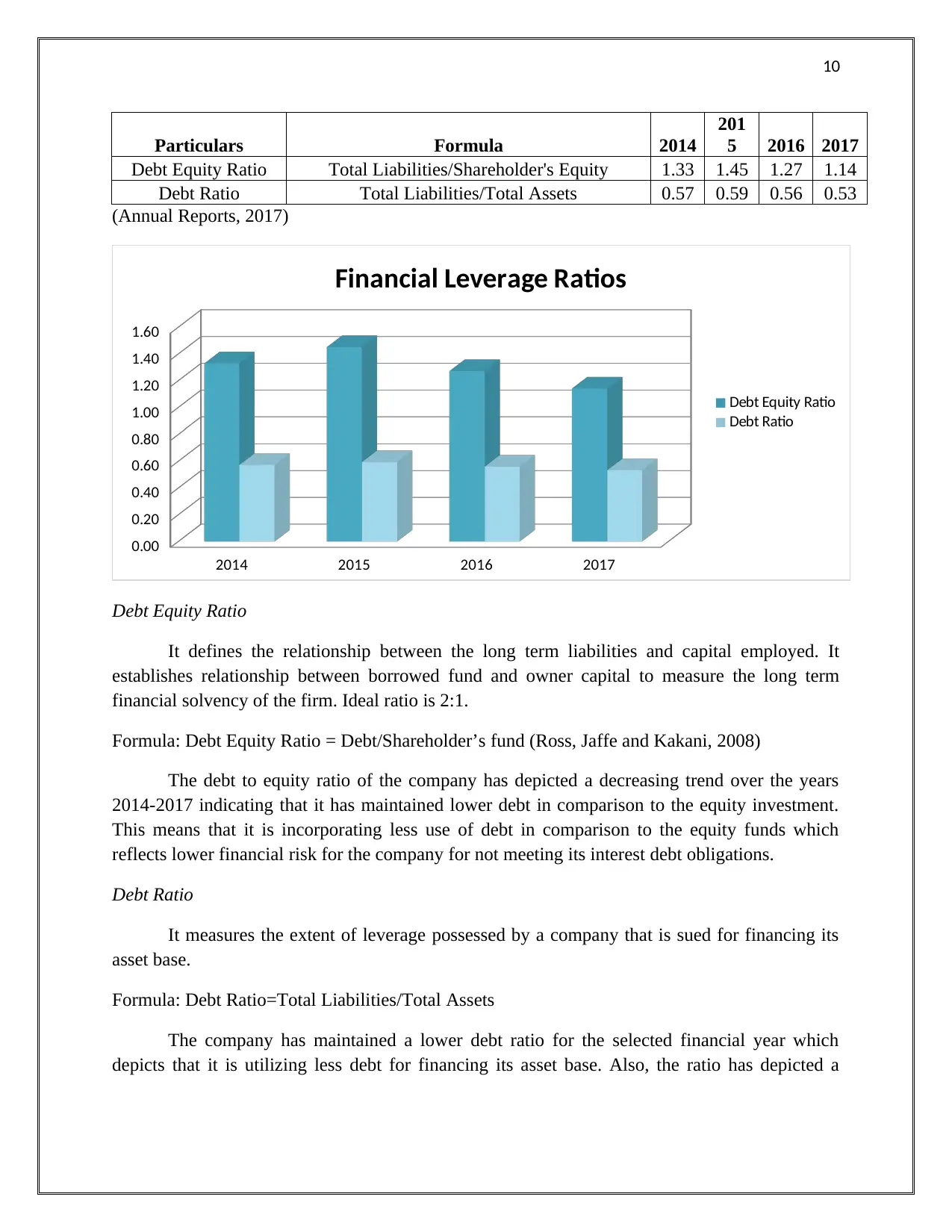

Particulars Formula 2014

201

5 2016 2017

Debt Equity Ratio Total Liabilities/Shareholder's Equity 1.33 1.45 1.27 1.14

Debt Ratio Total Liabilities/Total Assets 0.57 0.59 0.56 0.53

(Annual Reports, 2017)

2014 2015 2016 2017

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

1.60

Financial Leverage Ratios

Debt Equity Ratio

Debt Ratio

Debt Equity Ratio

It defines the relationship between the long term liabilities and capital employed. It

establishes relationship between borrowed fund and owner capital to measure the long term

financial solvency of the firm. Ideal ratio is 2:1.

Formula: Debt Equity Ratio = Debt/Shareholder’s fund (Ross, Jaffe and Kakani, 2008)

The debt to equity ratio of the company has depicted a decreasing trend over the years

2014-2017 indicating that it has maintained lower debt in comparison to the equity investment.

This means that it is incorporating less use of debt in comparison to the equity funds which

reflects lower financial risk for the company for not meeting its interest debt obligations.

Debt Ratio

It measures the extent of leverage possessed by a company that is sued for financing its

asset base.

Formula: Debt Ratio=Total Liabilities/Total Assets

The company has maintained a lower debt ratio for the selected financial year which

depicts that it is utilizing less debt for financing its asset base. Also, the ratio has depicted a

Particulars Formula 2014

201

5 2016 2017

Debt Equity Ratio Total Liabilities/Shareholder's Equity 1.33 1.45 1.27 1.14

Debt Ratio Total Liabilities/Total Assets 0.57 0.59 0.56 0.53

(Annual Reports, 2017)

2014 2015 2016 2017

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

1.60

Financial Leverage Ratios

Debt Equity Ratio

Debt Ratio

Debt Equity Ratio

It defines the relationship between the long term liabilities and capital employed. It

establishes relationship between borrowed fund and owner capital to measure the long term

financial solvency of the firm. Ideal ratio is 2:1.

Formula: Debt Equity Ratio = Debt/Shareholder’s fund (Ross, Jaffe and Kakani, 2008)

The debt to equity ratio of the company has depicted a decreasing trend over the years

2014-2017 indicating that it has maintained lower debt in comparison to the equity investment.

This means that it is incorporating less use of debt in comparison to the equity funds which

reflects lower financial risk for the company for not meeting its interest debt obligations.

Debt Ratio

It measures the extent of leverage possessed by a company that is sued for financing its

asset base.

Formula: Debt Ratio=Total Liabilities/Total Assets

The company has maintained a lower debt ratio for the selected financial year which

depicts that it is utilizing less debt for financing its asset base. Also, the ratio has depicted a

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

11

decreasing trend which means that there is less financial risk for it to default but it also

represents a doubt regarding the future financial growth prospects of the company.

Efficiency Analysis

Financial Ratios

Efficiency Analysis

Particulars Formula 2014 2015 2016 2017

Accounts

Receivables in Days

Average Account

Receivable*365/Revenue 31.74 31.49 31.58 31.47

Asset Turnover in

days Average total Assets*365/Revenue 833.12 1041.62 975.33 843.38

(Annual Reports, 2017)

Accounts Receivables in Days

The average number of days a company takes to collect payments on goods sold.

Formula: Accounts Receivables in days= 365/ (Average Accounts Receivable/Total value of

credit sales) (Weston and Brigham, 2015)

It can be stated on the basis of the trend of the ratio for the selected financial period that it

has maintained an effective control on the number of days required for collection of its

receivables from the customers. There was no major change in number of days required to

collect the account receivables during the last four years. Rio Tinto takes 1 month to collect all

its receivables that were due on starting of the month. It reflects high efficiency of management

at Rio Tinto. So it can be said that company manages its accounts receivables successfully and

helps to maintain the cash cycle in proper manner.

Asset turnover in day’s ratio

This ratio reflects the use of assets to earn the revenue by the management of the

company. The purpose of this ratio is to evaluate efficiency of the management to make optimum

utilization of resources to earn the maximum sales. This ratio shows times the revenue earned on

total assets for the selected period. This ratio takes average assets put to use within the process to

earn the sales revenue.

Formula: Asset turnover ratio in days: 365/ (Average Total assets/ Net Revenue)

Rio Tinto is the mining industry that requires heavy investment in machinery and many

other assets that makes value of total assets much more than the value of revenue earned by

company. Asset turnover ratio in days has increasing trend during the last four years that shows

Rio Tinto consume more assets to earn the same amount of sales in current as compared to

previous year. It shows management at Rio Tinto does not manage assets in proper manner.

decreasing trend which means that there is less financial risk for it to default but it also

represents a doubt regarding the future financial growth prospects of the company.

Efficiency Analysis

Financial Ratios

Efficiency Analysis

Particulars Formula 2014 2015 2016 2017

Accounts

Receivables in Days

Average Account

Receivable*365/Revenue 31.74 31.49 31.58 31.47

Asset Turnover in

days Average total Assets*365/Revenue 833.12 1041.62 975.33 843.38

(Annual Reports, 2017)

Accounts Receivables in Days

The average number of days a company takes to collect payments on goods sold.

Formula: Accounts Receivables in days= 365/ (Average Accounts Receivable/Total value of

credit sales) (Weston and Brigham, 2015)

It can be stated on the basis of the trend of the ratio for the selected financial period that it

has maintained an effective control on the number of days required for collection of its

receivables from the customers. There was no major change in number of days required to

collect the account receivables during the last four years. Rio Tinto takes 1 month to collect all

its receivables that were due on starting of the month. It reflects high efficiency of management

at Rio Tinto. So it can be said that company manages its accounts receivables successfully and

helps to maintain the cash cycle in proper manner.

Asset turnover in day’s ratio

This ratio reflects the use of assets to earn the revenue by the management of the

company. The purpose of this ratio is to evaluate efficiency of the management to make optimum

utilization of resources to earn the maximum sales. This ratio shows times the revenue earned on

total assets for the selected period. This ratio takes average assets put to use within the process to

earn the sales revenue.

Formula: Asset turnover ratio in days: 365/ (Average Total assets/ Net Revenue)

Rio Tinto is the mining industry that requires heavy investment in machinery and many

other assets that makes value of total assets much more than the value of revenue earned by

company. Asset turnover ratio in days has increasing trend during the last four years that shows

Rio Tinto consume more assets to earn the same amount of sales in current as compared to

previous year. It shows management at Rio Tinto does not manage assets in proper manner.

12

Overall considering the type of industry in which Rio Tinto belongs it can be said that

management needs to make sure that they can put more efforts in utilization of assets and earn

maximum amount of sales.

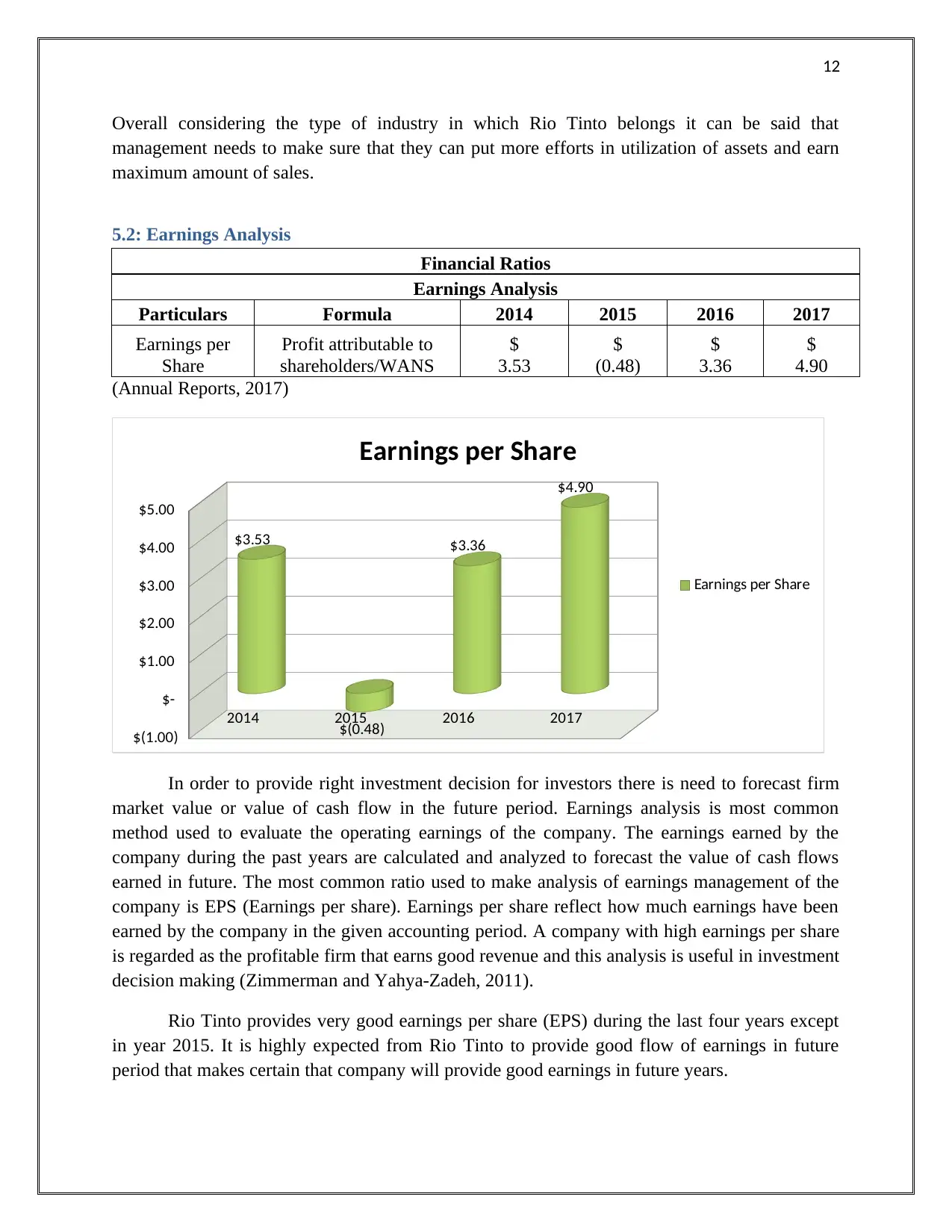

5.2: Earnings Analysis

Financial Ratios

Earnings Analysis

Particulars Formula 2014 2015 2016 2017

Earnings per

Share

Profit attributable to

shareholders/WANS

$

3.53

$

(0.48)

$

3.36

$

4.90

(Annual Reports, 2017)

2014 2015 2016 2017

$(1.00)

$-

$1.00

$2.00

$3.00

$4.00

$5.00

$3.53

$(0.48)

$3.36

$4.90

Earnings per Share

Earnings per Share

In order to provide right investment decision for investors there is need to forecast firm

market value or value of cash flow in the future period. Earnings analysis is most common

method used to evaluate the operating earnings of the company. The earnings earned by the

company during the past years are calculated and analyzed to forecast the value of cash flows

earned in future. The most common ratio used to make analysis of earnings management of the

company is EPS (Earnings per share). Earnings per share reflect how much earnings have been

earned by the company in the given accounting period. A company with high earnings per share

is regarded as the profitable firm that earns good revenue and this analysis is useful in investment

decision making (Zimmerman and Yahya-Zadeh, 2011).

Rio Tinto provides very good earnings per share (EPS) during the last four years except

in year 2015. It is highly expected from Rio Tinto to provide good flow of earnings in future

period that makes certain that company will provide good earnings in future years.

Overall considering the type of industry in which Rio Tinto belongs it can be said that

management needs to make sure that they can put more efforts in utilization of assets and earn

maximum amount of sales.

5.2: Earnings Analysis

Financial Ratios

Earnings Analysis

Particulars Formula 2014 2015 2016 2017

Earnings per

Share

Profit attributable to

shareholders/WANS

$

3.53

$

(0.48)

$

3.36

$

4.90

(Annual Reports, 2017)

2014 2015 2016 2017

$(1.00)

$-

$1.00

$2.00

$3.00

$4.00

$5.00

$3.53

$(0.48)

$3.36

$4.90

Earnings per Share

Earnings per Share

In order to provide right investment decision for investors there is need to forecast firm

market value or value of cash flow in the future period. Earnings analysis is most common

method used to evaluate the operating earnings of the company. The earnings earned by the

company during the past years are calculated and analyzed to forecast the value of cash flows

earned in future. The most common ratio used to make analysis of earnings management of the

company is EPS (Earnings per share). Earnings per share reflect how much earnings have been

earned by the company in the given accounting period. A company with high earnings per share

is regarded as the profitable firm that earns good revenue and this analysis is useful in investment

decision making (Zimmerman and Yahya-Zadeh, 2011).

Rio Tinto provides very good earnings per share (EPS) during the last four years except

in year 2015. It is highly expected from Rio Tinto to provide good flow of earnings in future

period that makes certain that company will provide good earnings in future years.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.