HI5002 Finance: Performance Analysis of ANZ and Commonwealth Bank

VerifiedAdded on 2020/11/23

|11

|2104

|67

Report

AI Summary

This report provides a detailed financial analysis of ANZ and Commonwealth Bank, examining their performance from 2016 to 2018. It begins with an executive summary and table of contents, followed by a calculation and analysis of selected performance ratios, including liquidity, profitability, efficiency, and solvency ratios. The report compares the banks' current and quick ratios, operating net profit margin, return on assets, fixed asset turnover, asset turnover, debt-equity ratio, and debt ratio. It also includes a cash management analysis, sensitivity analysis, and a discussion of systemic and unsystemic risk. The report calculates the WACC for both banks and analyzes their dividend payout ratios and dividend policies. Based on the analysis, recommendations are provided for stakeholders and investors, concluding that investment in ANZ Bank is more favorable. The report references annual reports and journals to support its findings.

Financial for business-

ANZ V

COMMENWEALTH

Bank

ANZ V

COMMENWEALTH

Bank

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

EXECUTIVE SUMMARY

The report covers the brief description about the operations of ANZ and commonwealth

bank and trend analysis have been identify with the help of financial ratios. In respective report

sensitivity analysis is performed to determine marketable securities and systematic and

unsystematic risk are discussed for the selected banks. The report also summaries the calculation

of dividend payout ratio and valuable recommendation are given for stakeholder.

The report covers the brief description about the operations of ANZ and commonwealth

bank and trend analysis have been identify with the help of financial ratios. In respective report

sensitivity analysis is performed to determine marketable securities and systematic and

unsystematic risk are discussed for the selected banks. The report also summaries the calculation

of dividend payout ratio and valuable recommendation are given for stakeholder.

Table of Contents

EXECUTIVE SUMMARY.............................................................................................................2

Table of Contents.............................................................................................................................3

TASK 2............................................................................................................................................1

2.2. Calculation and analysis of selected performance ratios......................................................1

2.3 Cash management analysis....................................................................................................4

2.4 Sensitivity analysis................................................................................................................5

2.5 Systemic risk and un-systemic risk........................................................................................6

2.6 Dividend payout ratio and dividend policy...........................................................................6

REFERENCES................................................................................................................................8

EXECUTIVE SUMMARY.............................................................................................................2

Table of Contents.............................................................................................................................3

TASK 2............................................................................................................................................1

2.2. Calculation and analysis of selected performance ratios......................................................1

2.3 Cash management analysis....................................................................................................4

2.4 Sensitivity analysis................................................................................................................5

2.5 Systemic risk and un-systemic risk........................................................................................6

2.6 Dividend payout ratio and dividend policy...........................................................................6

REFERENCES................................................................................................................................8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

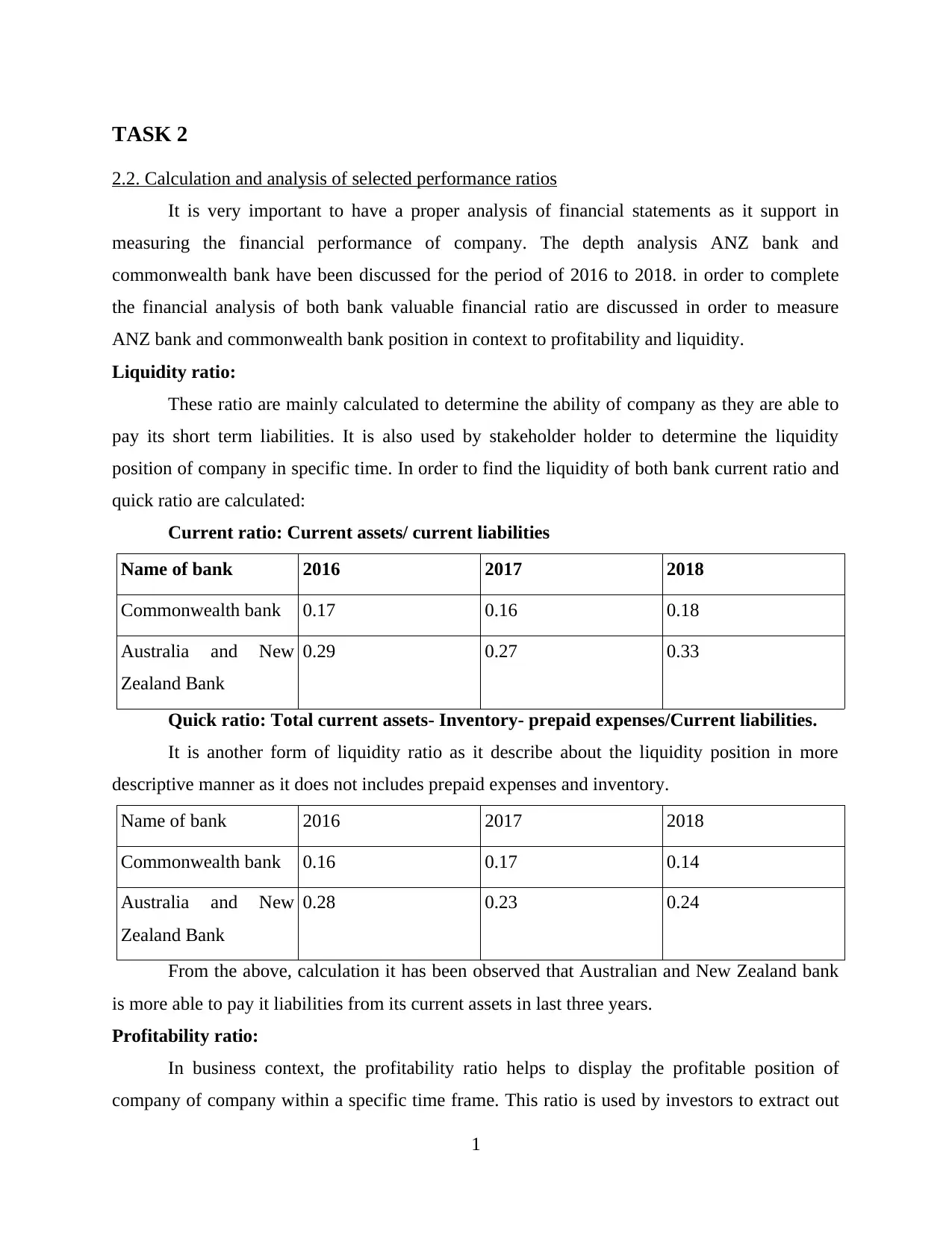

TASK 2

2.2. Calculation and analysis of selected performance ratios

It is very important to have a proper analysis of financial statements as it support in

measuring the financial performance of company. The depth analysis ANZ bank and

commonwealth bank have been discussed for the period of 2016 to 2018. in order to complete

the financial analysis of both bank valuable financial ratio are discussed in order to measure

ANZ bank and commonwealth bank position in context to profitability and liquidity.

Liquidity ratio:

These ratio are mainly calculated to determine the ability of company as they are able to

pay its short term liabilities. It is also used by stakeholder holder to determine the liquidity

position of company in specific time. In order to find the liquidity of both bank current ratio and

quick ratio are calculated:

Current ratio: Current assets/ current liabilities

Name of bank 2016 2017 2018

Commonwealth bank 0.17 0.16 0.18

Australia and New

Zealand Bank

0.29 0.27 0.33

Quick ratio: Total current assets- Inventory- prepaid expenses/Current liabilities.

It is another form of liquidity ratio as it describe about the liquidity position in more

descriptive manner as it does not includes prepaid expenses and inventory.

Name of bank 2016 2017 2018

Commonwealth bank 0.16 0.17 0.14

Australia and New

Zealand Bank

0.28 0.23 0.24

From the above, calculation it has been observed that Australian and New Zealand bank

is more able to pay it liabilities from its current assets in last three years.

Profitability ratio:

In business context, the profitability ratio helps to display the profitable position of

company of company within a specific time frame. This ratio is used by investors to extract out

1

2.2. Calculation and analysis of selected performance ratios

It is very important to have a proper analysis of financial statements as it support in

measuring the financial performance of company. The depth analysis ANZ bank and

commonwealth bank have been discussed for the period of 2016 to 2018. in order to complete

the financial analysis of both bank valuable financial ratio are discussed in order to measure

ANZ bank and commonwealth bank position in context to profitability and liquidity.

Liquidity ratio:

These ratio are mainly calculated to determine the ability of company as they are able to

pay its short term liabilities. It is also used by stakeholder holder to determine the liquidity

position of company in specific time. In order to find the liquidity of both bank current ratio and

quick ratio are calculated:

Current ratio: Current assets/ current liabilities

Name of bank 2016 2017 2018

Commonwealth bank 0.17 0.16 0.18

Australia and New

Zealand Bank

0.29 0.27 0.33

Quick ratio: Total current assets- Inventory- prepaid expenses/Current liabilities.

It is another form of liquidity ratio as it describe about the liquidity position in more

descriptive manner as it does not includes prepaid expenses and inventory.

Name of bank 2016 2017 2018

Commonwealth bank 0.16 0.17 0.14

Australia and New

Zealand Bank

0.28 0.23 0.24

From the above, calculation it has been observed that Australian and New Zealand bank

is more able to pay it liabilities from its current assets in last three years.

Profitability ratio:

In business context, the profitability ratio helps to display the profitable position of

company of company within a specific time frame. This ratio is used by investors to extract out

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

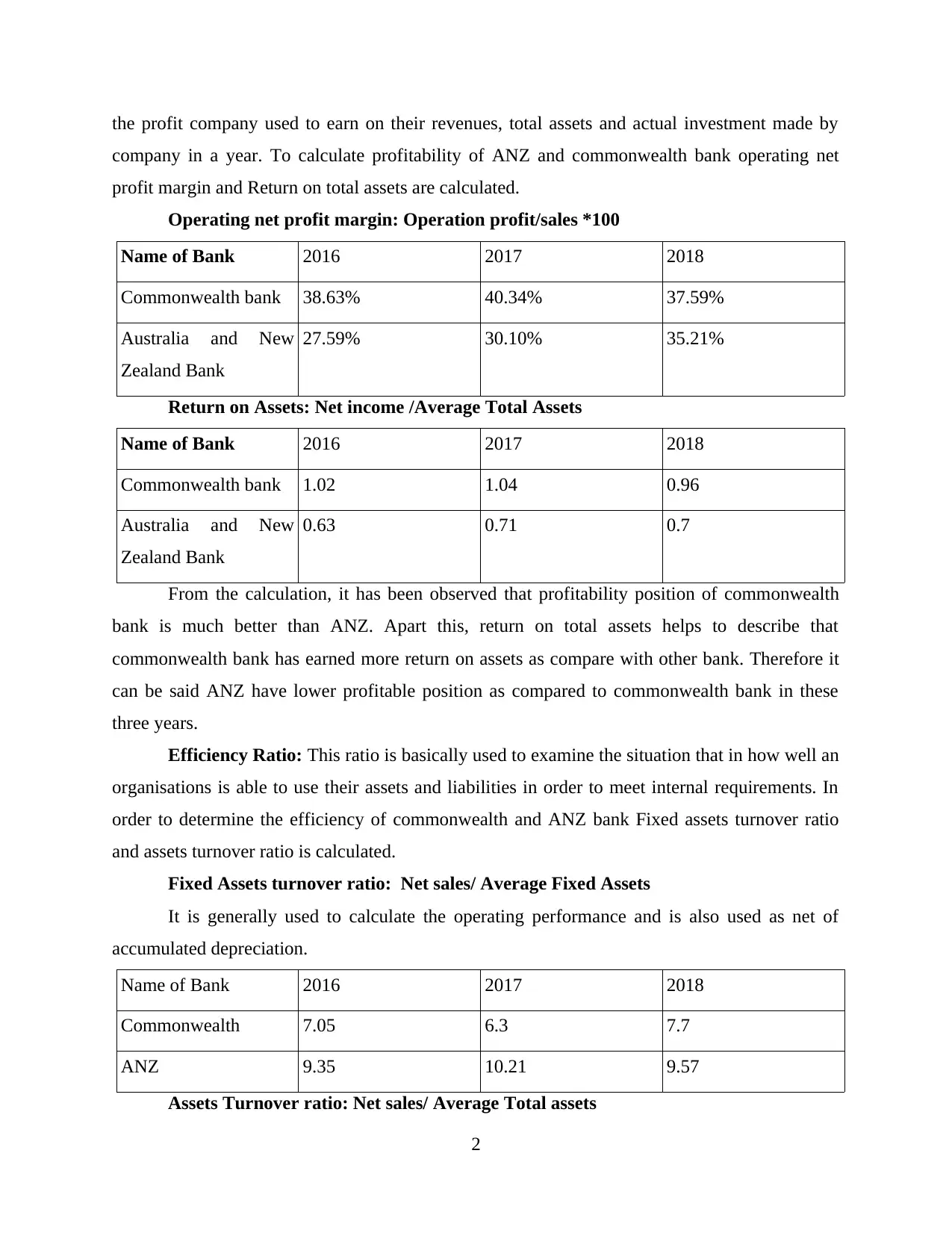

the profit company used to earn on their revenues, total assets and actual investment made by

company in a year. To calculate profitability of ANZ and commonwealth bank operating net

profit margin and Return on total assets are calculated.

Operating net profit margin: Operation profit/sales *100

Name of Bank 2016 2017 2018

Commonwealth bank 38.63% 40.34% 37.59%

Australia and New

Zealand Bank

27.59% 30.10% 35.21%

Return on Assets: Net income /Average Total Assets

Name of Bank 2016 2017 2018

Commonwealth bank 1.02 1.04 0.96

Australia and New

Zealand Bank

0.63 0.71 0.7

From the calculation, it has been observed that profitability position of commonwealth

bank is much better than ANZ. Apart this, return on total assets helps to describe that

commonwealth bank has earned more return on assets as compare with other bank. Therefore it

can be said ANZ have lower profitable position as compared to commonwealth bank in these

three years.

Efficiency Ratio: This ratio is basically used to examine the situation that in how well an

organisations is able to use their assets and liabilities in order to meet internal requirements. In

order to determine the efficiency of commonwealth and ANZ bank Fixed assets turnover ratio

and assets turnover ratio is calculated.

Fixed Assets turnover ratio: Net sales/ Average Fixed Assets

It is generally used to calculate the operating performance and is also used as net of

accumulated depreciation.

Name of Bank 2016 2017 2018

Commonwealth 7.05 6.3 7.7

ANZ 9.35 10.21 9.57

Assets Turnover ratio: Net sales/ Average Total assets

2

company in a year. To calculate profitability of ANZ and commonwealth bank operating net

profit margin and Return on total assets are calculated.

Operating net profit margin: Operation profit/sales *100

Name of Bank 2016 2017 2018

Commonwealth bank 38.63% 40.34% 37.59%

Australia and New

Zealand Bank

27.59% 30.10% 35.21%

Return on Assets: Net income /Average Total Assets

Name of Bank 2016 2017 2018

Commonwealth bank 1.02 1.04 0.96

Australia and New

Zealand Bank

0.63 0.71 0.7

From the calculation, it has been observed that profitability position of commonwealth

bank is much better than ANZ. Apart this, return on total assets helps to describe that

commonwealth bank has earned more return on assets as compare with other bank. Therefore it

can be said ANZ have lower profitable position as compared to commonwealth bank in these

three years.

Efficiency Ratio: This ratio is basically used to examine the situation that in how well an

organisations is able to use their assets and liabilities in order to meet internal requirements. In

order to determine the efficiency of commonwealth and ANZ bank Fixed assets turnover ratio

and assets turnover ratio is calculated.

Fixed Assets turnover ratio: Net sales/ Average Fixed Assets

It is generally used to calculate the operating performance and is also used as net of

accumulated depreciation.

Name of Bank 2016 2017 2018

Commonwealth 7.05 6.3 7.7

ANZ 9.35 10.21 9.57

Assets Turnover ratio: Net sales/ Average Total assets

2

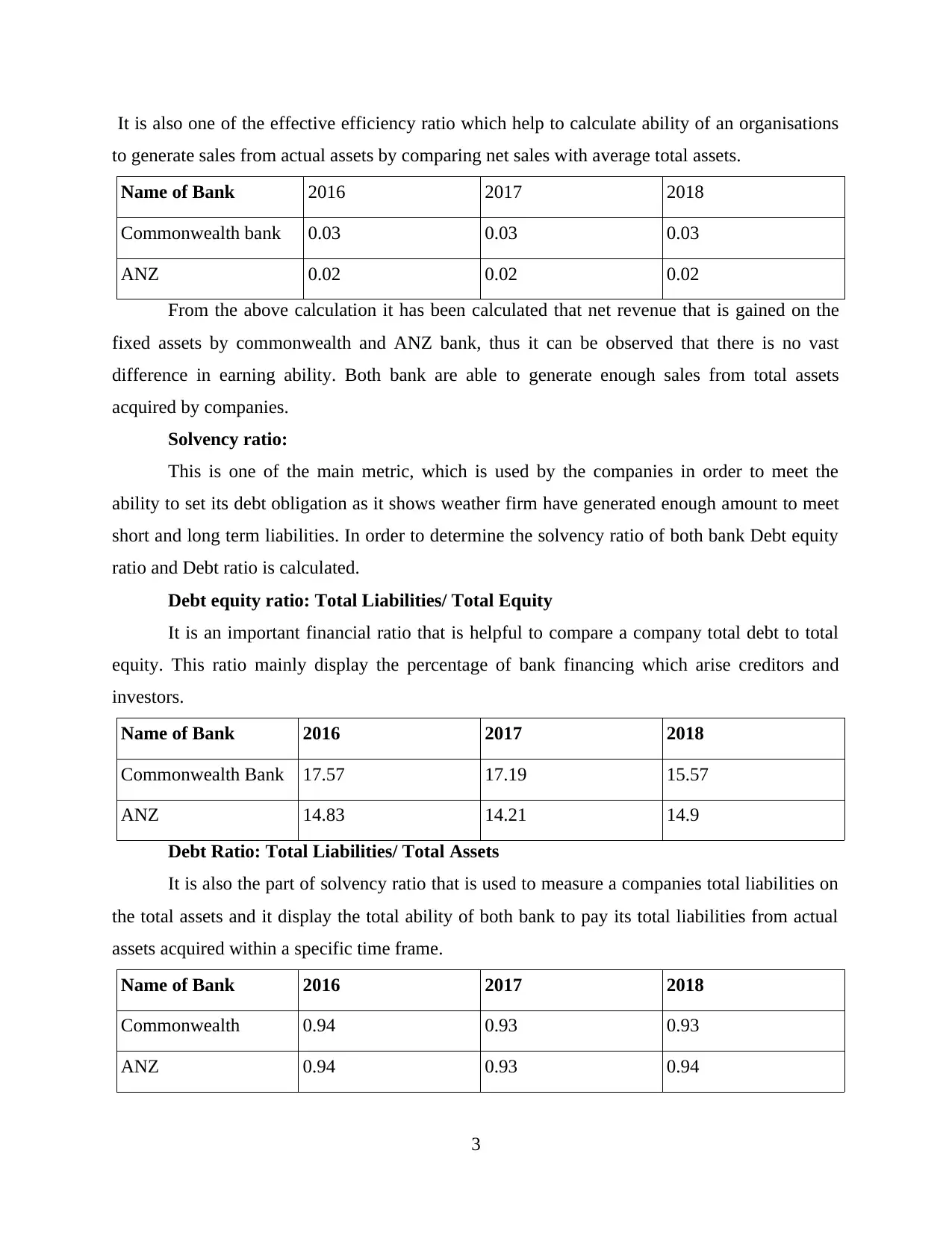

It is also one of the effective efficiency ratio which help to calculate ability of an organisations

to generate sales from actual assets by comparing net sales with average total assets.

Name of Bank 2016 2017 2018

Commonwealth bank 0.03 0.03 0.03

ANZ 0.02 0.02 0.02

From the above calculation it has been calculated that net revenue that is gained on the

fixed assets by commonwealth and ANZ bank, thus it can be observed that there is no vast

difference in earning ability. Both bank are able to generate enough sales from total assets

acquired by companies.

Solvency ratio:

This is one of the main metric, which is used by the companies in order to meet the

ability to set its debt obligation as it shows weather firm have generated enough amount to meet

short and long term liabilities. In order to determine the solvency ratio of both bank Debt equity

ratio and Debt ratio is calculated.

Debt equity ratio: Total Liabilities/ Total Equity

It is an important financial ratio that is helpful to compare a company total debt to total

equity. This ratio mainly display the percentage of bank financing which arise creditors and

investors.

Name of Bank 2016 2017 2018

Commonwealth Bank 17.57 17.19 15.57

ANZ 14.83 14.21 14.9

Debt Ratio: Total Liabilities/ Total Assets

It is also the part of solvency ratio that is used to measure a companies total liabilities on

the total assets and it display the total ability of both bank to pay its total liabilities from actual

assets acquired within a specific time frame.

Name of Bank 2016 2017 2018

Commonwealth 0.94 0.93 0.93

ANZ 0.94 0.93 0.94

3

to generate sales from actual assets by comparing net sales with average total assets.

Name of Bank 2016 2017 2018

Commonwealth bank 0.03 0.03 0.03

ANZ 0.02 0.02 0.02

From the above calculation it has been calculated that net revenue that is gained on the

fixed assets by commonwealth and ANZ bank, thus it can be observed that there is no vast

difference in earning ability. Both bank are able to generate enough sales from total assets

acquired by companies.

Solvency ratio:

This is one of the main metric, which is used by the companies in order to meet the

ability to set its debt obligation as it shows weather firm have generated enough amount to meet

short and long term liabilities. In order to determine the solvency ratio of both bank Debt equity

ratio and Debt ratio is calculated.

Debt equity ratio: Total Liabilities/ Total Equity

It is an important financial ratio that is helpful to compare a company total debt to total

equity. This ratio mainly display the percentage of bank financing which arise creditors and

investors.

Name of Bank 2016 2017 2018

Commonwealth Bank 17.57 17.19 15.57

ANZ 14.83 14.21 14.9

Debt Ratio: Total Liabilities/ Total Assets

It is also the part of solvency ratio that is used to measure a companies total liabilities on

the total assets and it display the total ability of both bank to pay its total liabilities from actual

assets acquired within a specific time frame.

Name of Bank 2016 2017 2018

Commonwealth 0.94 0.93 0.93

ANZ 0.94 0.93 0.94

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

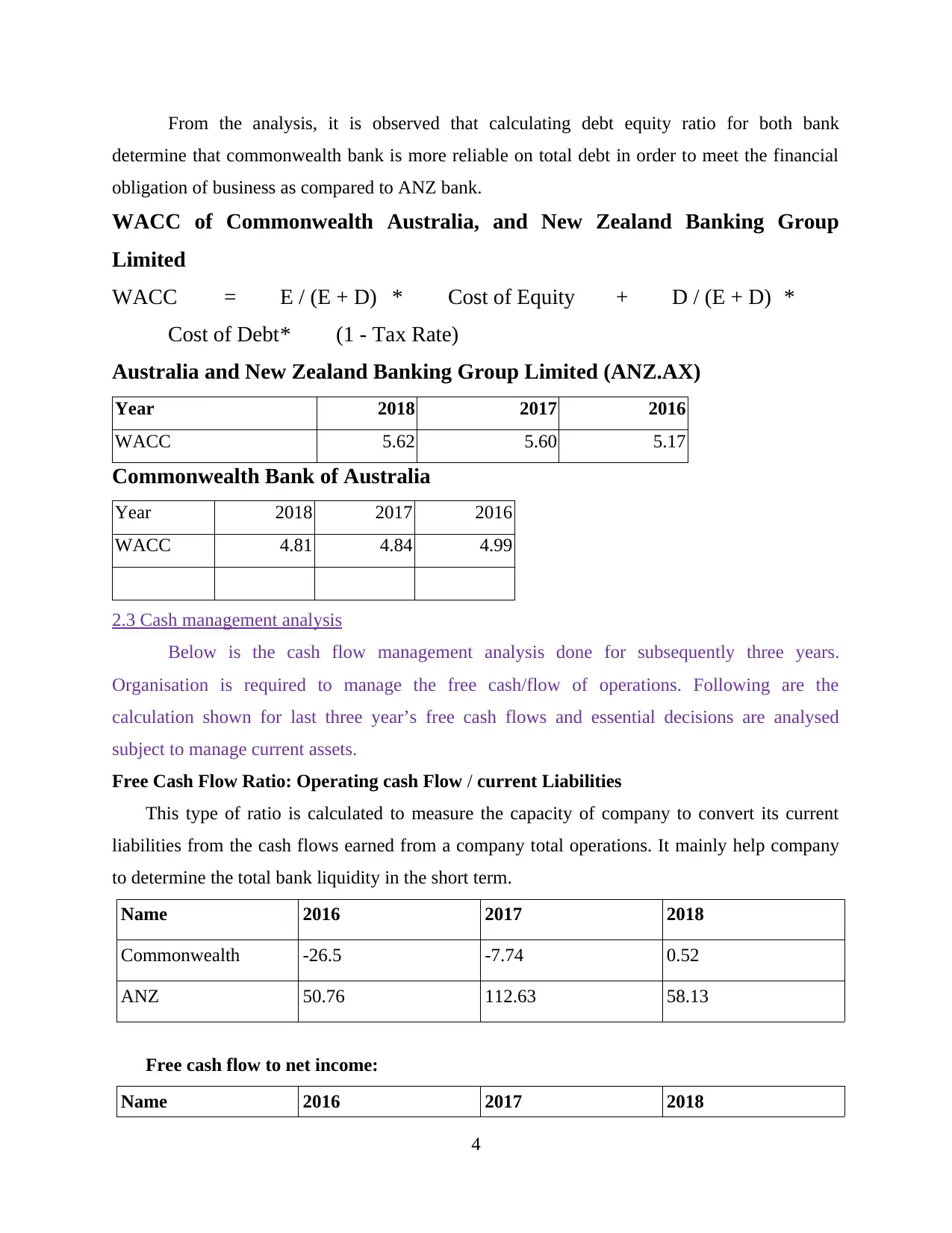

From the analysis, it is observed that calculating debt equity ratio for both bank

determine that commonwealth bank is more reliable on total debt in order to meet the financial

obligation of business as compared to ANZ bank.

WACC of Commonwealth Australia, and New Zealand Banking Group

Limited

WACC = E / (E + D) * Cost of Equity + D / (E + D) *

Cost of Debt* (1 - Tax Rate)

Australia and New Zealand Banking Group Limited (ANZ.AX)

Year 2018 2017 2016

WACC 5.62 5.60 5.17

Commonwealth Bank of Australia

Year 2018 2017 2016

WACC 4.81 4.84 4.99

2.3 Cash management analysis

Below is the cash flow management analysis done for subsequently three years.

Organisation is required to manage the free cash/flow of operations. Following are the

calculation shown for last three year’s free cash flows and essential decisions are analysed

subject to manage current assets.

Free Cash Flow Ratio: Operating cash Flow / current Liabilities

This type of ratio is calculated to measure the capacity of company to convert its current

liabilities from the cash flows earned from a company total operations. It mainly help company

to determine the total bank liquidity in the short term.

Name 2016 2017 2018

Commonwealth -26.5 -7.74 0.52

ANZ 50.76 112.63 58.13

Free cash flow to net income:

Name 2016 2017 2018

4

determine that commonwealth bank is more reliable on total debt in order to meet the financial

obligation of business as compared to ANZ bank.

WACC of Commonwealth Australia, and New Zealand Banking Group

Limited

WACC = E / (E + D) * Cost of Equity + D / (E + D) *

Cost of Debt* (1 - Tax Rate)

Australia and New Zealand Banking Group Limited (ANZ.AX)

Year 2018 2017 2016

WACC 5.62 5.60 5.17

Commonwealth Bank of Australia

Year 2018 2017 2016

WACC 4.81 4.84 4.99

2.3 Cash management analysis

Below is the cash flow management analysis done for subsequently three years.

Organisation is required to manage the free cash/flow of operations. Following are the

calculation shown for last three year’s free cash flows and essential decisions are analysed

subject to manage current assets.

Free Cash Flow Ratio: Operating cash Flow / current Liabilities

This type of ratio is calculated to measure the capacity of company to convert its current

liabilities from the cash flows earned from a company total operations. It mainly help company

to determine the total bank liquidity in the short term.

Name 2016 2017 2018

Commonwealth -26.5 -7.74 0.52

ANZ 50.76 112.63 58.13

Free cash flow to net income:

Name 2016 2017 2018

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

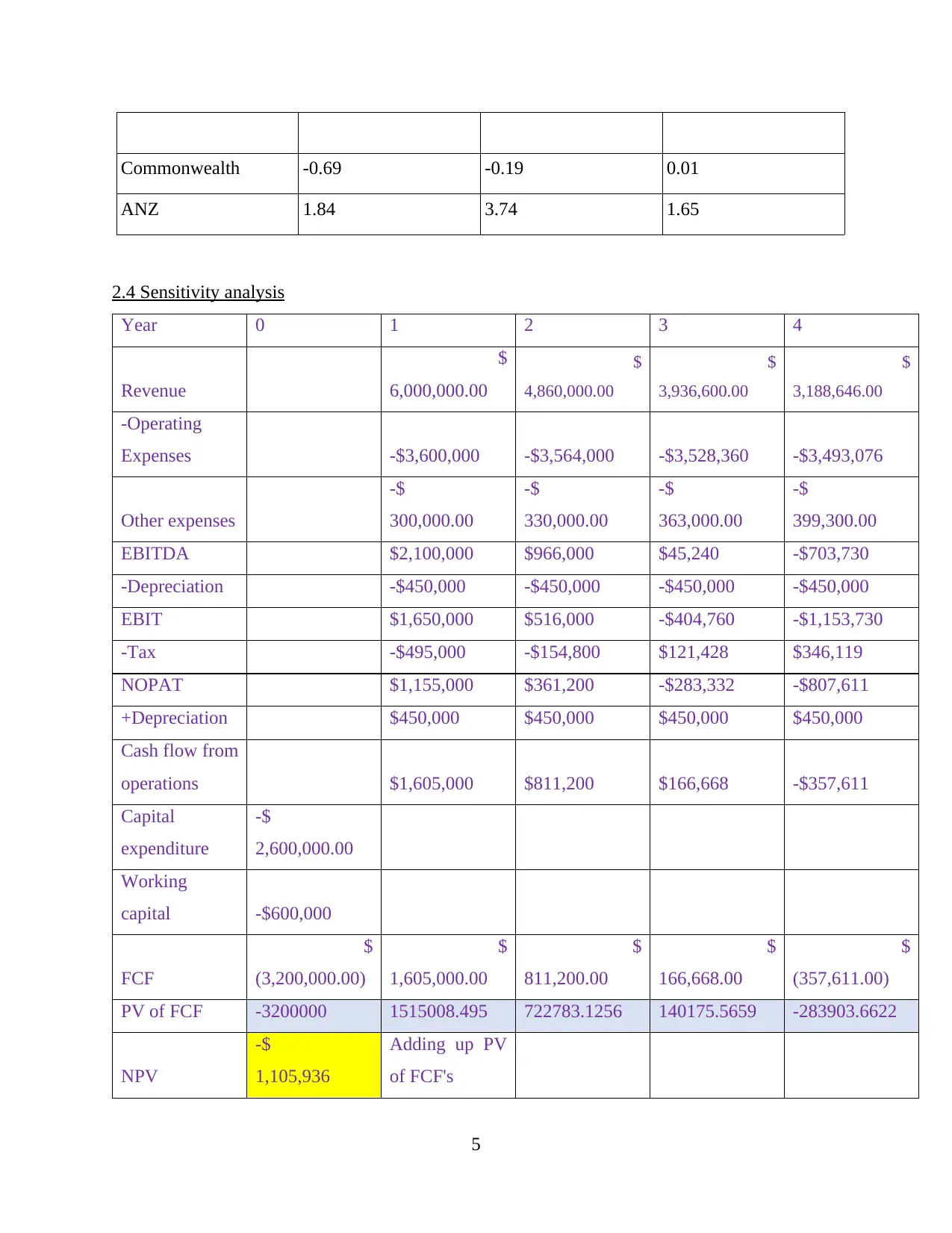

Commonwealth -0.69 -0.19 0.01

ANZ 1.84 3.74 1.65

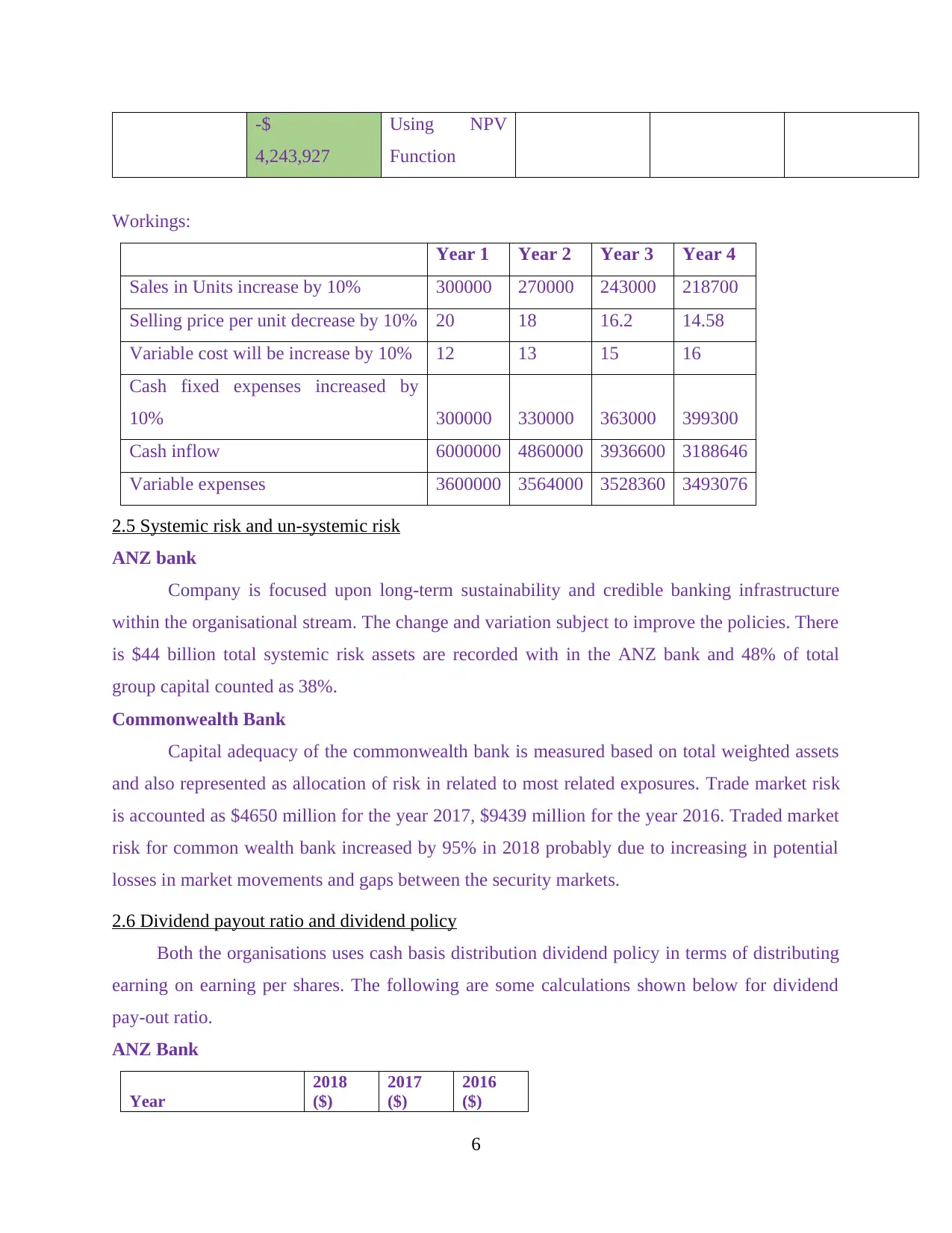

2.4 Sensitivity analysis

Year 0 1 2 3 4

Revenue

$

6,000,000.00

$

4,860,000.00

$

3,936,600.00

$

3,188,646.00

-Operating

Expenses -$3,600,000 -$3,564,000 -$3,528,360 -$3,493,076

Other expenses

-$

300,000.00

-$

330,000.00

-$

363,000.00

-$

399,300.00

EBITDA $2,100,000 $966,000 $45,240 -$703,730

-Depreciation -$450,000 -$450,000 -$450,000 -$450,000

EBIT $1,650,000 $516,000 -$404,760 -$1,153,730

-Tax -$495,000 -$154,800 $121,428 $346,119

NOPAT $1,155,000 $361,200 -$283,332 -$807,611

+Depreciation $450,000 $450,000 $450,000 $450,000

Cash flow from

operations $1,605,000 $811,200 $166,668 -$357,611

Capital

expenditure

-$

2,600,000.00

Working

capital -$600,000

FCF

$

(3,200,000.00)

$

1,605,000.00

$

811,200.00

$

166,668.00

$

(357,611.00)

PV of FCF -3200000 1515008.495 722783.1256 140175.5659 -283903.6622

NPV

-$

1,105,936

Adding up PV

of FCF's

5

ANZ 1.84 3.74 1.65

2.4 Sensitivity analysis

Year 0 1 2 3 4

Revenue

$

6,000,000.00

$

4,860,000.00

$

3,936,600.00

$

3,188,646.00

-Operating

Expenses -$3,600,000 -$3,564,000 -$3,528,360 -$3,493,076

Other expenses

-$

300,000.00

-$

330,000.00

-$

363,000.00

-$

399,300.00

EBITDA $2,100,000 $966,000 $45,240 -$703,730

-Depreciation -$450,000 -$450,000 -$450,000 -$450,000

EBIT $1,650,000 $516,000 -$404,760 -$1,153,730

-Tax -$495,000 -$154,800 $121,428 $346,119

NOPAT $1,155,000 $361,200 -$283,332 -$807,611

+Depreciation $450,000 $450,000 $450,000 $450,000

Cash flow from

operations $1,605,000 $811,200 $166,668 -$357,611

Capital

expenditure

-$

2,600,000.00

Working

capital -$600,000

FCF

$

(3,200,000.00)

$

1,605,000.00

$

811,200.00

$

166,668.00

$

(357,611.00)

PV of FCF -3200000 1515008.495 722783.1256 140175.5659 -283903.6622

NPV

-$

1,105,936

Adding up PV

of FCF's

5

-$

4,243,927

Using NPV

Function

Workings:

Year 1 Year 2 Year 3 Year 4

Sales in Units increase by 10% 300000 270000 243000 218700

Selling price per unit decrease by 10% 20 18 16.2 14.58

Variable cost will be increase by 10% 12 13 15 16

Cash fixed expenses increased by

10% 300000 330000 363000 399300

Cash inflow 6000000 4860000 3936600 3188646

Variable expenses 3600000 3564000 3528360 3493076

2.5 Systemic risk and un-systemic risk

ANZ bank

Company is focused upon long-term sustainability and credible banking infrastructure

within the organisational stream. The change and variation subject to improve the policies. There

is $44 billion total systemic risk assets are recorded with in the ANZ bank and 48% of total

group capital counted as 38%.

Commonwealth Bank

Capital adequacy of the commonwealth bank is measured based on total weighted assets

and also represented as allocation of risk in related to most related exposures. Trade market risk

is accounted as $4650 million for the year 2017, $9439 million for the year 2016. Traded market

risk for common wealth bank increased by 95% in 2018 probably due to increasing in potential

losses in market movements and gaps between the security markets.

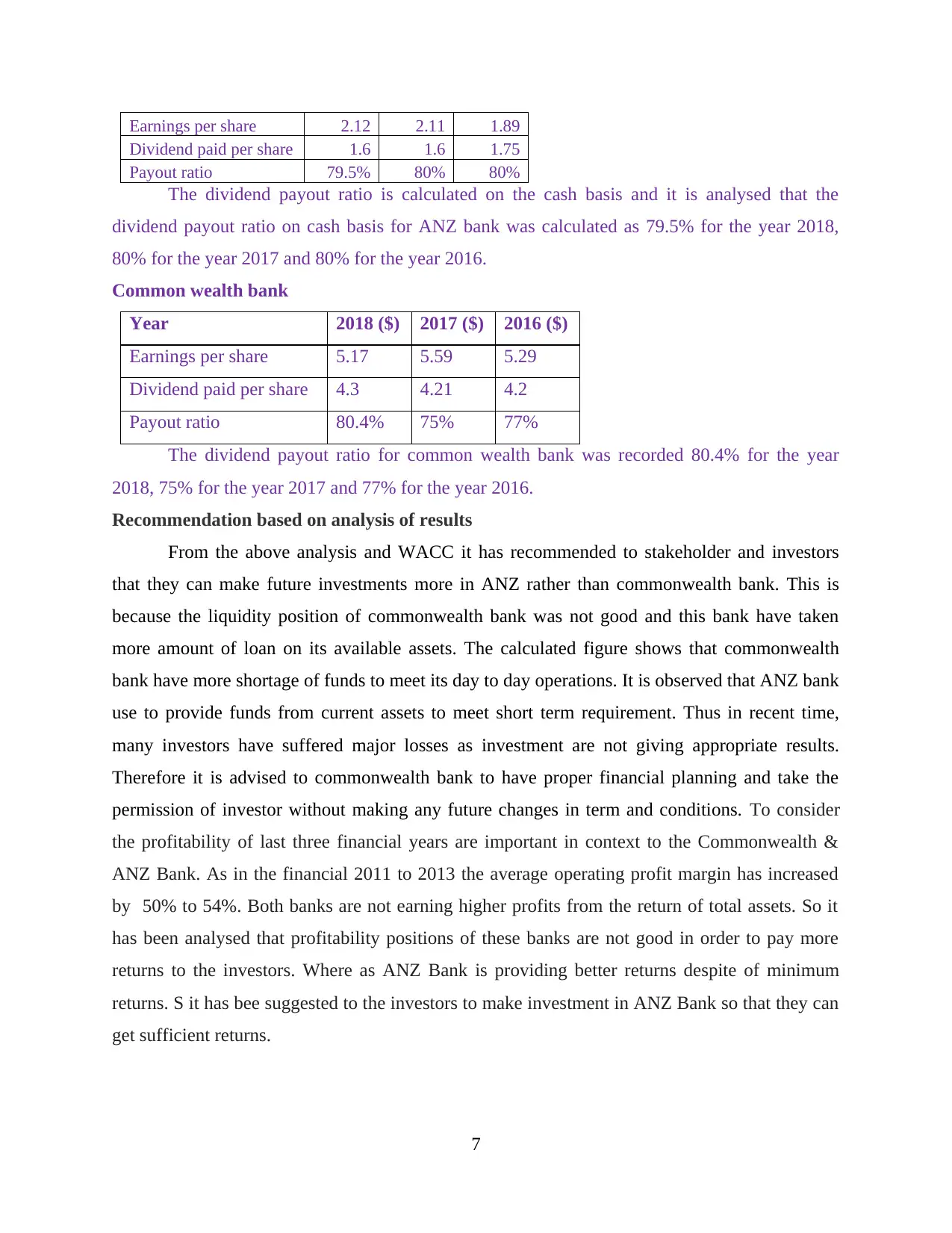

2.6 Dividend payout ratio and dividend policy

Both the organisations uses cash basis distribution dividend policy in terms of distributing

earning on earning per shares. The following are some calculations shown below for dividend

pay-out ratio.

ANZ Bank

Year

2018

($)

2017

($)

2016

($)

6

4,243,927

Using NPV

Function

Workings:

Year 1 Year 2 Year 3 Year 4

Sales in Units increase by 10% 300000 270000 243000 218700

Selling price per unit decrease by 10% 20 18 16.2 14.58

Variable cost will be increase by 10% 12 13 15 16

Cash fixed expenses increased by

10% 300000 330000 363000 399300

Cash inflow 6000000 4860000 3936600 3188646

Variable expenses 3600000 3564000 3528360 3493076

2.5 Systemic risk and un-systemic risk

ANZ bank

Company is focused upon long-term sustainability and credible banking infrastructure

within the organisational stream. The change and variation subject to improve the policies. There

is $44 billion total systemic risk assets are recorded with in the ANZ bank and 48% of total

group capital counted as 38%.

Commonwealth Bank

Capital adequacy of the commonwealth bank is measured based on total weighted assets

and also represented as allocation of risk in related to most related exposures. Trade market risk

is accounted as $4650 million for the year 2017, $9439 million for the year 2016. Traded market

risk for common wealth bank increased by 95% in 2018 probably due to increasing in potential

losses in market movements and gaps between the security markets.

2.6 Dividend payout ratio and dividend policy

Both the organisations uses cash basis distribution dividend policy in terms of distributing

earning on earning per shares. The following are some calculations shown below for dividend

pay-out ratio.

ANZ Bank

Year

2018

($)

2017

($)

2016

($)

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Earnings per share 2.12 2.11 1.89

Dividend paid per share 1.6 1.6 1.75

Payout ratio 79.5% 80% 80%

The dividend payout ratio is calculated on the cash basis and it is analysed that the

dividend payout ratio on cash basis for ANZ bank was calculated as 79.5% for the year 2018,

80% for the year 2017 and 80% for the year 2016.

Common wealth bank

Year 2018 ($) 2017 ($) 2016 ($)

Earnings per share 5.17 5.59 5.29

Dividend paid per share 4.3 4.21 4.2

Payout ratio 80.4% 75% 77%

The dividend payout ratio for common wealth bank was recorded 80.4% for the year

2018, 75% for the year 2017 and 77% for the year 2016.

Recommendation based on analysis of results

From the above analysis and WACC it has recommended to stakeholder and investors

that they can make future investments more in ANZ rather than commonwealth bank. This is

because the liquidity position of commonwealth bank was not good and this bank have taken

more amount of loan on its available assets. The calculated figure shows that commonwealth

bank have more shortage of funds to meet its day to day operations. It is observed that ANZ bank

use to provide funds from current assets to meet short term requirement. Thus in recent time,

many investors have suffered major losses as investment are not giving appropriate results.

Therefore it is advised to commonwealth bank to have proper financial planning and take the

permission of investor without making any future changes in term and conditions. To consider

the profitability of last three financial years are important in context to the Commonwealth &

ANZ Bank. As in the financial 2011 to 2013 the average operating profit margin has increased

by 50% to 54%. Both banks are not earning higher profits from the return of total assets. So it

has been analysed that profitability positions of these banks are not good in order to pay more

returns to the investors. Where as ANZ Bank is providing better returns despite of minimum

returns. S it has bee suggested to the investors to make investment in ANZ Bank so that they can

get sufficient returns.

7

Dividend paid per share 1.6 1.6 1.75

Payout ratio 79.5% 80% 80%

The dividend payout ratio is calculated on the cash basis and it is analysed that the

dividend payout ratio on cash basis for ANZ bank was calculated as 79.5% for the year 2018,

80% for the year 2017 and 80% for the year 2016.

Common wealth bank

Year 2018 ($) 2017 ($) 2016 ($)

Earnings per share 5.17 5.59 5.29

Dividend paid per share 4.3 4.21 4.2

Payout ratio 80.4% 75% 77%

The dividend payout ratio for common wealth bank was recorded 80.4% for the year

2018, 75% for the year 2017 and 77% for the year 2016.

Recommendation based on analysis of results

From the above analysis and WACC it has recommended to stakeholder and investors

that they can make future investments more in ANZ rather than commonwealth bank. This is

because the liquidity position of commonwealth bank was not good and this bank have taken

more amount of loan on its available assets. The calculated figure shows that commonwealth

bank have more shortage of funds to meet its day to day operations. It is observed that ANZ bank

use to provide funds from current assets to meet short term requirement. Thus in recent time,

many investors have suffered major losses as investment are not giving appropriate results.

Therefore it is advised to commonwealth bank to have proper financial planning and take the

permission of investor without making any future changes in term and conditions. To consider

the profitability of last three financial years are important in context to the Commonwealth &

ANZ Bank. As in the financial 2011 to 2013 the average operating profit margin has increased

by 50% to 54%. Both banks are not earning higher profits from the return of total assets. So it

has been analysed that profitability positions of these banks are not good in order to pay more

returns to the investors. Where as ANZ Bank is providing better returns despite of minimum

returns. S it has bee suggested to the investors to make investment in ANZ Bank so that they can

get sufficient returns.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and journals

Annual-report commonwealth. 2019. [Online] Available Through:

<https://www.commbank.com.au/about-us/investors/annual-reports.html>.

Annual-report of 2019. [Online] Available Through: <https://shareholder.anz.com/pages/annual-

report-archive>.

8

Books and journals

Annual-report commonwealth. 2019. [Online] Available Through:

<https://www.commbank.com.au/about-us/investors/annual-reports.html>.

Annual-report of 2019. [Online] Available Through: <https://shareholder.anz.com/pages/annual-

report-archive>.

8

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.