Performance Analysis of Bega Cheese Limited

VerifiedAdded on 2021/06/14

|16

|3442

|53

AI Summary

FINANCIAL INFORMATION FOR DECISION MAKING 7 FINANCIAL INFORMATION FOR DECISION MAKING Financial information for decision making Name of the student Name of the university Student ID Author note Executive summary The main objective of the report is to analyse the performance of Bega Cheese Limited through various measures like profitability ratios, efficiency ratios, liquidity ratios and gearing ratio. It has been identified from the report that though the profitability ratio of the company significantly deteriorated over the years from 2014 to 2015, the company was able to improve the ratio during the

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: FINANCIAL INFORMATION FOR DECISION MAKING

Financial information for decision making

Name of the student

Name of the university

Student ID

Author note

Financial information for decision making

Name of the student

Name of the university

Student ID

Author note

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1FINANCIAL INFORMATION FOR DECISION MAKING

1. Executive summary

The main objective of the report is to analyse the performance of Bega Cheese Limited

through various measures like profitability ratios, efficiency ratios, liquidity ratios and

gearing ratio. For the purpose of analysis this report will take into consideration the

performance of the company over the years from 2014 to 2016. It has been identified from

the report that though the profitability ratio of the company significantly deteriorated over the

years from 2014 to 2015, the company was able to improve the ratio during the year 2016.

The liquidity ratio of the company reveals that the company is efficient in paying its short

term dues with the current assets of the company. Furthermore the gearing ratio of the

company is representing that the debt of the company is lower as compared to the asset

proportion. Further it is identified that the company is efficient in generating revenue from its

asset, converting its receivable into cash and selling or replacing it inventory over the specific

period of time. Therefore it can be stated from all the facts that the company’s financial

health is strong and sustainable. .

1. Executive summary

The main objective of the report is to analyse the performance of Bega Cheese Limited

through various measures like profitability ratios, efficiency ratios, liquidity ratios and

gearing ratio. For the purpose of analysis this report will take into consideration the

performance of the company over the years from 2014 to 2016. It has been identified from

the report that though the profitability ratio of the company significantly deteriorated over the

years from 2014 to 2015, the company was able to improve the ratio during the year 2016.

The liquidity ratio of the company reveals that the company is efficient in paying its short

term dues with the current assets of the company. Furthermore the gearing ratio of the

company is representing that the debt of the company is lower as compared to the asset

proportion. Further it is identified that the company is efficient in generating revenue from its

asset, converting its receivable into cash and selling or replacing it inventory over the specific

period of time. Therefore it can be stated from all the facts that the company’s financial

health is strong and sustainable. .

2FINANCIAL INFORMATION FOR DECISION MAKING

Table of Contents

1. Executive summary.............................................................................................................1

2. Introduction.........................................................................................................................4

3. Ratio calculation and interpretation....................................................................................5

Profitability ratio........................................................................................................................5

Return on shareholder’s equity..............................................................................................5

Return on total asset...............................................................................................................6

Net profit margin....................................................................................................................6

Efficiency ratio...........................................................................................................................6

Inventory turnover..................................................................................................................7

Account receivable turnover..................................................................................................7

Asset turnover............................................................................................................................8

Liquidity ratio.............................................................................................................................8

Current ratio...........................................................................................................................9

Quick ratio..............................................................................................................................9

Gearing ratio...............................................................................................................................9

Debt to asset ratio –..............................................................................................................10

Gearing ratio.........................................................................................................................10

4. Conclusion........................................................................................................................11

Table of Contents

1. Executive summary.............................................................................................................1

2. Introduction.........................................................................................................................4

3. Ratio calculation and interpretation....................................................................................5

Profitability ratio........................................................................................................................5

Return on shareholder’s equity..............................................................................................5

Return on total asset...............................................................................................................6

Net profit margin....................................................................................................................6

Efficiency ratio...........................................................................................................................6

Inventory turnover..................................................................................................................7

Account receivable turnover..................................................................................................7

Asset turnover............................................................................................................................8

Liquidity ratio.............................................................................................................................8

Current ratio...........................................................................................................................9

Quick ratio..............................................................................................................................9

Gearing ratio...............................................................................................................................9

Debt to asset ratio –..............................................................................................................10

Gearing ratio.........................................................................................................................10

4. Conclusion........................................................................................................................11

3FINANCIAL INFORMATION FOR DECISION MAKING

References................................................................................................................................12

Appendix..................................................................................................................................14

References................................................................................................................................12

Appendix..................................................................................................................................14

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4FINANCIAL INFORMATION FOR DECISION MAKING

2. Introduction

Australian Dairy company, Bega Cheese that is based in Bega of New South Wales of

Australia was initially established as the agricultural cooperative company in the year 1989

that was owned by the dairy suppliers and it became the public company during the year

2011. Major business of the company includes the core dairy products like powdered milk

and cream cheese. It also includes various nutritional products produced under the brand

name of Bega Bionutrients like Lactoferrin and milk protein concentrate. Through collected

resources from more than 100 dairy firms of Bega Valley the company is able to distribute

and produce cheese products that are of high quality and distribute it to more than 50

countries all over the world. Driving the challenges, embracing the challenges and building

towards future is the mission statement of the company (Bega Cheese 2018).

Out of total revenue of the company, approximately 27% of the revenues are

generated from these sources. The company holds 25% share of Capital Chilled Foods along

with the multinational company Lion that has the controlling interest. Further, approximately

half of the revenue of the company comes from the products related to processed cheese and

retail cheese. The company holds near about 15.70% of the entire Australian cheese market.

The company exports its product along with other retail business like Royal Victoria,

Melbourne, Dairymont and Tatura (Bega Cheese 2018).

The company falls under cheese manufacturing industry and for last 5 years the

industry is struggling due to varying demand in the export market. However, the positive

trend is supported by the increasing interest of the investors in the cheese manufacturing

industry. The major competitors of Bega Cheese Limited are Fonterra Co-op Group,

Devondale Murray Goulburn, Warrnambool Cheese and Butter and Lion Nathan National

Foods (Bega Cheese 2018).

2. Introduction

Australian Dairy company, Bega Cheese that is based in Bega of New South Wales of

Australia was initially established as the agricultural cooperative company in the year 1989

that was owned by the dairy suppliers and it became the public company during the year

2011. Major business of the company includes the core dairy products like powdered milk

and cream cheese. It also includes various nutritional products produced under the brand

name of Bega Bionutrients like Lactoferrin and milk protein concentrate. Through collected

resources from more than 100 dairy firms of Bega Valley the company is able to distribute

and produce cheese products that are of high quality and distribute it to more than 50

countries all over the world. Driving the challenges, embracing the challenges and building

towards future is the mission statement of the company (Bega Cheese 2018).

Out of total revenue of the company, approximately 27% of the revenues are

generated from these sources. The company holds 25% share of Capital Chilled Foods along

with the multinational company Lion that has the controlling interest. Further, approximately

half of the revenue of the company comes from the products related to processed cheese and

retail cheese. The company holds near about 15.70% of the entire Australian cheese market.

The company exports its product along with other retail business like Royal Victoria,

Melbourne, Dairymont and Tatura (Bega Cheese 2018).

The company falls under cheese manufacturing industry and for last 5 years the

industry is struggling due to varying demand in the export market. However, the positive

trend is supported by the increasing interest of the investors in the cheese manufacturing

industry. The major competitors of Bega Cheese Limited are Fonterra Co-op Group,

Devondale Murray Goulburn, Warrnambool Cheese and Butter and Lion Nathan National

Foods (Bega Cheese 2018).

5FINANCIAL INFORMATION FOR DECISION MAKING

3. Ratio calculation and interpretation

Profitability ratio

Ratio Formula 2016 2015 2014

Profitability ratio

Return on shareholder's

equity

Net income / shareholder's equity 8.99 3.96 22.92

Return on total asset Net income / total assets 5.05 2.25 12.03

Net profit margin Net profit / Sales *100 2.41 1.12 6.18

The profitability ratios are the financial metrics those are used by the analysts for

measuring the profitability of the company with regard to creation of income. Various

profitability ratios those are taken into consideration for measuring the profitability are the

return on assets, return on shareholders and net profit margin (Board and Skrzypacz 2016).

The higher ratio represents that the company is performing well through creation of revenues,

returns and profits. The profitability ratios are useful while the performance of the company

is analyzed and compared with the previous year’s performance.

Return on shareholder’s equity

It is the profitability ratio that is used for measuring the company’s ability for profit

generation from the investment made by the shareholders. In other words, it shows the dollar

earned on each dollar of investment made by the shareholders (Čermák 2015). It can be

identified from the annual report and calculation table that the return on shareholder’s equity

for Bega Cheese Limited for the year 2014, 2015 and 2016 had no particular trend. From

21.01% in 2014 it significantly fell to 3.97% in 2015. However, the company was able to

increase the ratio to 8.78% in 2016. The reason behind the fluctuation was the fluctuation in

net income of the company over the 3 years period under consideration.

3. Ratio calculation and interpretation

Profitability ratio

Ratio Formula 2016 2015 2014

Profitability ratio

Return on shareholder's

equity

Net income / shareholder's equity 8.99 3.96 22.92

Return on total asset Net income / total assets 5.05 2.25 12.03

Net profit margin Net profit / Sales *100 2.41 1.12 6.18

The profitability ratios are the financial metrics those are used by the analysts for

measuring the profitability of the company with regard to creation of income. Various

profitability ratios those are taken into consideration for measuring the profitability are the

return on assets, return on shareholders and net profit margin (Board and Skrzypacz 2016).

The higher ratio represents that the company is performing well through creation of revenues,

returns and profits. The profitability ratios are useful while the performance of the company

is analyzed and compared with the previous year’s performance.

Return on shareholder’s equity

It is the profitability ratio that is used for measuring the company’s ability for profit

generation from the investment made by the shareholders. In other words, it shows the dollar

earned on each dollar of investment made by the shareholders (Čermák 2015). It can be

identified from the annual report and calculation table that the return on shareholder’s equity

for Bega Cheese Limited for the year 2014, 2015 and 2016 had no particular trend. From

21.01% in 2014 it significantly fell to 3.97% in 2015. However, the company was able to

increase the ratio to 8.78% in 2016. The reason behind the fluctuation was the fluctuation in

net income of the company over the 3 years period under consideration.

6FINANCIAL INFORMATION FOR DECISION MAKING

Return on total asset

It provides the indication of the management efficiency with regard to utilization of

the company’s assets for creating the profits. As the initial investor the investor’s main focus

is purchasing the stock for lower than the stock’s intrinsic value. However, as the existing

investor the investor’s main focus is analysing the value along with the quality (Delen, Kuzey

and Uyar 2013). If the return of the company as compared to its asset is higher, the company

will be considered as more efficient as compared to the company that has lower return on

assets. Looking at the calculation it can be identified that the return on asset for the company

for the year 2014, 2015 and 2016 had no particular trend. From 12.03% in 2014 it

significantly fell to 2.25% in 2015. However, the company was able to increase the ratio to

5.05% in 2016. The reason behind the fluctuation was the fluctuation in net income of the

company over the 3 years period under consideration

Net profit margin

Net profit margin of the company states the proportion of sales revenue are kept with

the after paying all the operating expenses, finance expenses and tax expenses. Higher ratio

signifies strong financial position of the company. On the other hand lower net profit margin

signifies that the company is struggling to pay its expenses (Delen, Kuzey and Uyar 2013).

As the net income of the company for the year 2014, 2015 and 2016 were significantly

fluctuating the net profit margin of the company is also fluctuating. It can be observed that

the net profit margin of the company has reduced to 1.12% in 2015 from 6.18% in 2014.

However, the company was able to increase the net profit margin to 2.41% during the year

2016.

Efficiency ratio

Ratio Formula 2016 2015 2014

Return on total asset

It provides the indication of the management efficiency with regard to utilization of

the company’s assets for creating the profits. As the initial investor the investor’s main focus

is purchasing the stock for lower than the stock’s intrinsic value. However, as the existing

investor the investor’s main focus is analysing the value along with the quality (Delen, Kuzey

and Uyar 2013). If the return of the company as compared to its asset is higher, the company

will be considered as more efficient as compared to the company that has lower return on

assets. Looking at the calculation it can be identified that the return on asset for the company

for the year 2014, 2015 and 2016 had no particular trend. From 12.03% in 2014 it

significantly fell to 2.25% in 2015. However, the company was able to increase the ratio to

5.05% in 2016. The reason behind the fluctuation was the fluctuation in net income of the

company over the 3 years period under consideration

Net profit margin

Net profit margin of the company states the proportion of sales revenue are kept with

the after paying all the operating expenses, finance expenses and tax expenses. Higher ratio

signifies strong financial position of the company. On the other hand lower net profit margin

signifies that the company is struggling to pay its expenses (Delen, Kuzey and Uyar 2013).

As the net income of the company for the year 2014, 2015 and 2016 were significantly

fluctuating the net profit margin of the company is also fluctuating. It can be observed that

the net profit margin of the company has reduced to 1.12% in 2015 from 6.18% in 2014.

However, the company was able to increase the net profit margin to 2.41% during the year

2016.

Efficiency ratio

Ratio Formula 2016 2015 2014

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7FINANCIAL INFORMATION FOR DECISION MAKING

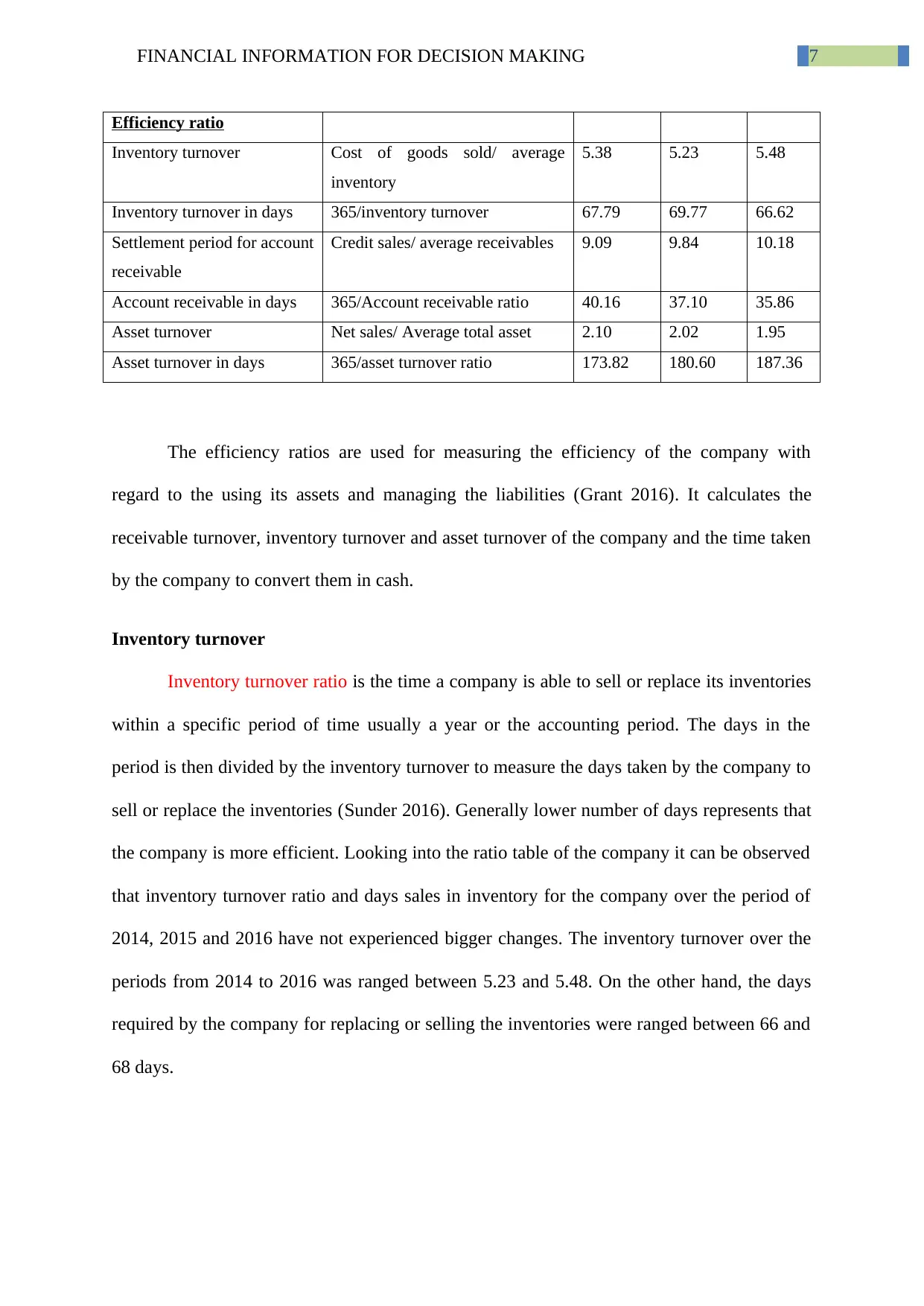

Efficiency ratio

Inventory turnover Cost of goods sold/ average

inventory

5.38 5.23 5.48

Inventory turnover in days 365/inventory turnover 67.79 69.77 66.62

Settlement period for account

receivable

Credit sales/ average receivables 9.09 9.84 10.18

Account receivable in days 365/Account receivable ratio 40.16 37.10 35.86

Asset turnover Net sales/ Average total asset 2.10 2.02 1.95

Asset turnover in days 365/asset turnover ratio 173.82 180.60 187.36

The efficiency ratios are used for measuring the efficiency of the company with

regard to the using its assets and managing the liabilities (Grant 2016). It calculates the

receivable turnover, inventory turnover and asset turnover of the company and the time taken

by the company to convert them in cash.

Inventory turnover

Inventory turnover ratio is the time a company is able to sell or replace its inventories

within a specific period of time usually a year or the accounting period. The days in the

period is then divided by the inventory turnover to measure the days taken by the company to

sell or replace the inventories (Sunder 2016). Generally lower number of days represents that

the company is more efficient. Looking into the ratio table of the company it can be observed

that inventory turnover ratio and days sales in inventory for the company over the period of

2014, 2015 and 2016 have not experienced bigger changes. The inventory turnover over the

periods from 2014 to 2016 was ranged between 5.23 and 5.48. On the other hand, the days

required by the company for replacing or selling the inventories were ranged between 66 and

68 days.

Efficiency ratio

Inventory turnover Cost of goods sold/ average

inventory

5.38 5.23 5.48

Inventory turnover in days 365/inventory turnover 67.79 69.77 66.62

Settlement period for account

receivable

Credit sales/ average receivables 9.09 9.84 10.18

Account receivable in days 365/Account receivable ratio 40.16 37.10 35.86

Asset turnover Net sales/ Average total asset 2.10 2.02 1.95

Asset turnover in days 365/asset turnover ratio 173.82 180.60 187.36

The efficiency ratios are used for measuring the efficiency of the company with

regard to the using its assets and managing the liabilities (Grant 2016). It calculates the

receivable turnover, inventory turnover and asset turnover of the company and the time taken

by the company to convert them in cash.

Inventory turnover

Inventory turnover ratio is the time a company is able to sell or replace its inventories

within a specific period of time usually a year or the accounting period. The days in the

period is then divided by the inventory turnover to measure the days taken by the company to

sell or replace the inventories (Sunder 2016). Generally lower number of days represents that

the company is more efficient. Looking into the ratio table of the company it can be observed

that inventory turnover ratio and days sales in inventory for the company over the period of

2014, 2015 and 2016 have not experienced bigger changes. The inventory turnover over the

periods from 2014 to 2016 was ranged between 5.23 and 5.48. On the other hand, the days

required by the company for replacing or selling the inventories were ranged between 66 and

68 days.

8FINANCIAL INFORMATION FOR DECISION MAKING

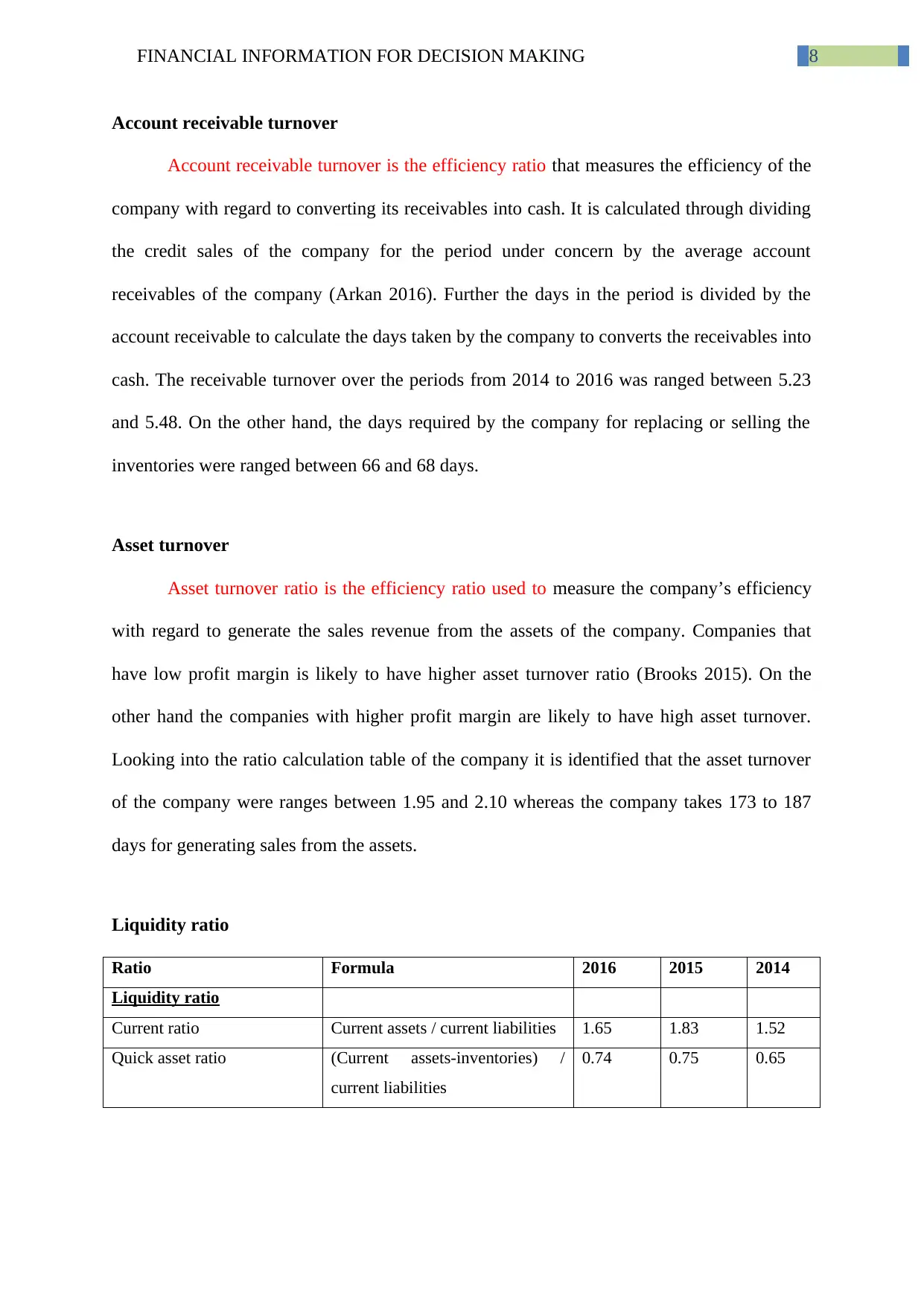

Account receivable turnover

Account receivable turnover is the efficiency ratio that measures the efficiency of the

company with regard to converting its receivables into cash. It is calculated through dividing

the credit sales of the company for the period under concern by the average account

receivables of the company (Arkan 2016). Further the days in the period is divided by the

account receivable to calculate the days taken by the company to converts the receivables into

cash. The receivable turnover over the periods from 2014 to 2016 was ranged between 5.23

and 5.48. On the other hand, the days required by the company for replacing or selling the

inventories were ranged between 66 and 68 days.

Asset turnover

Asset turnover ratio is the efficiency ratio used to measure the company’s efficiency

with regard to generate the sales revenue from the assets of the company. Companies that

have low profit margin is likely to have higher asset turnover ratio (Brooks 2015). On the

other hand the companies with higher profit margin are likely to have high asset turnover.

Looking into the ratio calculation table of the company it is identified that the asset turnover

of the company were ranges between 1.95 and 2.10 whereas the company takes 173 to 187

days for generating sales from the assets.

Liquidity ratio

Ratio Formula 2016 2015 2014

Liquidity ratio

Current ratio Current assets / current liabilities 1.65 1.83 1.52

Quick asset ratio (Current assets-inventories) /

current liabilities

0.74 0.75 0.65

Account receivable turnover

Account receivable turnover is the efficiency ratio that measures the efficiency of the

company with regard to converting its receivables into cash. It is calculated through dividing

the credit sales of the company for the period under concern by the average account

receivables of the company (Arkan 2016). Further the days in the period is divided by the

account receivable to calculate the days taken by the company to converts the receivables into

cash. The receivable turnover over the periods from 2014 to 2016 was ranged between 5.23

and 5.48. On the other hand, the days required by the company for replacing or selling the

inventories were ranged between 66 and 68 days.

Asset turnover

Asset turnover ratio is the efficiency ratio used to measure the company’s efficiency

with regard to generate the sales revenue from the assets of the company. Companies that

have low profit margin is likely to have higher asset turnover ratio (Brooks 2015). On the

other hand the companies with higher profit margin are likely to have high asset turnover.

Looking into the ratio calculation table of the company it is identified that the asset turnover

of the company were ranges between 1.95 and 2.10 whereas the company takes 173 to 187

days for generating sales from the assets.

Liquidity ratio

Ratio Formula 2016 2015 2014

Liquidity ratio

Current ratio Current assets / current liabilities 1.65 1.83 1.52

Quick asset ratio (Current assets-inventories) /

current liabilities

0.74 0.75 0.65

9FINANCIAL INFORMATION FOR DECISION MAKING

Company computes the liquidity ratios to measure its ability to make the payment of

its short-term obligations with the available marketable securities and cash of the company

(Nobes 2014). If the current ratio of the company is equal to more than 1 it signifies that the

current asset of the company is sufficient to meet the short-term obligation of the company. If

the company has continuous issues to meet its short term obligations it signals that the

company is heading towards bankruptcy (Drehmann and Nikolaou 2013).

Current ratio

It is the liquid ratio that states the current assets of the company as compared to its

current liabilities. This ratio is used as an indicator of the company’s liquidity position. If the

current assets of the company are more than the current liability it provides an assurance that

the short-term obligation of the company will be paid efficiently. Looking at the current ratio

of the company over the period from 2014 to 2016 it is identified that for all the years the

ratio of the company is more than 1. However, from 1.52 in 2014 it increased to 1.83 in 2015.

However, during 2016 the current ratio of the company fell to 1.65

Quick ratio

Quick ratios are also the liquidity ratio used for measuring the liquidity of the

company. The only difference between the current ratio and the quick asset ratio is that the

current ratio takes all the current assets of the company whereas the quick asset ratio

considers the asset which are readily available to convert into cash that is the assets like

inventory and prepaid expenses are not taken into consideration as these assets take some

time to get converted into cash (Luez and Wysocki 2016). From the calculation of quick asset

ratio it is identified that the quick asset of the company has been increased from 0.65 to 0.75

over the Year from 2014 to 2015. However it has been reduced to 0.74 in the year 2016.

Company computes the liquidity ratios to measure its ability to make the payment of

its short-term obligations with the available marketable securities and cash of the company

(Nobes 2014). If the current ratio of the company is equal to more than 1 it signifies that the

current asset of the company is sufficient to meet the short-term obligation of the company. If

the company has continuous issues to meet its short term obligations it signals that the

company is heading towards bankruptcy (Drehmann and Nikolaou 2013).

Current ratio

It is the liquid ratio that states the current assets of the company as compared to its

current liabilities. This ratio is used as an indicator of the company’s liquidity position. If the

current assets of the company are more than the current liability it provides an assurance that

the short-term obligation of the company will be paid efficiently. Looking at the current ratio

of the company over the period from 2014 to 2016 it is identified that for all the years the

ratio of the company is more than 1. However, from 1.52 in 2014 it increased to 1.83 in 2015.

However, during 2016 the current ratio of the company fell to 1.65

Quick ratio

Quick ratios are also the liquidity ratio used for measuring the liquidity of the

company. The only difference between the current ratio and the quick asset ratio is that the

current ratio takes all the current assets of the company whereas the quick asset ratio

considers the asset which are readily available to convert into cash that is the assets like

inventory and prepaid expenses are not taken into consideration as these assets take some

time to get converted into cash (Luez and Wysocki 2016). From the calculation of quick asset

ratio it is identified that the quick asset of the company has been increased from 0.65 to 0.75

over the Year from 2014 to 2015. However it has been reduced to 0.74 in the year 2016.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10FINANCIAL INFORMATION FOR DECISION MAKING

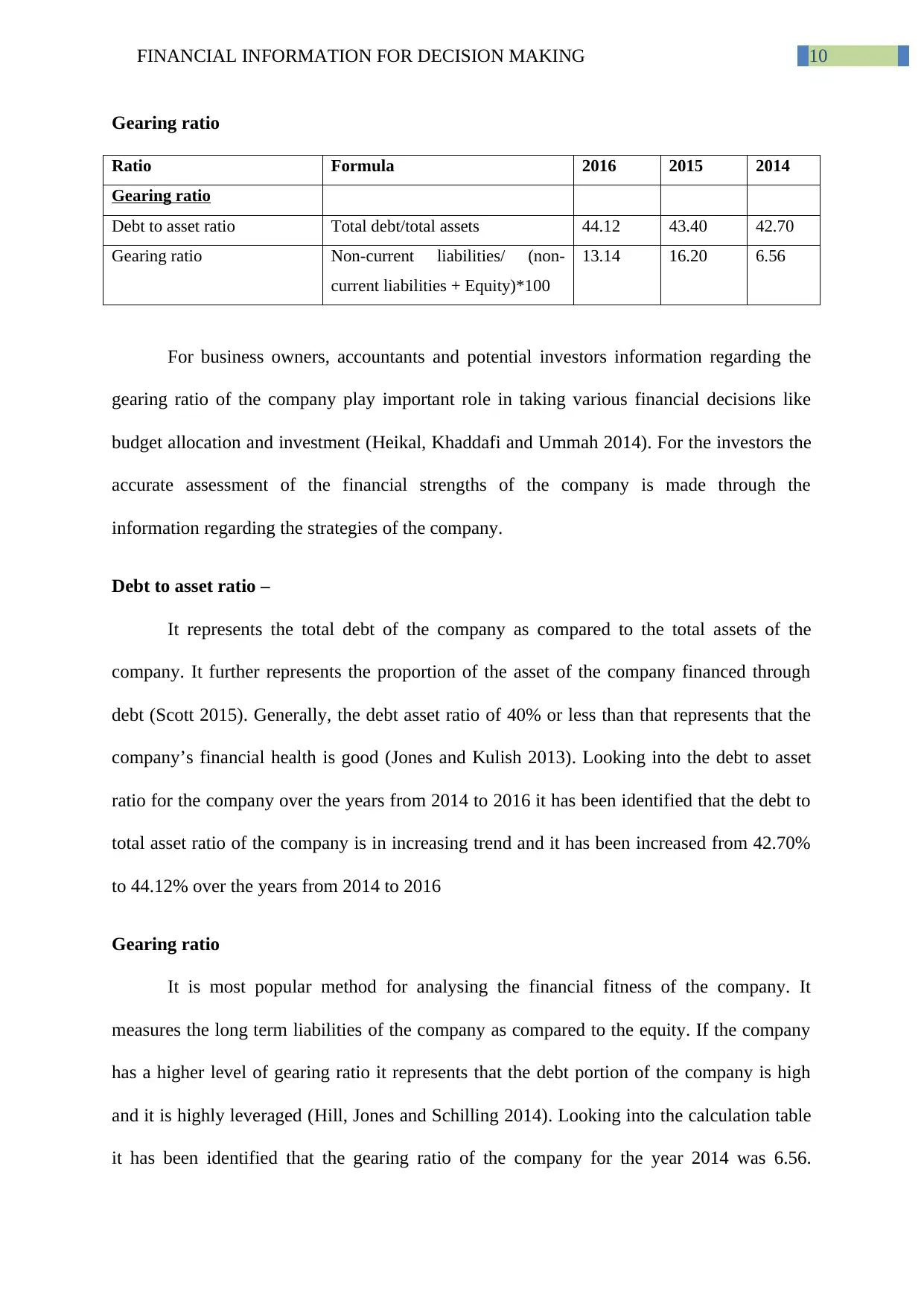

Gearing ratio

Ratio Formula 2016 2015 2014

Gearing ratio

Debt to asset ratio Total debt/total assets 44.12 43.40 42.70

Gearing ratio Non-current liabilities/ (non-

current liabilities + Equity)*100

13.14 16.20 6.56

For business owners, accountants and potential investors information regarding the

gearing ratio of the company play important role in taking various financial decisions like

budget allocation and investment (Heikal, Khaddafi and Ummah 2014). For the investors the

accurate assessment of the financial strengths of the company is made through the

information regarding the strategies of the company.

Debt to asset ratio –

It represents the total debt of the company as compared to the total assets of the

company. It further represents the proportion of the asset of the company financed through

debt (Scott 2015). Generally, the debt asset ratio of 40% or less than that represents that the

company’s financial health is good (Jones and Kulish 2013). Looking into the debt to asset

ratio for the company over the years from 2014 to 2016 it has been identified that the debt to

total asset ratio of the company is in increasing trend and it has been increased from 42.70%

to 44.12% over the years from 2014 to 2016

Gearing ratio

It is most popular method for analysing the financial fitness of the company. It

measures the long term liabilities of the company as compared to the equity. If the company

has a higher level of gearing ratio it represents that the debt portion of the company is high

and it is highly leveraged (Hill, Jones and Schilling 2014). Looking into the calculation table

it has been identified that the gearing ratio of the company for the year 2014 was 6.56.

Gearing ratio

Ratio Formula 2016 2015 2014

Gearing ratio

Debt to asset ratio Total debt/total assets 44.12 43.40 42.70

Gearing ratio Non-current liabilities/ (non-

current liabilities + Equity)*100

13.14 16.20 6.56

For business owners, accountants and potential investors information regarding the

gearing ratio of the company play important role in taking various financial decisions like

budget allocation and investment (Heikal, Khaddafi and Ummah 2014). For the investors the

accurate assessment of the financial strengths of the company is made through the

information regarding the strategies of the company.

Debt to asset ratio –

It represents the total debt of the company as compared to the total assets of the

company. It further represents the proportion of the asset of the company financed through

debt (Scott 2015). Generally, the debt asset ratio of 40% or less than that represents that the

company’s financial health is good (Jones and Kulish 2013). Looking into the debt to asset

ratio for the company over the years from 2014 to 2016 it has been identified that the debt to

total asset ratio of the company is in increasing trend and it has been increased from 42.70%

to 44.12% over the years from 2014 to 2016

Gearing ratio

It is most popular method for analysing the financial fitness of the company. It

measures the long term liabilities of the company as compared to the equity. If the company

has a higher level of gearing ratio it represents that the debt portion of the company is high

and it is highly leveraged (Hill, Jones and Schilling 2014). Looking into the calculation table

it has been identified that the gearing ratio of the company for the year 2014 was 6.56.

11FINANCIAL INFORMATION FOR DECISION MAKING

However during 2015 it has been significantly increased to 16.20 but the company was able

to reduce the gearing ratio to 13.14 during the year 2016 (Prasetyorini 2013).

4. Conclusion

From the above discussion it is concluded that though the profitability position of the

company has been deteriorated in 2015 as compared to the year 2014, the company was able

to improve the profitability during the year 2016. If the efficiency ratios of the company are

taken into consideration it can be identified that the company is quite efficient in converting

is assets into cash. Looking into the liquidity ratio of the company it is identified that the

current ratio as well as the quick asset ratio of the company representing that the company is

efficient in paying its short term obligations with the available short term assets. Further, the

gearing ratio represents that the company is lower leveraged which in turn ensures that the

company is sustainable over the long-term period.

However during 2015 it has been significantly increased to 16.20 but the company was able

to reduce the gearing ratio to 13.14 during the year 2016 (Prasetyorini 2013).

4. Conclusion

From the above discussion it is concluded that though the profitability position of the

company has been deteriorated in 2015 as compared to the year 2014, the company was able

to improve the profitability during the year 2016. If the efficiency ratios of the company are

taken into consideration it can be identified that the company is quite efficient in converting

is assets into cash. Looking into the liquidity ratio of the company it is identified that the

current ratio as well as the quick asset ratio of the company representing that the company is

efficient in paying its short term obligations with the available short term assets. Further, the

gearing ratio represents that the company is lower leveraged which in turn ensures that the

company is sustainable over the long-term period.

12FINANCIAL INFORMATION FOR DECISION MAKING

References

Arkan, T., 2016. The importance of financial ratios in predicting stock price trends: A case

study in emerging markets. Finanse. Rynki Finansowe, Ubezpieczenia, (1), p.79.

Bega Cheese., 2018. Home - Bega Cheese. [online] Available at:

https://www.begacheese.com.au/ [Accessed 17 May 2018].

Board, S., and Skrzypacz, A., 2016. Revenue management with forward-looking

buyers. Journal of Political Economy, 124(4), 1046-1087.

Brooks, R., 2015. Financial management: core concepts. Pearson.

Čermák, P., 2015. Customer profitability analysis and customer life time value models:

Portfolio analysis. Procedia Economics and Finance, 25, 14-25.

Delen, D., Kuzey, C. and Uyar, A., 2013. Measuring firm performance using financial ratios:

A decision tree approach. Expert Systems with Applications, 40(10), pp.3970-3983.

Drehmann, M., and Nikolaou, K., 2013. Funding liquidity risk: definition and

measurement. Journal of Banking and Finance, 37(7), 2173-2182.

Grant, R.M., 2016. Contemporary strategy analysis: Text and cases edition. John Wiley and

Sons.

Heikal, M., Khaddafi, M., and Ummah, A., 2014. Influence analysis of return on assets

(ROA), return on equity (ROE), net profit margin (NPM), debt to equity ratio (DER), and

current ratio (CR), against corporate profit growth in automotive in Indonesia Stock

Exchange. International Journal of Academic Research in Business and Social

Sciences, 4(12), 101.

References

Arkan, T., 2016. The importance of financial ratios in predicting stock price trends: A case

study in emerging markets. Finanse. Rynki Finansowe, Ubezpieczenia, (1), p.79.

Bega Cheese., 2018. Home - Bega Cheese. [online] Available at:

https://www.begacheese.com.au/ [Accessed 17 May 2018].

Board, S., and Skrzypacz, A., 2016. Revenue management with forward-looking

buyers. Journal of Political Economy, 124(4), 1046-1087.

Brooks, R., 2015. Financial management: core concepts. Pearson.

Čermák, P., 2015. Customer profitability analysis and customer life time value models:

Portfolio analysis. Procedia Economics and Finance, 25, 14-25.

Delen, D., Kuzey, C. and Uyar, A., 2013. Measuring firm performance using financial ratios:

A decision tree approach. Expert Systems with Applications, 40(10), pp.3970-3983.

Drehmann, M., and Nikolaou, K., 2013. Funding liquidity risk: definition and

measurement. Journal of Banking and Finance, 37(7), 2173-2182.

Grant, R.M., 2016. Contemporary strategy analysis: Text and cases edition. John Wiley and

Sons.

Heikal, M., Khaddafi, M., and Ummah, A., 2014. Influence analysis of return on assets

(ROA), return on equity (ROE), net profit margin (NPM), debt to equity ratio (DER), and

current ratio (CR), against corporate profit growth in automotive in Indonesia Stock

Exchange. International Journal of Academic Research in Business and Social

Sciences, 4(12), 101.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

13FINANCIAL INFORMATION FOR DECISION MAKING

Hill, C.W., Jones, G.R. and Schilling, M.A., 2014. Strategic management: theory: an

integrated approach. Cengage Learning.

Jones, C., and Kulish, M., 2013. Long-term interest rates, risk premia and unconventional

monetary policy. Journal of Economic Dynamics and Control, 37(12), 2547-2561.

Luez, C. and Wysocki, P., 2016. Economic Consequences of Financial Reporting and

Disclosure Regulation: A Review and Suggestions for Future Research. J. Acct. and

Econ., 50, p.525.

Nobes, C., 2014. International Classification of Financial Reporting 3e. Routledge.

Prasetyorini, B. F. 2013. Pengaruh ukuran perusahaan, leverage, price earnings ratio dan

profitabilitas terhadap nilai perusahaan. Jurnal Ilmu Manajemen, 1(1), 183-196.

Scott, W.R., 2015. Financial accounting theory (Vol. 2, No. 0, p. 0). Prentice Hall.

Sunder, S., 2016. Rethinking financial reporting: standards, norms and

institutions. Foundations and Trends® in Accounting, 11(1–2), pp.1-118.

Hill, C.W., Jones, G.R. and Schilling, M.A., 2014. Strategic management: theory: an

integrated approach. Cengage Learning.

Jones, C., and Kulish, M., 2013. Long-term interest rates, risk premia and unconventional

monetary policy. Journal of Economic Dynamics and Control, 37(12), 2547-2561.

Luez, C. and Wysocki, P., 2016. Economic Consequences of Financial Reporting and

Disclosure Regulation: A Review and Suggestions for Future Research. J. Acct. and

Econ., 50, p.525.

Nobes, C., 2014. International Classification of Financial Reporting 3e. Routledge.

Prasetyorini, B. F. 2013. Pengaruh ukuran perusahaan, leverage, price earnings ratio dan

profitabilitas terhadap nilai perusahaan. Jurnal Ilmu Manajemen, 1(1), 183-196.

Scott, W.R., 2015. Financial accounting theory (Vol. 2, No. 0, p. 0). Prentice Hall.

Sunder, S., 2016. Rethinking financial reporting: standards, norms and

institutions. Foundations and Trends® in Accounting, 11(1–2), pp.1-118.

14FINANCIAL INFORMATION FOR DECISION MAKING

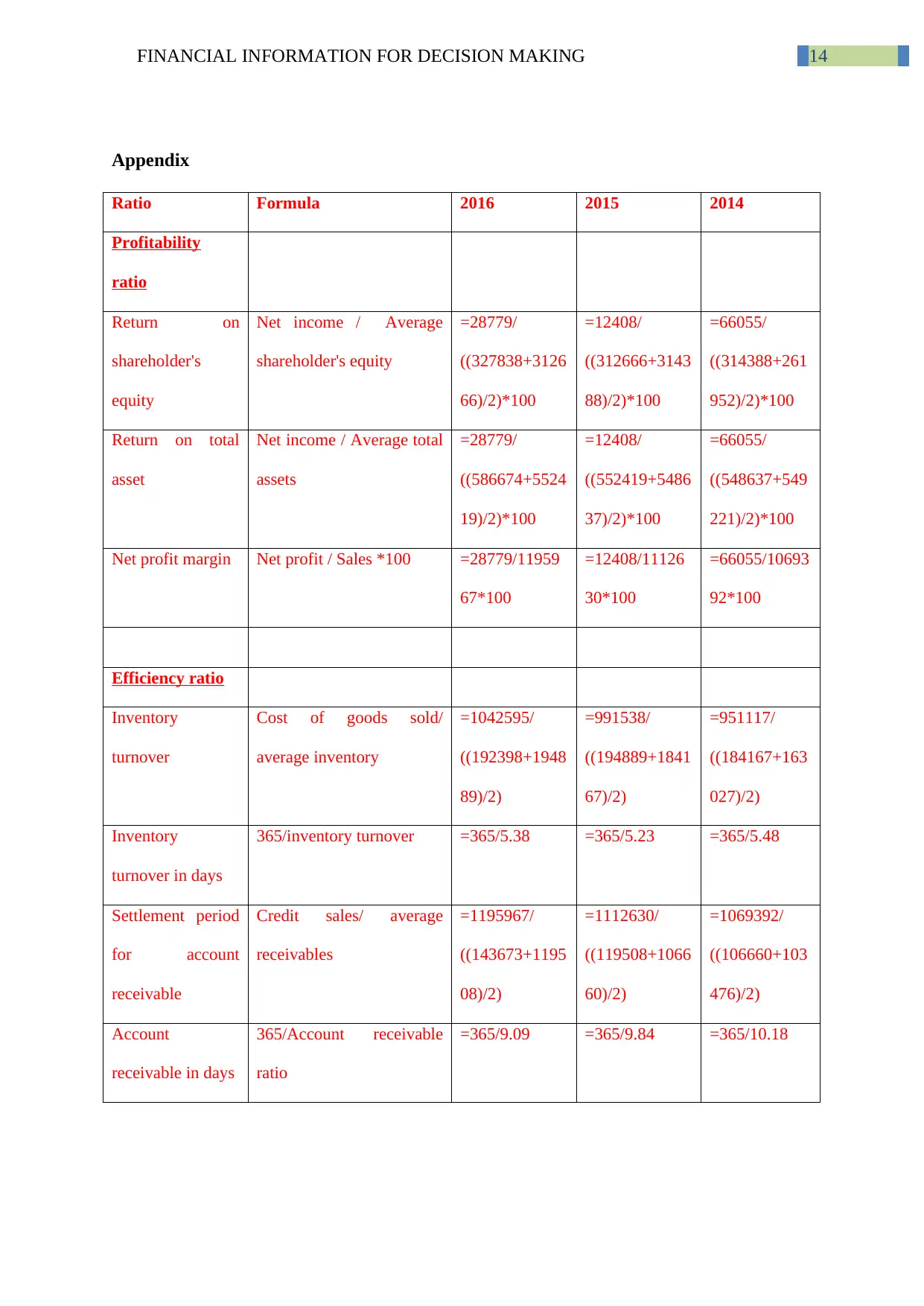

Appendix

Ratio Formula 2016 2015 2014

Profitability

ratio

Return on

shareholder's

equity

Net income / Average

shareholder's equity

=28779/

((327838+3126

66)/2)*100

=12408/

((312666+3143

88)/2)*100

=66055/

((314388+261

952)/2)*100

Return on total

asset

Net income / Average total

assets

=28779/

((586674+5524

19)/2)*100

=12408/

((552419+5486

37)/2)*100

=66055/

((548637+549

221)/2)*100

Net profit margin Net profit / Sales *100 =28779/11959

67*100

=12408/11126

30*100

=66055/10693

92*100

Efficiency ratio

Inventory

turnover

Cost of goods sold/

average inventory

=1042595/

((192398+1948

89)/2)

=991538/

((194889+1841

67)/2)

=951117/

((184167+163

027)/2)

Inventory

turnover in days

365/inventory turnover =365/5.38 =365/5.23 =365/5.48

Settlement period

for account

receivable

Credit sales/ average

receivables

=1195967/

((143673+1195

08)/2)

=1112630/

((119508+1066

60)/2)

=1069392/

((106660+103

476)/2)

Account

receivable in days

365/Account receivable

ratio

=365/9.09 =365/9.84 =365/10.18

Appendix

Ratio Formula 2016 2015 2014

Profitability

ratio

Return on

shareholder's

equity

Net income / Average

shareholder's equity

=28779/

((327838+3126

66)/2)*100

=12408/

((312666+3143

88)/2)*100

=66055/

((314388+261

952)/2)*100

Return on total

asset

Net income / Average total

assets

=28779/

((586674+5524

19)/2)*100

=12408/

((552419+5486

37)/2)*100

=66055/

((548637+549

221)/2)*100

Net profit margin Net profit / Sales *100 =28779/11959

67*100

=12408/11126

30*100

=66055/10693

92*100

Efficiency ratio

Inventory

turnover

Cost of goods sold/

average inventory

=1042595/

((192398+1948

89)/2)

=991538/

((194889+1841

67)/2)

=951117/

((184167+163

027)/2)

Inventory

turnover in days

365/inventory turnover =365/5.38 =365/5.23 =365/5.48

Settlement period

for account

receivable

Credit sales/ average

receivables

=1195967/

((143673+1195

08)/2)

=1112630/

((119508+1066

60)/2)

=1069392/

((106660+103

476)/2)

Account

receivable in days

365/Account receivable

ratio

=365/9.09 =365/9.84 =365/10.18

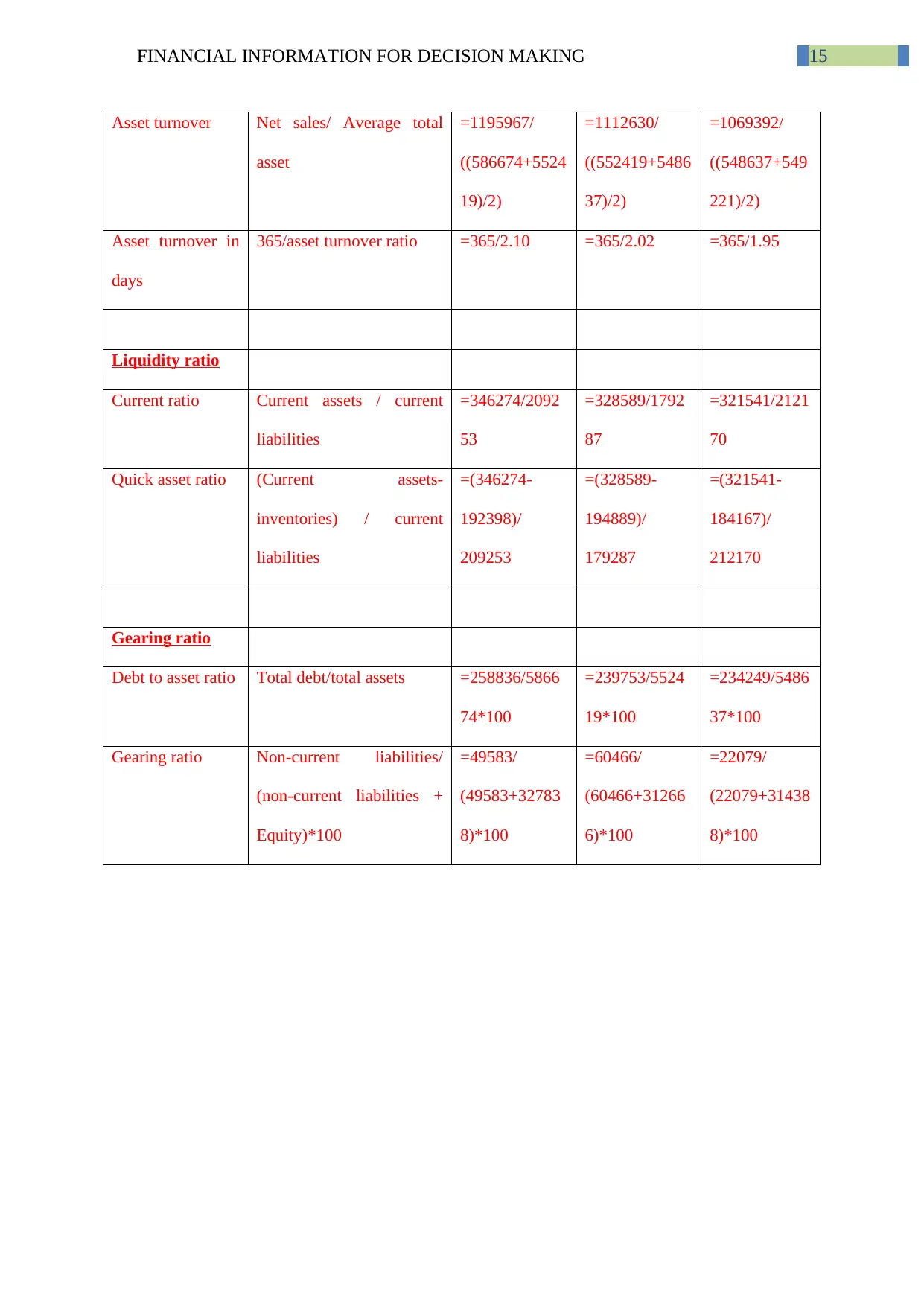

15FINANCIAL INFORMATION FOR DECISION MAKING

Asset turnover Net sales/ Average total

asset

=1195967/

((586674+5524

19)/2)

=1112630/

((552419+5486

37)/2)

=1069392/

((548637+549

221)/2)

Asset turnover in

days

365/asset turnover ratio =365/2.10 =365/2.02 =365/1.95

Liquidity ratio

Current ratio Current assets / current

liabilities

=346274/2092

53

=328589/1792

87

=321541/2121

70

Quick asset ratio (Current assets-

inventories) / current

liabilities

=(346274-

192398)/

209253

=(328589-

194889)/

179287

=(321541-

184167)/

212170

Gearing ratio

Debt to asset ratio Total debt/total assets =258836/5866

74*100

=239753/5524

19*100

=234249/5486

37*100

Gearing ratio Non-current liabilities/

(non-current liabilities +

Equity)*100

=49583/

(49583+32783

8)*100

=60466/

(60466+31266

6)*100

=22079/

(22079+31438

8)*100

Asset turnover Net sales/ Average total

asset

=1195967/

((586674+5524

19)/2)

=1112630/

((552419+5486

37)/2)

=1069392/

((548637+549

221)/2)

Asset turnover in

days

365/asset turnover ratio =365/2.10 =365/2.02 =365/1.95

Liquidity ratio

Current ratio Current assets / current

liabilities

=346274/2092

53

=328589/1792

87

=321541/2121

70

Quick asset ratio (Current assets-

inventories) / current

liabilities

=(346274-

192398)/

209253

=(328589-

194889)/

179287

=(321541-

184167)/

212170

Gearing ratio

Debt to asset ratio Total debt/total assets =258836/5866

74*100

=239753/5524

19*100

=234249/5486

37*100

Gearing ratio Non-current liabilities/

(non-current liabilities +

Equity)*100

=49583/

(49583+32783

8)*100

=60466/

(60466+31266

6)*100

=22079/

(22079+31438

8)*100

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.