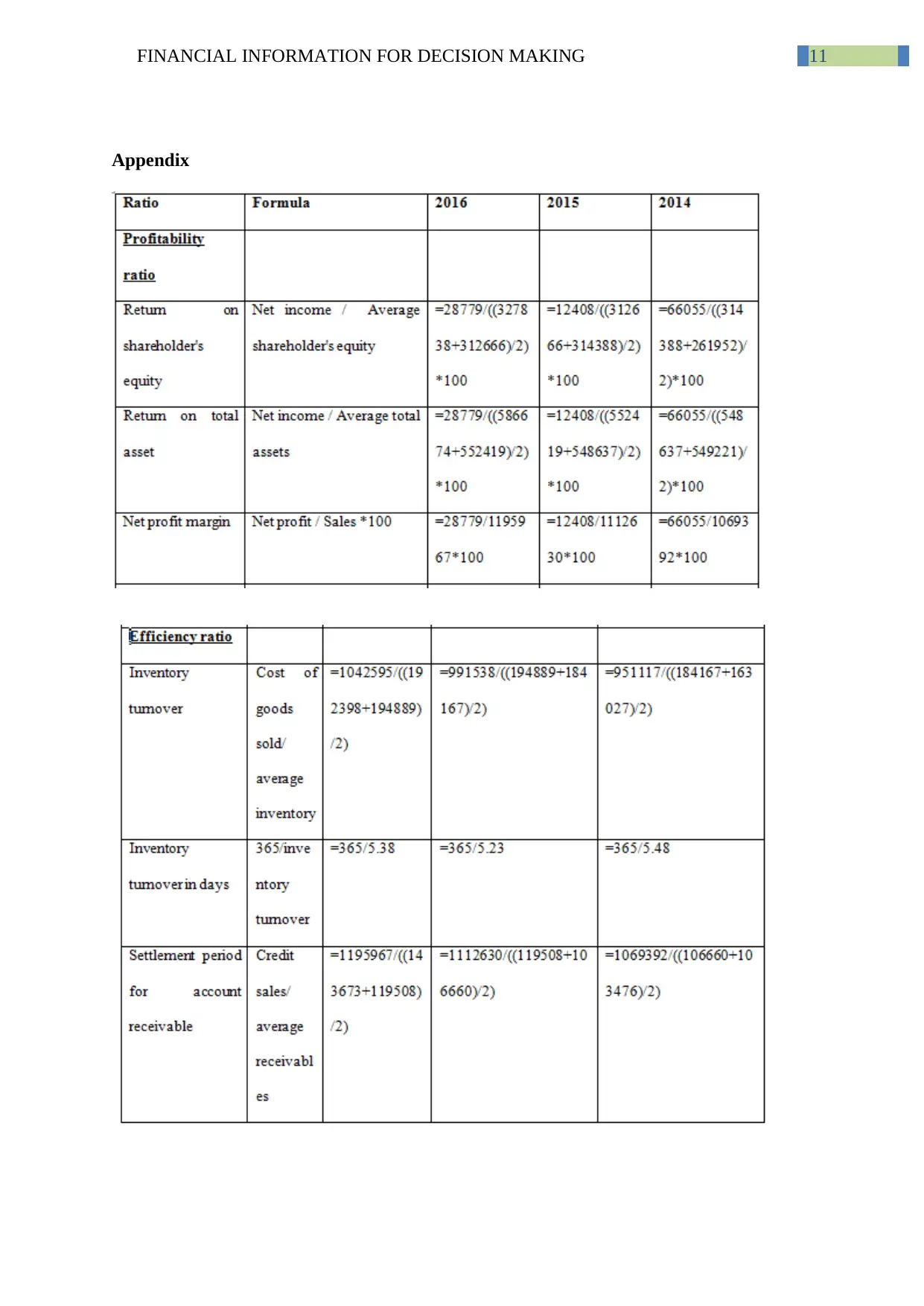

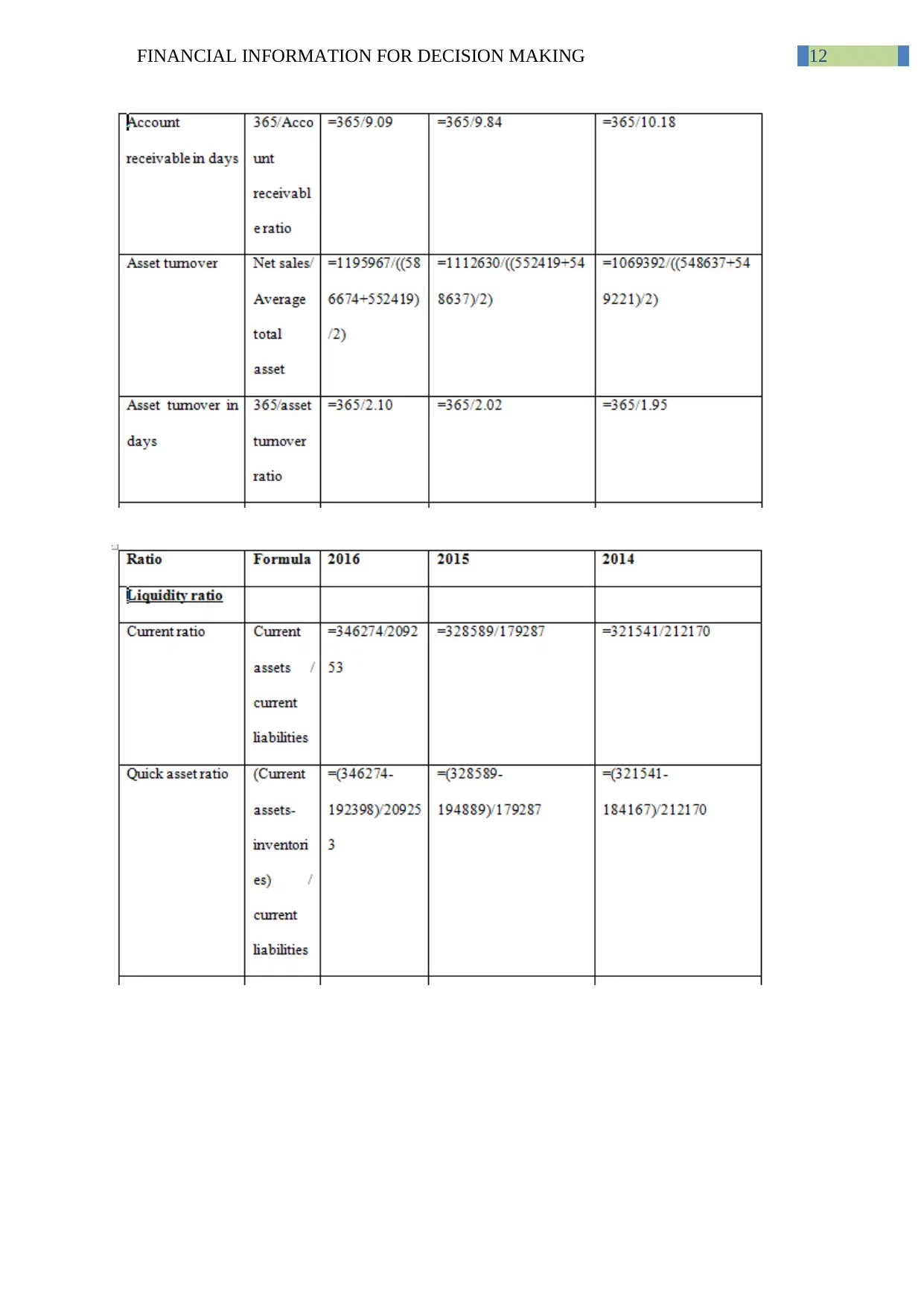

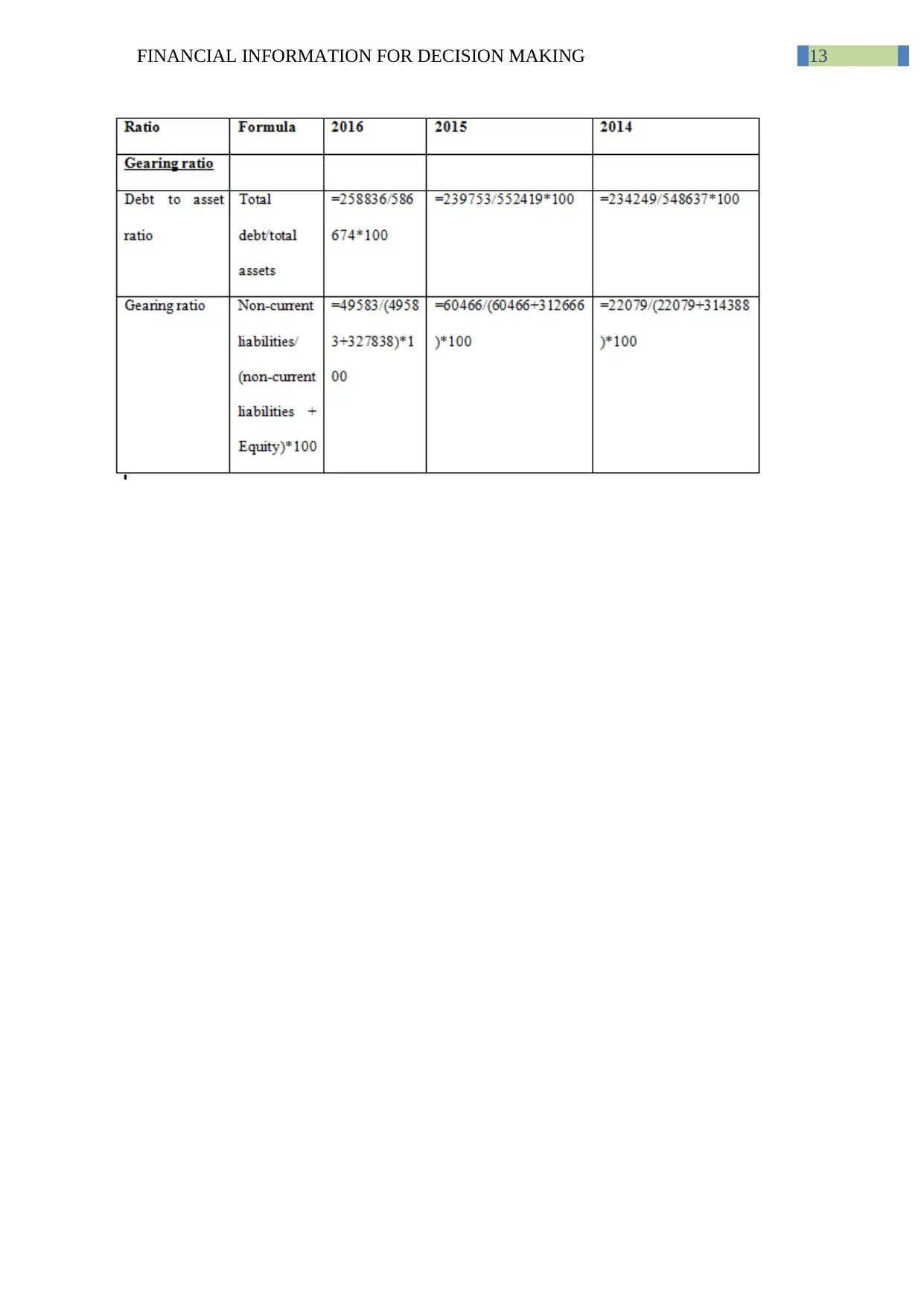

The report analyses the financial performance of Bega Cheese Limited through measuring the efficiency ratios, profitability ratios, gearing ratios and liquidity ratios over the years from 2014 to 2016. The report reveals that the company is capable in generating return, collecting of dues and paying off the short-term obligations. However, the profitability ratios of the company have been decreased from the year 2014 to 2015 though it was able to improve the profitability position in the year 2016. Further, the company was efficient with regard to its efficiency ratios undertaken for analysing its efficiency. The liquid ratio of the company is representing that the company is capable in paying-off its short-term obligation. However, the gearing ratios of the company are revealing that the leverage position of the company is deteriorating.

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)