Financial Interpretation Report: Cochlear Ltd Performance Analysis

VerifiedAdded on 2022/11/28

|12

|2732

|253

Report

AI Summary

This report presents a comprehensive financial interpretation of Cochlear Ltd, analyzing its performance from 2014 to 2018. The analysis includes a detailed examination of profitability ratios (gross profit margin, net profit margin, asset turnover, and return on equity), operational ratios (accounts receivable turnover, inventory turnover), liquidity ratios (current ratio, quick ratio), solvency ratios (debt-to-equity ratio, financial leverage), and market performance ratios. The report compares Cochlear Ltd's financial metrics with industry averages and assesses trends to provide insights into the company's efficiency, solvency, and overall financial health. The report also discusses the company's strategic management, credit policies, and inventory management in relation to its financial performance.

Running head: FINANCIAL INTERPRETATION

Financial Interpretation

Name of the Student:

Name of the University:

Author’s Note:

Financial Interpretation

Name of the Student:

Name of the University:

Author’s Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1FINANCIAL INTERPRETATION

Table of Contents

Trend and Cross Sectional Financial Analysis................................................................................2

Profitability Ratio........................................................................................................................2

Operational Ratio.........................................................................................................................4

Liquidity Ratio.............................................................................................................................6

Solvency Ratio.............................................................................................................................7

Market Performance Ratio...........................................................................................................8

References......................................................................................................................................10

Table of Contents

Trend and Cross Sectional Financial Analysis................................................................................2

Profitability Ratio........................................................................................................................2

Operational Ratio.........................................................................................................................4

Liquidity Ratio.............................................................................................................................6

Solvency Ratio.............................................................................................................................7

Market Performance Ratio...........................................................................................................8

References......................................................................................................................................10

2FINANCIAL INTERPRETATION

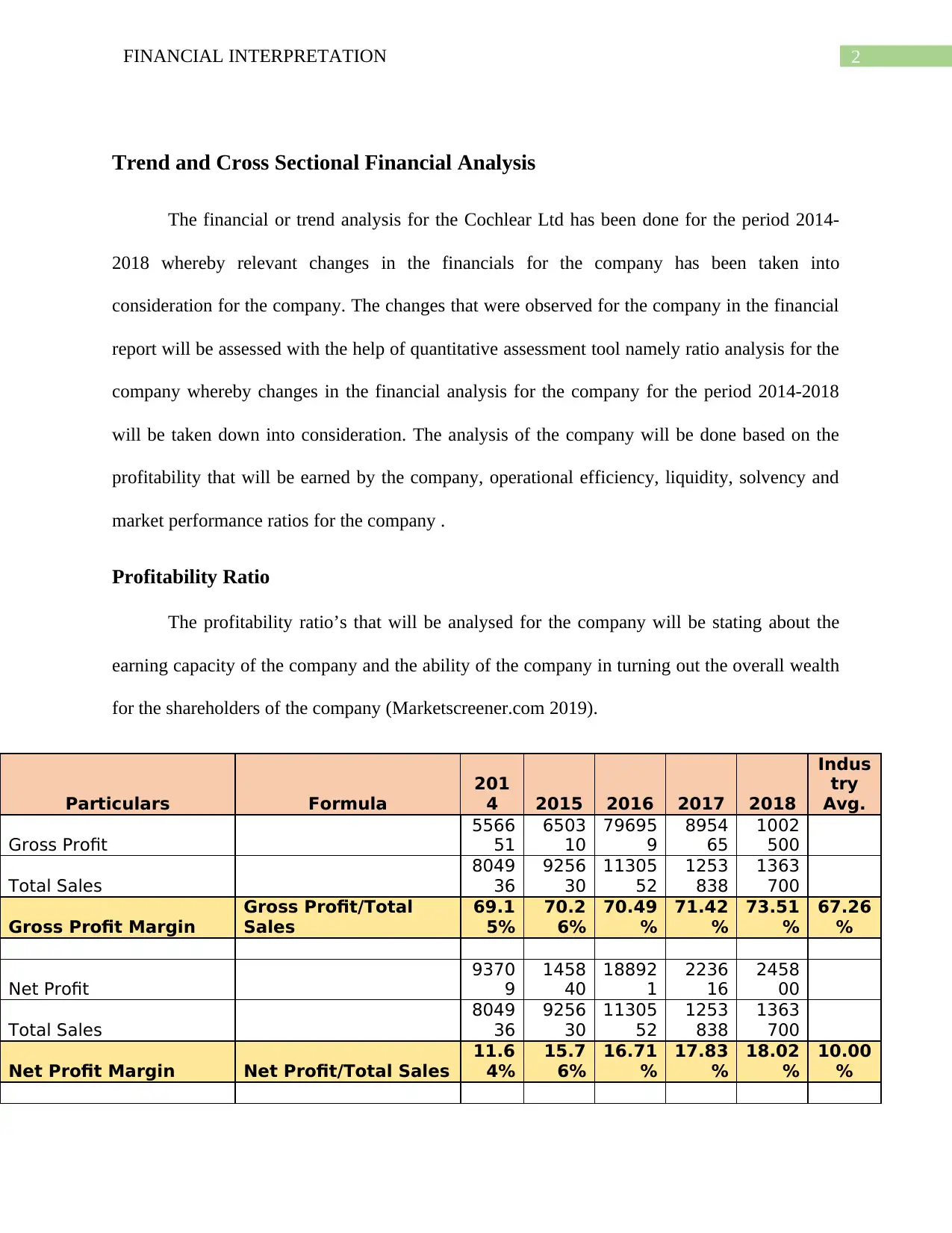

Trend and Cross Sectional Financial Analysis

The financial or trend analysis for the Cochlear Ltd has been done for the period 2014-

2018 whereby relevant changes in the financials for the company has been taken into

consideration for the company. The changes that were observed for the company in the financial

report will be assessed with the help of quantitative assessment tool namely ratio analysis for the

company whereby changes in the financial analysis for the company for the period 2014-2018

will be taken down into consideration. The analysis of the company will be done based on the

profitability that will be earned by the company, operational efficiency, liquidity, solvency and

market performance ratios for the company .

Profitability Ratio

The profitability ratio’s that will be analysed for the company will be stating about the

earning capacity of the company and the ability of the company in turning out the overall wealth

for the shareholders of the company (Marketscreener.com 2019).

Particulars Formula

201

4 2015 2016 2017 2018

Indus

try

Avg.

Gross Profit

5566

51

6503

10

79695

9

8954

65

1002

500

Total Sales

8049

36

9256

30

11305

52

1253

838

1363

700

Gross Profit Margin

Gross Profit/Total

Sales

69.1

5%

70.2

6%

70.49

%

71.42

%

73.51

%

67.26

%

Net Profit

9370

9

1458

40

18892

1

2236

16

2458

00

Total Sales

8049

36

9256

30

11305

52

1253

838

1363

700

Net Profit Margin Net Profit/Total Sales

11.6

4%

15.7

6%

16.71

%

17.83

%

18.02

%

10.00

%

Trend and Cross Sectional Financial Analysis

The financial or trend analysis for the Cochlear Ltd has been done for the period 2014-

2018 whereby relevant changes in the financials for the company has been taken into

consideration for the company. The changes that were observed for the company in the financial

report will be assessed with the help of quantitative assessment tool namely ratio analysis for the

company whereby changes in the financial analysis for the company for the period 2014-2018

will be taken down into consideration. The analysis of the company will be done based on the

profitability that will be earned by the company, operational efficiency, liquidity, solvency and

market performance ratios for the company .

Profitability Ratio

The profitability ratio’s that will be analysed for the company will be stating about the

earning capacity of the company and the ability of the company in turning out the overall wealth

for the shareholders of the company (Marketscreener.com 2019).

Particulars Formula

201

4 2015 2016 2017 2018

Indus

try

Avg.

Gross Profit

5566

51

6503

10

79695

9

8954

65

1002

500

Total Sales

8049

36

9256

30

11305

52

1253

838

1363

700

Gross Profit Margin

Gross Profit/Total

Sales

69.1

5%

70.2

6%

70.49

%

71.42

%

73.51

%

67.26

%

Net Profit

9370

9

1458

40

18892

1

2236

16

2458

00

Total Sales

8049

36

9256

30

11305

52

1253

838

1363

700

Net Profit Margin Net Profit/Total Sales

11.6

4%

15.7

6%

16.71

%

17.83

%

18.02

%

10.00

%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3FINANCIAL INTERPRETATION

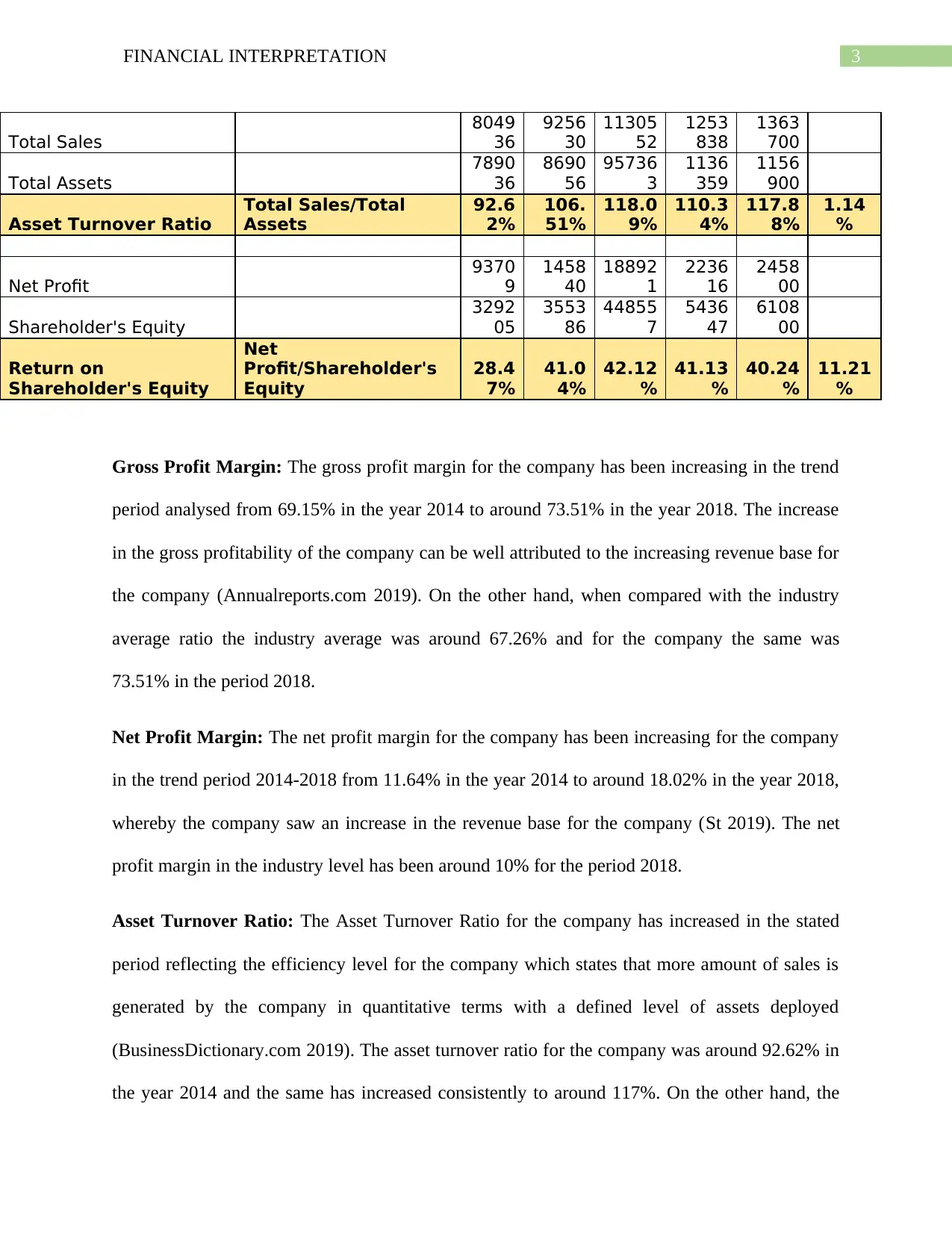

Total Sales

8049

36

9256

30

11305

52

1253

838

1363

700

Total Assets

7890

36

8690

56

95736

3

1136

359

1156

900

Asset Turnover Ratio

Total Sales/Total

Assets

92.6

2%

106.

51%

118.0

9%

110.3

4%

117.8

8%

1.14

%

Net Profit

9370

9

1458

40

18892

1

2236

16

2458

00

Shareholder's Equity

3292

05

3553

86

44855

7

5436

47

6108

00

Return on

Shareholder's Equity

Net

Profit/Shareholder's

Equity

28.4

7%

41.0

4%

42.12

%

41.13

%

40.24

%

11.21

%

Gross Profit Margin: The gross profit margin for the company has been increasing in the trend

period analysed from 69.15% in the year 2014 to around 73.51% in the year 2018. The increase

in the gross profitability of the company can be well attributed to the increasing revenue base for

the company (Annualreports.com 2019). On the other hand, when compared with the industry

average ratio the industry average was around 67.26% and for the company the same was

73.51% in the period 2018.

Net Profit Margin: The net profit margin for the company has been increasing for the company

in the trend period 2014-2018 from 11.64% in the year 2014 to around 18.02% in the year 2018,

whereby the company saw an increase in the revenue base for the company (St 2019). The net

profit margin in the industry level has been around 10% for the period 2018.

Asset Turnover Ratio: The Asset Turnover Ratio for the company has increased in the stated

period reflecting the efficiency level for the company which states that more amount of sales is

generated by the company in quantitative terms with a defined level of assets deployed

(BusinessDictionary.com 2019). The asset turnover ratio for the company was around 92.62% in

the year 2014 and the same has increased consistently to around 117%. On the other hand, the

Total Sales

8049

36

9256

30

11305

52

1253

838

1363

700

Total Assets

7890

36

8690

56

95736

3

1136

359

1156

900

Asset Turnover Ratio

Total Sales/Total

Assets

92.6

2%

106.

51%

118.0

9%

110.3

4%

117.8

8%

1.14

%

Net Profit

9370

9

1458

40

18892

1

2236

16

2458

00

Shareholder's Equity

3292

05

3553

86

44855

7

5436

47

6108

00

Return on

Shareholder's Equity

Net

Profit/Shareholder's

Equity

28.4

7%

41.0

4%

42.12

%

41.13

%

40.24

%

11.21

%

Gross Profit Margin: The gross profit margin for the company has been increasing in the trend

period analysed from 69.15% in the year 2014 to around 73.51% in the year 2018. The increase

in the gross profitability of the company can be well attributed to the increasing revenue base for

the company (Annualreports.com 2019). On the other hand, when compared with the industry

average ratio the industry average was around 67.26% and for the company the same was

73.51% in the period 2018.

Net Profit Margin: The net profit margin for the company has been increasing for the company

in the trend period 2014-2018 from 11.64% in the year 2014 to around 18.02% in the year 2018,

whereby the company saw an increase in the revenue base for the company (St 2019). The net

profit margin in the industry level has been around 10% for the period 2018.

Asset Turnover Ratio: The Asset Turnover Ratio for the company has increased in the stated

period reflecting the efficiency level for the company which states that more amount of sales is

generated by the company in quantitative terms with a defined level of assets deployed

(BusinessDictionary.com 2019). The asset turnover ratio for the company was around 92.62% in

the year 2014 and the same has increased consistently to around 117%. On the other hand, the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4FINANCIAL INTERPRETATION

same for industry average ratio has been around 1.14% stating that the operational efficiency

from the view point of company is comparatively better carried out.

Return on Shareholder’s Equity: The return generated on the equity shareholders for the

company has been much more consistent where the overall return generated for the shareholders

of the company has increased from 28% to around 40% in the trend period 2014-2018. On the

other hand, the industry average has been just around 11% and the consistent increase in the

profitability and wealth creation can be attributed to the strategic management in terms of

product diversification and increase in the overall customer base.

Operational Ratio

The operational ratio for the company has been analysed in order to view and analyse the

various activities undertaken by the company and the undertaken results achieved by the

company.

Operating Ratio

Particulars Formula 2014 2015 2016 2017 2018

Indus

try

Avg.

Total Sales

8049

36

9256

30

11305

52

12538

38

13637

00

Accounts Receivables

2103

94

2367

28

28046

8

29306

4

30900

0

Accounts Receivable

Turnover Ratio

Total Sales/Accounts

Receivable 3.83 3.91 4.03 4.28 4.41 5

No of Days in Year 365 365 365 365 365 365

Accounts Receivable

Turnover Ratio 3.83 3.91 4.03 4.28 4.41 5

Average No of Days

Receivable

Outstanding

No of Days/Accounts

Receivable Turnover 95 93 91 85 83 73

Cost of Goods Sold

2482

85

2753

20

33359

3

35837

3

36120

0

Inventory 1286 1458 15410 16001 16740

same for industry average ratio has been around 1.14% stating that the operational efficiency

from the view point of company is comparatively better carried out.

Return on Shareholder’s Equity: The return generated on the equity shareholders for the

company has been much more consistent where the overall return generated for the shareholders

of the company has increased from 28% to around 40% in the trend period 2014-2018. On the

other hand, the industry average has been just around 11% and the consistent increase in the

profitability and wealth creation can be attributed to the strategic management in terms of

product diversification and increase in the overall customer base.

Operational Ratio

The operational ratio for the company has been analysed in order to view and analyse the

various activities undertaken by the company and the undertaken results achieved by the

company.

Operating Ratio

Particulars Formula 2014 2015 2016 2017 2018

Indus

try

Avg.

Total Sales

8049

36

9256

30

11305

52

12538

38

13637

00

Accounts Receivables

2103

94

2367

28

28046

8

29306

4

30900

0

Accounts Receivable

Turnover Ratio

Total Sales/Accounts

Receivable 3.83 3.91 4.03 4.28 4.41 5

No of Days in Year 365 365 365 365 365 365

Accounts Receivable

Turnover Ratio 3.83 3.91 4.03 4.28 4.41 5

Average No of Days

Receivable

Outstanding

No of Days/Accounts

Receivable Turnover 95 93 91 85 83 73

Cost of Goods Sold

2482

85

2753

20

33359

3

35837

3

36120

0

Inventory 1286 1458 15410 16001 16740

5FINANCIAL INTERPRETATION

13 61 3 1 0

Inventory Turnover

Ratio

Cost of Goods

Sold/Inventory 1.93 1.89 2.16 2.24 2.16 2.33

No of Days in Year 365 365 365 365 365 365

Inventory Turnover Ratio 1.93 1.89 2.16 2.24 2.16 2.33

Average No of Days

Inventory in Stock

No of Days/Inventory

Turnover Ratio 189 193 169 163 169 157

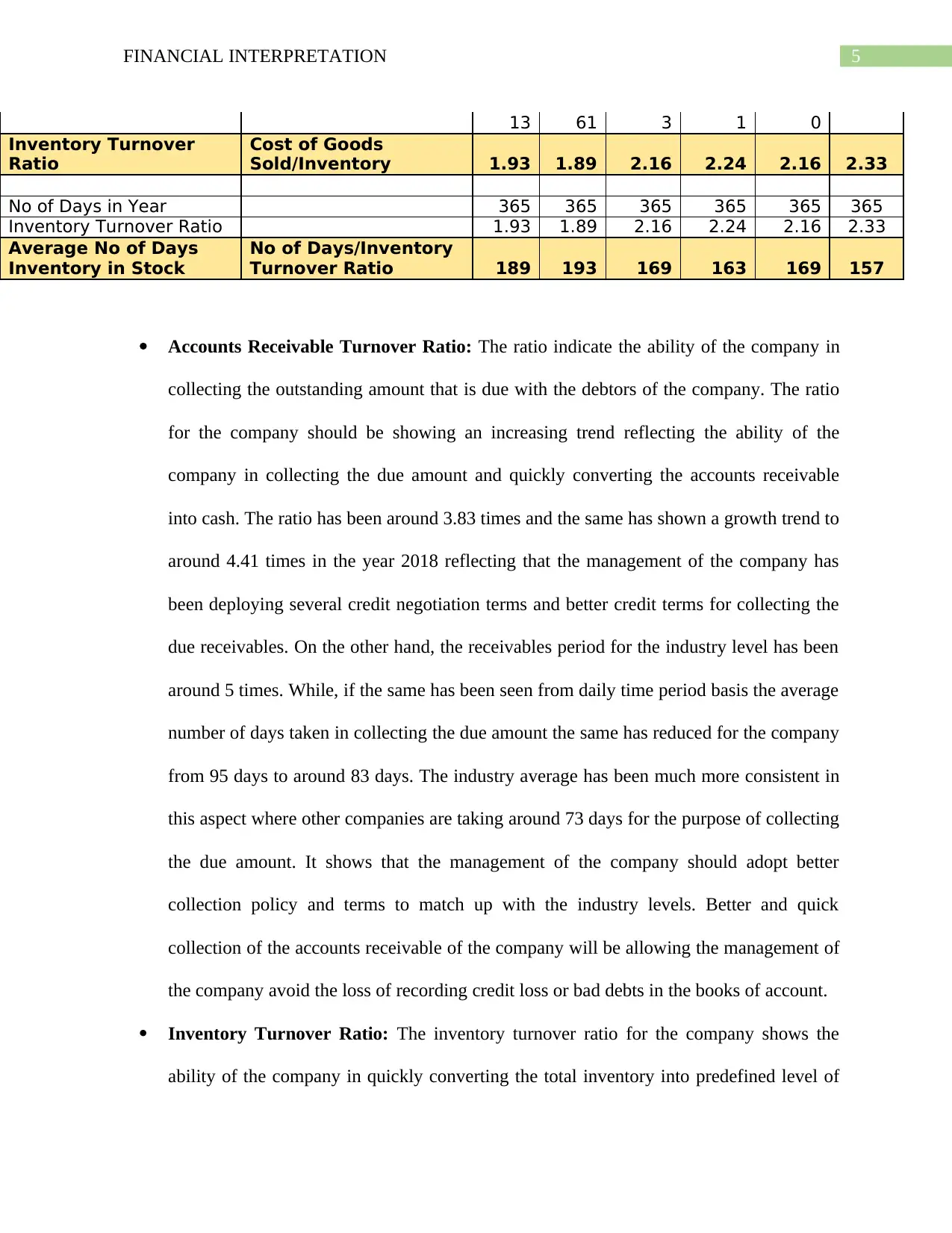

Accounts Receivable Turnover Ratio: The ratio indicate the ability of the company in

collecting the outstanding amount that is due with the debtors of the company. The ratio

for the company should be showing an increasing trend reflecting the ability of the

company in collecting the due amount and quickly converting the accounts receivable

into cash. The ratio has been around 3.83 times and the same has shown a growth trend to

around 4.41 times in the year 2018 reflecting that the management of the company has

been deploying several credit negotiation terms and better credit terms for collecting the

due receivables. On the other hand, the receivables period for the industry level has been

around 5 times. While, if the same has been seen from daily time period basis the average

number of days taken in collecting the due amount the same has reduced for the company

from 95 days to around 83 days. The industry average has been much more consistent in

this aspect where other companies are taking around 73 days for the purpose of collecting

the due amount. It shows that the management of the company should adopt better

collection policy and terms to match up with the industry levels. Better and quick

collection of the accounts receivable of the company will be allowing the management of

the company avoid the loss of recording credit loss or bad debts in the books of account.

Inventory Turnover Ratio: The inventory turnover ratio for the company shows the

ability of the company in quickly converting the total inventory into predefined level of

13 61 3 1 0

Inventory Turnover

Ratio

Cost of Goods

Sold/Inventory 1.93 1.89 2.16 2.24 2.16 2.33

No of Days in Year 365 365 365 365 365 365

Inventory Turnover Ratio 1.93 1.89 2.16 2.24 2.16 2.33

Average No of Days

Inventory in Stock

No of Days/Inventory

Turnover Ratio 189 193 169 163 169 157

Accounts Receivable Turnover Ratio: The ratio indicate the ability of the company in

collecting the outstanding amount that is due with the debtors of the company. The ratio

for the company should be showing an increasing trend reflecting the ability of the

company in collecting the due amount and quickly converting the accounts receivable

into cash. The ratio has been around 3.83 times and the same has shown a growth trend to

around 4.41 times in the year 2018 reflecting that the management of the company has

been deploying several credit negotiation terms and better credit terms for collecting the

due receivables. On the other hand, the receivables period for the industry level has been

around 5 times. While, if the same has been seen from daily time period basis the average

number of days taken in collecting the due amount the same has reduced for the company

from 95 days to around 83 days. The industry average has been much more consistent in

this aspect where other companies are taking around 73 days for the purpose of collecting

the due amount. It shows that the management of the company should adopt better

collection policy and terms to match up with the industry levels. Better and quick

collection of the accounts receivable of the company will be allowing the management of

the company avoid the loss of recording credit loss or bad debts in the books of account.

Inventory Turnover Ratio: The inventory turnover ratio for the company shows the

ability of the company in quickly converting the total inventory into predefined level of

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6FINANCIAL INTERPRETATION

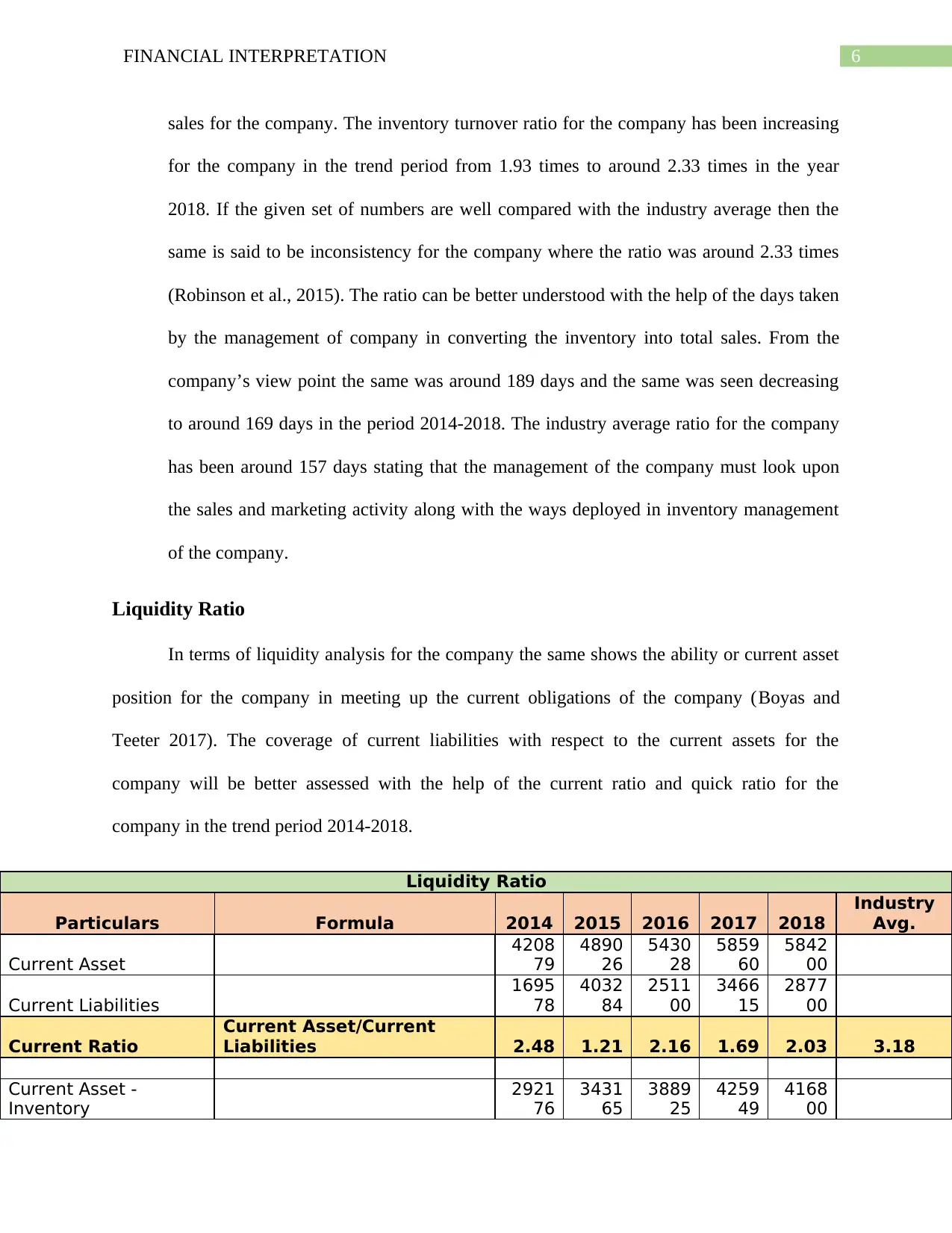

sales for the company. The inventory turnover ratio for the company has been increasing

for the company in the trend period from 1.93 times to around 2.33 times in the year

2018. If the given set of numbers are well compared with the industry average then the

same is said to be inconsistency for the company where the ratio was around 2.33 times

(Robinson et al., 2015). The ratio can be better understood with the help of the days taken

by the management of company in converting the inventory into total sales. From the

company’s view point the same was around 189 days and the same was seen decreasing

to around 169 days in the period 2014-2018. The industry average ratio for the company

has been around 157 days stating that the management of the company must look upon

the sales and marketing activity along with the ways deployed in inventory management

of the company.

Liquidity Ratio

In terms of liquidity analysis for the company the same shows the ability or current asset

position for the company in meeting up the current obligations of the company (Boyas and

Teeter 2017). The coverage of current liabilities with respect to the current assets for the

company will be better assessed with the help of the current ratio and quick ratio for the

company in the trend period 2014-2018.

Liquidity Ratio

Particulars Formula 2014 2015 2016 2017 2018

Industry

Avg.

Current Asset

4208

79

4890

26

5430

28

5859

60

5842

00

Current Liabilities

1695

78

4032

84

2511

00

3466

15

2877

00

Current Ratio

Current Asset/Current

Liabilities 2.48 1.21 2.16 1.69 2.03 3.18

Current Asset -

Inventory

2921

76

3431

65

3889

25

4259

49

4168

00

sales for the company. The inventory turnover ratio for the company has been increasing

for the company in the trend period from 1.93 times to around 2.33 times in the year

2018. If the given set of numbers are well compared with the industry average then the

same is said to be inconsistency for the company where the ratio was around 2.33 times

(Robinson et al., 2015). The ratio can be better understood with the help of the days taken

by the management of company in converting the inventory into total sales. From the

company’s view point the same was around 189 days and the same was seen decreasing

to around 169 days in the period 2014-2018. The industry average ratio for the company

has been around 157 days stating that the management of the company must look upon

the sales and marketing activity along with the ways deployed in inventory management

of the company.

Liquidity Ratio

In terms of liquidity analysis for the company the same shows the ability or current asset

position for the company in meeting up the current obligations of the company (Boyas and

Teeter 2017). The coverage of current liabilities with respect to the current assets for the

company will be better assessed with the help of the current ratio and quick ratio for the

company in the trend period 2014-2018.

Liquidity Ratio

Particulars Formula 2014 2015 2016 2017 2018

Industry

Avg.

Current Asset

4208

79

4890

26

5430

28

5859

60

5842

00

Current Liabilities

1695

78

4032

84

2511

00

3466

15

2877

00

Current Ratio

Current Asset/Current

Liabilities 2.48 1.21 2.16 1.69 2.03 3.18

Current Asset -

Inventory

2921

76

3431

65

3889

25

4259

49

4168

00

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7FINANCIAL INTERPRETATION

Current Liabilities

1695

78

4032

84

2511

00

3466

15

2877

00

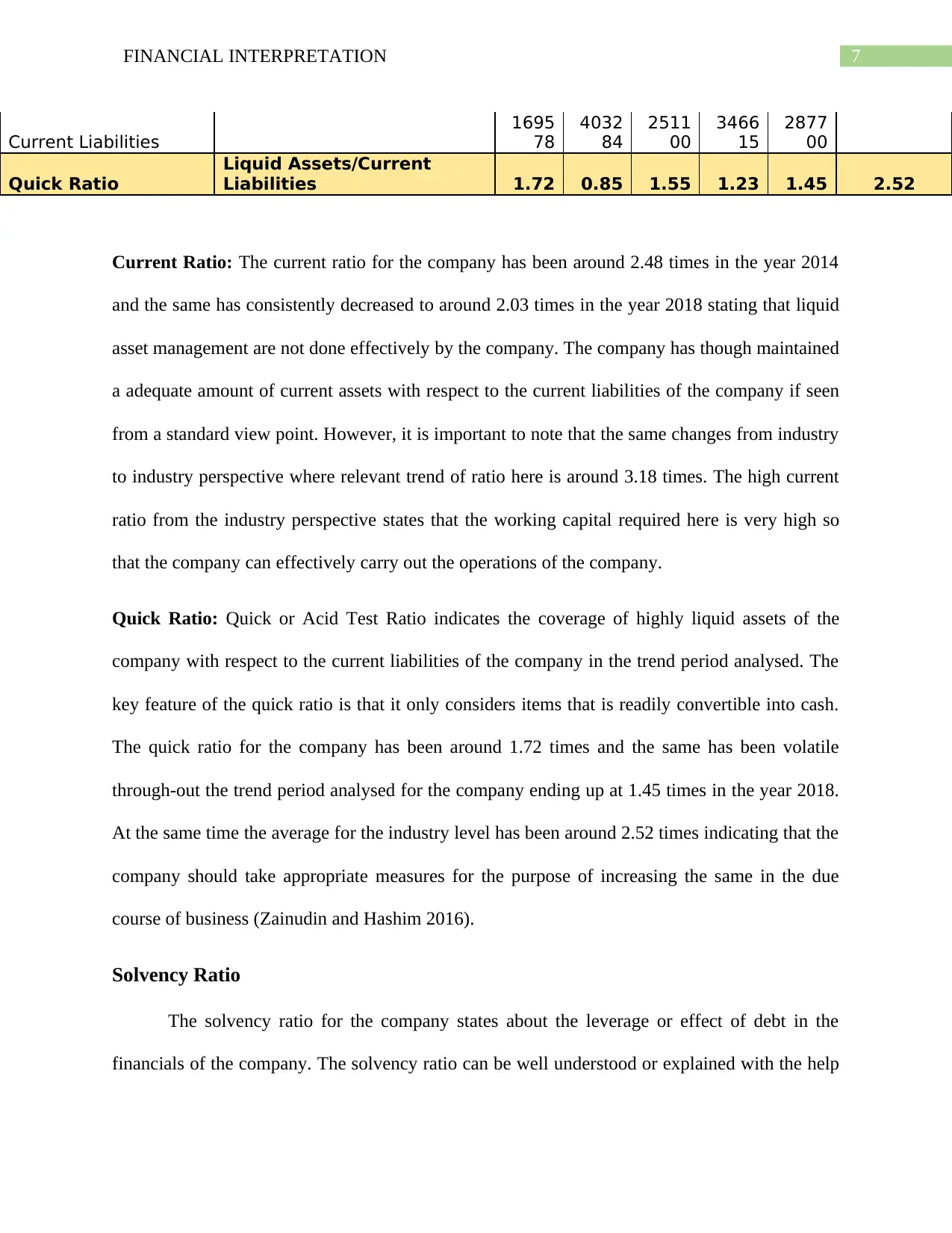

Quick Ratio

Liquid Assets/Current

Liabilities 1.72 0.85 1.55 1.23 1.45 2.52

Current Ratio: The current ratio for the company has been around 2.48 times in the year 2014

and the same has consistently decreased to around 2.03 times in the year 2018 stating that liquid

asset management are not done effectively by the company. The company has though maintained

a adequate amount of current assets with respect to the current liabilities of the company if seen

from a standard view point. However, it is important to note that the same changes from industry

to industry perspective where relevant trend of ratio here is around 3.18 times. The high current

ratio from the industry perspective states that the working capital required here is very high so

that the company can effectively carry out the operations of the company.

Quick Ratio: Quick or Acid Test Ratio indicates the coverage of highly liquid assets of the

company with respect to the current liabilities of the company in the trend period analysed. The

key feature of the quick ratio is that it only considers items that is readily convertible into cash.

The quick ratio for the company has been around 1.72 times and the same has been volatile

through-out the trend period analysed for the company ending up at 1.45 times in the year 2018.

At the same time the average for the industry level has been around 2.52 times indicating that the

company should take appropriate measures for the purpose of increasing the same in the due

course of business (Zainudin and Hashim 2016).

Solvency Ratio

The solvency ratio for the company states about the leverage or effect of debt in the

financials of the company. The solvency ratio can be well understood or explained with the help

Current Liabilities

1695

78

4032

84

2511

00

3466

15

2877

00

Quick Ratio

Liquid Assets/Current

Liabilities 1.72 0.85 1.55 1.23 1.45 2.52

Current Ratio: The current ratio for the company has been around 2.48 times in the year 2014

and the same has consistently decreased to around 2.03 times in the year 2018 stating that liquid

asset management are not done effectively by the company. The company has though maintained

a adequate amount of current assets with respect to the current liabilities of the company if seen

from a standard view point. However, it is important to note that the same changes from industry

to industry perspective where relevant trend of ratio here is around 3.18 times. The high current

ratio from the industry perspective states that the working capital required here is very high so

that the company can effectively carry out the operations of the company.

Quick Ratio: Quick or Acid Test Ratio indicates the coverage of highly liquid assets of the

company with respect to the current liabilities of the company in the trend period analysed. The

key feature of the quick ratio is that it only considers items that is readily convertible into cash.

The quick ratio for the company has been around 1.72 times and the same has been volatile

through-out the trend period analysed for the company ending up at 1.45 times in the year 2018.

At the same time the average for the industry level has been around 2.52 times indicating that the

company should take appropriate measures for the purpose of increasing the same in the due

course of business (Zainudin and Hashim 2016).

Solvency Ratio

The solvency ratio for the company states about the leverage or effect of debt in the

financials of the company. The solvency ratio can be well understood or explained with the help

8FINANCIAL INTERPRETATION

of the coverage of equity and assets with respect to debt levels presented in the financials of the

company (Rodrigues and Rodrigues 2018).

Solvency Ratio

Particulars Formula 2014 2015 2016 2017 2018

Industry

Avg.

Long-Term

Debt

2342

74

4455

2

1892

60

13423

5

14400

0

Shareholder's

Equity

3292

05

3553

86

4485

57

54364

7

61080

0

Debt to

Equity Ratio

Long Term

Debt/Shareholder Equity

71.1

6%

12.5

4%

42.1

9%

24.69

%

23.58

% 27.00%

Total Assets

7890

36

8690

56

9573

63

11363

59

11569

00

Shareholder's

Equity

3292

05

3553

86

4485

57

54364

7

61080

0

Financial

Leverage

Total Asset/Shareholder

Equity 2.64 2.45 2.13 2.09 1.89 2.00

Debt to Equity Ratio: The debt to equity ratio for the company has been around 71.16% in the

year 2014 and the same has reduced to a significant level to around 23.58% which is well

adhered to the industry levels that stands around to 27%. High levels of debt in the financials of

the company can increase the financial risk of the company affecting the operations of the

company and the overall risk associated with the company. The company in the year 2018-2019

has stated that they do undertake the importance of the debt levels in the company and they

would be deploying various courses of actions for the better management of financing sources

and there consequences on the overall capital structure of the company (Rey and Santelli 2017).

Financial Leverage: The financial leverage ratio for the company shows the proportion of

equity finance that is responsible for the present asset that is included with the company. The

Ratio has been around 2.64 times in the year 2014 and the same has consistently decreased to

around 1.89 times in the year 2018 stating that the management of the company has increased the

of the coverage of equity and assets with respect to debt levels presented in the financials of the

company (Rodrigues and Rodrigues 2018).

Solvency Ratio

Particulars Formula 2014 2015 2016 2017 2018

Industry

Avg.

Long-Term

Debt

2342

74

4455

2

1892

60

13423

5

14400

0

Shareholder's

Equity

3292

05

3553

86

4485

57

54364

7

61080

0

Debt to

Equity Ratio

Long Term

Debt/Shareholder Equity

71.1

6%

12.5

4%

42.1

9%

24.69

%

23.58

% 27.00%

Total Assets

7890

36

8690

56

9573

63

11363

59

11569

00

Shareholder's

Equity

3292

05

3553

86

4485

57

54364

7

61080

0

Financial

Leverage

Total Asset/Shareholder

Equity 2.64 2.45 2.13 2.09 1.89 2.00

Debt to Equity Ratio: The debt to equity ratio for the company has been around 71.16% in the

year 2014 and the same has reduced to a significant level to around 23.58% which is well

adhered to the industry levels that stands around to 27%. High levels of debt in the financials of

the company can increase the financial risk of the company affecting the operations of the

company and the overall risk associated with the company. The company in the year 2018-2019

has stated that they do undertake the importance of the debt levels in the company and they

would be deploying various courses of actions for the better management of financing sources

and there consequences on the overall capital structure of the company (Rey and Santelli 2017).

Financial Leverage: The financial leverage ratio for the company shows the proportion of

equity finance that is responsible for the present asset that is included with the company. The

Ratio has been around 2.64 times in the year 2014 and the same has consistently decreased to

around 1.89 times in the year 2018 stating that the management of the company has increased the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9FINANCIAL INTERPRETATION

value of equity with respect to equity level in the company (Lee, Lin and Shin 2018). While, if

the same is considered from an industry average perspective the company has done effectively

well as the industry average turns out to be around 2.00 times that is currently higher than that of

company ratio (COH 2019).

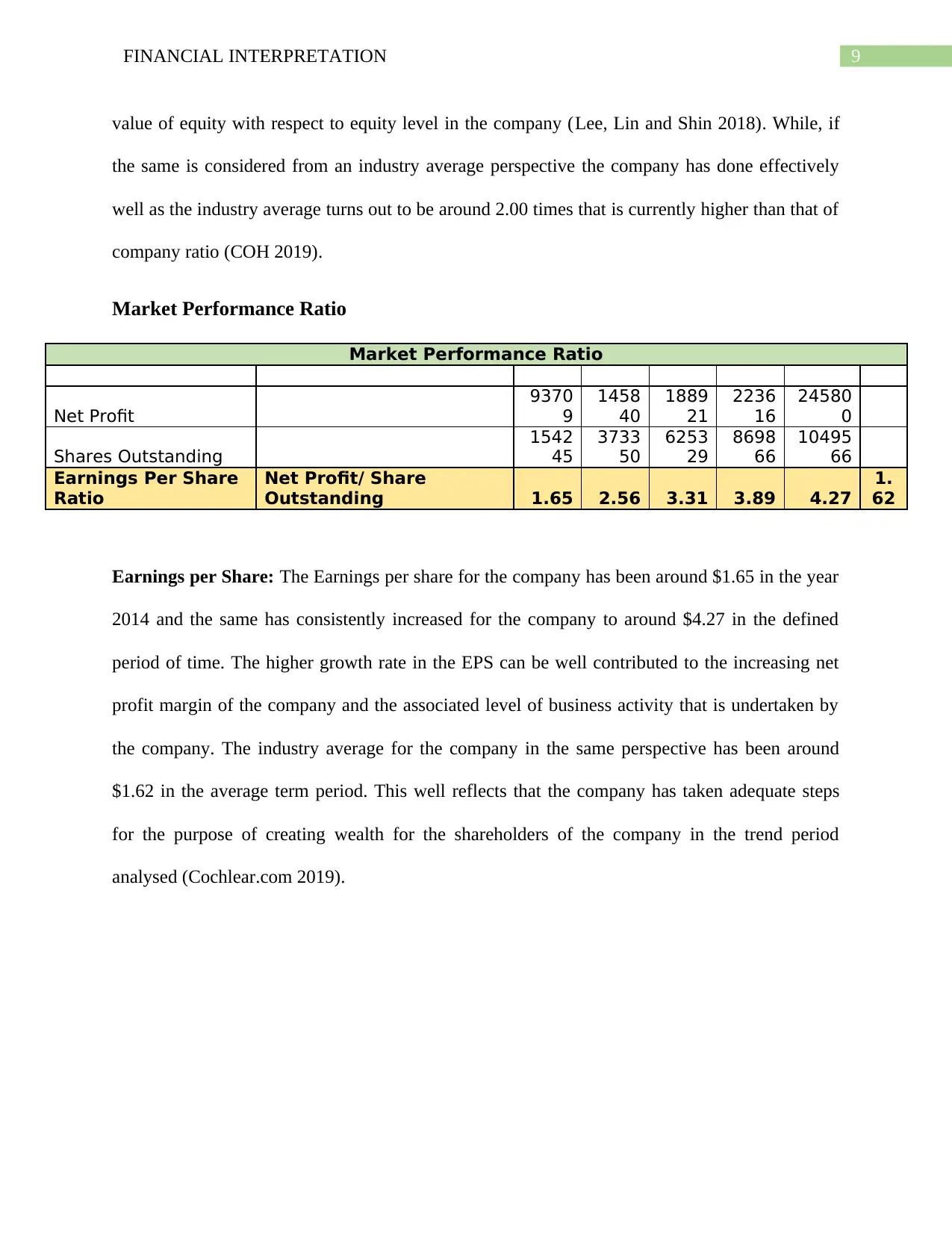

Market Performance Ratio

Market Performance Ratio

Net Profit

9370

9

1458

40

1889

21

2236

16

24580

0

Shares Outstanding

1542

45

3733

50

6253

29

8698

66

10495

66

Earnings Per Share

Ratio

Net Profit/ Share

Outstanding 1.65 2.56 3.31 3.89 4.27

1.

62

Earnings per Share: The Earnings per share for the company has been around $1.65 in the year

2014 and the same has consistently increased for the company to around $4.27 in the defined

period of time. The higher growth rate in the EPS can be well contributed to the increasing net

profit margin of the company and the associated level of business activity that is undertaken by

the company. The industry average for the company in the same perspective has been around

$1.62 in the average term period. This well reflects that the company has taken adequate steps

for the purpose of creating wealth for the shareholders of the company in the trend period

analysed (Cochlear.com 2019).

value of equity with respect to equity level in the company (Lee, Lin and Shin 2018). While, if

the same is considered from an industry average perspective the company has done effectively

well as the industry average turns out to be around 2.00 times that is currently higher than that of

company ratio (COH 2019).

Market Performance Ratio

Market Performance Ratio

Net Profit

9370

9

1458

40

1889

21

2236

16

24580

0

Shares Outstanding

1542

45

3733

50

6253

29

8698

66

10495

66

Earnings Per Share

Ratio

Net Profit/ Share

Outstanding 1.65 2.56 3.31 3.89 4.27

1.

62

Earnings per Share: The Earnings per share for the company has been around $1.65 in the year

2014 and the same has consistently increased for the company to around $4.27 in the defined

period of time. The higher growth rate in the EPS can be well contributed to the increasing net

profit margin of the company and the associated level of business activity that is undertaken by

the company. The industry average for the company in the same perspective has been around

$1.62 in the average term period. This well reflects that the company has taken adequate steps

for the purpose of creating wealth for the shareholders of the company in the trend period

analysed (Cochlear.com 2019).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10FINANCIAL INTERPRETATION

References

(COH), C. 2019. Cochlear Ltd (COH) Financial Ratios. [online] Investing.com. Available at:

https://www.investing.com/equities/cochlear-limited-ratios [Accessed 8 Sep. 2019].

Annualreports.com. 2019. [online] Available at:

http://www.annualreports.com/HostedData/AnnualReports/PDF/ASX_COH_2018.pdf [Accessed

8 Sep. 2019].

Boyas, E. and Teeter, R., 2017. Teaching Financial Ratio Analysis using XBRL.

In Developments in Business Simulation and Experiential Learning: Proceedings of the Annual

ABSEL conference (Vol. 44, No. 1).

BusinessDictionary.com. 2019. What are operating ratios? definition and meaning. [online]

Available at: http://www.businessdictionary.com/definition/operating-ratios.html [Accessed 8

Sep. 2019].

Cochlear.com. 2019. [online] Available at: https://www.cochlear.com/2a3956c0-f09d-4ce7-

a8c9-8b0ddccf1999/en_corporate_annualreport2015_financial_1.54mb.pdf?

MOD=AJPERES&CONVERT_TO=url&CACHEID=ROOTWORKSPACE-

2a3956c0-f09d-4ce7-a8c9-8b0ddccf1999-l5rAnvz [Accessed 8 Sep. 2019].

Lee, P.T.W., Lin, C.W. and Shin, S.H., 2018. Financial performance evaluation of shipping

companies using entropy and grey relation analysis. In Multi-Criteria Decision Making in

Maritime Studies and Logistics (pp. 219-247). Springer, Cham.

References

(COH), C. 2019. Cochlear Ltd (COH) Financial Ratios. [online] Investing.com. Available at:

https://www.investing.com/equities/cochlear-limited-ratios [Accessed 8 Sep. 2019].

Annualreports.com. 2019. [online] Available at:

http://www.annualreports.com/HostedData/AnnualReports/PDF/ASX_COH_2018.pdf [Accessed

8 Sep. 2019].

Boyas, E. and Teeter, R., 2017. Teaching Financial Ratio Analysis using XBRL.

In Developments in Business Simulation and Experiential Learning: Proceedings of the Annual

ABSEL conference (Vol. 44, No. 1).

BusinessDictionary.com. 2019. What are operating ratios? definition and meaning. [online]

Available at: http://www.businessdictionary.com/definition/operating-ratios.html [Accessed 8

Sep. 2019].

Cochlear.com. 2019. [online] Available at: https://www.cochlear.com/2a3956c0-f09d-4ce7-

a8c9-8b0ddccf1999/en_corporate_annualreport2015_financial_1.54mb.pdf?

MOD=AJPERES&CONVERT_TO=url&CACHEID=ROOTWORKSPACE-

2a3956c0-f09d-4ce7-a8c9-8b0ddccf1999-l5rAnvz [Accessed 8 Sep. 2019].

Lee, P.T.W., Lin, C.W. and Shin, S.H., 2018. Financial performance evaluation of shipping

companies using entropy and grey relation analysis. In Multi-Criteria Decision Making in

Maritime Studies and Logistics (pp. 219-247). Springer, Cham.

11FINANCIAL INTERPRETATION

Marketscreener.com. 2019. COCHLEAR LIMITED : Financial Data Forecasts Estimates and

Expectations | COH | AU000000COH5 | MarketScreener. [online] Available at:

https://www.marketscreener.com/COCHLEAR-LIMITED-6491483/financials/ [Accessed 8 Sep.

2019].

Rey, A. and Santelli, F., 2017. The relationship between financial ratios and sporting

performance in Italy‟ s Serie A. International Journal of Business and Management, 12(12),

pp.53-63.

Robinson, T.R., Henry, E., Pirie, W.L. and Broihahn, M.A., 2015. International financial

statement analysis. John Wiley & Sons.

Rodrigues, L. and Rodrigues, L., 2018. Economic-financial performance of the Brazilian

sugarcane energy industry: An empirical evaluation using financial ratio, cluster and

discriminant analysis. Biomass and bioenergy, 108, pp.289-296.

St, S. 2019. Is Cochlear Limited (ASX:COH) A Financially Strong Company?. [online] Simply

Wall St. Available at: https://simplywall.st/stocks/au/healthcare/asx-coh/cochlear-shares/news/is-

cochlear-limited-asxcoh-a-financially-strong-company/ [Accessed 8 Sep. 2019].

Zainudin, E.F. and Hashim, H.A., 2016. Detecting fraudulent financial reporting using financial

ratio. Journal of Financial Reporting and Accounting, 14(2), pp.266-278.

Marketscreener.com. 2019. COCHLEAR LIMITED : Financial Data Forecasts Estimates and

Expectations | COH | AU000000COH5 | MarketScreener. [online] Available at:

https://www.marketscreener.com/COCHLEAR-LIMITED-6491483/financials/ [Accessed 8 Sep.

2019].

Rey, A. and Santelli, F., 2017. The relationship between financial ratios and sporting

performance in Italy‟ s Serie A. International Journal of Business and Management, 12(12),

pp.53-63.

Robinson, T.R., Henry, E., Pirie, W.L. and Broihahn, M.A., 2015. International financial

statement analysis. John Wiley & Sons.

Rodrigues, L. and Rodrigues, L., 2018. Economic-financial performance of the Brazilian

sugarcane energy industry: An empirical evaluation using financial ratio, cluster and

discriminant analysis. Biomass and bioenergy, 108, pp.289-296.

St, S. 2019. Is Cochlear Limited (ASX:COH) A Financially Strong Company?. [online] Simply

Wall St. Available at: https://simplywall.st/stocks/au/healthcare/asx-coh/cochlear-shares/news/is-

cochlear-limited-asxcoh-a-financially-strong-company/ [Accessed 8 Sep. 2019].

Zainudin, E.F. and Hashim, H.A., 2016. Detecting fraudulent financial reporting using financial

ratio. Journal of Financial Reporting and Accounting, 14(2), pp.266-278.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.