APC308 Financial Management Report: Dividend and Investment Analysis

VerifiedAdded on 2023/01/07

|12

|3060

|75

Report

AI Summary

This report delves into the core concepts of financial management, focusing on dividend policy and investment appraisal techniques. It begins by analyzing the factors influencing the size of annual dividends and the practical considerations involved in determining dividend payments, including the impact of different dividend options like cash and scrip dividends on shareholder ownership. The report then transitions to investment appraisal, exploring techniques such as payback period, net present value (NPV), accounting rate of return (ARR), and internal rate of return (IRR) to assess the suitability of investment options. It provides detailed calculations and discusses the benefits and limitations of each technique, offering a comprehensive understanding of financial decision-making processes. The report concludes with recommendations based on the analysis and calculations presented.

Financial

Management

Management

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Table of Contents.............................................................................................................................2

INTRODUCTION...........................................................................................................................1

QUESTION 1..................................................................................................................................1

a. Analysing the size of dividend to return to the shareholders...................................................1

b. Practical issues which should be analysed while deciding size of dividend payment.............2

c. Impact of all the alternatives upon the ownership of shareholders..........................................2

d. Analysis of the way in which the decision of company could be influenced by opportunity

to invest specific amount in a project which is having positive net present value......................3

QUESTION 3..................................................................................................................................4

1. Calculation using various techniques of investment appraisal to determine suitability of the

investment option.........................................................................................................................4

2. Discussion of different limitation and benefits of all the investment appraisal techniques....8

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................10

Table of Contents.............................................................................................................................2

INTRODUCTION...........................................................................................................................1

QUESTION 1..................................................................................................................................1

a. Analysing the size of dividend to return to the shareholders...................................................1

b. Practical issues which should be analysed while deciding size of dividend payment.............2

c. Impact of all the alternatives upon the ownership of shareholders..........................................2

d. Analysis of the way in which the decision of company could be influenced by opportunity

to invest specific amount in a project which is having positive net present value......................3

QUESTION 3..................................................................................................................................4

1. Calculation using various techniques of investment appraisal to determine suitability of the

investment option.........................................................................................................................4

2. Discussion of different limitation and benefits of all the investment appraisal techniques....8

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................10

INTRODUCTION

Financial management is a broad concept which is focused with formulation of different

types of accounts and reports that are covering detailed information of financial transactions of

an entity. While planning to attain growth and development for business it will be very important

for businesses to assure that all the final accounts are formulated in systematic manner. With the

help of it, the management teams can assure that all the plans that were formed by them

previously are resulting positively or negatively for business (Ajam and Fourie, 2016). Main aim

of this assignment is to understand the importance of financial accounting for the businesses to

attain success in future. First question which is selected to complete this report is question 1 and

the topics which will be covered in it are size of annual dividend to return to shareholders, issues

that are required to be focused while deciding the size, assessment of different options of

dividend etc. Second question which is selected for this report is question 3 which is mainly

based upon use of investment appraisal techniques that could be used by the organisation. These

techniques are payback period, net present value, accounting and internal rate of return. Apart

from this, benefits and drawbacks of using them are also covered in this assignment.

QUESTION 1

a. Analysing the size of dividend to return to the shareholders

For all the businesses it is very important to analyse that they are able to provide returns

to all the shareholders on their ownership so that they could be retained for long run. While

deciding the size of the dividend different factors are required to be focused by the organisations.

The size of it could be small or big and it is dependent upon following factors. Discussion of

them is as follows:

Ownership of the shareholders: It is one of the key factors which decides the size of

dividend because while offering dividend to the shareholders it is required to be assessed that

they are having large or small part in the ownership. When it will be large them high dividend

will be offered the shareholders will small part will receive lower dividend.

Preference of shareholders: It is another key element which helps to decide the size of

dividend of the shareholders. Most of the stakeholders want dividend on their ownership but

some of them want to increase their ownership so they prefer share against the dividend. While

1

Financial management is a broad concept which is focused with formulation of different

types of accounts and reports that are covering detailed information of financial transactions of

an entity. While planning to attain growth and development for business it will be very important

for businesses to assure that all the final accounts are formulated in systematic manner. With the

help of it, the management teams can assure that all the plans that were formed by them

previously are resulting positively or negatively for business (Ajam and Fourie, 2016). Main aim

of this assignment is to understand the importance of financial accounting for the businesses to

attain success in future. First question which is selected to complete this report is question 1 and

the topics which will be covered in it are size of annual dividend to return to shareholders, issues

that are required to be focused while deciding the size, assessment of different options of

dividend etc. Second question which is selected for this report is question 3 which is mainly

based upon use of investment appraisal techniques that could be used by the organisation. These

techniques are payback period, net present value, accounting and internal rate of return. Apart

from this, benefits and drawbacks of using them are also covered in this assignment.

QUESTION 1

a. Analysing the size of dividend to return to the shareholders

For all the businesses it is very important to analyse that they are able to provide returns

to all the shareholders on their ownership so that they could be retained for long run. While

deciding the size of the dividend different factors are required to be focused by the organisations.

The size of it could be small or big and it is dependent upon following factors. Discussion of

them is as follows:

Ownership of the shareholders: It is one of the key factors which decides the size of

dividend because while offering dividend to the shareholders it is required to be assessed that

they are having large or small part in the ownership. When it will be large them high dividend

will be offered the shareholders will small part will receive lower dividend.

Preference of shareholders: It is another key element which helps to decide the size of

dividend of the shareholders. Most of the stakeholders want dividend on their ownership but

some of them want to increase their ownership so they prefer share against the dividend. While

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

deciding the size of the dividend then it will be very important to analyse preferences of all the

stakeholders (Danes, Garbow and Jokela, 2016).

b. Practical issues which should be analysed while deciding size of dividend payment

When deciding the size of the dividend to the shareholders it will be very important for

all the managers of the companies to determine the issues which may take place in future. All of

them are discussed below:

Lack of funding: It is one of the main issues which may affect the decision of deciding

the size of dividend. When the organisation will not be having sufficient funds then it will be

very difficult to offer dividend to the shareholders. In case of lower profits, the dividend of them

is retained so that it could be used in future to fund all the operations.

Conflict of interest of shareholders: It is very important for all the entities to determine

that shareholders agree to the dividend scheme which is selected by the organisation whether it is

regarding cash or scrip dividend. If some of them need cash or some of them are agreed with

scrip scheme then it will result in conflict of interest of shareholders. Due to this, the managers

can face issues for meeting expectation of all the shareholders (Delkhosh and Mousavi, 2016).

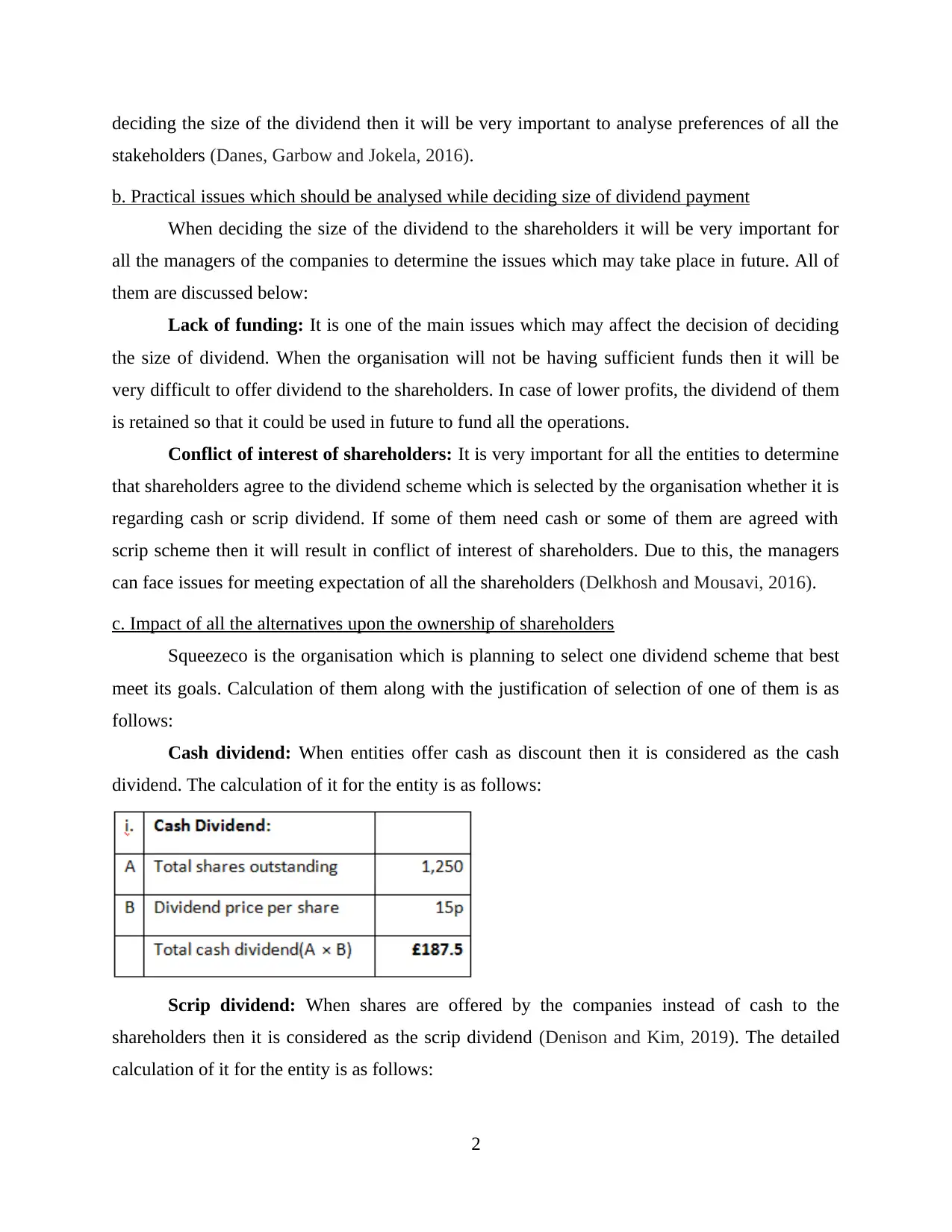

c. Impact of all the alternatives upon the ownership of shareholders

Squeezeco is the organisation which is planning to select one dividend scheme that best

meet its goals. Calculation of them along with the justification of selection of one of them is as

follows:

Cash dividend: When entities offer cash as discount then it is considered as the cash

dividend. The calculation of it for the entity is as follows:

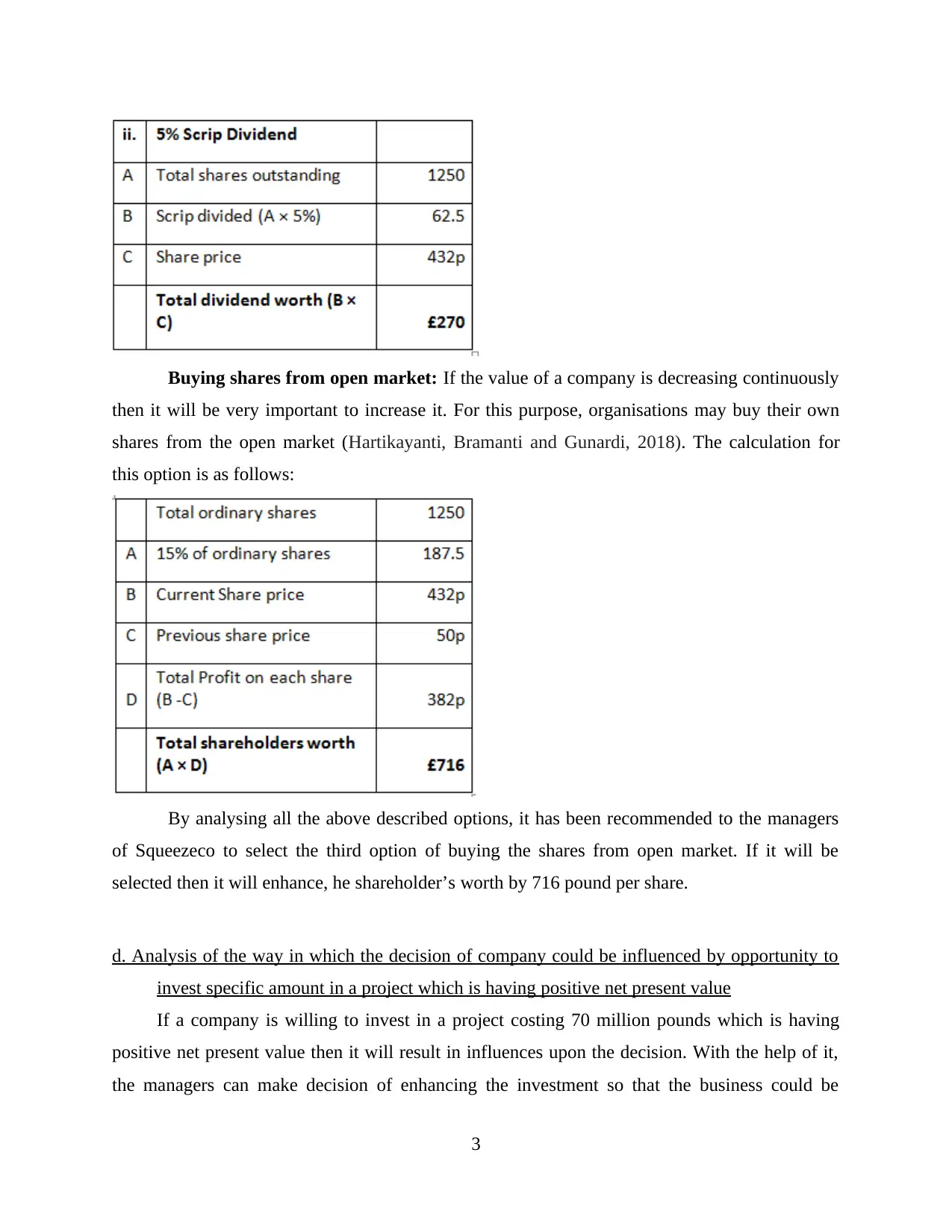

Scrip dividend: When shares are offered by the companies instead of cash to the

shareholders then it is considered as the scrip dividend (Denison and Kim, 2019). The detailed

calculation of it for the entity is as follows:

2

stakeholders (Danes, Garbow and Jokela, 2016).

b. Practical issues which should be analysed while deciding size of dividend payment

When deciding the size of the dividend to the shareholders it will be very important for

all the managers of the companies to determine the issues which may take place in future. All of

them are discussed below:

Lack of funding: It is one of the main issues which may affect the decision of deciding

the size of dividend. When the organisation will not be having sufficient funds then it will be

very difficult to offer dividend to the shareholders. In case of lower profits, the dividend of them

is retained so that it could be used in future to fund all the operations.

Conflict of interest of shareholders: It is very important for all the entities to determine

that shareholders agree to the dividend scheme which is selected by the organisation whether it is

regarding cash or scrip dividend. If some of them need cash or some of them are agreed with

scrip scheme then it will result in conflict of interest of shareholders. Due to this, the managers

can face issues for meeting expectation of all the shareholders (Delkhosh and Mousavi, 2016).

c. Impact of all the alternatives upon the ownership of shareholders

Squeezeco is the organisation which is planning to select one dividend scheme that best

meet its goals. Calculation of them along with the justification of selection of one of them is as

follows:

Cash dividend: When entities offer cash as discount then it is considered as the cash

dividend. The calculation of it for the entity is as follows:

Scrip dividend: When shares are offered by the companies instead of cash to the

shareholders then it is considered as the scrip dividend (Denison and Kim, 2019). The detailed

calculation of it for the entity is as follows:

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

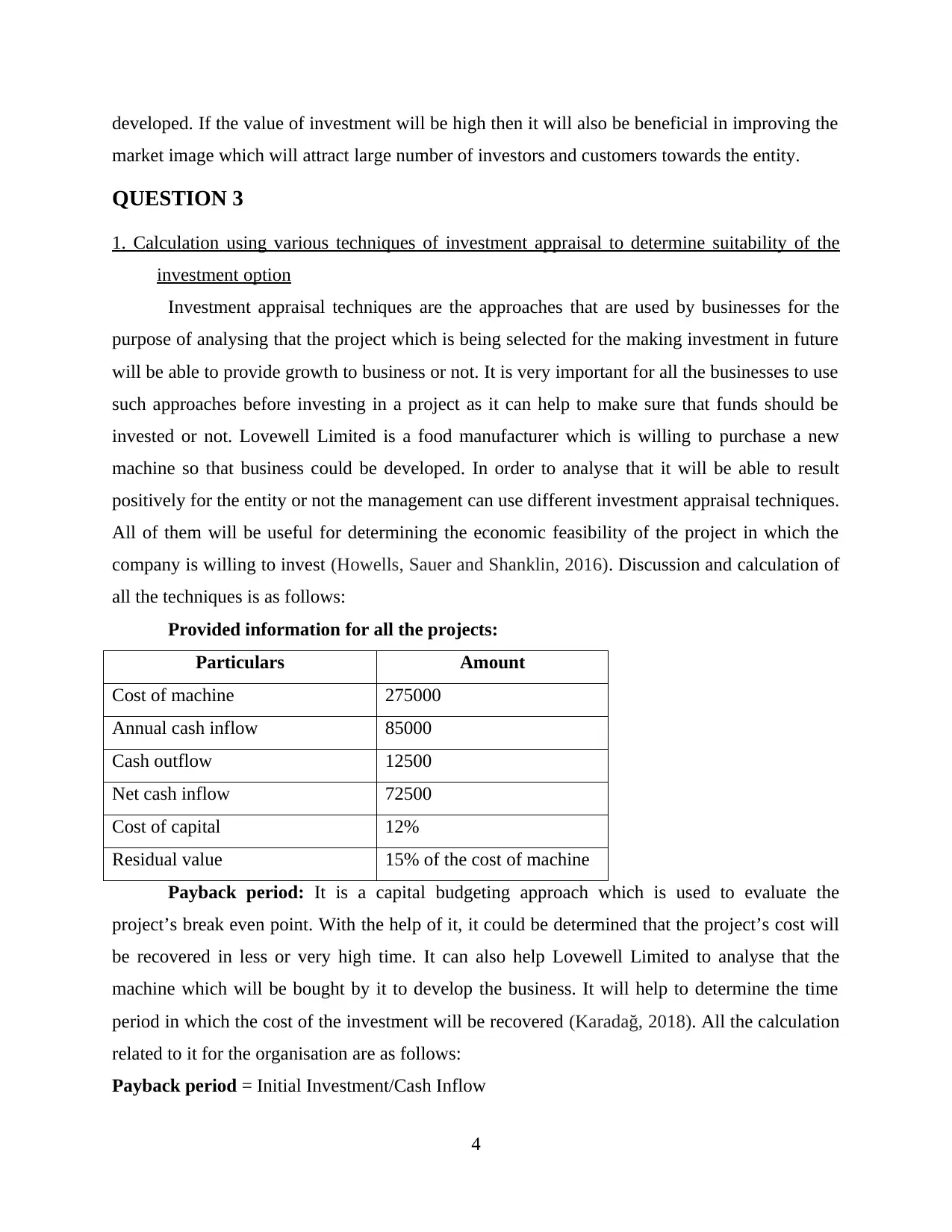

Buying shares from open market: If the value of a company is decreasing continuously

then it will be very important to increase it. For this purpose, organisations may buy their own

shares from the open market (Hartikayanti, Bramanti and Gunardi, 2018). The calculation for

this option is as follows:

By analysing all the above described options, it has been recommended to the managers

of Squeezeco to select the third option of buying the shares from open market. If it will be

selected then it will enhance, he shareholder’s worth by 716 pound per share.

d. Analysis of the way in which the decision of company could be influenced by opportunity to

invest specific amount in a project which is having positive net present value

If a company is willing to invest in a project costing 70 million pounds which is having

positive net present value then it will result in influences upon the decision. With the help of it,

the managers can make decision of enhancing the investment so that the business could be

3

then it will be very important to increase it. For this purpose, organisations may buy their own

shares from the open market (Hartikayanti, Bramanti and Gunardi, 2018). The calculation for

this option is as follows:

By analysing all the above described options, it has been recommended to the managers

of Squeezeco to select the third option of buying the shares from open market. If it will be

selected then it will enhance, he shareholder’s worth by 716 pound per share.

d. Analysis of the way in which the decision of company could be influenced by opportunity to

invest specific amount in a project which is having positive net present value

If a company is willing to invest in a project costing 70 million pounds which is having

positive net present value then it will result in influences upon the decision. With the help of it,

the managers can make decision of enhancing the investment so that the business could be

3

developed. If the value of investment will be high then it will also be beneficial in improving the

market image which will attract large number of investors and customers towards the entity.

QUESTION 3

1. Calculation using various techniques of investment appraisal to determine suitability of the

investment option

Investment appraisal techniques are the approaches that are used by businesses for the

purpose of analysing that the project which is being selected for the making investment in future

will be able to provide growth to business or not. It is very important for all the businesses to use

such approaches before investing in a project as it can help to make sure that funds should be

invested or not. Lovewell Limited is a food manufacturer which is willing to purchase a new

machine so that business could be developed. In order to analyse that it will be able to result

positively for the entity or not the management can use different investment appraisal techniques.

All of them will be useful for determining the economic feasibility of the project in which the

company is willing to invest (Howells, Sauer and Shanklin, 2016). Discussion and calculation of

all the techniques is as follows:

Provided information for all the projects:

Particulars Amount

Cost of machine 275000

Annual cash inflow 85000

Cash outflow 12500

Net cash inflow 72500

Cost of capital 12%

Residual value 15% of the cost of machine

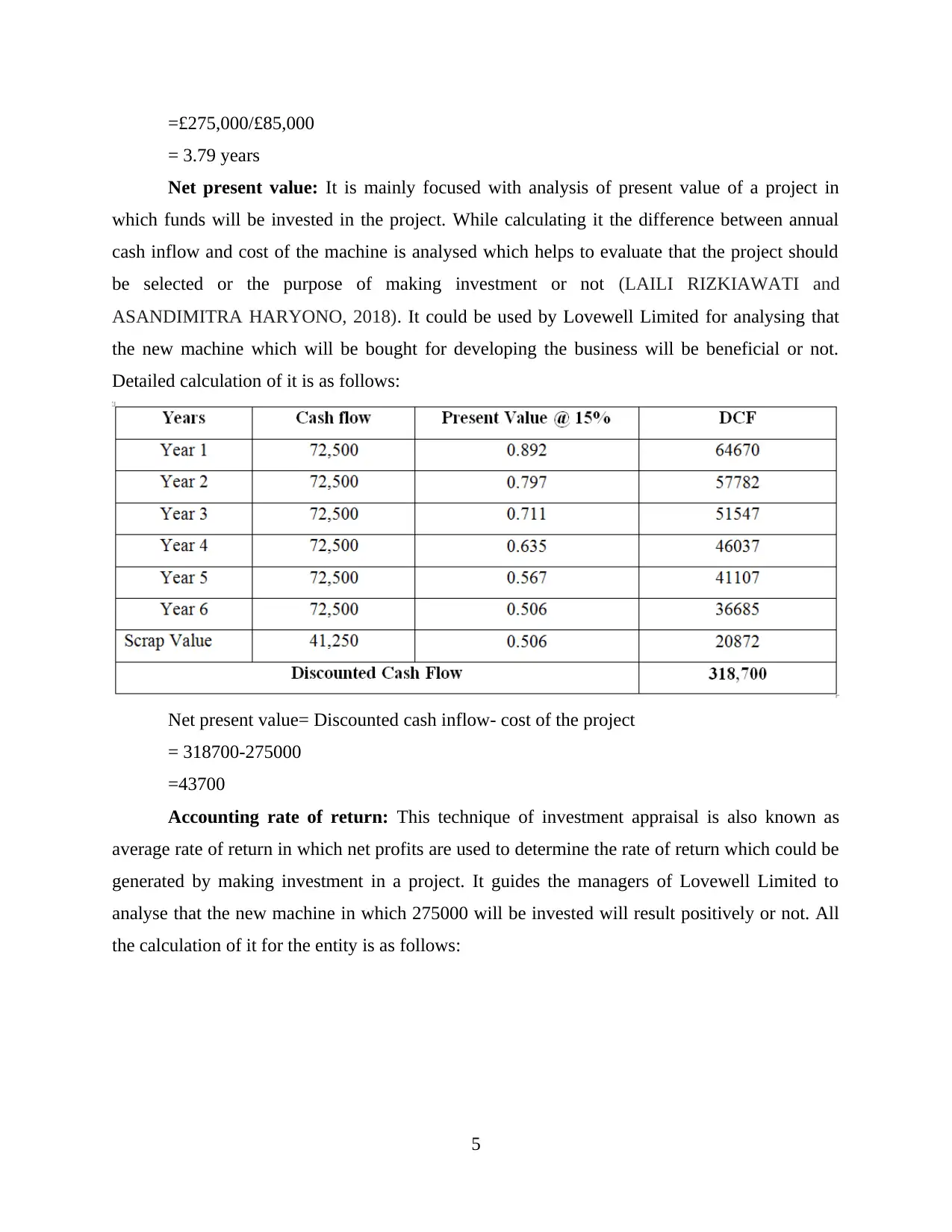

Payback period: It is a capital budgeting approach which is used to evaluate the

project’s break even point. With the help of it, it could be determined that the project’s cost will

be recovered in less or very high time. It can also help Lovewell Limited to analyse that the

machine which will be bought by it to develop the business. It will help to determine the time

period in which the cost of the investment will be recovered (Karadağ, 2018). All the calculation

related to it for the organisation are as follows:

Payback period = Initial Investment/Cash Inflow

4

market image which will attract large number of investors and customers towards the entity.

QUESTION 3

1. Calculation using various techniques of investment appraisal to determine suitability of the

investment option

Investment appraisal techniques are the approaches that are used by businesses for the

purpose of analysing that the project which is being selected for the making investment in future

will be able to provide growth to business or not. It is very important for all the businesses to use

such approaches before investing in a project as it can help to make sure that funds should be

invested or not. Lovewell Limited is a food manufacturer which is willing to purchase a new

machine so that business could be developed. In order to analyse that it will be able to result

positively for the entity or not the management can use different investment appraisal techniques.

All of them will be useful for determining the economic feasibility of the project in which the

company is willing to invest (Howells, Sauer and Shanklin, 2016). Discussion and calculation of

all the techniques is as follows:

Provided information for all the projects:

Particulars Amount

Cost of machine 275000

Annual cash inflow 85000

Cash outflow 12500

Net cash inflow 72500

Cost of capital 12%

Residual value 15% of the cost of machine

Payback period: It is a capital budgeting approach which is used to evaluate the

project’s break even point. With the help of it, it could be determined that the project’s cost will

be recovered in less or very high time. It can also help Lovewell Limited to analyse that the

machine which will be bought by it to develop the business. It will help to determine the time

period in which the cost of the investment will be recovered (Karadağ, 2018). All the calculation

related to it for the organisation are as follows:

Payback period = Initial Investment/Cash Inflow

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

=£275,000/£85,000

= 3.79 years

Net present value: It is mainly focused with analysis of present value of a project in

which funds will be invested in the project. While calculating it the difference between annual

cash inflow and cost of the machine is analysed which helps to evaluate that the project should

be selected or the purpose of making investment or not (LAILI RIZKIAWATI and

ASANDIMITRA HARYONO, 2018). It could be used by Lovewell Limited for analysing that

the new machine which will be bought for developing the business will be beneficial or not.

Detailed calculation of it is as follows:

Net present value= Discounted cash inflow- cost of the project

= 318700-275000

=43700

Accounting rate of return: This technique of investment appraisal is also known as

average rate of return in which net profits are used to determine the rate of return which could be

generated by making investment in a project. It guides the managers of Lovewell Limited to

analyse that the new machine in which 275000 will be invested will result positively or not. All

the calculation of it for the entity is as follows:

5

= 3.79 years

Net present value: It is mainly focused with analysis of present value of a project in

which funds will be invested in the project. While calculating it the difference between annual

cash inflow and cost of the machine is analysed which helps to evaluate that the project should

be selected or the purpose of making investment or not (LAILI RIZKIAWATI and

ASANDIMITRA HARYONO, 2018). It could be used by Lovewell Limited for analysing that

the new machine which will be bought for developing the business will be beneficial or not.

Detailed calculation of it is as follows:

Net present value= Discounted cash inflow- cost of the project

= 318700-275000

=43700

Accounting rate of return: This technique of investment appraisal is also known as

average rate of return in which net profits are used to determine the rate of return which could be

generated by making investment in a project. It guides the managers of Lovewell Limited to

analyse that the new machine in which 275000 will be invested will result positively or not. All

the calculation of it for the entity is as follows:

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Accounting Rate of Return =£33,541.67/£275,000*100

=12.19%

Working notes:

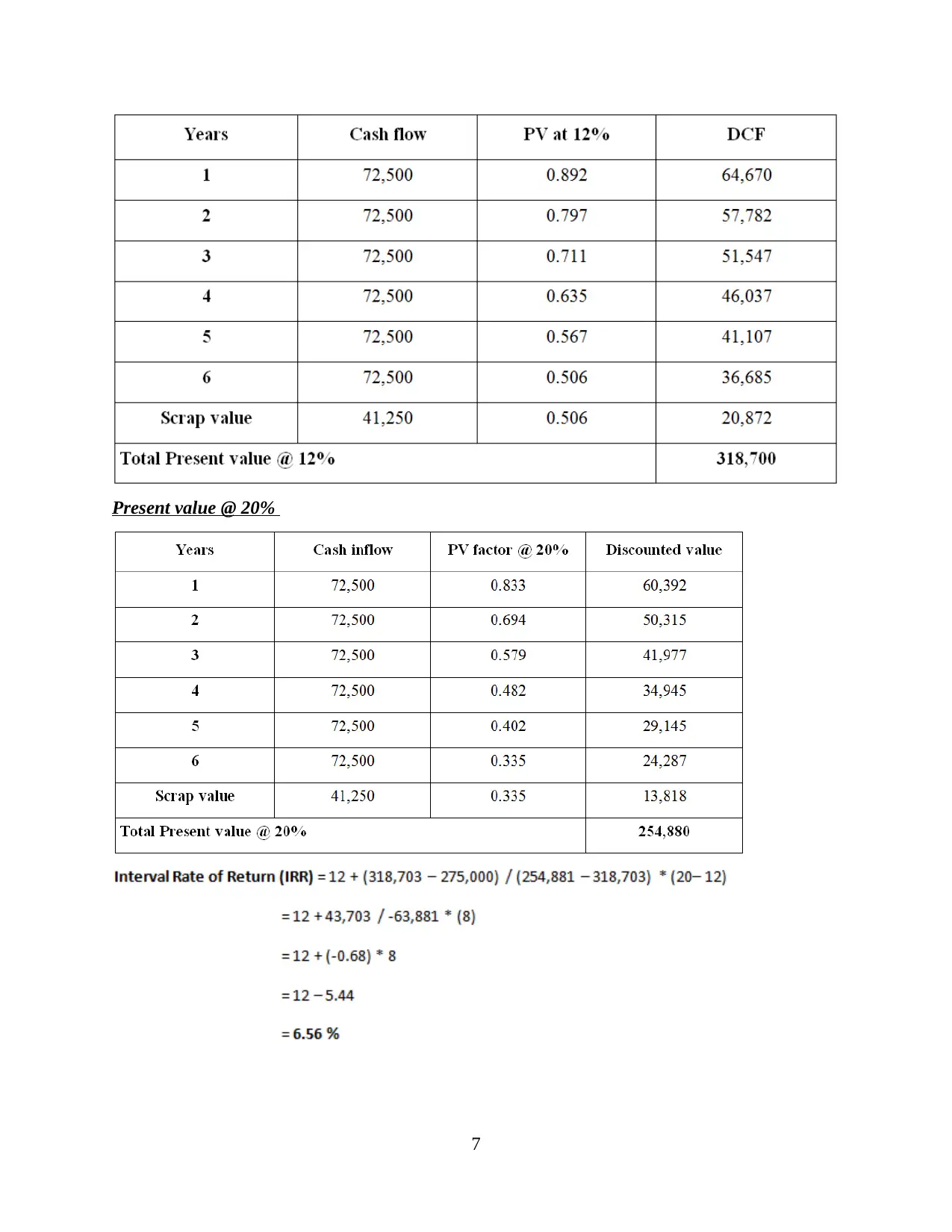

Internal rate of return: It is profitability measurement technique which is used by the

organisations to analyse profitability of the project in which funds will be invested. By using it

the enterprise will be able to determine that investment should be made or not. If it will be used

by Lovewell Limited then the organisation can analyse that the new machine will provide good

returns or not. The detailed calculation of it is as follows:

PV @ 12 %

6

=12.19%

Working notes:

Internal rate of return: It is profitability measurement technique which is used by the

organisations to analyse profitability of the project in which funds will be invested. By using it

the enterprise will be able to determine that investment should be made or not. If it will be used

by Lovewell Limited then the organisation can analyse that the new machine will provide good

returns or not. The detailed calculation of it is as follows:

PV @ 12 %

6

Present value @ 20%

7

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Recommendations: With the help of the calculation of all the investment appraisal

techniques it has been analysed that the company should invest in the new machine as the results

of all the techniques is positive.

2. Discussion of different limitation and benefits of all the investment appraisal techniques

In Lovewell Limited different investment appraisal techniques will be used by the

managers to determine that new machine in which investment of 275000 will be made will result

positively or no. While using all of them it will be very important to make sure that they are able

to analyse all the benefits and drawbacks of all the techniques. Discussion of all of them is as

follows for all the techniques:

Net present value: When the managers of Lovewell Limited will use this technique then

it will be very important for them to be aware of all the benefits and drawbacks of it. All of them

are as follows:

Benefits: It helps to formulate the decision of making investment and make sure that the

decision is right because time value of money is considered in it. It provides good

measure of profitability as the actual present value of the project is analysed in this

technique (Spearman, 2019).

Drawbacks: Sunk cost is ignored in this investment appraisal technique which may leave

negative impact upon the results. When the main objective of it is comparison and they

are different in the size then it could not be used as it is not suitable for such types of

projects.

Payback period: If the managers are using it then it is very important for them to make

sure that they are aware of all the benefits and drawbacks of it. Discussion of them is as follows:

Benefits: The formula of calculation of payback period is very simple and

straightforward which can help to analyse that project will be able to meet breakeven

point is less time period or not. It will also help to evaluate the project quickly as it

results in reduction of risk of the losses.

Drawbacks: Time value of money is ignored in this method of investment appraisal

which may affect the level of accuracy of the results. If the payback period is analysed

then it ignores the inflow of the cash after the payback period is calculated. Apart from

this, it is biased against all the projects that are having long-term life.

8

techniques it has been analysed that the company should invest in the new machine as the results

of all the techniques is positive.

2. Discussion of different limitation and benefits of all the investment appraisal techniques

In Lovewell Limited different investment appraisal techniques will be used by the

managers to determine that new machine in which investment of 275000 will be made will result

positively or no. While using all of them it will be very important to make sure that they are able

to analyse all the benefits and drawbacks of all the techniques. Discussion of all of them is as

follows for all the techniques:

Net present value: When the managers of Lovewell Limited will use this technique then

it will be very important for them to be aware of all the benefits and drawbacks of it. All of them

are as follows:

Benefits: It helps to formulate the decision of making investment and make sure that the

decision is right because time value of money is considered in it. It provides good

measure of profitability as the actual present value of the project is analysed in this

technique (Spearman, 2019).

Drawbacks: Sunk cost is ignored in this investment appraisal technique which may leave

negative impact upon the results. When the main objective of it is comparison and they

are different in the size then it could not be used as it is not suitable for such types of

projects.

Payback period: If the managers are using it then it is very important for them to make

sure that they are aware of all the benefits and drawbacks of it. Discussion of them is as follows:

Benefits: The formula of calculation of payback period is very simple and

straightforward which can help to analyse that project will be able to meet breakeven

point is less time period or not. It will also help to evaluate the project quickly as it

results in reduction of risk of the losses.

Drawbacks: Time value of money is ignored in this method of investment appraisal

which may affect the level of accuracy of the results. If the payback period is analysed

then it ignores the inflow of the cash after the payback period is calculated. Apart from

this, it is biased against all the projects that are having long-term life.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Accounting rate of return: With the help of it, the managers can analyse that the project

will result in higher returns or not. All the benefits and drawbacks of it are discussed below that

should be focused by Lovewell Limited are as follows:

Benefits: This method is very easy for computation and understanding. As net profit is

used in it for the purpose of calculations so it can help to analyse the rate of return easily.

While using it entire life of project is analysed which may lead towards effective analysis

of the economic stability of the project.

Drawbacks: The results of it could be manipulated easily because when the method of

depreciation will be changed then it will affect the net profits that are used for

calculations in it. Time factor of money is not used in it which also results in inaccurate

results which may affect the decision of investment in which funds will be invested.

Internal rate of return: There are various types of positive as well as negative aspects

of this technique. Discussion of all of them is as follows:

Benefits: Time value of money is used in this technique which helps to calculate the

accurate results. The level of simplicity in this approach is very high as it is very easy to

interpret. Apart from this, it is used for dependent or contingent projects so that actual

benefits of the project could be determined (Tsai, 2017).

Drawbacks: There are various factors which are not focused in this technique when it is

used by the entities. These are future cost, size of the project, duration of the project etc.

All of them are required to be focused in context of investment for the purpose of

determining actual return for the projects. Ignorance of them may result in negative

impacts upon the results.

CONCLUSION

From the above project report, it has been concluded that with the help of financial

management the managers can analyse that the business will be able to reach the desired level of

success. While planning to offer dividend to the shareholders then the companies can pay

attention towards different alternatives that are available to them. These are cash of scrip

dividend. One of them should be selected on the basis of suitability of them for business. There

are various types of investment appraisal techniques that are required to be focused while

planning to make investment in a project. These are internal and accounting rate of return, net

present value and payback period.

9

will result in higher returns or not. All the benefits and drawbacks of it are discussed below that

should be focused by Lovewell Limited are as follows:

Benefits: This method is very easy for computation and understanding. As net profit is

used in it for the purpose of calculations so it can help to analyse the rate of return easily.

While using it entire life of project is analysed which may lead towards effective analysis

of the economic stability of the project.

Drawbacks: The results of it could be manipulated easily because when the method of

depreciation will be changed then it will affect the net profits that are used for

calculations in it. Time factor of money is not used in it which also results in inaccurate

results which may affect the decision of investment in which funds will be invested.

Internal rate of return: There are various types of positive as well as negative aspects

of this technique. Discussion of all of them is as follows:

Benefits: Time value of money is used in this technique which helps to calculate the

accurate results. The level of simplicity in this approach is very high as it is very easy to

interpret. Apart from this, it is used for dependent or contingent projects so that actual

benefits of the project could be determined (Tsai, 2017).

Drawbacks: There are various factors which are not focused in this technique when it is

used by the entities. These are future cost, size of the project, duration of the project etc.

All of them are required to be focused in context of investment for the purpose of

determining actual return for the projects. Ignorance of them may result in negative

impacts upon the results.

CONCLUSION

From the above project report, it has been concluded that with the help of financial

management the managers can analyse that the business will be able to reach the desired level of

success. While planning to offer dividend to the shareholders then the companies can pay

attention towards different alternatives that are available to them. These are cash of scrip

dividend. One of them should be selected on the basis of suitability of them for business. There

are various types of investment appraisal techniques that are required to be focused while

planning to make investment in a project. These are internal and accounting rate of return, net

present value and payback period.

9

REFERENCES

Books and journals:

Ajam, T. and Fourie, D. J., 2016. Public financial management reform in South African

provincial basic education departments. Public Administration and Development. 36(4).

pp.263-282.

Danes, S. M., Garbow, J. and Jokela, B. H., 2016. Financial Management and Culture: The

American Indian Case. Journal of Financial Counseling and Planning. 27(1). pp.61-79.

Delkhosh, M. and Mousavi, H., 2016. Strategic Financial Management Review on the Financial

Success of an Organization. Mediterranean Journal of Social Sciences. 7(2 S2). p.30.

Denison, D. V. and Kim, S., 2019. Linking practice and classroom: Nonprofit financial

management curricula in MPA and MPP programs. Journal of Public Affairs Education.

25(4). pp.457-474.

Hartikayanti, H. N., Bramanti, F. L. and Gunardi, A., 2018. Financial management information

system: an empirical evidence.

Howells, A., Sauer, K. and Shanklin, C., 2016. Evaluating human resource and financial

management responsibilities of clinical nutrition managers. Journal of the Academy of

Nutrition and Dietetics. 116(12). pp.1883-1891.

Karadağ, H., 2018. Cash, receivables and inventory management practices in small enterprises:

Their associations with financial performance and competitiveness. Small enterprise

research. 25(1). pp.69-89.

LAILI RIZKIAWATI, N. U. R. and ASANDIMITRA HARYONO, N. A. D. I. A., 2018.

Pengaruh demografi, financial knowledge, financial attitude, locus of control dan

financial self-efficacy terhadap financial management behavior masyarakat

surabaya. Jurnal Ilmu Manajemen (JIM), 6(3).

Spearman, K., 2019. Financial management for local government (Vol. 1). Routledge.

Tsai, L. C., 2017. Household financial management and women’s experiences of intimate partner

violence in the Philippines: A study using propensity score methods. Violence against

women. 23(3). pp.330-350.

10

Books and journals:

Ajam, T. and Fourie, D. J., 2016. Public financial management reform in South African

provincial basic education departments. Public Administration and Development. 36(4).

pp.263-282.

Danes, S. M., Garbow, J. and Jokela, B. H., 2016. Financial Management and Culture: The

American Indian Case. Journal of Financial Counseling and Planning. 27(1). pp.61-79.

Delkhosh, M. and Mousavi, H., 2016. Strategic Financial Management Review on the Financial

Success of an Organization. Mediterranean Journal of Social Sciences. 7(2 S2). p.30.

Denison, D. V. and Kim, S., 2019. Linking practice and classroom: Nonprofit financial

management curricula in MPA and MPP programs. Journal of Public Affairs Education.

25(4). pp.457-474.

Hartikayanti, H. N., Bramanti, F. L. and Gunardi, A., 2018. Financial management information

system: an empirical evidence.

Howells, A., Sauer, K. and Shanklin, C., 2016. Evaluating human resource and financial

management responsibilities of clinical nutrition managers. Journal of the Academy of

Nutrition and Dietetics. 116(12). pp.1883-1891.

Karadağ, H., 2018. Cash, receivables and inventory management practices in small enterprises:

Their associations with financial performance and competitiveness. Small enterprise

research. 25(1). pp.69-89.

LAILI RIZKIAWATI, N. U. R. and ASANDIMITRA HARYONO, N. A. D. I. A., 2018.

Pengaruh demografi, financial knowledge, financial attitude, locus of control dan

financial self-efficacy terhadap financial management behavior masyarakat

surabaya. Jurnal Ilmu Manajemen (JIM), 6(3).

Spearman, K., 2019. Financial management for local government (Vol. 1). Routledge.

Tsai, L. C., 2017. Household financial management and women’s experiences of intimate partner

violence in the Philippines: A study using propensity score methods. Violence against

women. 23(3). pp.330-350.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.