Financial Management Report: Financial Strategies for Ryanair DAC

VerifiedAdded on 2023/01/06

|25

|7936

|63

Report

AI Summary

This report provides a comprehensive overview of financial management principles, techniques, and processes, using Ryanair DAC as a case study. It explores management accounting techniques supporting facilities management, financial systems, and processes for effective budget management. The report delves into financial auditing principles, corporate ethics, and transparency, including how to present a true and fair view of financial data. It examines revenue and capital budgeting, including techniques for setting, reviewing, and managing budgets, alongside financial appraisal tools. Furthermore, it covers cash-flow projections, their application in managing cash flow within the business cycle, and the preparation of financial cases to secure required approvals. The report integrates these concepts to provide a holistic understanding of financial management practices within a real-world context, offering insights into decision-making and operational efficiency.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Financial

Management

Management

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................4

LO 1.................................................................................................................................................4

1.1. Describe management accounting techniques which support the facilities management

process and the financial systems and processes used for the effective management of facilities

management budget within your company..................................................................................4

1.2 Financial systems and processes used for the effective management:.................................5

LO 2.................................................................................................................................................6

2.1 Explain the principles of financial auditing and describe how these principles are deployed

within your own area of responsibility........................................................................................6

2.2 Describe how these principles within own

area of responsibility...................................................................................................................6

2.3 Review the financial implications of using codes of ethics within in the context of

corporate responsibility................................................................................................................7

2.4 Explain how you would make suitable adjustments to improve good practice and

transparency ................................................................................................................................8

2.5 Explain ways in which a true and fair view of assets, liabilities, profits and costs can be

presented .....................................................................................................................................9

LO 3...............................................................................................................................................11

3.1 Explain how organizations would prepare, review and manage revenue budgets .............11

3.2 Review and manage budgets................................................................................................13

3.3 Set out how to apply the techniques used by facilities managers to set, acquire, review and

manage capital budgets..............................................................................................................14

3.4 Set capital budgets...............................................................................................................15

3.5 Review and manage capital budgets....................................................................................17

3.6 Explain the tools of financial appraisal and how these are used to inform financial

management and budgetary decisions ......................................................................................17

LO 4...............................................................................................................................................18

4.1. Apply the principles, techniques and processes of cash-flow projections to manage the

flow of cash within the facilities management business cycle, including how this impacts on

contracts and projects.................................................................................................................18

1

MAIN BODY...................................................................................................................................4

LO 1.................................................................................................................................................4

1.1. Describe management accounting techniques which support the facilities management

process and the financial systems and processes used for the effective management of facilities

management budget within your company..................................................................................4

1.2 Financial systems and processes used for the effective management:.................................5

LO 2.................................................................................................................................................6

2.1 Explain the principles of financial auditing and describe how these principles are deployed

within your own area of responsibility........................................................................................6

2.2 Describe how these principles within own

area of responsibility...................................................................................................................6

2.3 Review the financial implications of using codes of ethics within in the context of

corporate responsibility................................................................................................................7

2.4 Explain how you would make suitable adjustments to improve good practice and

transparency ................................................................................................................................8

2.5 Explain ways in which a true and fair view of assets, liabilities, profits and costs can be

presented .....................................................................................................................................9

LO 3...............................................................................................................................................11

3.1 Explain how organizations would prepare, review and manage revenue budgets .............11

3.2 Review and manage budgets................................................................................................13

3.3 Set out how to apply the techniques used by facilities managers to set, acquire, review and

manage capital budgets..............................................................................................................14

3.4 Set capital budgets...............................................................................................................15

3.5 Review and manage capital budgets....................................................................................17

3.6 Explain the tools of financial appraisal and how these are used to inform financial

management and budgetary decisions ......................................................................................17

LO 4...............................................................................................................................................18

4.1. Apply the principles, techniques and processes of cash-flow projections to manage the

flow of cash within the facilities management business cycle, including how this impacts on

contracts and projects.................................................................................................................18

1

4.2 Apply the principles, techniques and

processes in the management of cash flow

for contracts and projects..........................................................................................................18

LO 5...............................................................................................................................................21

5.1 & 5.2 Identify and apply the principles and techniques to prepare financial cases and

prepare a financial case to secure the required approval...........................................................21

CONCLUSION..............................................................................................................................22

REFERENCES .............................................................................................................................23

2

processes in the management of cash flow

for contracts and projects..........................................................................................................18

LO 5...............................................................................................................................................21

5.1 & 5.2 Identify and apply the principles and techniques to prepare financial cases and

prepare a financial case to secure the required approval...........................................................21

CONCLUSION..............................................................................................................................22

REFERENCES .............................................................................................................................23

2

INTRODUCTION

Financial management involves the planning, implementation, coordination, management

and regulation of business operations, such as the acquisition and use of company funds. It

involves identifying general accounting management concepts to the company's financial capital.

It contains a list of types of decisions, such as investment decisions, including spending on fixed

assets (called capital budgeting). Invested capital is also part of financial decisions referred to as

decision making on working capital. Financial decisions relating to the increasing of funding

from different resources, that will focus on the form of source, the length of financing, the

expense of funding and the returns (Aman, 2016). Dividend decision is taken by the financial

manager who has to make decision on the allocation of net profits. Net profits were also broadly

divided into two dividends for shareholders where even the dividend as well as the rate of the

dividend has to be determined. Retained earnings are the proportion of retained earnings to be

determined, that will depend on the company's growth and diversifying plans.

For the better understanding of this financial management concept, Ryanair DAC is selected

which is Ireland based airline corporation. Ryanair DAC (Designated Activity Company) is an

Irish low cost airline established in 1984, headquarter based in Swords, Dublin, with its

principal operating base at Dublin and London Stansted airports. It is the biggest chunk of

Ryanair Holdings' airline community, and Ryanair is the UK, Buzz, Malta Air and Lauda 's sister

airlines. Ryanair was the biggest scheduled airline budgeted airline in Europe in 2016, carrying

more foreign passengers than just about any other carrier. The organisation has been criticised

for the treatment of its workers and the extensive use of additional charges. It was also

remembered for its deliberate exploitation of conflict as a way of creating free ads and terrible

customer service. This assessment covers several topics such as management accounting

techniques which facilitates the management process and also implement such techniques to

improve their management practices. Principles of financial auditing help the managers to

improving their own area of responsibilities. Also review the code of ethics within corporate

responsibility and further management need to done some adjustment for better practice and

transparency. In addition, also evaluate that how manager review and manage the revenue budget

and some techniques which facilitates the managers to manage capital budget.

3

Financial management involves the planning, implementation, coordination, management

and regulation of business operations, such as the acquisition and use of company funds. It

involves identifying general accounting management concepts to the company's financial capital.

It contains a list of types of decisions, such as investment decisions, including spending on fixed

assets (called capital budgeting). Invested capital is also part of financial decisions referred to as

decision making on working capital. Financial decisions relating to the increasing of funding

from different resources, that will focus on the form of source, the length of financing, the

expense of funding and the returns (Aman, 2016). Dividend decision is taken by the financial

manager who has to make decision on the allocation of net profits. Net profits were also broadly

divided into two dividends for shareholders where even the dividend as well as the rate of the

dividend has to be determined. Retained earnings are the proportion of retained earnings to be

determined, that will depend on the company's growth and diversifying plans.

For the better understanding of this financial management concept, Ryanair DAC is selected

which is Ireland based airline corporation. Ryanair DAC (Designated Activity Company) is an

Irish low cost airline established in 1984, headquarter based in Swords, Dublin, with its

principal operating base at Dublin and London Stansted airports. It is the biggest chunk of

Ryanair Holdings' airline community, and Ryanair is the UK, Buzz, Malta Air and Lauda 's sister

airlines. Ryanair was the biggest scheduled airline budgeted airline in Europe in 2016, carrying

more foreign passengers than just about any other carrier. The organisation has been criticised

for the treatment of its workers and the extensive use of additional charges. It was also

remembered for its deliberate exploitation of conflict as a way of creating free ads and terrible

customer service. This assessment covers several topics such as management accounting

techniques which facilitates the management process and also implement such techniques to

improve their management practices. Principles of financial auditing help the managers to

improving their own area of responsibilities. Also review the code of ethics within corporate

responsibility and further management need to done some adjustment for better practice and

transparency. In addition, also evaluate that how manager review and manage the revenue budget

and some techniques which facilitates the managers to manage capital budget.

3

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

MAIN BODY

LO 1

1.1. Describe management accounting techniques which support the facilities management

process and the financial systems and processes used for the effective management of

facilities management budget within your company

Management accounting techniques that support the management process:

Management accounting also called cost accounting or managerial accounting which is an

accounting division dealing with the recognition, calculation, review and evaluation of

accounting data because it can be seemed to help managers or management process to make the

required decisions and managing their operational performance efficiently (Antonopoulos and

Hall, 2016). With exception of financial accounting, which focuses mainly on the proper

coordination and disclosure of the firm's financial situations to stakeholders ( e.g. investors,

lenders), management accounting focuses on decision-making process which is taken by the

internal people of management for effective operational process. Management accountant have

to evaluate different incidents and organisational metrics in required to persuade data into

valuable knowledge that can be used by the management of the organisation in their decision

making process. The goal would be to provide comprehensive details on the operation of the

business by evaluating each specific product line, operational activity, facility, etc. There are

several management accounting techniques which are followed by the managers of Ryanair

Airline Corporation and these are discussed below:

Margin analysis: The marginal analysis is mainly associated with the incremental effects

of improved output. Margin analysis is among the most basic and important strategies in

management accounting. It involves the measurement of the breakeven point that defines

the optimum selling price for the firm's products.

Constraint analysis: This analysis is used for company's production lines that identify

the key inefficiencies, the shortfalls generated by such obstacles, and their effect on the

firm's capacity to produce sales and profits.

Capital budgeting: Capital budgeting is involved with the review of the details used to

make sufficient capital spending decisions. In this analysis, managers measure the

4

LO 1

1.1. Describe management accounting techniques which support the facilities management

process and the financial systems and processes used for the effective management of

facilities management budget within your company

Management accounting techniques that support the management process:

Management accounting also called cost accounting or managerial accounting which is an

accounting division dealing with the recognition, calculation, review and evaluation of

accounting data because it can be seemed to help managers or management process to make the

required decisions and managing their operational performance efficiently (Antonopoulos and

Hall, 2016). With exception of financial accounting, which focuses mainly on the proper

coordination and disclosure of the firm's financial situations to stakeholders ( e.g. investors,

lenders), management accounting focuses on decision-making process which is taken by the

internal people of management for effective operational process. Management accountant have

to evaluate different incidents and organisational metrics in required to persuade data into

valuable knowledge that can be used by the management of the organisation in their decision

making process. The goal would be to provide comprehensive details on the operation of the

business by evaluating each specific product line, operational activity, facility, etc. There are

several management accounting techniques which are followed by the managers of Ryanair

Airline Corporation and these are discussed below:

Margin analysis: The marginal analysis is mainly associated with the incremental effects

of improved output. Margin analysis is among the most basic and important strategies in

management accounting. It involves the measurement of the breakeven point that defines

the optimum selling price for the firm's products.

Constraint analysis: This analysis is used for company's production lines that identify

the key inefficiencies, the shortfalls generated by such obstacles, and their effect on the

firm's capacity to produce sales and profits.

Capital budgeting: Capital budgeting is involved with the review of the details used to

make sufficient capital spending decisions. In this analysis, managers measure the

4

NPV and the IRR to allowing management to make future capital budgeting decisions for

effective management process.

Inventory valuation and product costing: Inventory assessment involves determining

and assessing the real expenses involved with the goods and inventories of the business

(Anwar, Marliani and Gunawan, 2016). The method usually includes the measurement

and distribution of overheads, as well as the evaluation of specific costs associated with

the cost of goods sold.

Trend analysis and forecasting: This technique is mainly concerned with the detection

of commodity cost trends and patterns, and also the identification of significant variances

from anticipated values and the explanations for such variances.

1.2 Financial systems and processes used for the effective management:

The financial system is a collection of several institutions which provide money lending

options to the organisations such as banks, insurance firms and stock exchanges, which facilitate

the exchange of funds. Financial processes operate at the business, domestic and international

levels. Borrowers, creditors and investors exchange current earnings to fund ventures, either for

usage or profitable investment, and to repay their financial assets. The financial system also

contains a set of policies and procedures that creditors and lenders are using to determine the

projects are funded, the projects are funded, and the conditions of financial transactions. With the

help of financial system, organization such as Ryanair able to fulfil their financial needs or

achieve their business goals & objectives by performing their daily basis operational activities.

Facility budget management is one of the most dynamic systems currently facing by

the facility managers. This is far more than a periodic analysis of needs and the distribution of

funds. Based on the size of the organization, handling the budget may be the primary

responsibility of thousands of staff, and any divergence from the budget may have disastrous

consequences. Instead of giving into the uncertainty of modern budgets and putting stuff on the

back - burner, Facilities Administrators need to learn a few stuff about the fundamentals of good

budgeting (Arianti, 2018). While preparing budget for the organization, management need to

ensure that which financial systems helps in resolving their financial needs with minimum

expenses and risk.

5

effective management process.

Inventory valuation and product costing: Inventory assessment involves determining

and assessing the real expenses involved with the goods and inventories of the business

(Anwar, Marliani and Gunawan, 2016). The method usually includes the measurement

and distribution of overheads, as well as the evaluation of specific costs associated with

the cost of goods sold.

Trend analysis and forecasting: This technique is mainly concerned with the detection

of commodity cost trends and patterns, and also the identification of significant variances

from anticipated values and the explanations for such variances.

1.2 Financial systems and processes used for the effective management:

The financial system is a collection of several institutions which provide money lending

options to the organisations such as banks, insurance firms and stock exchanges, which facilitate

the exchange of funds. Financial processes operate at the business, domestic and international

levels. Borrowers, creditors and investors exchange current earnings to fund ventures, either for

usage or profitable investment, and to repay their financial assets. The financial system also

contains a set of policies and procedures that creditors and lenders are using to determine the

projects are funded, the projects are funded, and the conditions of financial transactions. With the

help of financial system, organization such as Ryanair able to fulfil their financial needs or

achieve their business goals & objectives by performing their daily basis operational activities.

Facility budget management is one of the most dynamic systems currently facing by

the facility managers. This is far more than a periodic analysis of needs and the distribution of

funds. Based on the size of the organization, handling the budget may be the primary

responsibility of thousands of staff, and any divergence from the budget may have disastrous

consequences. Instead of giving into the uncertainty of modern budgets and putting stuff on the

back - burner, Facilities Administrators need to learn a few stuff about the fundamentals of good

budgeting (Arianti, 2018). While preparing budget for the organization, management need to

ensure that which financial systems helps in resolving their financial needs with minimum

expenses and risk.

5

LO 2

2.1 Explain the principles of financial auditing and describe how these principles are deployed

within your own area of responsibility

Financial auditing is an impartial review and assessment of an entity's financial statements

to ensure that the accounting records are a true and correct reflection of the expenditures they

appear to represent. Financial auditing recommendations to the accounting procedure used in the

corporate sector. The method requires the use of an independent entity to analyse the financial

activities and the company's statements. The main aim of the financial audit is to provide an

accurate estimate of the company's operational transactions.

2.2 Describe how these principles within own

area of responsibility.

There are various principles of financial auditing which can be followed by the

management of Ryanair and these are discussed below:

Planning and accountability: Until beginning their job, the auditor must prepare for their

work. In preparation, the auditor shall settle on the accounting of the organisation and the

internal management protocols. The auditors should behave in the preferences of the key

stakeholders, taking into account the broader public interest.

Honesty and Integrity (Probity): Probability is the attribute of possessing good moral

values, i.e. fairness and integrity. Probity requires more than preventing unethical or unethical

conduct. Probity guarantees that all complicated procedures are performed in a manner that is

equitable, unbiased, and transparent and always in the best interest of the organizations. This

process includes the several activities such as procurement, disposal of assets, sponsorship,

marketing, administration of grant etc.

Impartiality, Objectivity, and Independence: The auditor’s approach must be unbiased.

Specific opinions would not be included in the investigation report (Banerjee and et.al., 2016).

The auditors must be seen as impartial in all their interactions with the clients. They express

view should be independently of the company and its management. Objectivity creates a

reasonable description of the whole article, i.e. content and expression. The integrity of the report

is greatly improved as it addresses facts in an objective manner.

6

2.1 Explain the principles of financial auditing and describe how these principles are deployed

within your own area of responsibility

Financial auditing is an impartial review and assessment of an entity's financial statements

to ensure that the accounting records are a true and correct reflection of the expenditures they

appear to represent. Financial auditing recommendations to the accounting procedure used in the

corporate sector. The method requires the use of an independent entity to analyse the financial

activities and the company's statements. The main aim of the financial audit is to provide an

accurate estimate of the company's operational transactions.

2.2 Describe how these principles within own

area of responsibility.

There are various principles of financial auditing which can be followed by the

management of Ryanair and these are discussed below:

Planning and accountability: Until beginning their job, the auditor must prepare for their

work. In preparation, the auditor shall settle on the accounting of the organisation and the

internal management protocols. The auditors should behave in the preferences of the key

stakeholders, taking into account the broader public interest.

Honesty and Integrity (Probity): Probability is the attribute of possessing good moral

values, i.e. fairness and integrity. Probity requires more than preventing unethical or unethical

conduct. Probity guarantees that all complicated procedures are performed in a manner that is

equitable, unbiased, and transparent and always in the best interest of the organizations. This

process includes the several activities such as procurement, disposal of assets, sponsorship,

marketing, administration of grant etc.

Impartiality, Objectivity, and Independence: The auditor’s approach must be unbiased.

Specific opinions would not be included in the investigation report (Banerjee and et.al., 2016).

The auditors must be seen as impartial in all their interactions with the clients. They express

view should be independently of the company and its management. Objectivity creates a

reasonable description of the whole article, i.e. content and expression. The integrity of the report

is greatly improved as it addresses facts in an objective manner.

6

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Conformance: The function of the independent auditors must be conducted out in

compliance with the standards of the accounting bodies as well as the legislative criteria. The

internal audit work is carried out during compliance with the International Guidelines for the

Professional Practice of Internal Auditing which adopted by the Institute of Internal Auditors

(IIA).

Above discussed principles should be in auditor and they need to understand their

obligations and accountability towards organization and their work. In context of Ryanair airline,

organization appoints internal as well as external auditors and make sure that these people are

aware about the principles of financial auditing. Auditor need to be honest, integrated, should be

independent for their activities and accountable for their actions. In addition, financial auditor of

Ryanair has to follow each and every accounting standard and keep important information

confidential from others (Brusca, Gómez‐villegas and Montesinos, 2016). During the auditing

process, auditor needs to keep evidences from others and give their final opinion or review on

the basis of it. This is the auditor's ability to perform a professional role with great experience,

competence and precision. The auditors must have expertise based on gained skills, training and

practical knowledge. Auditing needs an understanding of financial reporting and business

concerns, along with experience in collecting and analysing facts required to form an opinion.

2.3 Review the financial implications of using codes of ethics within in the context of corporate

responsibilit

The Code of Ethics is a guideline of standards meant to help businesses operate with

dignity and fairness. The Code of Ethics should describe the mission and values of a company or

company, the manner in which staff are required to solve problems, the moral principles focused

on the company’s values, and the requirements which the practitioner is bound. The Code of

Ethics also related to as the Code of Ethics, which covers areas such as corporate ethics, the

Code of Professional Practice and the Code of Conduct for employees. In relation to Ryanair

airline, organization needs to follow such code of ethics in order to fulfil their corporate

responsibilities (Darwanis, Saputra and Kartini, 2016). The financial implication of Code of

Ethics is important for Ryanair airline because it allows workers or representatives of the

corporation to make effective decisions that are compatible with company principles in the

absence guideline or direct oversight. The Code of Ethics will improve decision making

7

compliance with the standards of the accounting bodies as well as the legislative criteria. The

internal audit work is carried out during compliance with the International Guidelines for the

Professional Practice of Internal Auditing which adopted by the Institute of Internal Auditors

(IIA).

Above discussed principles should be in auditor and they need to understand their

obligations and accountability towards organization and their work. In context of Ryanair airline,

organization appoints internal as well as external auditors and make sure that these people are

aware about the principles of financial auditing. Auditor need to be honest, integrated, should be

independent for their activities and accountable for their actions. In addition, financial auditor of

Ryanair has to follow each and every accounting standard and keep important information

confidential from others (Brusca, Gómez‐villegas and Montesinos, 2016). During the auditing

process, auditor needs to keep evidences from others and give their final opinion or review on

the basis of it. This is the auditor's ability to perform a professional role with great experience,

competence and precision. The auditors must have expertise based on gained skills, training and

practical knowledge. Auditing needs an understanding of financial reporting and business

concerns, along with experience in collecting and analysing facts required to form an opinion.

2.3 Review the financial implications of using codes of ethics within in the context of corporate

responsibilit

The Code of Ethics is a guideline of standards meant to help businesses operate with

dignity and fairness. The Code of Ethics should describe the mission and values of a company or

company, the manner in which staff are required to solve problems, the moral principles focused

on the company’s values, and the requirements which the practitioner is bound. The Code of

Ethics also related to as the Code of Ethics, which covers areas such as corporate ethics, the

Code of Professional Practice and the Code of Conduct for employees. In relation to Ryanair

airline, organization needs to follow such code of ethics in order to fulfil their corporate

responsibilities (Darwanis, Saputra and Kartini, 2016). The financial implication of Code of

Ethics is important for Ryanair airline because it allows workers or representatives of the

corporation to make effective decisions that are compatible with company principles in the

absence guideline or direct oversight. The Code of Ethics will improve decision making

7

process in an organisation and make things easier for workers to be self-employed. There is some

most effective and essential code of ethics which required implementing and these are as follow:

Honesty: Ethical leaders are honest and fair throughout all their activities, and therefore do

not knowingly mislead or manipulate others by falsehoods, overgeneralizations, half-truths,

systematic omissions, by every other way.

Integrity: Ethical managers show the integrity and strength of the principles and doing

what they believe is the truth even though there is massive pressure to do anything else. They are

trustworthy, honest and upright and they will struggle for their values. They would not betray the

concept of opportunism, be dishonest or opportunistic.

Fairness: Ethical management have to be honest and equitable in all involvements, they do

not wield power unfairly but don't use over-arching or immoral means to achieve or retain any

benefit or take unfair advantage of the errors or problems of someone else (Dennis, 2018).

People manifest a dedication to fairness, equal rights of persons, empathy and appreciation of

differences. They are open-minded and able to recognise that they are incorrect and, where

necessary, they will change their positions and convictions.

Law abiding: Ethical leaders comply with the statutes, laws and guidelines applicable to

their business practises.

Accountable: Ethical managers and management should be understand and take personal

responsibility for the ethical consistency of their actions and omissions against themselves, their

employees, their businesses and their societies.

2.4 Explain how you would make suitable adjustments to improve good practice and

transparency

In order to improve good practice and transparency, management of Ryanair airline need to

do some modification for the effective results. They need to improve their communication with

the entire staff and it should be in flow on regular basis and managers of Ryanair also need to

manage individual performance by use of effective appraisal system. In addition, they need to

motivate people to perform better which helps in boosting their performance as well as employee

efficiency. These are best ways to improve their good practices and further for transparency,

managers need to make this a part of company’s policy which has to follow each and every one

in their work. Managers or leaders most of the time face lot of difficult situations and should

have such competencies to resolve such issues or conflict at workplace. In addition, management

8

most effective and essential code of ethics which required implementing and these are as follow:

Honesty: Ethical leaders are honest and fair throughout all their activities, and therefore do

not knowingly mislead or manipulate others by falsehoods, overgeneralizations, half-truths,

systematic omissions, by every other way.

Integrity: Ethical managers show the integrity and strength of the principles and doing

what they believe is the truth even though there is massive pressure to do anything else. They are

trustworthy, honest and upright and they will struggle for their values. They would not betray the

concept of opportunism, be dishonest or opportunistic.

Fairness: Ethical management have to be honest and equitable in all involvements, they do

not wield power unfairly but don't use over-arching or immoral means to achieve or retain any

benefit or take unfair advantage of the errors or problems of someone else (Dennis, 2018).

People manifest a dedication to fairness, equal rights of persons, empathy and appreciation of

differences. They are open-minded and able to recognise that they are incorrect and, where

necessary, they will change their positions and convictions.

Law abiding: Ethical leaders comply with the statutes, laws and guidelines applicable to

their business practises.

Accountable: Ethical managers and management should be understand and take personal

responsibility for the ethical consistency of their actions and omissions against themselves, their

employees, their businesses and their societies.

2.4 Explain how you would make suitable adjustments to improve good practice and

transparency

In order to improve good practice and transparency, management of Ryanair airline need to

do some modification for the effective results. They need to improve their communication with

the entire staff and it should be in flow on regular basis and managers of Ryanair also need to

manage individual performance by use of effective appraisal system. In addition, they need to

motivate people to perform better which helps in boosting their performance as well as employee

efficiency. These are best ways to improve their good practices and further for transparency,

managers need to make this a part of company’s policy which has to follow each and every one

in their work. Managers or leaders most of the time face lot of difficult situations and should

have such competencies to resolve such issues or conflict at workplace. In addition, management

8

and managers need to provide a chance to their subordinates to ask anything through conducting

proper session (Hope, Thomas and Vyas, 2013). This activity will give

staff member’s opportunity to ask a question that they would not otherwise have the opportunity

to say. Leader of a larger company such as Ryanair airline, this kind of practice may be

especially important, as workers can never had an opportunity to meet them and ask anything.

2.5 Explain ways in which a true and fair view of assets, liabilities, profits and costs can be

presented

True and fair view of assets, liability, profitability and cost will be possible

through auditing of each account. That means, financial statements of a company is free

from material misstatement and accurately represent the financial condition and performance of

the organisation.

True view of accounts suggests that the financial reports are completely accurate and have

also been ready in accordance with the relevant accounting principles, such as IFRS, and

therefore do not encompass any fraudulent activities that may manipulate users of financial

reports (Karadag, 2017). Misstatements can arise from material mistakes in the accounts of

transactions and balances.

Fair view of accounts ensures that the overall financial reports present the details

accurately without any aspect of prejudice and represent the accounting treatment of the

activities instead of just the legal type.

In relation to Ryanair Airline, in order to identify the ways of presenting true and fair view

of several components. Organizations need to produce different financial statement for it, such as

balance sheet for the fair and true view of assets and liabilities. On the other side, profit and

expenses of the organizations will be evaluated with the help of income and loss statements.

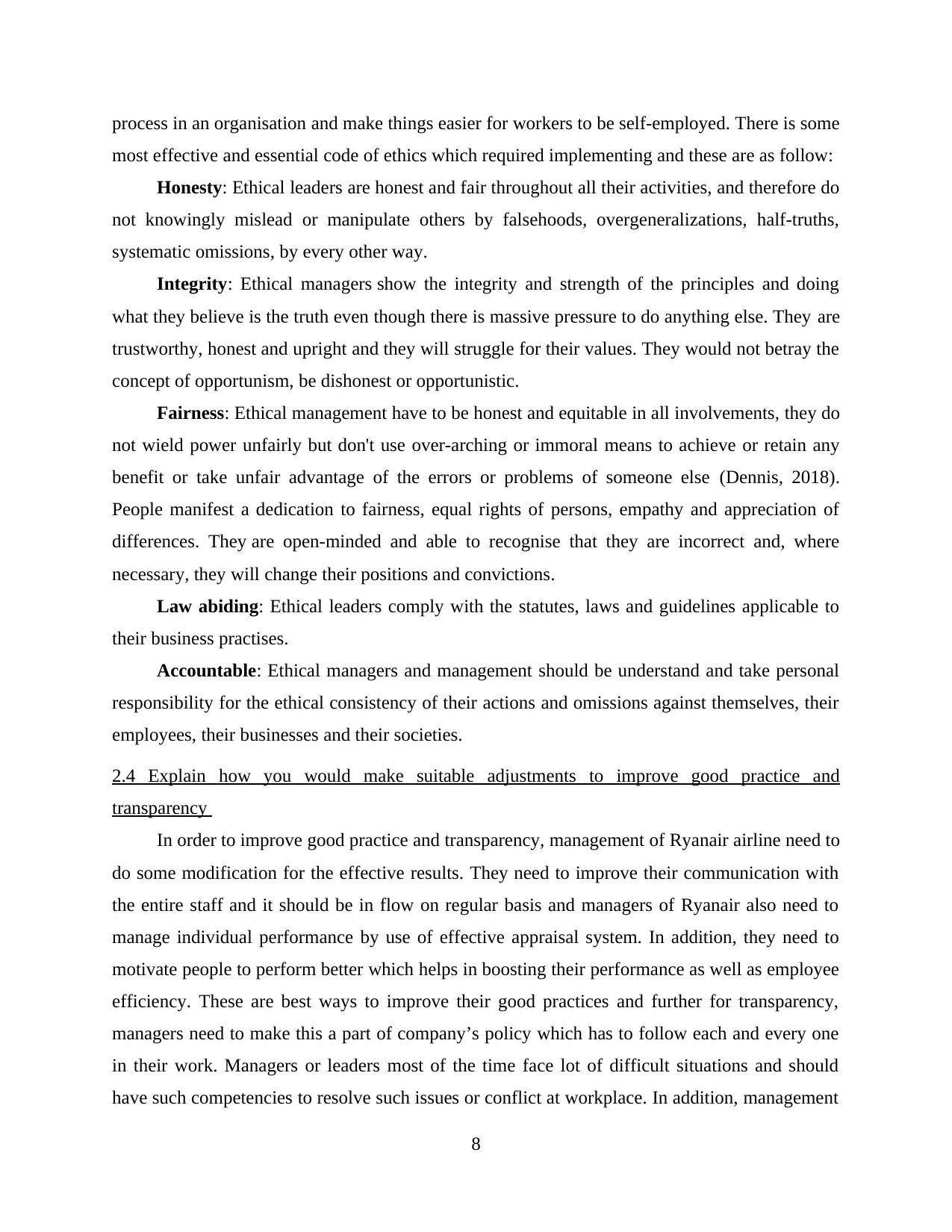

Balance sheet: It is one of the financial statements which help the organization to identify

their financial position in terms of their resources and obligations. This statement is the way

which provides true and fair view of assets and liabilities (Kourtis, Kourtis and Curtis, 2019).

Amount of each item recorded in this account for the purpose of analysis and to make future

decisions. In addition, any realistic gain or loss also recorded in this will be beneficial for

stakeholders to analyse before making any investment decisions. There are several items

recorded in this financial statement which provide true and fair view of total liabilities and total

assets. These are as follow:

9

proper session (Hope, Thomas and Vyas, 2013). This activity will give

staff member’s opportunity to ask a question that they would not otherwise have the opportunity

to say. Leader of a larger company such as Ryanair airline, this kind of practice may be

especially important, as workers can never had an opportunity to meet them and ask anything.

2.5 Explain ways in which a true and fair view of assets, liabilities, profits and costs can be

presented

True and fair view of assets, liability, profitability and cost will be possible

through auditing of each account. That means, financial statements of a company is free

from material misstatement and accurately represent the financial condition and performance of

the organisation.

True view of accounts suggests that the financial reports are completely accurate and have

also been ready in accordance with the relevant accounting principles, such as IFRS, and

therefore do not encompass any fraudulent activities that may manipulate users of financial

reports (Karadag, 2017). Misstatements can arise from material mistakes in the accounts of

transactions and balances.

Fair view of accounts ensures that the overall financial reports present the details

accurately without any aspect of prejudice and represent the accounting treatment of the

activities instead of just the legal type.

In relation to Ryanair Airline, in order to identify the ways of presenting true and fair view

of several components. Organizations need to produce different financial statement for it, such as

balance sheet for the fair and true view of assets and liabilities. On the other side, profit and

expenses of the organizations will be evaluated with the help of income and loss statements.

Balance sheet: It is one of the financial statements which help the organization to identify

their financial position in terms of their resources and obligations. This statement is the way

which provides true and fair view of assets and liabilities (Kourtis, Kourtis and Curtis, 2019).

Amount of each item recorded in this account for the purpose of analysis and to make future

decisions. In addition, any realistic gain or loss also recorded in this will be beneficial for

stakeholders to analyse before making any investment decisions. There are several items

recorded in this financial statement which provide true and fair view of total liabilities and total

assets. These are as follow:

9

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

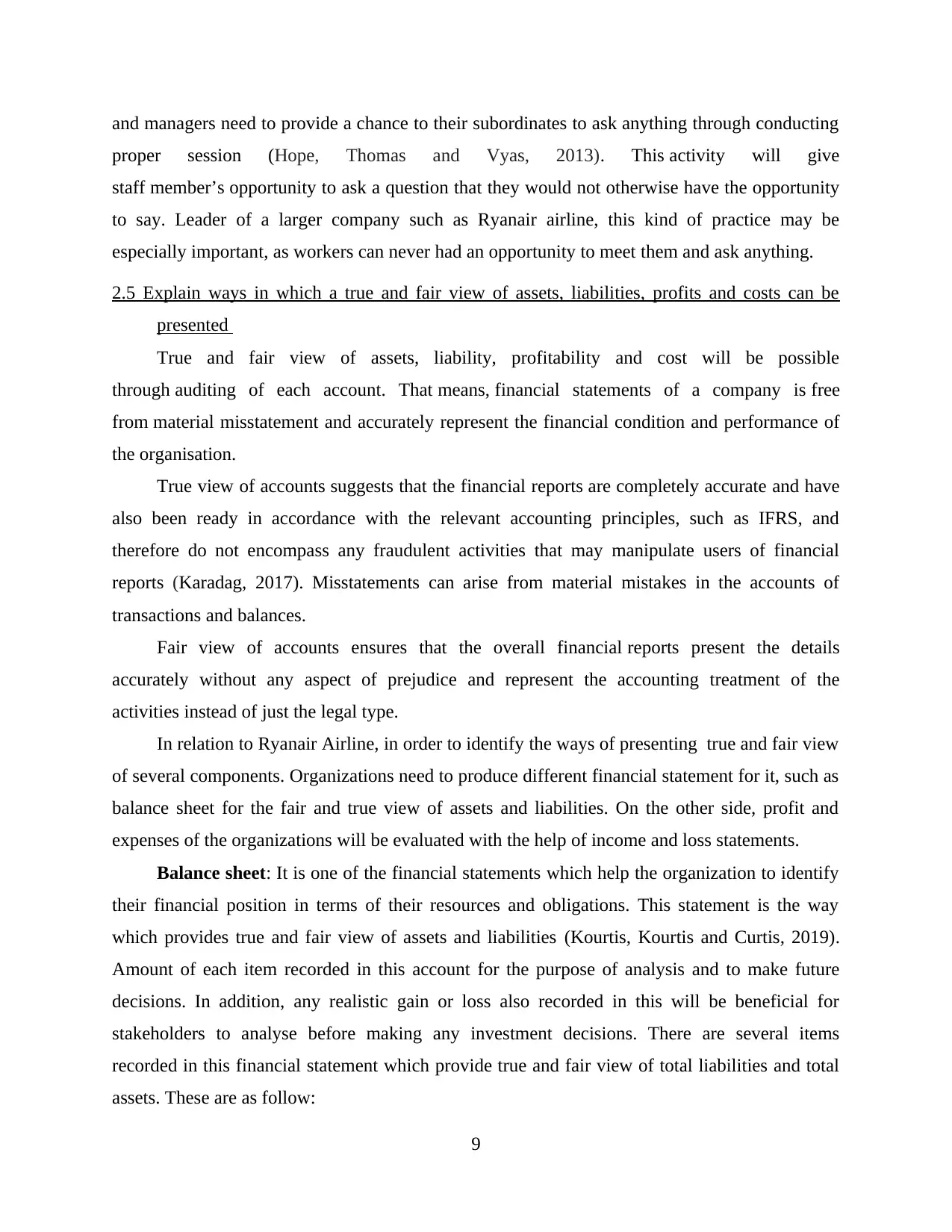

Income and loss statement: With the help of this statement organization able to identify

their actual profit or loss (cost) of business. This is the way of identifying true and fair view of

their activities (Lawrence, 2013). All the unrealised profit or loss recorded in this profit and loss

statement. Since reasonable expectations are constantly increasing, some suggest that the

acknowledgment of net income profit and losses is deceptive. In an attempt to address this

dilemma, a framework of comprehensive income has been implemented. Comprehensive income

covers income and sales, expenditures and losses recorded in net income, plus any gains and

losses that circumvent net income but influence the equity of the shareholder.

10

their actual profit or loss (cost) of business. This is the way of identifying true and fair view of

their activities (Lawrence, 2013). All the unrealised profit or loss recorded in this profit and loss

statement. Since reasonable expectations are constantly increasing, some suggest that the

acknowledgment of net income profit and losses is deceptive. In an attempt to address this

dilemma, a framework of comprehensive income has been implemented. Comprehensive income

covers income and sales, expenditures and losses recorded in net income, plus any gains and

losses that circumvent net income but influence the equity of the shareholder.

10

In the case of fair and true view of accounting, the declaration of sales is the residual

indicator of the balance sheet (Loke, 2017). The statement of income indicates adjustments in the

fair value measured on the balance sheet, and no independent definition of income guides the

statement of income.

The details given by the true or fair value of balance sheets and the income statement does

have the following characteristics:

The balance sheet is a total value accounting and the purpose of the assessment is

fulfilled in the balance sheet.

The income statement measures 'financial income' since it is essentially a shift of price

over a period of time.

Income records management stewardship of value-added owners.

Incomes are unspecific about potential income and valuation; earnings are increases in

valuation and do not forecast future values, nor do they notify regarding this value.

Although the income statement doesn't really disclose value, it tracks frequent price

movements and therefore communicates about risk.

Whereas the report is prepared for annual basis. The time series of income volatility

shows the risk of the company.

LO 3

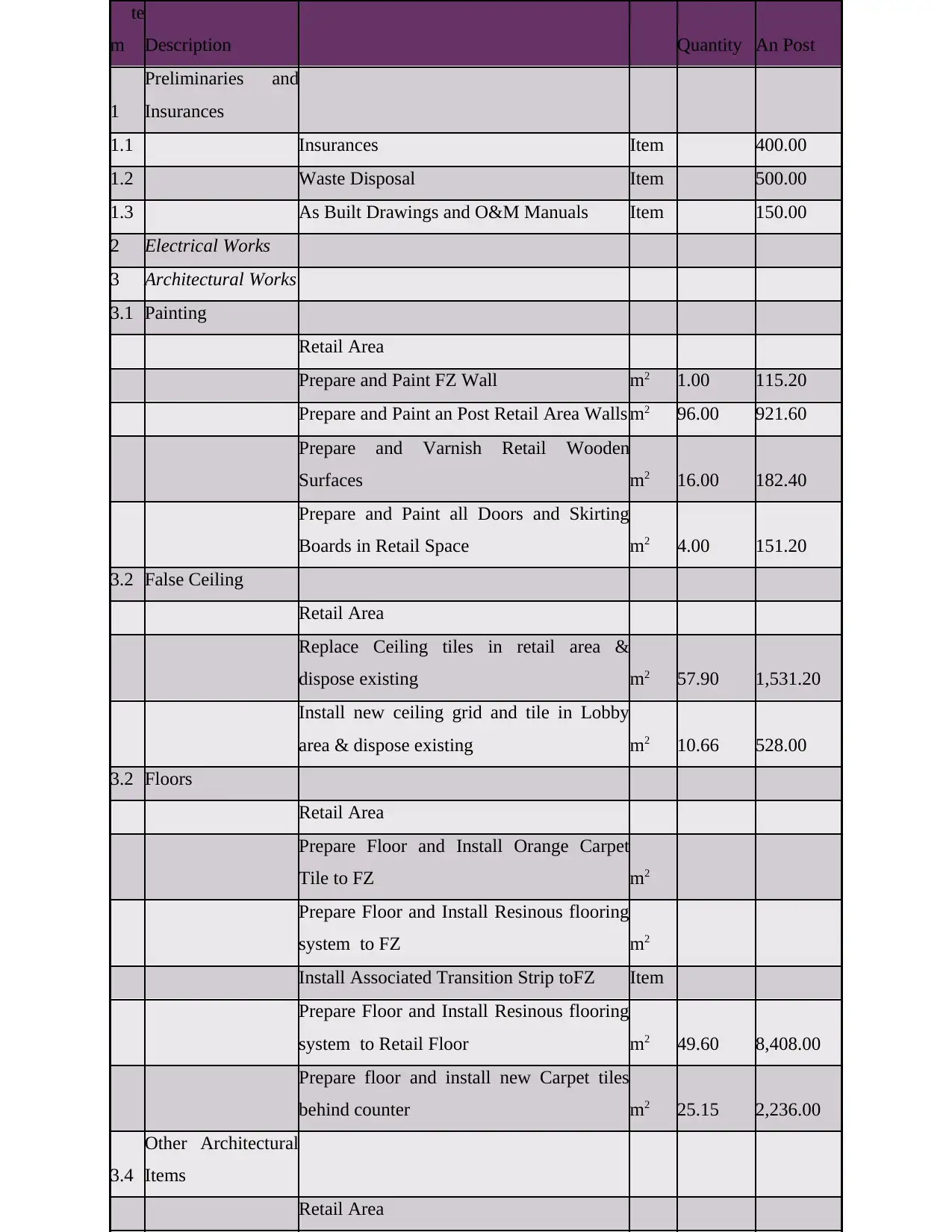

3.1 Explain how organizations would prepare, review and manage revenue budgets

Revenue budgets are projected sales profits and expenses of a corporation, including

capital spending. It is important that business decide whether they have sufficient financial

resources to function, expand business, and eventually make money (Michalak, 2016). Without

such a preparation, the future of the business will be unclear; since they may not know how often

money should take or spend. Revenue budgets will ensure that a company distribute capital

efficiently and therefore save time, effort as well as money. There is an example of revenue

budget which mentioned in the below table. It will provide better understanding that what kind of

items mentioned in this budget which helps the organization to estimate their sales revenue.

Similarly, Ryanair airline prepare their revenue budget to perform their further activities

accordingly and ensure to maximise their earnings and minimise the expanses.

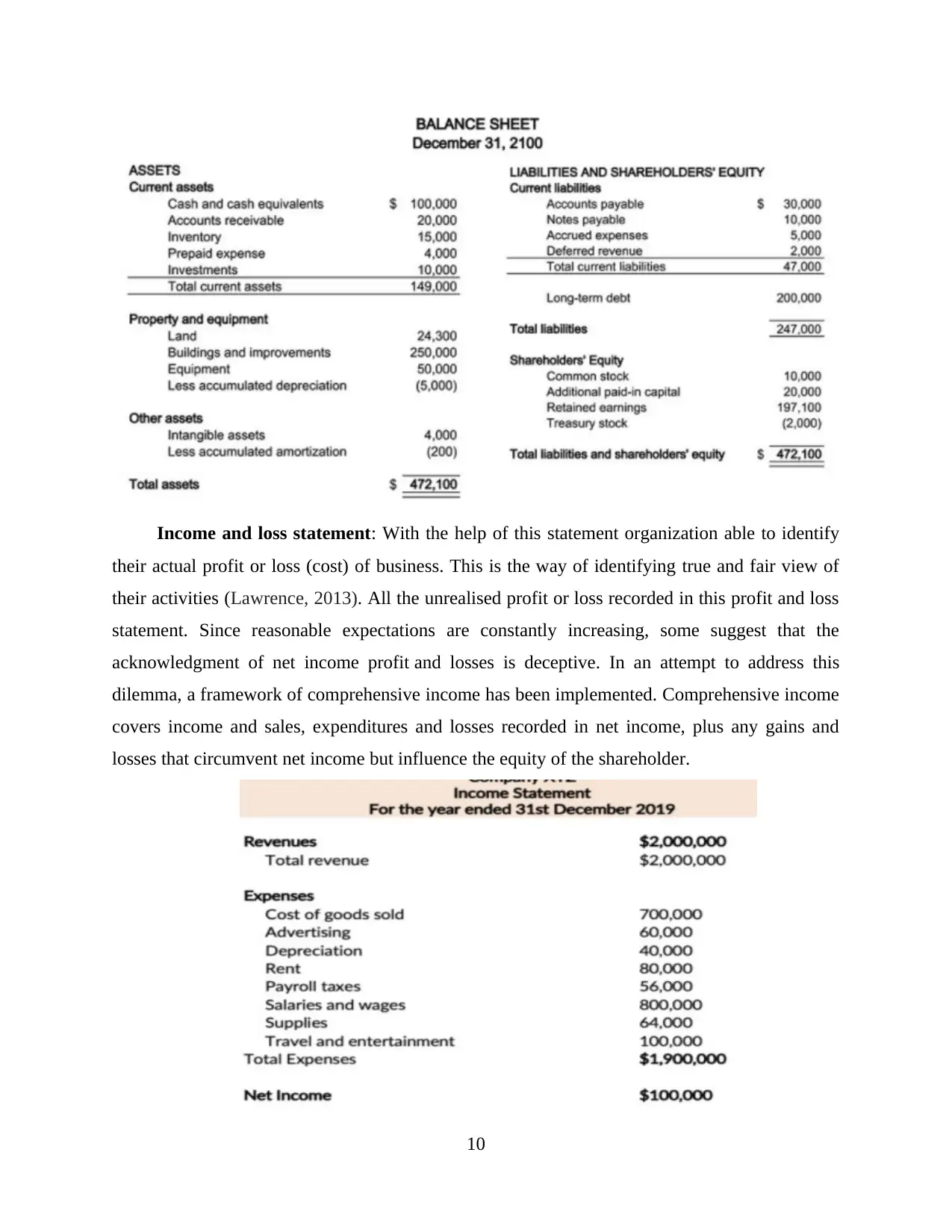

Facilities Budget

11

indicator of the balance sheet (Loke, 2017). The statement of income indicates adjustments in the

fair value measured on the balance sheet, and no independent definition of income guides the

statement of income.

The details given by the true or fair value of balance sheets and the income statement does

have the following characteristics:

The balance sheet is a total value accounting and the purpose of the assessment is

fulfilled in the balance sheet.

The income statement measures 'financial income' since it is essentially a shift of price

over a period of time.

Income records management stewardship of value-added owners.

Incomes are unspecific about potential income and valuation; earnings are increases in

valuation and do not forecast future values, nor do they notify regarding this value.

Although the income statement doesn't really disclose value, it tracks frequent price

movements and therefore communicates about risk.

Whereas the report is prepared for annual basis. The time series of income volatility

shows the risk of the company.

LO 3

3.1 Explain how organizations would prepare, review and manage revenue budgets

Revenue budgets are projected sales profits and expenses of a corporation, including

capital spending. It is important that business decide whether they have sufficient financial

resources to function, expand business, and eventually make money (Michalak, 2016). Without

such a preparation, the future of the business will be unclear; since they may not know how often

money should take or spend. Revenue budgets will ensure that a company distribute capital

efficiently and therefore save time, effort as well as money. There is an example of revenue

budget which mentioned in the below table. It will provide better understanding that what kind of

items mentioned in this budget which helps the organization to estimate their sales revenue.

Similarly, Ryanair airline prepare their revenue budget to perform their further activities

accordingly and ensure to maximise their earnings and minimise the expanses.

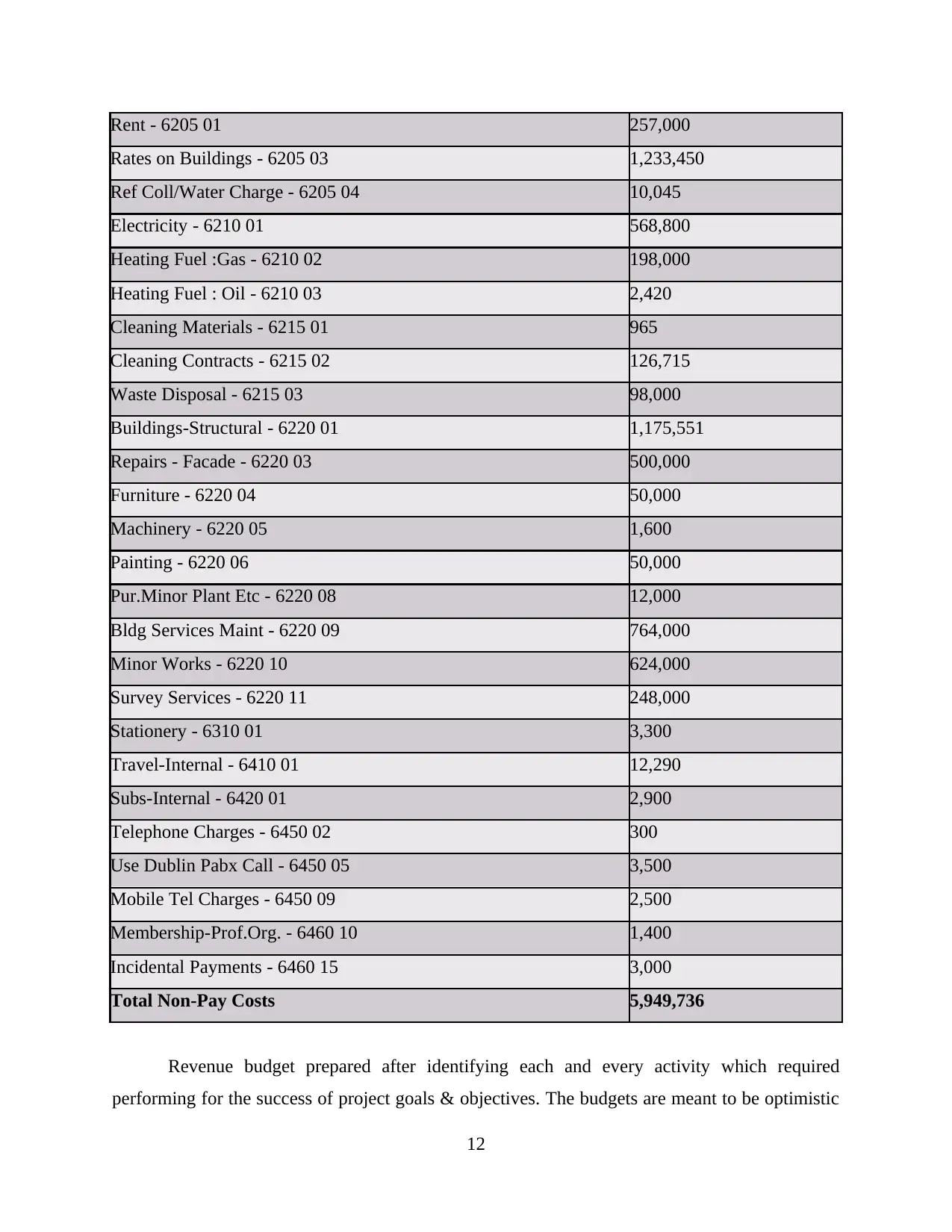

Facilities Budget

11

Rent - 6205 01 257,000

Rates on Buildings - 6205 03 1,233,450

Ref Coll/Water Charge - 6205 04 10,045

Electricity - 6210 01 568,800

Heating Fuel :Gas - 6210 02 198,000

Heating Fuel : Oil - 6210 03 2,420

Cleaning Materials - 6215 01 965

Cleaning Contracts - 6215 02 126,715

Waste Disposal - 6215 03 98,000

Buildings-Structural - 6220 01 1,175,551

Repairs - Facade - 6220 03 500,000

Furniture - 6220 04 50,000

Machinery - 6220 05 1,600

Painting - 6220 06 50,000

Pur.Minor Plant Etc - 6220 08 12,000

Bldg Services Maint - 6220 09 764,000

Minor Works - 6220 10 624,000

Survey Services - 6220 11 248,000

Stationery - 6310 01 3,300

Travel-Internal - 6410 01 12,290

Subs-Internal - 6420 01 2,900

Telephone Charges - 6450 02 300

Use Dublin Pabx Call - 6450 05 3,500

Mobile Tel Charges - 6450 09 2,500

Membership-Prof.Org. - 6460 10 1,400

Incidental Payments - 6460 15 3,000

Total Non-Pay Costs 5,949,736

Revenue budget prepared after identifying each and every activity which required

performing for the success of project goals & objectives. The budgets are meant to be optimistic

12

Rates on Buildings - 6205 03 1,233,450

Ref Coll/Water Charge - 6205 04 10,045

Electricity - 6210 01 568,800

Heating Fuel :Gas - 6210 02 198,000

Heating Fuel : Oil - 6210 03 2,420

Cleaning Materials - 6215 01 965

Cleaning Contracts - 6215 02 126,715

Waste Disposal - 6215 03 98,000

Buildings-Structural - 6220 01 1,175,551

Repairs - Facade - 6220 03 500,000

Furniture - 6220 04 50,000

Machinery - 6220 05 1,600

Painting - 6220 06 50,000

Pur.Minor Plant Etc - 6220 08 12,000

Bldg Services Maint - 6220 09 764,000

Minor Works - 6220 10 624,000

Survey Services - 6220 11 248,000

Stationery - 6310 01 3,300

Travel-Internal - 6410 01 12,290

Subs-Internal - 6420 01 2,900

Telephone Charges - 6450 02 300

Use Dublin Pabx Call - 6450 05 3,500

Mobile Tel Charges - 6450 09 2,500

Membership-Prof.Org. - 6460 10 1,400

Incidental Payments - 6460 15 3,000

Total Non-Pay Costs 5,949,736

Revenue budget prepared after identifying each and every activity which required

performing for the success of project goals & objectives. The budgets are meant to be optimistic

12

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

but practical. Don't project a budget that they didn't fulfil but just don't underestimate the

potential. This is how to get started. Next, list the two to six goals that organization plan to

accomplish over the duration that company is budgeting for (Miller and Oldroyd, 2018). There

are some essential steps which required to follow when managers of Ryanair going to prepare

revenue budget. These are as follow:

Review the company's environment assumptions which are used as the foundation over

the previous budget, and modify as required.

Determine the adequacy of the main bottleneck that prevents the business from

producing additional revenues and identify how it would influence any extra revenue

success of the firm.

Evaluate a most probable level of fund that would be accessible during the budget cycle

that will restrict development plans.

Copy the planning stage guidelines from the instruction booklet used in the previous

year. Review it by providing the real cost accrued in the current year and also sneezes

this data for the entire current year. Add a statement to the package, defining phase

costing detail, bottlenecks, and projected funding limits for the next budget year.

Get the sales estimate from the sales manager, verify this with the CEO, and then

allocate to the other department heads. They use sales details as a basis for the creation

of their own budgets.

Get budget plan from all agencies, check mistakes, and compare bottleneck, funding,

and stage cost constraints. Change the budgets as needed.

Justify all capital budget proposals and forward ideas and questions to the management

team for the further analysis.

3.2 Review and manage budgets

In order to review the revenue budget, senior management team need to discuss the budget.

Highlight potential restriction concerns and any constraints created by difficulties with funding.

Note down all suggestions which made by the team of management and communicate this

information to the budget makers, asking them to change their budgets accordingly.

Review of budget is the best way to manage the entire budget properly because managers

need to monitor each and every activity and ensure that everything will be work according to the

budget (Mitchell, 2017). Team members perform their task accordingly and spend allotted

13

potential. This is how to get started. Next, list the two to six goals that organization plan to

accomplish over the duration that company is budgeting for (Miller and Oldroyd, 2018). There

are some essential steps which required to follow when managers of Ryanair going to prepare

revenue budget. These are as follow:

Review the company's environment assumptions which are used as the foundation over

the previous budget, and modify as required.

Determine the adequacy of the main bottleneck that prevents the business from

producing additional revenues and identify how it would influence any extra revenue

success of the firm.

Evaluate a most probable level of fund that would be accessible during the budget cycle

that will restrict development plans.

Copy the planning stage guidelines from the instruction booklet used in the previous

year. Review it by providing the real cost accrued in the current year and also sneezes

this data for the entire current year. Add a statement to the package, defining phase

costing detail, bottlenecks, and projected funding limits for the next budget year.

Get the sales estimate from the sales manager, verify this with the CEO, and then

allocate to the other department heads. They use sales details as a basis for the creation

of their own budgets.

Get budget plan from all agencies, check mistakes, and compare bottleneck, funding,

and stage cost constraints. Change the budgets as needed.

Justify all capital budget proposals and forward ideas and questions to the management

team for the further analysis.

3.2 Review and manage budgets

In order to review the revenue budget, senior management team need to discuss the budget.

Highlight potential restriction concerns and any constraints created by difficulties with funding.

Note down all suggestions which made by the team of management and communicate this

information to the budget makers, asking them to change their budgets accordingly.

Review of budget is the best way to manage the entire budget properly because managers

need to monitor each and every activity and ensure that everything will be work according to the

budget (Mitchell, 2017). Team members perform their task accordingly and spend allotted

13

amount which helps in completing project within project budget. Managers make sure that, all

the work completed according to the plan and for this, they need to review each activity of staff

members and further discussed with the entire management team for transparency and if any

changes they required doing. They can modify during the project which helps in achieving

business goals & objectives.

3.3 Set out how to apply the techniques used by facilities managers to set, acquire, review and

manage capital budgets

In this capital budgets, cost associated with long-term investments are referred to as capital

costs. These costs are mostly covered by capital investment that could be used to develop or

liberalise a business. It is mainly focuses on various information regarding buildings, appliances,

plant and fixtures that the organization needs to carry out its operations. Assessing what may or

cannot be spelled correctly is usually the responsibility of the finance manager. There are some

effective techniques which are used by the Ryanair airline managers to set, acquire, review and

manage capital budget. Some of the techniques are as follow:

Payback Method: This is the easiest way to estimate budget for new asset. This method of

repaying is to determine how long it would take for a business to repay an asset (Muneer, Ahmad

and Ali, 2017). The shorter the recovery period is define that faster the business is able to restore

their cost of a new device.

Net Present Value (NPV) Method: This system is like a system of repaying; apart from

one crucial aspect that money does not have the same long term value. This formula computes

the variation between the cost of the asset and the cumulative cash flows of the asset. The word

'current value' is used when potential cash flows decline in value. If the discounted potential cash

flows surpass the value of the product, the investment is projected to be sustainable. However, if

the expenses surpass cash flows, the plan is not projected to be profitable. The greatest advantage

of the NPV approach over the repayment method is that it allows for a drop in the value over

time. However, a big downside would be that the NPV approach is based on assumptions. If the

business encounters unforeseen problems after the capital has been spent, the figures might be

inaccurate, creating confusion in the profit margin.

Internal Rate of Return (IRR) Method: This method is perhaps the most complicated of

the three. This approach contrasts the yield on the asset with the expense of funding the project.

It is identical to, and contains, the NPV formula used to measure the rate of return. If the IRR is

14

the work completed according to the plan and for this, they need to review each activity of staff

members and further discussed with the entire management team for transparency and if any

changes they required doing. They can modify during the project which helps in achieving

business goals & objectives.

3.3 Set out how to apply the techniques used by facilities managers to set, acquire, review and

manage capital budgets

In this capital budgets, cost associated with long-term investments are referred to as capital

costs. These costs are mostly covered by capital investment that could be used to develop or

liberalise a business. It is mainly focuses on various information regarding buildings, appliances,

plant and fixtures that the organization needs to carry out its operations. Assessing what may or

cannot be spelled correctly is usually the responsibility of the finance manager. There are some

effective techniques which are used by the Ryanair airline managers to set, acquire, review and

manage capital budget. Some of the techniques are as follow:

Payback Method: This is the easiest way to estimate budget for new asset. This method of

repaying is to determine how long it would take for a business to repay an asset (Muneer, Ahmad

and Ali, 2017). The shorter the recovery period is define that faster the business is able to restore

their cost of a new device.

Net Present Value (NPV) Method: This system is like a system of repaying; apart from

one crucial aspect that money does not have the same long term value. This formula computes

the variation between the cost of the asset and the cumulative cash flows of the asset. The word

'current value' is used when potential cash flows decline in value. If the discounted potential cash

flows surpass the value of the product, the investment is projected to be sustainable. However, if

the expenses surpass cash flows, the plan is not projected to be profitable. The greatest advantage

of the NPV approach over the repayment method is that it allows for a drop in the value over

time. However, a big downside would be that the NPV approach is based on assumptions. If the

business encounters unforeseen problems after the capital has been spent, the figures might be

inaccurate, creating confusion in the profit margin.

Internal Rate of Return (IRR) Method: This method is perhaps the most complicated of

the three. This approach contrasts the yield on the asset with the expense of funding the project.

It is identical to, and contains, the NPV formula used to measure the rate of return. If the IRR is

14

higher than the cost, the project is meant to be profitable. However, unless the cost exceeds the

return, the project is meant to have a loss.

Above of the capital budgeting methods are used to make decisions in context of the

organization (Schroeder, Clark and Cathey, 2019). These methods helps the managers of Ryanair

airline to review and manage capital budget and ensure that team members will perform their

work accordingly which helps in achieving their business goals & objectives.

3.4 Set capital budgets

Capital budgeting techniques are used by the managers for decision-making procedures

which are set of analyses that help organizations to determine that which plan is best. Managers

use capital budgeting strategies to determine which project can bring the most value to the

business.

15

return, the project is meant to have a loss.

Above of the capital budgeting methods are used to make decisions in context of the

organization (Schroeder, Clark and Cathey, 2019). These methods helps the managers of Ryanair

airline to review and manage capital budget and ensure that team members will perform their

work accordingly which helps in achieving their business goals & objectives.

3.4 Set capital budgets

Capital budgeting techniques are used by the managers for decision-making procedures

which are set of analyses that help organizations to determine that which plan is best. Managers

use capital budgeting strategies to determine which project can bring the most value to the

business.

15

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

16

te

m Description Quantity An Post

1

Preliminaries and

Insurances

1.1 Insurances Item 400.00

1.2 Waste Disposal Item 500.00

1.3 As Built Drawings and O&M Manuals Item 150.00

2 Electrical Works

3 Architectural Works

3.1 Painting

Retail Area

Prepare and Paint FZ Wall m2 1.00 115.20

Prepare and Paint an Post Retail Area Walls m2 96.00 921.60

Prepare and Varnish Retail Wooden

Surfaces m2 16.00 182.40

Prepare and Paint all Doors and Skirting

Boards in Retail Space m2 4.00 151.20

3.2 False Ceiling

Retail Area

Replace Ceiling tiles in retail area &

dispose existing m2 57.90 1,531.20

Install new ceiling grid and tile in Lobby

area & dispose existing m2 10.66 528.00

3.2 Floors

Retail Area

Prepare Floor and Install Orange Carpet

Tile to FZ m2

Prepare Floor and Install Resinous flooring

system to FZ m2

Install Associated Transition Strip toFZ Item

Prepare Floor and Install Resinous flooring

system to Retail Floor m2 49.60 8,408.00

Prepare floor and install new Carpet tiles

behind counter m2 25.15 2,236.00

3.4

Other Architectural

Items

Retail Area

te

m Description Quantity An Post

1

Preliminaries and

Insurances

1.1 Insurances Item 400.00

1.2 Waste Disposal Item 500.00

1.3 As Built Drawings and O&M Manuals Item 150.00

2 Electrical Works

3 Architectural Works

3.1 Painting

Retail Area

Prepare and Paint FZ Wall m2 1.00 115.20

Prepare and Paint an Post Retail Area Walls m2 96.00 921.60

Prepare and Varnish Retail Wooden

Surfaces m2 16.00 182.40

Prepare and Paint all Doors and Skirting

Boards in Retail Space m2 4.00 151.20

3.2 False Ceiling

Retail Area

Replace Ceiling tiles in retail area &

dispose existing m2 57.90 1,531.20

Install new ceiling grid and tile in Lobby

area & dispose existing m2 10.66 528.00

3.2 Floors

Retail Area

Prepare Floor and Install Orange Carpet

Tile to FZ m2

Prepare Floor and Install Resinous flooring

system to FZ m2

Install Associated Transition Strip toFZ Item

Prepare Floor and Install Resinous flooring

system to Retail Floor m2 49.60 8,408.00

Prepare floor and install new Carpet tiles

behind counter m2 25.15 2,236.00

3.4

Other Architectural

Items

Retail Area

3.5 Review and manage capital budgets

There are several ways that managers or organizations can use to manage and review

capital budget through identifying and evaluating potential opportunities, estimating operating

and implementing cost, estimate the entire cash flow from the different stages, identify potential

risk and further formulate strategies to mitigate such risk etc. These activities used to review the

entire process and further manage these things through communicating with senior management

for the valuable feedback. Adjustment will be modified in the current budget for effective

performance.

3.6 Explain the tools of financial appraisal and how these are used to inform financial

management and budgetary decisions

There are several financial appraisal tools which are used by the organizations to inform

financial management and make budgetary decisions. These tools also used by the management

of Ryanair airlines when they are going to invest somewhere and they wanted to evaluate that

investment is beneficial for their organizations and not. These are discussed below:

Accounting rate of return (ARR): It compares the income they plan to make on

their investment to the sum intend to spend (Siminica, Motoi and Dumitru, 2017). It is typically

measured as the average annual benefit that expect and over lifetime of a capital budgeting

compared to the overall amount of invested by the organizations. Higher the ARR is beneficial as

well as promotable for the organization to invest money into particular project. In case of two

options, lower ARR is rejected due to low profitability.

Payback period: It is a straightforward method for measuring expenditure by the amount

of time it will take to be repaid. It is typically a default strategy for smaller companies and

depends on cash flow, not benefit. In this case, lower the recovery period is beneficial for the

organization because company able to recover their initial cost more faster in comparison to any

other project or option. Managers will make their investment decisions on the basis of recovery

period.

Discounted cash flow: It applies a discount rate to figure out the actual approximation of a

potential cash flow. There have been 2 types of discounting calculation methods such as net

present value (NPV) and the internal rate of return (IRR). In context of organization, NPV and

17

There are several ways that managers or organizations can use to manage and review

capital budget through identifying and evaluating potential opportunities, estimating operating

and implementing cost, estimate the entire cash flow from the different stages, identify potential

risk and further formulate strategies to mitigate such risk etc. These activities used to review the

entire process and further manage these things through communicating with senior management

for the valuable feedback. Adjustment will be modified in the current budget for effective

performance.

3.6 Explain the tools of financial appraisal and how these are used to inform financial

management and budgetary decisions

There are several financial appraisal tools which are used by the organizations to inform

financial management and make budgetary decisions. These tools also used by the management

of Ryanair airlines when they are going to invest somewhere and they wanted to evaluate that

investment is beneficial for their organizations and not. These are discussed below:

Accounting rate of return (ARR): It compares the income they plan to make on

their investment to the sum intend to spend (Siminica, Motoi and Dumitru, 2017). It is typically

measured as the average annual benefit that expect and over lifetime of a capital budgeting

compared to the overall amount of invested by the organizations. Higher the ARR is beneficial as

well as promotable for the organization to invest money into particular project. In case of two

options, lower ARR is rejected due to low profitability.

Payback period: It is a straightforward method for measuring expenditure by the amount

of time it will take to be repaid. It is typically a default strategy for smaller companies and

depends on cash flow, not benefit. In this case, lower the recovery period is beneficial for the

organization because company able to recover their initial cost more faster in comparison to any

other project or option. Managers will make their investment decisions on the basis of recovery

period.

Discounted cash flow: It applies a discount rate to figure out the actual approximation of a

potential cash flow. There have been 2 types of discounting calculation methods such as net

present value (NPV) and the internal rate of return (IRR). In context of organization, NPV and

17

IRR both are need to be high in compare to any other project and it should be prefer because it is

more profitable for the organization.

Analysis of investment risk and sensitivity: It is important for a practical risk assessment

where it helps in identifying potential risk. In practise, the greatest risk too many investments is

the damage they can create (White, 2017). Managers of the organization identify the potential

risk with the help of this tools and it further helps in financial management and making

budgetary decisions in respect of the organization.

Above discussed financial appraisal tools helps the managers or management to select best

project which helps in effective financial management as well as, it also helps in making

budgetary decisions.

LO 4

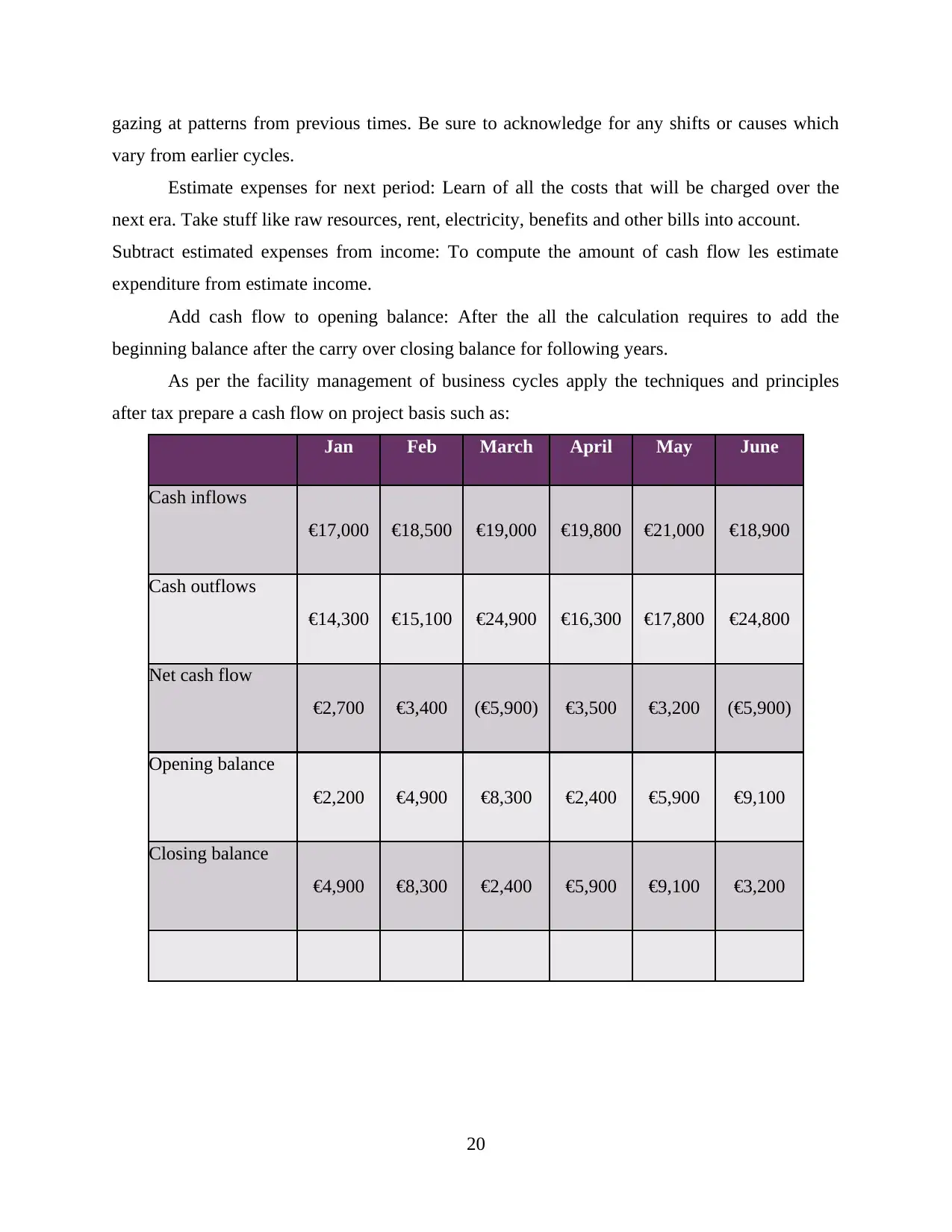

4.1. Apply the principles, techniques and processes of cash-flow projections to manage the flow

of cash within the facilities management business cycle, including how this impacts on

contracts and projects.

Cash flow forecasting helps to anticipate deposit account peaks and valleys. It helps to

organize lending and informs how often excess funds are expected to have at a particular point.

Most banks need projections until accepting a loan. Cash-flow errors are some of the toughest

and most popular errors start-ups make, including such avoiding them or comparing them with

income. Sometimes, investors just look for earnings that equal revenue less expenditures. Cash

flow refers to the flows of cash respectively into or out of a company (Hall and Antonopoulos,

2017). Cash inflows are transactions from clients or other outlets through a business. Cash

outflows apply to payments that a company makes

Total cash flow = cash inflow – cash outflow

Cash flow reflects the quality of a company's desire to implement its debt responsibilities.

Free cash flow allows businesses to fulfill payroll, reimburse vendors, meet loan obligations and

make dividends to holders. Cash may be produced by activities, or given by lenders or owners.

4.2 Apply the principles, techniques and

processes in the management of cash flow

for contracts and projects.

Principles of cash flow:

18

more profitable for the organization.

Analysis of investment risk and sensitivity: It is important for a practical risk assessment

where it helps in identifying potential risk. In practise, the greatest risk too many investments is

the damage they can create (White, 2017). Managers of the organization identify the potential

risk with the help of this tools and it further helps in financial management and making

budgetary decisions in respect of the organization.

Above discussed financial appraisal tools helps the managers or management to select best

project which helps in effective financial management as well as, it also helps in making

budgetary decisions.

LO 4

4.1. Apply the principles, techniques and processes of cash-flow projections to manage the flow

of cash within the facilities management business cycle, including how this impacts on

contracts and projects.

Cash flow forecasting helps to anticipate deposit account peaks and valleys. It helps to

organize lending and informs how often excess funds are expected to have at a particular point.

Most banks need projections until accepting a loan. Cash-flow errors are some of the toughest

and most popular errors start-ups make, including such avoiding them or comparing them with