Financial Analysis and Performance of United Overseas Bank

VerifiedAdded on 2023/01/13

|22

|4734

|89

Report

AI Summary

This report conducts a comprehensive financial analysis of United Overseas Bank (UOB), a major Singaporean multinational banking firm. The analysis begins with an introduction to UOB's operations and services, followed by a deep dive into its financial statements, employing horizontal and vertical analysis to assess trends in assets, liabilities, and revenue. The report then examines the economic landscape of the Singapore banking industry, highlighting its significance as a global financial hub. Key financial ratios are calculated and analyzed, including profitability (net margin, ROA, ROE), dividend ratios (yield, payout), stability and liquidity ratios (debt to equity, gearing, current ratio), and efficiency ratios (asset turnover, current asset turnover). UOB's performance is compared to industry averages, and its current market share price is assessed. The report also touches upon UOB's customer service and corporate governance compliance, including news impacts and brand reputation. Appendices provide detailed financial data, and the report concludes with an overview of UOB's financial standing and recommendations.

Financial Management 1

FINANCIAL MANAGEMENT

Author

Course

Professor

University

Date

FINANCIAL MANAGEMENT

Author

Course

Professor

University

Date

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Financial Management 2

Table of Contents

SECTION A...............................................................................................................................3

Introduction................................................................................................................................3

Financial Analysis......................................................................................................................3

Horizontal and Vertical Analysis of UOB Financial Statements...........................................3

Economic Analysis of the Banking Industry.........................................................................4

Financial Ratios......................................................................................................................4

Profitability........................................................................................................................4

Dividend Ratios..................................................................................................................6

Stability and Liquidity Ratios............................................................................................7

Efficiency...........................................................................................................................8

Compare UOB with Industry Average.......................................................................................9

UOB current market share price analysis.............................................................................10

UOB Customer Service........................................................................................................11

Section B: UOB Corporate Governance Compliance..............................................................12

News That Has Impact On Bank’s Financial Performance.................................................12

Impact on Brand and Reputation..........................................................................................12

Corporate Governance.........................................................................................................13

Conclusion................................................................................................................................13

REFERENCES.........................................................................................................................15

APPENDICES..........................................................................................................................17

Appendix 1: Horizontal analysis of UOB balance sheet......................................................17

Appendix 2: Vertical analysis of UOB balance sheet..........................................................18

Appendix 3: Horizontal analysis of UOB income statement...............................................19

Appendix 4: Vertical analysis of UOB income statement...................................................20

Table of Contents

SECTION A...............................................................................................................................3

Introduction................................................................................................................................3

Financial Analysis......................................................................................................................3

Horizontal and Vertical Analysis of UOB Financial Statements...........................................3

Economic Analysis of the Banking Industry.........................................................................4

Financial Ratios......................................................................................................................4

Profitability........................................................................................................................4

Dividend Ratios..................................................................................................................6

Stability and Liquidity Ratios............................................................................................7

Efficiency...........................................................................................................................8

Compare UOB with Industry Average.......................................................................................9

UOB current market share price analysis.............................................................................10

UOB Customer Service........................................................................................................11

Section B: UOB Corporate Governance Compliance..............................................................12

News That Has Impact On Bank’s Financial Performance.................................................12

Impact on Brand and Reputation..........................................................................................12

Corporate Governance.........................................................................................................13

Conclusion................................................................................................................................13

REFERENCES.........................................................................................................................15

APPENDICES..........................................................................................................................17

Appendix 1: Horizontal analysis of UOB balance sheet......................................................17

Appendix 2: Vertical analysis of UOB balance sheet..........................................................18

Appendix 3: Horizontal analysis of UOB income statement...............................................19

Appendix 4: Vertical analysis of UOB income statement...................................................20

Financial Management 3

Financial Management of United Overseas Bank Ltd

SECTION A

Introduction

United Overseas Bank Ltd is usually Singapore multinational banking firm. The company

operates across Singapore with several branches located in Southeast Asian nations.

Established in the year 1935, the bank is third largest financial institution in the South-East

Asia by total assets. It provides wide range of services including corporate and commercial

banking services, private banking, corporate financial, performance financial services,

venture capital, insurance and investment services. Generally, UOB has over 68 branches

across Singapore and over 500 offices across 19 nations and regions within North American,

the Western Europe and Asia Pacific. Currently, UOB is one of the top banks in the world as

the company has grown rapidly since its establishment as a result of several strategic

acquisitions. The bank offers several financial services across the globe through its three

chief segments; that is, global markets, global wholesale banking as well as global retail.

Through its subsidiaries, UOB offer insurance services, venture capital management as well

as asset management.

Financial Analysis

As a financial analyst or an investor, one should dig into an organization’s financial

statements. One can look at the financial statements in isolations; nonetheless, it is crucial to

company organization’s financial results to selected firms within the industry, companies

outside the sector as well as against other period in determining whether the firm might be a

good investment. There are different forms of analysis which could be performed; these are;

vertical, horizontal or ratio analysis.

Horizontal and Vertical Analysis of UOB Financial Statements

Financial Management of United Overseas Bank Ltd

SECTION A

Introduction

United Overseas Bank Ltd is usually Singapore multinational banking firm. The company

operates across Singapore with several branches located in Southeast Asian nations.

Established in the year 1935, the bank is third largest financial institution in the South-East

Asia by total assets. It provides wide range of services including corporate and commercial

banking services, private banking, corporate financial, performance financial services,

venture capital, insurance and investment services. Generally, UOB has over 68 branches

across Singapore and over 500 offices across 19 nations and regions within North American,

the Western Europe and Asia Pacific. Currently, UOB is one of the top banks in the world as

the company has grown rapidly since its establishment as a result of several strategic

acquisitions. The bank offers several financial services across the globe through its three

chief segments; that is, global markets, global wholesale banking as well as global retail.

Through its subsidiaries, UOB offer insurance services, venture capital management as well

as asset management.

Financial Analysis

As a financial analyst or an investor, one should dig into an organization’s financial

statements. One can look at the financial statements in isolations; nonetheless, it is crucial to

company organization’s financial results to selected firms within the industry, companies

outside the sector as well as against other period in determining whether the firm might be a

good investment. There are different forms of analysis which could be performed; these are;

vertical, horizontal or ratio analysis.

Horizontal and Vertical Analysis of UOB Financial Statements

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Financial Management 4

Based on Appendix 1 below, it is evident that UOB total assets increased year by year,

though the amount differed over the years. Similarly, its total liabilities for the bank increased

year by year. Further, it is evident that its total liabilities represented at least 90% of the total

assets over the past five years (Appendix 2). Moreover, based on Appendix 3 below, it is

clear that the total revenue increased every year except in the year 2016 where a slight

decrease was recorded. Despite the decrease in 2016, UOB has gained significant increase in

its total revenue. On the other hand, its net profit is said to have decreased in the year 2015

and 2016, nonetheless, it gained momentum in 2017.

Economic Analysis of the Banking Industry

Singapore is presently the most renowned financial hub across the globe with its banking

sector account for over 10% of city state’s GDP (Bestar 2019). This industry employs just a

small portion of Singapore personnel which makes it among the highest value-added sector

across the country. Generally, Singapore is considered as one of the powerful banking centre

that caters for both domestic finances as well as monetary activities for the entire Asia-Pacific

(3E Accounting 2019). Being heartened by nation’s stable economic and political climate,

law enforcement against money crimes and frauds, effective taxation and legislation, the

country banking sectors is one of the most competitive sectors across the globe. Furthermore,

it is the Asian third-largest financial institution that provides several services from the

consumer credits to insurance and investment operations (One Visa 2019).

Financial Ratios

Profitability

Net profit ratio

2014 2015 2016 2017 2018

Industr

y

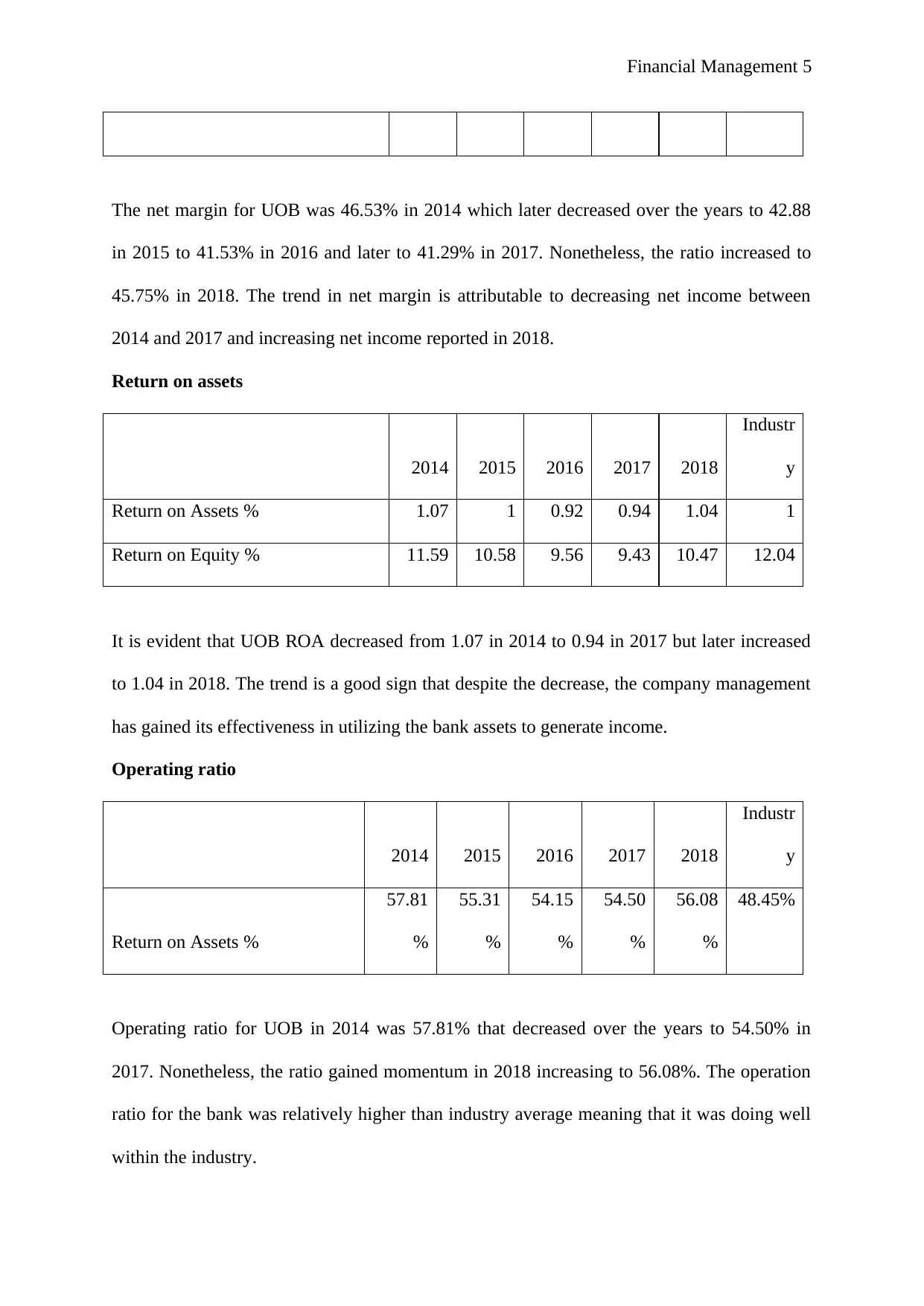

Net Margin % 46.53 42.88 41.53 41.29 45.75 39.2%

Based on Appendix 1 below, it is evident that UOB total assets increased year by year,

though the amount differed over the years. Similarly, its total liabilities for the bank increased

year by year. Further, it is evident that its total liabilities represented at least 90% of the total

assets over the past five years (Appendix 2). Moreover, based on Appendix 3 below, it is

clear that the total revenue increased every year except in the year 2016 where a slight

decrease was recorded. Despite the decrease in 2016, UOB has gained significant increase in

its total revenue. On the other hand, its net profit is said to have decreased in the year 2015

and 2016, nonetheless, it gained momentum in 2017.

Economic Analysis of the Banking Industry

Singapore is presently the most renowned financial hub across the globe with its banking

sector account for over 10% of city state’s GDP (Bestar 2019). This industry employs just a

small portion of Singapore personnel which makes it among the highest value-added sector

across the country. Generally, Singapore is considered as one of the powerful banking centre

that caters for both domestic finances as well as monetary activities for the entire Asia-Pacific

(3E Accounting 2019). Being heartened by nation’s stable economic and political climate,

law enforcement against money crimes and frauds, effective taxation and legislation, the

country banking sectors is one of the most competitive sectors across the globe. Furthermore,

it is the Asian third-largest financial institution that provides several services from the

consumer credits to insurance and investment operations (One Visa 2019).

Financial Ratios

Profitability

Net profit ratio

2014 2015 2016 2017 2018

Industr

y

Net Margin % 46.53 42.88 41.53 41.29 45.75 39.2%

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Financial Management 5

The net margin for UOB was 46.53% in 2014 which later decreased over the years to 42.88

in 2015 to 41.53% in 2016 and later to 41.29% in 2017. Nonetheless, the ratio increased to

45.75% in 2018. The trend in net margin is attributable to decreasing net income between

2014 and 2017 and increasing net income reported in 2018.

Return on assets

2014 2015 2016 2017 2018

Industr

y

Return on Assets % 1.07 1 0.92 0.94 1.04 1

Return on Equity % 11.59 10.58 9.56 9.43 10.47 12.04

It is evident that UOB ROA decreased from 1.07 in 2014 to 0.94 in 2017 but later increased

to 1.04 in 2018. The trend is a good sign that despite the decrease, the company management

has gained its effectiveness in utilizing the bank assets to generate income.

Operating ratio

2014 2015 2016 2017 2018

Industr

y

Return on Assets %

57.81

%

55.31

%

54.15

%

54.50

%

56.08

%

48.45%

Operating ratio for UOB in 2014 was 57.81% that decreased over the years to 54.50% in

2017. Nonetheless, the ratio gained momentum in 2018 increasing to 56.08%. The operation

ratio for the bank was relatively higher than industry average meaning that it was doing well

within the industry.

The net margin for UOB was 46.53% in 2014 which later decreased over the years to 42.88

in 2015 to 41.53% in 2016 and later to 41.29% in 2017. Nonetheless, the ratio increased to

45.75% in 2018. The trend in net margin is attributable to decreasing net income between

2014 and 2017 and increasing net income reported in 2018.

Return on assets

2014 2015 2016 2017 2018

Industr

y

Return on Assets % 1.07 1 0.92 0.94 1.04 1

Return on Equity % 11.59 10.58 9.56 9.43 10.47 12.04

It is evident that UOB ROA decreased from 1.07 in 2014 to 0.94 in 2017 but later increased

to 1.04 in 2018. The trend is a good sign that despite the decrease, the company management

has gained its effectiveness in utilizing the bank assets to generate income.

Operating ratio

2014 2015 2016 2017 2018

Industr

y

Return on Assets %

57.81

%

55.31

%

54.15

%

54.50

%

56.08

%

48.45%

Operating ratio for UOB in 2014 was 57.81% that decreased over the years to 54.50% in

2017. Nonetheless, the ratio gained momentum in 2018 increasing to 56.08%. The operation

ratio for the bank was relatively higher than industry average meaning that it was doing well

within the industry.

Financial Management 6

Return on Equity / Return on Investment

2014 2015 2016 2017 2018

Industr

y

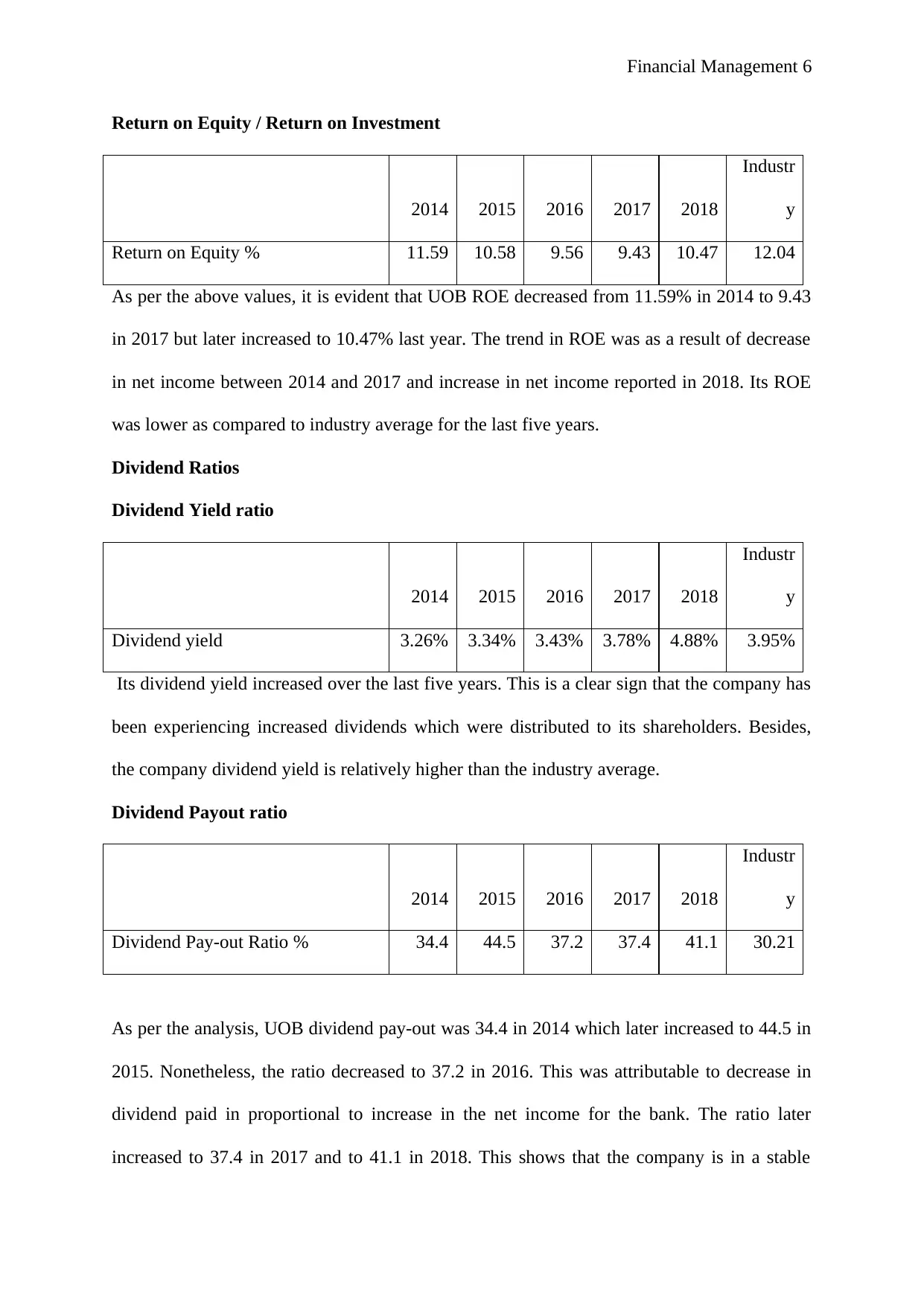

Return on Equity % 11.59 10.58 9.56 9.43 10.47 12.04

As per the above values, it is evident that UOB ROE decreased from 11.59% in 2014 to 9.43

in 2017 but later increased to 10.47% last year. The trend in ROE was as a result of decrease

in net income between 2014 and 2017 and increase in net income reported in 2018. Its ROE

was lower as compared to industry average for the last five years.

Dividend Ratios

Dividend Yield ratio

2014 2015 2016 2017 2018

Industr

y

Dividend yield 3.26% 3.34% 3.43% 3.78% 4.88% 3.95%

Its dividend yield increased over the last five years. This is a clear sign that the company has

been experiencing increased dividends which were distributed to its shareholders. Besides,

the company dividend yield is relatively higher than the industry average.

Dividend Payout ratio

2014 2015 2016 2017 2018

Industr

y

Dividend Pay-out Ratio % 34.4 44.5 37.2 37.4 41.1 30.21

As per the analysis, UOB dividend pay-out was 34.4 in 2014 which later increased to 44.5 in

2015. Nonetheless, the ratio decreased to 37.2 in 2016. This was attributable to decrease in

dividend paid in proportional to increase in the net income for the bank. The ratio later

increased to 37.4 in 2017 and to 41.1 in 2018. This shows that the company is in a stable

Return on Equity / Return on Investment

2014 2015 2016 2017 2018

Industr

y

Return on Equity % 11.59 10.58 9.56 9.43 10.47 12.04

As per the above values, it is evident that UOB ROE decreased from 11.59% in 2014 to 9.43

in 2017 but later increased to 10.47% last year. The trend in ROE was as a result of decrease

in net income between 2014 and 2017 and increase in net income reported in 2018. Its ROE

was lower as compared to industry average for the last five years.

Dividend Ratios

Dividend Yield ratio

2014 2015 2016 2017 2018

Industr

y

Dividend yield 3.26% 3.34% 3.43% 3.78% 4.88% 3.95%

Its dividend yield increased over the last five years. This is a clear sign that the company has

been experiencing increased dividends which were distributed to its shareholders. Besides,

the company dividend yield is relatively higher than the industry average.

Dividend Payout ratio

2014 2015 2016 2017 2018

Industr

y

Dividend Pay-out Ratio % 34.4 44.5 37.2 37.4 41.1 30.21

As per the analysis, UOB dividend pay-out was 34.4 in 2014 which later increased to 44.5 in

2015. Nonetheless, the ratio decreased to 37.2 in 2016. This was attributable to decrease in

dividend paid in proportional to increase in the net income for the bank. The ratio later

increased to 37.4 in 2017 and to 41.1 in 2018. This shows that the company is in a stable

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Financial Management 7

position financially. The bank dividend pay-out was higher compared to industry average for

the past five year meaning that the company is amongst the best company giving good return

to shareholders.

Price earnings ratio

2014 2015 2016 2017 2018

P/E 9.0 10.7 11.0 13.4 10.5 9.31

UOB P/E ratio for the past five years has been experiencing asymmetric trend with increasing

and decreasing trend over the period. The company P/E ratio increased from 2014 to 2017

and later decreased in 2018. Despite the decrease in UOB P/E in 2018, the ratio was higher

compared to industry average.

Earnings per share ratio

2014 2015 2016 2017 2018

Industr

y

Earnings Per Share SGD 1.97 1.93 1.85 1.98 2.33 1.54

In this case, UOB EPS ratio for the year ending 2014 was 1.97, nonetheless, the ratio

decreased to 1.93 in 2015 and further to 1.85 in 2016. The decrease was attributed to decrease

in its net income over the same period. Nonetheless, the ratio increased to 1.98 in 2017 and

later to 2.33 in 2018. This was attributable to increase in the bank net income over the years.

Its EPS was higher compared to industry average over the last five years.

Stability and Liquidity Ratios

Debt to Equity ratio

2014 2015 2016 2017 2018 Industry

Debt/Equity 0.76 0.69 0.81 0.7 0.83 0.65

position financially. The bank dividend pay-out was higher compared to industry average for

the past five year meaning that the company is amongst the best company giving good return

to shareholders.

Price earnings ratio

2014 2015 2016 2017 2018

P/E 9.0 10.7 11.0 13.4 10.5 9.31

UOB P/E ratio for the past five years has been experiencing asymmetric trend with increasing

and decreasing trend over the period. The company P/E ratio increased from 2014 to 2017

and later decreased in 2018. Despite the decrease in UOB P/E in 2018, the ratio was higher

compared to industry average.

Earnings per share ratio

2014 2015 2016 2017 2018

Industr

y

Earnings Per Share SGD 1.97 1.93 1.85 1.98 2.33 1.54

In this case, UOB EPS ratio for the year ending 2014 was 1.97, nonetheless, the ratio

decreased to 1.93 in 2015 and further to 1.85 in 2016. The decrease was attributed to decrease

in its net income over the same period. Nonetheless, the ratio increased to 1.98 in 2017 and

later to 2.33 in 2018. This was attributable to increase in the bank net income over the years.

Its EPS was higher compared to industry average over the last five years.

Stability and Liquidity Ratios

Debt to Equity ratio

2014 2015 2016 2017 2018 Industry

Debt/Equity 0.76 0.69 0.81 0.7 0.83 0.65

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Financial Management 8

UOB debt to equity was 0.76 in 2014 that later decreased to 0.69 in 2015 but later increased

to 0.81 in 2016. Furthermore, the ratio decreased to 0.7 in 2017 and later increased to 0.83.

Hence, it is evident that UOB debt/equity ratio has been experiencing asymmetric trend over

the past five years. Despite the trend, it is evident that the company has been financing its

operations using equity rather than relying on debt finances. The ratio was higher compared

to industry average though was not badly off.

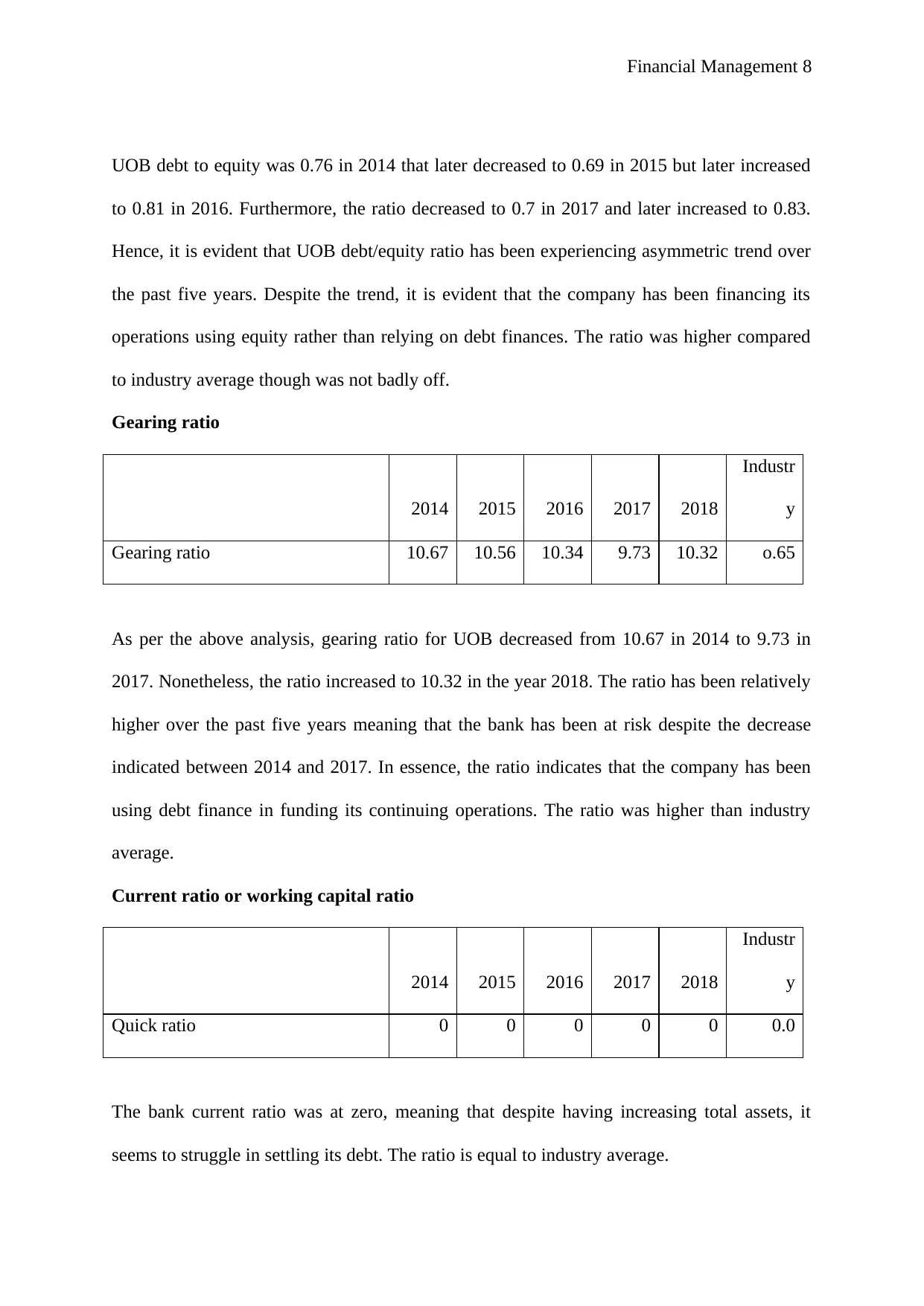

Gearing ratio

2014 2015 2016 2017 2018

Industr

y

Gearing ratio 10.67 10.56 10.34 9.73 10.32 o.65

As per the above analysis, gearing ratio for UOB decreased from 10.67 in 2014 to 9.73 in

2017. Nonetheless, the ratio increased to 10.32 in the year 2018. The ratio has been relatively

higher over the past five years meaning that the bank has been at risk despite the decrease

indicated between 2014 and 2017. In essence, the ratio indicates that the company has been

using debt finance in funding its continuing operations. The ratio was higher than industry

average.

Current ratio or working capital ratio

2014 2015 2016 2017 2018

Industr

y

Quick ratio 0 0 0 0 0 0.0

The bank current ratio was at zero, meaning that despite having increasing total assets, it

seems to struggle in settling its debt. The ratio is equal to industry average.

UOB debt to equity was 0.76 in 2014 that later decreased to 0.69 in 2015 but later increased

to 0.81 in 2016. Furthermore, the ratio decreased to 0.7 in 2017 and later increased to 0.83.

Hence, it is evident that UOB debt/equity ratio has been experiencing asymmetric trend over

the past five years. Despite the trend, it is evident that the company has been financing its

operations using equity rather than relying on debt finances. The ratio was higher compared

to industry average though was not badly off.

Gearing ratio

2014 2015 2016 2017 2018

Industr

y

Gearing ratio 10.67 10.56 10.34 9.73 10.32 o.65

As per the above analysis, gearing ratio for UOB decreased from 10.67 in 2014 to 9.73 in

2017. Nonetheless, the ratio increased to 10.32 in the year 2018. The ratio has been relatively

higher over the past five years meaning that the bank has been at risk despite the decrease

indicated between 2014 and 2017. In essence, the ratio indicates that the company has been

using debt finance in funding its continuing operations. The ratio was higher than industry

average.

Current ratio or working capital ratio

2014 2015 2016 2017 2018

Industr

y

Quick ratio 0 0 0 0 0 0.0

The bank current ratio was at zero, meaning that despite having increasing total assets, it

seems to struggle in settling its debt. The ratio is equal to industry average.

Financial Management 9

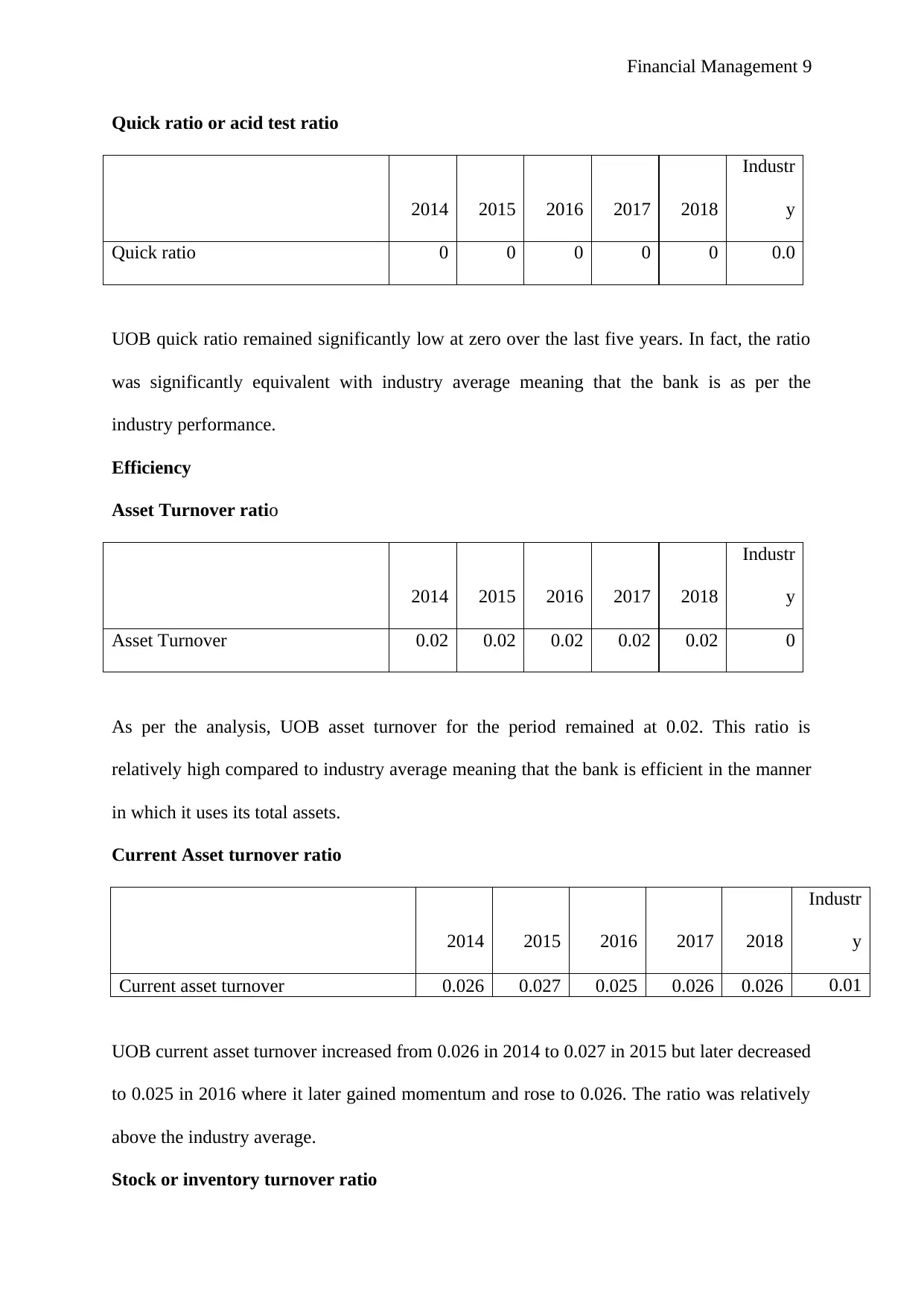

Quick ratio or acid test ratio

2014 2015 2016 2017 2018

Industr

y

Quick ratio 0 0 0 0 0 0.0

UOB quick ratio remained significantly low at zero over the last five years. In fact, the ratio

was significantly equivalent with industry average meaning that the bank is as per the

industry performance.

Efficiency

Asset Turnover ratio

2014 2015 2016 2017 2018

Industr

y

Asset Turnover 0.02 0.02 0.02 0.02 0.02 0

As per the analysis, UOB asset turnover for the period remained at 0.02. This ratio is

relatively high compared to industry average meaning that the bank is efficient in the manner

in which it uses its total assets.

Current Asset turnover ratio

2014 2015 2016 2017 2018

Industr

y

Current asset turnover 0.026 0.027 0.025 0.026 0.026 0.01

UOB current asset turnover increased from 0.026 in 2014 to 0.027 in 2015 but later decreased

to 0.025 in 2016 where it later gained momentum and rose to 0.026. The ratio was relatively

above the industry average.

Stock or inventory turnover ratio

Quick ratio or acid test ratio

2014 2015 2016 2017 2018

Industr

y

Quick ratio 0 0 0 0 0 0.0

UOB quick ratio remained significantly low at zero over the last five years. In fact, the ratio

was significantly equivalent with industry average meaning that the bank is as per the

industry performance.

Efficiency

Asset Turnover ratio

2014 2015 2016 2017 2018

Industr

y

Asset Turnover 0.02 0.02 0.02 0.02 0.02 0

As per the analysis, UOB asset turnover for the period remained at 0.02. This ratio is

relatively high compared to industry average meaning that the bank is efficient in the manner

in which it uses its total assets.

Current Asset turnover ratio

2014 2015 2016 2017 2018

Industr

y

Current asset turnover 0.026 0.027 0.025 0.026 0.026 0.01

UOB current asset turnover increased from 0.026 in 2014 to 0.027 in 2015 but later decreased

to 0.025 in 2016 where it later gained momentum and rose to 0.026. The ratio was relatively

above the industry average.

Stock or inventory turnover ratio

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

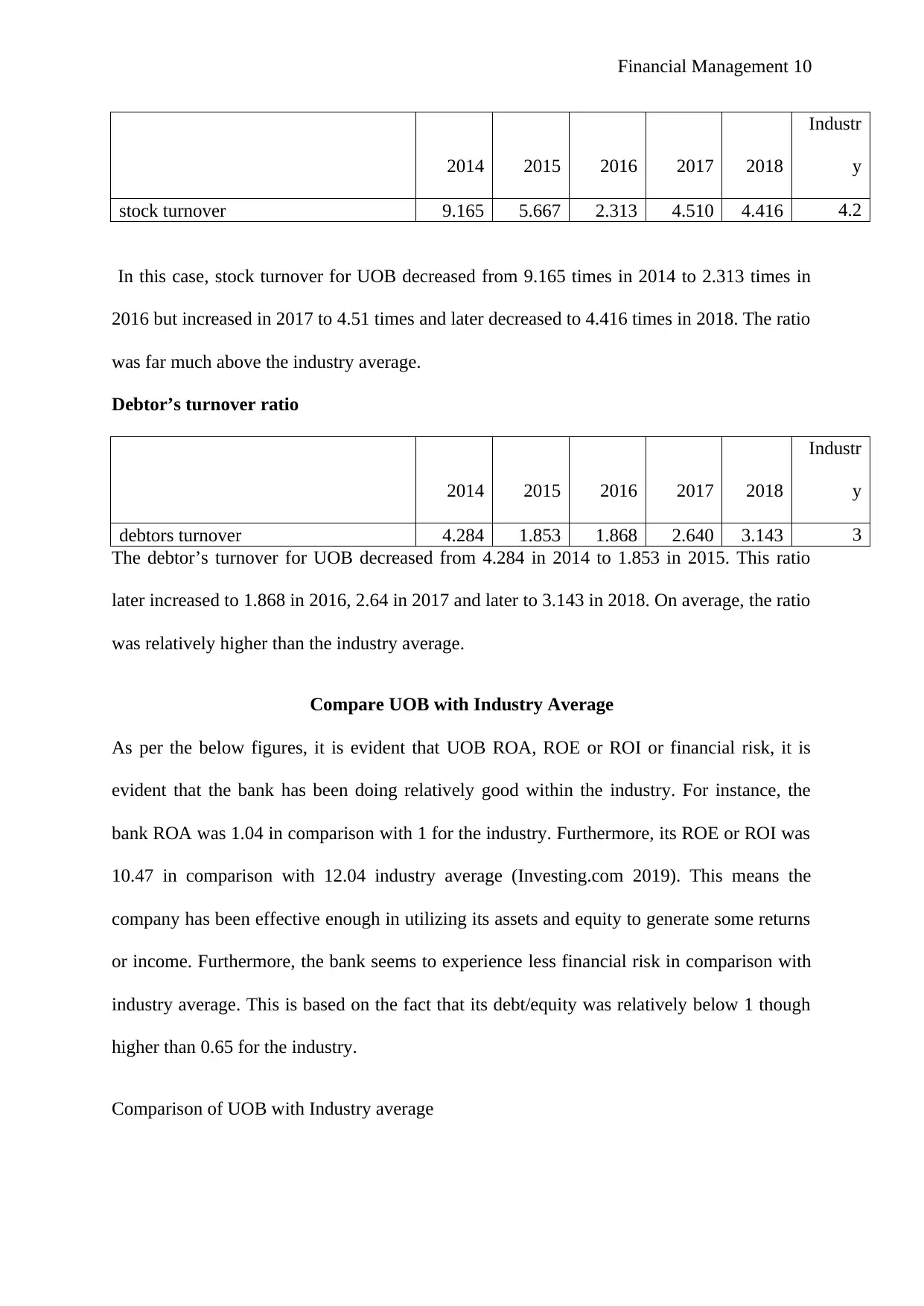

Financial Management 10

2014 2015 2016 2017 2018

Industr

y

stock turnover 9.165 5.667 2.313 4.510 4.416 4.2

In this case, stock turnover for UOB decreased from 9.165 times in 2014 to 2.313 times in

2016 but increased in 2017 to 4.51 times and later decreased to 4.416 times in 2018. The ratio

was far much above the industry average.

Debtor’s turnover ratio

2014 2015 2016 2017 2018

Industr

y

debtors turnover 4.284 1.853 1.868 2.640 3.143 3

The debtor’s turnover for UOB decreased from 4.284 in 2014 to 1.853 in 2015. This ratio

later increased to 1.868 in 2016, 2.64 in 2017 and later to 3.143 in 2018. On average, the ratio

was relatively higher than the industry average.

Compare UOB with Industry Average

As per the below figures, it is evident that UOB ROA, ROE or ROI or financial risk, it is

evident that the bank has been doing relatively good within the industry. For instance, the

bank ROA was 1.04 in comparison with 1 for the industry. Furthermore, its ROE or ROI was

10.47 in comparison with 12.04 industry average (Investing.com 2019). This means the

company has been effective enough in utilizing its assets and equity to generate some returns

or income. Furthermore, the bank seems to experience less financial risk in comparison with

industry average. This is based on the fact that its debt/equity was relatively below 1 though

higher than 0.65 for the industry.

Comparison of UOB with Industry average

2014 2015 2016 2017 2018

Industr

y

stock turnover 9.165 5.667 2.313 4.510 4.416 4.2

In this case, stock turnover for UOB decreased from 9.165 times in 2014 to 2.313 times in

2016 but increased in 2017 to 4.51 times and later decreased to 4.416 times in 2018. The ratio

was far much above the industry average.

Debtor’s turnover ratio

2014 2015 2016 2017 2018

Industr

y

debtors turnover 4.284 1.853 1.868 2.640 3.143 3

The debtor’s turnover for UOB decreased from 4.284 in 2014 to 1.853 in 2015. This ratio

later increased to 1.868 in 2016, 2.64 in 2017 and later to 3.143 in 2018. On average, the ratio

was relatively higher than the industry average.

Compare UOB with Industry Average

As per the below figures, it is evident that UOB ROA, ROE or ROI or financial risk, it is

evident that the bank has been doing relatively good within the industry. For instance, the

bank ROA was 1.04 in comparison with 1 for the industry. Furthermore, its ROE or ROI was

10.47 in comparison with 12.04 industry average (Investing.com 2019). This means the

company has been effective enough in utilizing its assets and equity to generate some returns

or income. Furthermore, the bank seems to experience less financial risk in comparison with

industry average. This is based on the fact that its debt/equity was relatively below 1 though

higher than 0.65 for the industry.

Comparison of UOB with Industry average

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Financial Management 11

2014 2015 2016 2017 2018

Industr

y

Return on Assets % 1.07 1 0.92 0.94 1.04 1

Return on Equity % 11.59 10.58 9.56 9.43 10.47 12.04

Debt/Equity 0.76 0.69 0.81 0.7 0.83 0.65

UOB current market share price analysis

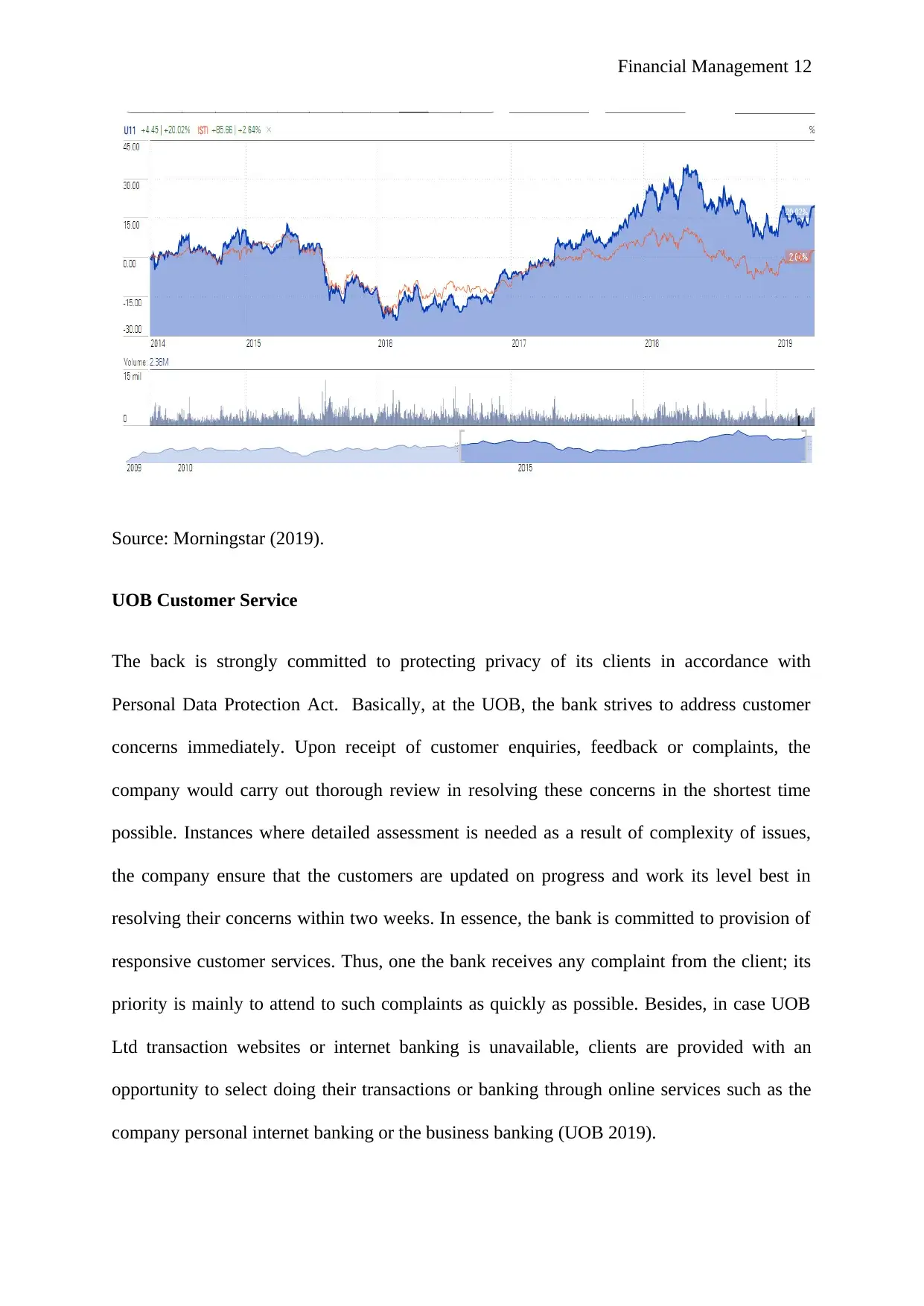

Over the last five years, UOB share price has been on the rise despite the decrease recorded

in the year 2016. It is evident that the company share price gained momentum in the mid-

2016 where its share price started to increase with a steady growth on daily basis. The share

price reached its peak in early 2018. Generally, UOB share price between 2014 and 2016 has

been experiencing similar trend in comparison to STI; nonetheless, the share price for the

company rose with a significant margin in comparison to STI (Morningstar 2019). This

shows that the company has gained popularity within Singapore security exchange. Hence, it

presents a better investment opportunity for potential investors. Generally, UOB share price

is linear with Singapore stock exchange indicator, Strait Times Index-STI.

Figure 1: Comparison of UOB share price with STI-Trait Times Index

2014 2015 2016 2017 2018

Industr

y

Return on Assets % 1.07 1 0.92 0.94 1.04 1

Return on Equity % 11.59 10.58 9.56 9.43 10.47 12.04

Debt/Equity 0.76 0.69 0.81 0.7 0.83 0.65

UOB current market share price analysis

Over the last five years, UOB share price has been on the rise despite the decrease recorded

in the year 2016. It is evident that the company share price gained momentum in the mid-

2016 where its share price started to increase with a steady growth on daily basis. The share

price reached its peak in early 2018. Generally, UOB share price between 2014 and 2016 has

been experiencing similar trend in comparison to STI; nonetheless, the share price for the

company rose with a significant margin in comparison to STI (Morningstar 2019). This

shows that the company has gained popularity within Singapore security exchange. Hence, it

presents a better investment opportunity for potential investors. Generally, UOB share price

is linear with Singapore stock exchange indicator, Strait Times Index-STI.

Figure 1: Comparison of UOB share price with STI-Trait Times Index

Financial Management 12

Source: Morningstar (2019).

UOB Customer Service

The back is strongly committed to protecting privacy of its clients in accordance with

Personal Data Protection Act. Basically, at the UOB, the bank strives to address customer

concerns immediately. Upon receipt of customer enquiries, feedback or complaints, the

company would carry out thorough review in resolving these concerns in the shortest time

possible. Instances where detailed assessment is needed as a result of complexity of issues,

the company ensure that the customers are updated on progress and work its level best in

resolving their concerns within two weeks. In essence, the bank is committed to provision of

responsive customer services. Thus, one the bank receives any complaint from the client; its

priority is mainly to attend to such complaints as quickly as possible. Besides, in case UOB

Ltd transaction websites or internet banking is unavailable, clients are provided with an

opportunity to select doing their transactions or banking through online services such as the

company personal internet banking or the business banking (UOB 2019).

Source: Morningstar (2019).

UOB Customer Service

The back is strongly committed to protecting privacy of its clients in accordance with

Personal Data Protection Act. Basically, at the UOB, the bank strives to address customer

concerns immediately. Upon receipt of customer enquiries, feedback or complaints, the

company would carry out thorough review in resolving these concerns in the shortest time

possible. Instances where detailed assessment is needed as a result of complexity of issues,

the company ensure that the customers are updated on progress and work its level best in

resolving their concerns within two weeks. In essence, the bank is committed to provision of

responsive customer services. Thus, one the bank receives any complaint from the client; its

priority is mainly to attend to such complaints as quickly as possible. Besides, in case UOB

Ltd transaction websites or internet banking is unavailable, clients are provided with an

opportunity to select doing their transactions or banking through online services such as the

company personal internet banking or the business banking (UOB 2019).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 22

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.