Financial Management Report: Equity Finance and Investment Appraisal

VerifiedAdded on 2020/07/22

|14

|3730

|38

Report

AI Summary

This report delves into the realm of financial management, commencing with an introduction to its core principles and the importance of effective fund management in achieving organizational objectives. The report subsequently explores long-term finance, specifically focusing on equity finance. It details the process of determining the number of shares to be issued, calculating the theoretical ex-rights price, and estimating expected earnings per share. Furthermore, the report presents the forms of issue for each rights issue price and provides a critical evaluation of the best option among different rights issues. The significance of scrip dividends is also elaborated upon. The report then transitions to investment appraisal techniques, calculating various methods such as Net Present Value (NPV), Internal Rate of Return (IRR), Accounting Rate of Return (ARR), and payback period, along with their respective merits and demerits. Detailed calculations and interpretations for each technique are included, providing recommendations for investment decisions. The report concludes with a summary of the key findings and a comprehensive reference list.

Financial management

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

QUESTION 2 LONG TERM FINANCE; EQUITY FINANCE.....................................................1

2.1 Determining the:...................................................................................................................1

2.1.1 Number of shares need to be issued ..................................................................................1

2.1.2 Computation of theoretical ex-right price .........................................................................1

2.1.3 Expected earnings per share ..............................................................................................2

2.1.4 Presenting the form of the issue for each rights issue price...............................................2

2.1.5 Presenting results in a tabular form and critically evaluating the best option among the

three right issues..........................................................................................................................3

2.2 Scrip dividends with its critical views..................................................................................3

Question 3 Investment appraisal techniques...............................................................................5

3.1 Calculating different investment appraisal techniques with recommendations....................5

3.2 Merits and demerits of investment appraisal techniques (Payback period, Accounting rate

of return, Internal rate of return and Net present value).............................................................7

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION...........................................................................................................................1

QUESTION 2 LONG TERM FINANCE; EQUITY FINANCE.....................................................1

2.1 Determining the:...................................................................................................................1

2.1.1 Number of shares need to be issued ..................................................................................1

2.1.2 Computation of theoretical ex-right price .........................................................................1

2.1.3 Expected earnings per share ..............................................................................................2

2.1.4 Presenting the form of the issue for each rights issue price...............................................2

2.1.5 Presenting results in a tabular form and critically evaluating the best option among the

three right issues..........................................................................................................................3

2.2 Scrip dividends with its critical views..................................................................................3

Question 3 Investment appraisal techniques...............................................................................5

3.1 Calculating different investment appraisal techniques with recommendations....................5

3.2 Merits and demerits of investment appraisal techniques (Payback period, Accounting rate

of return, Internal rate of return and Net present value).............................................................7

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION

Financial management gives an effective and efficient management of fund which will be

attaining the organization's objective as it is directly specialised function along with top

management. It is integrated with proper decision making process. Future planning of a person or

business ensure a cash flow which is positive which also includes maintenance and

administration of financial assets. It also gives ways and its alternative that how business can

finance it from shareholders fund with the combination of equity share capital, preference share

capital and profits which are accumulated. All the financial decision which consists of

acquisition of finance which is required from perspective of long term investments. In this report

there is a brief discussion about dividend decisions i.e. particular profit which has been earned

and there alternatives for retaining profit and how to distribute the margins from shareholders.

The present report gives an understanding about how to identify the shares which are to issued

with there theoretical ex rights price, earnings per share which has been expected, forms of issue

for every rights issue price and that results with interpretation in tabular form. And significance

of scrip dividend has been elaborated. Different investment appraisal techniques like Net present

value, Internal rate of return, accounting rate of return and payback period with the merits and

demerits has been explained.

QUESTION 2 LONG TERM FINANCE; EQUITY FINANCE

2.1 Determining the:

2.1.1 Number of shares need to be issued

Company wants to raise : 180000

Total shares issued by company: 300000

rate of per share: 50

Number of shares needed to be issued is = 180000/50 i.e. 3600

2.1.2 Computation of theoretical ex-right price

Theoretical Ex-Rights Price:

= Market Value of shares prior to rights issue + Cash raised from rights issue

Number of shares after rights issue

When price of right issue is £1.80

1

Financial management gives an effective and efficient management of fund which will be

attaining the organization's objective as it is directly specialised function along with top

management. It is integrated with proper decision making process. Future planning of a person or

business ensure a cash flow which is positive which also includes maintenance and

administration of financial assets. It also gives ways and its alternative that how business can

finance it from shareholders fund with the combination of equity share capital, preference share

capital and profits which are accumulated. All the financial decision which consists of

acquisition of finance which is required from perspective of long term investments. In this report

there is a brief discussion about dividend decisions i.e. particular profit which has been earned

and there alternatives for retaining profit and how to distribute the margins from shareholders.

The present report gives an understanding about how to identify the shares which are to issued

with there theoretical ex rights price, earnings per share which has been expected, forms of issue

for every rights issue price and that results with interpretation in tabular form. And significance

of scrip dividend has been elaborated. Different investment appraisal techniques like Net present

value, Internal rate of return, accounting rate of return and payback period with the merits and

demerits has been explained.

QUESTION 2 LONG TERM FINANCE; EQUITY FINANCE

2.1 Determining the:

2.1.1 Number of shares need to be issued

Company wants to raise : 180000

Total shares issued by company: 300000

rate of per share: 50

Number of shares needed to be issued is = 180000/50 i.e. 3600

2.1.2 Computation of theoretical ex-right price

Theoretical Ex-Rights Price:

= Market Value of shares prior to rights issue + Cash raised from rights issue

Number of shares after rights issue

When price of right issue is £1.80

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

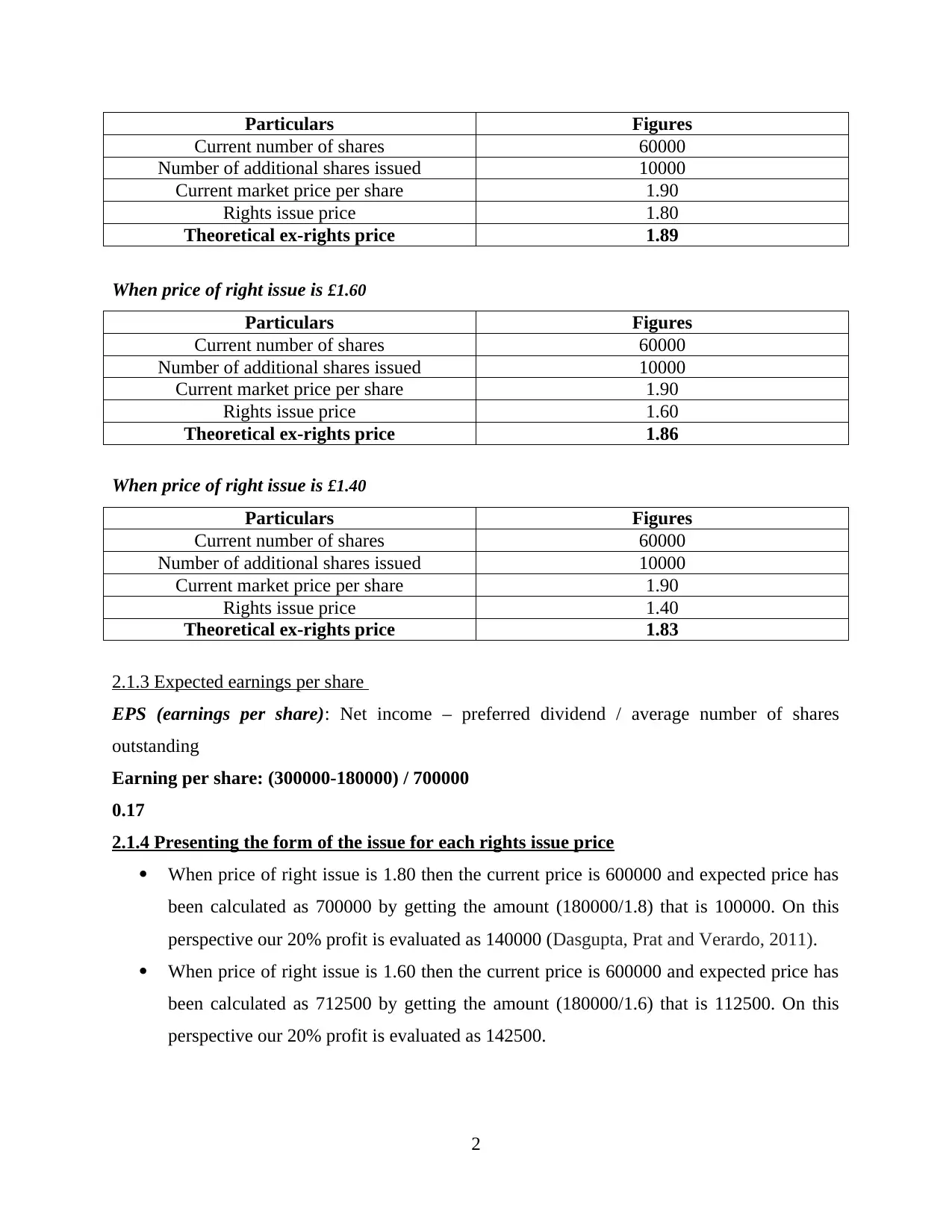

Particulars Figures

Current number of shares 60000

Number of additional shares issued 10000

Current market price per share 1.90

Rights issue price 1.80

Theoretical ex-rights price 1.89

When price of right issue is £1.60

Particulars Figures

Current number of shares 60000

Number of additional shares issued 10000

Current market price per share 1.90

Rights issue price 1.60

Theoretical ex-rights price 1.86

When price of right issue is £1.40

Particulars Figures

Current number of shares 60000

Number of additional shares issued 10000

Current market price per share 1.90

Rights issue price 1.40

Theoretical ex-rights price 1.83

2.1.3 Expected earnings per share

EPS (earnings per share): Net income – preferred dividend / average number of shares

outstanding

Earning per share: (300000-180000) / 700000

0.17

2.1.4 Presenting the form of the issue for each rights issue price

When price of right issue is 1.80 then the current price is 600000 and expected price has

been calculated as 700000 by getting the amount (180000/1.8) that is 100000. On this

perspective our 20% profit is evaluated as 140000 (Dasgupta, Prat and Verardo, 2011).

When price of right issue is 1.60 then the current price is 600000 and expected price has

been calculated as 712500 by getting the amount (180000/1.6) that is 112500. On this

perspective our 20% profit is evaluated as 142500.

2

Current number of shares 60000

Number of additional shares issued 10000

Current market price per share 1.90

Rights issue price 1.80

Theoretical ex-rights price 1.89

When price of right issue is £1.60

Particulars Figures

Current number of shares 60000

Number of additional shares issued 10000

Current market price per share 1.90

Rights issue price 1.60

Theoretical ex-rights price 1.86

When price of right issue is £1.40

Particulars Figures

Current number of shares 60000

Number of additional shares issued 10000

Current market price per share 1.90

Rights issue price 1.40

Theoretical ex-rights price 1.83

2.1.3 Expected earnings per share

EPS (earnings per share): Net income – preferred dividend / average number of shares

outstanding

Earning per share: (300000-180000) / 700000

0.17

2.1.4 Presenting the form of the issue for each rights issue price

When price of right issue is 1.80 then the current price is 600000 and expected price has

been calculated as 700000 by getting the amount (180000/1.8) that is 100000. On this

perspective our 20% profit is evaluated as 140000 (Dasgupta, Prat and Verardo, 2011).

When price of right issue is 1.60 then the current price is 600000 and expected price has

been calculated as 712500 by getting the amount (180000/1.6) that is 112500. On this

perspective our 20% profit is evaluated as 142500.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

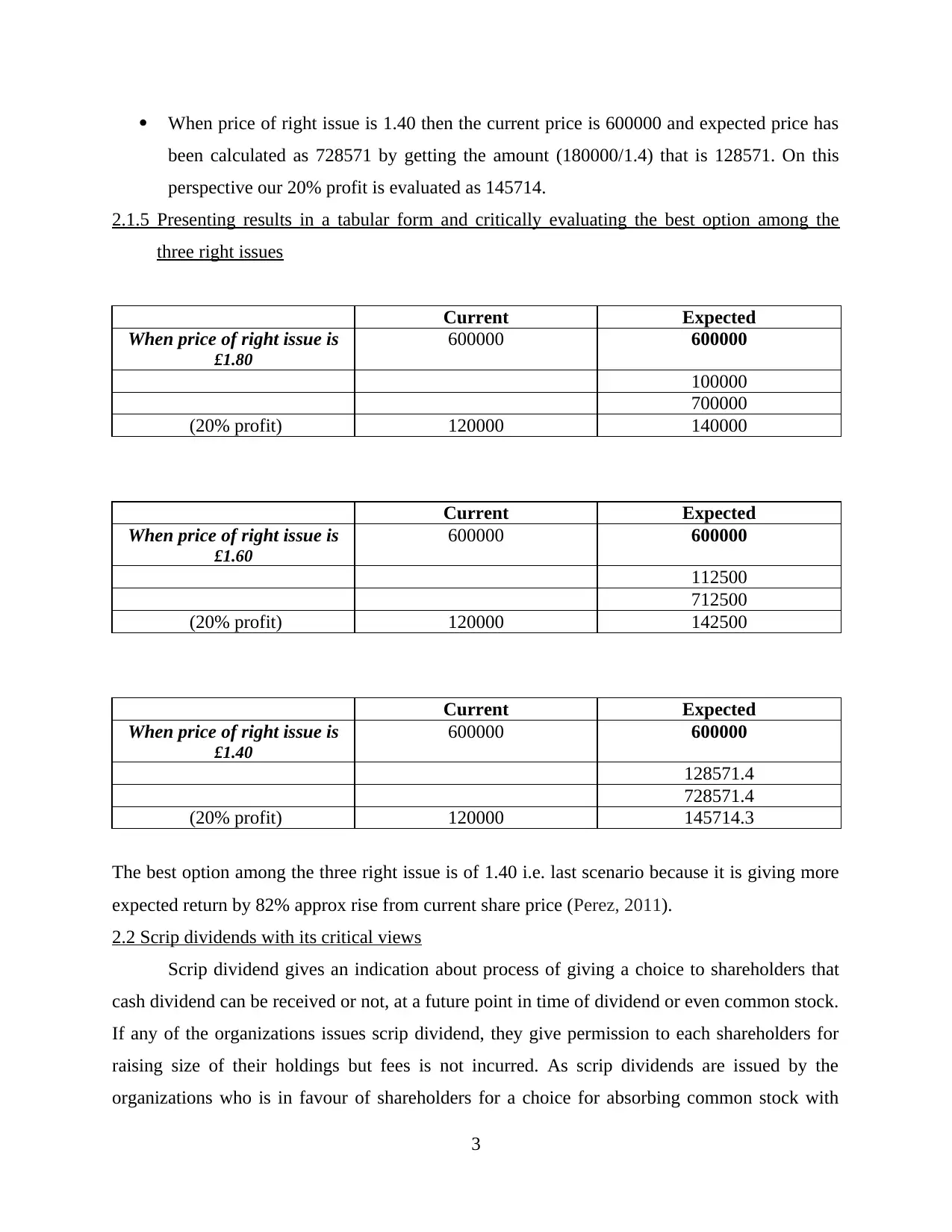

When price of right issue is 1.40 then the current price is 600000 and expected price has

been calculated as 728571 by getting the amount (180000/1.4) that is 128571. On this

perspective our 20% profit is evaluated as 145714.

2.1.5 Presenting results in a tabular form and critically evaluating the best option among the

three right issues

Current Expected

When price of right issue is

£1.80

600000 600000

100000

700000

(20% profit) 120000 140000

Current Expected

When price of right issue is

£1.60

600000 600000

112500

712500

(20% profit) 120000 142500

Current Expected

When price of right issue is

£1.40

600000 600000

128571.4

728571.4

(20% profit) 120000 145714.3

The best option among the three right issue is of 1.40 i.e. last scenario because it is giving more

expected return by 82% approx rise from current share price (Perez, 2011).

2.2 Scrip dividends with its critical views

Scrip dividend gives an indication about process of giving a choice to shareholders that

cash dividend can be received or not, at a future point in time of dividend or even common stock.

If any of the organizations issues scrip dividend, they give permission to each shareholders for

raising size of their holdings but fees is not incurred. As scrip dividends are issued by the

organizations who is in favour of shareholders for a choice for absorbing common stock with

3

been calculated as 728571 by getting the amount (180000/1.4) that is 128571. On this

perspective our 20% profit is evaluated as 145714.

2.1.5 Presenting results in a tabular form and critically evaluating the best option among the

three right issues

Current Expected

When price of right issue is

£1.80

600000 600000

100000

700000

(20% profit) 120000 140000

Current Expected

When price of right issue is

£1.60

600000 600000

112500

712500

(20% profit) 120000 142500

Current Expected

When price of right issue is

£1.40

600000 600000

128571.4

728571.4

(20% profit) 120000 145714.3

The best option among the three right issue is of 1.40 i.e. last scenario because it is giving more

expected return by 82% approx rise from current share price (Perez, 2011).

2.2 Scrip dividends with its critical views

Scrip dividend gives an indication about process of giving a choice to shareholders that

cash dividend can be received or not, at a future point in time of dividend or even common stock.

If any of the organizations issues scrip dividend, they give permission to each shareholders for

raising size of their holdings but fees is not incurred. As scrip dividends are issued by the

organizations who is in favour of shareholders for a choice for absorbing common stock with

3

respect of cash dividend which can be also reflected as capitalization issue. It is properly tied to

particular common stock from which the issuing company has permission for retaining and

creating ability to shareholders for providing and increasing the holdings of their organization.

This will lead to lowering the cost which is associated to acquirement of shares of the stock and

along with these investors will be gaining advantages related to taxation. In the same series

example can be formed that capital gain has been realized by investor instead of income so there

will be less tax on capital gain and even lower rate as compared to ordinary dividends (Carse,

2011).

As this scrip dividend policy is drawn for enabling the ordinary shareholders of bank for

electing to getting new shares rather than getting cash dividends. In the same series scrip

dividends increase the capital of company but there is requirement of extra effort by

organisation. There are many people who wants to raise their financial position of company and

even they benefit it fiscally. On the contrary side moment of stock market might not be the

efficient and even it could be more good for monetizing assets if share value is been going down.

And these shareholders only will be giving more preference to money paid rather than shares.

The issue related to scrip dividends is a wider topic for discussing on financial management with

dividend policy. Scrip issue and scrip dividends sound similar but they are not.

The main benefit of scrip dividend to shareholder that without pain he can raise

shareholding in the company without incurring any broker's cost, stamp duty or any commission

on any purchase of shares. And on the perspective of company it does not have to arrange cash

for paying it in form of dividend and in some of certain circumstances it can also help in

taxation. Many of the companies gives priority to shareholders that selection of cash dividends or

scrap dividends. Mostly shareholders prefers choice of scrip dividends because of increment in

wealth along with decrease in wealth if cash is selected. This arrangement can be also referred as

enhanced scrip. This scrip dividend efficiently transforms retained margin into share capital

which is permanent. Cash can be preserved for investing again in organisation or re-investment.

If any of scrip issue which is significant and will be not diluted the share price. As company's

gearing can be reduced by more shares and borrowing capacity will increase. Without any of

transaction cost shares will be owned by shareholders. The major limitation of scrip dividend can

be that there is not any presence of cash to shareholders along with it they have to pay taxes on

the particular dividends (Ghahremani, Aghaie, and Abedzadeh, 2012).

4

particular common stock from which the issuing company has permission for retaining and

creating ability to shareholders for providing and increasing the holdings of their organization.

This will lead to lowering the cost which is associated to acquirement of shares of the stock and

along with these investors will be gaining advantages related to taxation. In the same series

example can be formed that capital gain has been realized by investor instead of income so there

will be less tax on capital gain and even lower rate as compared to ordinary dividends (Carse,

2011).

As this scrip dividend policy is drawn for enabling the ordinary shareholders of bank for

electing to getting new shares rather than getting cash dividends. In the same series scrip

dividends increase the capital of company but there is requirement of extra effort by

organisation. There are many people who wants to raise their financial position of company and

even they benefit it fiscally. On the contrary side moment of stock market might not be the

efficient and even it could be more good for monetizing assets if share value is been going down.

And these shareholders only will be giving more preference to money paid rather than shares.

The issue related to scrip dividends is a wider topic for discussing on financial management with

dividend policy. Scrip issue and scrip dividends sound similar but they are not.

The main benefit of scrip dividend to shareholder that without pain he can raise

shareholding in the company without incurring any broker's cost, stamp duty or any commission

on any purchase of shares. And on the perspective of company it does not have to arrange cash

for paying it in form of dividend and in some of certain circumstances it can also help in

taxation. Many of the companies gives priority to shareholders that selection of cash dividends or

scrap dividends. Mostly shareholders prefers choice of scrip dividends because of increment in

wealth along with decrease in wealth if cash is selected. This arrangement can be also referred as

enhanced scrip. This scrip dividend efficiently transforms retained margin into share capital

which is permanent. Cash can be preserved for investing again in organisation or re-investment.

If any of scrip issue which is significant and will be not diluted the share price. As company's

gearing can be reduced by more shares and borrowing capacity will increase. Without any of

transaction cost shares will be owned by shareholders. The major limitation of scrip dividend can

be that there is not any presence of cash to shareholders along with it they have to pay taxes on

the particular dividends (Ghahremani, Aghaie, and Abedzadeh, 2012).

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

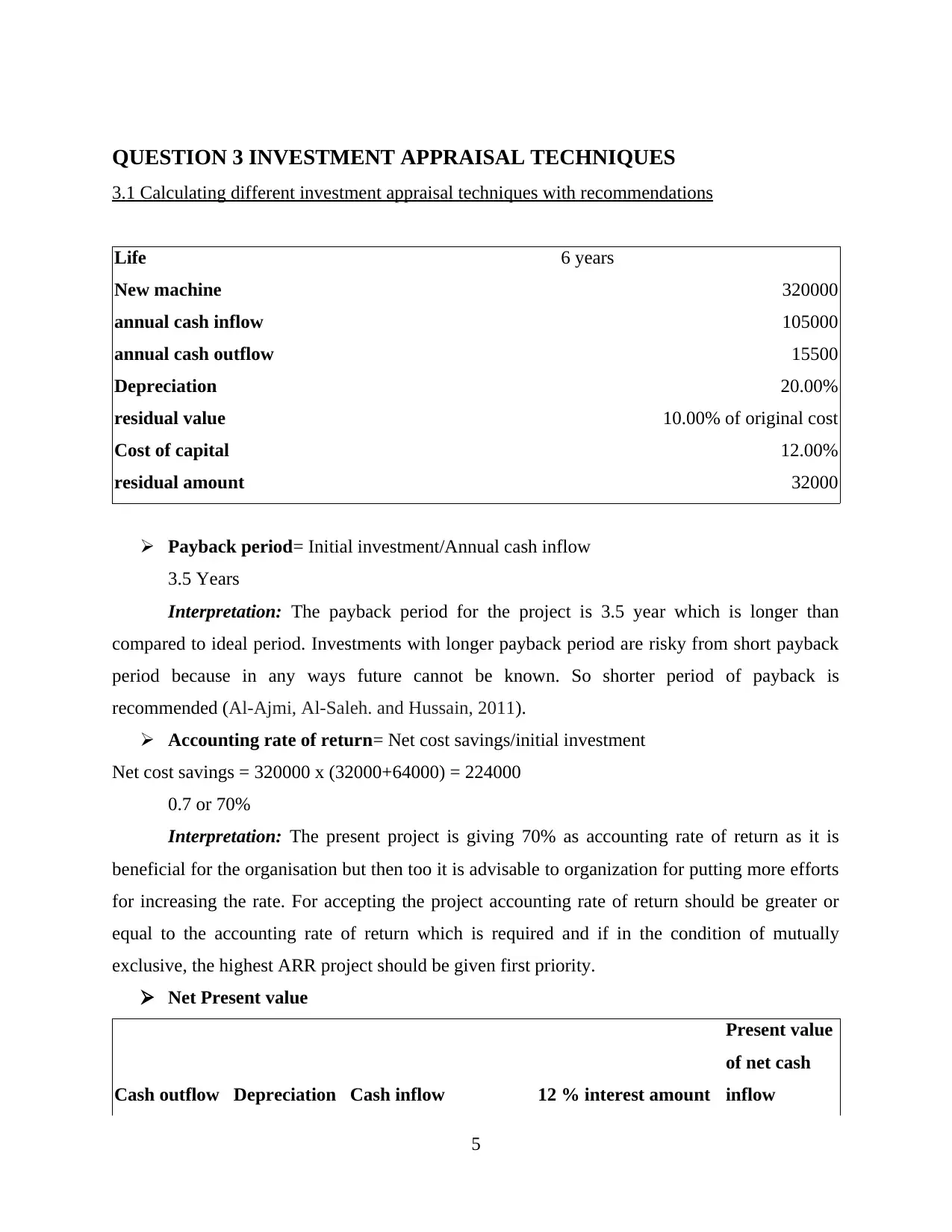

QUESTION 3 INVESTMENT APPRAISAL TECHNIQUES

3.1 Calculating different investment appraisal techniques with recommendations

Life 6 years

New machine 320000

annual cash inflow 105000

annual cash outflow 15500

Depreciation 20.00%

residual value 10.00% of original cost

Cost of capital 12.00%

residual amount 32000

Payback period= Initial investment/Annual cash inflow

3.5 Years

Interpretation: The payback period for the project is 3.5 year which is longer than

compared to ideal period. Investments with longer payback period are risky from short payback

period because in any ways future cannot be known. So shorter period of payback is

recommended (Al-Ajmi, Al-Saleh. and Hussain, 2011).

Accounting rate of return= Net cost savings/initial investment

Net cost savings = 320000 x (32000+64000) = 224000

0.7 or 70%

Interpretation: The present project is giving 70% as accounting rate of return as it is

beneficial for the organisation but then too it is advisable to organization for putting more efforts

for increasing the rate. For accepting the project accounting rate of return should be greater or

equal to the accounting rate of return which is required and if in the condition of mutually

exclusive, the highest ARR project should be given first priority.

Net Present value

Cash outflow Depreciation Cash inflow 12 % interest amount

Present value

of net cash

inflow

5

3.1 Calculating different investment appraisal techniques with recommendations

Life 6 years

New machine 320000

annual cash inflow 105000

annual cash outflow 15500

Depreciation 20.00%

residual value 10.00% of original cost

Cost of capital 12.00%

residual amount 32000

Payback period= Initial investment/Annual cash inflow

3.5 Years

Interpretation: The payback period for the project is 3.5 year which is longer than

compared to ideal period. Investments with longer payback period are risky from short payback

period because in any ways future cannot be known. So shorter period of payback is

recommended (Al-Ajmi, Al-Saleh. and Hussain, 2011).

Accounting rate of return= Net cost savings/initial investment

Net cost savings = 320000 x (32000+64000) = 224000

0.7 or 70%

Interpretation: The present project is giving 70% as accounting rate of return as it is

beneficial for the organisation but then too it is advisable to organization for putting more efforts

for increasing the rate. For accepting the project accounting rate of return should be greater or

equal to the accounting rate of return which is required and if in the condition of mutually

exclusive, the highest ARR project should be given first priority.

Net Present value

Cash outflow Depreciation Cash inflow 12 % interest amount

Present value

of net cash

inflow

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

15500 64000 79500 0.8928571429

70982.142857

1429

15500 64000 79500 0.7971938776

63376.913265

3061

15500 64000 79500 0.7117802478

56586.529701

1662

15500 64000 79500 0.6355180784

50523.687233

1841

15500 64000 79500 0.5674268557

45110.435029

6286

15500 64000 79500 0.5066311212

40277.174133

597

93000 326856.88

Price paid for new

machine 320000

Net present value of

new machine 6856.88

Interpretation: The above project net present value is 6856.88 which indicates that machine will

not pay machine will not pay for its own but it will also make value of 6856.88. For accepting

project net present value should be positive and while giving comparison between two projects

NPV should be greater than it will be considered as good investment (Kumar, Mahadevan and

Gunasekar, 2012).

Internal rate of return

Machine amount -320000

Cash Inflow year 1 79500

Year 2 79500

Year 3 79500

Year 4 79500

Year 5 79500

6

70982.142857

1429

15500 64000 79500 0.7971938776

63376.913265

3061

15500 64000 79500 0.7117802478

56586.529701

1662

15500 64000 79500 0.6355180784

50523.687233

1841

15500 64000 79500 0.5674268557

45110.435029

6286

15500 64000 79500 0.5066311212

40277.174133

597

93000 326856.88

Price paid for new

machine 320000

Net present value of

new machine 6856.88

Interpretation: The above project net present value is 6856.88 which indicates that machine will

not pay machine will not pay for its own but it will also make value of 6856.88. For accepting

project net present value should be positive and while giving comparison between two projects

NPV should be greater than it will be considered as good investment (Kumar, Mahadevan and

Gunasekar, 2012).

Internal rate of return

Machine amount -320000

Cash Inflow year 1 79500

Year 2 79500

Year 3 79500

Year 4 79500

Year 5 79500

6

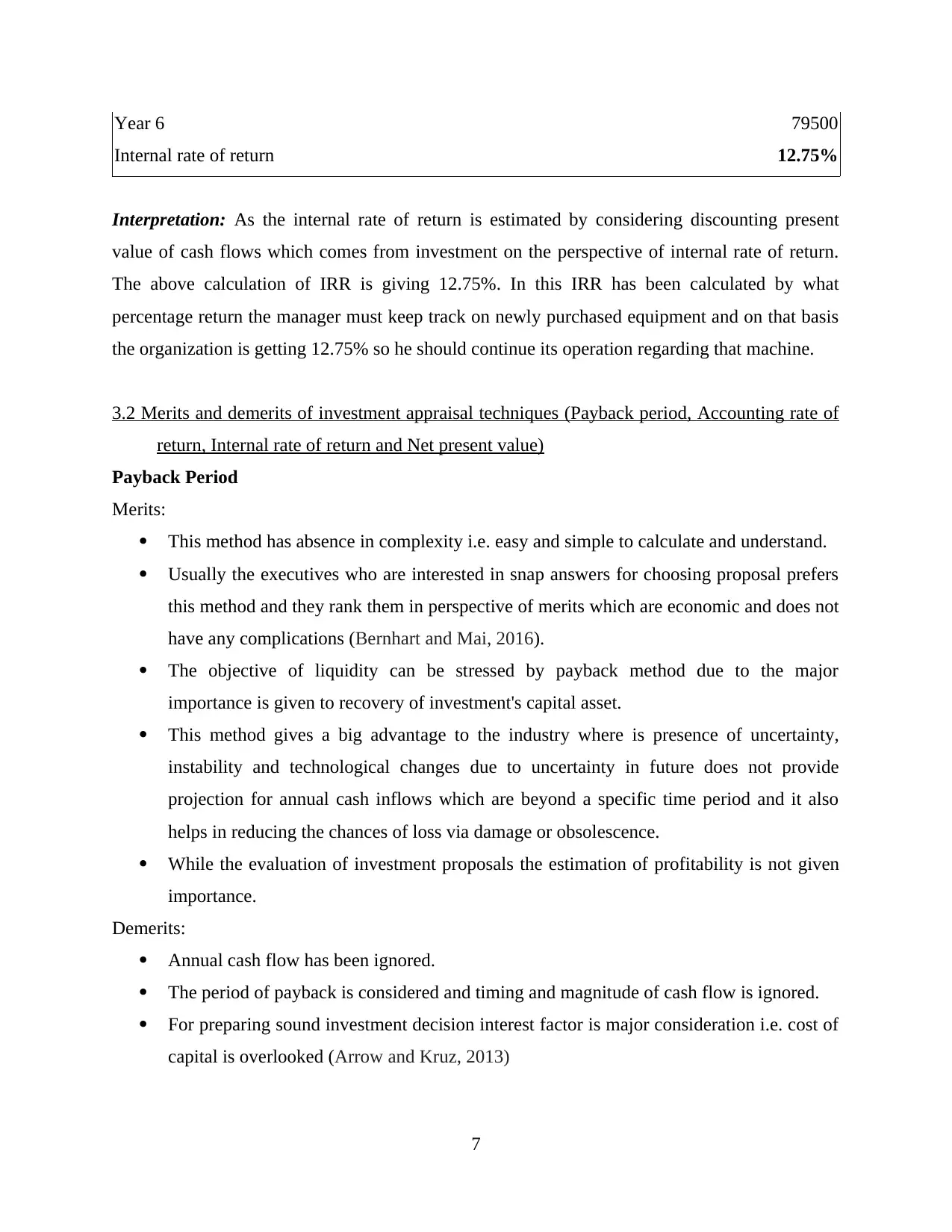

Year 6 79500

Internal rate of return 12.75%

Interpretation: As the internal rate of return is estimated by considering discounting present

value of cash flows which comes from investment on the perspective of internal rate of return.

The above calculation of IRR is giving 12.75%. In this IRR has been calculated by what

percentage return the manager must keep track on newly purchased equipment and on that basis

the organization is getting 12.75% so he should continue its operation regarding that machine.

3.2 Merits and demerits of investment appraisal techniques (Payback period, Accounting rate of

return, Internal rate of return and Net present value)

Payback Period

Merits:

This method has absence in complexity i.e. easy and simple to calculate and understand.

Usually the executives who are interested in snap answers for choosing proposal prefers

this method and they rank them in perspective of merits which are economic and does not

have any complications (Bernhart and Mai, 2016).

The objective of liquidity can be stressed by payback method due to the major

importance is given to recovery of investment's capital asset.

This method gives a big advantage to the industry where is presence of uncertainty,

instability and technological changes due to uncertainty in future does not provide

projection for annual cash inflows which are beyond a specific time period and it also

helps in reducing the chances of loss via damage or obsolescence.

While the evaluation of investment proposals the estimation of profitability is not given

importance.

Demerits:

Annual cash flow has been ignored.

The period of payback is considered and timing and magnitude of cash flow is ignored.

For preparing sound investment decision interest factor is major consideration i.e. cost of

capital is overlooked (Arrow and Kruz, 2013)

7

Internal rate of return 12.75%

Interpretation: As the internal rate of return is estimated by considering discounting present

value of cash flows which comes from investment on the perspective of internal rate of return.

The above calculation of IRR is giving 12.75%. In this IRR has been calculated by what

percentage return the manager must keep track on newly purchased equipment and on that basis

the organization is getting 12.75% so he should continue its operation regarding that machine.

3.2 Merits and demerits of investment appraisal techniques (Payback period, Accounting rate of

return, Internal rate of return and Net present value)

Payback Period

Merits:

This method has absence in complexity i.e. easy and simple to calculate and understand.

Usually the executives who are interested in snap answers for choosing proposal prefers

this method and they rank them in perspective of merits which are economic and does not

have any complications (Bernhart and Mai, 2016).

The objective of liquidity can be stressed by payback method due to the major

importance is given to recovery of investment's capital asset.

This method gives a big advantage to the industry where is presence of uncertainty,

instability and technological changes due to uncertainty in future does not provide

projection for annual cash inflows which are beyond a specific time period and it also

helps in reducing the chances of loss via damage or obsolescence.

While the evaluation of investment proposals the estimation of profitability is not given

importance.

Demerits:

Annual cash flow has been ignored.

The period of payback is considered and timing and magnitude of cash flow is ignored.

For preparing sound investment decision interest factor is major consideration i.e. cost of

capital is overlooked (Arrow and Kruz, 2013)

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Usually it is subjective decision of management where so many administrative

difficulties are created and decision are not on rational basis.

Rigidity and delicacy is present in this method.

It has special emphasis on liquidity on the perspective of objective of decisions which are

related to expenditure.

Accounting rate of return

Merits:

This method has similarity of payback period that it is very simple and concise for

understanding and calculating.

Total earnings are been considered from the project along with whole economic life.

Due weight has been provided by this approach and project has been profitable from this.

ARR is based on proper accounting information instead of cash inflows.

It has been used by many people because of simplicity of capital budgeting technique and

its attractiveness of investment project.

For measuring current performance and stability of organisation it is used and in extreme

long lives, there will be presence of simple rate of return which is absolute rate of return.

Demerits:

The results relate to this approach are very inconsistent (Penman and Zhu, 2014).

As this method is very simple averaging technique so it does not consider the impacts of

external factors on the aggregate profit of the organisation.

Time factor or time value of money is ignored that is a very crucial aspect of business.

The fair and faithful rate of return on investment is not identified and it is kept hold on

discretion of management and arbitrary returns' rate may impact very serious problems

for choosing capital projects.

Risk are not adjusted for forecasts on the perspective of long term.

As this method can be calculated in various ways so it will lead to various outcomes.

Net Present value

Merits:

Net present value gives special emphasis on time value of money.

For the entire life of project earnings and savings are been considered and they can be

easily transformed into present value of money.

8

difficulties are created and decision are not on rational basis.

Rigidity and delicacy is present in this method.

It has special emphasis on liquidity on the perspective of objective of decisions which are

related to expenditure.

Accounting rate of return

Merits:

This method has similarity of payback period that it is very simple and concise for

understanding and calculating.

Total earnings are been considered from the project along with whole economic life.

Due weight has been provided by this approach and project has been profitable from this.

ARR is based on proper accounting information instead of cash inflows.

It has been used by many people because of simplicity of capital budgeting technique and

its attractiveness of investment project.

For measuring current performance and stability of organisation it is used and in extreme

long lives, there will be presence of simple rate of return which is absolute rate of return.

Demerits:

The results relate to this approach are very inconsistent (Penman and Zhu, 2014).

As this method is very simple averaging technique so it does not consider the impacts of

external factors on the aggregate profit of the organisation.

Time factor or time value of money is ignored that is a very crucial aspect of business.

The fair and faithful rate of return on investment is not identified and it is kept hold on

discretion of management and arbitrary returns' rate may impact very serious problems

for choosing capital projects.

Risk are not adjusted for forecasts on the perspective of long term.

As this method can be calculated in various ways so it will lead to various outcomes.

Net Present value

Merits:

Net present value gives special emphasis on time value of money.

For the entire life of project earnings and savings are been considered and they can be

easily transformed into present value of money.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

It gives proper classification and comparison of assessment of various projects.

While comparing on the basis of net present value, the highest amount of NPV can be

implemented and this will maximise profit of organizations and its efficiency will

increase.

The implementation can be on basis of cash flow which are even or non even.

Usually every economists prefer this method due to theoretically unassailable.

High priority has been assigned to profitability and risk.

Demerits:

The expected rate of return which is gained cannot be indicated in this method.

When there is requirement of various different levels of investment amount along with

this different economic life span of projects so this method has not capability to provide

satisfactory result.

There is basic requirement of knowledge of cost of capital's rate and if there is deficiency

of cost of capital then this method cannot be implemented.

While ranking some typical and complicated projects NPV gives very much

contradictory and confusing result.

The most typical task in this method to identify appropriate discount rate.

This method cannot be implemented for evaluating of finding the life span or years which

are required for recoup expenditure of capital that is amount required for project.

Internal rate of return

Merits:

Time value of money or time factor is been considered by this method along with cash

flow whether it is even or uneven.

Profitability of project is been evaluated very perfectly that whole economic life is

considered in the project.

There is not any requirement related to pre determining the capital's cost or the cut off

rate. It overcomes the weakness of net present value.

The above pre determination capital's cost is very difficult task and on that particular time

for evaluating project internal rate of return method is used.

The project proposals can be ranked very easily in the mentioned method because it gives

specific percentage return.

9

While comparing on the basis of net present value, the highest amount of NPV can be

implemented and this will maximise profit of organizations and its efficiency will

increase.

The implementation can be on basis of cash flow which are even or non even.

Usually every economists prefer this method due to theoretically unassailable.

High priority has been assigned to profitability and risk.

Demerits:

The expected rate of return which is gained cannot be indicated in this method.

When there is requirement of various different levels of investment amount along with

this different economic life span of projects so this method has not capability to provide

satisfactory result.

There is basic requirement of knowledge of cost of capital's rate and if there is deficiency

of cost of capital then this method cannot be implemented.

While ranking some typical and complicated projects NPV gives very much

contradictory and confusing result.

The most typical task in this method to identify appropriate discount rate.

This method cannot be implemented for evaluating of finding the life span or years which

are required for recoup expenditure of capital that is amount required for project.

Internal rate of return

Merits:

Time value of money or time factor is been considered by this method along with cash

flow whether it is even or uneven.

Profitability of project is been evaluated very perfectly that whole economic life is

considered in the project.

There is not any requirement related to pre determining the capital's cost or the cut off

rate. It overcomes the weakness of net present value.

The above pre determination capital's cost is very difficult task and on that particular time

for evaluating project internal rate of return method is used.

The project proposals can be ranked very easily in the mentioned method because it gives

specific percentage return.

9

Profitability can be maximized from this method (Mahlia, Razak. and Nursahida, 2011).

The total cash outflows and inflows can be accounted in internal rate of return.

The special importance is been provided for maximising wealth of shareholder.

Demerits:

In this method margin or earnings are reinvested at internal rate of return for life of

project which is remaining. The profit related to project are not properly justifiable.

It has very difficult and tedious calculations.

Special importance have been given to profit but capital expenditure which has been

recouped earlier is not considered because of this method is in favour of projects which

are in need of long term period as compared to other project and conditions which are

regarding to this or future uncertainty so whole capital expenditure is not recouped if IRR

is adopted.

The outcome of NPV and IRR are usually different because of under evaluation in their

life, size or even timings related to cash inflows.

CONCLUSION

From the above report it has been concluded that financial management plays very

important role in any business and organisation. The proper way to identify and determine the

share price, theoretical rights issue price with its explanation has been understood. Scrip

dividends plays vital role in any organisations. Scrip dividends are shares issue which are

performed in a way as to again compensate shareholders rather than traditional dividend which

also helps in raising capital of the organisation. Further it can be said that investment proposal

techniques are basic means for measuring capital of investment of any business project which

includes net present value, Internal rate of return, Accounting rate of return and payback period.

Every technique has its own advantages and disadvantages.

10

The total cash outflows and inflows can be accounted in internal rate of return.

The special importance is been provided for maximising wealth of shareholder.

Demerits:

In this method margin or earnings are reinvested at internal rate of return for life of

project which is remaining. The profit related to project are not properly justifiable.

It has very difficult and tedious calculations.

Special importance have been given to profit but capital expenditure which has been

recouped earlier is not considered because of this method is in favour of projects which

are in need of long term period as compared to other project and conditions which are

regarding to this or future uncertainty so whole capital expenditure is not recouped if IRR

is adopted.

The outcome of NPV and IRR are usually different because of under evaluation in their

life, size or even timings related to cash inflows.

CONCLUSION

From the above report it has been concluded that financial management plays very

important role in any business and organisation. The proper way to identify and determine the

share price, theoretical rights issue price with its explanation has been understood. Scrip

dividends plays vital role in any organisations. Scrip dividends are shares issue which are

performed in a way as to again compensate shareholders rather than traditional dividend which

also helps in raising capital of the organisation. Further it can be said that investment proposal

techniques are basic means for measuring capital of investment of any business project which

includes net present value, Internal rate of return, Accounting rate of return and payback period.

Every technique has its own advantages and disadvantages.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.