Financial Management Report: Dividend Policy and Appraisal Techniques

VerifiedAdded on 2020/11/12

|14

|3703

|143

Report

AI Summary

This report delves into the core aspects of financial management, commencing with an analysis of dividend policy as adopted by Planet for distributing dividends to its shareholders. It explores the application of the dividend growth model for share valuation, providing calculations and addressing the associated challenges. Furthermore, the report examines investment appraisal techniques, including payback period, accounting rate of return, net present value, and internal rate of return, offering detailed calculations and recommendations for Lovewell Limited, a food manufacturing company considering the purchase of a new machine. It also outlines the benefits and limitations of each investment appraisal technique, providing a comprehensive overview of financial management principles and their practical applications in investment decision-making.

Financial Management

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................2

MAIN BODY...................................................................................................................................3

QUESTION 1...................................................................................................................................3

a. Fair share price for Planet's shares..........................................................................................3

b. Calculating new share price for Planet's share........................................................................3

c. Dividend growth model use for valuing shares and problem faced........................................4

QUESTION 3. Investment Appraisal Techniques...........................................................................5

1. Calculating following techniques along with recommendations............................................5

....................................................................................................................................................5

a. Payback period........................................................................................................................5

b. Computation of Accounting Rate of Return...........................................................................6

c. Computation of Net Present Value.........................................................................................6

d. Internal rate of return (IRR)....................................................................................................7

2. Benefits and limitations of various Investment appraisal techniques.....................................8

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION...........................................................................................................................2

MAIN BODY...................................................................................................................................3

QUESTION 1...................................................................................................................................3

a. Fair share price for Planet's shares..........................................................................................3

b. Calculating new share price for Planet's share........................................................................3

c. Dividend growth model use for valuing shares and problem faced........................................4

QUESTION 3. Investment Appraisal Techniques...........................................................................5

1. Calculating following techniques along with recommendations............................................5

....................................................................................................................................................5

a. Payback period........................................................................................................................5

b. Computation of Accounting Rate of Return...........................................................................6

c. Computation of Net Present Value.........................................................................................6

d. Internal rate of return (IRR)....................................................................................................7

2. Benefits and limitations of various Investment appraisal techniques.....................................8

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

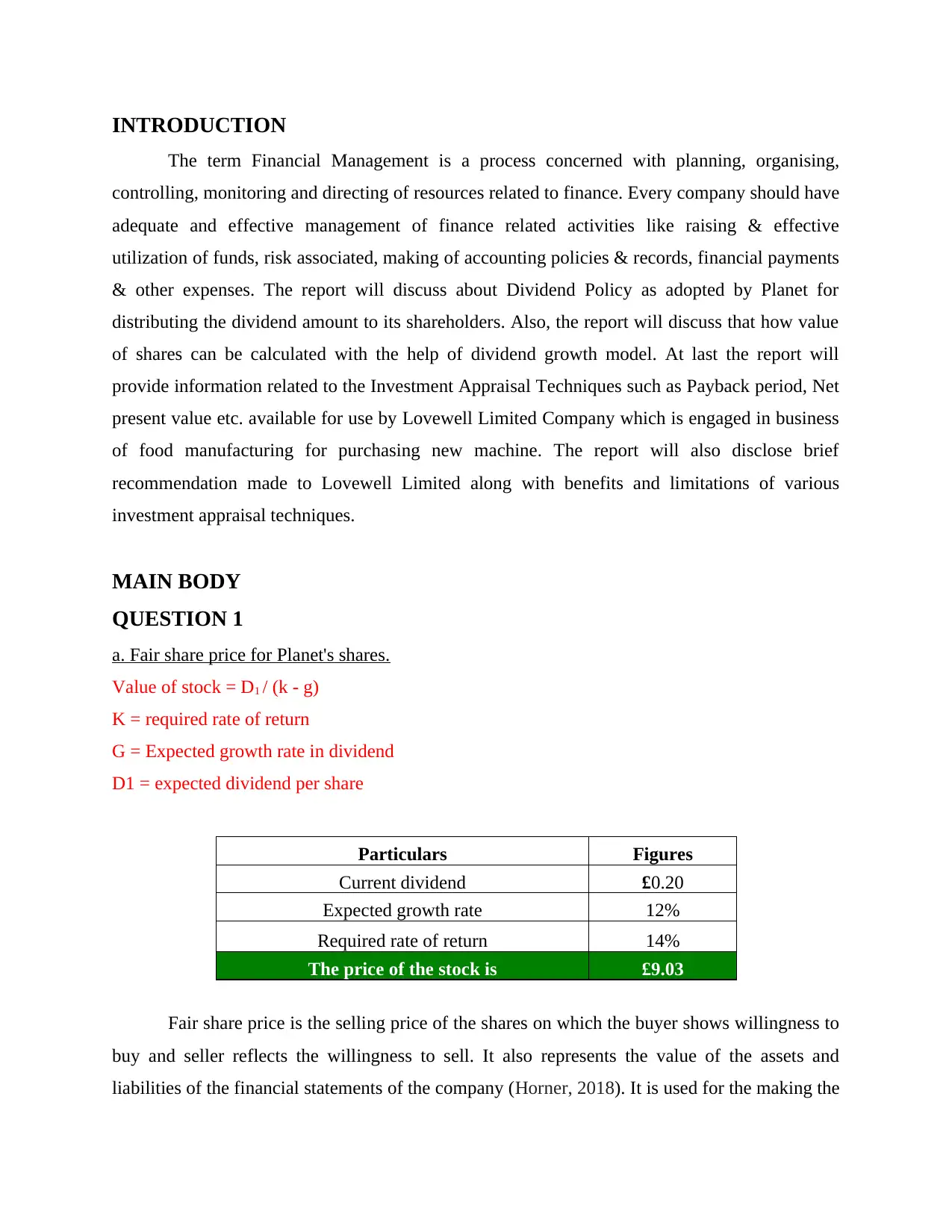

INTRODUCTION

The term Financial Management is a process concerned with planning, organising,

controlling, monitoring and directing of resources related to finance. Every company should have

adequate and effective management of finance related activities like raising & effective

utilization of funds, risk associated, making of accounting policies & records, financial payments

& other expenses. The report will discuss about Dividend Policy as adopted by Planet for

distributing the dividend amount to its shareholders. Also, the report will discuss that how value

of shares can be calculated with the help of dividend growth model. At last the report will

provide information related to the Investment Appraisal Techniques such as Payback period, Net

present value etc. available for use by Lovewell Limited Company which is engaged in business

of food manufacturing for purchasing new machine. The report will also disclose brief

recommendation made to Lovewell Limited along with benefits and limitations of various

investment appraisal techniques.

MAIN BODY

QUESTION 1

a. Fair share price for Planet's shares.

Value of stock = D1 / (k - g)

K = required rate of return

G = Expected growth rate in dividend

D1 = expected dividend per share

Particulars Figures

Current dividend £0.20

Expected growth rate 12%

Required rate of return 14%

The price of the stock is £9.03

Fair share price is the selling price of the shares on which the buyer shows willingness to

buy and seller reflects the willingness to sell. It also represents the value of the assets and

liabilities of the financial statements of the company (Horner, 2018). It is used for the making the

The term Financial Management is a process concerned with planning, organising,

controlling, monitoring and directing of resources related to finance. Every company should have

adequate and effective management of finance related activities like raising & effective

utilization of funds, risk associated, making of accounting policies & records, financial payments

& other expenses. The report will discuss about Dividend Policy as adopted by Planet for

distributing the dividend amount to its shareholders. Also, the report will discuss that how value

of shares can be calculated with the help of dividend growth model. At last the report will

provide information related to the Investment Appraisal Techniques such as Payback period, Net

present value etc. available for use by Lovewell Limited Company which is engaged in business

of food manufacturing for purchasing new machine. The report will also disclose brief

recommendation made to Lovewell Limited along with benefits and limitations of various

investment appraisal techniques.

MAIN BODY

QUESTION 1

a. Fair share price for Planet's shares.

Value of stock = D1 / (k - g)

K = required rate of return

G = Expected growth rate in dividend

D1 = expected dividend per share

Particulars Figures

Current dividend £0.20

Expected growth rate 12%

Required rate of return 14%

The price of the stock is £9.03

Fair share price is the selling price of the shares on which the buyer shows willingness to

buy and seller reflects the willingness to sell. It also represents the value of the assets and

liabilities of the financial statements of the company (Horner, 2018). It is used for the making the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

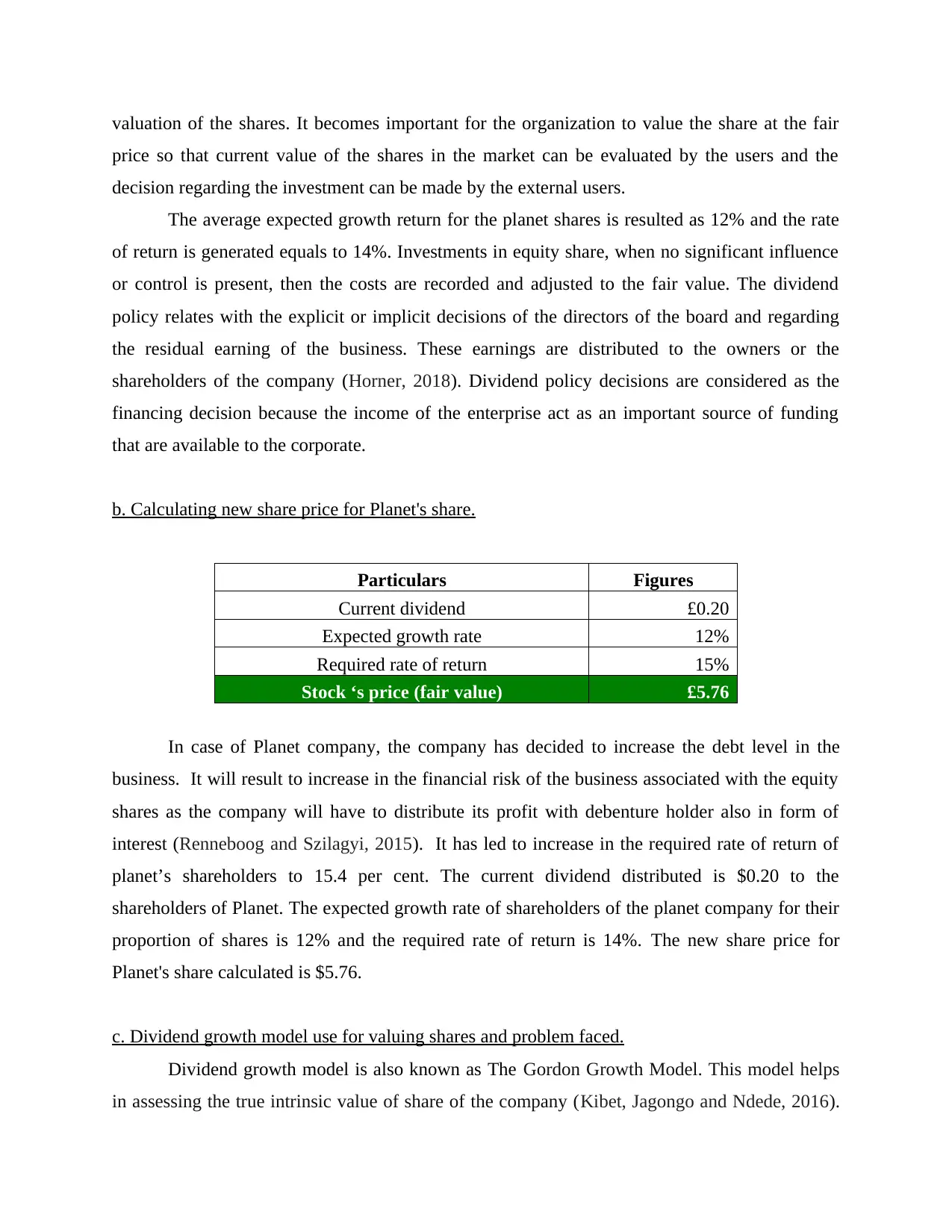

valuation of the shares. It becomes important for the organization to value the share at the fair

price so that current value of the shares in the market can be evaluated by the users and the

decision regarding the investment can be made by the external users.

The average expected growth return for the planet shares is resulted as 12% and the rate

of return is generated equals to 14%. Investments in equity share, when no significant influence

or control is present, then the costs are recorded and adjusted to the fair value. The dividend

policy relates with the explicit or implicit decisions of the directors of the board and regarding

the residual earning of the business. These earnings are distributed to the owners or the

shareholders of the company (Horner, 2018). Dividend policy decisions are considered as the

financing decision because the income of the enterprise act as an important source of funding

that are available to the corporate.

b. Calculating new share price for Planet's share.

Particulars Figures

Current dividend £0.20

Expected growth rate 12%

Required rate of return 15%

Stock ‘s price (fair value) £5.76

In case of Planet company, the company has decided to increase the debt level in the

business. It will result to increase in the financial risk of the business associated with the equity

shares as the company will have to distribute its profit with debenture holder also in form of

interest (Renneboog and Szilagyi, 2015). It has led to increase in the required rate of return of

planet’s shareholders to 15.4 per cent. The current dividend distributed is $0.20 to the

shareholders of Planet. The expected growth rate of shareholders of the planet company for their

proportion of shares is 12% and the required rate of return is 14%. The new share price for

Planet's share calculated is $5.76.

c. Dividend growth model use for valuing shares and problem faced.

Dividend growth model is also known as The Gordon Growth Model. This model helps

in assessing the true intrinsic value of share of the company (Kibet, Jagongo and Ndede, 2016).

price so that current value of the shares in the market can be evaluated by the users and the

decision regarding the investment can be made by the external users.

The average expected growth return for the planet shares is resulted as 12% and the rate

of return is generated equals to 14%. Investments in equity share, when no significant influence

or control is present, then the costs are recorded and adjusted to the fair value. The dividend

policy relates with the explicit or implicit decisions of the directors of the board and regarding

the residual earning of the business. These earnings are distributed to the owners or the

shareholders of the company (Horner, 2018). Dividend policy decisions are considered as the

financing decision because the income of the enterprise act as an important source of funding

that are available to the corporate.

b. Calculating new share price for Planet's share.

Particulars Figures

Current dividend £0.20

Expected growth rate 12%

Required rate of return 15%

Stock ‘s price (fair value) £5.76

In case of Planet company, the company has decided to increase the debt level in the

business. It will result to increase in the financial risk of the business associated with the equity

shares as the company will have to distribute its profit with debenture holder also in form of

interest (Renneboog and Szilagyi, 2015). It has led to increase in the required rate of return of

planet’s shareholders to 15.4 per cent. The current dividend distributed is $0.20 to the

shareholders of Planet. The expected growth rate of shareholders of the planet company for their

proportion of shares is 12% and the required rate of return is 14%. The new share price for

Planet's share calculated is $5.76.

c. Dividend growth model use for valuing shares and problem faced.

Dividend growth model is also known as The Gordon Growth Model. This model helps

in assessing the true intrinsic value of share of the company (Kibet, Jagongo and Ndede, 2016).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

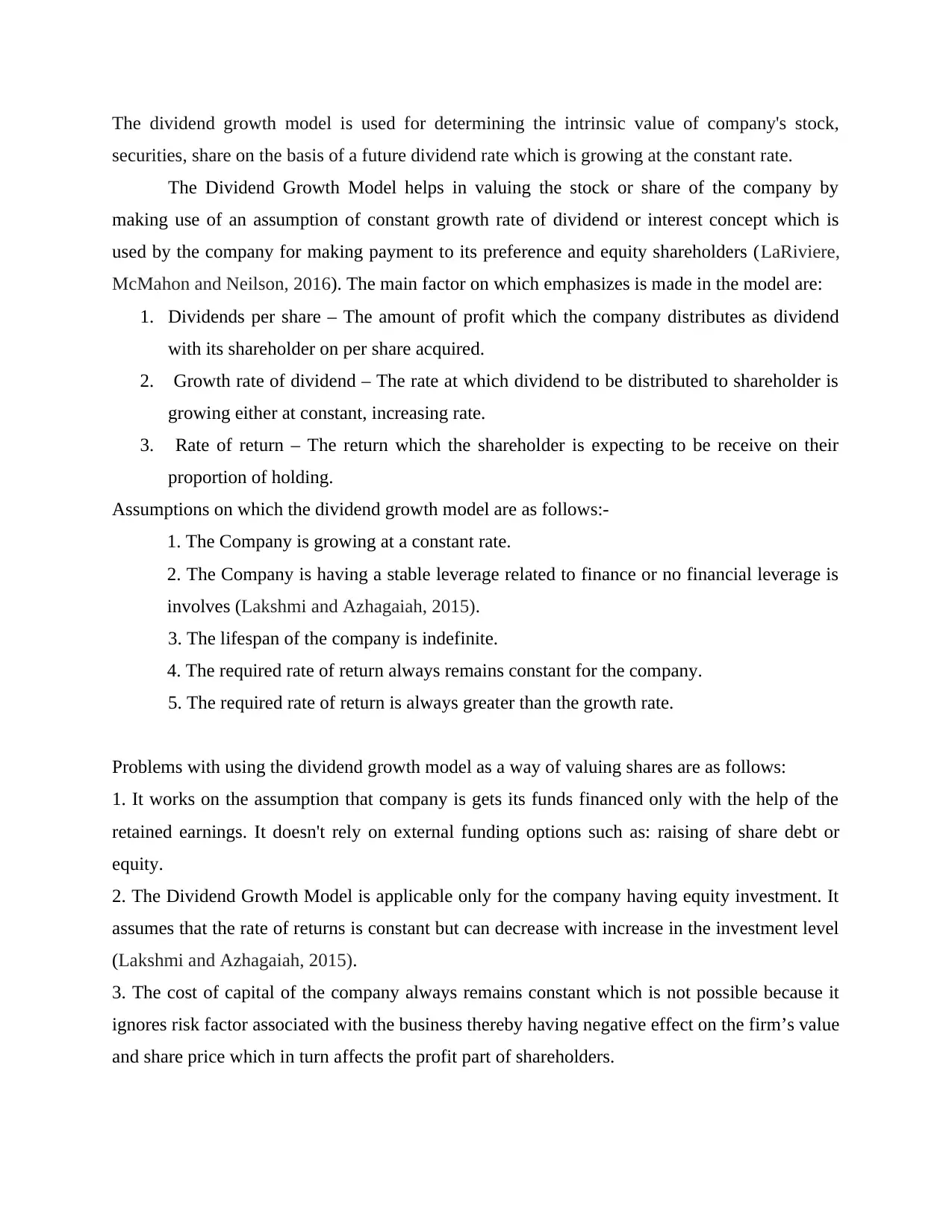

The dividend growth model is used for determining the intrinsic value of company's stock,

securities, share on the basis of a future dividend rate which is growing at the constant rate.

The Dividend Growth Model helps in valuing the stock or share of the company by

making use of an assumption of constant growth rate of dividend or interest concept which is

used by the company for making payment to its preference and equity shareholders (LaRiviere,

McMahon and Neilson, 2016). The main factor on which emphasizes is made in the model are:

1. Dividends per share – The amount of profit which the company distributes as dividend

with its shareholder on per share acquired.

2. Growth rate of dividend – The rate at which dividend to be distributed to shareholder is

growing either at constant, increasing rate.

3. Rate of return – The return which the shareholder is expecting to be receive on their

proportion of holding.

Assumptions on which the dividend growth model are as follows:-

1. The Company is growing at a constant rate.

2. The Company is having a stable leverage related to finance or no financial leverage is

involves (Lakshmi and Azhagaiah, 2015).

3. The lifespan of the company is indefinite.

4. The required rate of return always remains constant for the company.

5. The required rate of return is always greater than the growth rate.

Problems with using the dividend growth model as a way of valuing shares are as follows:

1. It works on the assumption that company is gets its funds financed only with the help of the

retained earnings. It doesn't rely on external funding options such as: raising of share debt or

equity.

2. The Dividend Growth Model is applicable only for the company having equity investment. It

assumes that the rate of returns is constant but can decrease with increase in the investment level

(Lakshmi and Azhagaiah, 2015).

3. The cost of capital of the company always remains constant which is not possible because it

ignores risk factor associated with the business thereby having negative effect on the firm’s value

and share price which in turn affects the profit part of shareholders.

securities, share on the basis of a future dividend rate which is growing at the constant rate.

The Dividend Growth Model helps in valuing the stock or share of the company by

making use of an assumption of constant growth rate of dividend or interest concept which is

used by the company for making payment to its preference and equity shareholders (LaRiviere,

McMahon and Neilson, 2016). The main factor on which emphasizes is made in the model are:

1. Dividends per share – The amount of profit which the company distributes as dividend

with its shareholder on per share acquired.

2. Growth rate of dividend – The rate at which dividend to be distributed to shareholder is

growing either at constant, increasing rate.

3. Rate of return – The return which the shareholder is expecting to be receive on their

proportion of holding.

Assumptions on which the dividend growth model are as follows:-

1. The Company is growing at a constant rate.

2. The Company is having a stable leverage related to finance or no financial leverage is

involves (Lakshmi and Azhagaiah, 2015).

3. The lifespan of the company is indefinite.

4. The required rate of return always remains constant for the company.

5. The required rate of return is always greater than the growth rate.

Problems with using the dividend growth model as a way of valuing shares are as follows:

1. It works on the assumption that company is gets its funds financed only with the help of the

retained earnings. It doesn't rely on external funding options such as: raising of share debt or

equity.

2. The Dividend Growth Model is applicable only for the company having equity investment. It

assumes that the rate of returns is constant but can decrease with increase in the investment level

(Lakshmi and Azhagaiah, 2015).

3. The cost of capital of the company always remains constant which is not possible because it

ignores risk factor associated with the business thereby having negative effect on the firm’s value

and share price which in turn affects the profit part of shareholders.

QUESTION 3. Investment Appraisal Techniques

1. Calculating following techniques along with recommendations.

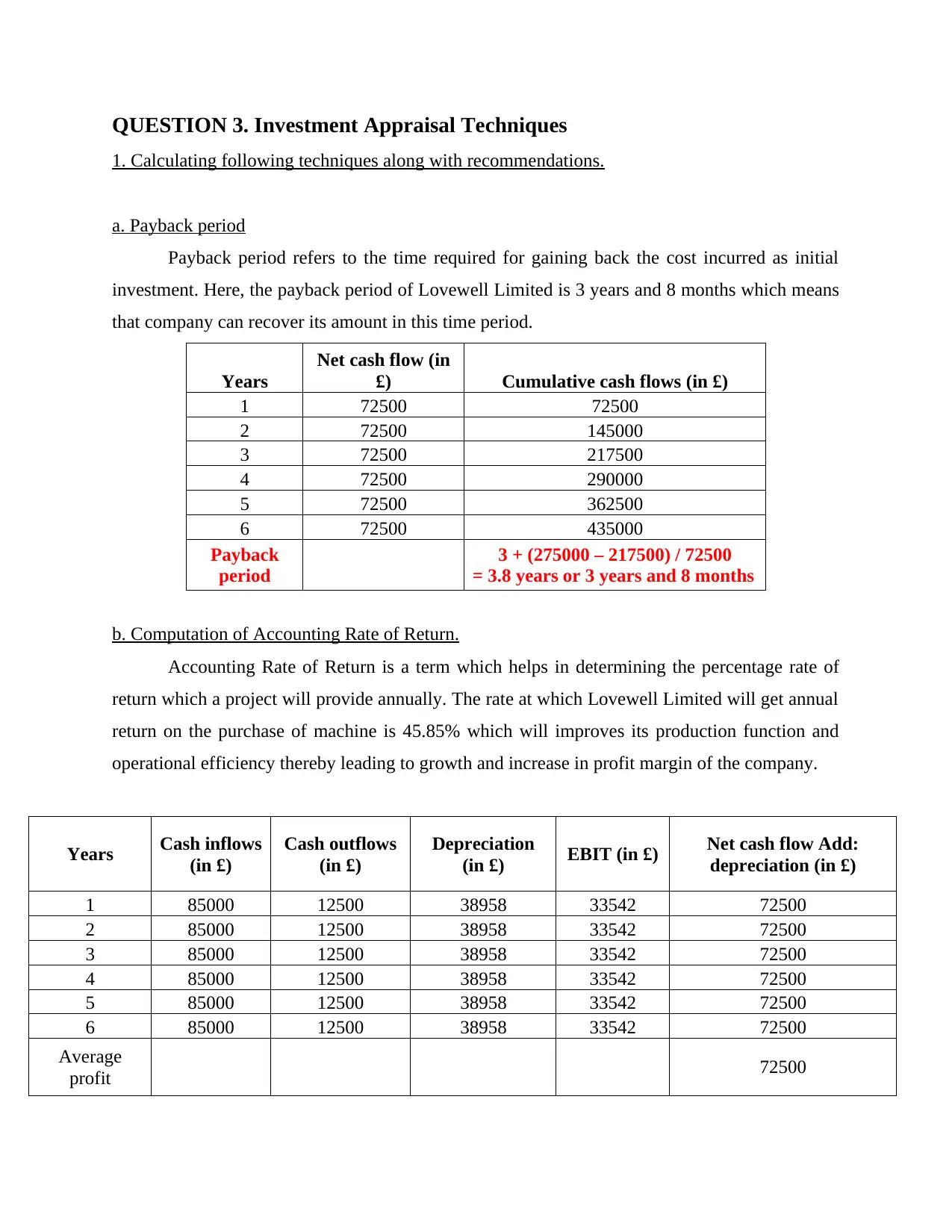

a. Payback period

Payback period refers to the time required for gaining back the cost incurred as initial

investment. Here, the payback period of Lovewell Limited is 3 years and 8 months which means

that company can recover its amount in this time period.

Years

Net cash flow (in

£) Cumulative cash flows (in £)

1 72500 72500

2 72500 145000

3 72500 217500

4 72500 290000

5 72500 362500

6 72500 435000

Payback

period

3 + (275000 – 217500) / 72500

= 3.8 years or 3 years and 8 months

b. Computation of Accounting Rate of Return.

Accounting Rate of Return is a term which helps in determining the percentage rate of

return which a project will provide annually. The rate at which Lovewell Limited will get annual

return on the purchase of machine is 45.85% which will improves its production function and

operational efficiency thereby leading to growth and increase in profit margin of the company.

Years Cash inflows

(in £)

Cash outflows

(in £)

Depreciation

(in £) EBIT (in £) Net cash flow Add:

depreciation (in £)

1 85000 12500 38958 33542 72500

2 85000 12500 38958 33542 72500

3 85000 12500 38958 33542 72500

4 85000 12500 38958 33542 72500

5 85000 12500 38958 33542 72500

6 85000 12500 38958 33542 72500

Average

profit 72500

1. Calculating following techniques along with recommendations.

a. Payback period

Payback period refers to the time required for gaining back the cost incurred as initial

investment. Here, the payback period of Lovewell Limited is 3 years and 8 months which means

that company can recover its amount in this time period.

Years

Net cash flow (in

£) Cumulative cash flows (in £)

1 72500 72500

2 72500 145000

3 72500 217500

4 72500 290000

5 72500 362500

6 72500 435000

Payback

period

3 + (275000 – 217500) / 72500

= 3.8 years or 3 years and 8 months

b. Computation of Accounting Rate of Return.

Accounting Rate of Return is a term which helps in determining the percentage rate of

return which a project will provide annually. The rate at which Lovewell Limited will get annual

return on the purchase of machine is 45.85% which will improves its production function and

operational efficiency thereby leading to growth and increase in profit margin of the company.

Years Cash inflows

(in £)

Cash outflows

(in £)

Depreciation

(in £) EBIT (in £) Net cash flow Add:

depreciation (in £)

1 85000 12500 38958 33542 72500

2 85000 12500 38958 33542 72500

3 85000 12500 38958 33542 72500

4 85000 12500 38958 33542 72500

5 85000 12500 38958 33542 72500

6 85000 12500 38958 33542 72500

Average

profit 72500

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

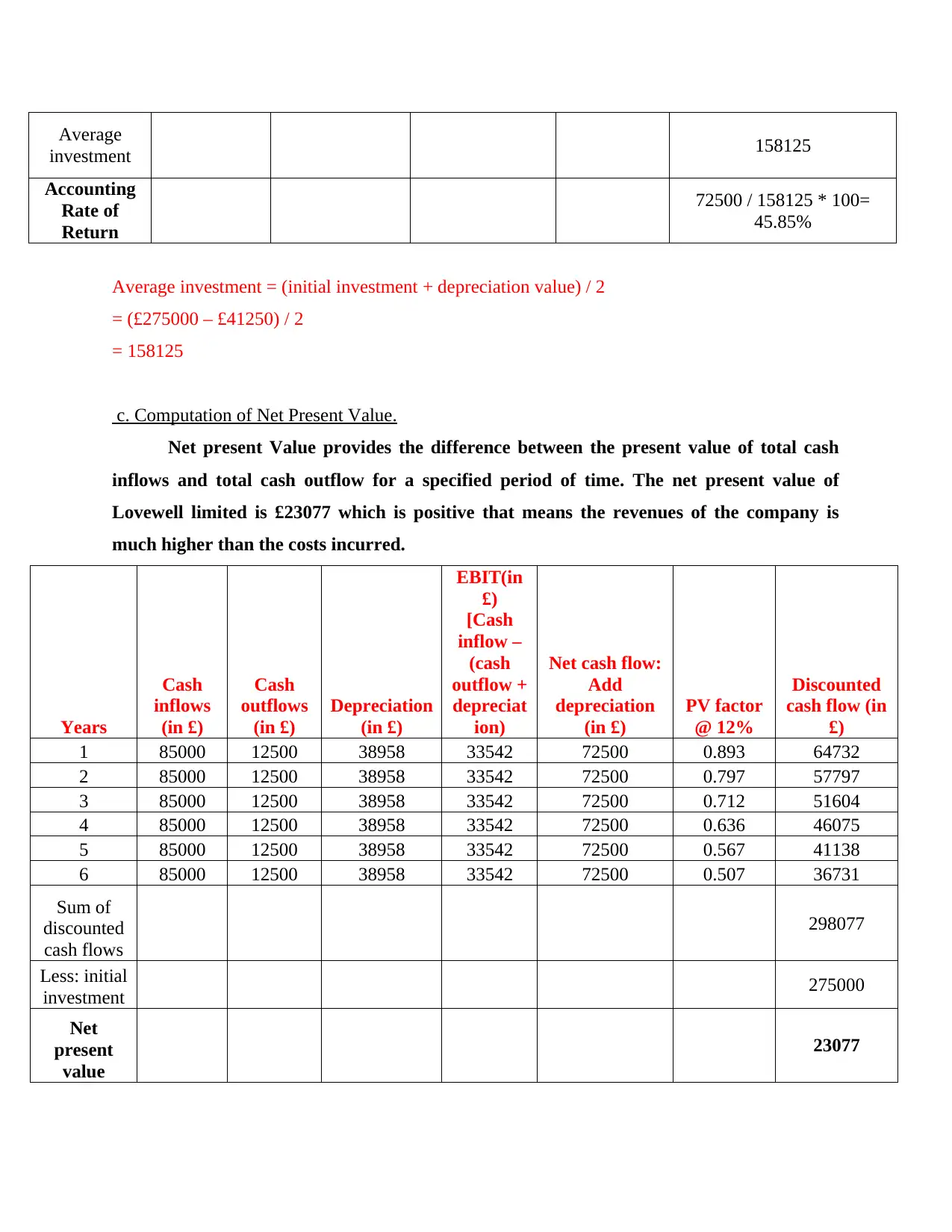

Average

investment 158125

Accounting

Rate of

Return

72500 / 158125 * 100=

45.85%

Average investment = (initial investment + depreciation value) / 2

= (£275000 – £41250) / 2

= 158125

c. Computation of Net Present Value.

Net present Value provides the difference between the present value of total cash

inflows and total cash outflow for a specified period of time. The net present value of

Lovewell limited is £23077 which is positive that means the revenues of the company is

much higher than the costs incurred.

Years

Cash

inflows

(in £)

Cash

outflows

(in £)

Depreciation

(in £)

EBIT(in

£)

[Cash

inflow –

(cash

outflow +

depreciat

ion)

Net cash flow:

Add

depreciation

(in £)

PV factor

@ 12%

Discounted

cash flow (in

£)

1 85000 12500 38958 33542 72500 0.893 64732

2 85000 12500 38958 33542 72500 0.797 57797

3 85000 12500 38958 33542 72500 0.712 51604

4 85000 12500 38958 33542 72500 0.636 46075

5 85000 12500 38958 33542 72500 0.567 41138

6 85000 12500 38958 33542 72500 0.507 36731

Sum of

discounted

cash flows

298077

Less: initial

investment 275000

Net

present

value

23077

investment 158125

Accounting

Rate of

Return

72500 / 158125 * 100=

45.85%

Average investment = (initial investment + depreciation value) / 2

= (£275000 – £41250) / 2

= 158125

c. Computation of Net Present Value.

Net present Value provides the difference between the present value of total cash

inflows and total cash outflow for a specified period of time. The net present value of

Lovewell limited is £23077 which is positive that means the revenues of the company is

much higher than the costs incurred.

Years

Cash

inflows

(in £)

Cash

outflows

(in £)

Depreciation

(in £)

EBIT(in

£)

[Cash

inflow –

(cash

outflow +

depreciat

ion)

Net cash flow:

Add

depreciation

(in £)

PV factor

@ 12%

Discounted

cash flow (in

£)

1 85000 12500 38958 33542 72500 0.893 64732

2 85000 12500 38958 33542 72500 0.797 57797

3 85000 12500 38958 33542 72500 0.712 51604

4 85000 12500 38958 33542 72500 0.636 46075

5 85000 12500 38958 33542 72500 0.567 41138

6 85000 12500 38958 33542 72500 0.507 36731

Sum of

discounted

cash flows

298077

Less: initial

investment 275000

Net

present

value

23077

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

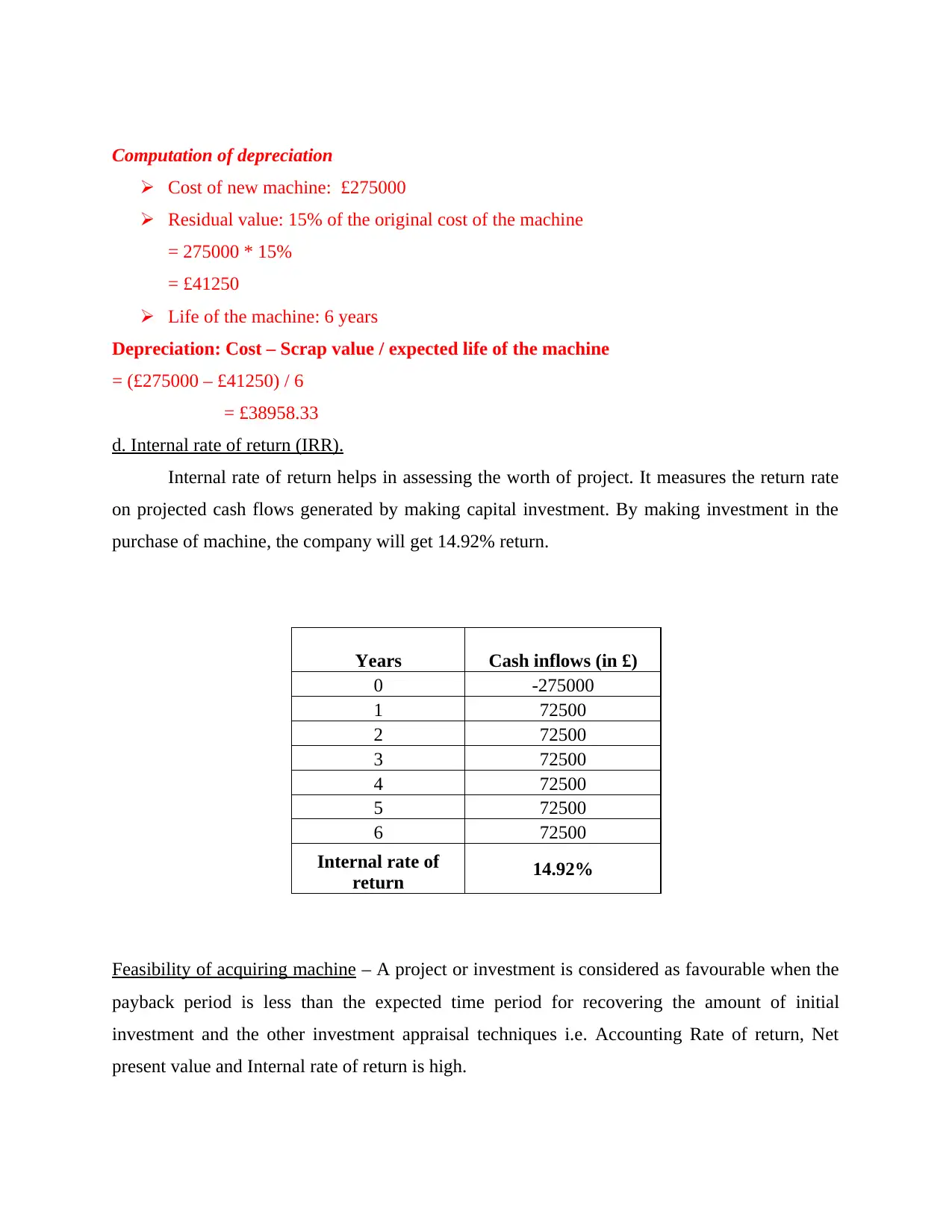

Computation of depreciation

Cost of new machine: £275000

Residual value: 15% of the original cost of the machine

= 275000 * 15%

= £41250

Life of the machine: 6 years

Depreciation: Cost – Scrap value / expected life of the machine

= (£275000 – £41250) / 6

= £38958.33

d. Internal rate of return (IRR).

Internal rate of return helps in assessing the worth of project. It measures the return rate

on projected cash flows generated by making capital investment. By making investment in the

purchase of machine, the company will get 14.92% return.

Years Cash inflows (in £)

0 -275000

1 72500

2 72500

3 72500

4 72500

5 72500

6 72500

Internal rate of

return 14.92%

Feasibility of acquiring machine – A project or investment is considered as favourable when the

payback period is less than the expected time period for recovering the amount of initial

investment and the other investment appraisal techniques i.e. Accounting Rate of return, Net

present value and Internal rate of return is high.

Cost of new machine: £275000

Residual value: 15% of the original cost of the machine

= 275000 * 15%

= £41250

Life of the machine: 6 years

Depreciation: Cost – Scrap value / expected life of the machine

= (£275000 – £41250) / 6

= £38958.33

d. Internal rate of return (IRR).

Internal rate of return helps in assessing the worth of project. It measures the return rate

on projected cash flows generated by making capital investment. By making investment in the

purchase of machine, the company will get 14.92% return.

Years Cash inflows (in £)

0 -275000

1 72500

2 72500

3 72500

4 72500

5 72500

6 72500

Internal rate of

return 14.92%

Feasibility of acquiring machine – A project or investment is considered as favourable when the

payback period is less than the expected time period for recovering the amount of initial

investment and the other investment appraisal techniques i.e. Accounting Rate of return, Net

present value and Internal rate of return is high.

In this case, the payback period of Lovewell Limited is 3 years and 8 months which

depicts that it company makes investment in purchasing of new machine than it will be able to

recover the cost involves in purchasing within 3 years and 8 months.

Also, the accounting rate of return of the company is 45.85% which shows that company

will get such percentage amount as the rate of return on purchase of machine.

The net present value of the company is also positive which shows that it will be

favorable for the company to acquire new machine as it will lead to increase in the productivity

as well as profitability of the company thereby improving the performance of the company as a

whole.

When it comes to internal rate of return, Lovewell Limited is having 14.92%. It shows

that company will get 14.92% rate of return when it will make capital investment in acquisition

of new machine.

Thus, it can be said that on purchasing of new machine, Lovewell Limited can recover its

cost in 3.8 year with positive net present value of £23077 having 14.92% and 45.85% as internal

and accounting rate of return respectively.

2. Benefits and limitations of various Investment appraisal techniques.

Lovewell Limited is engaged in food manufacturing business, who wants to purchase a

new machine for improving its overall productivity as well as operational efficiency. Thus,

various Investment appraisal techniques are available for acquiring machine such as payback

period, net present value, accounting rate of return and internal rate of return.

Benefits of Investment appraisal techniques are as follows:

1. Payback period – The term payback period simply defined the time required for

recovering the amount of investment made in the initial period i.e. initial investment. It

evaluates the length of time which is needed so as to recover the cost of an initial investment

(Lin, Chang and Chung, 2015). The longer payback period is not considered desirable for

investment purpose.

Benefits of payback period is as follows:

1. It provides importance of liquidity factor as required for making decision related to

investment proposals.

depicts that it company makes investment in purchasing of new machine than it will be able to

recover the cost involves in purchasing within 3 years and 8 months.

Also, the accounting rate of return of the company is 45.85% which shows that company

will get such percentage amount as the rate of return on purchase of machine.

The net present value of the company is also positive which shows that it will be

favorable for the company to acquire new machine as it will lead to increase in the productivity

as well as profitability of the company thereby improving the performance of the company as a

whole.

When it comes to internal rate of return, Lovewell Limited is having 14.92%. It shows

that company will get 14.92% rate of return when it will make capital investment in acquisition

of new machine.

Thus, it can be said that on purchasing of new machine, Lovewell Limited can recover its

cost in 3.8 year with positive net present value of £23077 having 14.92% and 45.85% as internal

and accounting rate of return respectively.

2. Benefits and limitations of various Investment appraisal techniques.

Lovewell Limited is engaged in food manufacturing business, who wants to purchase a

new machine for improving its overall productivity as well as operational efficiency. Thus,

various Investment appraisal techniques are available for acquiring machine such as payback

period, net present value, accounting rate of return and internal rate of return.

Benefits of Investment appraisal techniques are as follows:

1. Payback period – The term payback period simply defined the time required for

recovering the amount of investment made in the initial period i.e. initial investment. It

evaluates the length of time which is needed so as to recover the cost of an initial investment

(Lin, Chang and Chung, 2015). The longer payback period is not considered desirable for

investment purpose.

Benefits of payback period is as follows:

1. It provides importance of liquidity factor as required for making decision related to

investment proposals.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

2. It mainly focuses on risk. The project having short period is less risky as compared to

longer period.

3. With the help of payback period the decision making process becomes easy related to

investment as lower payback period is considered better for the investment.

4. Pay-back period method is very simple and easy to calculate and also provides ease in

understanding with the help of formula: Pay-back period = Cost of project / Net annual

cash inflows.

Limitations of payback period is as follows:

1. Payback period only emphasizes on liquidity and not on profitability.

2. The most important limitation of payback period is that time value of money is not

recognized for the project.

3. Another limitation of this technique is that it doesn't take into consideration the amount

of cash inflow which is generated after payback period.

2. Accounting Rate of Return – The term accounting rate of return is also known as

Average rate of return which defines the rate of return to be received on investment made

or on purchase of any asset in comparison with the cost incurred for initial investment

(De Villiers, 2015). It helps in determining the investment profitability.

Benefits of Accounting Rate of return:

1. This helps in measuring the profitability level as well as the existing performance

level of the business organization.

2. It is easy to calculate Accounting Rate of Return for different project and investment

with the help of formula:

Accounting Rate of Return = (Average Net Income/Average Investment) x 100

3. It helps in recognizing the earnings after tax and depreciation amount, also known as

the net earnings or income of the business which plays an important role in

investment appraisal.

4. With the help of accounting rate of return, comparison of new project with the cost or

similar competitive project can be made.

Limitation of Accounting Rate of return:

longer period.

3. With the help of payback period the decision making process becomes easy related to

investment as lower payback period is considered better for the investment.

4. Pay-back period method is very simple and easy to calculate and also provides ease in

understanding with the help of formula: Pay-back period = Cost of project / Net annual

cash inflows.

Limitations of payback period is as follows:

1. Payback period only emphasizes on liquidity and not on profitability.

2. The most important limitation of payback period is that time value of money is not

recognized for the project.

3. Another limitation of this technique is that it doesn't take into consideration the amount

of cash inflow which is generated after payback period.

2. Accounting Rate of Return – The term accounting rate of return is also known as

Average rate of return which defines the rate of return to be received on investment made

or on purchase of any asset in comparison with the cost incurred for initial investment

(De Villiers, 2015). It helps in determining the investment profitability.

Benefits of Accounting Rate of return:

1. This helps in measuring the profitability level as well as the existing performance

level of the business organization.

2. It is easy to calculate Accounting Rate of Return for different project and investment

with the help of formula:

Accounting Rate of Return = (Average Net Income/Average Investment) x 100

3. It helps in recognizing the earnings after tax and depreciation amount, also known as

the net earnings or income of the business which plays an important role in

investment appraisal.

4. With the help of accounting rate of return, comparison of new project with the cost or

similar competitive project can be made.

Limitation of Accounting Rate of return:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1. It doesn't consider time factor related to selection of various funds use. Accounting

rate of return doesn't focus on the time value of funds.

2. It doesn't take into consideration the negative impact of external factors on the

profitability level of the business project.

3. When investment is made in form of instalments of two or more at different times,

this method cannot evaluate the worth of project.

3. Net Present Value – It shows the difference between the present value of cash inflow

and present value of cash outflow for a definite period of time (Dash and Motukuri,

2018). Net present value can be used in making investment planning which further helps

in assessing the success or profitability situation of a project or investment.

Benefits of Net present value:

1. It helps in discounting future year cash flow back to the present for ascertaining the worth of

project.

2. With the help of net present value the value related to both shareholders and firm can be

maximize.

3. In project assessment, the profitability factor and risk factor are taken into consideration at

high priority.

Limitations of Net present value:

1. Net present value doesn't provide appropriate calculation of the discount rate as it is difficult

to calculate.

2. Sometimes, net present value doesn't provide the adequate or correct decision making in case

of unequal life of projects.

3. It is of no use when comparison is made between projects having differing investment

amounts.

4. Internal rate of return – It is defined as that rate of interest at which the company's net

present value of all the positive cash flows including the negative, from the investment is

equal to zero amount (Mellichamp, 2017). This investment appraisal technique of

Internal rate of return helps in evaluating or assessing the benefits or profits of a

particular project or investment.

rate of return doesn't focus on the time value of funds.

2. It doesn't take into consideration the negative impact of external factors on the

profitability level of the business project.

3. When investment is made in form of instalments of two or more at different times,

this method cannot evaluate the worth of project.

3. Net Present Value – It shows the difference between the present value of cash inflow

and present value of cash outflow for a definite period of time (Dash and Motukuri,

2018). Net present value can be used in making investment planning which further helps

in assessing the success or profitability situation of a project or investment.

Benefits of Net present value:

1. It helps in discounting future year cash flow back to the present for ascertaining the worth of

project.

2. With the help of net present value the value related to both shareholders and firm can be

maximize.

3. In project assessment, the profitability factor and risk factor are taken into consideration at

high priority.

Limitations of Net present value:

1. Net present value doesn't provide appropriate calculation of the discount rate as it is difficult

to calculate.

2. Sometimes, net present value doesn't provide the adequate or correct decision making in case

of unequal life of projects.

3. It is of no use when comparison is made between projects having differing investment

amounts.

4. Internal rate of return – It is defined as that rate of interest at which the company's net

present value of all the positive cash flows including the negative, from the investment is

equal to zero amount (Mellichamp, 2017). This investment appraisal technique of

Internal rate of return helps in evaluating or assessing the benefits or profits of a

particular project or investment.

Benefits of Internal Rate of return:

1. It can be used when annual cash flow is both even and uneven by considering time

value of money.

2. Internal Rate of Return considers both the total cash inflow and outflows for definite

period of time.

3. It emphasizes on maximization of profit level as well as wealth of the shareholders.

Limitation of Internal Rate of return:

1. It is only concerned with projected cash flows which is created with the help of

injection of capital rather than considering future costs which can affect profit.

2. The most important limitation of this technique is that it doesn't consider the project

size when making comparison between two projects.

3. It compares cash flow of project with project cost only. It doesn't consider factors such

as future costs, duration of project etc.

CONCLUSION

From the above report it can be concluded that financial management is a process which

is concerned with the effective management of financial activities of the business organization.

The report has discussed about the dividend policy of Planet company. It has also shown the

calculation of fair share price of Planet's share with the past four years’ dividends per share

distribution. Further the report has shown the calculation of new share value of planet's share

after the increase in its debt level which has led to increase in Planet’s shareholders price of up to

15.4 per cent return. Also, the report has discussed that how dividend policy is used in valuing

share price. Lovewell Limited, a food manufacturer is thinking of acquiring new machine for

which various investment appraisal techniques such as payback period, accounting rate of return,

net present value and internal rate of return has been calculated to assess the feasibility of

purchasing such machine. The report has discussed the benefits of payback period, accounting

rate of return, net present value and internal rate of return along with their limitations.

1. It can be used when annual cash flow is both even and uneven by considering time

value of money.

2. Internal Rate of Return considers both the total cash inflow and outflows for definite

period of time.

3. It emphasizes on maximization of profit level as well as wealth of the shareholders.

Limitation of Internal Rate of return:

1. It is only concerned with projected cash flows which is created with the help of

injection of capital rather than considering future costs which can affect profit.

2. The most important limitation of this technique is that it doesn't consider the project

size when making comparison between two projects.

3. It compares cash flow of project with project cost only. It doesn't consider factors such

as future costs, duration of project etc.

CONCLUSION

From the above report it can be concluded that financial management is a process which

is concerned with the effective management of financial activities of the business organization.

The report has discussed about the dividend policy of Planet company. It has also shown the

calculation of fair share price of Planet's share with the past four years’ dividends per share

distribution. Further the report has shown the calculation of new share value of planet's share

after the increase in its debt level which has led to increase in Planet’s shareholders price of up to

15.4 per cent return. Also, the report has discussed that how dividend policy is used in valuing

share price. Lovewell Limited, a food manufacturer is thinking of acquiring new machine for

which various investment appraisal techniques such as payback period, accounting rate of return,

net present value and internal rate of return has been calculated to assess the feasibility of

purchasing such machine. The report has discussed the benefits of payback period, accounting

rate of return, net present value and internal rate of return along with their limitations.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.