Financial Management Report: Fortescue Metals Group Analysis

VerifiedAdded on 2021/05/31

|23

|2601

|23

Report

AI Summary

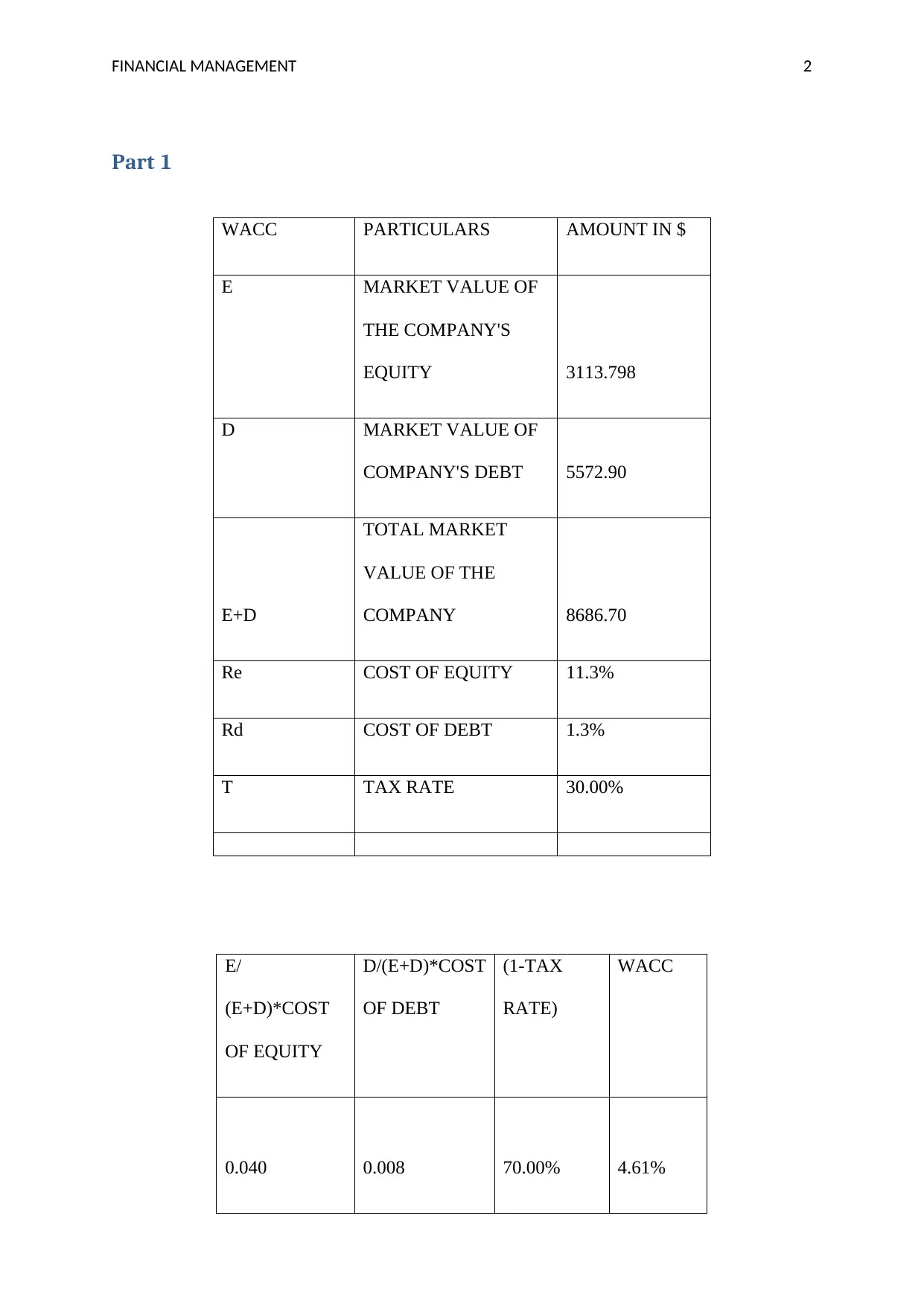

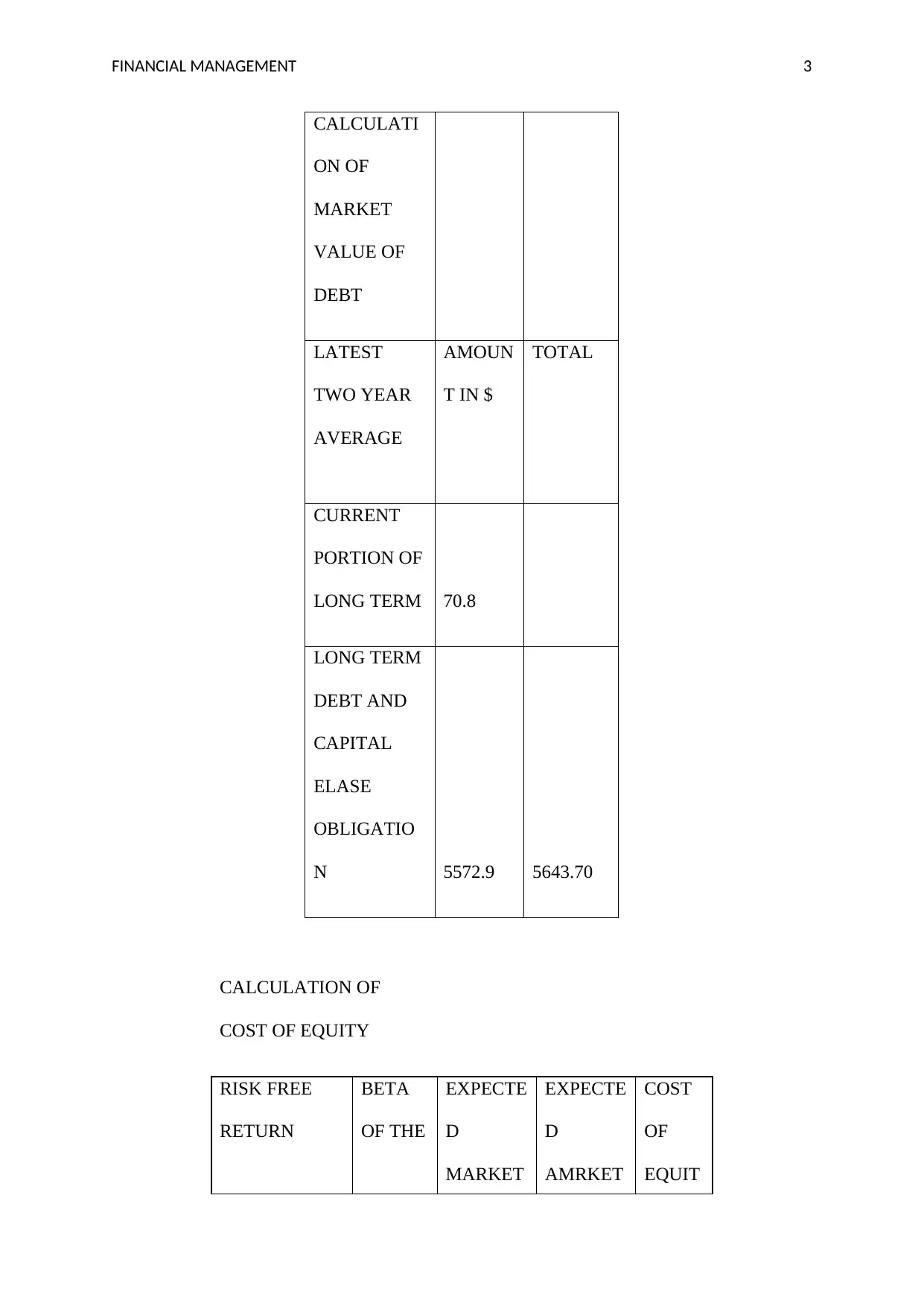

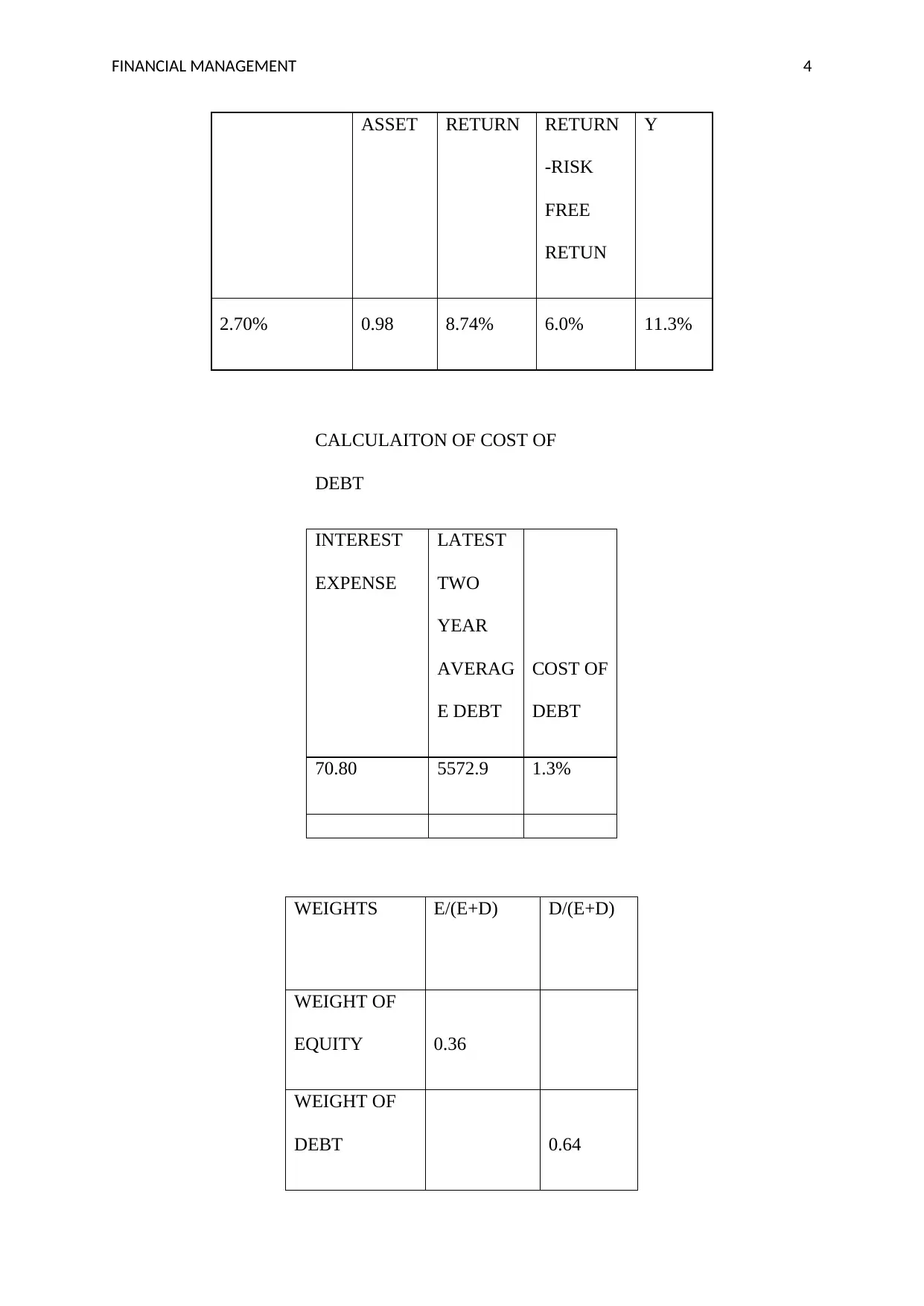

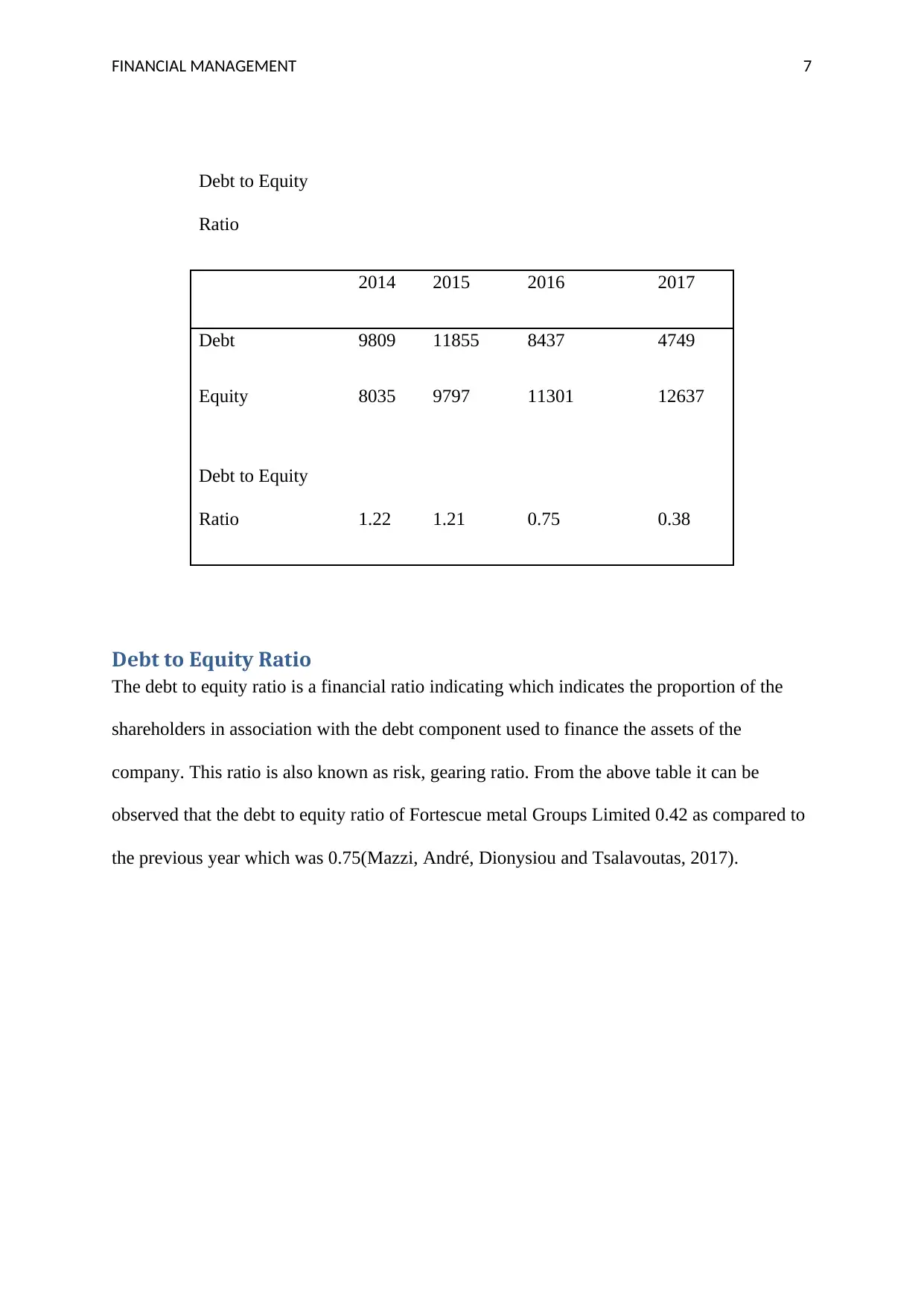

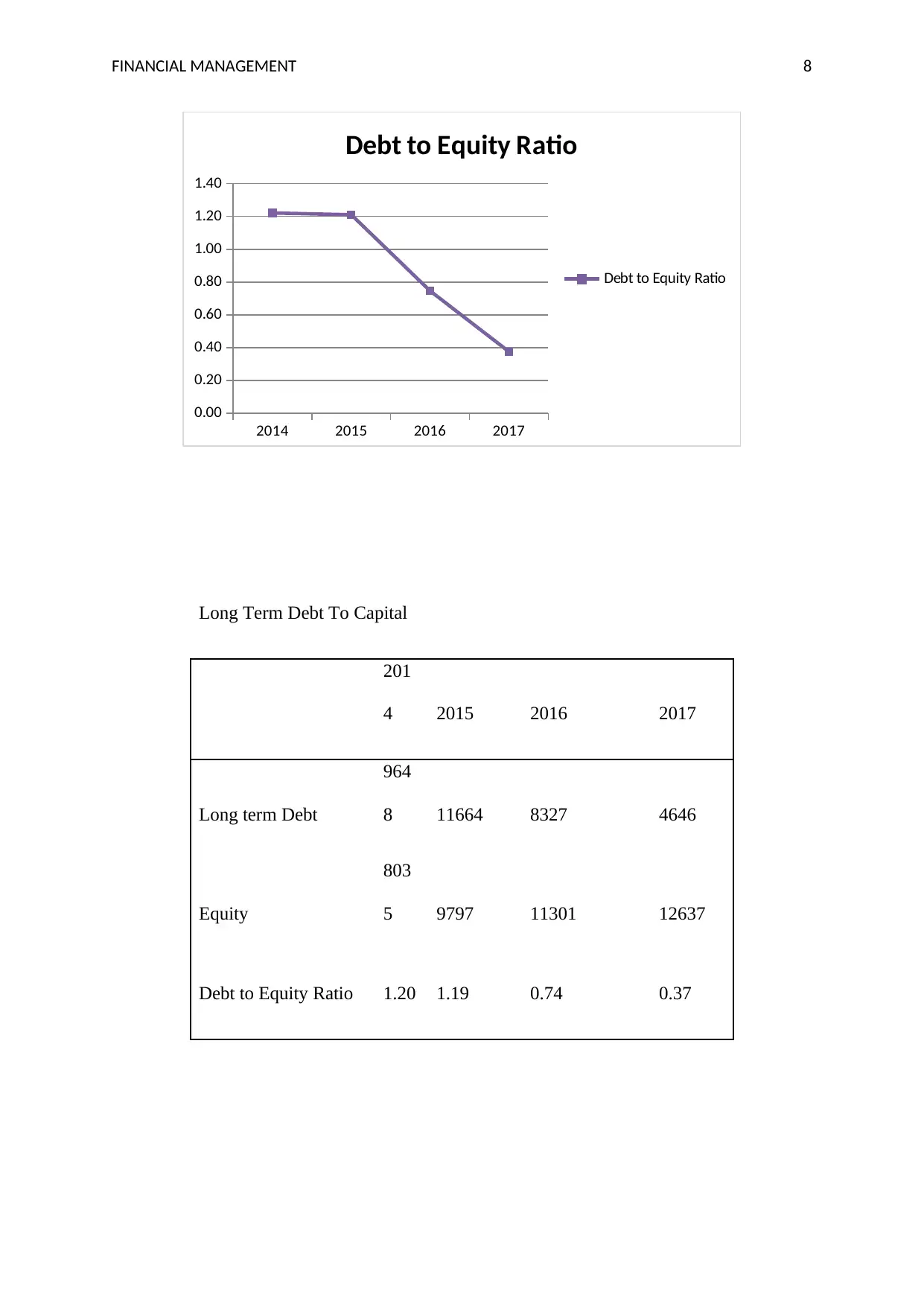

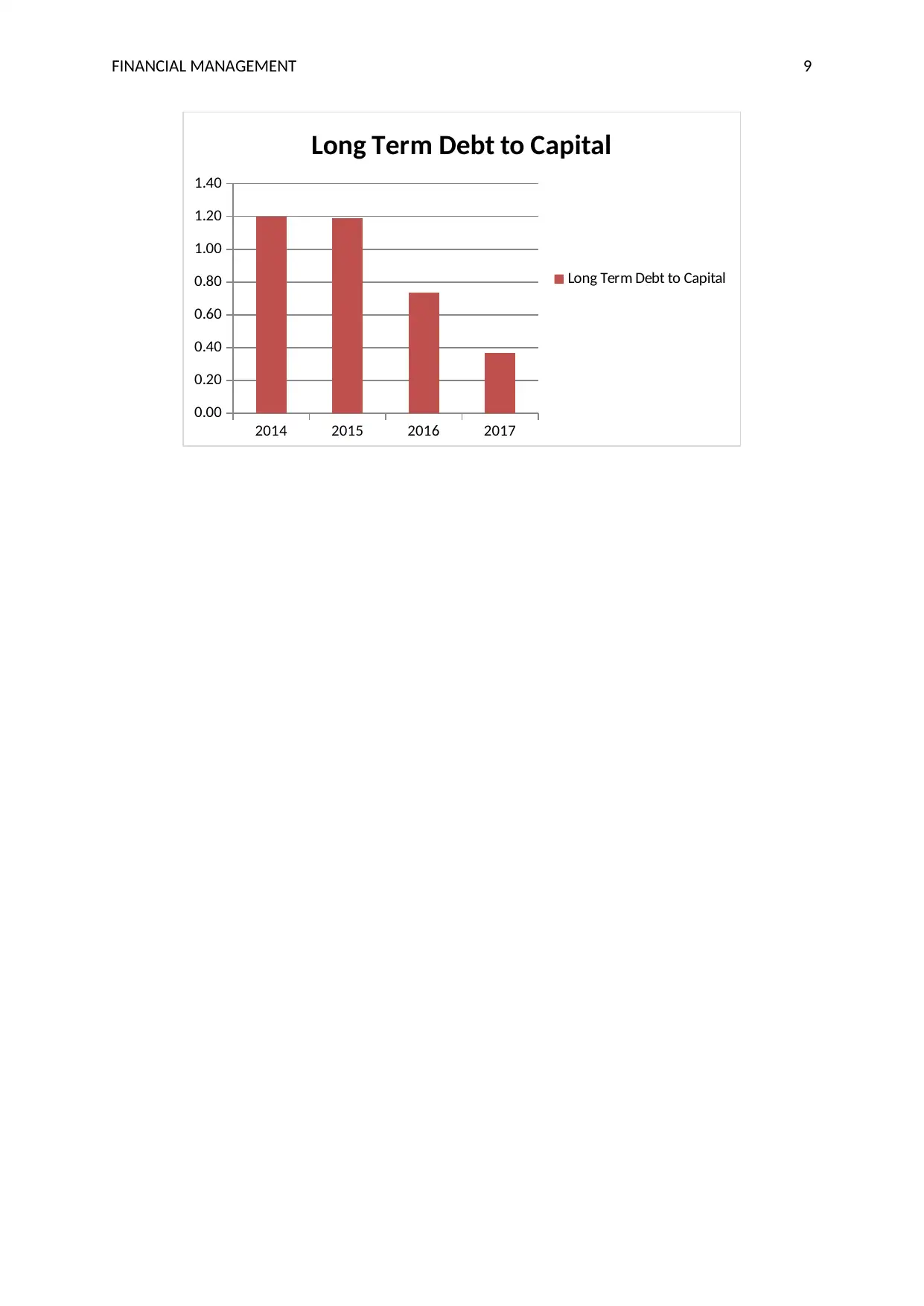

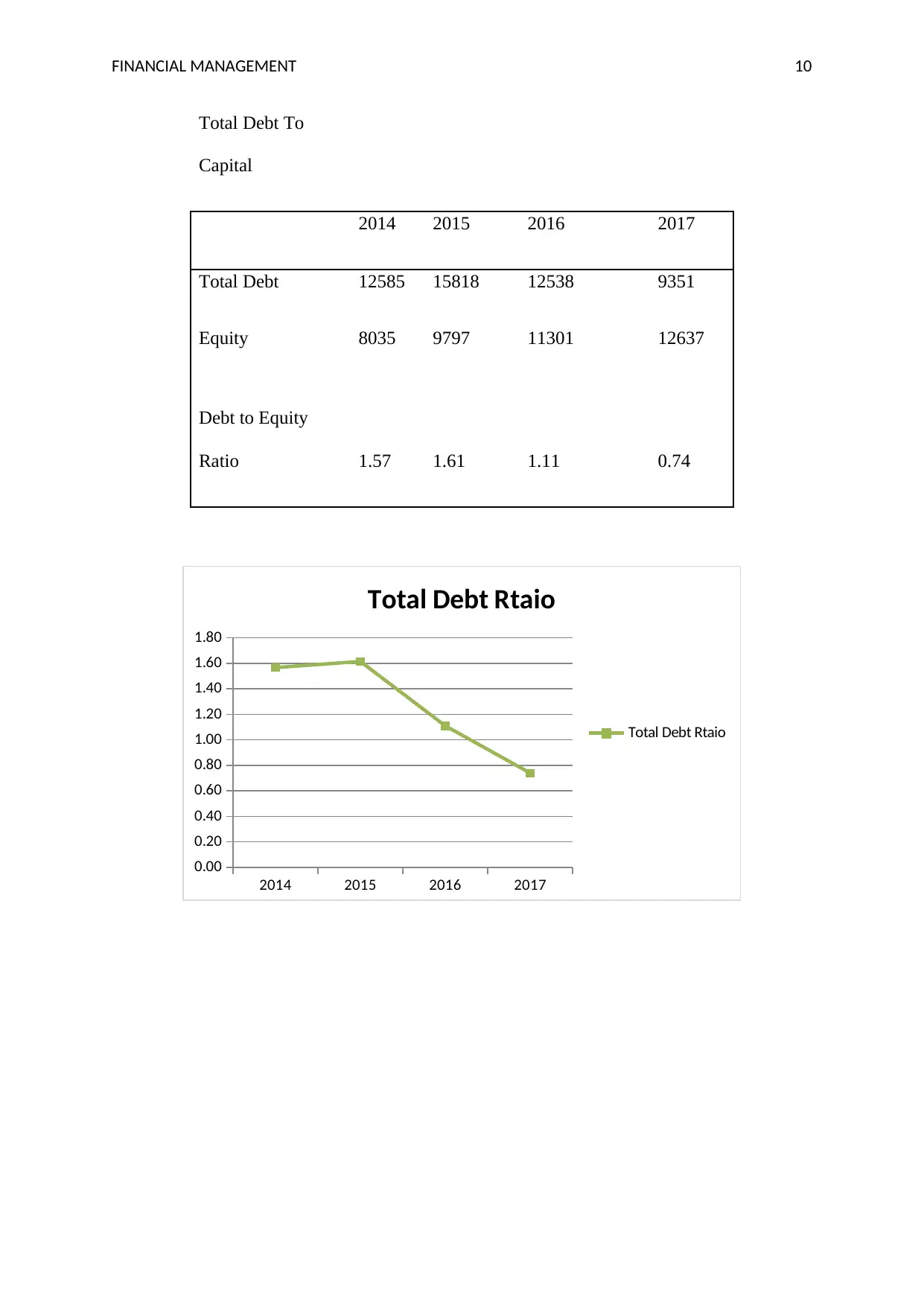

This report provides a comprehensive financial analysis of Fortescue Metals Group (FMG), covering key aspects of financial management. It begins with the calculation of the Weighted Average Cost of Capital (WACC), detailing the market value of equity and debt, cost of equity and debt, and tax rate to determine the overall WACC. The report then delves into capital structure ratios, including debt-to-equity ratios, long-term debt to capital, and total debt to capital, analyzing trends from 2014 to 2017. Working capital management policies and investment policies, particularly FMG's liberal approach, are discussed. Profitability ratios, such as net profit ratio and return on equity, are examined to assess the company's performance. The report also explores dividend distribution policies, including dividend equations, tax systems in Australia (franked and un-franked dividends), and dividend reinvestment plans. Finally, the report incorporates price-earnings ratios and provides relevant references to support the analysis.

1 out of 23

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.