Financial Analysis Report: Supplier Evaluation and Recommendations

VerifiedAdded on 2020/02/03

|15

|4299

|100

Report

AI Summary

This report provides a comprehensive financial analysis of a supplier, evaluating their financial performance to determine their suitability for a sourcing exercise for Facilities Management Services. The analysis includes an examination of profitability, liquidity, and solvency ratios, comparing data from 2013 and 2014. The report highlights the supplier's strengths, such as improved profitability and a low gearing ratio, indicating a stable financial position. Weaknesses, including poor performance in 2013 and low liquidity, are also discussed. The report uses Kraljic’s matrix for supplier evaluation and provides recommendations on whether to consider the organization for the sourcing exercise. The report also covers the purchasing process, including specification of needs, contract terms, supplier identification, and evaluation. The findings suggest that while the supplier has shown improvement, the client should exercise caution and consider further due diligence before making a final decision. The report concludes with a justified recommendation based on the financial analysis.

Financial management

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION ..........................................................................................................................1

a) Evaluate the finances of this organisation highlighting the strengths and weaknesses of their

position........................................................................................................................................1

b) Provide a justified recommendation as to whether you would consider this organisation for

a sourcing

exercise for Facilities Management Services.............................................................................6

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................10

INTRODUCTION ..........................................................................................................................1

a) Evaluate the finances of this organisation highlighting the strengths and weaknesses of their

position........................................................................................................................................1

b) Provide a justified recommendation as to whether you would consider this organisation for

a sourcing

exercise for Facilities Management Services.............................................................................6

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................10

Illustration Index

Illustration 1: Kraljic’s matrix for suppliers evaluation...................................................................2

Illustration 1: Kraljic’s matrix for suppliers evaluation...................................................................2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Index of Tables

Table 1: Financial ratios of the supplier..........................................................................................3

Table 2: Performance of the supplier...............................................................................................7

Table 1: Financial ratios of the supplier..........................................................................................3

Table 2: Performance of the supplier...............................................................................................7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTRODUCTION

Financial management is a specialized function which is carried by the top management.

It involves efficient use of funds to accomplish the goal of the organisation. It focusses on

planning, allocating, organising and utilization of funds. It ensure that the financial resources are

utilized in an efficient manner (How to evaluate potential buyers, 2012). All the investment,

financial and dividends decisions are taken after proper evaluation and analysis. The report

focusses on the evaluation of the financial statement, technical and commercial capabilities of an

organisation. Furthermore, the use of ratio analysis for the evaluation of potential suppliers is

also been included in the report.

a) Evaluate the finances of this organisation highlighting the strengths and weaknesses of their

position.

Purchasing is the an important element for a company. It is a highly complex procedure

and it takes into consideration the performance of the suppliers before choosing him. There are

five major sections in which the entire process can be divided (Cheung. and et.al., 2014). It

includes supply continuity, developing supply base management, alignment of stakeholders,

management of sourcing process and integration of purchasing strategies into the goals of the

organisation (Kiondo, 2004). The basic procurement process includes:

Specification of the needs: Initially a company as to identify the needs of the organisation

(Krishnamurthy and Vissing-Jorgensen, 2013). The needs can be products, services or a

specific function of the organisation. The company has to decide whether they will make

the product or purchase it from others.

Development of contract terms: Then all the terms and conditions including the cost,

quality, quantity, delivery and technological capabilities are developed (Krzysko. and

Marciniak, 2001).

Identification of potential suppliers: The next step is to identify the type of supplier that is

needed by the company. It can be from a single source or multiple sources, short term or

long term contracts, domestic or foreign suppliers etc (Lavoori and Paramanik, 2014).

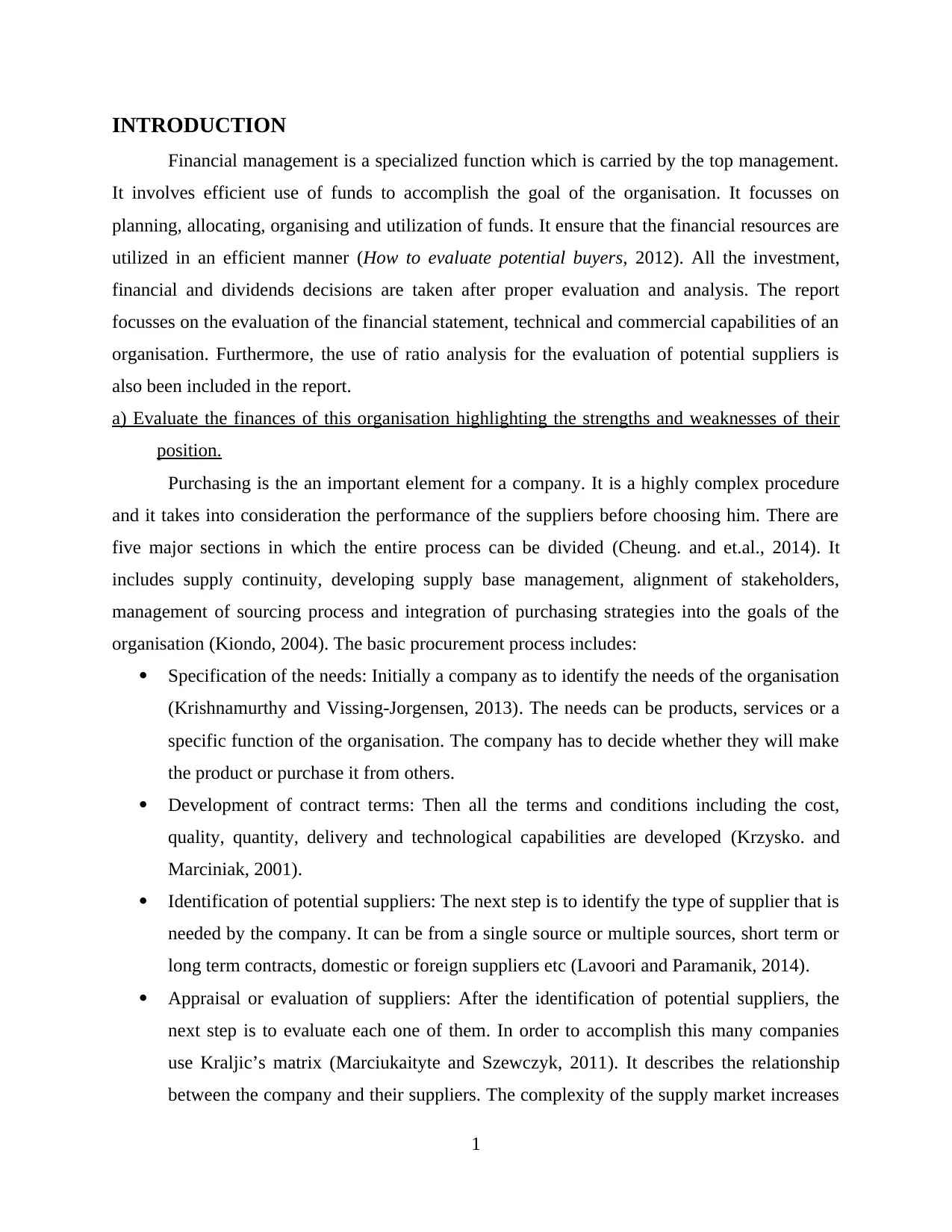

Appraisal or evaluation of suppliers: After the identification of potential suppliers, the

next step is to evaluate each one of them. In order to accomplish this many companies

use Kraljic’s matrix (Marciukaityte and Szewczyk, 2011). It describes the relationship

between the company and their suppliers. The complexity of the supply market increases

1

Financial management is a specialized function which is carried by the top management.

It involves efficient use of funds to accomplish the goal of the organisation. It focusses on

planning, allocating, organising and utilization of funds. It ensure that the financial resources are

utilized in an efficient manner (How to evaluate potential buyers, 2012). All the investment,

financial and dividends decisions are taken after proper evaluation and analysis. The report

focusses on the evaluation of the financial statement, technical and commercial capabilities of an

organisation. Furthermore, the use of ratio analysis for the evaluation of potential suppliers is

also been included in the report.

a) Evaluate the finances of this organisation highlighting the strengths and weaknesses of their

position.

Purchasing is the an important element for a company. It is a highly complex procedure

and it takes into consideration the performance of the suppliers before choosing him. There are

five major sections in which the entire process can be divided (Cheung. and et.al., 2014). It

includes supply continuity, developing supply base management, alignment of stakeholders,

management of sourcing process and integration of purchasing strategies into the goals of the

organisation (Kiondo, 2004). The basic procurement process includes:

Specification of the needs: Initially a company as to identify the needs of the organisation

(Krishnamurthy and Vissing-Jorgensen, 2013). The needs can be products, services or a

specific function of the organisation. The company has to decide whether they will make

the product or purchase it from others.

Development of contract terms: Then all the terms and conditions including the cost,

quality, quantity, delivery and technological capabilities are developed (Krzysko. and

Marciniak, 2001).

Identification of potential suppliers: The next step is to identify the type of supplier that is

needed by the company. It can be from a single source or multiple sources, short term or

long term contracts, domestic or foreign suppliers etc (Lavoori and Paramanik, 2014).

Appraisal or evaluation of suppliers: After the identification of potential suppliers, the

next step is to evaluate each one of them. In order to accomplish this many companies

use Kraljic’s matrix (Marciukaityte and Szewczyk, 2011). It describes the relationship

between the company and their suppliers. The complexity of the supply market increases

1

if the goods are from strategic items. There are many ways which can be used to evaluate

the financial health of the supplier (Maxwell, Ogden and McTavish, 2007). If the contract

is of high amount then it becomes necessary to involve financial analysis in the

evaluation stage. It will ensure that the suppliers maintain the quality of the goods and

continue the delivery of the goods.

Financial ratio

Financial ratio analyses can be an effective way to determine the the capabilities of the

supplier. It will allow the company to find out the profitability, efficiency, liquidity and solvency

of the supplier. It can be used to analyse the overall performance of the supplier. It will allow the

company to make decisions about the future (Murphy, 2001). It gives insights about the

efficiency of the management. It ensure that the supplier continue to supply the products over the

given time frame. The ratio which can be used for evaluation of supplier are:

Profitability ratios: It measures the performance and the capacity of the company to

make profits (Ryan, 2009). It is useful method to calculate the revenues and profits of suppliers.

It will ensure that the supplier is making enough operational profits to continue its business.

Liquidity ratios: It measures the liquidity position of the company. It gives essential

details about the ability of the supplier to meet its short term obligations. The suppliers are not

2

Ill

ustration 1: Kraljic’s matrix for suppliers evaluation

(Source: The purchasing process, 2014)

the financial health of the supplier (Maxwell, Ogden and McTavish, 2007). If the contract

is of high amount then it becomes necessary to involve financial analysis in the

evaluation stage. It will ensure that the suppliers maintain the quality of the goods and

continue the delivery of the goods.

Financial ratio

Financial ratio analyses can be an effective way to determine the the capabilities of the

supplier. It will allow the company to find out the profitability, efficiency, liquidity and solvency

of the supplier. It can be used to analyse the overall performance of the supplier. It will allow the

company to make decisions about the future (Murphy, 2001). It gives insights about the

efficiency of the management. It ensure that the supplier continue to supply the products over the

given time frame. The ratio which can be used for evaluation of supplier are:

Profitability ratios: It measures the performance and the capacity of the company to

make profits (Ryan, 2009). It is useful method to calculate the revenues and profits of suppliers.

It will ensure that the supplier is making enough operational profits to continue its business.

Liquidity ratios: It measures the liquidity position of the company. It gives essential

details about the ability of the supplier to meet its short term obligations. The suppliers are not

2

Ill

ustration 1: Kraljic’s matrix for suppliers evaluation

(Source: The purchasing process, 2014)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

required to pay anything to the company but it affects the sustainability of the company (Seiver,

Haddad and Do, 2014).

Gearing ratios: It calculates the solvency position of the company. It takes into

consideration debts and equity of the company (Shea, 2000). It gives details about the financial

leverage of the suppliers and the risk in his business.

Investment: It measures the profitability of shareholder's funds and the Price to Earning

(PE) ratios of the suppliers (Smit and Trigeorgis, 2012).

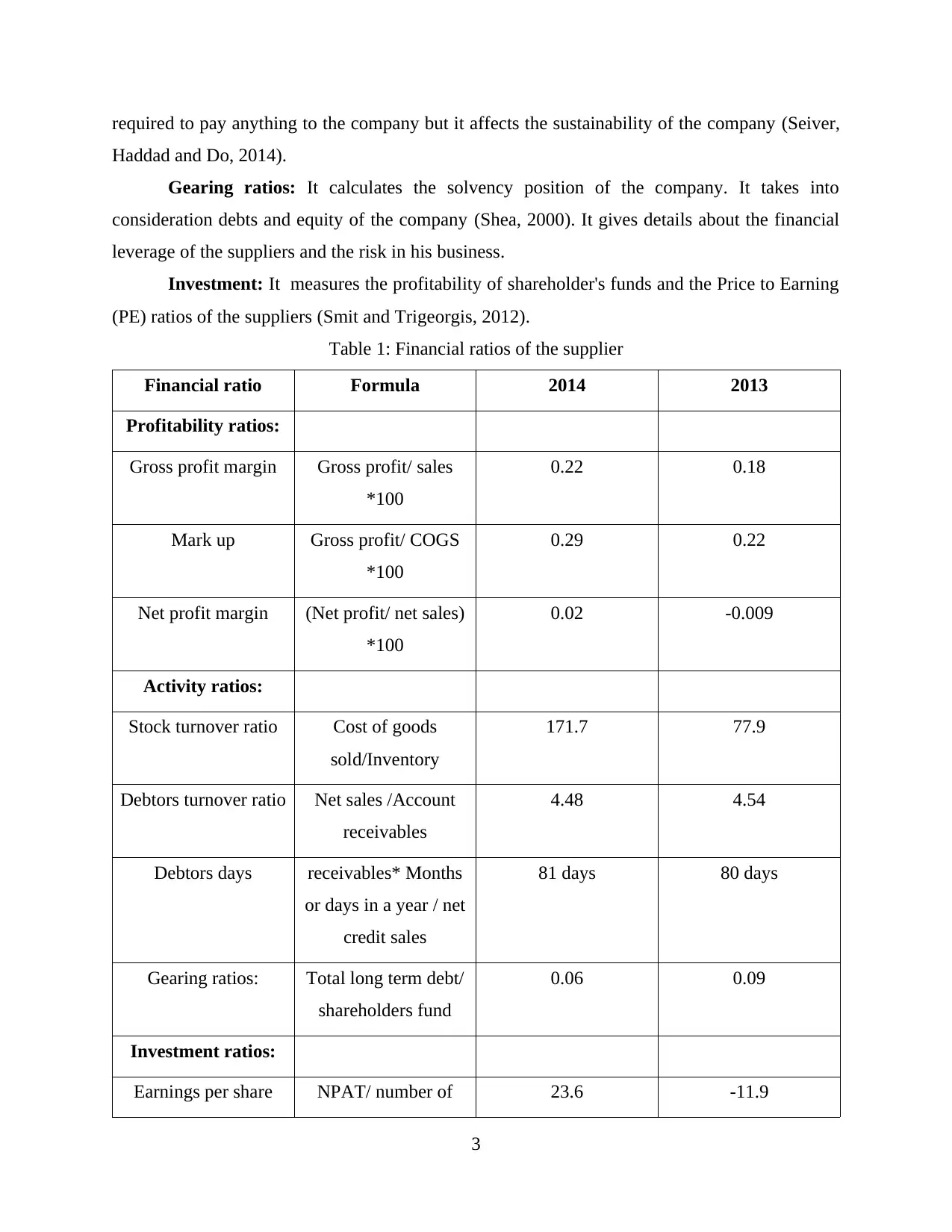

Table 1: Financial ratios of the supplier

Financial ratio Formula 2014 2013

Profitability ratios:

Gross profit margin Gross profit/ sales

*100

0.22 0.18

Mark up Gross profit/ COGS

*100

0.29 0.22

Net profit margin (Net profit/ net sales)

*100

0.02 -0.009

Activity ratios:

Stock turnover ratio Cost of goods

sold/Inventory

171.7 77.9

Debtors turnover ratio Net sales /Account

receivables

4.48 4.54

Debtors days receivables* Months

or days in a year / net

credit sales

81 days 80 days

Gearing ratios: Total long term debt/

shareholders fund

0.06 0.09

Investment ratios:

Earnings per share NPAT/ number of 23.6 -11.9

3

Haddad and Do, 2014).

Gearing ratios: It calculates the solvency position of the company. It takes into

consideration debts and equity of the company (Shea, 2000). It gives details about the financial

leverage of the suppliers and the risk in his business.

Investment: It measures the profitability of shareholder's funds and the Price to Earning

(PE) ratios of the suppliers (Smit and Trigeorgis, 2012).

Table 1: Financial ratios of the supplier

Financial ratio Formula 2014 2013

Profitability ratios:

Gross profit margin Gross profit/ sales

*100

0.22 0.18

Mark up Gross profit/ COGS

*100

0.29 0.22

Net profit margin (Net profit/ net sales)

*100

0.02 -0.009

Activity ratios:

Stock turnover ratio Cost of goods

sold/Inventory

171.7 77.9

Debtors turnover ratio Net sales /Account

receivables

4.48 4.54

Debtors days receivables* Months

or days in a year / net

credit sales

81 days 80 days

Gearing ratios: Total long term debt/

shareholders fund

0.06 0.09

Investment ratios:

Earnings per share NPAT/ number of 23.6 -11.9

3

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

(EPS) equity shares

Profitability:

Current ratio Current assets/ current

liabilities

1.12 1.10

Quick ratio Liquid assets/ current

liabilities

1.10 1.06

It can be seen from the above table that the gross profit margin of the supplier was 0.18 in

2013 which gone up to 0.22 in the year 2014. It shows that the company has improved their

profits from the last year. Their mark up cost has also improved from 0.22 in 2013 to 0.29 in the

year 2014. The supplier has improved their profitability and this is a good sign for the client.

Their Net profits have gone up from -0.009 to 0.02 in 2004 (Sofat and Hiro, 2011). The supplier

was making losses in the last year but in 2014 they have shown good performance. It can be seen

from the profitability ratios that the supplier has done significantly well in increasing their

profitability. The Stock turnover ratio of the supplier was 77.9 which has increased to 171.7 in

2004. Higher Stock turnover ratio implies that the company has been performing well and their

sales have increased (Srinivasan, 2012). Their Debtors turnover ratio has decreased from the last

year. It means that the suppliers take 80 days to collect the receivables. It will help the client to

get the goods on credit from the supplier. The gearing ratio of the supplier in 0.06 in 2014 and it

was 0.09 in 2013. Low debt turnover ratio is good for the company (Tugas, 2012). It means that

the supplier has less long term obligations. Furthermore, it gives an idea about the solvency

position of the company. The company of supplier if funded by the shareholders rather than the

lenders. Their leverage is also very low which is a good sign for the client (Weaver and Weston,

2007).

Investment ratios shows how much money will an investor get from the company. The

EPS of the supplier was -11.9 which was not favourable. It cannot be considered a good

company for an investor (Weygandt and et. al., 2009). But in the year the supplier has been able

to improve their EPS to 23.6. It manes for every $100 an investor would get $123.6. He will

receive the profit of $23.6 over the money invested. Current and quick ratio measures the

liquidity of the company. Is shows the ability of a company to pay of its short term obligations.

The ideal current ratio is 2:1 while the ideal quick ratio is 1:1. The current ratio of the supplier

4

Profitability:

Current ratio Current assets/ current

liabilities

1.12 1.10

Quick ratio Liquid assets/ current

liabilities

1.10 1.06

It can be seen from the above table that the gross profit margin of the supplier was 0.18 in

2013 which gone up to 0.22 in the year 2014. It shows that the company has improved their

profits from the last year. Their mark up cost has also improved from 0.22 in 2013 to 0.29 in the

year 2014. The supplier has improved their profitability and this is a good sign for the client.

Their Net profits have gone up from -0.009 to 0.02 in 2004 (Sofat and Hiro, 2011). The supplier

was making losses in the last year but in 2014 they have shown good performance. It can be seen

from the profitability ratios that the supplier has done significantly well in increasing their

profitability. The Stock turnover ratio of the supplier was 77.9 which has increased to 171.7 in

2004. Higher Stock turnover ratio implies that the company has been performing well and their

sales have increased (Srinivasan, 2012). Their Debtors turnover ratio has decreased from the last

year. It means that the suppliers take 80 days to collect the receivables. It will help the client to

get the goods on credit from the supplier. The gearing ratio of the supplier in 0.06 in 2014 and it

was 0.09 in 2013. Low debt turnover ratio is good for the company (Tugas, 2012). It means that

the supplier has less long term obligations. Furthermore, it gives an idea about the solvency

position of the company. The company of supplier if funded by the shareholders rather than the

lenders. Their leverage is also very low which is a good sign for the client (Weaver and Weston,

2007).

Investment ratios shows how much money will an investor get from the company. The

EPS of the supplier was -11.9 which was not favourable. It cannot be considered a good

company for an investor (Weygandt and et. al., 2009). But in the year the supplier has been able

to improve their EPS to 23.6. It manes for every $100 an investor would get $123.6. He will

receive the profit of $23.6 over the money invested. Current and quick ratio measures the

liquidity of the company. Is shows the ability of a company to pay of its short term obligations.

The ideal current ratio is 2:1 while the ideal quick ratio is 1:1. The current ratio of the supplier

4

was 1.10 in 2013 which increased to 1.12 in 2014. The supplier has improved its liquidity

position from the last year (Weaver and Weston, 2007). Their quick ratio has also improved from

the last year. Both the liquidity ratio have improved but it can be seen from the table that they

have less stock in the inventory. They have more cash and other marketable securities which has

improved their liquidity. It is important for the client to ensure that the supplier maintain more

inventory and improves their current ratios. It will allow them to fulfil the requirements of the

client. But still, their liquidity position has been good and the supplier can be considered for the

procurement of goods.

Invitation of tenders: Tenders are price quotations in which large number of suppliers

take part. Tenders have a particular deadline in which the suppliers can bid for the

agreement (Zohra and et.al., 2015).

Analysis of quotations: After obtaining all the tender, the company compares the

quotations ans select the most appropriate from them.

Negotiation: The company negotiates with the suppliers about the terms and conditions

mentioned in the tender (The purchasing process, 2014).

Monitoring the performance: It is important for the company to measure the performance

of the supplier because the performance of the supplier also affect their own profitability.

Strengths of the supplier

The supplier has been able to recover from the losses of last year. This shows that the

company has great potential to grow their business. Their profit margins and mark up has

improved significantly. They have increased their fixed assets and debtors from the last year. The

company has managed to cut down their expenses and improve their efficiency. They have the

resources to meet their obligations in future (How to evaluate potential buyers, 2012). The best

of the supplier is that their business is funded from the equity shares and not the debts. It reduces

their leverage and risk of the business. There is no obligation of the company to pay off interest

rate irrespective of losses. Even the supplier can meet the growing demands of the raw material

of the client (Supplier evaluation and selection, 2007). They can easily take loans from the

external parties because their gearing ratio is very low. It is a favourable situation and the suppler

can be chosen on the basis of its financial performance.

Weaknesses of the supplier

5

position from the last year (Weaver and Weston, 2007). Their quick ratio has also improved from

the last year. Both the liquidity ratio have improved but it can be seen from the table that they

have less stock in the inventory. They have more cash and other marketable securities which has

improved their liquidity. It is important for the client to ensure that the supplier maintain more

inventory and improves their current ratios. It will allow them to fulfil the requirements of the

client. But still, their liquidity position has been good and the supplier can be considered for the

procurement of goods.

Invitation of tenders: Tenders are price quotations in which large number of suppliers

take part. Tenders have a particular deadline in which the suppliers can bid for the

agreement (Zohra and et.al., 2015).

Analysis of quotations: After obtaining all the tender, the company compares the

quotations ans select the most appropriate from them.

Negotiation: The company negotiates with the suppliers about the terms and conditions

mentioned in the tender (The purchasing process, 2014).

Monitoring the performance: It is important for the company to measure the performance

of the supplier because the performance of the supplier also affect their own profitability.

Strengths of the supplier

The supplier has been able to recover from the losses of last year. This shows that the

company has great potential to grow their business. Their profit margins and mark up has

improved significantly. They have increased their fixed assets and debtors from the last year. The

company has managed to cut down their expenses and improve their efficiency. They have the

resources to meet their obligations in future (How to evaluate potential buyers, 2012). The best

of the supplier is that their business is funded from the equity shares and not the debts. It reduces

their leverage and risk of the business. There is no obligation of the company to pay off interest

rate irrespective of losses. Even the supplier can meet the growing demands of the raw material

of the client (Supplier evaluation and selection, 2007). They can easily take loans from the

external parties because their gearing ratio is very low. It is a favourable situation and the suppler

can be chosen on the basis of its financial performance.

Weaknesses of the supplier

5

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The biggest problem in the ratio analysis of the supplier is that they have not performed

well in 2013. Their performance has been very low and it cannot be overlooked. Though the

company has significantly improved in the next year but the client has to remain cautious about

this (Seiver, Haddad and Do, 2014). The client has analyse the data of 3-5 years to see if the

supplier as been stable or not. Furthermore, Their liquidity ratios are low and they have less

investment in the goods. It has to be improved but the supplier because it projects that the

supplier won't be able to meet the demands of the client. They have more investment in the liquid

assets and mostly in cash. They have to invest the excess in their business and manage it

properly. If the supplier can improve all these aspects of their business then they can be a

profitable investment for the client (Maxwell, Ogden and McTavish, 2007). They can go ahead

with the sourcing exercise for Facilities management Services. Furthermore, they can check the

ratings of the supplier from any authentic credit agencies which can be helpful for them to find

out their credit position.

b) Provide a justified recommendation as to whether you would consider this organisation for a

sourcing

exercise for Facilities Management Services

The above analysis shows that the supplier can be chosen for the sourcing

exercise for Facilities Management Services. They have performed exceptionally in 2014 and

their growth rate is high (Krishnamurthy and Vissing-Jorgensen, 2013). The liquidity and

solvency position if the supplier is also good. It would be beneficial for the client to choose the

company as it has shown improvements in their business. Furthermore, the supplier is also

capable to meet the demands of the client in the future. Some of the financial information which

justifies the selection of the supplier are :

Balance Sheet

Balance sheet shows the summary of the financial performance of a company. The

supplier has good amount of fixed assets in the company. Their total assets have also increased

from the last year even though the company was in losses (Kiondo, 2004). They have also kept

funds for the future uncertainty which reduce the risk of the business. They have funds for tax,

pension and lease on the property. The supplier has also paid off its hire purchase amount. The

balance sheet also shows that their is less external funds in the company. Most of the business

activities are funded with the equity. It reduces the risk and leverage of the company. In future

6

well in 2013. Their performance has been very low and it cannot be overlooked. Though the

company has significantly improved in the next year but the client has to remain cautious about

this (Seiver, Haddad and Do, 2014). The client has analyse the data of 3-5 years to see if the

supplier as been stable or not. Furthermore, Their liquidity ratios are low and they have less

investment in the goods. It has to be improved but the supplier because it projects that the

supplier won't be able to meet the demands of the client. They have more investment in the liquid

assets and mostly in cash. They have to invest the excess in their business and manage it

properly. If the supplier can improve all these aspects of their business then they can be a

profitable investment for the client (Maxwell, Ogden and McTavish, 2007). They can go ahead

with the sourcing exercise for Facilities management Services. Furthermore, they can check the

ratings of the supplier from any authentic credit agencies which can be helpful for them to find

out their credit position.

b) Provide a justified recommendation as to whether you would consider this organisation for a

sourcing

exercise for Facilities Management Services

The above analysis shows that the supplier can be chosen for the sourcing

exercise for Facilities Management Services. They have performed exceptionally in 2014 and

their growth rate is high (Krishnamurthy and Vissing-Jorgensen, 2013). The liquidity and

solvency position if the supplier is also good. It would be beneficial for the client to choose the

company as it has shown improvements in their business. Furthermore, the supplier is also

capable to meet the demands of the client in the future. Some of the financial information which

justifies the selection of the supplier are :

Balance Sheet

Balance sheet shows the summary of the financial performance of a company. The

supplier has good amount of fixed assets in the company. Their total assets have also increased

from the last year even though the company was in losses (Kiondo, 2004). They have also kept

funds for the future uncertainty which reduce the risk of the business. They have funds for tax,

pension and lease on the property. The supplier has also paid off its hire purchase amount. The

balance sheet also shows that their is less external funds in the company. Most of the business

activities are funded with the equity. It reduces the risk and leverage of the company. In future

6

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

they can take loans from the bank to expand or grow their business (Krzysko. and Marciniak,

2001). Supplier has shown good performance in the year 2014 and it can be chosen for the

sourcing

exercise for Facilities Management Services.

Profit and loss statement

Profit and loss statement shows the profit and expenses of the business for a given period

of time. The performance of supplier in 2013 has been very disappointing but it has shown

significant growth in 2014. Their sales have increased from 138 million to 161.4 million. Their

gross and net profits have also increased. The company has been able to cut down their operating

expenses and it has improved their revenues. The best thing about the supplier is that they have

become efficient and their profitable (Maxwell, Ogden and McTavish, 2007). Their tax on

ordinary activities has reduced their profits and the supplier has to take this into consideration.

There are no external debts of the company so they are not required to pay any interest. Interest

payments reduce the profitability of the company. It furthermore creates burden on the

organisation as they have be to paid no matter if there are losses in the business.

Cash flow statements

The client can also make use of cash flow statement so understand the flow of cash (Smit

and Trigeorgis, 2012). It has three major activities which are financing, investment and dividend

decisions.

Performance of the supplier

Table 2: Performance of the supplier

Financial ratio Performance

Liquidity ratios Poor

Activity ratios Good

Gearing ratios Very good

Investment ratios Very good

It can be seen from the table that the supplier has performed well. They have maintained

high level of efficiency in the company which will also benefit the client. It will reduce the cost

of the product for the client as well. Both the companies will be benefited from it. Their gearing

and investment ratio has also been good (Weaver and Weston, 2007). It means that the supplier

7

2001). Supplier has shown good performance in the year 2014 and it can be chosen for the

sourcing

exercise for Facilities Management Services.

Profit and loss statement

Profit and loss statement shows the profit and expenses of the business for a given period

of time. The performance of supplier in 2013 has been very disappointing but it has shown

significant growth in 2014. Their sales have increased from 138 million to 161.4 million. Their

gross and net profits have also increased. The company has been able to cut down their operating

expenses and it has improved their revenues. The best thing about the supplier is that they have

become efficient and their profitable (Maxwell, Ogden and McTavish, 2007). Their tax on

ordinary activities has reduced their profits and the supplier has to take this into consideration.

There are no external debts of the company so they are not required to pay any interest. Interest

payments reduce the profitability of the company. It furthermore creates burden on the

organisation as they have be to paid no matter if there are losses in the business.

Cash flow statements

The client can also make use of cash flow statement so understand the flow of cash (Smit

and Trigeorgis, 2012). It has three major activities which are financing, investment and dividend

decisions.

Performance of the supplier

Table 2: Performance of the supplier

Financial ratio Performance

Liquidity ratios Poor

Activity ratios Good

Gearing ratios Very good

Investment ratios Very good

It can be seen from the table that the supplier has performed well. They have maintained

high level of efficiency in the company which will also benefit the client. It will reduce the cost

of the product for the client as well. Both the companies will be benefited from it. Their gearing

and investment ratio has also been good (Weaver and Weston, 2007). It means that the supplier

7

has great potentate to growth in the future and it has enough funds to pay off its debts. Supplier

has maintained its solvency and liquidity position. The biggest weakness for the supplier is that

they have less investment in the goods. Their lot of funds are in the form of cash which is lying

idle in the business. They need to find a way and use the extra cash in the business.

Recommendations for the company

The client should analyse other factors apart from the financial statements of the supplier.

It will ensure that they have selected the right company for the sourcing

exercise for Facilities Management Services. It will benefit them in short run as well in the

future. Some of the recommendations for the company are as follows:

Altman Z score: The client can use the formula of Altman Z score for the evaluation and

appraisal of the supplier. It helps to find out the solvency position of the company. It takes into

consideration liquid assets, earning power, operating efficiency, leverage, market dimensions ans

asset turnover ratios of the industry (The purchasing process, 2014). The supplier should have

total points +4.48 which indicates stability of the company. On the other hand, -0.25 points

indicates insolvency. The formula for Altman Z score is as follows:

Z= 1.2T1 + 1.4T2 + 3.3T3 + 0.6T4 + 0.99T5

Scoring criteria: The scoring criteria has range of questions which helps in the appraisal

of the potential supplier. The purchaser or the client can include all the aspects of his business

and use it to evaluate the performance of the supplier (Supplier evaluation and selection, 2007).

A scoring criteria includes QA system, track record, employment policy, environmental systems,

financial stability and technical capacity of the supplier. It will ensure that all the criteria are

fulfilled by the potential supplier.

Suppliers surveys: It helps the client to gather the information about the supplier. It

includes referrals, surveys, questionnaires, Profit and loss history, defect arte and quality

management system.

Third party analysis: These are organisations which are hired to evaluate and audit the

performance of the suppliers (How to evaluate potential buyers, 2012). They have all the

resources to analyse different aspects of the business like profitability, management efficiency,

employees turnover, litigations and process of handling of hazardous wastes.

8

has maintained its solvency and liquidity position. The biggest weakness for the supplier is that

they have less investment in the goods. Their lot of funds are in the form of cash which is lying

idle in the business. They need to find a way and use the extra cash in the business.

Recommendations for the company

The client should analyse other factors apart from the financial statements of the supplier.

It will ensure that they have selected the right company for the sourcing

exercise for Facilities Management Services. It will benefit them in short run as well in the

future. Some of the recommendations for the company are as follows:

Altman Z score: The client can use the formula of Altman Z score for the evaluation and

appraisal of the supplier. It helps to find out the solvency position of the company. It takes into

consideration liquid assets, earning power, operating efficiency, leverage, market dimensions ans

asset turnover ratios of the industry (The purchasing process, 2014). The supplier should have

total points +4.48 which indicates stability of the company. On the other hand, -0.25 points

indicates insolvency. The formula for Altman Z score is as follows:

Z= 1.2T1 + 1.4T2 + 3.3T3 + 0.6T4 + 0.99T5

Scoring criteria: The scoring criteria has range of questions which helps in the appraisal

of the potential supplier. The purchaser or the client can include all the aspects of his business

and use it to evaluate the performance of the supplier (Supplier evaluation and selection, 2007).

A scoring criteria includes QA system, track record, employment policy, environmental systems,

financial stability and technical capacity of the supplier. It will ensure that all the criteria are

fulfilled by the potential supplier.

Suppliers surveys: It helps the client to gather the information about the supplier. It

includes referrals, surveys, questionnaires, Profit and loss history, defect arte and quality

management system.

Third party analysis: These are organisations which are hired to evaluate and audit the

performance of the suppliers (How to evaluate potential buyers, 2012). They have all the

resources to analyse different aspects of the business like profitability, management efficiency,

employees turnover, litigations and process of handling of hazardous wastes.

8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.