APC308 Financial Management: Dividend Policy, Mergers & Acquisitions

VerifiedAdded on 2023/01/12

|12

|3864

|69

Report

AI Summary

This report delves into key aspects of financial management, examining dividend policy and mergers & acquisitions (M&A). It analyzes factors influencing dividend decisions, including the size of annual dividends and practical considerations for listed companies. The report evaluates different dividend options for Squeezeco, such as cash dividends, scrip dividends, and share repurchases, comparing their effects. Furthermore, it explores M&A concepts, focusing on valuation methods like the price-earnings ratio, dividend valuation model, and discounted cash flow. The report discusses problems associated with valuation models, using case studies of Squeezeco, Aztec, and Trojan to illustrate the concepts and provide a comprehensive understanding of financial decision-making in these areas.

Financial Management

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Table of Contents.............................................................................................................................2

INTRODUCTION...........................................................................................................................1

MAIN BODY..................................................................................................................................1

Question 1 – Dividend Policy..........................................................................................................1

1. Size of annual dividend which return to their shareholders....................................................1

2. Practical issues need to be consider at the time of deciding size of dividend.........................3

3. Calculate the effect of three options........................................................................................3

4. Critically evaluate that how company’s decisions affect the investment opportunity of £70

million in a project.......................................................................................................................5

Question 2 – Merger and Acquisition..............................................................................................6

1. Price earnings ratio..................................................................................................................6

2. Dividend valuation model........................................................................................................7

3. Discounted cash flow method..................................................................................................8

4. Discuss the problems which associated with valuation model................................................8

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................10

Table of Contents.............................................................................................................................2

INTRODUCTION...........................................................................................................................1

MAIN BODY..................................................................................................................................1

Question 1 – Dividend Policy..........................................................................................................1

1. Size of annual dividend which return to their shareholders....................................................1

2. Practical issues need to be consider at the time of deciding size of dividend.........................3

3. Calculate the effect of three options........................................................................................3

4. Critically evaluate that how company’s decisions affect the investment opportunity of £70

million in a project.......................................................................................................................5

Question 2 – Merger and Acquisition..............................................................................................6

1. Price earnings ratio..................................................................................................................6

2. Dividend valuation model........................................................................................................7

3. Discounted cash flow method..................................................................................................8

4. Discuss the problems which associated with valuation model................................................8

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................10

INTRODUCTION

Financial management involves planning, coordination, direction and regulation of monetary

operations such as acquisition and use of company funds. It implies application of principles of

general management to company’s financial capital. It concentrates on percentages, equity, and

debt (Anthony, 2019). This is beneficial for management of portfolio, distribution of dividends,

capital accumulation, hedging and managing foreign exchange and product life cycle changes.

Financial managers are individuals who conduct research and determine which kind of capital to

raise to finance company's assets along with enhancing the company's value to all shareholders

based on their research. This also applies to an efficient and effective management of funds in a

way that achieves organization's objectives that is to maximize its profit and improve its financial

position to gain competitive advantage over its competitors. For the better understanding of two

companies Squeezo and Aztec are taken which states the impact of various dividend policies

along with merger and acquisition concepts. This report contains calculation of divided with

three different strategies from which best is taken in to consideration, where for detail

understanding of merger and acquisition take of Trojan is taken which states various issues faced

by Aztec.

MAIN BODY

Question 1 – Dividend Policy

1. Size of annual dividend which return to their shareholders

Dividend is just the portion of income of the business under the determination and selection

of the board of directors; it is reported and paid as a ratio of par securities or per share. In

addition, dividend is a percentage of the surplus that exists after making adequate provision for

various forms of resources and taxes etc. after subtracting all expenditures in overall revenue

(Greve and Man Zhang, 2017). The firm's representatives have the obligation to this profit even

if they can not agree on its prompt sale. If the company wants money so the corporation will

keep the full share of the profit without distributing dividend.

Dividend is also not declared in case the entire income is permitted to be in the context of

different funds or surplus. When settling on a dividend statement, the owners should implement

the normal two things into account which mentioned below:

Fair consideration to the shareholders:

1

Financial management involves planning, coordination, direction and regulation of monetary

operations such as acquisition and use of company funds. It implies application of principles of

general management to company’s financial capital. It concentrates on percentages, equity, and

debt (Anthony, 2019). This is beneficial for management of portfolio, distribution of dividends,

capital accumulation, hedging and managing foreign exchange and product life cycle changes.

Financial managers are individuals who conduct research and determine which kind of capital to

raise to finance company's assets along with enhancing the company's value to all shareholders

based on their research. This also applies to an efficient and effective management of funds in a

way that achieves organization's objectives that is to maximize its profit and improve its financial

position to gain competitive advantage over its competitors. For the better understanding of two

companies Squeezo and Aztec are taken which states the impact of various dividend policies

along with merger and acquisition concepts. This report contains calculation of divided with

three different strategies from which best is taken in to consideration, where for detail

understanding of merger and acquisition take of Trojan is taken which states various issues faced

by Aztec.

MAIN BODY

Question 1 – Dividend Policy

1. Size of annual dividend which return to their shareholders

Dividend is just the portion of income of the business under the determination and selection

of the board of directors; it is reported and paid as a ratio of par securities or per share. In

addition, dividend is a percentage of the surplus that exists after making adequate provision for

various forms of resources and taxes etc. after subtracting all expenditures in overall revenue

(Greve and Man Zhang, 2017). The firm's representatives have the obligation to this profit even

if they can not agree on its prompt sale. If the company wants money so the corporation will

keep the full share of the profit without distributing dividend.

Dividend is also not declared in case the entire income is permitted to be in the context of

different funds or surplus. When settling on a dividend statement, the owners should implement

the normal two things into account which mentioned below:

Fair consideration to the shareholders:

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The managers should provide a reasonable estimation of the degree to which owners plan to

get a gain in return for money and taking risks. If it is not done, keeping the investors completely

happy can be challenging and this can often negatively affect the business performance of the

company's shares goodwill (Buchanan, Cao, Liljeblom and Weihrich, 2017).

Company requirements:

Managing the overall financial status is the first responsibility of managers, even as leaders

are asked to make certain sacrifices for doing so. This is also extremely important for the

investor to be able to accurately determine how much extra funding the company needs in order

to grow and expand.

Factors are evaluating at the time of making dividend decisions:

Life of company: New firms also aren't able to pay the shareholders fair returns for a few

years. They will need adequate money for growth in the early years, which they're not in

a place to quickly acquire from the marketplace (Ehrhardt and Brigham, 2016).

Therefore, they would return with their own internal financial resources. In comparison,

older firms may need comparatively less money, but even if they do, they are receiving it

from the economy. A Moderate dividends policy can be implemented in such a scenario.

Nature of Business: It is only Squeezeco, which distributing revenue in regular who will

pay monthly dividends. Industries in this grouping include businesses manufacturing

daily-use specifications. Only businesses participating in public service will pay

dividends to the shareholders on a regular basis. Companies concerned with the

manufacture of expensive goods cannot continue to pay daily dividends.

Financial position: Even though the Squeezeco is able to earn adequate income to pay

dividends due to its earnings condition but they cannot pay dividends in cash. Given

income and excess the company's liquid situation can worsen. The organization will pay

dividends in the form of incentive shares in this situation.

Capital requirement in the future: The dividend strategy also impacts on the

Squeezeco 's future ambitions. If a specific growth plan occurs before the business,

otherwise such a corporation must adopt a stringent dividend strategy, so that extra

resources can be properly managed by restricted access. Under such a case the re-

appropriation of profits would be given greater priority.

2

get a gain in return for money and taking risks. If it is not done, keeping the investors completely

happy can be challenging and this can often negatively affect the business performance of the

company's shares goodwill (Buchanan, Cao, Liljeblom and Weihrich, 2017).

Company requirements:

Managing the overall financial status is the first responsibility of managers, even as leaders

are asked to make certain sacrifices for doing so. This is also extremely important for the

investor to be able to accurately determine how much extra funding the company needs in order

to grow and expand.

Factors are evaluating at the time of making dividend decisions:

Life of company: New firms also aren't able to pay the shareholders fair returns for a few

years. They will need adequate money for growth in the early years, which they're not in

a place to quickly acquire from the marketplace (Ehrhardt and Brigham, 2016).

Therefore, they would return with their own internal financial resources. In comparison,

older firms may need comparatively less money, but even if they do, they are receiving it

from the economy. A Moderate dividends policy can be implemented in such a scenario.

Nature of Business: It is only Squeezeco, which distributing revenue in regular who will

pay monthly dividends. Industries in this grouping include businesses manufacturing

daily-use specifications. Only businesses participating in public service will pay

dividends to the shareholders on a regular basis. Companies concerned with the

manufacture of expensive goods cannot continue to pay daily dividends.

Financial position: Even though the Squeezeco is able to earn adequate income to pay

dividends due to its earnings condition but they cannot pay dividends in cash. Given

income and excess the company's liquid situation can worsen. The organization will pay

dividends in the form of incentive shares in this situation.

Capital requirement in the future: The dividend strategy also impacts on the

Squeezeco 's future ambitions. If a specific growth plan occurs before the business,

otherwise such a corporation must adopt a stringent dividend strategy, so that extra

resources can be properly managed by restricted access. Under such a case the re-

appropriation of profits would be given greater priority.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Economic condition: This is a minor shift in the earnings-policy consistent with market

cycles. The sum of income in the temple products is diminishing. Firms are being pushed

to slash dividend prices (Renneboog and Szilagyi, 2020). Any businesses, which retain

large quantities of Dividend Equalization Funds, resolve these tough times quickly and

do not cause their reputation to slip by keeping a fair dividend rate.

2. Practical issues need to be consider at the time of deciding size of dividend

While deciding the size of dividend which has to pay its shareholders by giving ranking

and it will be provided by the directors. They face several issues which are discussed below:

Selection of investors: The main problem is investor’s selection because all have different

preferences and emotions. Often creditors don't worry about money; they need to have the

company where they received wages to acquire new activities or to grow current enterprise. As

this advancement rises the cost of the deal even as it increases the demand quality of the supply

of the bid, which at the point of sale the deals will favour the buyers.

Various alternatives: There are two systems where company’s leaders will follow

generate profits such as cash income and profit break. The organization's key problem is to select

which option to please creditors by fulfilling their preference of income and capital benefit

Desires of investors: It is impossible for an company to determine the expectations of

customers for income esteem; consumers will presume spending more than expected if the entity

will not concentrate on growth and will expect the expense of the deal to decline later.

Guidelines Act: The regulatory authority agreed with a set of guidelines for the

corporation, in which the entity will have to spend what might. For example, it allows the

company to retain a certain proportion of savings for profit (He, Ng, Zaiats and Zhang, 2017). If

the company generated a income of 15 per cent, it would keep 7.5 per cent of savings in any

case.

3. Calculate the effect of three options

Cash dividend payout of 15p per share:

3

cycles. The sum of income in the temple products is diminishing. Firms are being pushed

to slash dividend prices (Renneboog and Szilagyi, 2020). Any businesses, which retain

large quantities of Dividend Equalization Funds, resolve these tough times quickly and

do not cause their reputation to slip by keeping a fair dividend rate.

2. Practical issues need to be consider at the time of deciding size of dividend

While deciding the size of dividend which has to pay its shareholders by giving ranking

and it will be provided by the directors. They face several issues which are discussed below:

Selection of investors: The main problem is investor’s selection because all have different

preferences and emotions. Often creditors don't worry about money; they need to have the

company where they received wages to acquire new activities or to grow current enterprise. As

this advancement rises the cost of the deal even as it increases the demand quality of the supply

of the bid, which at the point of sale the deals will favour the buyers.

Various alternatives: There are two systems where company’s leaders will follow

generate profits such as cash income and profit break. The organization's key problem is to select

which option to please creditors by fulfilling their preference of income and capital benefit

Desires of investors: It is impossible for an company to determine the expectations of

customers for income esteem; consumers will presume spending more than expected if the entity

will not concentrate on growth and will expect the expense of the deal to decline later.

Guidelines Act: The regulatory authority agreed with a set of guidelines for the

corporation, in which the entity will have to spend what might. For example, it allows the

company to retain a certain proportion of savings for profit (He, Ng, Zaiats and Zhang, 2017). If

the company generated a income of 15 per cent, it would keep 7.5 per cent of savings in any

case.

3. Calculate the effect of three options

Cash dividend payout of 15p per share:

3

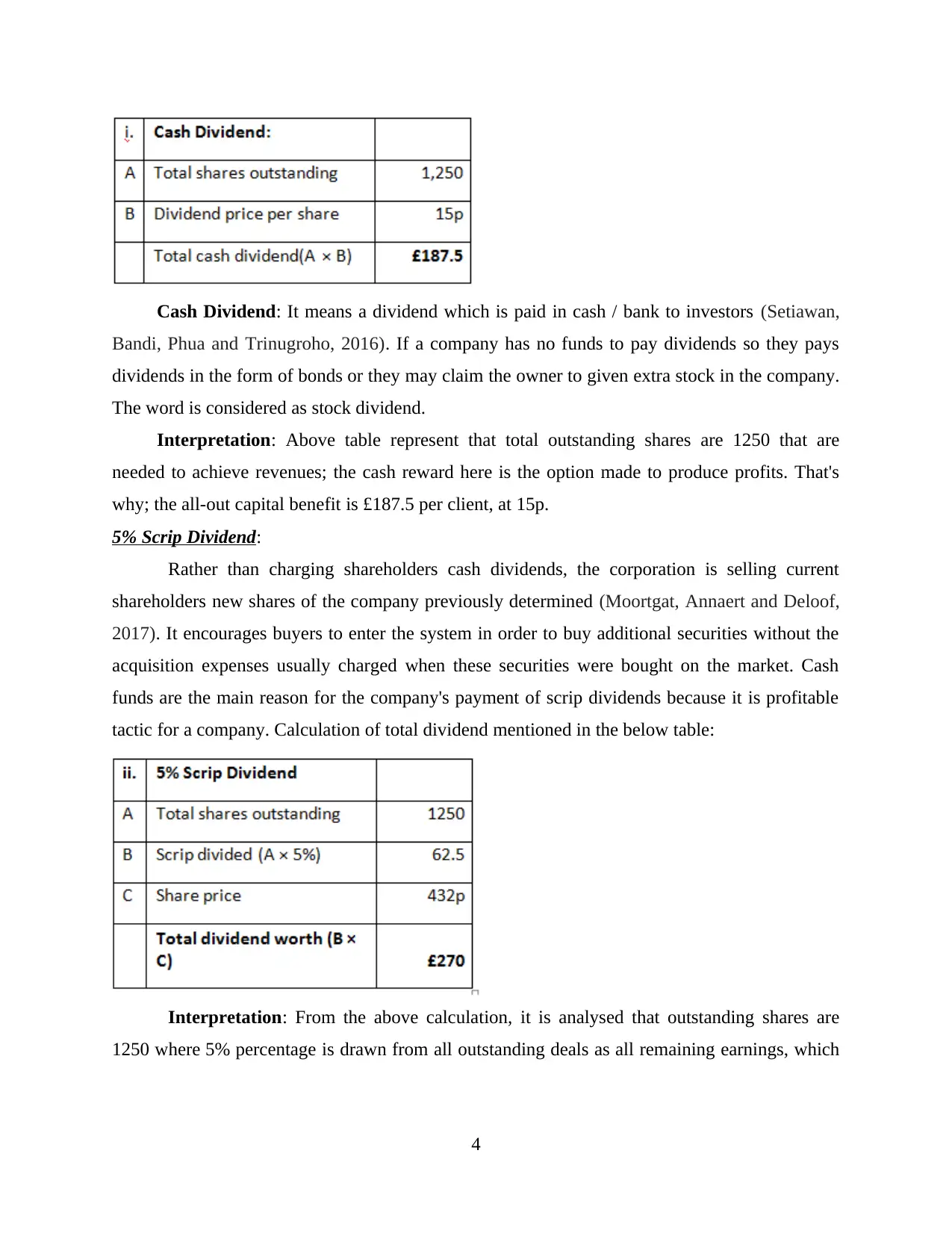

Cash Dividend: It means a dividend which is paid in cash / bank to investors (Setiawan,

Bandi, Phua and Trinugroho, 2016). If a company has no funds to pay dividends so they pays

dividends in the form of bonds or they may claim the owner to given extra stock in the company.

The word is considered as stock dividend.

Interpretation: Above table represent that total outstanding shares are 1250 that are

needed to achieve revenues; the cash reward here is the option made to produce profits. That's

why; the all-out capital benefit is £187.5 per client, at 15p.

5% Scrip Dividend:

Rather than charging shareholders cash dividends, the corporation is selling current

shareholders new shares of the company previously determined (Moortgat, Annaert and Deloof,

2017). It encourages buyers to enter the system in order to buy additional securities without the

acquisition expenses usually charged when these securities were bought on the market. Cash

funds are the main reason for the company's payment of scrip dividends because it is profitable

tactic for a company. Calculation of total dividend mentioned in the below table:

Interpretation: From the above calculation, it is analysed that outstanding shares are

1250 where 5% percentage is drawn from all outstanding deals as all remaining earnings, which

4

Bandi, Phua and Trinugroho, 2016). If a company has no funds to pay dividends so they pays

dividends in the form of bonds or they may claim the owner to given extra stock in the company.

The word is considered as stock dividend.

Interpretation: Above table represent that total outstanding shares are 1250 that are

needed to achieve revenues; the cash reward here is the option made to produce profits. That's

why; the all-out capital benefit is £187.5 per client, at 15p.

5% Scrip Dividend:

Rather than charging shareholders cash dividends, the corporation is selling current

shareholders new shares of the company previously determined (Moortgat, Annaert and Deloof,

2017). It encourages buyers to enter the system in order to buy additional securities without the

acquisition expenses usually charged when these securities were bought on the market. Cash

funds are the main reason for the company's payment of scrip dividends because it is profitable

tactic for a company. Calculation of total dividend mentioned in the below table:

Interpretation: From the above calculation, it is analysed that outstanding shares are

1250 where 5% percentage is drawn from all outstanding deals as all remaining earnings, which

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

is 62.5. The expense per share is issued at £270 therefore the full benefit of the business holder

from having new deals is £ 270.

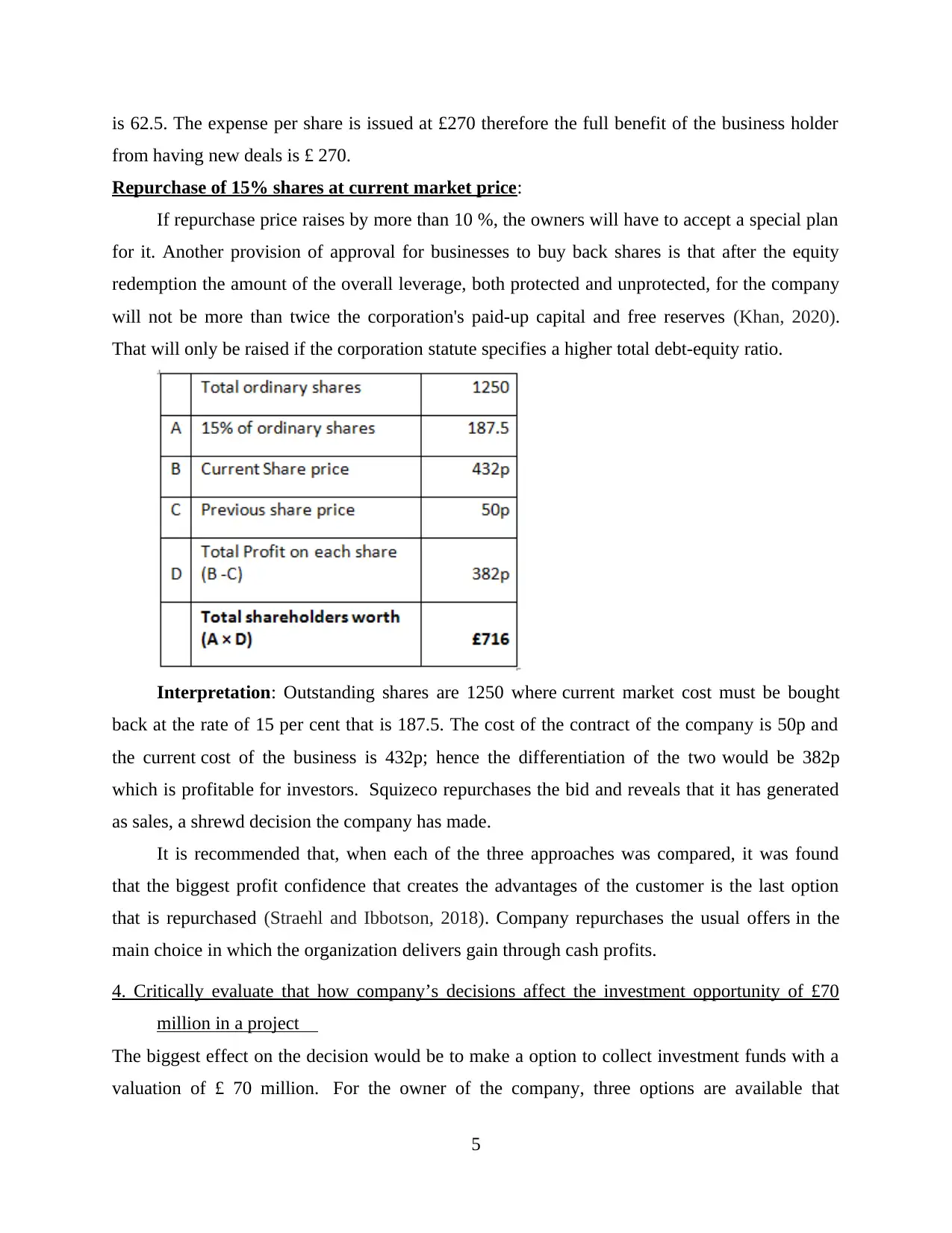

Repurchase of 15% shares at current market price:

If repurchase price raises by more than 10 %, the owners will have to accept a special plan

for it. Another provision of approval for businesses to buy back shares is that after the equity

redemption the amount of the overall leverage, both protected and unprotected, for the company

will not be more than twice the corporation's paid-up capital and free reserves (Khan, 2020).

That will only be raised if the corporation statute specifies a higher total debt-equity ratio.

Interpretation: Outstanding shares are 1250 where current market cost must be bought

back at the rate of 15 per cent that is 187.5. The cost of the contract of the company is 50p and

the current cost of the business is 432p; hence the differentiation of the two would be 382p

which is profitable for investors. Squizeco repurchases the bid and reveals that it has generated

as sales, a shrewd decision the company has made.

It is recommended that, when each of the three approaches was compared, it was found

that the biggest profit confidence that creates the advantages of the customer is the last option

that is repurchased (Straehl and Ibbotson, 2018). Company repurchases the usual offers in the

main choice in which the organization delivers gain through cash profits.

4. Critically evaluate that how company’s decisions affect the investment opportunity of £70

million in a project

The biggest effect on the decision would be to make a option to collect investment funds with a

valuation of £ 70 million. For the owner of the company, three options are available that

5

from having new deals is £ 270.

Repurchase of 15% shares at current market price:

If repurchase price raises by more than 10 %, the owners will have to accept a special plan

for it. Another provision of approval for businesses to buy back shares is that after the equity

redemption the amount of the overall leverage, both protected and unprotected, for the company

will not be more than twice the corporation's paid-up capital and free reserves (Khan, 2020).

That will only be raised if the corporation statute specifies a higher total debt-equity ratio.

Interpretation: Outstanding shares are 1250 where current market cost must be bought

back at the rate of 15 per cent that is 187.5. The cost of the contract of the company is 50p and

the current cost of the business is 432p; hence the differentiation of the two would be 382p

which is profitable for investors. Squizeco repurchases the bid and reveals that it has generated

as sales, a shrewd decision the company has made.

It is recommended that, when each of the three approaches was compared, it was found

that the biggest profit confidence that creates the advantages of the customer is the last option

that is repurchased (Straehl and Ibbotson, 2018). Company repurchases the usual offers in the

main choice in which the organization delivers gain through cash profits.

4. Critically evaluate that how company’s decisions affect the investment opportunity of £70

million in a project

The biggest effect on the decision would be to make a option to collect investment funds with a

valuation of £ 70 million. For the owner of the company, three options are available that

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

are funding by contract, expanding properties by utilizing shops and excess through issue of

interest shares. Such three options have their massive disservice and points of concern. Using a

combination of each of these strategies could be predicted. For example; the company should

split the requirement of the store into three amounts, e.g. 30 percent through duty, 60 percent

through issue of interest shares and 10 percent through store keeping. When an question of sales

may arise, the company has three alternatives such as:

Right issue of securities to current stock investors.

Issuing preferred stock with a fixed dividend payout rate.

To sell ordinary shares at a cheaper selling level.

Question 2 – Merger and Acquisition

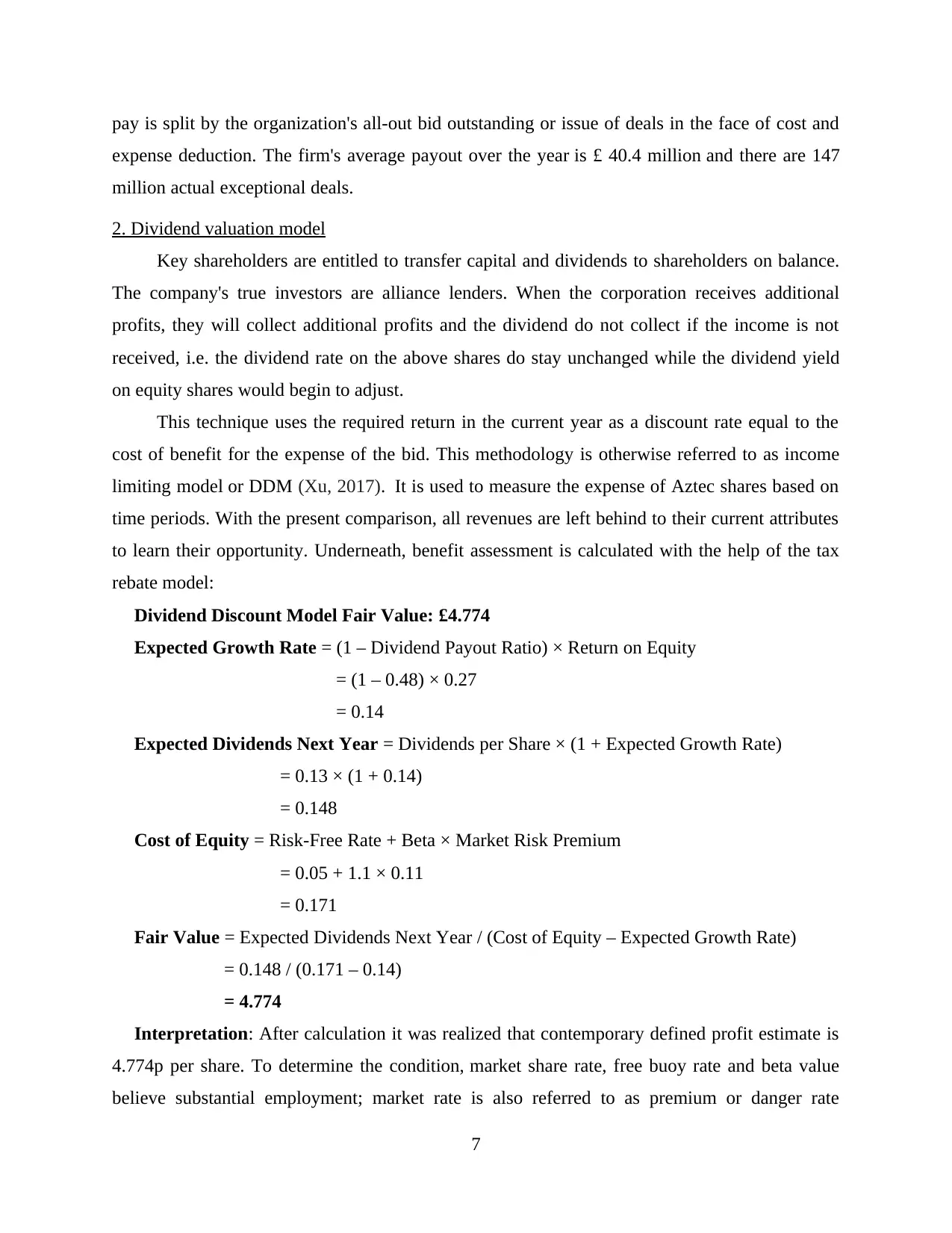

1. Price earnings ratio

It is also known as P / E Ratio which include the firm's share price to the company's market

share. Proportions are used to measure businesses to determine that they are undervalued or

overvalued. Share price determined by the benefit of per share of the company (after tax) is

considered the Price-to-earnings ratio. Small numerical prices indicate the share price is

comparatively low to the income of the company (Zietlow, Hankin, Seidner and O'Brien, 2018).

It is used as a guideline for investments in securities. Stock market internationalization, enhanced

understanding of growth and likewise, the significance of price-earnings ratios as indices became

relevant

Interpretation: The figure reveals that shareholders from Trojan plc have gained

27percent a share. To achieve the benefit acquisition ratio or P / E ratio; gross allocated overall

6

interest shares. Such three options have their massive disservice and points of concern. Using a

combination of each of these strategies could be predicted. For example; the company should

split the requirement of the store into three amounts, e.g. 30 percent through duty, 60 percent

through issue of interest shares and 10 percent through store keeping. When an question of sales

may arise, the company has three alternatives such as:

Right issue of securities to current stock investors.

Issuing preferred stock with a fixed dividend payout rate.

To sell ordinary shares at a cheaper selling level.

Question 2 – Merger and Acquisition

1. Price earnings ratio

It is also known as P / E Ratio which include the firm's share price to the company's market

share. Proportions are used to measure businesses to determine that they are undervalued or

overvalued. Share price determined by the benefit of per share of the company (after tax) is

considered the Price-to-earnings ratio. Small numerical prices indicate the share price is

comparatively low to the income of the company (Zietlow, Hankin, Seidner and O'Brien, 2018).

It is used as a guideline for investments in securities. Stock market internationalization, enhanced

understanding of growth and likewise, the significance of price-earnings ratios as indices became

relevant

Interpretation: The figure reveals that shareholders from Trojan plc have gained

27percent a share. To achieve the benefit acquisition ratio or P / E ratio; gross allocated overall

6

pay is split by the organization's all-out bid outstanding or issue of deals in the face of cost and

expense deduction. The firm's average payout over the year is £ 40.4 million and there are 147

million actual exceptional deals.

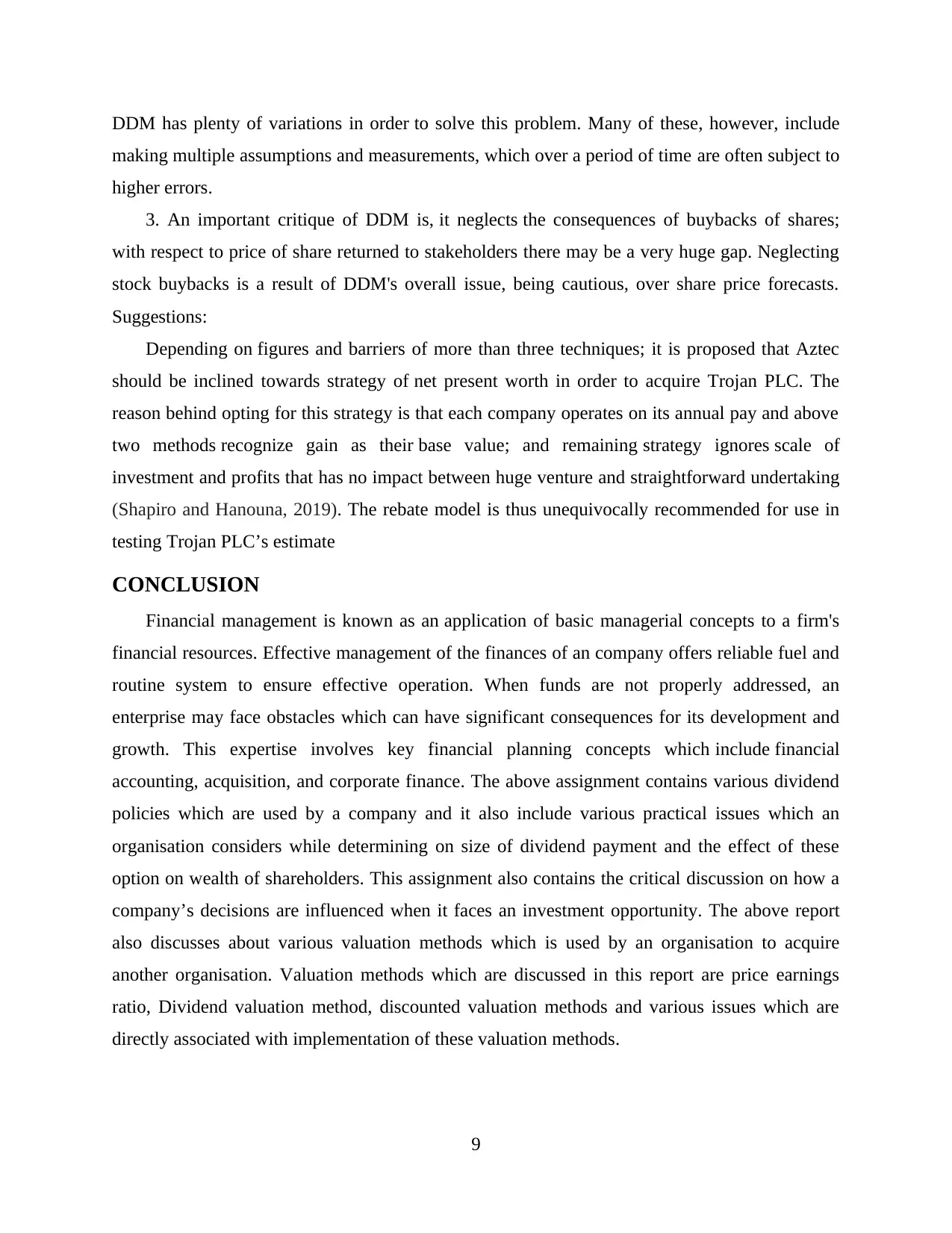

2. Dividend valuation model

Key shareholders are entitled to transfer capital and dividends to shareholders on balance.

The company's true investors are alliance lenders. When the corporation receives additional

profits, they will collect additional profits and the dividend do not collect if the income is not

received, i.e. the dividend rate on the above shares do stay unchanged while the dividend yield

on equity shares would begin to adjust.

This technique uses the required return in the current year as a discount rate equal to the

cost of benefit for the expense of the bid. This methodology is otherwise referred to as income

limiting model or DDM (Xu, 2017). It is used to measure the expense of Aztec shares based on

time periods. With the present comparison, all revenues are left behind to their current attributes

to learn their opportunity. Underneath, benefit assessment is calculated with the help of the tax

rebate model:

Dividend Discount Model Fair Value: £4.774

Expected Growth Rate = (1 – Dividend Payout Ratio) × Return on Equity

= (1 – 0.48) × 0.27

= 0.14

Expected Dividends Next Year = Dividends per Share × (1 + Expected Growth Rate)

= 0.13 × (1 + 0.14)

= 0.148

Cost of Equity = Risk-Free Rate + Beta × Market Risk Premium

= 0.05 + 1.1 × 0.11

= 0.171

Fair Value = Expected Dividends Next Year / (Cost of Equity – Expected Growth Rate)

= 0.148 / (0.171 – 0.14)

= 4.774

Interpretation: After calculation it was realized that contemporary defined profit estimate is

4.774p per share. To determine the condition, market share rate, free buoy rate and beta value

believe substantial employment; market rate is also referred to as premium or danger rate

7

expense deduction. The firm's average payout over the year is £ 40.4 million and there are 147

million actual exceptional deals.

2. Dividend valuation model

Key shareholders are entitled to transfer capital and dividends to shareholders on balance.

The company's true investors are alliance lenders. When the corporation receives additional

profits, they will collect additional profits and the dividend do not collect if the income is not

received, i.e. the dividend rate on the above shares do stay unchanged while the dividend yield

on equity shares would begin to adjust.

This technique uses the required return in the current year as a discount rate equal to the

cost of benefit for the expense of the bid. This methodology is otherwise referred to as income

limiting model or DDM (Xu, 2017). It is used to measure the expense of Aztec shares based on

time periods. With the present comparison, all revenues are left behind to their current attributes

to learn their opportunity. Underneath, benefit assessment is calculated with the help of the tax

rebate model:

Dividend Discount Model Fair Value: £4.774

Expected Growth Rate = (1 – Dividend Payout Ratio) × Return on Equity

= (1 – 0.48) × 0.27

= 0.14

Expected Dividends Next Year = Dividends per Share × (1 + Expected Growth Rate)

= 0.13 × (1 + 0.14)

= 0.148

Cost of Equity = Risk-Free Rate + Beta × Market Risk Premium

= 0.05 + 1.1 × 0.11

= 0.171

Fair Value = Expected Dividends Next Year / (Cost of Equity – Expected Growth Rate)

= 0.148 / (0.171 – 0.14)

= 4.774

Interpretation: After calculation it was realized that contemporary defined profit estimate is

4.774p per share. To determine the condition, market share rate, free buoy rate and beta value

believe substantial employment; market rate is also referred to as premium or danger rate

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

because conjecture takes this additional premium to experience challenge. Though free buoy

levels are not risky because there would be no risk of losing the value of the company.

3. Discounted cash flow method

Discounted cash flow (DCF) is known as an estimation tool which is used to measure an

investment's worth on a basis of its potential cash flows. DCF analysis tries to determine worth

of today’s investment on a basis of estimations of that how much money will it be able to

produce in future (Zhang, Li and Ren, 2016). This appears to apply to investors' capital assets

and also to company owners seeking to make adjustments in their businesses, such as acquiring

new technology or buying new equipment.

Discounted cash flow method

Year Net Income £m Discounted cash flow @7%

Year 1 40.40 37.76

Year 2 41.21 35.99

Year 3 42.03 34.31

Year 4 42.87 32.71

Year 5 43.73 31.18

171.95

Interpretation: From the above calculation of small distributed pay profits with an

average growth rate of 2 percent per annum, it is established that after completion of 5 years

from its investment a company will get £ 171.95m at a present value.

4. Discuss the problems which associated with valuation model

Following discussed are some of the issues while calculating a value of an investment using

above valuation methods:

1. It could not be used while investing in stocks in order to determine a stock that does not

yield dividends, irrespective of capital gains. DDM is based on a faulty premise; it says that a

share's sole value is return on investment which is generated by dividends.

2. Another limitation is a fact that it uses number of estimations about issues like rate of

growth and expected rate of return which are included in calculation of price. An example of this

is when dividend yields shift dramatically over time (Shakeel and Datta, 2020). If one of

its assumptions or estimations made in calculation is substantially in error, it could result in an

analyst, who calculates value for stock, being undervalued or upgraded considerably. Closed

8

levels are not risky because there would be no risk of losing the value of the company.

3. Discounted cash flow method

Discounted cash flow (DCF) is known as an estimation tool which is used to measure an

investment's worth on a basis of its potential cash flows. DCF analysis tries to determine worth

of today’s investment on a basis of estimations of that how much money will it be able to

produce in future (Zhang, Li and Ren, 2016). This appears to apply to investors' capital assets

and also to company owners seeking to make adjustments in their businesses, such as acquiring

new technology or buying new equipment.

Discounted cash flow method

Year Net Income £m Discounted cash flow @7%

Year 1 40.40 37.76

Year 2 41.21 35.99

Year 3 42.03 34.31

Year 4 42.87 32.71

Year 5 43.73 31.18

171.95

Interpretation: From the above calculation of small distributed pay profits with an

average growth rate of 2 percent per annum, it is established that after completion of 5 years

from its investment a company will get £ 171.95m at a present value.

4. Discuss the problems which associated with valuation model

Following discussed are some of the issues while calculating a value of an investment using

above valuation methods:

1. It could not be used while investing in stocks in order to determine a stock that does not

yield dividends, irrespective of capital gains. DDM is based on a faulty premise; it says that a

share's sole value is return on investment which is generated by dividends.

2. Another limitation is a fact that it uses number of estimations about issues like rate of

growth and expected rate of return which are included in calculation of price. An example of this

is when dividend yields shift dramatically over time (Shakeel and Datta, 2020). If one of

its assumptions or estimations made in calculation is substantially in error, it could result in an

analyst, who calculates value for stock, being undervalued or upgraded considerably. Closed

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

DDM has plenty of variations in order to solve this problem. Many of these, however, include

making multiple assumptions and measurements, which over a period of time are often subject to

higher errors.

3. An important critique of DDM is, it neglects the consequences of buybacks of shares;

with respect to price of share returned to stakeholders there may be a very huge gap. Neglecting

stock buybacks is a result of DDM's overall issue, being cautious, over share price forecasts.

Suggestions:

Depending on figures and barriers of more than three techniques; it is proposed that Aztec

should be inclined towards strategy of net present worth in order to acquire Trojan PLC. The

reason behind opting for this strategy is that each company operates on its annual pay and above

two methods recognize gain as their base value; and remaining strategy ignores scale of

investment and profits that has no impact between huge venture and straightforward undertaking

(Shapiro and Hanouna, 2019). The rebate model is thus unequivocally recommended for use in

testing Trojan PLC’s estimate

CONCLUSION

Financial management is known as an application of basic managerial concepts to a firm's

financial resources. Effective management of the finances of an company offers reliable fuel and

routine system to ensure effective operation. When funds are not properly addressed, an

enterprise may face obstacles which can have significant consequences for its development and

growth. This expertise involves key financial planning concepts which include financial

accounting, acquisition, and corporate finance. The above assignment contains various dividend

policies which are used by a company and it also include various practical issues which an

organisation considers while determining on size of dividend payment and the effect of these

option on wealth of shareholders. This assignment also contains the critical discussion on how a

company’s decisions are influenced when it faces an investment opportunity. The above report

also discusses about various valuation methods which is used by an organisation to acquire

another organisation. Valuation methods which are discussed in this report are price earnings

ratio, Dividend valuation method, discounted valuation methods and various issues which are

directly associated with implementation of these valuation methods.

9

making multiple assumptions and measurements, which over a period of time are often subject to

higher errors.

3. An important critique of DDM is, it neglects the consequences of buybacks of shares;

with respect to price of share returned to stakeholders there may be a very huge gap. Neglecting

stock buybacks is a result of DDM's overall issue, being cautious, over share price forecasts.

Suggestions:

Depending on figures and barriers of more than three techniques; it is proposed that Aztec

should be inclined towards strategy of net present worth in order to acquire Trojan PLC. The

reason behind opting for this strategy is that each company operates on its annual pay and above

two methods recognize gain as their base value; and remaining strategy ignores scale of

investment and profits that has no impact between huge venture and straightforward undertaking

(Shapiro and Hanouna, 2019). The rebate model is thus unequivocally recommended for use in

testing Trojan PLC’s estimate

CONCLUSION

Financial management is known as an application of basic managerial concepts to a firm's

financial resources. Effective management of the finances of an company offers reliable fuel and

routine system to ensure effective operation. When funds are not properly addressed, an

enterprise may face obstacles which can have significant consequences for its development and

growth. This expertise involves key financial planning concepts which include financial

accounting, acquisition, and corporate finance. The above assignment contains various dividend

policies which are used by a company and it also include various practical issues which an

organisation considers while determining on size of dividend payment and the effect of these

option on wealth of shareholders. This assignment also contains the critical discussion on how a

company’s decisions are influenced when it faces an investment opportunity. The above report

also discusses about various valuation methods which is used by an organisation to acquire

another organisation. Valuation methods which are discussed in this report are price earnings

ratio, Dividend valuation method, discounted valuation methods and various issues which are

directly associated with implementation of these valuation methods.

9

REFERENCES

Books & Journals

Anthony, M.U.G.O., 2019. Effects of merger and acquisition on financial performance: case

study of commercial banks. International Journal of Business Management and

Finance, 1(1).

Greve, H.R. and Man Zhang, C., 2017. Institutional logics and power sources: Merger and

acquisition decisions. Academy of Management Journal, 60(2), pp.671-694.

Buchanan, B.G., Cao, C.X., Liljeblom, E. and Weihrich, S., 2017. Uncertainty and firm dividend

policy—A natural experiment. Journal of Corporate Finance, 42, pp.179-197.

Ehrhardt, M.C. and Brigham, E.F., 2016. Corporate finance: A focused approach. Cengage

learning.

Renneboog, L. and Szilagyi, P.G., 2020. How relevant is dividend policy under low shareholder

protection?. Journal of International Financial Markets, Institutions and Money, 64,

p.100776.

He, W., Ng, L., Zaiats, N. and Zhang, B., 2017. Dividend policy and earnings management

across countries. Journal of Corporate Finance, 42, pp.267-286.

Moortgat, L., Annaert, J. and Deloof, M., 2017. Investor protection, taxation and dividend

policy: long-run evidence, 1838–2012. Journal of Banking & Finance, 85, pp.113-

131.

Setiawan, D., Bandi, B., Phua, L.K. and Trinugroho, I., 2016. Ownership structure and dividend

policy in Indonesia. Journal of Asia Business Studies.

Khan, F., 2020. Does Dividend Policy Determine Stock Price Volatility?(A Case Study of

Malaysian Manufacturing Sector). Journal Global Policy and Governance, 9(1),

pp.67-78.

Straehl, P.U. and Ibbotson, R.G., 2018. “The Long-Run Drivers of Stock Returns: Total Payouts

and the Real Economy”: Author Response. Financial Analysts Journal, 74(1).

Zietlow, J., Hankin, J.A., Seidner, A. and O'Brien, T., 2018. Financial management for nonprofit

organizations: policies and practices. John Wiley & Sons.

Xu, J., 2017. Growing through the merger and acquisition. Journal of Economic Dynamics and

Control, 80, pp.54-74.

Zhang, C., Li, D. and Ren, R., 2016. Pythagorean fuzzy multigranulation rough set over two

universes and its applications in merger and acquisition. International Journal of

Intelligent Systems, 31(9), pp.921-943.

Shakeel, S. and Datta, S., 2020. Role of Internal Audit in Merger and Acquisition. The

Management Accountant Journal, 55(4), pp.40-45.

Shapiro, A.C. and Hanouna, P., 2019. Multinational financial management. Wiley.

10

Books & Journals

Anthony, M.U.G.O., 2019. Effects of merger and acquisition on financial performance: case

study of commercial banks. International Journal of Business Management and

Finance, 1(1).

Greve, H.R. and Man Zhang, C., 2017. Institutional logics and power sources: Merger and

acquisition decisions. Academy of Management Journal, 60(2), pp.671-694.

Buchanan, B.G., Cao, C.X., Liljeblom, E. and Weihrich, S., 2017. Uncertainty and firm dividend

policy—A natural experiment. Journal of Corporate Finance, 42, pp.179-197.

Ehrhardt, M.C. and Brigham, E.F., 2016. Corporate finance: A focused approach. Cengage

learning.

Renneboog, L. and Szilagyi, P.G., 2020. How relevant is dividend policy under low shareholder

protection?. Journal of International Financial Markets, Institutions and Money, 64,

p.100776.

He, W., Ng, L., Zaiats, N. and Zhang, B., 2017. Dividend policy and earnings management

across countries. Journal of Corporate Finance, 42, pp.267-286.

Moortgat, L., Annaert, J. and Deloof, M., 2017. Investor protection, taxation and dividend

policy: long-run evidence, 1838–2012. Journal of Banking & Finance, 85, pp.113-

131.

Setiawan, D., Bandi, B., Phua, L.K. and Trinugroho, I., 2016. Ownership structure and dividend

policy in Indonesia. Journal of Asia Business Studies.

Khan, F., 2020. Does Dividend Policy Determine Stock Price Volatility?(A Case Study of

Malaysian Manufacturing Sector). Journal Global Policy and Governance, 9(1),

pp.67-78.

Straehl, P.U. and Ibbotson, R.G., 2018. “The Long-Run Drivers of Stock Returns: Total Payouts

and the Real Economy”: Author Response. Financial Analysts Journal, 74(1).

Zietlow, J., Hankin, J.A., Seidner, A. and O'Brien, T., 2018. Financial management for nonprofit

organizations: policies and practices. John Wiley & Sons.

Xu, J., 2017. Growing through the merger and acquisition. Journal of Economic Dynamics and

Control, 80, pp.54-74.

Zhang, C., Li, D. and Ren, R., 2016. Pythagorean fuzzy multigranulation rough set over two

universes and its applications in merger and acquisition. International Journal of

Intelligent Systems, 31(9), pp.921-943.

Shakeel, S. and Datta, S., 2020. Role of Internal Audit in Merger and Acquisition. The

Management Accountant Journal, 55(4), pp.40-45.

Shapiro, A.C. and Hanouna, P., 2019. Multinational financial management. Wiley.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.