Financial Management Report: Kadlex, Lexbel, Happy Meal Analysis

VerifiedAdded on 2021/02/19

|14

|4052

|57

Report

AI Summary

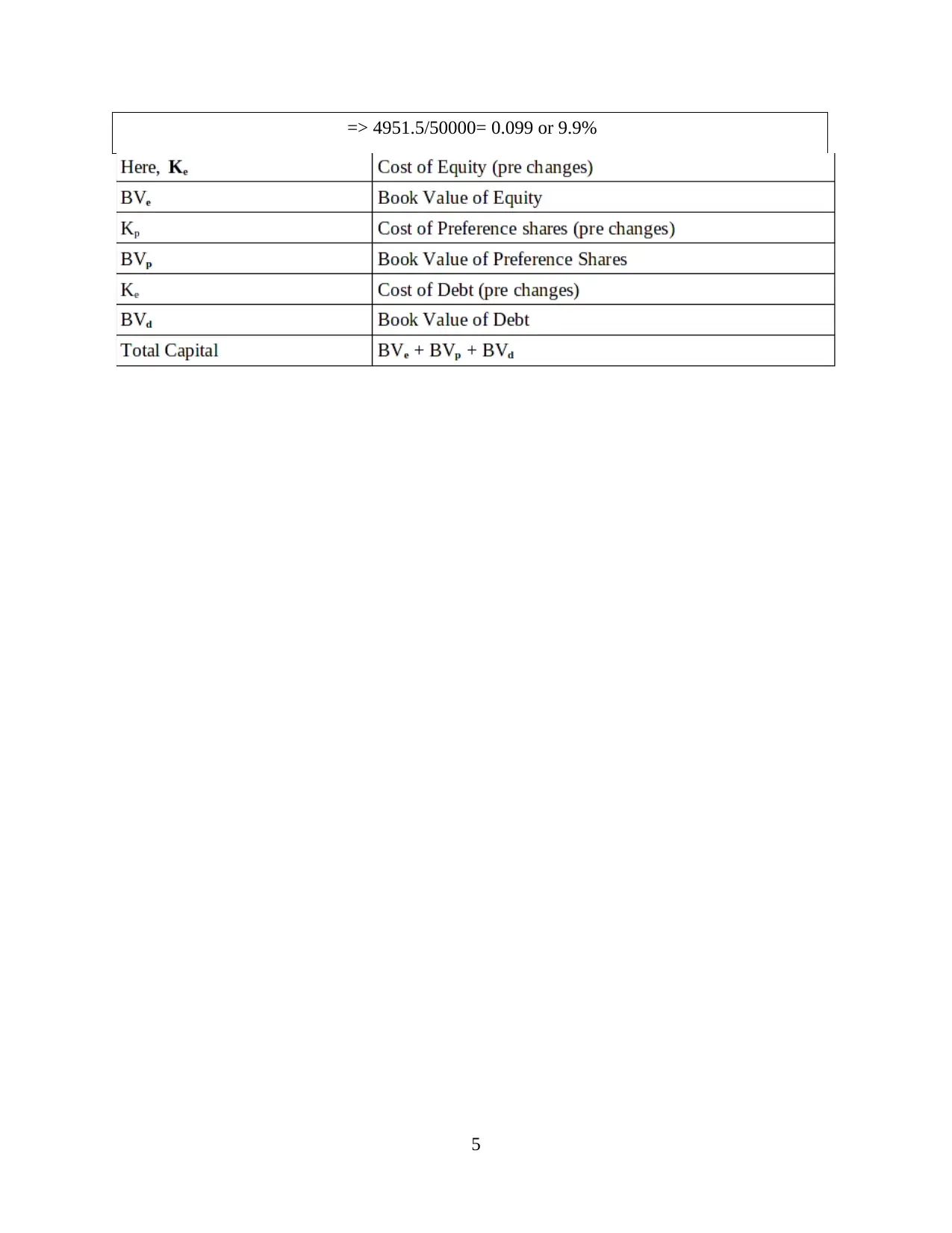

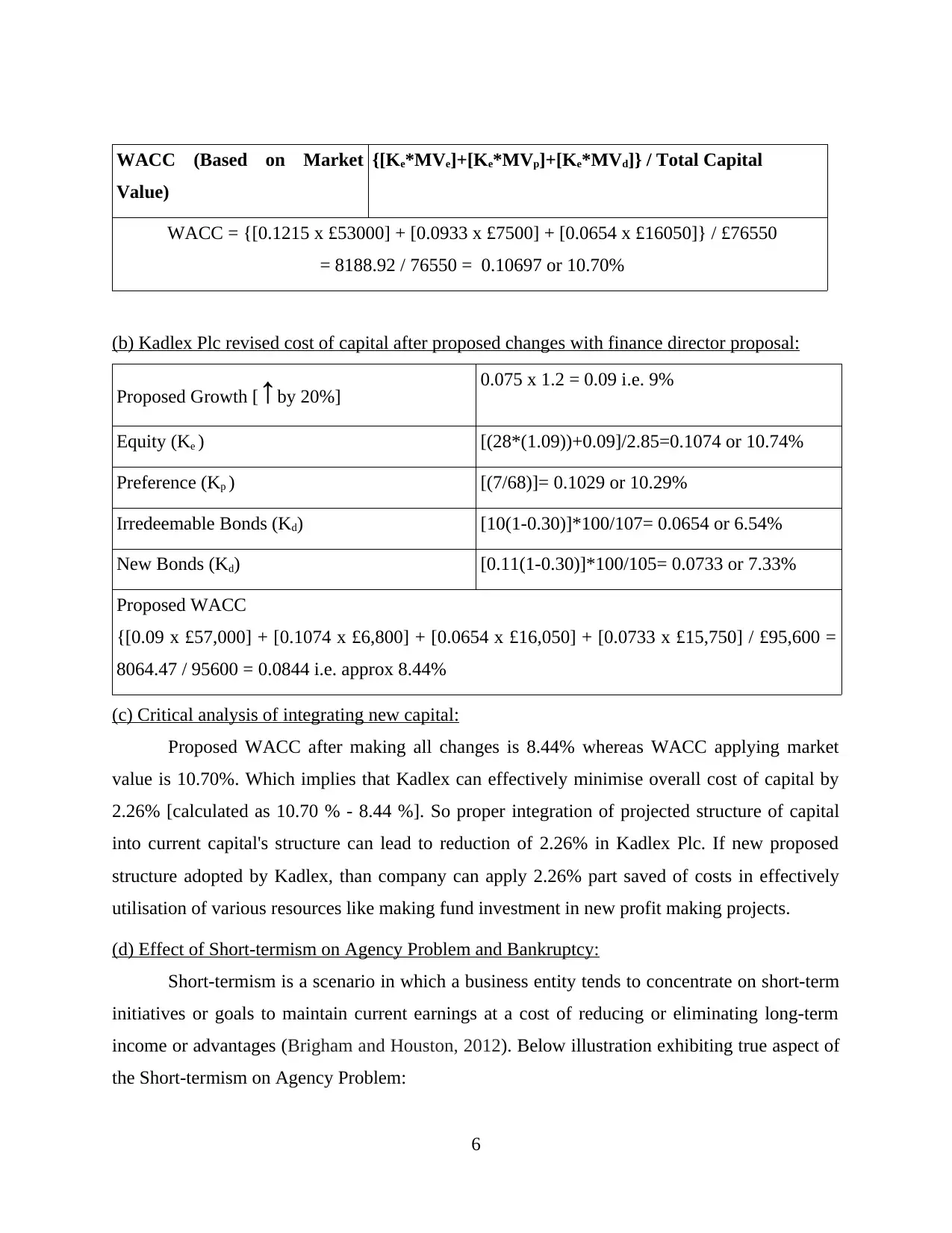

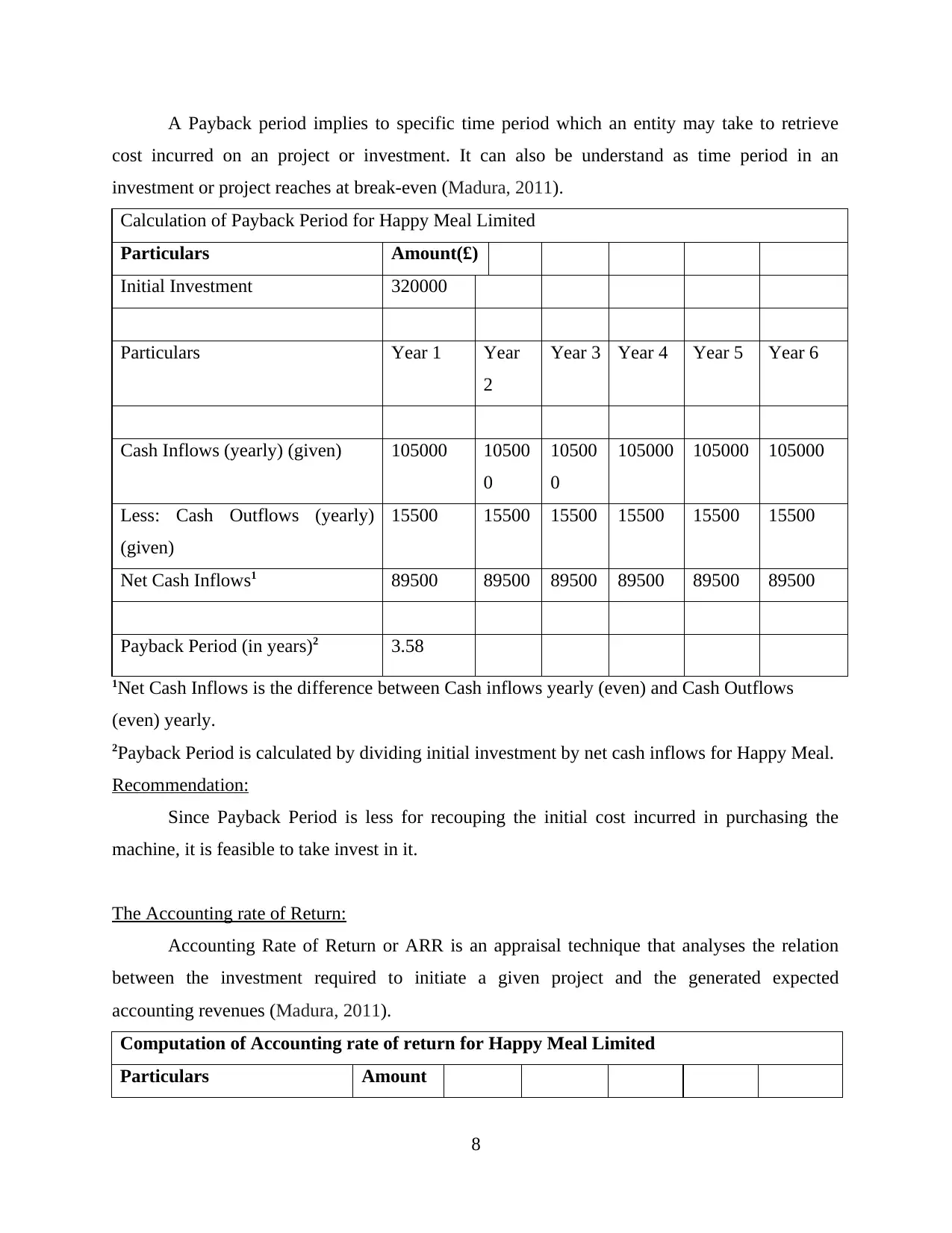

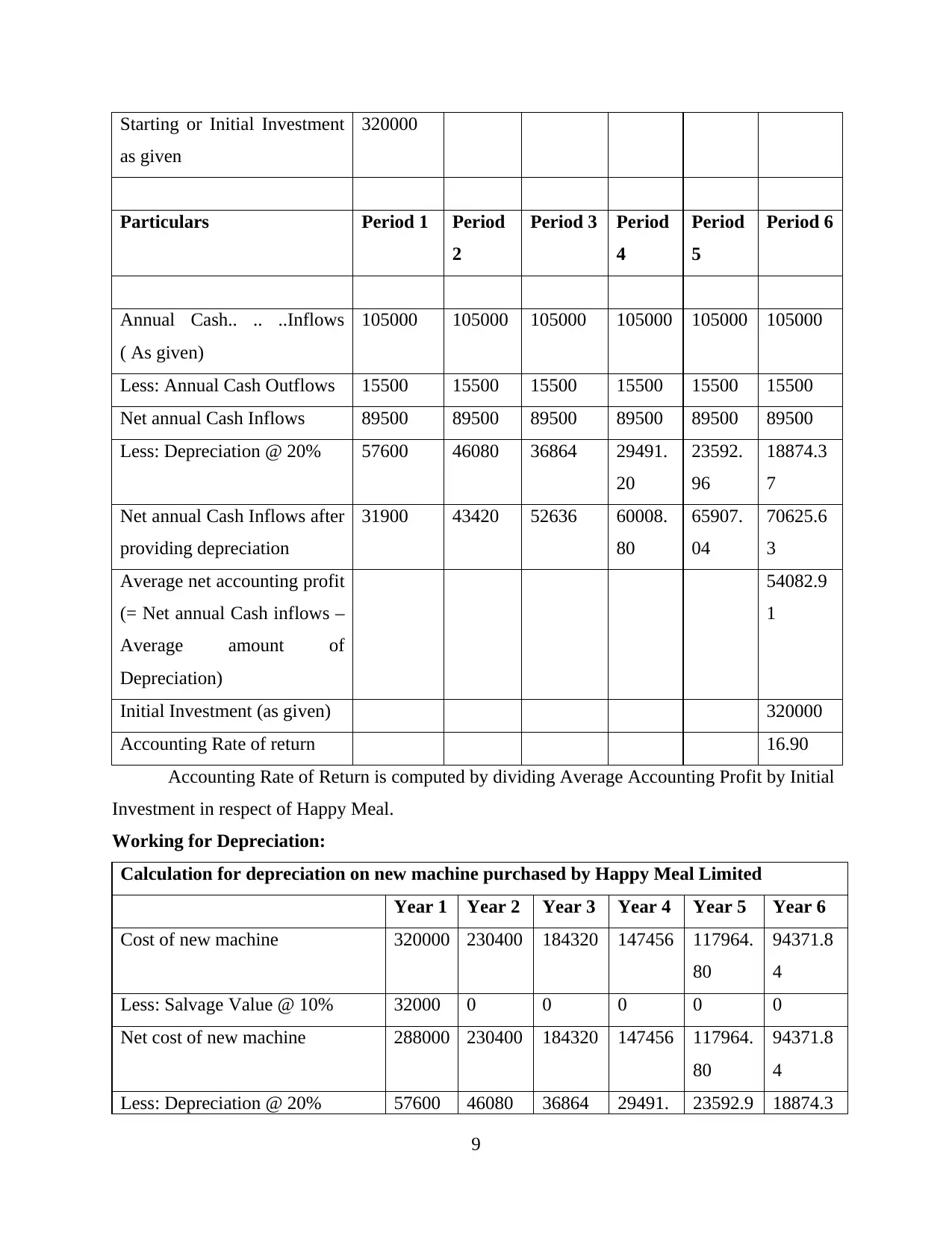

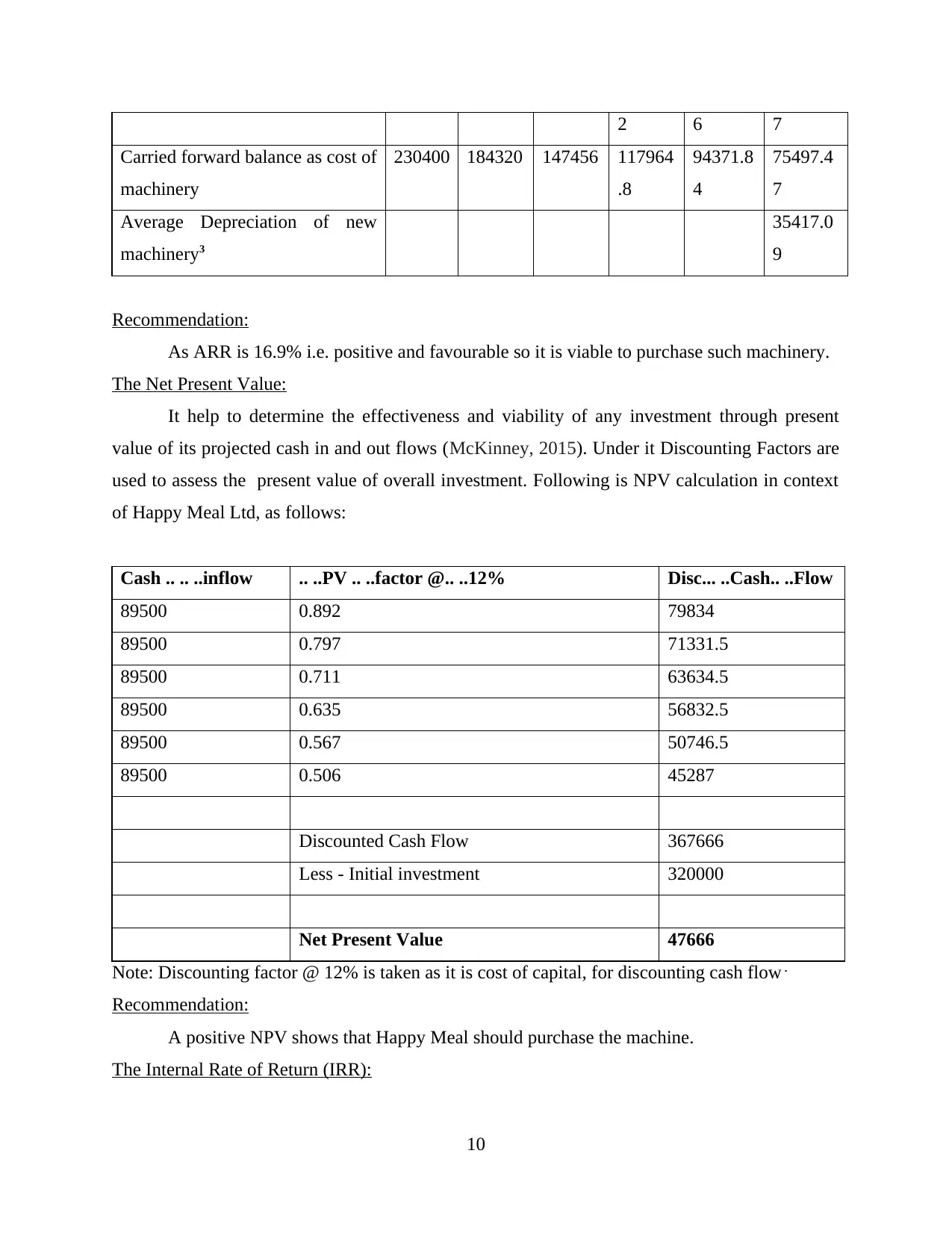

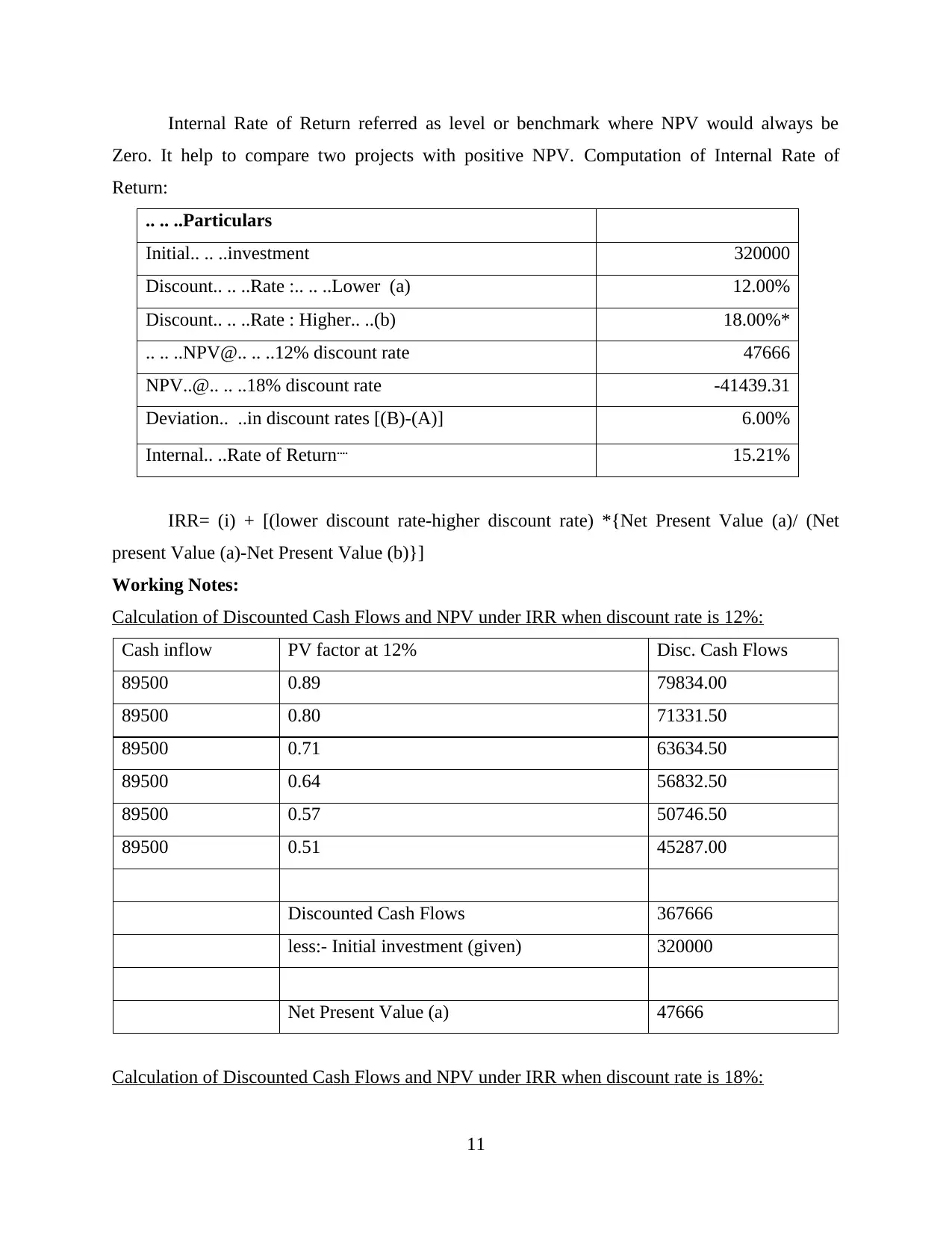

This report provides a detailed analysis of financial management principles, focusing on capital structure, cost of capital, and investment appraisal techniques. It examines the Weighted Average Cost of Capital (WACC) calculation for Kadlex Plc, considering both book and market values, and assesses the impact of proposed changes in capital structure. The report further explores investment appraisal techniques such as payback period, Accounting Rate of Return (ARR), and Net Present Value (NPV) in the context of Happy Meal Limited's investment in new machinery. Additionally, it addresses the effects of short-termism on agency problems and bankruptcy. The analysis includes detailed calculations, critical evaluations, and recommendations, offering a comprehensive understanding of financial decision-making processes within the context of the provided case studies. The report also presents a revised cost of capital analysis, integrating proposed changes and critically analyzing the implications of integrating new capital, along with an exploration of the impact of short-termism on agency problems and bankruptcy.

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.