FIN303 Financial Management TMA: Investment and Finance Analysis

VerifiedAdded on 2023/01/19

|8

|1530

|24

Homework Assignment

AI Summary

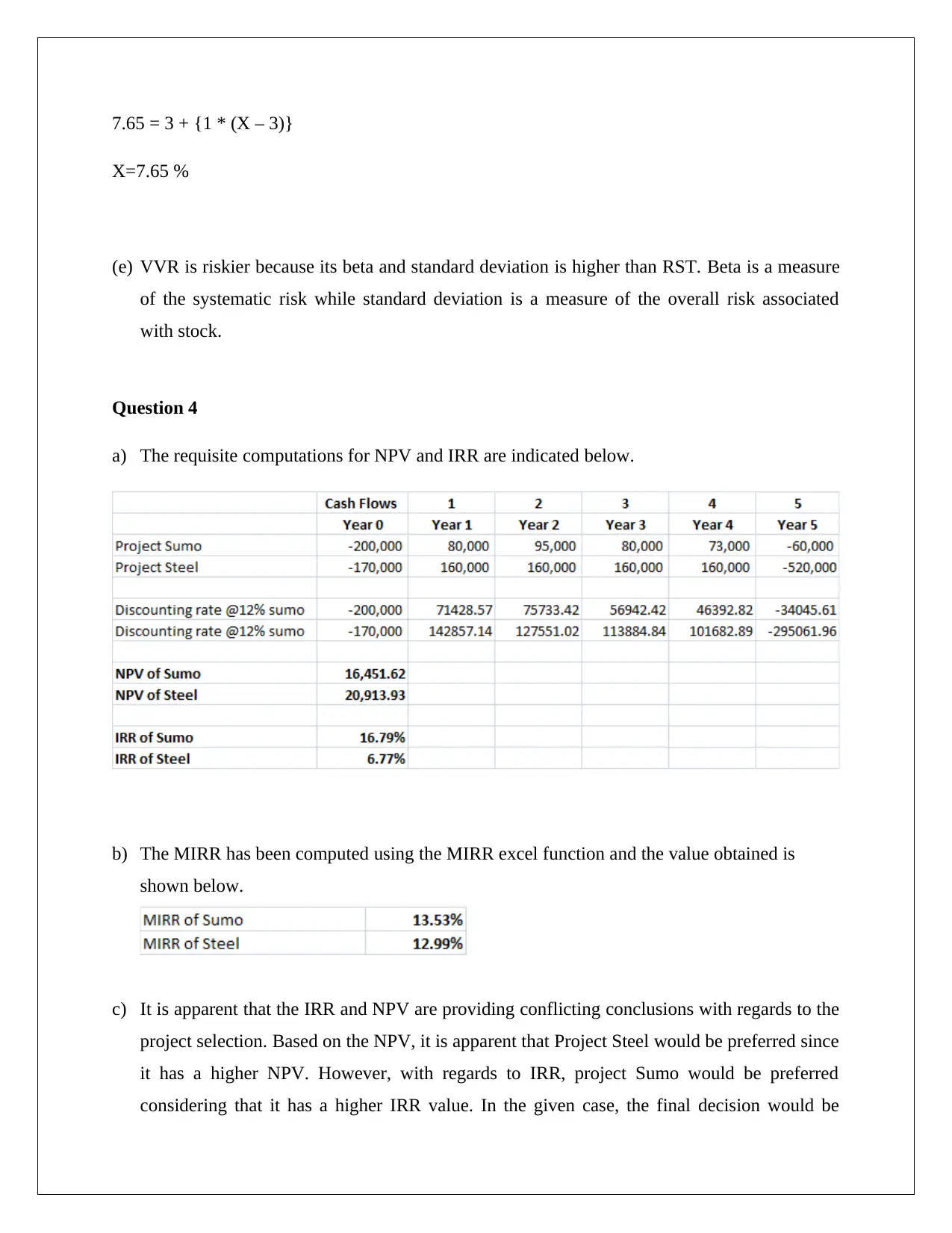

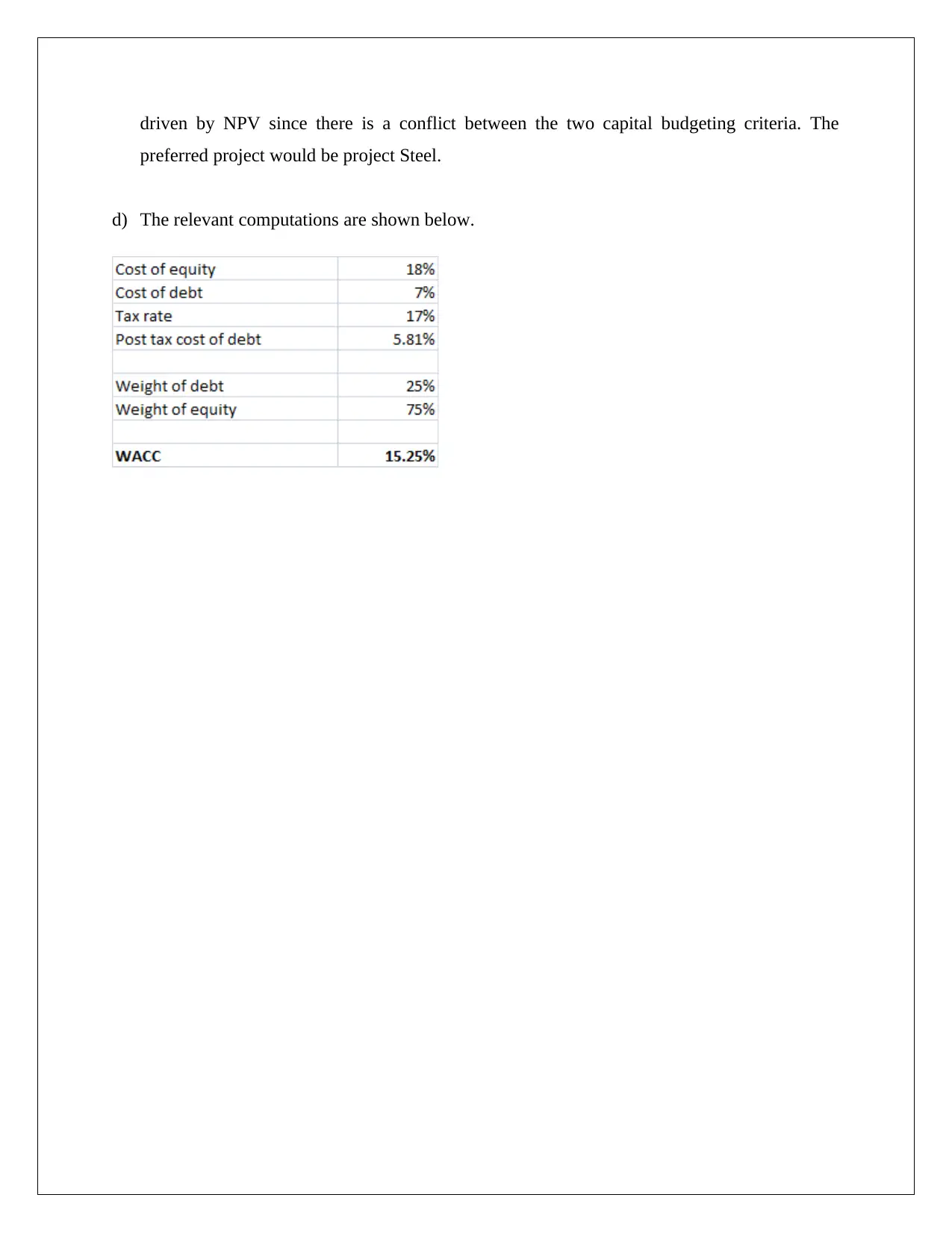

This document presents a comprehensive solution to a FIN303 Financial Management Tutor-Marked Assignment. The assignment covers a range of financial topics, including investment analysis, portfolio management, bond valuation, and the cost of equity. The solution begins with an analysis of investment products, calculating future values under different recession scenarios and comparing investment options like Product Ace and Product Bee. It then delves into bond valuation, calculating YTM and pricing bonds, along with recommendations to reduce coupon rates. The assignment continues with portfolio analysis, computing expected returns, standard deviations, and assessing portfolio risk. The solution also includes calculations for NPV, IRR, and MIRR, and concludes with a discussion of the preferred project based on the capital budgeting criteria. The document provides detailed computations, explanations, and recommendations, offering a thorough understanding of financial management principles and their practical application.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.