Stell Co Ltd Financial Accounting: Profitability Analysis and BEP

VerifiedAdded on 2023/06/11

|10

|2474

|125

Report

AI Summary

This assignment provides a comprehensive financial analysis of Stell Co Ltd, examining its profitability and financial position across two accounting years. It calculates gross and net profit, analyzes profit-to-sales ratios, and assesses the reasons for declining profits and increasing cash flow problems between 2020 and 2021. The report recommends strategies for improving the company's financial standing, including reducing unnecessary expenditure, selling unused assets, and adjusting pricing strategies. Additionally, it computes the break-even point (BEP) using the net contribution method, assesses how BEP analysis can be used for setting profitable targets, and defines how Activity-Based Budgeting (ABB) can be used for setting and monitoring short and long-term objectives. Furthermore, the report computes significant variances, identifies possible causes, projects likely consequences, and recommends strategies for business improvements, while also presenting the advantages and disadvantages of switching from Incremental Based Budgeting to Zero-Based Budgeting (ZBB).

Financial and Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

QUESTION 1

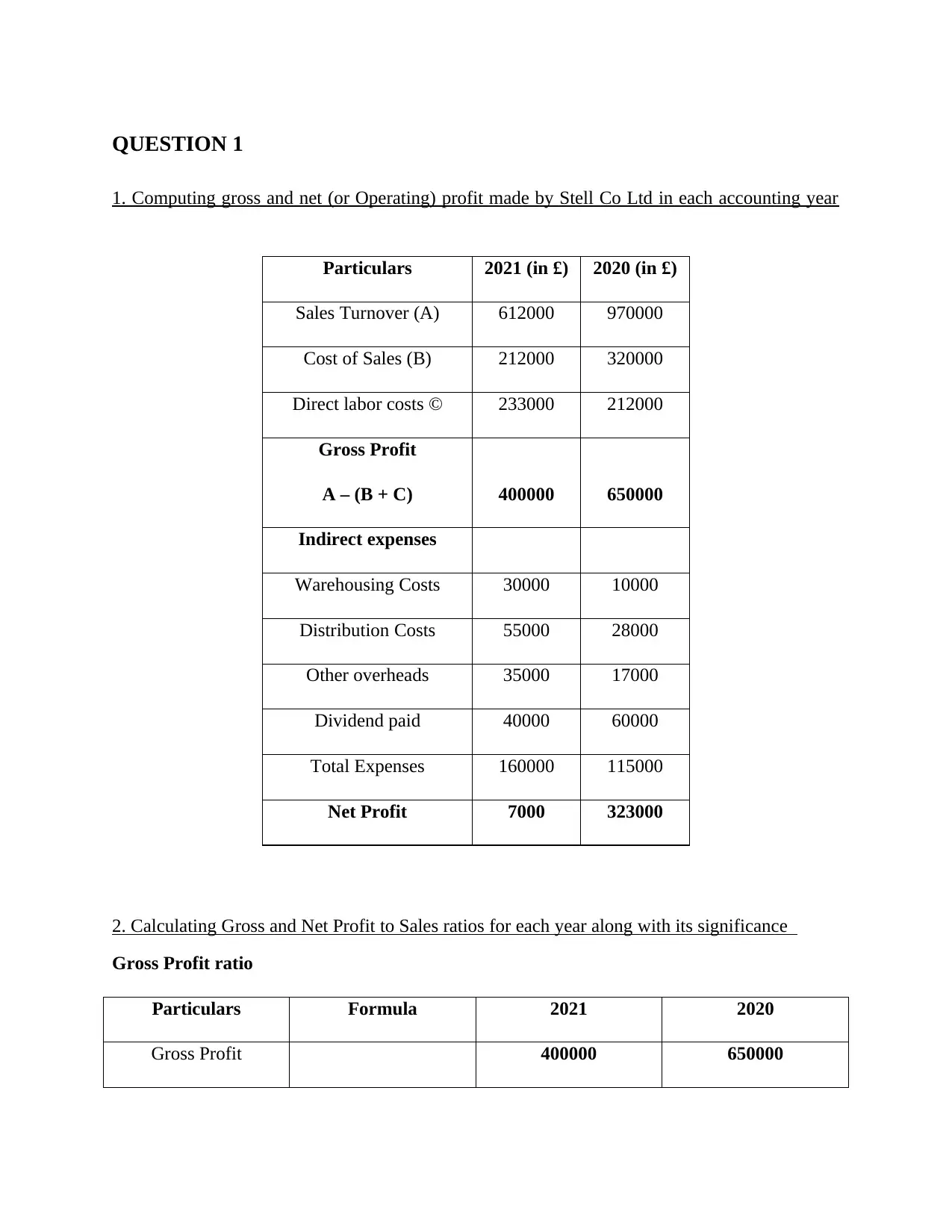

1. Computing gross and net (or Operating) profit made by Stell Co Ltd in each accounting year

Particulars 2021 (in £) 2020 (in £)

Sales Turnover (A) 612000 970000

Cost of Sales (B) 212000 320000

Direct labor costs © 233000 212000

Gross Profit

A – (B + C) 400000 650000

Indirect expenses

Warehousing Costs 30000 10000

Distribution Costs 55000 28000

Other overheads 35000 17000

Dividend paid 40000 60000

Total Expenses 160000 115000

Net Profit 7000 323000

2. Calculating Gross and Net Profit to Sales ratios for each year along with its significance

Gross Profit ratio

Particulars Formula 2021 2020

Gross Profit 400000 650000

1. Computing gross and net (or Operating) profit made by Stell Co Ltd in each accounting year

Particulars 2021 (in £) 2020 (in £)

Sales Turnover (A) 612000 970000

Cost of Sales (B) 212000 320000

Direct labor costs © 233000 212000

Gross Profit

A – (B + C) 400000 650000

Indirect expenses

Warehousing Costs 30000 10000

Distribution Costs 55000 28000

Other overheads 35000 17000

Dividend paid 40000 60000

Total Expenses 160000 115000

Net Profit 7000 323000

2. Calculating Gross and Net Profit to Sales ratios for each year along with its significance

Gross Profit ratio

Particulars Formula 2021 2020

Gross Profit 400000 650000

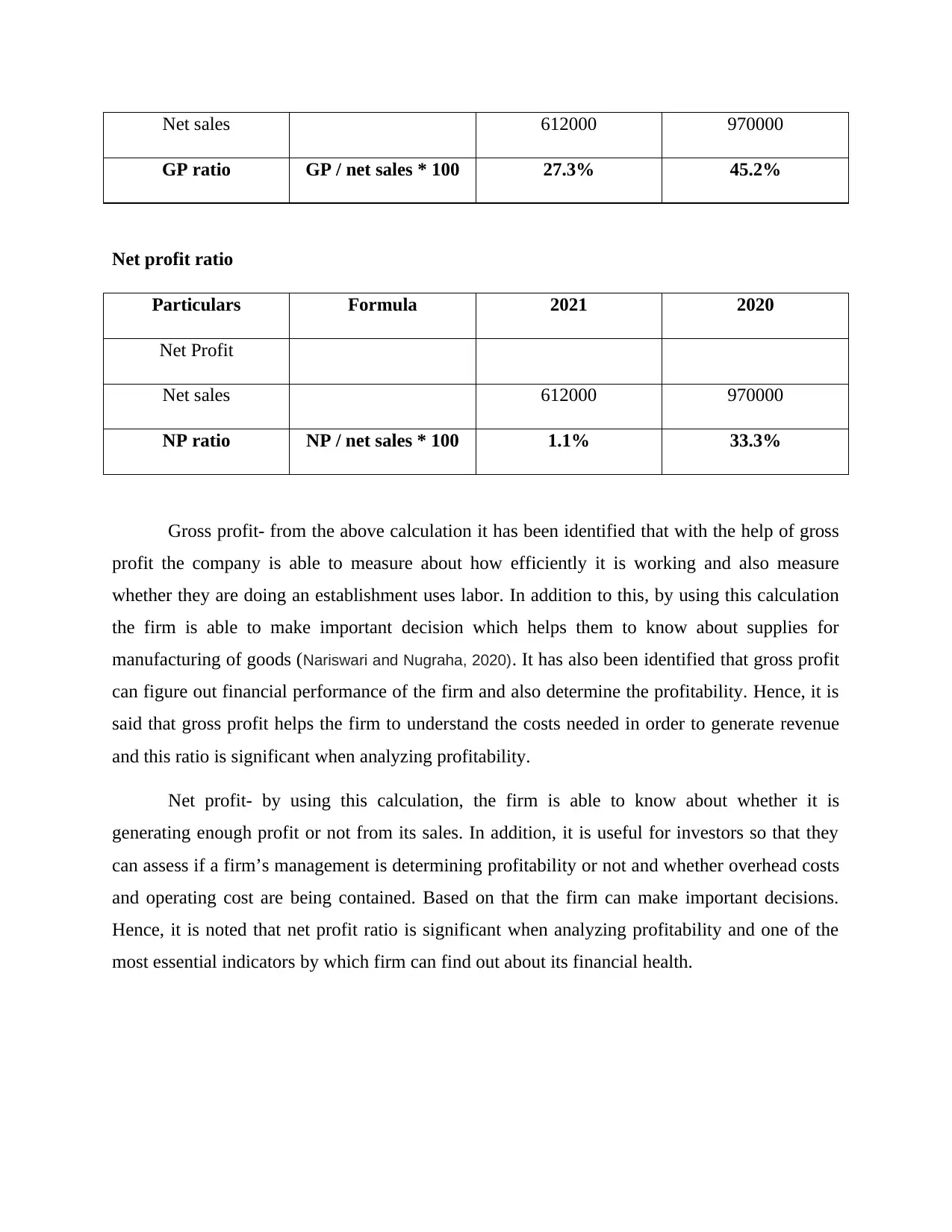

Net sales 612000 970000

GP ratio GP / net sales * 100 27.3% 45.2%

Net profit ratio

Particulars Formula 2021 2020

Net Profit

Net sales 612000 970000

NP ratio NP / net sales * 100 1.1% 33.3%

Gross profit- from the above calculation it has been identified that with the help of gross

profit the company is able to measure about how efficiently it is working and also measure

whether they are doing an establishment uses labor. In addition to this, by using this calculation

the firm is able to make important decision which helps them to know about supplies for

manufacturing of goods (Nariswari and Nugraha, 2020). It has also been identified that gross profit

can figure out financial performance of the firm and also determine the profitability. Hence, it is

said that gross profit helps the firm to understand the costs needed in order to generate revenue

and this ratio is significant when analyzing profitability.

Net profit- by using this calculation, the firm is able to know about whether it is

generating enough profit or not from its sales. In addition, it is useful for investors so that they

can assess if a firm’s management is determining profitability or not and whether overhead costs

and operating cost are being contained. Based on that the firm can make important decisions.

Hence, it is noted that net profit ratio is significant when analyzing profitability and one of the

most essential indicators by which firm can find out about its financial health.

GP ratio GP / net sales * 100 27.3% 45.2%

Net profit ratio

Particulars Formula 2021 2020

Net Profit

Net sales 612000 970000

NP ratio NP / net sales * 100 1.1% 33.3%

Gross profit- from the above calculation it has been identified that with the help of gross

profit the company is able to measure about how efficiently it is working and also measure

whether they are doing an establishment uses labor. In addition to this, by using this calculation

the firm is able to make important decision which helps them to know about supplies for

manufacturing of goods (Nariswari and Nugraha, 2020). It has also been identified that gross profit

can figure out financial performance of the firm and also determine the profitability. Hence, it is

said that gross profit helps the firm to understand the costs needed in order to generate revenue

and this ratio is significant when analyzing profitability.

Net profit- by using this calculation, the firm is able to know about whether it is

generating enough profit or not from its sales. In addition, it is useful for investors so that they

can assess if a firm’s management is determining profitability or not and whether overhead costs

and operating cost are being contained. Based on that the firm can make important decisions.

Hence, it is noted that net profit ratio is significant when analyzing profitability and one of the

most essential indicators by which firm can find out about its financial health.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

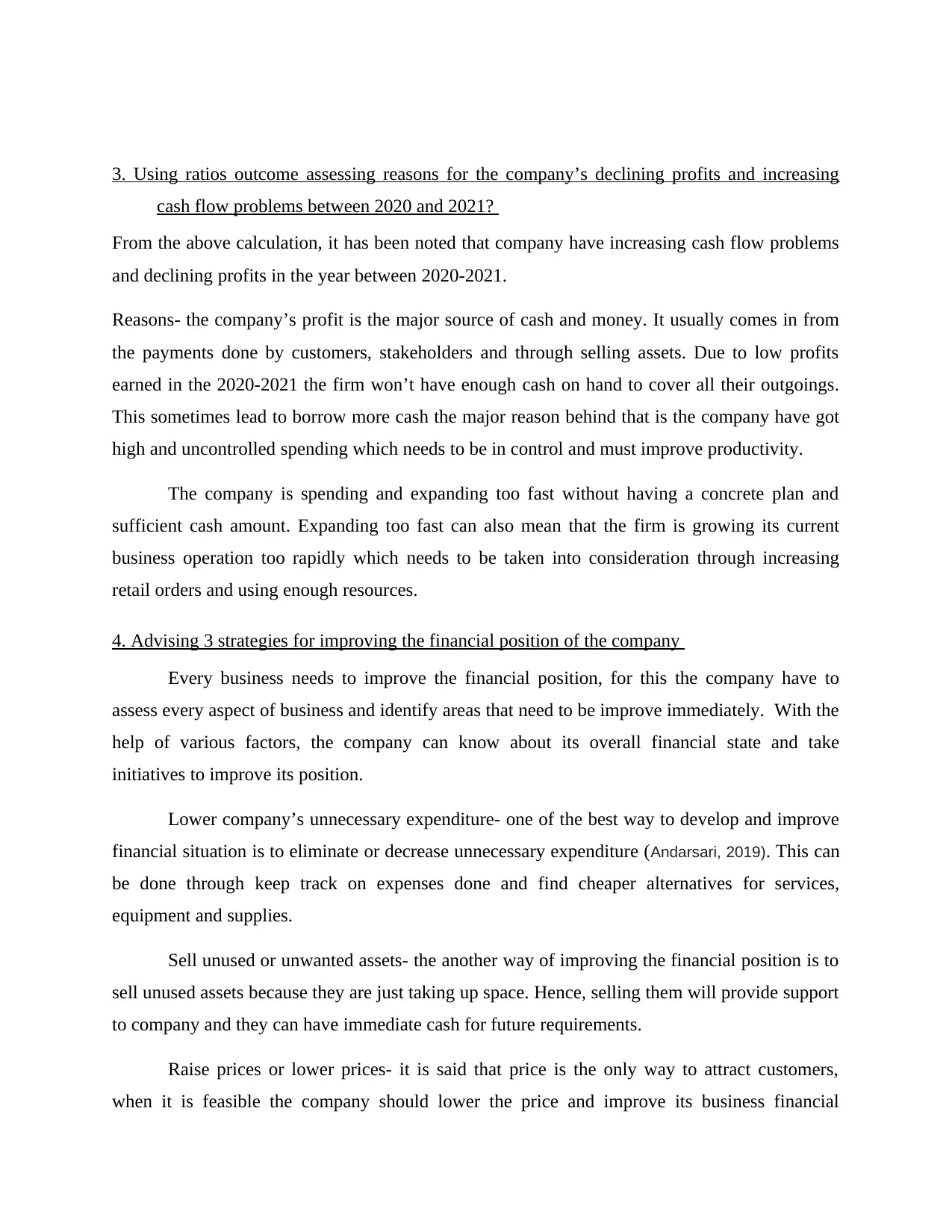

3. Using ratios outcome assessing reasons for the company’s declining profits and increasing

cash flow problems between 2020 and 2021?

From the above calculation, it has been noted that company have increasing cash flow problems

and declining profits in the year between 2020-2021.

Reasons- the company’s profit is the major source of cash and money. It usually comes in from

the payments done by customers, stakeholders and through selling assets. Due to low profits

earned in the 2020-2021 the firm won’t have enough cash on hand to cover all their outgoings.

This sometimes lead to borrow more cash the major reason behind that is the company have got

high and uncontrolled spending which needs to be in control and must improve productivity.

The company is spending and expanding too fast without having a concrete plan and

sufficient cash amount. Expanding too fast can also mean that the firm is growing its current

business operation too rapidly which needs to be taken into consideration through increasing

retail orders and using enough resources.

4. Advising 3 strategies for improving the financial position of the company

Every business needs to improve the financial position, for this the company have to

assess every aspect of business and identify areas that need to be improve immediately. With the

help of various factors, the company can know about its overall financial state and take

initiatives to improve its position.

Lower company’s unnecessary expenditure- one of the best way to develop and improve

financial situation is to eliminate or decrease unnecessary expenditure (Andarsari, 2019). This can

be done through keep track on expenses done and find cheaper alternatives for services,

equipment and supplies.

Sell unused or unwanted assets- the another way of improving the financial position is to

sell unused assets because they are just taking up space. Hence, selling them will provide support

to company and they can have immediate cash for future requirements.

Raise prices or lower prices- it is said that price is the only way to attract customers,

when it is feasible the company should lower the price and improve its business financial

cash flow problems between 2020 and 2021?

From the above calculation, it has been noted that company have increasing cash flow problems

and declining profits in the year between 2020-2021.

Reasons- the company’s profit is the major source of cash and money. It usually comes in from

the payments done by customers, stakeholders and through selling assets. Due to low profits

earned in the 2020-2021 the firm won’t have enough cash on hand to cover all their outgoings.

This sometimes lead to borrow more cash the major reason behind that is the company have got

high and uncontrolled spending which needs to be in control and must improve productivity.

The company is spending and expanding too fast without having a concrete plan and

sufficient cash amount. Expanding too fast can also mean that the firm is growing its current

business operation too rapidly which needs to be taken into consideration through increasing

retail orders and using enough resources.

4. Advising 3 strategies for improving the financial position of the company

Every business needs to improve the financial position, for this the company have to

assess every aspect of business and identify areas that need to be improve immediately. With the

help of various factors, the company can know about its overall financial state and take

initiatives to improve its position.

Lower company’s unnecessary expenditure- one of the best way to develop and improve

financial situation is to eliminate or decrease unnecessary expenditure (Andarsari, 2019). This can

be done through keep track on expenses done and find cheaper alternatives for services,

equipment and supplies.

Sell unused or unwanted assets- the another way of improving the financial position is to

sell unused assets because they are just taking up space. Hence, selling them will provide support

to company and they can have immediate cash for future requirements.

Raise prices or lower prices- it is said that price is the only way to attract customers,

when it is feasible the company should lower the price and improve its business financial

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

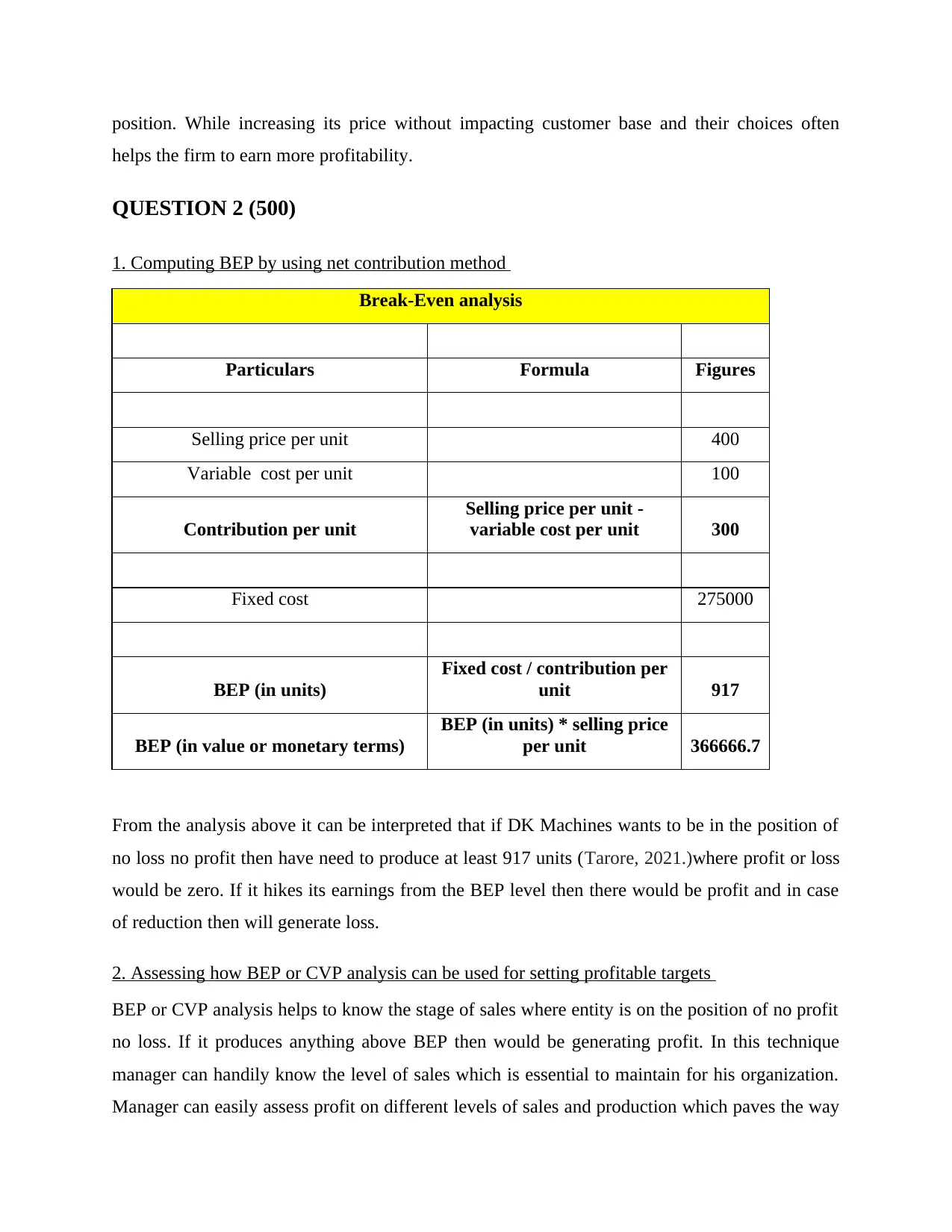

position. While increasing its price without impacting customer base and their choices often

helps the firm to earn more profitability.

QUESTION 2 (500)

1. Computing BEP by using net contribution method

Break-Even analysis

Particulars Formula Figures

Selling price per unit 400

Variable cost per unit 100

Contribution per unit

Selling price per unit -

variable cost per unit 300

Fixed cost 275000

BEP (in units)

Fixed cost / contribution per

unit 917

BEP (in value or monetary terms)

BEP (in units) * selling price

per unit 366666.7

From the analysis above it can be interpreted that if DK Machines wants to be in the position of

no loss no profit then have need to produce at least 917 units (Tarore, 2021.)where profit or loss

would be zero. If it hikes its earnings from the BEP level then there would be profit and in case

of reduction then will generate loss.

2. Assessing how BEP or CVP analysis can be used for setting profitable targets

BEP or CVP analysis helps to know the stage of sales where entity is on the position of no profit

no loss. If it produces anything above BEP then would be generating profit. In this technique

manager can handily know the level of sales which is essential to maintain for his organization.

Manager can easily assess profit on different levels of sales and production which paves the way

helps the firm to earn more profitability.

QUESTION 2 (500)

1. Computing BEP by using net contribution method

Break-Even analysis

Particulars Formula Figures

Selling price per unit 400

Variable cost per unit 100

Contribution per unit

Selling price per unit -

variable cost per unit 300

Fixed cost 275000

BEP (in units)

Fixed cost / contribution per

unit 917

BEP (in value or monetary terms)

BEP (in units) * selling price

per unit 366666.7

From the analysis above it can be interpreted that if DK Machines wants to be in the position of

no loss no profit then have need to produce at least 917 units (Tarore, 2021.)where profit or loss

would be zero. If it hikes its earnings from the BEP level then there would be profit and in case

of reduction then will generate loss.

2. Assessing how BEP or CVP analysis can be used for setting profitable targets

BEP or CVP analysis helps to know the stage of sales where entity is on the position of no profit

no loss. If it produces anything above BEP then would be generating profit. In this technique

manager can handily know the level of sales which is essential to maintain for his organization.

Manager can easily assess profit on different levels of sales and production which paves the way

for speculating the production quantity and can also reduce other sinking costs too. BEP or CVP

analysis broadly defines relationship between both variable and fixed cost so by using this

technique in a business their structure and relationship between the variable and fixed cost

factors can be easily assessed and which aids in drafting suitable policies to enhance

profitability. While setting targets one of the common error is disability of understanding effect

of cost and changes on efficiency which ultimately leads to profits, with this regard the technique

makes this relationship clear and by using the technique most appropriate and rational targets can

be set for the business and profit factor would also be maximized (Soleimani, 2018.)

3. Defining how ABB can be used for setting as well as monitoring both short & long term

objectives

ABC is a costing method in which distribution of indirect cost or overhead is made on the basis

of various cost centres and considering cost drivers. These methods pay attention to the

distribution or apportionment of indirect cost using the most appropriate methodology. In the

modern form of market in industries the share of indirect expenditure is getting higher with this

respect the method helps to set both short and long term objectives with more appropriateness

(Robbins, 2021)

Besides from setting objectives by using the ABC method monitoring on the cost centres also

becomes easy, Since while practising various factors like cost centres and their relationship with

cost drives are considered. Other aspects unit of work, even or tasks and activities are also paid

attention which makes the task of monitoring easier. Time to time on the basis of cost drivers the

costs can be pointed out which makes the task of monitoring for both short term and long term

objectives makes easier. ABC is considered more scientific method since traditional methods are

not suitable for distribution of indirect cost which ultimately create perils in deciding prices of

the products and in long run business bears bigger losses. So ABC not only eradicate those

problems but also incentivize the pricing system and operational efficiency of the organisation.

analysis broadly defines relationship between both variable and fixed cost so by using this

technique in a business their structure and relationship between the variable and fixed cost

factors can be easily assessed and which aids in drafting suitable policies to enhance

profitability. While setting targets one of the common error is disability of understanding effect

of cost and changes on efficiency which ultimately leads to profits, with this regard the technique

makes this relationship clear and by using the technique most appropriate and rational targets can

be set for the business and profit factor would also be maximized (Soleimani, 2018.)

3. Defining how ABB can be used for setting as well as monitoring both short & long term

objectives

ABC is a costing method in which distribution of indirect cost or overhead is made on the basis

of various cost centres and considering cost drivers. These methods pay attention to the

distribution or apportionment of indirect cost using the most appropriate methodology. In the

modern form of market in industries the share of indirect expenditure is getting higher with this

respect the method helps to set both short and long term objectives with more appropriateness

(Robbins, 2021)

Besides from setting objectives by using the ABC method monitoring on the cost centres also

becomes easy, Since while practising various factors like cost centres and their relationship with

cost drives are considered. Other aspects unit of work, even or tasks and activities are also paid

attention which makes the task of monitoring easier. Time to time on the basis of cost drivers the

costs can be pointed out which makes the task of monitoring for both short term and long term

objectives makes easier. ABC is considered more scientific method since traditional methods are

not suitable for distribution of indirect cost which ultimately create perils in deciding prices of

the products and in long run business bears bigger losses. So ABC not only eradicate those

problems but also incentivize the pricing system and operational efficiency of the organisation.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

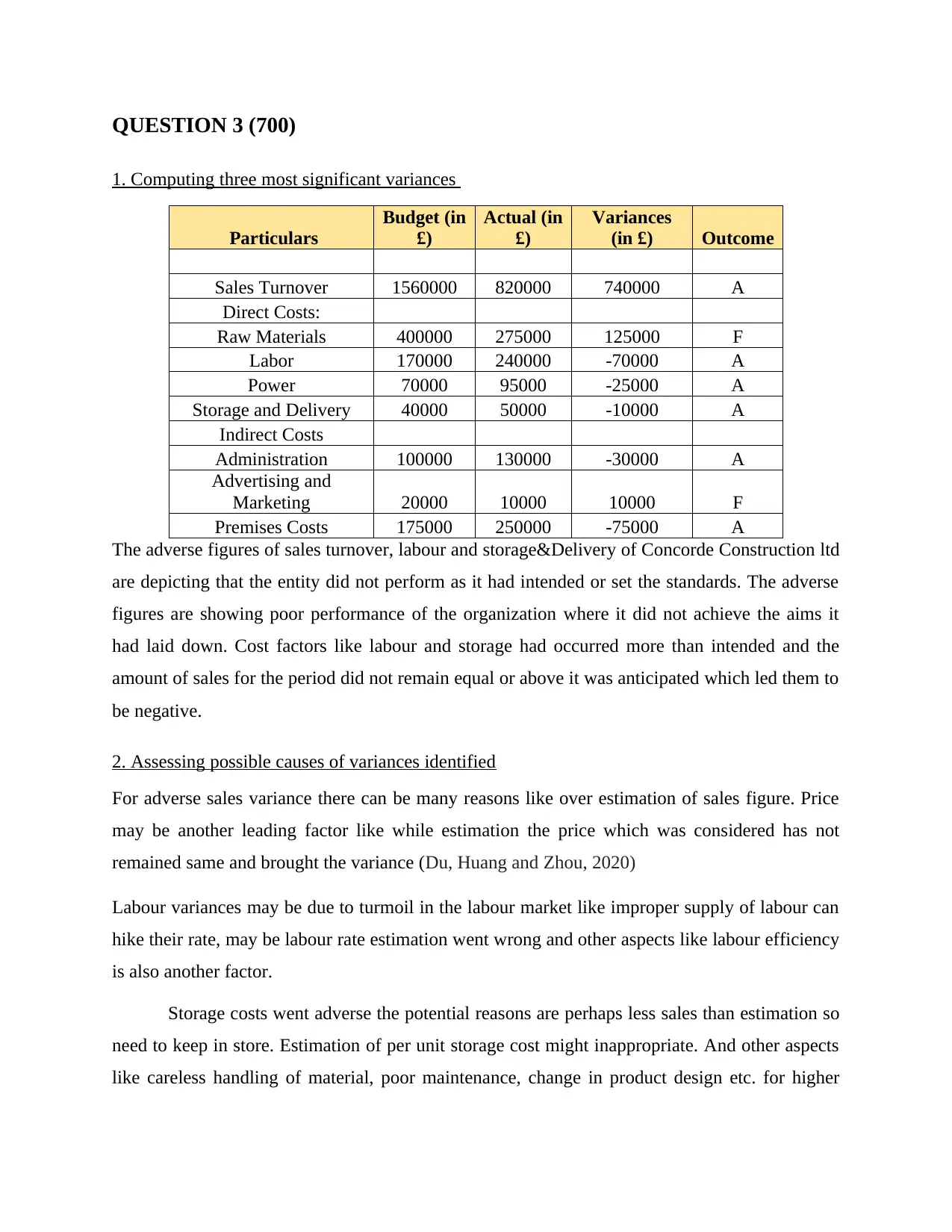

QUESTION 3 (700)

1. Computing three most significant variances

Particulars

Budget (in

£)

Actual (in

£)

Variances

(in £) Outcome

Sales Turnover 1560000 820000 740000 A

Direct Costs:

Raw Materials 400000 275000 125000 F

Labor 170000 240000 -70000 A

Power 70000 95000 -25000 A

Storage and Delivery 40000 50000 -10000 A

Indirect Costs

Administration 100000 130000 -30000 A

Advertising and

Marketing 20000 10000 10000 F

Premises Costs 175000 250000 -75000 A

The adverse figures of sales turnover, labour and storage&Delivery of Concorde Construction ltd

are depicting that the entity did not perform as it had intended or set the standards. The adverse

figures are showing poor performance of the organization where it did not achieve the aims it

had laid down. Cost factors like labour and storage had occurred more than intended and the

amount of sales for the period did not remain equal or above it was anticipated which led them to

be negative.

2. Assessing possible causes of variances identified

For adverse sales variance there can be many reasons like over estimation of sales figure. Price

may be another leading factor like while estimation the price which was considered has not

remained same and brought the variance (Du, Huang and Zhou, 2020)

Labour variances may be due to turmoil in the labour market like improper supply of labour can

hike their rate, may be labour rate estimation went wrong and other aspects like labour efficiency

is also another factor.

Storage costs went adverse the potential reasons are perhaps less sales than estimation so

need to keep in store. Estimation of per unit storage cost might inappropriate. And other aspects

like careless handling of material, poor maintenance, change in product design etc. for higher

1. Computing three most significant variances

Particulars

Budget (in

£)

Actual (in

£)

Variances

(in £) Outcome

Sales Turnover 1560000 820000 740000 A

Direct Costs:

Raw Materials 400000 275000 125000 F

Labor 170000 240000 -70000 A

Power 70000 95000 -25000 A

Storage and Delivery 40000 50000 -10000 A

Indirect Costs

Administration 100000 130000 -30000 A

Advertising and

Marketing 20000 10000 10000 F

Premises Costs 175000 250000 -75000 A

The adverse figures of sales turnover, labour and storage&Delivery of Concorde Construction ltd

are depicting that the entity did not perform as it had intended or set the standards. The adverse

figures are showing poor performance of the organization where it did not achieve the aims it

had laid down. Cost factors like labour and storage had occurred more than intended and the

amount of sales for the period did not remain equal or above it was anticipated which led them to

be negative.

2. Assessing possible causes of variances identified

For adverse sales variance there can be many reasons like over estimation of sales figure. Price

may be another leading factor like while estimation the price which was considered has not

remained same and brought the variance (Du, Huang and Zhou, 2020)

Labour variances may be due to turmoil in the labour market like improper supply of labour can

hike their rate, may be labour rate estimation went wrong and other aspects like labour efficiency

is also another factor.

Storage costs went adverse the potential reasons are perhaps less sales than estimation so

need to keep in store. Estimation of per unit storage cost might inappropriate. And other aspects

like careless handling of material, poor maintenance, change in product design etc. for higher

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

cost of delivery causes like- cost of travel, packaging and improper transportation management

may be the reasons behind.

3. Identifying projection of likely consequences for the business pertaining to each of the

variance chosen

Sales is the key elements which enshrines profits so if it is adverse then definitely take the

business to occur losses. It also brings problem of cash and liquidity which causes perils like

poor operational performance, low working capital and may also trap the business in vicious

circle of loss (Jiang, 2018)

Other adverse variances of labour and storage would hike the cost of production which

ultimately affects the prices and products with higher prices would topple the sales so the

business. Higher labour cost is bigger issue since the human element is involved. Storage cost is

mainly affected by level of sales.

4. Recommending strategies for business improvements

Concorde Construction private limited is recommended to look back the estimation practice

since all the figures are having variances either positive or negative. Budgets are needed to be

adjusted so can be more realistic in nature. Business is suggested to go for separate analysis and

contemplation over the adverse figures so can prepare separate policies for each of them.

Factors like adverse labour and storage costs ultimately leads the sales turnover so with this

regard special pondering in essential. Operational efficiency and proper management of

resources are other aspects by their use strong performance can be fetched by the business. So

these are a few strategies which are recommended for better business performance.

5. Presenting advantages disadvantages of a switch from Incremental Based Budgeting to ZBB

Advantages-

In IBB(Incremental based budgeting) former figures are used which create some

problems like dependency of resource allocation so in ZBB it can be avoided.

In fast going market trends it is better to begin with zero rather than taking previous data

and making adjustments.

may be the reasons behind.

3. Identifying projection of likely consequences for the business pertaining to each of the

variance chosen

Sales is the key elements which enshrines profits so if it is adverse then definitely take the

business to occur losses. It also brings problem of cash and liquidity which causes perils like

poor operational performance, low working capital and may also trap the business in vicious

circle of loss (Jiang, 2018)

Other adverse variances of labour and storage would hike the cost of production which

ultimately affects the prices and products with higher prices would topple the sales so the

business. Higher labour cost is bigger issue since the human element is involved. Storage cost is

mainly affected by level of sales.

4. Recommending strategies for business improvements

Concorde Construction private limited is recommended to look back the estimation practice

since all the figures are having variances either positive or negative. Budgets are needed to be

adjusted so can be more realistic in nature. Business is suggested to go for separate analysis and

contemplation over the adverse figures so can prepare separate policies for each of them.

Factors like adverse labour and storage costs ultimately leads the sales turnover so with this

regard special pondering in essential. Operational efficiency and proper management of

resources are other aspects by their use strong performance can be fetched by the business. So

these are a few strategies which are recommended for better business performance.

5. Presenting advantages disadvantages of a switch from Incremental Based Budgeting to ZBB

Advantages-

In IBB(Incremental based budgeting) former figures are used which create some

problems like dependency of resource allocation so in ZBB it can be avoided.

In fast going market trends it is better to begin with zero rather than taking previous data

and making adjustments.

ZBB also makes the task easier since without considering the previous data ones can

frame more suitable and rational plans for the business.

Disadvantages-

Incremental budgeting provides data of previous term which paves the way for making

new budgets but ZBB starts from zero which needs more resources and efforts to make

the budget.

ZBB is time taking and having unpredictable elements can mislead the budgeting process

and may be unrealistic figures (Debiasi, 2018)

Incremental budgeting keeps previous data while drafting new one. Which brings

rationality factors and also eliminate subjectivity but ZBB brings more subjectivity in

decision-making that can be a disadvantageous factor for the business.

frame more suitable and rational plans for the business.

Disadvantages-

Incremental budgeting provides data of previous term which paves the way for making

new budgets but ZBB starts from zero which needs more resources and efforts to make

the budget.

ZBB is time taking and having unpredictable elements can mislead the budgeting process

and may be unrealistic figures (Debiasi, 2018)

Incremental budgeting keeps previous data while drafting new one. Which brings

rationality factors and also eliminate subjectivity but ZBB brings more subjectivity in

decision-making that can be a disadvantageous factor for the business.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REFERENCES

Andarsari, P. R., 2019. The effect of firm size, gross profit margin and institutional ownership on

disclosure of Corporate Social Responsibility (CSR). Jurnal Apresiasi Ekonomi. 7(3). pp.301-308.

Debiasi, L., 2018, October. PRNU variance analysis for morphed face image detection. In 2018 IEEE 9th

International Conference on Biometrics Theory, Applications and Systems (BTAS) (pp. 1-9).

IEEE.

Du, G., Huang, L. and Zhou, M., 2020. Variance Analysis and Handling of Clinical Pathway:

An Overview of the State of Knowledge. IEEE Access. 8. pp.158208-158223.

Jiang, H., 2018. Single cell clustering based on cell-pair differentiability correlation and

variance analysis. Bioinformatics. 34(21). pp.3684-3694.

Nariswari, T. N. and Nugraha, N. M., 2020. Profit growth: impact of net profit margin, gross profit margin

and total assests turnover. International Journal of Finance & Banking Studies (2147-4486). 9(4). pp.87-

96.

Robbins, B. A., 2021. Random finite element analysis of backward erosion piping. Computers

and Geotechnics. 138. p.104322.

Soleimani, S., 2018. Approximate two-component incremental dynamic analysis using a

bidirectional energy-based pushover procedure. Engineering Structures. 157. pp.86-95.

Tarore, M. L. G., 2021. ANALISIS BREAK EVEN POINT (BEP) USAHATANI TOMAT DI

DESA TARAITAK I KECAMATAN LANGOWAN KABUPATEN MINAHASA

(BREAK EVEN POINT (BEP) ANALYSIS OF TOMATO FARMING BUSINESS IN

TARAITAK I VILLAGE, LANGOWAN DISTRICT, MINAHASA DISTRICT). Agri-

Sosioekonomi. 17(1). pp.85-92.

Andarsari, P. R., 2019. The effect of firm size, gross profit margin and institutional ownership on

disclosure of Corporate Social Responsibility (CSR). Jurnal Apresiasi Ekonomi. 7(3). pp.301-308.

Debiasi, L., 2018, October. PRNU variance analysis for morphed face image detection. In 2018 IEEE 9th

International Conference on Biometrics Theory, Applications and Systems (BTAS) (pp. 1-9).

IEEE.

Du, G., Huang, L. and Zhou, M., 2020. Variance Analysis and Handling of Clinical Pathway:

An Overview of the State of Knowledge. IEEE Access. 8. pp.158208-158223.

Jiang, H., 2018. Single cell clustering based on cell-pair differentiability correlation and

variance analysis. Bioinformatics. 34(21). pp.3684-3694.

Nariswari, T. N. and Nugraha, N. M., 2020. Profit growth: impact of net profit margin, gross profit margin

and total assests turnover. International Journal of Finance & Banking Studies (2147-4486). 9(4). pp.87-

96.

Robbins, B. A., 2021. Random finite element analysis of backward erosion piping. Computers

and Geotechnics. 138. p.104322.

Soleimani, S., 2018. Approximate two-component incremental dynamic analysis using a

bidirectional energy-based pushover procedure. Engineering Structures. 157. pp.86-95.

Tarore, M. L. G., 2021. ANALISIS BREAK EVEN POINT (BEP) USAHATANI TOMAT DI

DESA TARAITAK I KECAMATAN LANGOWAN KABUPATEN MINAHASA

(BREAK EVEN POINT (BEP) ANALYSIS OF TOMATO FARMING BUSINESS IN

TARAITAK I VILLAGE, LANGOWAN DISTRICT, MINAHASA DISTRICT). Agri-

Sosioekonomi. 17(1). pp.85-92.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.