Financial Health Assessment: A Report on State Trading Org. PLC

VerifiedAdded on 2023/06/10

|14

|4581

|183

Report

AI Summary

This report provides a comprehensive financial analysis of State Trading Organization PLC, focusing on its financial performance and position. It examines various long-term funding sources, including equity shares, preference shares, debentures, bank borrowings, and retained earnings, noting that 80% of the company's long-term capital is raised from equity. Despite this, the debt ratio and debt-equity ratio indicate exposure to financial risk. The analysis of financial leverage reveals that a significant portion of the capital is raised through debt, with a financial leverage of 2.07 suggesting high leverage and risk. While the company consistently pays dividends, profitability ratios show a decreasing trend. The report also touches upon dividend policies and provides insights for potential investors, recommending a cautious approach due to the identified financial risks.

Running head: FINANCIAL MANAGEMENT

Financial management

Name of the student

Name of the university

Student ID

Author note

Financial management

Name of the student

Name of the university

Student ID

Author note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1FINANCIAL MANAGEMENT

Abstract

The report focuses on the financial performance and financial position of State Trading

Organization PLC. Various long tern sources of fund available to the company as stated are

equity share, preference shares and debentures, borrowing from banks and retained earnings.

It is found that 80% of the company’s long term capital is raised from equity and only 20% of

the long term capital is raised through loans and borrowings. However, from the debt ratio

and debt equity ratio of the company it is found that the company is exposed to financial risk.

From the computation of financial leverage it is found that more than 2/3rd of the capital is

raised through debt and 1/3rd of the capital is raised through equity. Further, financial

leverage of 2.07 is indicating that the company is highly leveraged and financial risk is high.

It is further found that the company is that the company is regular in paying dividend to the

shareholders and creating return for the shareholders. However, the profitability ratios of the

company are in decreasing trend.

Abstract

The report focuses on the financial performance and financial position of State Trading

Organization PLC. Various long tern sources of fund available to the company as stated are

equity share, preference shares and debentures, borrowing from banks and retained earnings.

It is found that 80% of the company’s long term capital is raised from equity and only 20% of

the long term capital is raised through loans and borrowings. However, from the debt ratio

and debt equity ratio of the company it is found that the company is exposed to financial risk.

From the computation of financial leverage it is found that more than 2/3rd of the capital is

raised through debt and 1/3rd of the capital is raised through equity. Further, financial

leverage of 2.07 is indicating that the company is highly leveraged and financial risk is high.

It is further found that the company is that the company is regular in paying dividend to the

shareholders and creating return for the shareholders. However, the profitability ratios of the

company are in decreasing trend.

2FINANCIAL MANAGEMENT

Table of Contents

Introduction................................................................................................................................2

Availability of long-term finance...............................................................................................2

Long-term source of capital...................................................................................................2

Long-term capital structure of the company..........................................................................3

Optimum capital structure......................................................................................................4

Risk attitude...........................................................................................................................4

Leverage of the company...........................................................................................................5

Operating leverage.................................................................................................................5

Financial leverage..................................................................................................................6

Implications of findings for the investor................................................................................6

Dividend policies available to the company..............................................................................7

Dividend policy of State Trading Organization PLC.............................................................8

Profitability of the company and profitability trend..................................................................9

Conclusion and recommendation.............................................................................................10

Reference..................................................................................................................................11

Table of Contents

Introduction................................................................................................................................2

Availability of long-term finance...............................................................................................2

Long-term source of capital...................................................................................................2

Long-term capital structure of the company..........................................................................3

Optimum capital structure......................................................................................................4

Risk attitude...........................................................................................................................4

Leverage of the company...........................................................................................................5

Operating leverage.................................................................................................................5

Financial leverage..................................................................................................................6

Implications of findings for the investor................................................................................6

Dividend policies available to the company..............................................................................7

Dividend policy of State Trading Organization PLC.............................................................8

Profitability of the company and profitability trend..................................................................9

Conclusion and recommendation.............................................................................................10

Reference..................................................................................................................................11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3FINANCIAL MANAGEMENT

Introduction

State Trading Organization PLC along with the subsidiaries are engaged in

distribution, import, retail and wholesale of petroleum, construction materials and cooking

gas, pharmaceuticals, medical supplies, electronics, home appliances, insurance products and

supermarket products. The company was formerly known as Athireemaafannu Trading

Agency and during 1969 it changed its name to State Trading Organization PLC. However,

the company was established in Male, Maldives during 1964. Over the years the company

entered into wide areas of business and other trade for meeting the rising demand of the

developed nation with the growth in standards of living. Further, the company expanded

geographically, formed partnership and spun of the subsidiaries for meeting the available

opportunities. The company truly became diverse with regard to business organization

(Sto.mv, 2018).

Availability of long-term finance

Long-term source of capital

Various long-term sources available to the company are –

Equity shares – the equity shares represent the firm’s ownership capital. The company

may obtain the funds from the promoters or from public as the equity shares through

issuance of ordinary equity shares. The ordinary shareholders are those who receive

the return and dividend on the capital after payment to the preference shareholders are

made. Main advantage of equity shares is that it does not involve any fixed charges.

The company makes payment of dividends only when it earns sufficient divisible

profits (Véron & Wolff, 2016). However, legal obligation is not there to pay the

dividends. On the other hand, the main disadvantage of this is that the payment of

dividend is not deductible as expenses under tax.

Preference share – generally the preference shareholders are entitled to receive the

dividends at fixed rate before payment of other shares. Long-term fund raised from

the preference shares are done through public issue of the shares. However, it does not

have any impact on the ownership of the business and no security is required. The

characteristics of preference share involve both the characters of equity capital as well

Introduction

State Trading Organization PLC along with the subsidiaries are engaged in

distribution, import, retail and wholesale of petroleum, construction materials and cooking

gas, pharmaceuticals, medical supplies, electronics, home appliances, insurance products and

supermarket products. The company was formerly known as Athireemaafannu Trading

Agency and during 1969 it changed its name to State Trading Organization PLC. However,

the company was established in Male, Maldives during 1964. Over the years the company

entered into wide areas of business and other trade for meeting the rising demand of the

developed nation with the growth in standards of living. Further, the company expanded

geographically, formed partnership and spun of the subsidiaries for meeting the available

opportunities. The company truly became diverse with regard to business organization

(Sto.mv, 2018).

Availability of long-term finance

Long-term source of capital

Various long-term sources available to the company are –

Equity shares – the equity shares represent the firm’s ownership capital. The company

may obtain the funds from the promoters or from public as the equity shares through

issuance of ordinary equity shares. The ordinary shareholders are those who receive

the return and dividend on the capital after payment to the preference shareholders are

made. Main advantage of equity shares is that it does not involve any fixed charges.

The company makes payment of dividends only when it earns sufficient divisible

profits (Véron & Wolff, 2016). However, legal obligation is not there to pay the

dividends. On the other hand, the main disadvantage of this is that the payment of

dividend is not deductible as expenses under tax.

Preference share – generally the preference shareholders are entitled to receive the

dividends at fixed rate before payment of other shares. Long-term fund raised from

the preference shares are done through public issue of the shares. However, it does not

have any impact on the ownership of the business and no security is required. The

characteristics of preference share involve both the characters of equity capital as well

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4FINANCIAL MANAGEMENT

as debt (Peirson et al., 2014). However, like equity dividend the preference dividend

is not deductible as expenses under tax.

Debentures – it is the acknowledgement document of the debt with company’s

common seal. It includes the conditions and terms related to interest payment, loan,

redemption of loan and the offered security of the entity. Debenture holders are

regarded as the company’s creditors with no voting rights. It can be issued with or

without mortgage of any asset that means the debentures can be secured as well

unsecured (Turner, 2014). Further, the payment of debenture interest is payable even

if the company does not earn profit. However, the debenture interest is deductible

expenses under tax.

Borrowings from banks or financial institutions – many businesses raise funds

through ban loans that is more available for the growing and well established

businesses and not so for the start-up businesses. Repayment of the loan along with

interest depends on the duration and size of the loan and the interest rate. The main

advantage with the bank loan is that it does not have any impact on the ownership of

the business (Dhaliwal et al., 2014). However, the main disadvantage associated with

bank loan is that it requires security that shall be pledged with the bank.

Retained earnings – it is the undistributed part of the profits in form of the free

reserves that is used for diversification and expansion. The funds of retained earnings

are belonging to equity shareholders and it increases the business’s net worth

(Dhaliwal et al., 2016) Though it is used as the long-term finance option availability

of retained earnings depend on various factors like tax rate, company’s dividend

policy, appropriation policy of the company and extent of the profit earned.

Long-term capital structure of the company

From the annual report of State Trading Organization PLC for the year ended 2017

the long term capital structure of the company is as follows –

Type Amount Percentage

Equity 2,523,476,478.00 80%

Loans and borrowings 638,050,105.00 20%

Total 3,161,526,583.00 100%

As per above table it can be identified that 80% of the company’s long term capital is

raised from equity and only 20% of the long term capital is raised through loans and

as debt (Peirson et al., 2014). However, like equity dividend the preference dividend

is not deductible as expenses under tax.

Debentures – it is the acknowledgement document of the debt with company’s

common seal. It includes the conditions and terms related to interest payment, loan,

redemption of loan and the offered security of the entity. Debenture holders are

regarded as the company’s creditors with no voting rights. It can be issued with or

without mortgage of any asset that means the debentures can be secured as well

unsecured (Turner, 2014). Further, the payment of debenture interest is payable even

if the company does not earn profit. However, the debenture interest is deductible

expenses under tax.

Borrowings from banks or financial institutions – many businesses raise funds

through ban loans that is more available for the growing and well established

businesses and not so for the start-up businesses. Repayment of the loan along with

interest depends on the duration and size of the loan and the interest rate. The main

advantage with the bank loan is that it does not have any impact on the ownership of

the business (Dhaliwal et al., 2014). However, the main disadvantage associated with

bank loan is that it requires security that shall be pledged with the bank.

Retained earnings – it is the undistributed part of the profits in form of the free

reserves that is used for diversification and expansion. The funds of retained earnings

are belonging to equity shareholders and it increases the business’s net worth

(Dhaliwal et al., 2016) Though it is used as the long-term finance option availability

of retained earnings depend on various factors like tax rate, company’s dividend

policy, appropriation policy of the company and extent of the profit earned.

Long-term capital structure of the company

From the annual report of State Trading Organization PLC for the year ended 2017

the long term capital structure of the company is as follows –

Type Amount Percentage

Equity 2,523,476,478.00 80%

Loans and borrowings 638,050,105.00 20%

Total 3,161,526,583.00 100%

As per above table it can be identified that 80% of the company’s long term capital is

raised from equity and only 20% of the long term capital is raised through loans and

5FINANCIAL MANAGEMENT

borrowings. Rate of interest on borrowing made from various sources ranged from 5% to

9.75% and payment schedule is made till the year 2028. On the other hand, the equity

involves share capital, general reserves and retained earnings (Sto.mv, 2018).

Optimum capital structure

The optimal capital structure is the financial measurement that is used by the

company for determining best mix of the equity and debt for using in the expansion and

operation of the business. The structure lower the capital cost so that the company is less

dependent on the creditors and able to finance majorly through equity (Barton & Wiseman,

2014). Company’s capital structure can be computed through using the following ratios –

Ratio Formula 2017

Debt ratio Total liabilities / total assets 0.67

Debt equity ratio Total liabilities / total equity 2.07

Interest coverage ratio Operating profit / interest expenses 2.29

Debt ratio – it is the financial ratio used to measure the leverage extent of the company. It

measures the total debt used by the company to obtain the assets and is expressed in

percentage or decimal. From the above calculation it can be recognized that the debt ratio of

the company is 0.67 which will be considered as high (Checherita-Westphal, Hughes Hallett

& Rother, 2014).

Debt equity ratio – it states the percentage of debt and equity used by the company to finance

the assets and extent to which the equity of the shareholders can meet the creditor’s

obligation in case the business declines (Heikal, Khaddafi & Ummah, 2014). As per the

calculation the debt equity ratio of the company is 2.07 that indicate that more than 2/3rd of

the capital is raised through debt and 1/3rd of the capital is raised through equity.

Interest coverage ratio – it measures the ability of the company with regard to payment of

outstanding debt. Generally, interest coverage ratio of 2 or more is considered good and

indicates that the company is able to meet its debt obligation. The interest coverage ratio for

State Trading Organization PLC of 2.29 is indicating that the company is able to meet its debt

obligation.

Risk attitude

If the debt ratio is considered, from the perspective of pure risk 0.4 or lower debt ratio

is considered as better debt ratio. As the interest payment on debt is to be made irrespective

borrowings. Rate of interest on borrowing made from various sources ranged from 5% to

9.75% and payment schedule is made till the year 2028. On the other hand, the equity

involves share capital, general reserves and retained earnings (Sto.mv, 2018).

Optimum capital structure

The optimal capital structure is the financial measurement that is used by the

company for determining best mix of the equity and debt for using in the expansion and

operation of the business. The structure lower the capital cost so that the company is less

dependent on the creditors and able to finance majorly through equity (Barton & Wiseman,

2014). Company’s capital structure can be computed through using the following ratios –

Ratio Formula 2017

Debt ratio Total liabilities / total assets 0.67

Debt equity ratio Total liabilities / total equity 2.07

Interest coverage ratio Operating profit / interest expenses 2.29

Debt ratio – it is the financial ratio used to measure the leverage extent of the company. It

measures the total debt used by the company to obtain the assets and is expressed in

percentage or decimal. From the above calculation it can be recognized that the debt ratio of

the company is 0.67 which will be considered as high (Checherita-Westphal, Hughes Hallett

& Rother, 2014).

Debt equity ratio – it states the percentage of debt and equity used by the company to finance

the assets and extent to which the equity of the shareholders can meet the creditor’s

obligation in case the business declines (Heikal, Khaddafi & Ummah, 2014). As per the

calculation the debt equity ratio of the company is 2.07 that indicate that more than 2/3rd of

the capital is raised through debt and 1/3rd of the capital is raised through equity.

Interest coverage ratio – it measures the ability of the company with regard to payment of

outstanding debt. Generally, interest coverage ratio of 2 or more is considered good and

indicates that the company is able to meet its debt obligation. The interest coverage ratio for

State Trading Organization PLC of 2.29 is indicating that the company is able to meet its debt

obligation.

Risk attitude

If the debt ratio is considered, from the perspective of pure risk 0.4 or lower debt ratio

is considered as better debt ratio. As the interest payment on debt is to be made irrespective

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6FINANCIAL MANAGEMENT

of the profitability status of the company higher debt ratio like 0.6 or more will expose the

company to operational risk. Further, the debt equity ratio of 2.07 is indicating that the

company is highly leveraged and financial risk is high (Lebedeva et al., 2016).

Leverage of the company

The term leverage refers to borrowing or debt availed by the company for financing

the purchase of its equipment, inventory and other assets. The company can obtain the fund

through equity or debt for financing or purchasing the assets of the company. Using the debt

or leverage will increase the bankruptcy risk of the company. However, it increases the

returns of the company particularly the return on the equity. Further, payment on debt it

deductible expenses under tax and the company can establish positive history for payment

through making payment of debt in timely manner (Jarrow, 2013). From the above

calculation it can be identified that 67% of the company’s capital is raised from debt and only

33% of the capital is raised through equity. Therefore, the company will be considered as

highly leveraged as higher proportion of asset is financed through debt.

Operating leverage

It measures the fixed asset of the company as compared to the percentage of total

assets. Operating leverage matrix is used for analysing the break-even point of the business

and estimated profit levels on sale. Below mentioned two scenarios states about low

operating leverage and high operating leverage –

High operating leverage – Generally, large portion of the cost of any company are involved

fixed cost and in such cases the company earns profit for each incremental sales. However the

company shall attain enough sales volume for covering up the substantial fixed cost. If the

company can do so then it may earn high level of profit on the entire sales after paying off for

fixed cost (Kahl, Lunn & Nilsson, 2014).

Low operating leverage - large portion of the sales are considered as variable cost and

therefore the variable costs are incurred only when the sales take place. In such scenario the

entity earns smaller amount of profit on each level of incremental sales. However, the

company is not required to generate high level of sales for covering up lower amount of fixed

cost. Therefore it is easier for this kind of entity to generate the profit at lower level of sales.

However the company is not able to earn high level of profits even when it generates

additional sales.

of the profitability status of the company higher debt ratio like 0.6 or more will expose the

company to operational risk. Further, the debt equity ratio of 2.07 is indicating that the

company is highly leveraged and financial risk is high (Lebedeva et al., 2016).

Leverage of the company

The term leverage refers to borrowing or debt availed by the company for financing

the purchase of its equipment, inventory and other assets. The company can obtain the fund

through equity or debt for financing or purchasing the assets of the company. Using the debt

or leverage will increase the bankruptcy risk of the company. However, it increases the

returns of the company particularly the return on the equity. Further, payment on debt it

deductible expenses under tax and the company can establish positive history for payment

through making payment of debt in timely manner (Jarrow, 2013). From the above

calculation it can be identified that 67% of the company’s capital is raised from debt and only

33% of the capital is raised through equity. Therefore, the company will be considered as

highly leveraged as higher proportion of asset is financed through debt.

Operating leverage

It measures the fixed asset of the company as compared to the percentage of total

assets. Operating leverage matrix is used for analysing the break-even point of the business

and estimated profit levels on sale. Below mentioned two scenarios states about low

operating leverage and high operating leverage –

High operating leverage – Generally, large portion of the cost of any company are involved

fixed cost and in such cases the company earns profit for each incremental sales. However the

company shall attain enough sales volume for covering up the substantial fixed cost. If the

company can do so then it may earn high level of profit on the entire sales after paying off for

fixed cost (Kahl, Lunn & Nilsson, 2014).

Low operating leverage - large portion of the sales are considered as variable cost and

therefore the variable costs are incurred only when the sales take place. In such scenario the

entity earns smaller amount of profit on each level of incremental sales. However, the

company is not required to generate high level of sales for covering up lower amount of fixed

cost. Therefore it is easier for this kind of entity to generate the profit at lower level of sales.

However the company is not able to earn high level of profits even when it generates

additional sales.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7FINANCIAL MANAGEMENT

Operating leverage is computed through multiplying the quantity with the difference

in price and variable cost per unit and dividing it by multiplying the quantity with the

difference in price and variable cost per unit reduced by fixed operating cost.

Operating leverage = Quantity * (Price – variable cost per unit) / Quantity * (Price – variable

cost per unit) – Fixed operating cost.

However, in absence of the details regarding the variable costs and fixed costs the

operating leverage of the company could not be computed.

Financial leverage

Financial leverage is debt amount that the company uses for purchasing additional

assets. Leverage is used for avoiding usage of high level of equity funding for operation.

Excess financial leverage increases the failure risk as paying off the debt becomes difficult.

Financial leverage is computed through comparing the total debt of the company with the

total assets. if the portion of the debt as compared to the assets goes up the financial leverage

also goes up. Financial leverage will be considered as favourable if the return from debt is

higher than the expenses of interest related to the debt (Acheampong, Agalega & Shibu,

2014). Various companies use the financial leverage rather than using the equity capital

which in turn reduces the EPS for the existing shareholder. However, two major advantage of

financial leverage are –

Favourable for tax treatment – generally the interest payment on debt is deductible

under tax that lowers the debt’s net cost.

Improvement of earnings – it may also facilitate to earn the disproportionate amount

on the assets of the company.

Financial leverage of the company =

Total debt / Total equity = 52,14,346,408 / 25,23,476,478 = 2.07

Implications of findings for the investor

From the computation of financial leverage it is found that the financial leverage of

the company is 2.07. It indicates that more than 2/3rd of the capital is raised through debt and

1/3rd of the capital is raised through equity. Further, financial leverage of 2.07 is indicating

that the company is highly leveraged and financial risk is high. With the investors point of the

view the company will be regarded as more risky as the high financial leverage indicates that

Operating leverage is computed through multiplying the quantity with the difference

in price and variable cost per unit and dividing it by multiplying the quantity with the

difference in price and variable cost per unit reduced by fixed operating cost.

Operating leverage = Quantity * (Price – variable cost per unit) / Quantity * (Price – variable

cost per unit) – Fixed operating cost.

However, in absence of the details regarding the variable costs and fixed costs the

operating leverage of the company could not be computed.

Financial leverage

Financial leverage is debt amount that the company uses for purchasing additional

assets. Leverage is used for avoiding usage of high level of equity funding for operation.

Excess financial leverage increases the failure risk as paying off the debt becomes difficult.

Financial leverage is computed through comparing the total debt of the company with the

total assets. if the portion of the debt as compared to the assets goes up the financial leverage

also goes up. Financial leverage will be considered as favourable if the return from debt is

higher than the expenses of interest related to the debt (Acheampong, Agalega & Shibu,

2014). Various companies use the financial leverage rather than using the equity capital

which in turn reduces the EPS for the existing shareholder. However, two major advantage of

financial leverage are –

Favourable for tax treatment – generally the interest payment on debt is deductible

under tax that lowers the debt’s net cost.

Improvement of earnings – it may also facilitate to earn the disproportionate amount

on the assets of the company.

Financial leverage of the company =

Total debt / Total equity = 52,14,346,408 / 25,23,476,478 = 2.07

Implications of findings for the investor

From the computation of financial leverage it is found that the financial leverage of

the company is 2.07. It indicates that more than 2/3rd of the capital is raised through debt and

1/3rd of the capital is raised through equity. Further, financial leverage of 2.07 is indicating

that the company is highly leveraged and financial risk is high. With the investors point of the

view the company will be regarded as more risky as the high financial leverage indicates that

8FINANCIAL MANAGEMENT

major portion of the assets capital are funded through borrowing rather funding through own

funds. This may also state that the company’s performance is poor and therefore, it is

borrowing additional capital.

Dividend policies available to the company

Dividend policy is the approach of a company to distribute its profits to the

shareholders or owners of the company. If the company is in growth mode it is in the position

to decide that it will not pay any dividend, rather it will re-invest the profits into the business.

However, if the company decides for paying dividends it shall decide how much of the

earnings it will pay as dividends and how often it will be paid. Well established and big farms

often pay the dividend on fixed schedule however sometimes they declare the special

dividend. Payment of dividends has an impact on the perception of company in the financial

markets which in turn have direct impact on the stock price of the company. Dividend policy

guidelines are used for the company for deciding the proportion of earning that will be paid to

the shareholders as dividend (Gopalan, Nanda & Seru, 2014). Generally, the investors are not

concerned regarding the dividend policy of the company as they can sale a portion of equities

whenever they want. This is known as dividend irrelevance theory which indicates that issue

of dividend have no impact or has very little impact on the price of stock. Various dividend

policies available to the companies are as follows –

Regular Dividend policy – under this policy the investors gets the dividend at usual rate.

Generally, the investors here are the weaker sections of the society or the retired persons who

prefer regular income. This kind of dividend can be paid by the company if it has regular

income. Main advantages of this dividend policy are –

It helps to generate confidence in the shareholders

It helps to maintain the company’s goodwill

It helps to stabilize the share’s market value

It provides the shareholders with regular source of income (Hunting & Paulsen,

2013).

Stable dividend policy – under this policy certain percentage of earning is paid regularly to

the stakeholders. It is of 3 types as follows –

Constant payout ratio – the shareholders here are paid fixed earning percentage each

year as dividend

major portion of the assets capital are funded through borrowing rather funding through own

funds. This may also state that the company’s performance is poor and therefore, it is

borrowing additional capital.

Dividend policies available to the company

Dividend policy is the approach of a company to distribute its profits to the

shareholders or owners of the company. If the company is in growth mode it is in the position

to decide that it will not pay any dividend, rather it will re-invest the profits into the business.

However, if the company decides for paying dividends it shall decide how much of the

earnings it will pay as dividends and how often it will be paid. Well established and big farms

often pay the dividend on fixed schedule however sometimes they declare the special

dividend. Payment of dividends has an impact on the perception of company in the financial

markets which in turn have direct impact on the stock price of the company. Dividend policy

guidelines are used for the company for deciding the proportion of earning that will be paid to

the shareholders as dividend (Gopalan, Nanda & Seru, 2014). Generally, the investors are not

concerned regarding the dividend policy of the company as they can sale a portion of equities

whenever they want. This is known as dividend irrelevance theory which indicates that issue

of dividend have no impact or has very little impact on the price of stock. Various dividend

policies available to the companies are as follows –

Regular Dividend policy – under this policy the investors gets the dividend at usual rate.

Generally, the investors here are the weaker sections of the society or the retired persons who

prefer regular income. This kind of dividend can be paid by the company if it has regular

income. Main advantages of this dividend policy are –

It helps to generate confidence in the shareholders

It helps to maintain the company’s goodwill

It helps to stabilize the share’s market value

It provides the shareholders with regular source of income (Hunting & Paulsen,

2013).

Stable dividend policy – under this policy certain percentage of earning is paid regularly to

the stakeholders. It is of 3 types as follows –

Constant payout ratio – the shareholders here are paid fixed earning percentage each

year as dividend

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9FINANCIAL MANAGEMENT

Constant dividend per share – under this the company creates a reserve fund for

paying fixed dividend amount each year when it does not have sufficient earnings to

pay out the dividend. However, this policy is suitable for the companies those are

having stable income (Perretti, Allen & Shelton Weeks, 2013).

Main advantages of stable dividend policy are –

It helps to stabilize the share’s market value

It provides the shareholders with regular source of income

It helps to maintain the company’s goodwill

It helps to generate confidence in the shareholders

Irregular dividend – like the name, under this policy the entity does not pay dividend to the

shareholders regularly. This practice is generally used by the company for the following

reasons –

Owing to company’s uncertain earnings

Due to slow growth of the company

Lack of the liquid resources

No dividend policy – under this the company does not pay any dividend to the shareholders.

This policy is taken generally to reinvest the profit for the requirement of capital or for the

company’s growth (Naser, Nuseibeh & Rashed, 2013).

Dividend policy of State Trading Organization PLC

The company targets to pay at least 10% of the profit as dividend to the shareholders.

However, for last few years the dividend is paid at higher rate.

2017 2016 2015 2014

Earnings per share (MVR) 138.12 378 382 424

Dividend per share (MVR) 55 51 57 76

Dividend yield (%) 13.16 10.2 11.40 19.00

From the above data of the company for past 4 years it can be identified that the

company is regular in paying dividend to the shareholders and creating return for the

shareholders. EPS, dividend per share and dividend yield of the company till the year 2016

was in decreasing trend. However, the company was able to increase both dividends per share

Constant dividend per share – under this the company creates a reserve fund for

paying fixed dividend amount each year when it does not have sufficient earnings to

pay out the dividend. However, this policy is suitable for the companies those are

having stable income (Perretti, Allen & Shelton Weeks, 2013).

Main advantages of stable dividend policy are –

It helps to stabilize the share’s market value

It provides the shareholders with regular source of income

It helps to maintain the company’s goodwill

It helps to generate confidence in the shareholders

Irregular dividend – like the name, under this policy the entity does not pay dividend to the

shareholders regularly. This practice is generally used by the company for the following

reasons –

Owing to company’s uncertain earnings

Due to slow growth of the company

Lack of the liquid resources

No dividend policy – under this the company does not pay any dividend to the shareholders.

This policy is taken generally to reinvest the profit for the requirement of capital or for the

company’s growth (Naser, Nuseibeh & Rashed, 2013).

Dividend policy of State Trading Organization PLC

The company targets to pay at least 10% of the profit as dividend to the shareholders.

However, for last few years the dividend is paid at higher rate.

2017 2016 2015 2014

Earnings per share (MVR) 138.12 378 382 424

Dividend per share (MVR) 55 51 57 76

Dividend yield (%) 13.16 10.2 11.40 19.00

From the above data of the company for past 4 years it can be identified that the

company is regular in paying dividend to the shareholders and creating return for the

shareholders. EPS, dividend per share and dividend yield of the company till the year 2016

was in decreasing trend. However, the company was able to increase both dividends per share

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10FINANCIAL MANAGEMENT

and dividend yield in the year 2017, irrespective of the fact that the EPS of the company fell

significantly. Therefore, it can be stated that the dividend payment by the company for the

last 4 years are more that the target payout that is 10% (Sto.mv, 2018).

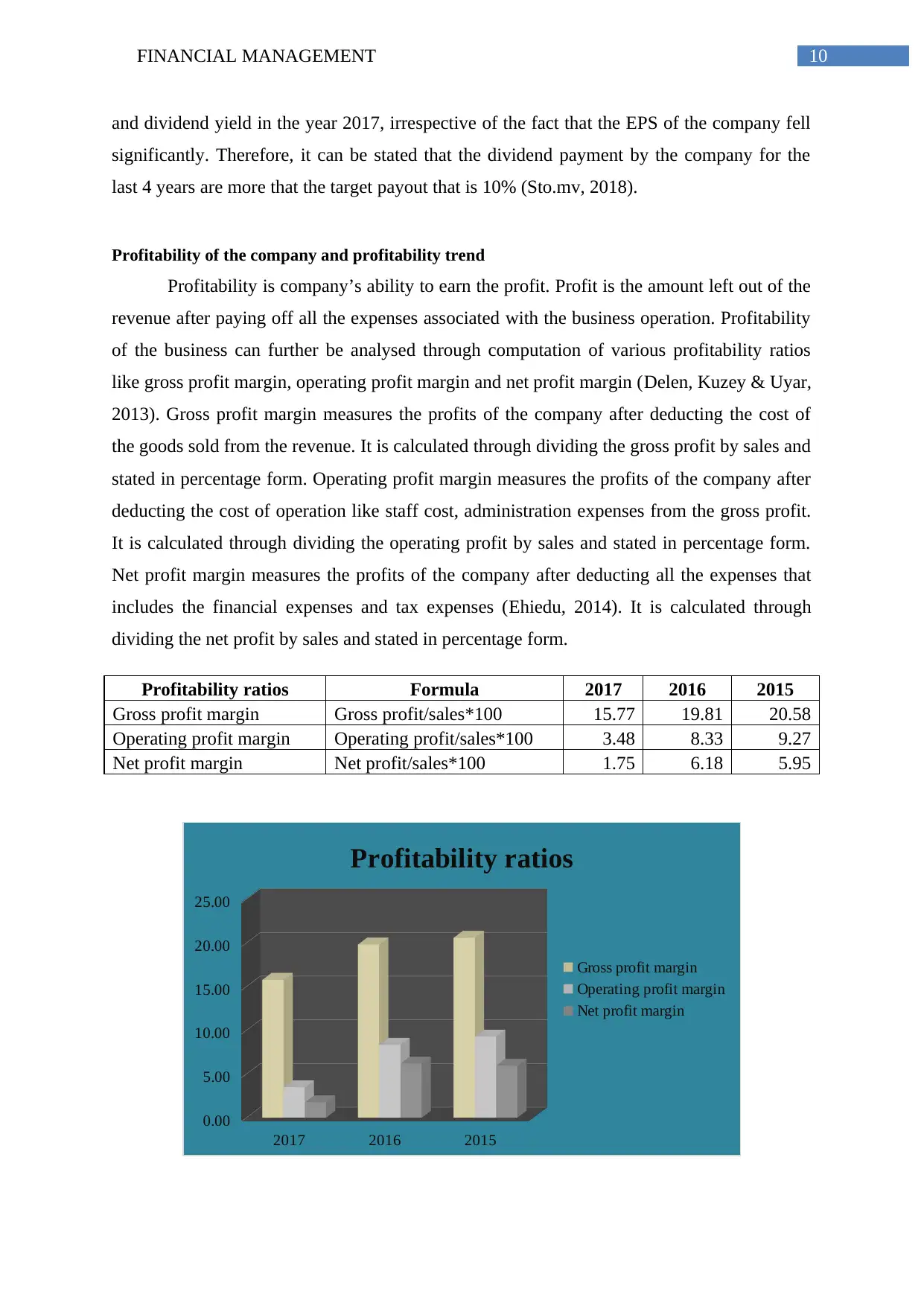

Profitability of the company and profitability trend

Profitability is company’s ability to earn the profit. Profit is the amount left out of the

revenue after paying off all the expenses associated with the business operation. Profitability

of the business can further be analysed through computation of various profitability ratios

like gross profit margin, operating profit margin and net profit margin (Delen, Kuzey & Uyar,

2013). Gross profit margin measures the profits of the company after deducting the cost of

the goods sold from the revenue. It is calculated through dividing the gross profit by sales and

stated in percentage form. Operating profit margin measures the profits of the company after

deducting the cost of operation like staff cost, administration expenses from the gross profit.

It is calculated through dividing the operating profit by sales and stated in percentage form.

Net profit margin measures the profits of the company after deducting all the expenses that

includes the financial expenses and tax expenses (Ehiedu, 2014). It is calculated through

dividing the net profit by sales and stated in percentage form.

Profitability ratios Formula 2017 2016 2015

Gross profit margin Gross profit/sales*100 15.77 19.81 20.58

Operating profit margin Operating profit/sales*100 3.48 8.33 9.27

Net profit margin Net profit/sales*100 1.75 6.18 5.95

2017 2016 2015

0.00

5.00

10.00

15.00

20.00

25.00

Profitability ratios

Gross profit margin

Operating profit margin

Net profit margin

and dividend yield in the year 2017, irrespective of the fact that the EPS of the company fell

significantly. Therefore, it can be stated that the dividend payment by the company for the

last 4 years are more that the target payout that is 10% (Sto.mv, 2018).

Profitability of the company and profitability trend

Profitability is company’s ability to earn the profit. Profit is the amount left out of the

revenue after paying off all the expenses associated with the business operation. Profitability

of the business can further be analysed through computation of various profitability ratios

like gross profit margin, operating profit margin and net profit margin (Delen, Kuzey & Uyar,

2013). Gross profit margin measures the profits of the company after deducting the cost of

the goods sold from the revenue. It is calculated through dividing the gross profit by sales and

stated in percentage form. Operating profit margin measures the profits of the company after

deducting the cost of operation like staff cost, administration expenses from the gross profit.

It is calculated through dividing the operating profit by sales and stated in percentage form.

Net profit margin measures the profits of the company after deducting all the expenses that

includes the financial expenses and tax expenses (Ehiedu, 2014). It is calculated through

dividing the net profit by sales and stated in percentage form.

Profitability ratios Formula 2017 2016 2015

Gross profit margin Gross profit/sales*100 15.77 19.81 20.58

Operating profit margin Operating profit/sales*100 3.48 8.33 9.27

Net profit margin Net profit/sales*100 1.75 6.18 5.95

2017 2016 2015

0.00

5.00

10.00

15.00

20.00

25.00

Profitability ratios

Gross profit margin

Operating profit margin

Net profit margin

11FINANCIAL MANAGEMENT

From the above table and graph it can be found out that the profitability status of the

company except the net profit for the year 2016 are in decreasing trend. The gross profit of

the company has been reduced from 20.58% to 15.7% over the period from 2015 to 2017.

Moreover, the operating profit of the company has been reduced from 9.27% to 3.48% over

the same period of time (Bauman, 2014). Though the net profit is increased from 5.95% to

6.18% over the year from 2015 to 2017, it significantly fell to 1.75% for the year ended 2017.

Therefore, all the profitability ratios of the company are in decreasing trend.

Conclusion and recommendation

From the above analysis it can be concluded that the company will be considered as

lower leveraged as 80% of the company’s long term capital is raised from equity and only

20% of the long term capital is raised through loans and borrowings. Therefore, the company

was majorly dependent on own funds rather than the creditors. Further, through the

profitability trend is reducing, the company is regular in paying dividend to the shareholders

and creating return for them. Therefore, it is recommended that the investors may consider

the stock of State Trading Organization PLC in their portfolio to get regular return through

dividends. Further, as 80% of long-term capital is raised through equity the investors will be

protected as the company is not overburdened with the interest payment for the debt.

From the above table and graph it can be found out that the profitability status of the

company except the net profit for the year 2016 are in decreasing trend. The gross profit of

the company has been reduced from 20.58% to 15.7% over the period from 2015 to 2017.

Moreover, the operating profit of the company has been reduced from 9.27% to 3.48% over

the same period of time (Bauman, 2014). Though the net profit is increased from 5.95% to

6.18% over the year from 2015 to 2017, it significantly fell to 1.75% for the year ended 2017.

Therefore, all the profitability ratios of the company are in decreasing trend.

Conclusion and recommendation

From the above analysis it can be concluded that the company will be considered as

lower leveraged as 80% of the company’s long term capital is raised from equity and only

20% of the long term capital is raised through loans and borrowings. Therefore, the company

was majorly dependent on own funds rather than the creditors. Further, through the

profitability trend is reducing, the company is regular in paying dividend to the shareholders

and creating return for them. Therefore, it is recommended that the investors may consider

the stock of State Trading Organization PLC in their portfolio to get regular return through

dividends. Further, as 80% of long-term capital is raised through equity the investors will be

protected as the company is not overburdened with the interest payment for the debt.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.