Optimizing Computer Screen Production: A Financial Management Analysis

VerifiedAdded on 2019/12/03

|13

|3347

|161

Report

AI Summary

The company is expanding its TV screen production unit to computer screen production. The gross profit and net operating income are £1,089,444.44 and £721,444.44 respectively. Under the marginal costing method, profits are £1,265,000 and £681,000. The selling price is calculated by adding a 20% profit margin to the total cost of production. The company's total cost and sales are £9,125,000 and £11,406,250 respectively. This leads to a profit of £228,125 and a profit per unit of £76.04. It can be concluded that the company can produce computer screen production, increasing business revenue and profitability.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Financial Management

and Accounting

and Accounting

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

Introduction................................................................................................................................1

FINANCIAL MANAGEMENT................................................................................................1

Raise funds through equity financing....................................................................................1

Business expansion................................................................................................................2

Calculation of WACC, NPV and IRR...................................................................................2

Management accounting.............................................................................................................5

Preparation of income statement...........................................................................................5

Calculation of selling price....................................................................................................7

CONCLUSION..........................................................................................................................8

REFERENCES...........................................................................................................................9

Introduction................................................................................................................................1

FINANCIAL MANAGEMENT................................................................................................1

Raise funds through equity financing....................................................................................1

Business expansion................................................................................................................2

Calculation of WACC, NPV and IRR...................................................................................2

Management accounting.............................................................................................................5

Preparation of income statement...........................................................................................5

Calculation of selling price....................................................................................................7

CONCLUSION..........................................................................................................................8

REFERENCES...........................................................................................................................9

INTRODUCTION

Financial management plays a vital role in the organization success. It is concerned

with efficient and effective management of the funds that helps to achieve business targets in

a great manner. It helps businesses to take effective financial decisions for the long term

sustainability of the organizations. Further, management accounting is also important as it

helps mangers in taking financial as well as non financial decisions effectively. In addition to

it, the present report describes different types of investment appraisal techniques in order to

take better investment decisions.

FINANCIAL MANAGEMENT

Raise funds through equity financing

Issue equity shares: All the entrepreneurs can raise funds through selling equity shares

in the market. Equity shareholders are considered as the owner of the company (Jenkinson

and Ljungqvist, 2001). The cost of getting funds in this way includes that equity shareholders

have controlling rights. Further, company is required to pay dividend to them.

Initial public offering (IPO): In case of newly shares, company requires to issue

initial public offering. It is an offer to the public for the sale of shares and mostly used

by companies to raise expansion (Schmid, 2001). Offering rights: Further, for acquiring additional capital, company can offer rights to

their investors (Carpenter and Petersen, 2002). It includes warrants and sweat equity

shares to the shareholders.

Personal capital: Another way of increasing the business equity funds is that

entrepreneurs can invest their personal savings and mutual funds in their business (Zezhong

and Hong, 2008). They can use their own funds for the business venture with the objectives

of bringing higher return on the investment.

Venture capital: A business organization that has good track record may provide

venture capital to the investors for acquiring funds. Before investing in the organization,

investors identify the risk and return so as to predict future business trend (Puri and Zarutskie,

2012). Thus, they provide capital to such organization that may yield greater returns.

Preference share capital: Along with the equity shares, organization also can issue

preference shares. Preferences shareholders have two rights regarding the dividend and

repayment of their capital (Rasoolpur, 2015). On contrary, shareholders have not any voting

rights hence; they cannot control the business operations. Company should issue these kinds

Financial management plays a vital role in the organization success. It is concerned

with efficient and effective management of the funds that helps to achieve business targets in

a great manner. It helps businesses to take effective financial decisions for the long term

sustainability of the organizations. Further, management accounting is also important as it

helps mangers in taking financial as well as non financial decisions effectively. In addition to

it, the present report describes different types of investment appraisal techniques in order to

take better investment decisions.

FINANCIAL MANAGEMENT

Raise funds through equity financing

Issue equity shares: All the entrepreneurs can raise funds through selling equity shares

in the market. Equity shareholders are considered as the owner of the company (Jenkinson

and Ljungqvist, 2001). The cost of getting funds in this way includes that equity shareholders

have controlling rights. Further, company is required to pay dividend to them.

Initial public offering (IPO): In case of newly shares, company requires to issue

initial public offering. It is an offer to the public for the sale of shares and mostly used

by companies to raise expansion (Schmid, 2001). Offering rights: Further, for acquiring additional capital, company can offer rights to

their investors (Carpenter and Petersen, 2002). It includes warrants and sweat equity

shares to the shareholders.

Personal capital: Another way of increasing the business equity funds is that

entrepreneurs can invest their personal savings and mutual funds in their business (Zezhong

and Hong, 2008). They can use their own funds for the business venture with the objectives

of bringing higher return on the investment.

Venture capital: A business organization that has good track record may provide

venture capital to the investors for acquiring funds. Before investing in the organization,

investors identify the risk and return so as to predict future business trend (Puri and Zarutskie,

2012). Thus, they provide capital to such organization that may yield greater returns.

Preference share capital: Along with the equity shares, organization also can issue

preference shares. Preferences shareholders have two rights regarding the dividend and

repayment of their capital (Rasoolpur, 2015). On contrary, shareholders have not any voting

rights hence; they cannot control the business operations. Company should issue these kinds

of shares if the mangers do not want to diversify the business control and have adequate

amount of profit available for dividend payments.

Business expansion

As per the given scenario, company has three options for rapid expansion over the

upcoming five years. The advantages and drawbacks are explained here as under:

1st option: Company can take loan of £10m from MidBarc Bank plc at initial annual

interest of 9%. The rate of interest is floating hence it may be possible that the rates

may be up and down in the future period (Yao, 2015). In case of higher rate, company

have to pay higher interest and vice versa. Therefore company cannot determine the

financial obligations correctly. For instance, at 9% interest rate, business requires to

pay £0.9m interest if rate goes increase to 9.25% then interest will be increased to

£0.925m. Therefore, it can increase or decrease the financial burden to the business.

However, the advantage is that if interest rates get decreases then financial obligations

also tend to decrease.

2nd Option: Company can issue Eurodollar bond worth $15m at 8% fixed interest

rate. Therefore, the yearly interest amount will be $1.2m for five years. The advantage

of this method is that company has fixed financial liability and can manage funds in

order to make timely payments. However, the disadvantage is that it creates fixed

financial burden to the company (Chakraborty and Yilmaz, 2011). For instance, if

company is facing loss then it will be a reason for financial risk to the business results

in reducing the company's financial position.

3rd Option: £10m convertible bond can be offered that will be redeemed at 6%. In

this case, company is required to make payment of £10.6m at the end of five years.

However, if company convert the bonds than it has to pay premium at 15% hence

total payments will be worth £11.5m. The advantage is that if investors convert the

bonds before maturity date than it can be converted at low and Zero coupon rate

(King and Mauer, 2014). However, disadvantage is that company is required to make

payments at premium at the point of redemption and conversion.

Calculation of WACC, NPV and IRR

Cash Flows: It is determined throough subtracting the cash expenditures to the total

cash revenues.

amount of profit available for dividend payments.

Business expansion

As per the given scenario, company has three options for rapid expansion over the

upcoming five years. The advantages and drawbacks are explained here as under:

1st option: Company can take loan of £10m from MidBarc Bank plc at initial annual

interest of 9%. The rate of interest is floating hence it may be possible that the rates

may be up and down in the future period (Yao, 2015). In case of higher rate, company

have to pay higher interest and vice versa. Therefore company cannot determine the

financial obligations correctly. For instance, at 9% interest rate, business requires to

pay £0.9m interest if rate goes increase to 9.25% then interest will be increased to

£0.925m. Therefore, it can increase or decrease the financial burden to the business.

However, the advantage is that if interest rates get decreases then financial obligations

also tend to decrease.

2nd Option: Company can issue Eurodollar bond worth $15m at 8% fixed interest

rate. Therefore, the yearly interest amount will be $1.2m for five years. The advantage

of this method is that company has fixed financial liability and can manage funds in

order to make timely payments. However, the disadvantage is that it creates fixed

financial burden to the company (Chakraborty and Yilmaz, 2011). For instance, if

company is facing loss then it will be a reason for financial risk to the business results

in reducing the company's financial position.

3rd Option: £10m convertible bond can be offered that will be redeemed at 6%. In

this case, company is required to make payment of £10.6m at the end of five years.

However, if company convert the bonds than it has to pay premium at 15% hence

total payments will be worth £11.5m. The advantage is that if investors convert the

bonds before maturity date than it can be converted at low and Zero coupon rate

(King and Mauer, 2014). However, disadvantage is that company is required to make

payments at premium at the point of redemption and conversion.

Calculation of WACC, NPV and IRR

Cash Flows: It is determined throough subtracting the cash expenditures to the total

cash revenues.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

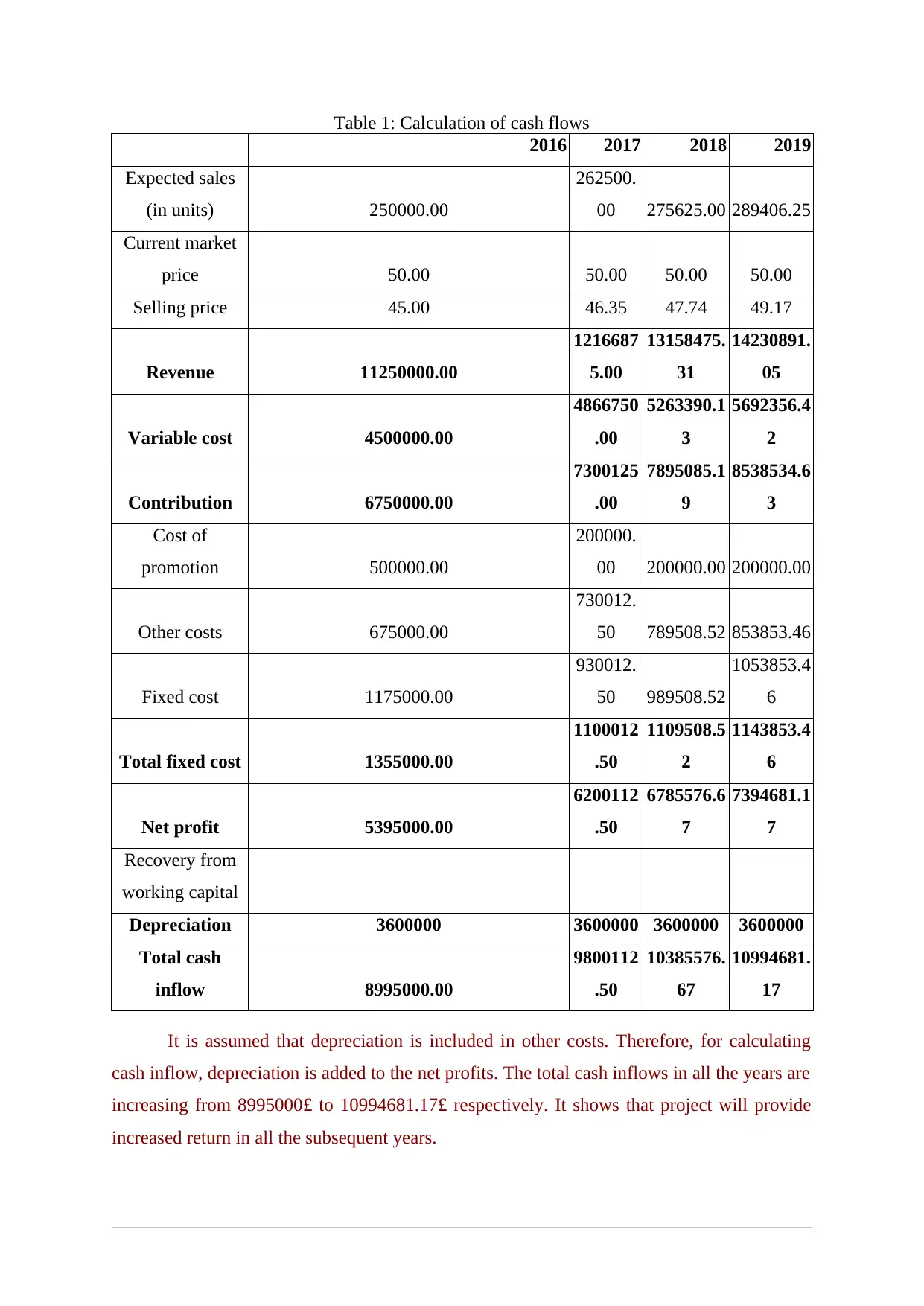

Table 1: Calculation of cash flows

2016 2017 2018 2019

Expected sales

(in units) 250000.00

262500.

00 275625.00 289406.25

Current market

price 50.00 50.00 50.00 50.00

Selling price 45.00 46.35 47.74 49.17

Revenue 11250000.00

1216687

5.00

13158475.

31

14230891.

05

Variable cost 4500000.00

4866750

.00

5263390.1

3

5692356.4

2

Contribution 6750000.00

7300125

.00

7895085.1

9

8538534.6

3

Cost of

promotion 500000.00

200000.

00 200000.00 200000.00

Other costs 675000.00

730012.

50 789508.52 853853.46

Fixed cost 1175000.00

930012.

50 989508.52

1053853.4

6

Total fixed cost 1355000.00

1100012

.50

1109508.5

2

1143853.4

6

Net profit 5395000.00

6200112

.50

6785576.6

7

7394681.1

7

Recovery from

working capital

Depreciation 3600000 3600000 3600000 3600000

Total cash

inflow 8995000.00

9800112

.50

10385576.

67

10994681.

17

It is assumed that depreciation is included in other costs. Therefore, for calculating

cash inflow, depreciation is added to the net profits. The total cash inflows in all the years are

increasing from 8995000£ to 10994681.17£ respectively. It shows that project will provide

increased return in all the subsequent years.

2016 2017 2018 2019

Expected sales

(in units) 250000.00

262500.

00 275625.00 289406.25

Current market

price 50.00 50.00 50.00 50.00

Selling price 45.00 46.35 47.74 49.17

Revenue 11250000.00

1216687

5.00

13158475.

31

14230891.

05

Variable cost 4500000.00

4866750

.00

5263390.1

3

5692356.4

2

Contribution 6750000.00

7300125

.00

7895085.1

9

8538534.6

3

Cost of

promotion 500000.00

200000.

00 200000.00 200000.00

Other costs 675000.00

730012.

50 789508.52 853853.46

Fixed cost 1175000.00

930012.

50 989508.52

1053853.4

6

Total fixed cost 1355000.00

1100012

.50

1109508.5

2

1143853.4

6

Net profit 5395000.00

6200112

.50

6785576.6

7

7394681.1

7

Recovery from

working capital

Depreciation 3600000 3600000 3600000 3600000

Total cash

inflow 8995000.00

9800112

.50

10385576.

67

10994681.

17

It is assumed that depreciation is included in other costs. Therefore, for calculating

cash inflow, depreciation is added to the net profits. The total cash inflows in all the years are

increasing from 8995000£ to 10994681.17£ respectively. It shows that project will provide

increased return in all the subsequent years.

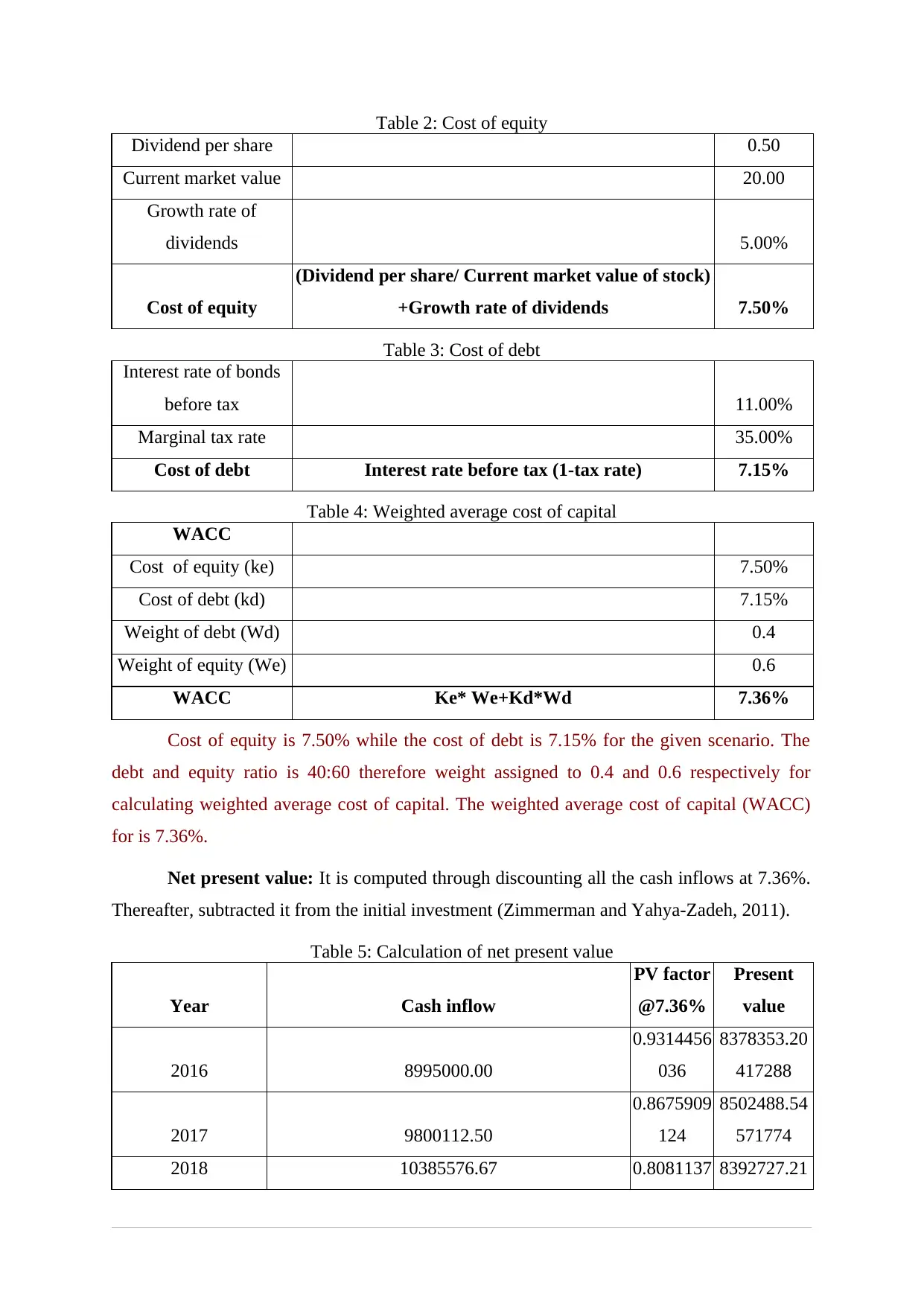

Table 2: Cost of equity

Dividend per share 0.50

Current market value 20.00

Growth rate of

dividends 5.00%

Cost of equity

(Dividend per share/ Current market value of stock)

+Growth rate of dividends 7.50%

Table 3: Cost of debt

Interest rate of bonds

before tax 11.00%

Marginal tax rate 35.00%

Cost of debt Interest rate before tax (1-tax rate) 7.15%

Table 4: Weighted average cost of capital

WACC

Cost of equity (ke) 7.50%

Cost of debt (kd) 7.15%

Weight of debt (Wd) 0.4

Weight of equity (We) 0.6

WACC Ke* We+Kd*Wd 7.36%

Cost of equity is 7.50% while the cost of debt is 7.15% for the given scenario. The

debt and equity ratio is 40:60 therefore weight assigned to 0.4 and 0.6 respectively for

calculating weighted average cost of capital. The weighted average cost of capital (WACC)

for is 7.36%.

Net present value: It is computed through discounting all the cash inflows at 7.36%.

Thereafter, subtracted it from the initial investment (Zimmerman and Yahya-Zadeh, 2011).

Table 5: Calculation of net present value

Year Cash inflow

PV factor

@7.36%

Present

value

2016 8995000.00

0.9314456

036

8378353.20

417288

2017 9800112.50

0.8675909

124

8502488.54

571774

2018 10385576.67 0.8081137 8392727.21

Dividend per share 0.50

Current market value 20.00

Growth rate of

dividends 5.00%

Cost of equity

(Dividend per share/ Current market value of stock)

+Growth rate of dividends 7.50%

Table 3: Cost of debt

Interest rate of bonds

before tax 11.00%

Marginal tax rate 35.00%

Cost of debt Interest rate before tax (1-tax rate) 7.15%

Table 4: Weighted average cost of capital

WACC

Cost of equity (ke) 7.50%

Cost of debt (kd) 7.15%

Weight of debt (Wd) 0.4

Weight of equity (We) 0.6

WACC Ke* We+Kd*Wd 7.36%

Cost of equity is 7.50% while the cost of debt is 7.15% for the given scenario. The

debt and equity ratio is 40:60 therefore weight assigned to 0.4 and 0.6 respectively for

calculating weighted average cost of capital. The weighted average cost of capital (WACC)

for is 7.36%.

Net present value: It is computed through discounting all the cash inflows at 7.36%.

Thereafter, subtracted it from the initial investment (Zimmerman and Yahya-Zadeh, 2011).

Table 5: Calculation of net present value

Year Cash inflow

PV factor

@7.36%

Present

value

2016 8995000.00

0.9314456

036

8378353.20

417288

2017 9800112.50

0.8675909

124

8502488.54

571774

2018 10385576.67 0.8081137 8392727.21

411 504677

2019 10994681.17

0.7527139

913

8275850.34

467232

2020 11110982.68

0.7011121

38

7790044.82

33262

Total present value

41339464.1

329359

Less: Initial investment 21,000,000

Net present value 20,339,464

Conclusion: According to the net present value method if the project indicate

positive net present value than the investment should be made and vice versa. As per the

given scenario, the total investment is amounted to 21000000£ however the present value of

total cash inflows is 41339464.1329359£. Therefore the investment will provide positive

return amounted to 20,339,464 at WACC 7.36%. Thus, it can be concluded that Mr. Robert

should make investment in such project. By doing this they can get return of 20339464£. on

the invested funds.

IRR: It is the rate at which the investment outlay will be equal to the discounted cash

inflows associated with the investment (Carmichael, 2011).

Table 6: Calculation of internal rate of return

Year Cash inflow

Initial investment -21,000,000

2016 8995000.00

2017 9800112.50

2018 10385576.67

2019 10994681.17

2020 11110982.68

Internal rate of return 38%

Conclusion: The decision rule of this method is that if the internal rate of return of

any project is greater than its cost of capital than funds can be invested and vice versa. In the

given scenario, it indicate that at 38% return rate the project total discounted cash inflows and

cash outflow will be same and the net present value will be zero. Further, the internal rate of

2019 10994681.17

0.7527139

913

8275850.34

467232

2020 11110982.68

0.7011121

38

7790044.82

33262

Total present value

41339464.1

329359

Less: Initial investment 21,000,000

Net present value 20,339,464

Conclusion: According to the net present value method if the project indicate

positive net present value than the investment should be made and vice versa. As per the

given scenario, the total investment is amounted to 21000000£ however the present value of

total cash inflows is 41339464.1329359£. Therefore the investment will provide positive

return amounted to 20,339,464 at WACC 7.36%. Thus, it can be concluded that Mr. Robert

should make investment in such project. By doing this they can get return of 20339464£. on

the invested funds.

IRR: It is the rate at which the investment outlay will be equal to the discounted cash

inflows associated with the investment (Carmichael, 2011).

Table 6: Calculation of internal rate of return

Year Cash inflow

Initial investment -21,000,000

2016 8995000.00

2017 9800112.50

2018 10385576.67

2019 10994681.17

2020 11110982.68

Internal rate of return 38%

Conclusion: The decision rule of this method is that if the internal rate of return of

any project is greater than its cost of capital than funds can be invested and vice versa. In the

given scenario, it indicate that at 38% return rate the project total discounted cash inflows and

cash outflow will be same and the net present value will be zero. Further, the internal rate of

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

return of the investment is 38% that is higher than cost of capital which is 7.36%. Therefore it

can be said that Mr. Robert can make invest in this project as the project provide will provide

good return to him.

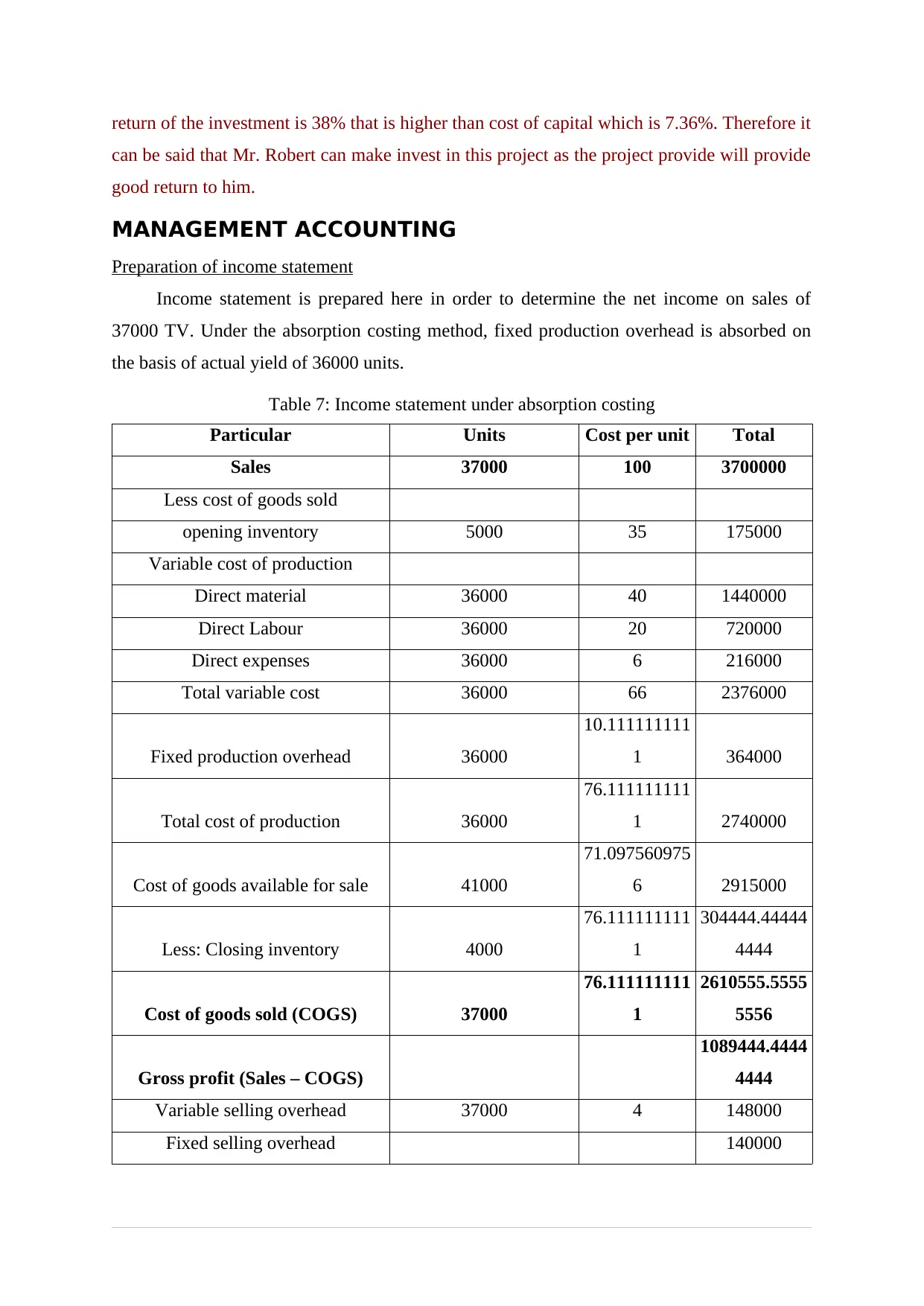

MANAGEMENT ACCOUNTING

Preparation of income statement

Income statement is prepared here in order to determine the net income on sales of

37000 TV. Under the absorption costing method, fixed production overhead is absorbed on

the basis of actual yield of 36000 units.

Table 7: Income statement under absorption costing

Particular Units Cost per unit Total

Sales 37000 100 3700000

Less cost of goods sold

opening inventory 5000 35 175000

Variable cost of production

Direct material 36000 40 1440000

Direct Labour 36000 20 720000

Direct expenses 36000 6 216000

Total variable cost 36000 66 2376000

Fixed production overhead 36000

10.111111111

1 364000

Total cost of production 36000

76.111111111

1 2740000

Cost of goods available for sale 41000

71.097560975

6 2915000

Less: Closing inventory 4000

76.111111111

1

304444.44444

4444

Cost of goods sold (COGS) 37000

76.111111111

1

2610555.5555

5556

Gross profit (Sales – COGS)

1089444.4444

4444

Variable selling overhead 37000 4 148000

Fixed selling overhead 140000

can be said that Mr. Robert can make invest in this project as the project provide will provide

good return to him.

MANAGEMENT ACCOUNTING

Preparation of income statement

Income statement is prepared here in order to determine the net income on sales of

37000 TV. Under the absorption costing method, fixed production overhead is absorbed on

the basis of actual yield of 36000 units.

Table 7: Income statement under absorption costing

Particular Units Cost per unit Total

Sales 37000 100 3700000

Less cost of goods sold

opening inventory 5000 35 175000

Variable cost of production

Direct material 36000 40 1440000

Direct Labour 36000 20 720000

Direct expenses 36000 6 216000

Total variable cost 36000 66 2376000

Fixed production overhead 36000

10.111111111

1 364000

Total cost of production 36000

76.111111111

1 2740000

Cost of goods available for sale 41000

71.097560975

6 2915000

Less: Closing inventory 4000

76.111111111

1

304444.44444

4444

Cost of goods sold (COGS) 37000

76.111111111

1

2610555.5555

5556

Gross profit (Sales – COGS)

1089444.4444

4444

Variable selling overhead 37000 4 148000

Fixed selling overhead 140000

Fixed administration overhead 80000

Total 368000

Net operating income 37000

721444.44444

4445

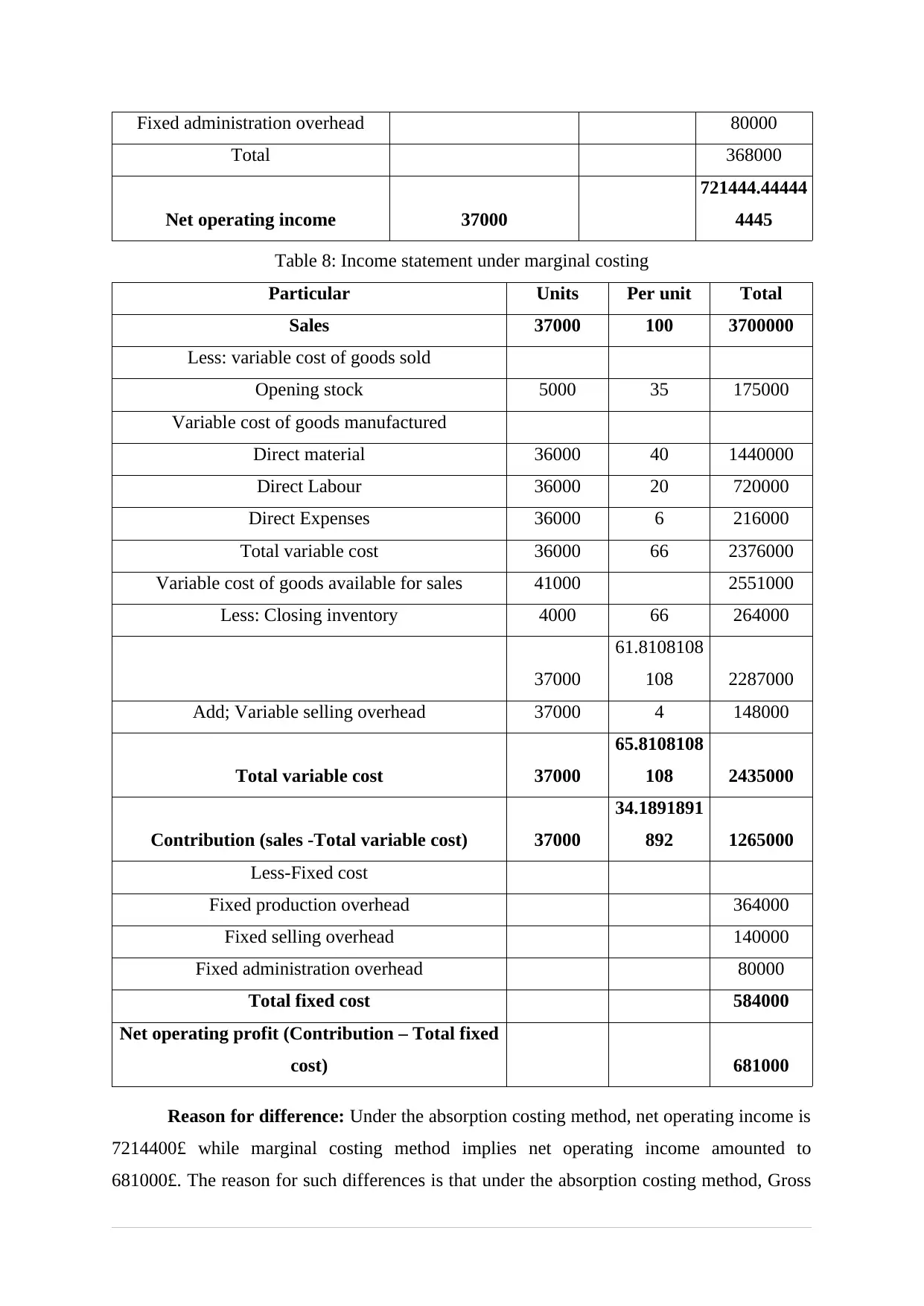

Table 8: Income statement under marginal costing

Particular Units Per unit Total

Sales 37000 100 3700000

Less: variable cost of goods sold

Opening stock 5000 35 175000

Variable cost of goods manufactured

Direct material 36000 40 1440000

Direct Labour 36000 20 720000

Direct Expenses 36000 6 216000

Total variable cost 36000 66 2376000

Variable cost of goods available for sales 41000 2551000

Less: Closing inventory 4000 66 264000

37000

61.8108108

108 2287000

Add; Variable selling overhead 37000 4 148000

Total variable cost 37000

65.8108108

108 2435000

Contribution (sales -Total variable cost) 37000

34.1891891

892 1265000

Less-Fixed cost

Fixed production overhead 364000

Fixed selling overhead 140000

Fixed administration overhead 80000

Total fixed cost 584000

Net operating profit (Contribution – Total fixed

cost) 681000

Reason for difference: Under the absorption costing method, net operating income is

7214400£ while marginal costing method implies net operating income amounted to

681000£. The reason for such differences is that under the absorption costing method, Gross

Total 368000

Net operating income 37000

721444.44444

4445

Table 8: Income statement under marginal costing

Particular Units Per unit Total

Sales 37000 100 3700000

Less: variable cost of goods sold

Opening stock 5000 35 175000

Variable cost of goods manufactured

Direct material 36000 40 1440000

Direct Labour 36000 20 720000

Direct Expenses 36000 6 216000

Total variable cost 36000 66 2376000

Variable cost of goods available for sales 41000 2551000

Less: Closing inventory 4000 66 264000

37000

61.8108108

108 2287000

Add; Variable selling overhead 37000 4 148000

Total variable cost 37000

65.8108108

108 2435000

Contribution (sales -Total variable cost) 37000

34.1891891

892 1265000

Less-Fixed cost

Fixed production overhead 364000

Fixed selling overhead 140000

Fixed administration overhead 80000

Total fixed cost 584000

Net operating profit (Contribution – Total fixed

cost) 681000

Reason for difference: Under the absorption costing method, net operating income is

7214400£ while marginal costing method implies net operating income amounted to

681000£. The reason for such differences is that under the absorption costing method, Gross

profit is determined through subtracting total cost of production from the total sales.

However, operating income is the difference between gross profit and total selling and

administration overhead (DRURY, 2013). On contrary, under the marginal costing method,

total variable cost is deducted from sales so as to determine contribution. Under this method,

if the selling and variable cost are variable in nature than it must be subtracted from the sales

to calculate gross profit. However, net operating income is calculated by subtracting

contribution to the total fixed cost (Jorgensen, Patrick and Soderstrom, 2012). As per the

given scenario, the cost of goods sold under both the methods are 2610555.55£ and 2435000£

respectively. The reason for such difference is that under the absorption costing method fixed

production overhead of 364000£ are included while calculating cost of goods sold. However,

under the marginal costing method it is the deducted from the gross profit to calcualte net

operaeting income. Moreover, variable selling and distribution overhead amounted to

148000£ are included in the marginal costing method for calucalting total cost whereas under

the absorption costing method all selling and distribution expenditures are subtracted from

the gross profit in order to determine net operaeting income. Further, it is different because

under the absorption costing method closing invenotry valued at 76.11£ per unit while under

the marginal costing method it is valued at 66£ per unit. Therefore the gross profit and the net

operating income tends to very. Under the absorption costing method the gross profit and net

operating income are 1089444.44£ and 721444.44£ respectively while under the marginal

costing method the profits are 1265000£ and 681000£.

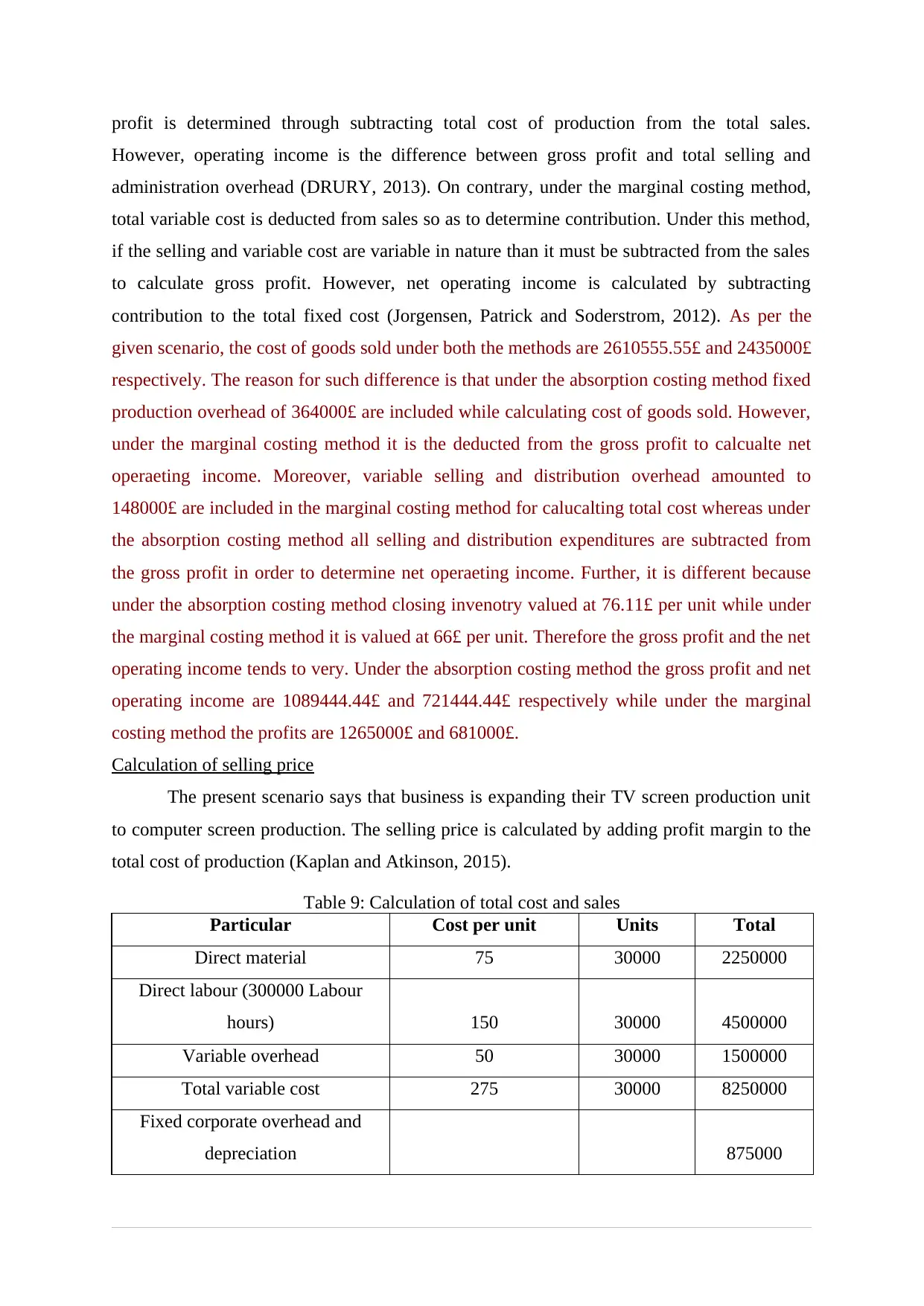

Calculation of selling price

The present scenario says that business is expanding their TV screen production unit

to computer screen production. The selling price is calculated by adding profit margin to the

total cost of production (Kaplan and Atkinson, 2015).

Table 9: Calculation of total cost and sales

Particular Cost per unit Units Total

Direct material 75 30000 2250000

Direct labour (300000 Labour

hours) 150 30000 4500000

Variable overhead 50 30000 1500000

Total variable cost 275 30000 8250000

Fixed corporate overhead and

depreciation 875000

However, operating income is the difference between gross profit and total selling and

administration overhead (DRURY, 2013). On contrary, under the marginal costing method,

total variable cost is deducted from sales so as to determine contribution. Under this method,

if the selling and variable cost are variable in nature than it must be subtracted from the sales

to calculate gross profit. However, net operating income is calculated by subtracting

contribution to the total fixed cost (Jorgensen, Patrick and Soderstrom, 2012). As per the

given scenario, the cost of goods sold under both the methods are 2610555.55£ and 2435000£

respectively. The reason for such difference is that under the absorption costing method fixed

production overhead of 364000£ are included while calculating cost of goods sold. However,

under the marginal costing method it is the deducted from the gross profit to calcualte net

operaeting income. Moreover, variable selling and distribution overhead amounted to

148000£ are included in the marginal costing method for calucalting total cost whereas under

the absorption costing method all selling and distribution expenditures are subtracted from

the gross profit in order to determine net operaeting income. Further, it is different because

under the absorption costing method closing invenotry valued at 76.11£ per unit while under

the marginal costing method it is valued at 66£ per unit. Therefore the gross profit and the net

operating income tends to very. Under the absorption costing method the gross profit and net

operating income are 1089444.44£ and 721444.44£ respectively while under the marginal

costing method the profits are 1265000£ and 681000£.

Calculation of selling price

The present scenario says that business is expanding their TV screen production unit

to computer screen production. The selling price is calculated by adding profit margin to the

total cost of production (Kaplan and Atkinson, 2015).

Table 9: Calculation of total cost and sales

Particular Cost per unit Units Total

Direct material 75 30000 2250000

Direct labour (300000 Labour

hours) 150 30000 4500000

Variable overhead 50 30000 1500000

Total variable cost 275 30000 8250000

Fixed corporate overhead and

depreciation 875000

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

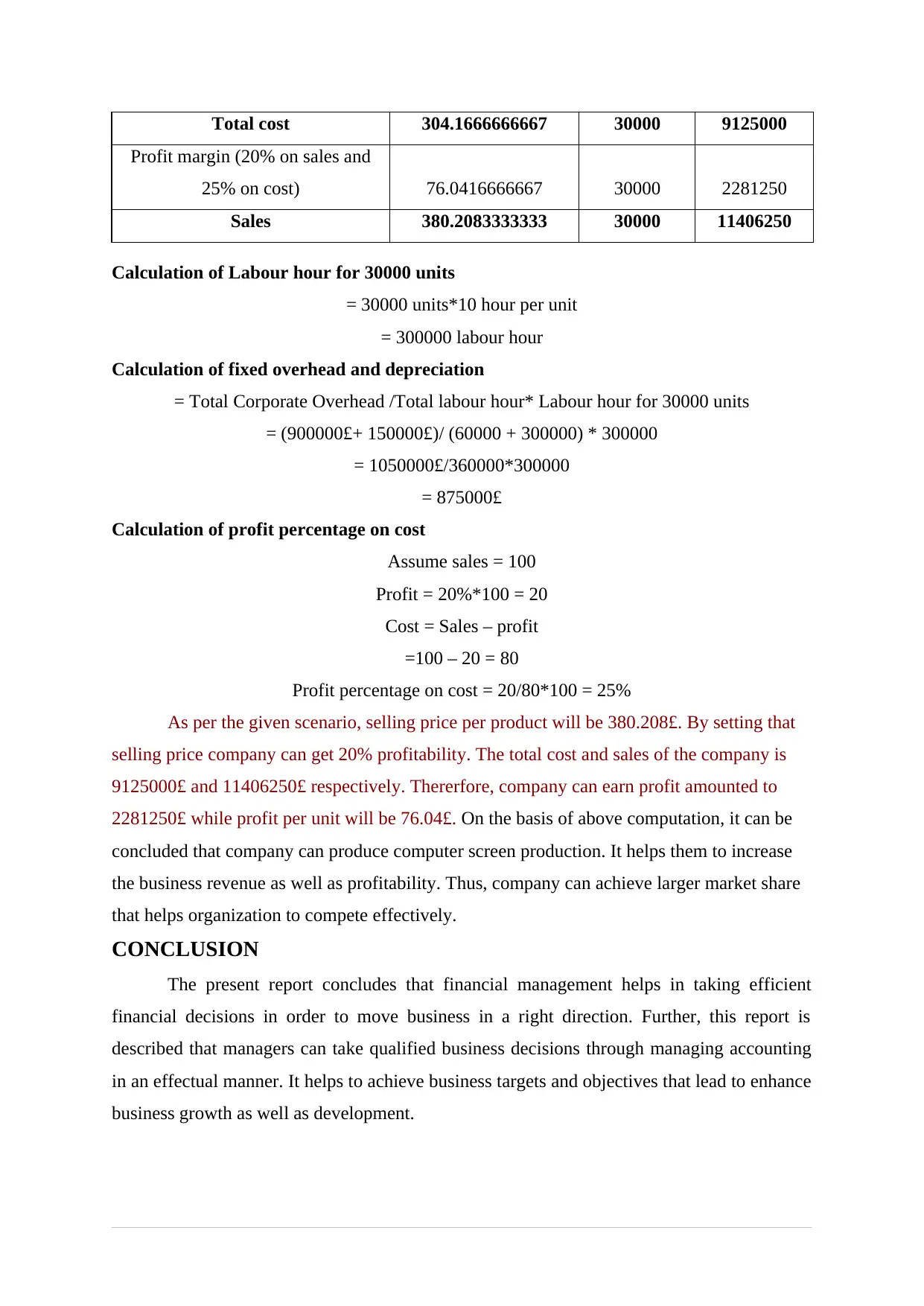

Total cost 304.1666666667 30000 9125000

Profit margin (20% on sales and

25% on cost) 76.0416666667 30000 2281250

Sales 380.2083333333 30000 11406250

Calculation of Labour hour for 30000 units

= 30000 units*10 hour per unit

= 300000 labour hour

Calculation of fixed overhead and depreciation

= Total Corporate Overhead /Total labour hour* Labour hour for 30000 units

= (900000£+ 150000£)/ (60000 + 300000) * 300000

= 1050000£/360000*300000

= 875000£

Calculation of profit percentage on cost

Assume sales = 100

Profit = 20%*100 = 20

Cost = Sales – profit

=100 – 20 = 80

Profit percentage on cost = 20/80*100 = 25%

As per the given scenario, selling price per product will be 380.208£. By setting that

selling price company can get 20% profitability. The total cost and sales of the company is

9125000£ and 11406250£ respectively. Thererfore, company can earn profit amounted to

2281250£ while profit per unit will be 76.04£. On the basis of above computation, it can be

concluded that company can produce computer screen production. It helps them to increase

the business revenue as well as profitability. Thus, company can achieve larger market share

that helps organization to compete effectively.

CONCLUSION

The present report concludes that financial management helps in taking efficient

financial decisions in order to move business in a right direction. Further, this report is

described that managers can take qualified business decisions through managing accounting

in an effectual manner. It helps to achieve business targets and objectives that lead to enhance

business growth as well as development.

Profit margin (20% on sales and

25% on cost) 76.0416666667 30000 2281250

Sales 380.2083333333 30000 11406250

Calculation of Labour hour for 30000 units

= 30000 units*10 hour per unit

= 300000 labour hour

Calculation of fixed overhead and depreciation

= Total Corporate Overhead /Total labour hour* Labour hour for 30000 units

= (900000£+ 150000£)/ (60000 + 300000) * 300000

= 1050000£/360000*300000

= 875000£

Calculation of profit percentage on cost

Assume sales = 100

Profit = 20%*100 = 20

Cost = Sales – profit

=100 – 20 = 80

Profit percentage on cost = 20/80*100 = 25%

As per the given scenario, selling price per product will be 380.208£. By setting that

selling price company can get 20% profitability. The total cost and sales of the company is

9125000£ and 11406250£ respectively. Thererfore, company can earn profit amounted to

2281250£ while profit per unit will be 76.04£. On the basis of above computation, it can be

concluded that company can produce computer screen production. It helps them to increase

the business revenue as well as profitability. Thus, company can achieve larger market share

that helps organization to compete effectively.

CONCLUSION

The present report concludes that financial management helps in taking efficient

financial decisions in order to move business in a right direction. Further, this report is

described that managers can take qualified business decisions through managing accounting

in an effectual manner. It helps to achieve business targets and objectives that lead to enhance

business growth as well as development.

REFERENCES

Books and journals

Carmichael, D.G., 2011. An alternative approach to capital investment appraisal. The

Engineering Economist. 56(2). pp.123-139.

Carpenter, R.E. and Petersen, B.C., 2002. Capital market imperfections, high‐tech

investment, and new equity financing. The Economic Journal. 112(477). pp. F54-F72.

Chakraborty, A. and Yilmaz, B., 2011. Adverse selection and convertible bonds. The Review

of Economic Studies. 78(1). pp.148-175.

DRURY, C.M., 2013. Management and cost accounting. Springer.

Jenkinson, T. and Ljungqvist, A., 2001. Going public: The theory and evidence on how

companies raise equity finance. Oxford University Press.

Jorgensen, B., Patrick, P.H. and Soderstrom, N.S., 2012, December. Overhead Cost

Measurement: Evidence from Danish Firms’ Switch from Variable to Absorption

Costing. AAA.

Kaplan, R.S. and Atkinson, A.A., 2015. Advanced management accounting. PHI Learning.

King, T.H.D. and Mauer, D.C., 2014. Determinants of corporate call policy for convertible

bonds. Journal of Corporate Finance. 24. pp.112-134.

Puri, M. and Zarutskie, R., 2012. On the life cycle dynamics of venture‐capital‐and non‐

venture‐capital‐financed firms. The Journal of Finance. 67(6). pp. 2247-2293.

Rasoolpur, G.S., 2015. Impact of Preference Share Capital on Equity Networth: An Empirical

Case from the Indian Corporate Sector. International Journal of Research in Business

and Technology. 6(3). pp. 849-855.

Yao, K., 2015. Uncertain contour process and its application in stock model with floating

interest rate. Fuzzy Optimization and Decision Making. pp.1-26.

Zezhong, X. and Hong, Z., 2008. The Determinants of Capital Structure and Equity

Financing Preference in Listed Chinese Companies [J]. Economic Research Journal. 6.

pp.119-134.

Zimmerman, J.L. and Yahya-Zadeh, M., 2011. Accounting for decision making and control.

Issues in Accounting Education. 26(1). pp.258-259.

Online

Schmid, A. F., 2001. [Pdf]. Available Through:

<https://research.stlouisfed.org/publications/review/01/11/15-28Schmid.pdf>.

[Accessed on 23rd December, 2015].

Books and journals

Carmichael, D.G., 2011. An alternative approach to capital investment appraisal. The

Engineering Economist. 56(2). pp.123-139.

Carpenter, R.E. and Petersen, B.C., 2002. Capital market imperfections, high‐tech

investment, and new equity financing. The Economic Journal. 112(477). pp. F54-F72.

Chakraborty, A. and Yilmaz, B., 2011. Adverse selection and convertible bonds. The Review

of Economic Studies. 78(1). pp.148-175.

DRURY, C.M., 2013. Management and cost accounting. Springer.

Jenkinson, T. and Ljungqvist, A., 2001. Going public: The theory and evidence on how

companies raise equity finance. Oxford University Press.

Jorgensen, B., Patrick, P.H. and Soderstrom, N.S., 2012, December. Overhead Cost

Measurement: Evidence from Danish Firms’ Switch from Variable to Absorption

Costing. AAA.

Kaplan, R.S. and Atkinson, A.A., 2015. Advanced management accounting. PHI Learning.

King, T.H.D. and Mauer, D.C., 2014. Determinants of corporate call policy for convertible

bonds. Journal of Corporate Finance. 24. pp.112-134.

Puri, M. and Zarutskie, R., 2012. On the life cycle dynamics of venture‐capital‐and non‐

venture‐capital‐financed firms. The Journal of Finance. 67(6). pp. 2247-2293.

Rasoolpur, G.S., 2015. Impact of Preference Share Capital on Equity Networth: An Empirical

Case from the Indian Corporate Sector. International Journal of Research in Business

and Technology. 6(3). pp. 849-855.

Yao, K., 2015. Uncertain contour process and its application in stock model with floating

interest rate. Fuzzy Optimization and Decision Making. pp.1-26.

Zezhong, X. and Hong, Z., 2008. The Determinants of Capital Structure and Equity

Financing Preference in Listed Chinese Companies [J]. Economic Research Journal. 6.

pp.119-134.

Zimmerman, J.L. and Yahya-Zadeh, M., 2011. Accounting for decision making and control.

Issues in Accounting Education. 26(1). pp.258-259.

Online

Schmid, A. F., 2001. [Pdf]. Available Through:

<https://research.stlouisfed.org/publications/review/01/11/15-28Schmid.pdf>.

[Accessed on 23rd December, 2015].

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.