Financial Management and Control

This assessment covers the key strategic financial statements of an organisation, evaluation of accounting information, theoretical concepts and frameworks, critical thinking and analysis of the finance function, communication skills, and processing financial data.

19 Pages4719 Words62 Views

Added on 2023-01-19

About This Document

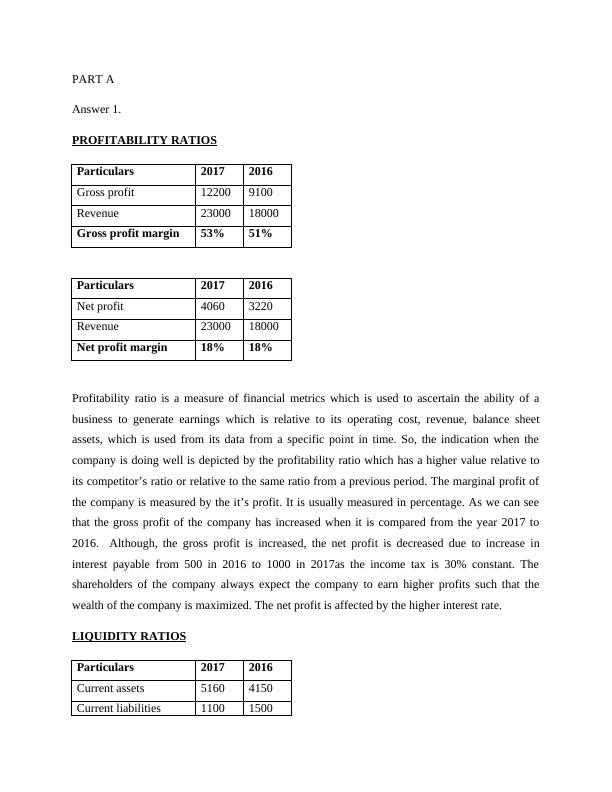

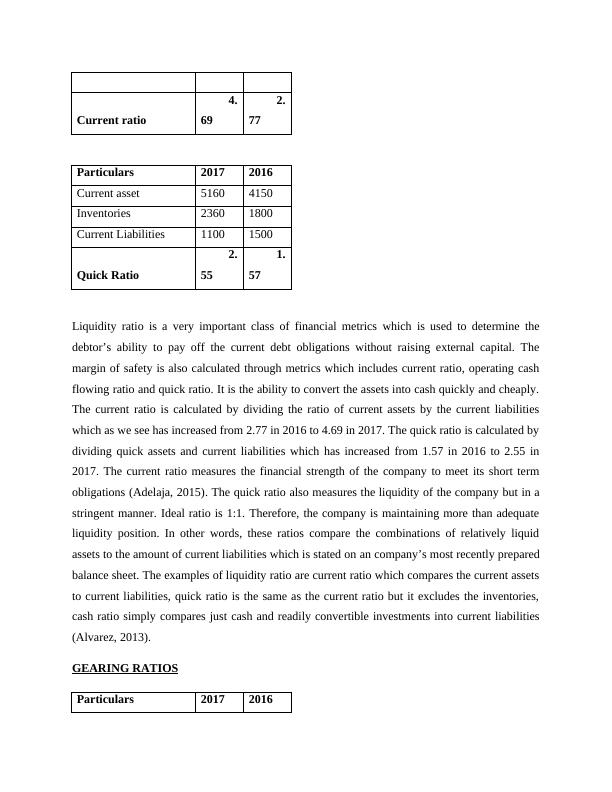

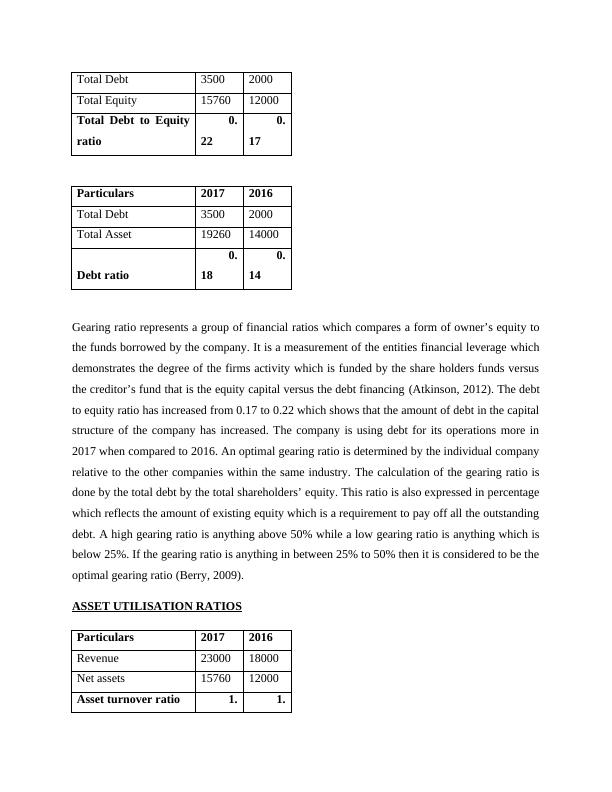

This document discusses various financial ratios such as profitability ratios, liquidity ratios, gearing ratios, asset utilization ratios, and investor potential ratio. It also explains the working capital cycle and different investment evaluation techniques.

Financial Management and Control

This assessment covers the key strategic financial statements of an organisation, evaluation of accounting information, theoretical concepts and frameworks, critical thinking and analysis of the finance function, communication skills, and processing financial data.

Added on 2023-01-19

ShareRelated Documents

End of preview

Want to access all the pages? Upload your documents or become a member.

Financial Management and Control

|19

|4439

|96

Assignment on Finance (PDF)

|9

|1405

|31

Financial Performance Analysis

|6

|1077

|152

Financial Management in Hotel and Tourism Industry

|12

|878

|77

Ratio Analysis and Financial Analysis on Wesfarmers Limited

|8

|557

|316

Statement of Profit and Loss and Balance Sheet Analysis

|12

|3099

|33