APC308 Financial Management: Investment Appraisal Techniques Report

VerifiedAdded on 2023/06/12

|14

|3966

|279

Report

AI Summary

This report provides an overview of financial management, focusing on investment appraisal techniques such as Net Present Value (NPV), Internal Rate of Return (IRR), payback period, and discounted cash flow methods. It evaluates these methods in the context of project attractiveness and profitability, including calculations and recommendations for Kings PLC. The report also discusses the benefits and drawbacks of each technique, offering insights into their practical applications and limitations in financial decision-making. Additionally, the report touches on the effects of financial proposals on firms, such as share repurchases and dividend distribution.

FINANCIAL

MANAGEMENT

MANAGEMENT

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION .........................................................................................................................3

QUESTION-2.................................................................................................................................3

A-) Evaluation of various methods in connection to the investment appraisal techniques.......3

B-) Critical evaluation of effects of proposal on the firm.........................................................6

C-) Discussion of benefits and drawbacks of different investment appraisal techniques.........6

QUESTION 3.................................................................................................................................8

A) Price earning ratio model (P/E ratio): ..................................................................................8

(B) Discounted cash flow technique .........................................................................................9

C) Dividend calculation method:...............................................................................................9

d) From the above techniques it must clear that the problems are finding while using the

various methods and give suggestion with economic explanation of kings plc......................10

CONCLUSION............................................................................................................................13

REFERENCES.............................................................................................................................14

INTRODUCTION .........................................................................................................................3

QUESTION-2.................................................................................................................................3

A-) Evaluation of various methods in connection to the investment appraisal techniques.......3

B-) Critical evaluation of effects of proposal on the firm.........................................................6

C-) Discussion of benefits and drawbacks of different investment appraisal techniques.........6

QUESTION 3.................................................................................................................................8

A) Price earning ratio model (P/E ratio): ..................................................................................8

(B) Discounted cash flow technique .........................................................................................9

C) Dividend calculation method:...............................................................................................9

d) From the above techniques it must clear that the problems are finding while using the

various methods and give suggestion with economic explanation of kings plc......................10

CONCLUSION............................................................................................................................13

REFERENCES.............................................................................................................................14

INTRODUCTION

The term financial management comprises of two words i.e. finance and management. It

refers to the tool of organising, planning, directing and controlling the financial activities of the

business organisation to maintain the appropriate utilization and maintenance of funds

(Baihaqqy and et.al., 2020). This reports looks into the various aspects that are associated with

the investment appraisal techniques and the calculations of same. In addition to this , the

following report also highlights the benefits and drawbacks associated with the various capital

budgeting methods. Moreover, this reports also holds the evaluation task in accordance with the

takeovers and mergers and also involves the estimation of price earning ratio, discounted cash

flow method and dividend valuation method. Furthermore, it also encompasses the problems

encountered in using different valuation metrics.

QUESTION-2

A-) Evaluation of various methods in connection to the investment appraisal techniques

Investment appraisal is a method by which a firm can examine the attractiveness of the

upcoming projects by using different techniques. They are- Net present value method,

profitability index, Accounting rate of return method, and payback period. These techniques

provide valuable insights on the project acceptability and profitability.

Payback Period- This means the amount of time taken to recoup the initial cost of investment

on a project. Or, it can also be elaborated as the length of time taken by an investor to reach the

break-even point. If the payback period is shorter then it is considered that the investment shall

be made on that project, but if the payback period is longer than it is not an attractive

investment and hence it shall be rejected (Dalal and Thaker, 2019.). The evaluation using this

method is carried out through dividing the amount of investment by the annual cash flow. This

tool is mainly used by the investors and corporates to calculate the return on investments and is

beneficial in helping the firm by providing them the base for decision making.

Year Annual Cash

Inflow

Annual Cash

Outflow

Annual Net cash

flows

Cumulative cash

flows

The term financial management comprises of two words i.e. finance and management. It

refers to the tool of organising, planning, directing and controlling the financial activities of the

business organisation to maintain the appropriate utilization and maintenance of funds

(Baihaqqy and et.al., 2020). This reports looks into the various aspects that are associated with

the investment appraisal techniques and the calculations of same. In addition to this , the

following report also highlights the benefits and drawbacks associated with the various capital

budgeting methods. Moreover, this reports also holds the evaluation task in accordance with the

takeovers and mergers and also involves the estimation of price earning ratio, discounted cash

flow method and dividend valuation method. Furthermore, it also encompasses the problems

encountered in using different valuation metrics.

QUESTION-2

A-) Evaluation of various methods in connection to the investment appraisal techniques

Investment appraisal is a method by which a firm can examine the attractiveness of the

upcoming projects by using different techniques. They are- Net present value method,

profitability index, Accounting rate of return method, and payback period. These techniques

provide valuable insights on the project acceptability and profitability.

Payback Period- This means the amount of time taken to recoup the initial cost of investment

on a project. Or, it can also be elaborated as the length of time taken by an investor to reach the

break-even point. If the payback period is shorter then it is considered that the investment shall

be made on that project, but if the payback period is longer than it is not an attractive

investment and hence it shall be rejected (Dalal and Thaker, 2019.). The evaluation using this

method is carried out through dividing the amount of investment by the annual cash flow. This

tool is mainly used by the investors and corporates to calculate the return on investments and is

beneficial in helping the firm by providing them the base for decision making.

Year Annual Cash

Inflow

Annual Cash

Outflow

Annual Net cash

flows

Cumulative cash

flows

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

0 -588.5 -588.5 0

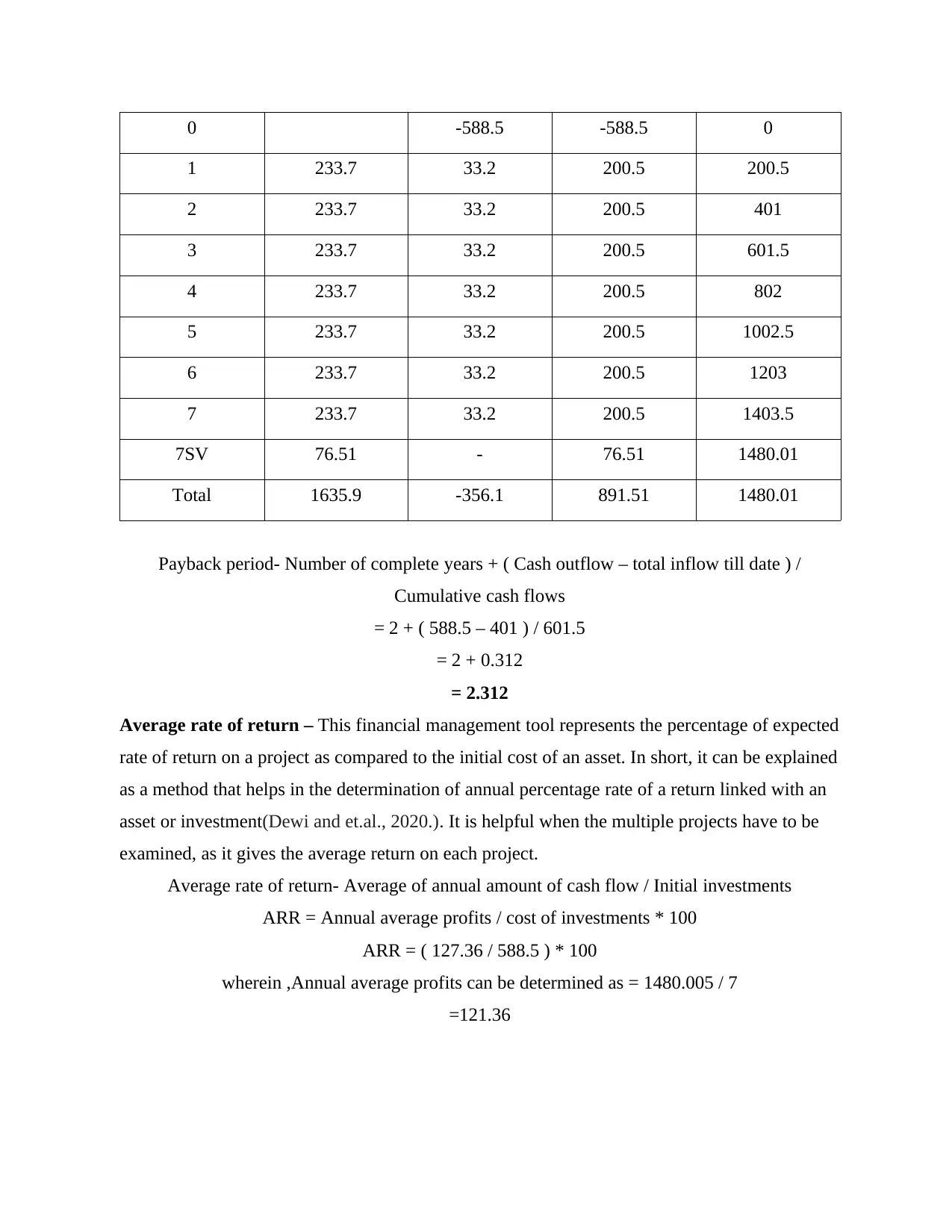

1 233.7 33.2 200.5 200.5

2 233.7 33.2 200.5 401

3 233.7 33.2 200.5 601.5

4 233.7 33.2 200.5 802

5 233.7 33.2 200.5 1002.5

6 233.7 33.2 200.5 1203

7 233.7 33.2 200.5 1403.5

7SV 76.51 - 76.51 1480.01

Total 1635.9 -356.1 891.51 1480.01

Payback period- Number of complete years + ( Cash outflow – total inflow till date ) /

Cumulative cash flows

= 2 + ( 588.5 – 401 ) / 601.5

= 2 + 0.312

= 2.312

Average rate of return – This financial management tool represents the percentage of expected

rate of return on a project as compared to the initial cost of an asset. In short, it can be explained

as a method that helps in the determination of annual percentage rate of a return linked with an

asset or investment(Dewi and et.al., 2020.). It is helpful when the multiple projects have to be

examined, as it gives the average return on each project.

Average rate of return- Average of annual amount of cash flow / Initial investments

ARR = Annual average profits / cost of investments * 100

ARR = ( 127.36 / 588.5 ) * 100

wherein ,Annual average profits can be determined as = 1480.005 / 7

=121.36

1 233.7 33.2 200.5 200.5

2 233.7 33.2 200.5 401

3 233.7 33.2 200.5 601.5

4 233.7 33.2 200.5 802

5 233.7 33.2 200.5 1002.5

6 233.7 33.2 200.5 1203

7 233.7 33.2 200.5 1403.5

7SV 76.51 - 76.51 1480.01

Total 1635.9 -356.1 891.51 1480.01

Payback period- Number of complete years + ( Cash outflow – total inflow till date ) /

Cumulative cash flows

= 2 + ( 588.5 – 401 ) / 601.5

= 2 + 0.312

= 2.312

Average rate of return – This financial management tool represents the percentage of expected

rate of return on a project as compared to the initial cost of an asset. In short, it can be explained

as a method that helps in the determination of annual percentage rate of a return linked with an

asset or investment(Dewi and et.al., 2020.). It is helpful when the multiple projects have to be

examined, as it gives the average return on each project.

Average rate of return- Average of annual amount of cash flow / Initial investments

ARR = Annual average profits / cost of investments * 100

ARR = ( 127.36 / 588.5 ) * 100

wherein ,Annual average profits can be determined as = 1480.005 / 7

=121.36

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

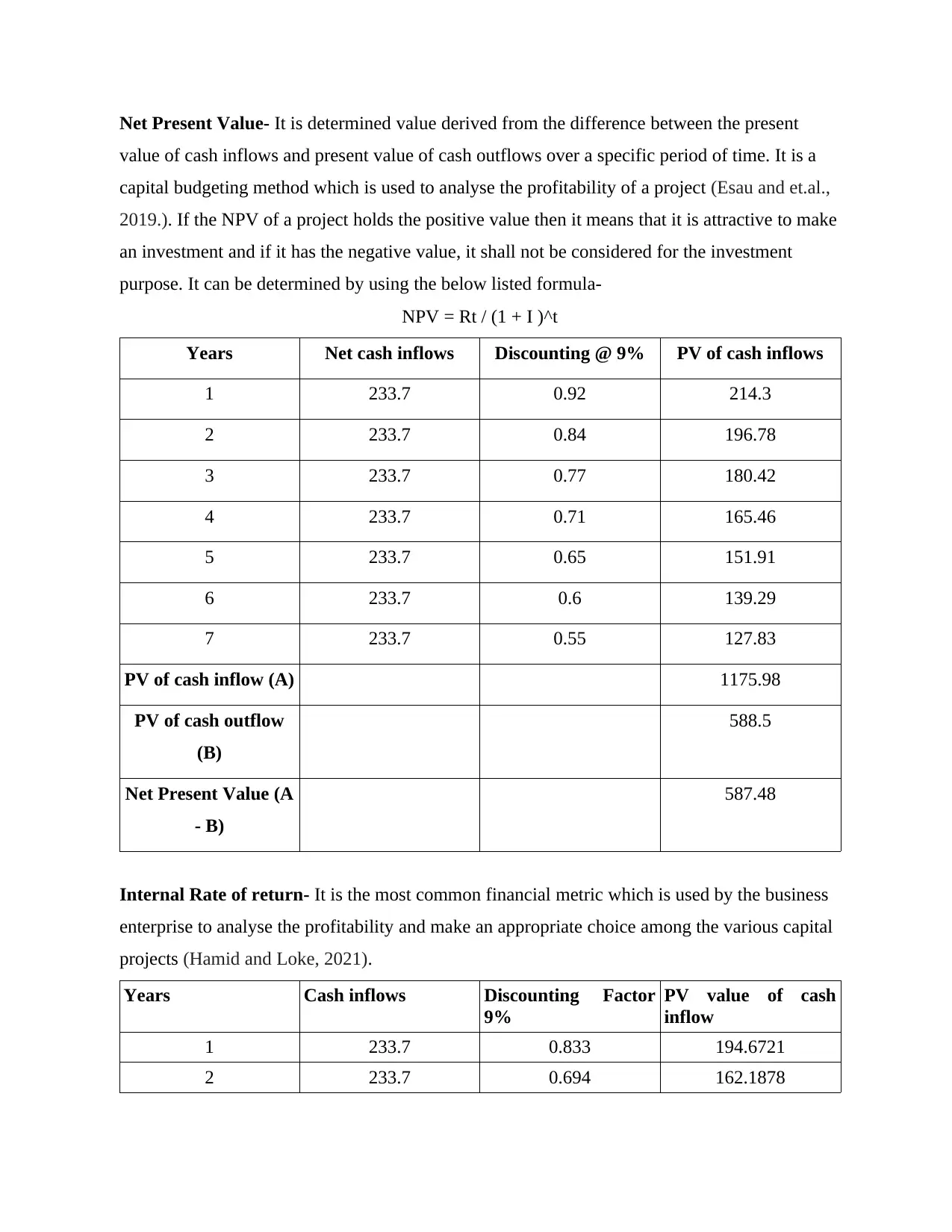

Net Present Value- It is determined value derived from the difference between the present

value of cash inflows and present value of cash outflows over a specific period of time. It is a

capital budgeting method which is used to analyse the profitability of a project (Esau and et.al.,

2019.). If the NPV of a project holds the positive value then it means that it is attractive to make

an investment and if it has the negative value, it shall not be considered for the investment

purpose. It can be determined by using the below listed formula-

NPV = Rt / (1 + I )^t

Years Net cash inflows Discounting @ 9% PV of cash inflows

1 233.7 0.92 214.3

2 233.7 0.84 196.78

3 233.7 0.77 180.42

4 233.7 0.71 165.46

5 233.7 0.65 151.91

6 233.7 0.6 139.29

7 233.7 0.55 127.83

PV of cash inflow (A) 1175.98

PV of cash outflow

(B)

588.5

Net Present Value (A

- B)

587.48

Internal Rate of return- It is the most common financial metric which is used by the business

enterprise to analyse the profitability and make an appropriate choice among the various capital

projects (Hamid and Loke, 2021).

Years Cash inflows Discounting Factor

9%

PV value of cash

inflow

1 233.7 0.833 194.6721

2 233.7 0.694 162.1878

value of cash inflows and present value of cash outflows over a specific period of time. It is a

capital budgeting method which is used to analyse the profitability of a project (Esau and et.al.,

2019.). If the NPV of a project holds the positive value then it means that it is attractive to make

an investment and if it has the negative value, it shall not be considered for the investment

purpose. It can be determined by using the below listed formula-

NPV = Rt / (1 + I )^t

Years Net cash inflows Discounting @ 9% PV of cash inflows

1 233.7 0.92 214.3

2 233.7 0.84 196.78

3 233.7 0.77 180.42

4 233.7 0.71 165.46

5 233.7 0.65 151.91

6 233.7 0.6 139.29

7 233.7 0.55 127.83

PV of cash inflow (A) 1175.98

PV of cash outflow

(B)

588.5

Net Present Value (A

- B)

587.48

Internal Rate of return- It is the most common financial metric which is used by the business

enterprise to analyse the profitability and make an appropriate choice among the various capital

projects (Hamid and Loke, 2021).

Years Cash inflows Discounting Factor

9%

PV value of cash

inflow

1 233.7 0.833 194.6721

2 233.7 0.694 162.1878

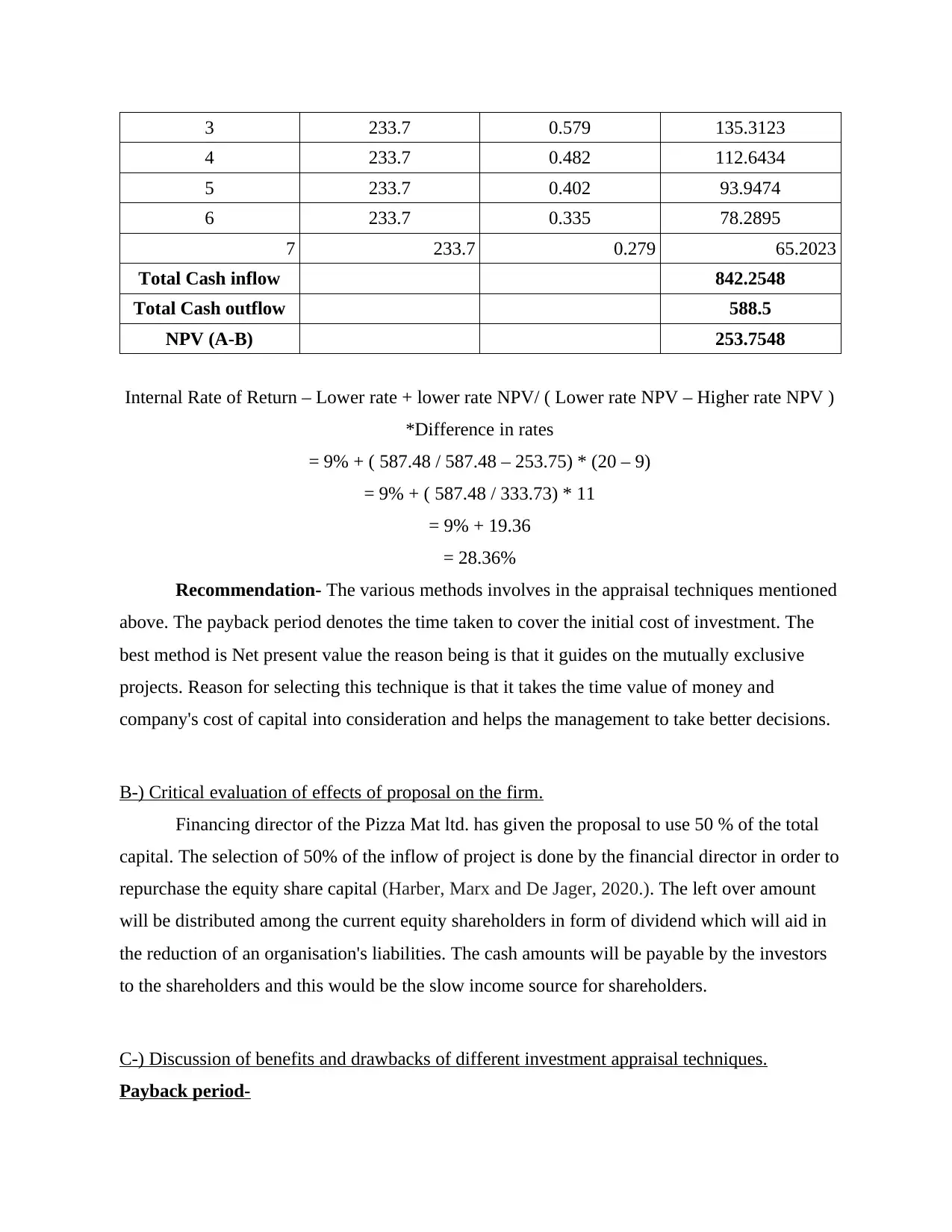

3 233.7 0.579 135.3123

4 233.7 0.482 112.6434

5 233.7 0.402 93.9474

6 233.7 0.335 78.2895

7 233.7 0.279 65.2023

Total Cash inflow 842.2548

Total Cash outflow 588.5

NPV (A-B) 253.7548

Internal Rate of Return – Lower rate + lower rate NPV/ ( Lower rate NPV – Higher rate NPV )

*Difference in rates

= 9% + ( 587.48 / 587.48 – 253.75) * (20 – 9)

= 9% + ( 587.48 / 333.73) * 11

= 9% + 19.36

= 28.36%

Recommendation- The various methods involves in the appraisal techniques mentioned

above. The payback period denotes the time taken to cover the initial cost of investment. The

best method is Net present value the reason being is that it guides on the mutually exclusive

projects. Reason for selecting this technique is that it takes the time value of money and

company's cost of capital into consideration and helps the management to take better decisions.

B-) Critical evaluation of effects of proposal on the firm.

Financing director of the Pizza Mat ltd. has given the proposal to use 50 % of the total

capital. The selection of 50% of the inflow of project is done by the financial director in order to

repurchase the equity share capital (Harber, Marx and De Jager, 2020.). The left over amount

will be distributed among the current equity shareholders in form of dividend which will aid in

the reduction of an organisation's liabilities. The cash amounts will be payable by the investors

to the shareholders and this would be the slow income source for shareholders.

C-) Discussion of benefits and drawbacks of different investment appraisal techniques.

Payback period-

4 233.7 0.482 112.6434

5 233.7 0.402 93.9474

6 233.7 0.335 78.2895

7 233.7 0.279 65.2023

Total Cash inflow 842.2548

Total Cash outflow 588.5

NPV (A-B) 253.7548

Internal Rate of Return – Lower rate + lower rate NPV/ ( Lower rate NPV – Higher rate NPV )

*Difference in rates

= 9% + ( 587.48 / 587.48 – 253.75) * (20 – 9)

= 9% + ( 587.48 / 333.73) * 11

= 9% + 19.36

= 28.36%

Recommendation- The various methods involves in the appraisal techniques mentioned

above. The payback period denotes the time taken to cover the initial cost of investment. The

best method is Net present value the reason being is that it guides on the mutually exclusive

projects. Reason for selecting this technique is that it takes the time value of money and

company's cost of capital into consideration and helps the management to take better decisions.

B-) Critical evaluation of effects of proposal on the firm.

Financing director of the Pizza Mat ltd. has given the proposal to use 50 % of the total

capital. The selection of 50% of the inflow of project is done by the financial director in order to

repurchase the equity share capital (Harber, Marx and De Jager, 2020.). The left over amount

will be distributed among the current equity shareholders in form of dividend which will aid in

the reduction of an organisation's liabilities. The cash amounts will be payable by the investors

to the shareholders and this would be the slow income source for shareholders.

C-) Discussion of benefits and drawbacks of different investment appraisal techniques.

Payback period-

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

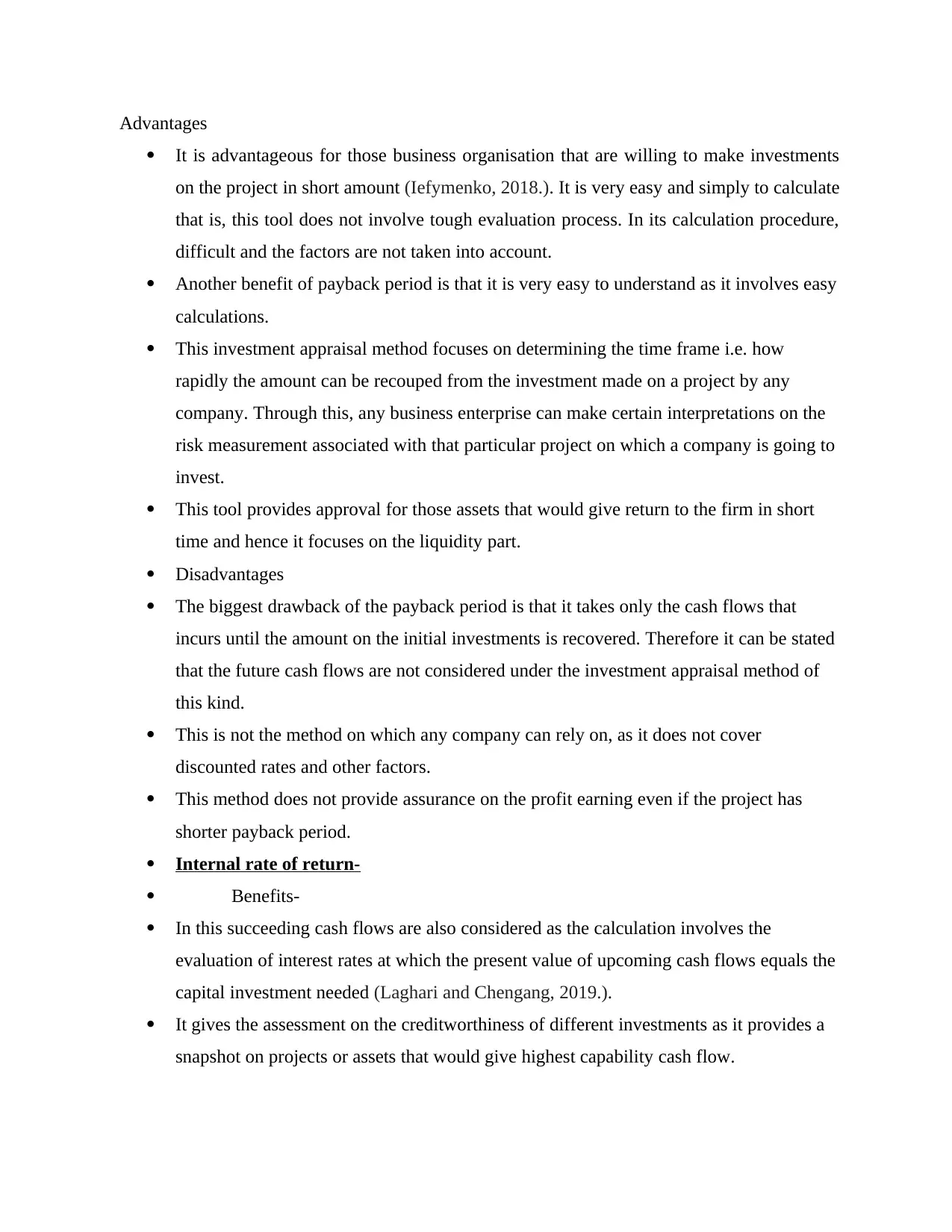

Advantages

It is advantageous for those business organisation that are willing to make investments

on the project in short amount (Iefymenko, 2018.). It is very easy and simply to calculate

that is, this tool does not involve tough evaluation process. In its calculation procedure,

difficult and the factors are not taken into account.

Another benefit of payback period is that it is very easy to understand as it involves easy

calculations.

This investment appraisal method focuses on determining the time frame i.e. how

rapidly the amount can be recouped from the investment made on a project by any

company. Through this, any business enterprise can make certain interpretations on the

risk measurement associated with that particular project on which a company is going to

invest.

This tool provides approval for those assets that would give return to the firm in short

time and hence it focuses on the liquidity part.

Disadvantages

The biggest drawback of the payback period is that it takes only the cash flows that

incurs until the amount on the initial investments is recovered. Therefore it can be stated

that the future cash flows are not considered under the investment appraisal method of

this kind.

This is not the method on which any company can rely on, as it does not cover

discounted rates and other factors.

This method does not provide assurance on the profit earning even if the project has

shorter payback period.

Internal rate of return-

Benefits-

In this succeeding cash flows are also considered as the calculation involves the

evaluation of interest rates at which the present value of upcoming cash flows equals the

capital investment needed (Laghari and Chengang, 2019.).

It gives the assessment on the creditworthiness of different investments as it provides a

snapshot on projects or assets that would give highest capability cash flow.

It is advantageous for those business organisation that are willing to make investments

on the project in short amount (Iefymenko, 2018.). It is very easy and simply to calculate

that is, this tool does not involve tough evaluation process. In its calculation procedure,

difficult and the factors are not taken into account.

Another benefit of payback period is that it is very easy to understand as it involves easy

calculations.

This investment appraisal method focuses on determining the time frame i.e. how

rapidly the amount can be recouped from the investment made on a project by any

company. Through this, any business enterprise can make certain interpretations on the

risk measurement associated with that particular project on which a company is going to

invest.

This tool provides approval for those assets that would give return to the firm in short

time and hence it focuses on the liquidity part.

Disadvantages

The biggest drawback of the payback period is that it takes only the cash flows that

incurs until the amount on the initial investments is recovered. Therefore it can be stated

that the future cash flows are not considered under the investment appraisal method of

this kind.

This is not the method on which any company can rely on, as it does not cover

discounted rates and other factors.

This method does not provide assurance on the profit earning even if the project has

shorter payback period.

Internal rate of return-

Benefits-

In this succeeding cash flows are also considered as the calculation involves the

evaluation of interest rates at which the present value of upcoming cash flows equals the

capital investment needed (Laghari and Chengang, 2019.).

It gives the assessment on the creditworthiness of different investments as it provides a

snapshot on projects or assets that would give highest capability cash flow.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

It does not deal with the problematic rate, which makes it convenient for the firm to

select those project that will give higher returns.

Drawbacks-

This investment appraisal method does not outline the report on the size of a project

when the comparison between the projects is done.

Though, it takes in account the future cash flows, but this tool assumes that the

upcoming cash flows can be invested at equal rate as the internal rate of return.

Net present value-

Benefits

It assists the company regarding the nature of investment, whether it would good for a

firm or not.

This methods includes risk factors and cost of capital in accordance with the upcoming

projects.

Disadvantages

The huge drawback is, this financial metric is not implied to the projects that have

changes in the investment amounts.

This speculates the upcoming cash flows, which can report in the inferior investments.

It is very tough to put in this financial approach because when the projects are compared

then each of them has differences in their life time (Mahendru, 2020.).

QUESTION 3

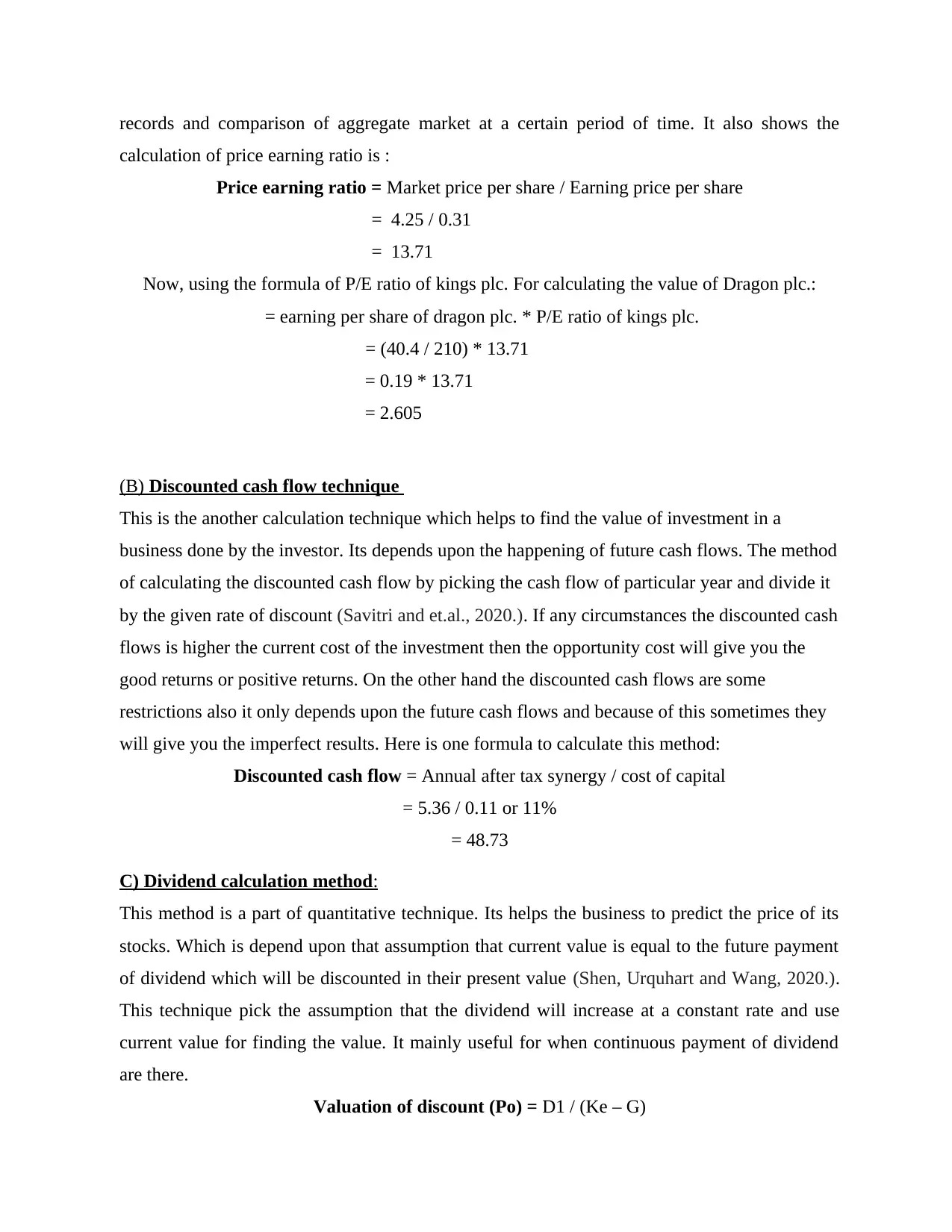

A) Price earning ratio model (P/E ratio):

This technique is also called as numerous price and numerous earning. This use of the ratio is it

helps to find the financial condition of firm. Which assist to find the current price of the share in

relation with earning per share(EPS) of the company (Nawn and Banerjee, 2019.). This

technique is very useful for the backward looking and future projected method. The calculation

of this method by using formula is: Market price per share divided by the Earning per

share(EPS). This tool is very frequently use of stakeholders to find out the value of stock.

Higher earning price per share mark that the shares are overestimated or investors are

demanding the increment of growth rate in future. It is also useful for the measuring of past

select those project that will give higher returns.

Drawbacks-

This investment appraisal method does not outline the report on the size of a project

when the comparison between the projects is done.

Though, it takes in account the future cash flows, but this tool assumes that the

upcoming cash flows can be invested at equal rate as the internal rate of return.

Net present value-

Benefits

It assists the company regarding the nature of investment, whether it would good for a

firm or not.

This methods includes risk factors and cost of capital in accordance with the upcoming

projects.

Disadvantages

The huge drawback is, this financial metric is not implied to the projects that have

changes in the investment amounts.

This speculates the upcoming cash flows, which can report in the inferior investments.

It is very tough to put in this financial approach because when the projects are compared

then each of them has differences in their life time (Mahendru, 2020.).

QUESTION 3

A) Price earning ratio model (P/E ratio):

This technique is also called as numerous price and numerous earning. This use of the ratio is it

helps to find the financial condition of firm. Which assist to find the current price of the share in

relation with earning per share(EPS) of the company (Nawn and Banerjee, 2019.). This

technique is very useful for the backward looking and future projected method. The calculation

of this method by using formula is: Market price per share divided by the Earning per

share(EPS). This tool is very frequently use of stakeholders to find out the value of stock.

Higher earning price per share mark that the shares are overestimated or investors are

demanding the increment of growth rate in future. It is also useful for the measuring of past

records and comparison of aggregate market at a certain period of time. It also shows the

calculation of price earning ratio is :

Price earning ratio = Market price per share / Earning price per share

= 4.25 / 0.31

= 13.71

Now, using the formula of P/E ratio of kings plc. For calculating the value of Dragon plc.:

= earning per share of dragon plc. * P/E ratio of kings plc.

= (40.4 / 210) * 13.71

= 0.19 * 13.71

= 2.605

(B) Discounted cash flow technique

This is the another calculation technique which helps to find the value of investment in a

business done by the investor. Its depends upon the happening of future cash flows. The method

of calculating the discounted cash flow by picking the cash flow of particular year and divide it

by the given rate of discount (Savitri and et.al., 2020.). If any circumstances the discounted cash

flows is higher the current cost of the investment then the opportunity cost will give you the

good returns or positive returns. On the other hand the discounted cash flows are some

restrictions also it only depends upon the future cash flows and because of this sometimes they

will give you the imperfect results. Here is one formula to calculate this method:

Discounted cash flow = Annual after tax synergy / cost of capital

= 5.36 / 0.11 or 11%

= 48.73

C) Dividend calculation method:

This method is a part of quantitative technique. Its helps the business to predict the price of its

stocks. Which is depend upon that assumption that current value is equal to the future payment

of dividend which will be discounted in their present value (Shen, Urquhart and Wang, 2020.).

This technique pick the assumption that the dividend will increase at a constant rate and use

current value for finding the value. It mainly useful for when continuous payment of dividend

are there.

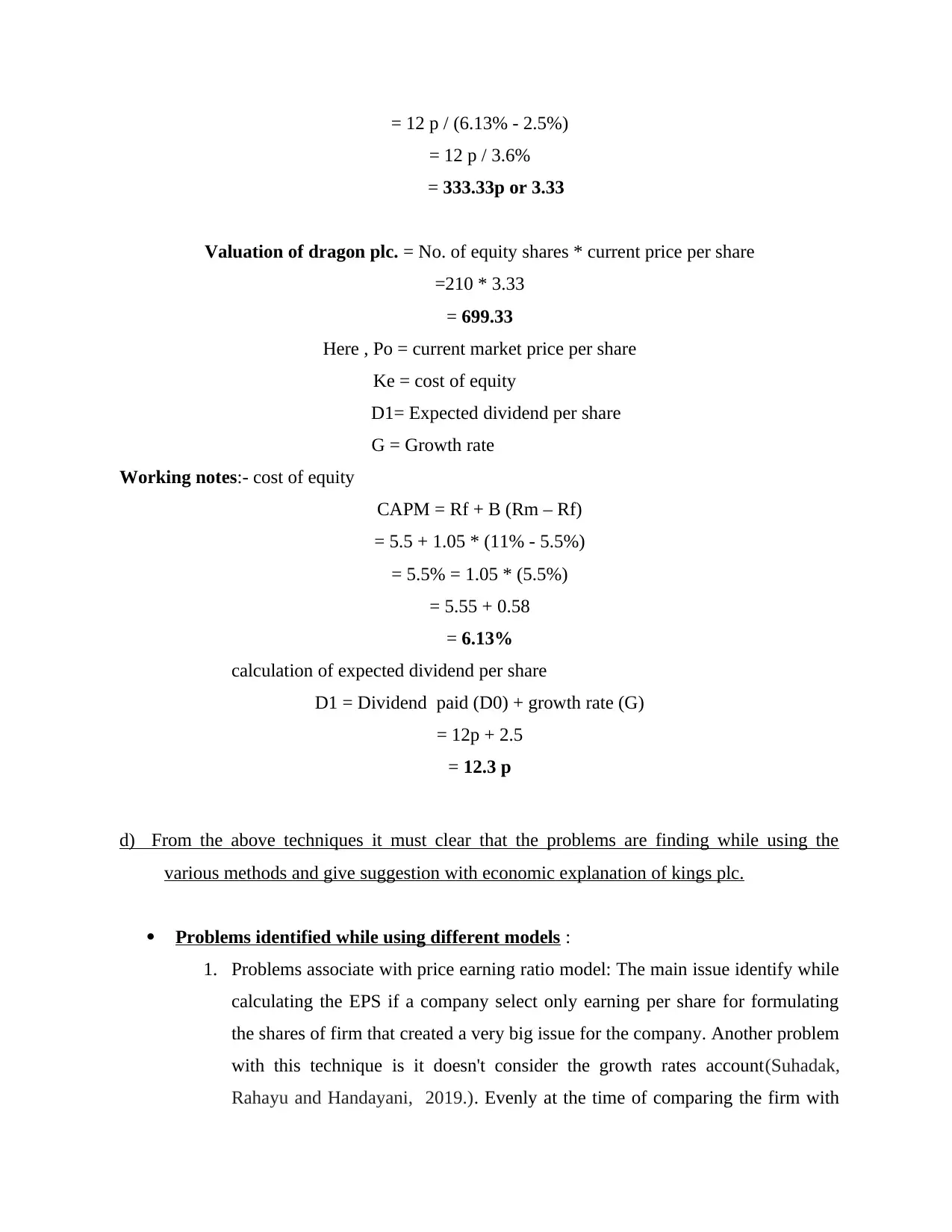

Valuation of discount (Po) = D1 / (Ke – G)

calculation of price earning ratio is :

Price earning ratio = Market price per share / Earning price per share

= 4.25 / 0.31

= 13.71

Now, using the formula of P/E ratio of kings plc. For calculating the value of Dragon plc.:

= earning per share of dragon plc. * P/E ratio of kings plc.

= (40.4 / 210) * 13.71

= 0.19 * 13.71

= 2.605

(B) Discounted cash flow technique

This is the another calculation technique which helps to find the value of investment in a

business done by the investor. Its depends upon the happening of future cash flows. The method

of calculating the discounted cash flow by picking the cash flow of particular year and divide it

by the given rate of discount (Savitri and et.al., 2020.). If any circumstances the discounted cash

flows is higher the current cost of the investment then the opportunity cost will give you the

good returns or positive returns. On the other hand the discounted cash flows are some

restrictions also it only depends upon the future cash flows and because of this sometimes they

will give you the imperfect results. Here is one formula to calculate this method:

Discounted cash flow = Annual after tax synergy / cost of capital

= 5.36 / 0.11 or 11%

= 48.73

C) Dividend calculation method:

This method is a part of quantitative technique. Its helps the business to predict the price of its

stocks. Which is depend upon that assumption that current value is equal to the future payment

of dividend which will be discounted in their present value (Shen, Urquhart and Wang, 2020.).

This technique pick the assumption that the dividend will increase at a constant rate and use

current value for finding the value. It mainly useful for when continuous payment of dividend

are there.

Valuation of discount (Po) = D1 / (Ke – G)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

= 12 p / (6.13% - 2.5%)

= 12 p / 3.6%

= 333.33p or 3.33

Valuation of dragon plc. = No. of equity shares * current price per share

=210 * 3.33

= 699.33

Here , Po = current market price per share

Ke = cost of equity

D1= Expected dividend per share

G = Growth rate

Working notes:- cost of equity

CAPM = Rf + B (Rm – Rf)

= 5.5 + 1.05 * (11% - 5.5%)

= 5.5% = 1.05 * (5.5%)

= 5.55 + 0.58

= 6.13%

calculation of expected dividend per share

D1 = Dividend paid (D0) + growth rate (G)

= 12p + 2.5

= 12.3 p

d) From the above techniques it must clear that the problems are finding while using the

various methods and give suggestion with economic explanation of kings plc.

Problems identified while using different models :

1. Problems associate with price earning ratio model: The main issue identify while

calculating the EPS if a company select only earning per share for formulating

the shares of firm that created a very big issue for the company. Another problem

with this technique is it doesn't consider the growth rates account(Suhadak,

Rahayu and Handayani, 2019.). Evenly at the time of comparing the firm with

= 12 p / 3.6%

= 333.33p or 3.33

Valuation of dragon plc. = No. of equity shares * current price per share

=210 * 3.33

= 699.33

Here , Po = current market price per share

Ke = cost of equity

D1= Expected dividend per share

G = Growth rate

Working notes:- cost of equity

CAPM = Rf + B (Rm – Rf)

= 5.5 + 1.05 * (11% - 5.5%)

= 5.5% = 1.05 * (5.5%)

= 5.55 + 0.58

= 6.13%

calculation of expected dividend per share

D1 = Dividend paid (D0) + growth rate (G)

= 12p + 2.5

= 12.3 p

d) From the above techniques it must clear that the problems are finding while using the

various methods and give suggestion with economic explanation of kings plc.

Problems identified while using different models :

1. Problems associate with price earning ratio model: The main issue identify while

calculating the EPS if a company select only earning per share for formulating

the shares of firm that created a very big issue for the company. Another problem

with this technique is it doesn't consider the growth rates account(Suhadak,

Rahayu and Handayani, 2019.). Evenly at the time of comparing the firm with

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

some other industry at that particular point of time it not consider price earning

ration of the business. Sometimes this technique misguide the company

stakeholder it only show its good part of the company like, it only consider the

value of equity shares and not showing the debts of the company because of this

some investors mislead and invest in the company and suffer a loss in future. So,

this are the some negative points of price earning ratio every company needs to

understand and try to solve the problem of this technique or using this method by

these negative points keep in mind.

2. Problem involved in discounted cash flow method: The main problem in this

technique is it depends upon the various assumptions and in this their must be a

chances of error occurred while using discounted cash flow method. It overlooks

the calculation of company in isolation. Another problem is it must be difficulty

to find the scrap value of a large share of the total price. Also in this it is a big

challenge to calculate weighted average cost of capital (WACC). If it comes to

the rate of growth and rate of discount, there must be chances of

continuously change and the resultant fair value wouldn't be viable. Its not good

for short term investment it only emphasis on long term (Widarnawati, Santoso

and Suparman, 2018.). They work effectively when they know there is high cash

flows in future then in that case they boost the confidence and perform the

activities for achieving the higher cash flows in future. If the department of the

company lack visibility then it creates a problem to predict sales, operating

expenses and investment in capital with full certainty. This model wants fixed

modification and fair value of the firm so they can change it accordingly for the

demand of the model.

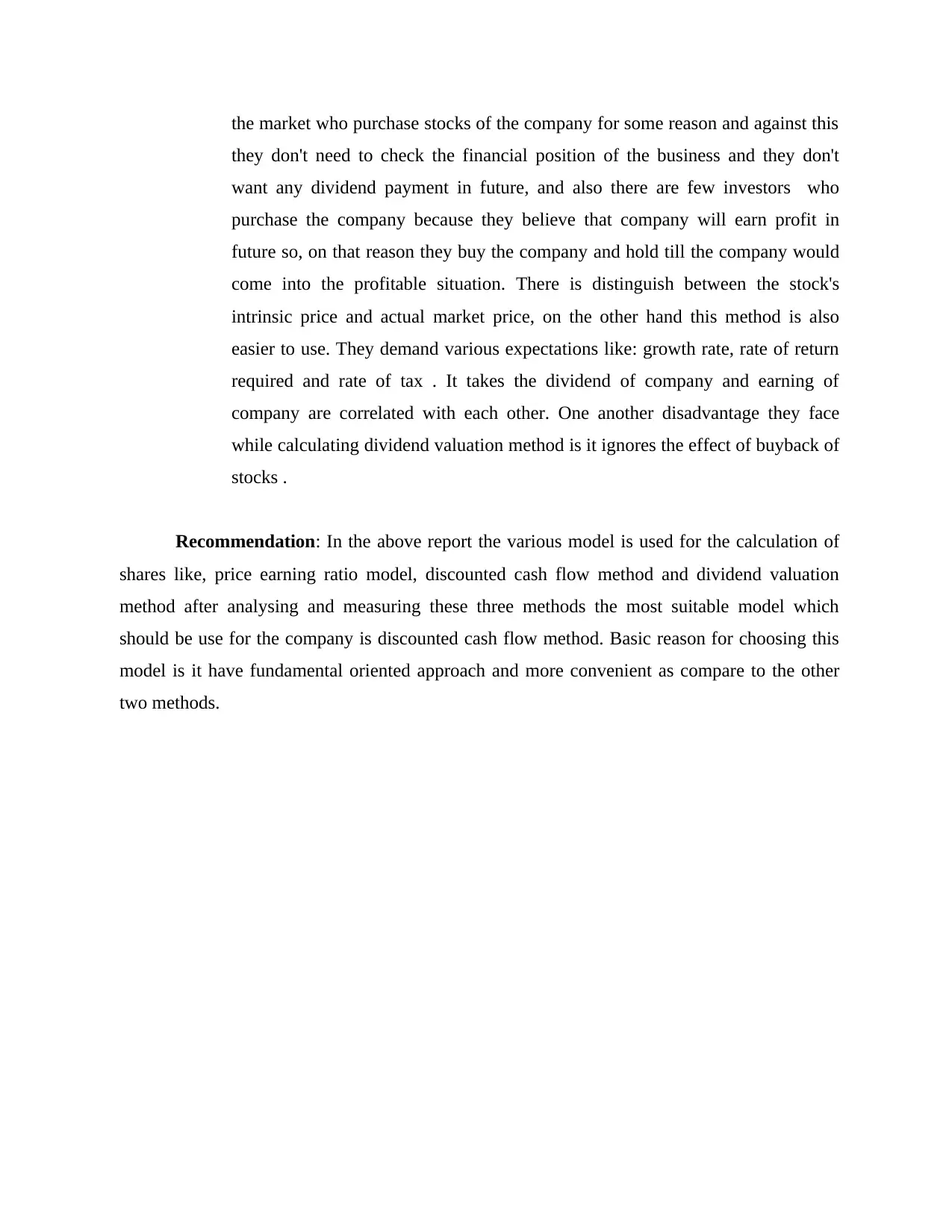

3. Problems involved in dividend valuation method: Every investor if he/she invest

money in any company then they check the profitability in the business because

every investor need good returns for the company but some investors use this

technique for checking the dividend earn by the company in following year but

not its less relevant model in today's times. Basically in this concept stakeholders

who invest in the stocks of company plough those stocks in which they pay

more money to the company(Tao and et.al., 2021.). There are many investors in

ration of the business. Sometimes this technique misguide the company

stakeholder it only show its good part of the company like, it only consider the

value of equity shares and not showing the debts of the company because of this

some investors mislead and invest in the company and suffer a loss in future. So,

this are the some negative points of price earning ratio every company needs to

understand and try to solve the problem of this technique or using this method by

these negative points keep in mind.

2. Problem involved in discounted cash flow method: The main problem in this

technique is it depends upon the various assumptions and in this their must be a

chances of error occurred while using discounted cash flow method. It overlooks

the calculation of company in isolation. Another problem is it must be difficulty

to find the scrap value of a large share of the total price. Also in this it is a big

challenge to calculate weighted average cost of capital (WACC). If it comes to

the rate of growth and rate of discount, there must be chances of

continuously change and the resultant fair value wouldn't be viable. Its not good

for short term investment it only emphasis on long term (Widarnawati, Santoso

and Suparman, 2018.). They work effectively when they know there is high cash

flows in future then in that case they boost the confidence and perform the

activities for achieving the higher cash flows in future. If the department of the

company lack visibility then it creates a problem to predict sales, operating

expenses and investment in capital with full certainty. This model wants fixed

modification and fair value of the firm so they can change it accordingly for the

demand of the model.

3. Problems involved in dividend valuation method: Every investor if he/she invest

money in any company then they check the profitability in the business because

every investor need good returns for the company but some investors use this

technique for checking the dividend earn by the company in following year but

not its less relevant model in today's times. Basically in this concept stakeholders

who invest in the stocks of company plough those stocks in which they pay

more money to the company(Tao and et.al., 2021.). There are many investors in

the market who purchase stocks of the company for some reason and against this

they don't need to check the financial position of the business and they don't

want any dividend payment in future, and also there are few investors who

purchase the company because they believe that company will earn profit in

future so, on that reason they buy the company and hold till the company would

come into the profitable situation. There is distinguish between the stock's

intrinsic price and actual market price, on the other hand this method is also

easier to use. They demand various expectations like: growth rate, rate of return

required and rate of tax . It takes the dividend of company and earning of

company are correlated with each other. One another disadvantage they face

while calculating dividend valuation method is it ignores the effect of buyback of

stocks .

Recommendation: In the above report the various model is used for the calculation of

shares like, price earning ratio model, discounted cash flow method and dividend valuation

method after analysing and measuring these three methods the most suitable model which

should be use for the company is discounted cash flow method. Basic reason for choosing this

model is it have fundamental oriented approach and more convenient as compare to the other

two methods.

they don't need to check the financial position of the business and they don't

want any dividend payment in future, and also there are few investors who

purchase the company because they believe that company will earn profit in

future so, on that reason they buy the company and hold till the company would

come into the profitable situation. There is distinguish between the stock's

intrinsic price and actual market price, on the other hand this method is also

easier to use. They demand various expectations like: growth rate, rate of return

required and rate of tax . It takes the dividend of company and earning of

company are correlated with each other. One another disadvantage they face

while calculating dividend valuation method is it ignores the effect of buyback of

stocks .

Recommendation: In the above report the various model is used for the calculation of

shares like, price earning ratio model, discounted cash flow method and dividend valuation

method after analysing and measuring these three methods the most suitable model which

should be use for the company is discounted cash flow method. Basic reason for choosing this

model is it have fundamental oriented approach and more convenient as compare to the other

two methods.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.