Financial Management Report: MSc Business with Financial Management

VerifiedAdded on 2020/02/17

|15

|3426

|59

Report

AI Summary

This report provides a detailed analysis of financial management principles and their application in real-world scenarios. It begins with an introduction to financial management and its importance in corporate decision-making, emphasizing the role of finance managers in estimating capital requirements, determining capital structure, and managing funds. The report then delves into specific valuation techniques, including the price-earnings ratio, dividend valuation method, and discounted cash flow method, using the financial statements of Trojan PLC as a case study. Furthermore, the report explores investment appraisal techniques such as payback period, net present value, accounting rate of return, and internal rate of return, to evaluate the potential purchase of a new machine by Love-well Limited. The analysis includes detailed calculations, interpretations, and recommendations, offering insights into the selection of the most suitable valuation and appraisal methods for different business contexts, particularly in the context of mergers and acquisitions.

Financial Management

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTRODUCTION

In each and every company financial management is necessary as well as essential as it

helps the investors in making the correct and appropriate decisions. Supervision of finance helps

in flow of money in the effective and efficient manner so that employees of the business entity

can accomplish the goals and objectives. It is the function which is specified in the firm and it is

directly associated with the top management of the enterprise. In the company, finance manager

having the different functions which includes the estimating the amount which requires the

capital. Along with this they have to determine the capital structure and also have to manage the

funds by using the appropriate resources. Financial manager of the business entity have to

provide the proper control so that they can evaluate or analyse the financial performance. For

putting control on the activities they can use Return on Investment method (MSc Business with

Financial Management, 2017). In Question 1, the calculation needs to be done on the basis of

financial statement of Trojan PLC. In question 2, computation needs to be done by using the

distinctive investment appraisal technique and the values to be taken of Love-well Limited

company along with the benefits and limitations.

Question 2

a)

Price earning ratio- It is a common practice for the investors to use this ratio as it assist in

determining the company's stock price whether it is over or undervalued. If companies having

high earning price ratio then it having typically growth shares (Petty and et. al., 2015). Price

earning ratio is also known as earnings multiple and it is one of the most popular valuation

measures which is used by the investors to do analysis. It is calculated by using the formula that

is market price per share which is divided by earning per share.

Ke = Rf + beta(Rm – Rf)

= 5 + 1.1( 11-5)

In each and every company financial management is necessary as well as essential as it

helps the investors in making the correct and appropriate decisions. Supervision of finance helps

in flow of money in the effective and efficient manner so that employees of the business entity

can accomplish the goals and objectives. It is the function which is specified in the firm and it is

directly associated with the top management of the enterprise. In the company, finance manager

having the different functions which includes the estimating the amount which requires the

capital. Along with this they have to determine the capital structure and also have to manage the

funds by using the appropriate resources. Financial manager of the business entity have to

provide the proper control so that they can evaluate or analyse the financial performance. For

putting control on the activities they can use Return on Investment method (MSc Business with

Financial Management, 2017). In Question 1, the calculation needs to be done on the basis of

financial statement of Trojan PLC. In question 2, computation needs to be done by using the

distinctive investment appraisal technique and the values to be taken of Love-well Limited

company along with the benefits and limitations.

Question 2

a)

Price earning ratio- It is a common practice for the investors to use this ratio as it assist in

determining the company's stock price whether it is over or undervalued. If companies having

high earning price ratio then it having typically growth shares (Petty and et. al., 2015). Price

earning ratio is also known as earnings multiple and it is one of the most popular valuation

measures which is used by the investors to do analysis. It is calculated by using the formula that

is market price per share which is divided by earning per share.

Ke = Rf + beta(Rm – Rf)

= 5 + 1.1( 11-5)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

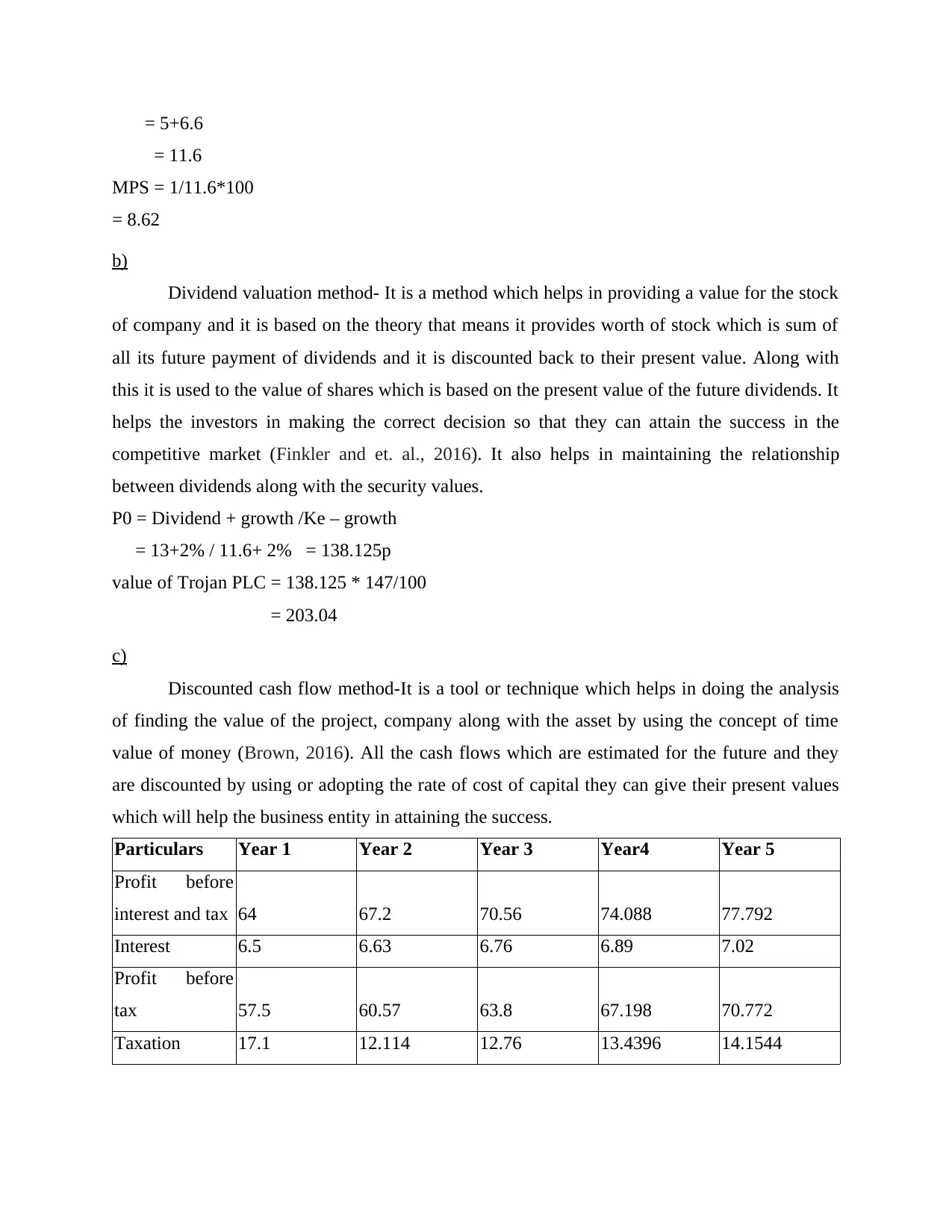

= 5+6.6

= 11.6

MPS = 1/11.6*100

= 8.62

b)

Dividend valuation method- It is a method which helps in providing a value for the stock

of company and it is based on the theory that means it provides worth of stock which is sum of

all its future payment of dividends and it is discounted back to their present value. Along with

this it is used to the value of shares which is based on the present value of the future dividends. It

helps the investors in making the correct decision so that they can attain the success in the

competitive market (Finkler and et. al., 2016). It also helps in maintaining the relationship

between dividends along with the security values.

P0 = Dividend + growth /Ke – growth

= 13+2% / 11.6+ 2% = 138.125p

value of Trojan PLC = 138.125 * 147/100

= 203.04

c)

Discounted cash flow method-It is a tool or technique which helps in doing the analysis

of finding the value of the project, company along with the asset by using the concept of time

value of money (Brown, 2016). All the cash flows which are estimated for the future and they

are discounted by using or adopting the rate of cost of capital they can give their present values

which will help the business entity in attaining the success.

Particulars Year 1 Year 2 Year 3 Year4 Year 5

Profit before

interest and tax 64 67.2 70.56 74.088 77.792

Interest 6.5 6.63 6.76 6.89 7.02

Profit before

tax 57.5 60.57 63.8 67.198 70.772

Taxation 17.1 12.114 12.76 13.4396 14.1544

= 11.6

MPS = 1/11.6*100

= 8.62

b)

Dividend valuation method- It is a method which helps in providing a value for the stock

of company and it is based on the theory that means it provides worth of stock which is sum of

all its future payment of dividends and it is discounted back to their present value. Along with

this it is used to the value of shares which is based on the present value of the future dividends. It

helps the investors in making the correct decision so that they can attain the success in the

competitive market (Finkler and et. al., 2016). It also helps in maintaining the relationship

between dividends along with the security values.

P0 = Dividend + growth /Ke – growth

= 13+2% / 11.6+ 2% = 138.125p

value of Trojan PLC = 138.125 * 147/100

= 203.04

c)

Discounted cash flow method-It is a tool or technique which helps in doing the analysis

of finding the value of the project, company along with the asset by using the concept of time

value of money (Brown, 2016). All the cash flows which are estimated for the future and they

are discounted by using or adopting the rate of cost of capital they can give their present values

which will help the business entity in attaining the success.

Particulars Year 1 Year 2 Year 3 Year4 Year 5

Profit before

interest and tax 64 67.2 70.56 74.088 77.792

Interest 6.5 6.63 6.76 6.89 7.02

Profit before

tax 57.5 60.57 63.8 67.198 70.772

Taxation 17.1 12.114 12.76 13.4396 14.1544

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

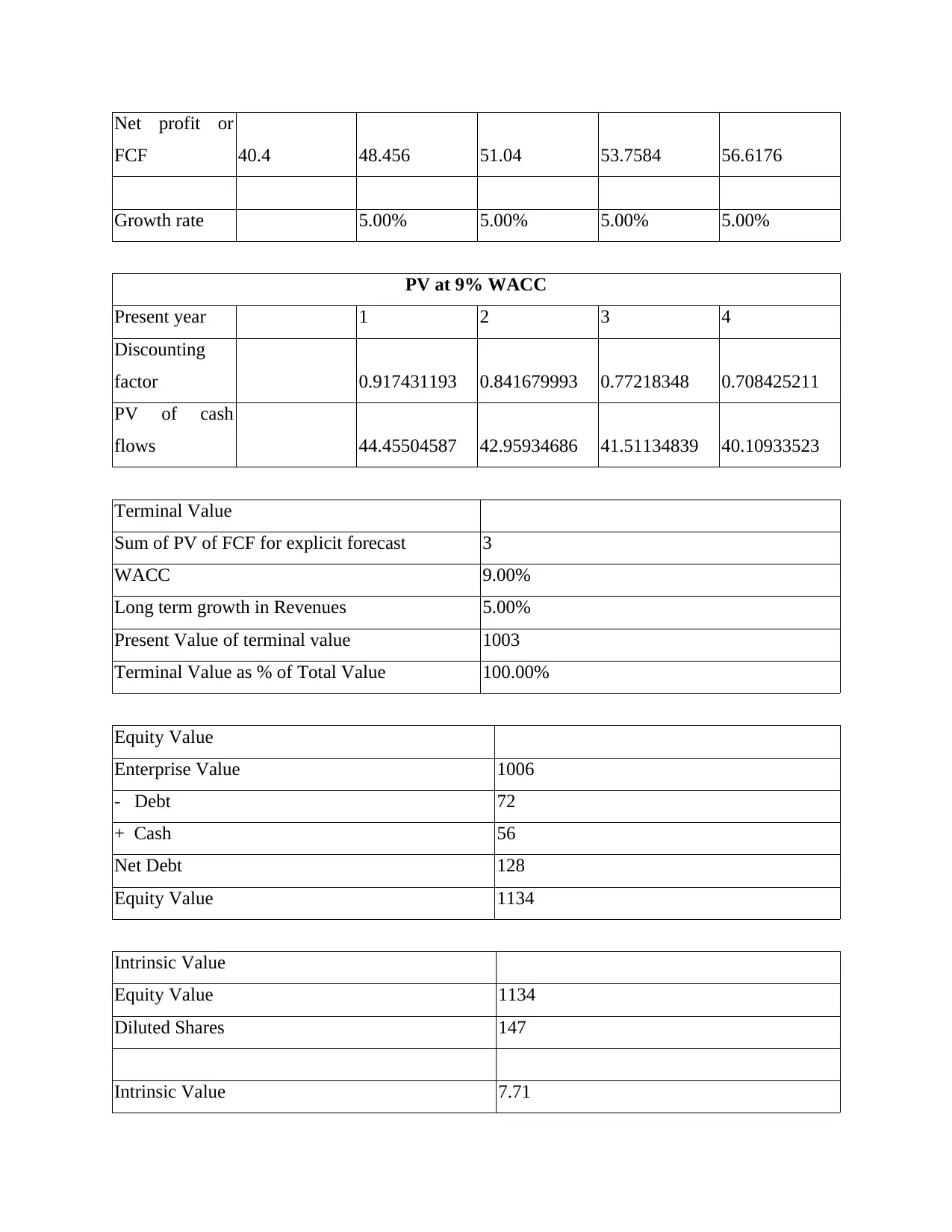

Net profit or

FCF 40.4 48.456 51.04 53.7584 56.6176

Growth rate 5.00% 5.00% 5.00% 5.00%

PV at 9% WACC

Present year 1 2 3 4

Discounting

factor 0.917431193 0.841679993 0.77218348 0.708425211

PV of cash

flows 44.45504587 42.95934686 41.51134839 40.10933523

Terminal Value

Sum of PV of FCF for explicit forecast 3

WACC 9.00%

Long term growth in Revenues 5.00%

Present Value of terminal value 1003

Terminal Value as % of Total Value 100.00%

Equity Value

Enterprise Value 1006

- Debt 72

+ Cash 56

Net Debt 128

Equity Value 1134

Intrinsic Value

Equity Value 1134

Diluted Shares 147

Intrinsic Value 7.71

FCF 40.4 48.456 51.04 53.7584 56.6176

Growth rate 5.00% 5.00% 5.00% 5.00%

PV at 9% WACC

Present year 1 2 3 4

Discounting

factor 0.917431193 0.841679993 0.77218348 0.708425211

PV of cash

flows 44.45504587 42.95934686 41.51134839 40.10933523

Terminal Value

Sum of PV of FCF for explicit forecast 3

WACC 9.00%

Long term growth in Revenues 5.00%

Present Value of terminal value 1003

Terminal Value as % of Total Value 100.00%

Equity Value

Enterprise Value 1006

- Debt 72

+ Cash 56

Net Debt 128

Equity Value 1134

Intrinsic Value

Equity Value 1134

Diluted Shares 147

Intrinsic Value 7.71

In the above discounted cash flow model growth rate used by an entity over the years is

5% which creates changes in he existing profit of the firm. The application of 5% growth rate

induces the current business performance of an enterprise owner over the years. Role of an entity

gets increases with the passage as in this particular approach quality of all the activities is

increases by utilising various factors in improving its current business conditions, Forecasting

plays a significant role in determining the future position of the firm by analysing the existing

facts and figures as their ultimate aim is to consider all the factors held responsible for inducing

the current performance (Renz, 2016). Interest rate expenses has increases at the rate of 2%

which is 3% less that the growth applied to the current profit of an entity that shows the ability of

an enterprise in generating higher outcomes in the external business environment.

Discounting cash flow model is based on the time value money concept n which present

facts and figures are analysed in relation to several parameters used by them, in inducing the

current business performance. Discounting rate is used in order to determine the future return

generated by a particular business project in a particular time period. In the current case scenario,

profit after tax is analysed on the basis of 9% discounting rate as through this approach an entity

owner will ascertain its future performance in the present as negative cash flows can be rectified

in advance by taking important decisions for the betterment of the business.

d)

Selection of the best suitable technique is based on the existing nature of the business as

how it helps an entity in improving its current business operations. Price earning ratio is not

suitable as it emphasises on the share price of the company which in case of mergers and

takeover gets zero which decreases the return generated by firm. Other technique of valuation is

dividend valuation technique that is also based on the existing income of the business as in

merger of the company the initially firm's capabilities gets reduces which in directly affected the

business performance in a particular financial year. Discounted cash flow model has used as one

of the valuation technique which is based on the profit generated by the firm which also provides

the forecasting effect in the existing firm which is regarded as the best suitable method for the

business in terms of merger and takeover of the firm. It is recommended to Aztec to select this

particular technique as this would help an enterprise owner in knowing its future returns after the

merger of current firm with another.

5% which creates changes in he existing profit of the firm. The application of 5% growth rate

induces the current business performance of an enterprise owner over the years. Role of an entity

gets increases with the passage as in this particular approach quality of all the activities is

increases by utilising various factors in improving its current business conditions, Forecasting

plays a significant role in determining the future position of the firm by analysing the existing

facts and figures as their ultimate aim is to consider all the factors held responsible for inducing

the current performance (Renz, 2016). Interest rate expenses has increases at the rate of 2%

which is 3% less that the growth applied to the current profit of an entity that shows the ability of

an enterprise in generating higher outcomes in the external business environment.

Discounting cash flow model is based on the time value money concept n which present

facts and figures are analysed in relation to several parameters used by them, in inducing the

current business performance. Discounting rate is used in order to determine the future return

generated by a particular business project in a particular time period. In the current case scenario,

profit after tax is analysed on the basis of 9% discounting rate as through this approach an entity

owner will ascertain its future performance in the present as negative cash flows can be rectified

in advance by taking important decisions for the betterment of the business.

d)

Selection of the best suitable technique is based on the existing nature of the business as

how it helps an entity in improving its current business operations. Price earning ratio is not

suitable as it emphasises on the share price of the company which in case of mergers and

takeover gets zero which decreases the return generated by firm. Other technique of valuation is

dividend valuation technique that is also based on the existing income of the business as in

merger of the company the initially firm's capabilities gets reduces which in directly affected the

business performance in a particular financial year. Discounted cash flow model has used as one

of the valuation technique which is based on the profit generated by the firm which also provides

the forecasting effect in the existing firm which is regarded as the best suitable method for the

business in terms of merger and takeover of the firm. It is recommended to Aztec to select this

particular technique as this would help an enterprise owner in knowing its future returns after the

merger of current firm with another.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Recommendation of discounted cash flow model by Aztec as it would emphasise on the

actual business performance of an entity in relation to various aspects to be covered by this

particular technique. Real worth of the business project will be easily evaluated with the help of

the current technique in which present of the firm are used as basic element in determining its

future performance. Mergers is the biggest decision taken by an entity as this technique will help

in verifying the tough decisions taken by the business concern by generating higher business

outcomes.

Question 3

A.

If the manager or owner of Love well Limited company wants to purchase a new

machines and before that they have to use different investment appraisal techniques which will

helps in finding out or analysing that they have to purchase the machine or not and on the basis

of that they can attain maximum profit or not (Egginton, Van Ness and Van Ness, 2016).

Purchasing new machine - £275,000

Annual Cash Inflow - £85000

Cash outflow - £12500 in every six year.

Depreciation would be charged by using Straight line method and it would be charged on

15%.

Cost of capital – 12%.

Different appraisal technique which they can use to find that they have to purchase

machine or not. They are pay back period method, accounting rate of return tool, net present

value and Internal rate of return method (Karadag, 2015). Along with this the owner of Love

well limited have to check that this method increase the profitability or economic feasibility by

acquiring the machines.

1. Pay back Period method:

Year Cash Inflow Cumulative Cash inflow

1 72500 72500

2 72500 145000

3 72500 217500

actual business performance of an entity in relation to various aspects to be covered by this

particular technique. Real worth of the business project will be easily evaluated with the help of

the current technique in which present of the firm are used as basic element in determining its

future performance. Mergers is the biggest decision taken by an entity as this technique will help

in verifying the tough decisions taken by the business concern by generating higher business

outcomes.

Question 3

A.

If the manager or owner of Love well Limited company wants to purchase a new

machines and before that they have to use different investment appraisal techniques which will

helps in finding out or analysing that they have to purchase the machine or not and on the basis

of that they can attain maximum profit or not (Egginton, Van Ness and Van Ness, 2016).

Purchasing new machine - £275,000

Annual Cash Inflow - £85000

Cash outflow - £12500 in every six year.

Depreciation would be charged by using Straight line method and it would be charged on

15%.

Cost of capital – 12%.

Different appraisal technique which they can use to find that they have to purchase

machine or not. They are pay back period method, accounting rate of return tool, net present

value and Internal rate of return method (Karadag, 2015). Along with this the owner of Love

well limited have to check that this method increase the profitability or economic feasibility by

acquiring the machines.

1. Pay back Period method:

Year Cash Inflow Cumulative Cash inflow

1 72500 72500

2 72500 145000

3 72500 217500

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4 72500 290000

5 72500 362500

6 113750 476250

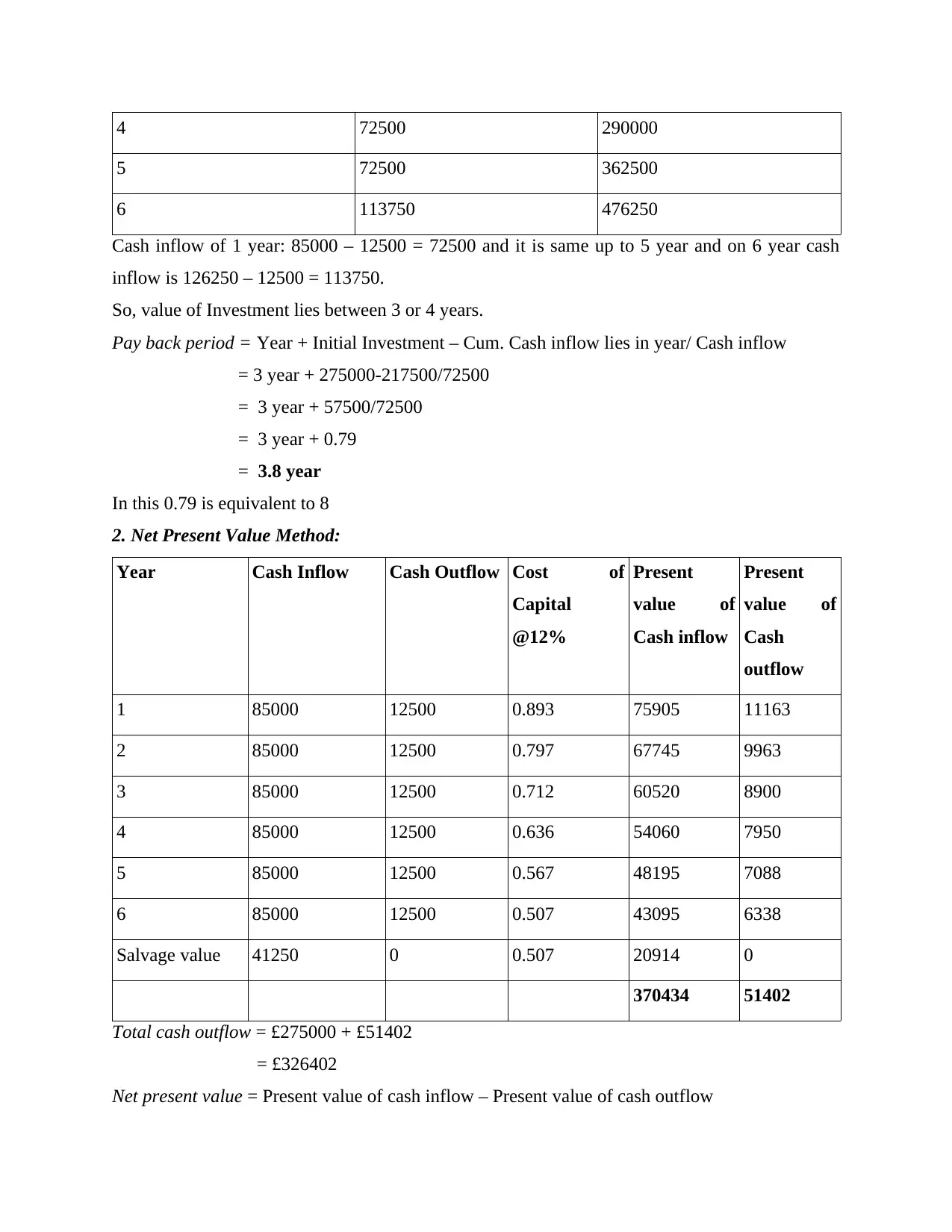

Cash inflow of 1 year: 85000 – 12500 = 72500 and it is same up to 5 year and on 6 year cash

inflow is 126250 – 12500 = 113750.

So, value of Investment lies between 3 or 4 years.

Pay back period = Year + Initial Investment – Cum. Cash inflow lies in year/ Cash inflow

= 3 year + 275000-217500/72500

= 3 year + 57500/72500

= 3 year + 0.79

= 3.8 year

In this 0.79 is equivalent to 8

2. Net Present Value Method:

Year Cash Inflow Cash Outflow Cost of

Capital

@12%

Present

value of

Cash inflow

Present

value of

Cash

outflow

1 85000 12500 0.893 75905 11163

2 85000 12500 0.797 67745 9963

3 85000 12500 0.712 60520 8900

4 85000 12500 0.636 54060 7950

5 85000 12500 0.567 48195 7088

6 85000 12500 0.507 43095 6338

Salvage value 41250 0 0.507 20914 0

370434 51402

Total cash outflow = £275000 + £51402

= £326402

Net present value = Present value of cash inflow – Present value of cash outflow

5 72500 362500

6 113750 476250

Cash inflow of 1 year: 85000 – 12500 = 72500 and it is same up to 5 year and on 6 year cash

inflow is 126250 – 12500 = 113750.

So, value of Investment lies between 3 or 4 years.

Pay back period = Year + Initial Investment – Cum. Cash inflow lies in year/ Cash inflow

= 3 year + 275000-217500/72500

= 3 year + 57500/72500

= 3 year + 0.79

= 3.8 year

In this 0.79 is equivalent to 8

2. Net Present Value Method:

Year Cash Inflow Cash Outflow Cost of

Capital

@12%

Present

value of

Cash inflow

Present

value of

Cash

outflow

1 85000 12500 0.893 75905 11163

2 85000 12500 0.797 67745 9963

3 85000 12500 0.712 60520 8900

4 85000 12500 0.636 54060 7950

5 85000 12500 0.567 48195 7088

6 85000 12500 0.507 43095 6338

Salvage value 41250 0 0.507 20914 0

370434 51402

Total cash outflow = £275000 + £51402

= £326402

Net present value = Present value of cash inflow – Present value of cash outflow

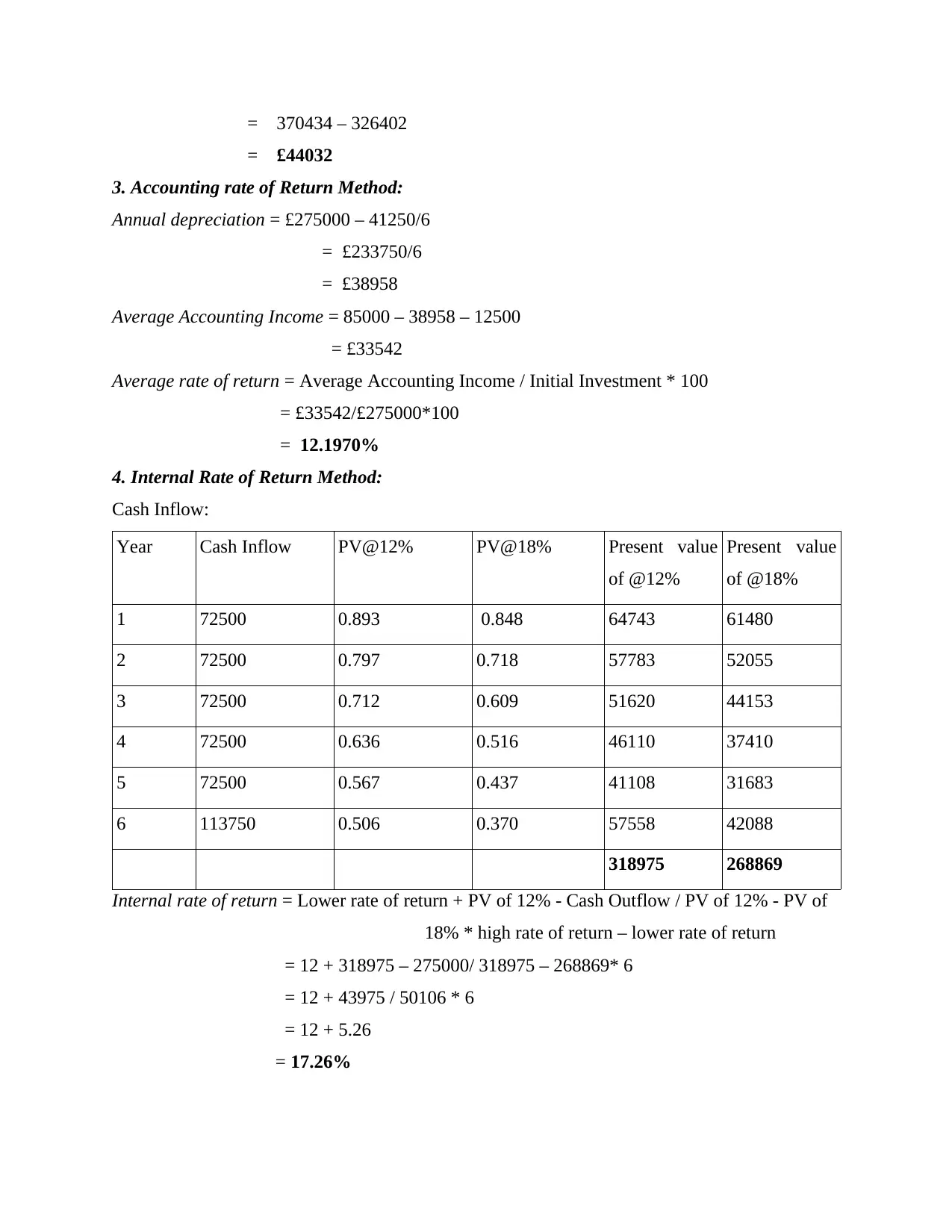

= 370434 – 326402

= £44032

3. Accounting rate of Return Method:

Annual depreciation = £275000 – 41250/6

= £233750/6

= £38958

Average Accounting Income = 85000 – 38958 – 12500

= £33542

Average rate of return = Average Accounting Income / Initial Investment * 100

= £33542/£275000*100

= 12.1970%

4. Internal Rate of Return Method:

Cash Inflow:

Year Cash Inflow PV@12% PV@18% Present value

of @12%

Present value

of @18%

1 72500 0.893 0.848 64743 61480

2 72500 0.797 0.718 57783 52055

3 72500 0.712 0.609 51620 44153

4 72500 0.636 0.516 46110 37410

5 72500 0.567 0.437 41108 31683

6 113750 0.506 0.370 57558 42088

318975 268869

Internal rate of return = Lower rate of return + PV of 12% - Cash Outflow / PV of 12% - PV of

18% * high rate of return – lower rate of return

= 12 + 318975 – 275000/ 318975 – 268869* 6

= 12 + 43975 / 50106 * 6

= 12 + 5.26

= 17.26%

= £44032

3. Accounting rate of Return Method:

Annual depreciation = £275000 – 41250/6

= £233750/6

= £38958

Average Accounting Income = 85000 – 38958 – 12500

= £33542

Average rate of return = Average Accounting Income / Initial Investment * 100

= £33542/£275000*100

= 12.1970%

4. Internal Rate of Return Method:

Cash Inflow:

Year Cash Inflow PV@12% PV@18% Present value

of @12%

Present value

of @18%

1 72500 0.893 0.848 64743 61480

2 72500 0.797 0.718 57783 52055

3 72500 0.712 0.609 51620 44153

4 72500 0.636 0.516 46110 37410

5 72500 0.567 0.437 41108 31683

6 113750 0.506 0.370 57558 42088

318975 268869

Internal rate of return = Lower rate of return + PV of 12% - Cash Outflow / PV of 12% - PV of

18% * high rate of return – lower rate of return

= 12 + 318975 – 275000/ 318975 – 268869* 6

= 12 + 43975 / 50106 * 6

= 12 + 5.26

= 17.26%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

By doing the computation using investment appraisal techniques, Pay back period is 3.8 year and

it denotes that company earn profit in approx 4 years, Net present value is 44032 and it is

positive, ARR is 12.1970% and IRR is 17.26% and it helps the company in making the decision

to purchase new machine all all positive so Love well company can purchase new machine as it

helps in generating maximum revenue.

B.

There are different appraisal techniques which company and some are stated above.

These techniques help in making the correct decisions and also helps in measuring the

productivity as well as profitability (Chua, Lowe and Puxty, 2015). They are:

Pay Back Period method: It is a part of capital budgeting and it requires the specific period of

time to use the appropriate funds which assist in expanding the investment or to reach at the

break even point.

Benefits

Pay back period method is a very simple method to understand.

This method consider as a one of the fastest return on investment which means it helps in

recover the capital in a minimum period of a time.

One of the major benefit of this method is that it also works effectively in a minimum

amount of investment.

This method is also implemented without the help of group of employees.

It is very simple to calculate the pay back period because of their simplest formula which

doesn't requires any specialised persons (Francis, Hasan and Wu, 2015).

Limitations

The first and foremost disadvantage of the pay back period is that it ignores the time

which means it doest not consider time value of money.

The other drawback is that it does not consider the cash inflows which may arise after the

recovery of a initial investment.

One of the major drawback is that pay back period motive is to earn only short term

profitability which means this method is not applicable on the long term projects.

Absence of skilled and specialised persons due to which hidden problems may arise

which may harm the organization as well as employees (Mulherin and Aziz Simsir,

2015).

it denotes that company earn profit in approx 4 years, Net present value is 44032 and it is

positive, ARR is 12.1970% and IRR is 17.26% and it helps the company in making the decision

to purchase new machine all all positive so Love well company can purchase new machine as it

helps in generating maximum revenue.

B.

There are different appraisal techniques which company and some are stated above.

These techniques help in making the correct decisions and also helps in measuring the

productivity as well as profitability (Chua, Lowe and Puxty, 2015). They are:

Pay Back Period method: It is a part of capital budgeting and it requires the specific period of

time to use the appropriate funds which assist in expanding the investment or to reach at the

break even point.

Benefits

Pay back period method is a very simple method to understand.

This method consider as a one of the fastest return on investment which means it helps in

recover the capital in a minimum period of a time.

One of the major benefit of this method is that it also works effectively in a minimum

amount of investment.

This method is also implemented without the help of group of employees.

It is very simple to calculate the pay back period because of their simplest formula which

doesn't requires any specialised persons (Francis, Hasan and Wu, 2015).

Limitations

The first and foremost disadvantage of the pay back period is that it ignores the time

which means it doest not consider time value of money.

The other drawback is that it does not consider the cash inflows which may arise after the

recovery of a initial investment.

One of the major drawback is that pay back period motive is to earn only short term

profitability which means this method is not applicable on the long term projects.

Absence of skilled and specialised persons due to which hidden problems may arise

which may harm the organization as well as employees (Mulherin and Aziz Simsir,

2015).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Net present value method: It is a type of techniques which is related to investment appraisal as

it succour in measuring the profitability. It is calculated by using the formula that is reducing the

value of cash outflow from the present value of cash inflow within a given time.

Benefits

The major advantage of the net present value method is that it express the accurate

information about a particular investment by describing their benefits for the company.

This means it helps in determining that project will increase firm's value or not.

It help the enterprise in understanding that project will maximize profit or not (Mathuva,

2015).

In fact this method also shows the actual amount incurred or profit of each year to make

effective budgeting with the help of previous facts and figures.

Apart from this net present value method helps in selecting best alternatives from

available project to maximize their profits.

Limitations

One of the biggest drawback of this method is that it does not calculate accurate results

which means there is a absence of accuracy which sometime create a problem for

enterprises in a selection of a project.

In fact this method is a very time consuming method because of their long path of

calculation.

It requires a expertise advice and specialised person to conduct this method effectively.

Apart from all the above disadvantages last one is that it is one of the expensive

technique in a capital budgeting (Marciukaityte, 2015).

Average rate of return method: It is ration which denotes the financial condition and used in

the capital budgeting. It is a concept of time and a value of money.

Benefits

Basically this method is based on the accounting information so that other data and

management reports are not required in average rate of return method.

ARR is one of the simplest method to understand and it is very simple in calculation.

In fact this method is mainly based on the profit of accounts so it measures the

investment profits (Bradley and Chen, 2015).

it succour in measuring the profitability. It is calculated by using the formula that is reducing the

value of cash outflow from the present value of cash inflow within a given time.

Benefits

The major advantage of the net present value method is that it express the accurate

information about a particular investment by describing their benefits for the company.

This means it helps in determining that project will increase firm's value or not.

It help the enterprise in understanding that project will maximize profit or not (Mathuva,

2015).

In fact this method also shows the actual amount incurred or profit of each year to make

effective budgeting with the help of previous facts and figures.

Apart from this net present value method helps in selecting best alternatives from

available project to maximize their profits.

Limitations

One of the biggest drawback of this method is that it does not calculate accurate results

which means there is a absence of accuracy which sometime create a problem for

enterprises in a selection of a project.

In fact this method is a very time consuming method because of their long path of

calculation.

It requires a expertise advice and specialised person to conduct this method effectively.

Apart from all the above disadvantages last one is that it is one of the expensive

technique in a capital budgeting (Marciukaityte, 2015).

Average rate of return method: It is ration which denotes the financial condition and used in

the capital budgeting. It is a concept of time and a value of money.

Benefits

Basically this method is based on the accounting information so that other data and

management reports are not required in average rate of return method.

ARR is one of the simplest method to understand and it is very simple in calculation.

In fact this method is mainly based on the profit of accounts so it measures the

investment profits (Bradley and Chen, 2015).

One of the useful and effective method which covers all the factors visible in the capital

budgeting so that accurate profit and loss must be calculated after tax and depreciation.

Limitations

The main and foremost limitations is that it did not consider the time value of money.

This method is calculated in different-different ways which resulted in different outcomes

or results which creates a state of confusion.

ARR is very much influenced by non cash items for example bad debts, depreciation

while calculating the profit (Nguyen, Nguyen and Yin, 2015).

Apart from this, this method is one of the complicated technique of calculating average

rate of return on investment.

Absence of other special reports of the accounting systems which may creates a

inappropriate presence of information and data.

Internal rate of return method: It is also used in capital budgeting and also assist in measuring

the profitability of the potential investments. IRR having a discount rate which makes the net

present values of all cash flows from a specific project to zero.

Benefits

One of the indispensable technique in a capital budgeting because only this method can

consider the time value of money while evaluation of a project.

The another benefit is that it is very simple while doing interpretations after calculation of

IRR.

In fact managers can easily estimate required rate of return and comfortably take the

decisions.

It covers all the relevant internal and external factors of the budgeting method to calculate

the internal rate of return with the help of discounting rate and present value of the

discounting rate (Financial Management and Risk, MSc, 2017).

It is not easy to practically apply this method because of their complex nature and broad

concept as well as due to absence of accuracy.

One of the major limitation of this method is that it ignores the size of the project while

evaluating the projects.

budgeting so that accurate profit and loss must be calculated after tax and depreciation.

Limitations

The main and foremost limitations is that it did not consider the time value of money.

This method is calculated in different-different ways which resulted in different outcomes

or results which creates a state of confusion.

ARR is very much influenced by non cash items for example bad debts, depreciation

while calculating the profit (Nguyen, Nguyen and Yin, 2015).

Apart from this, this method is one of the complicated technique of calculating average

rate of return on investment.

Absence of other special reports of the accounting systems which may creates a

inappropriate presence of information and data.

Internal rate of return method: It is also used in capital budgeting and also assist in measuring

the profitability of the potential investments. IRR having a discount rate which makes the net

present values of all cash flows from a specific project to zero.

Benefits

One of the indispensable technique in a capital budgeting because only this method can

consider the time value of money while evaluation of a project.

The another benefit is that it is very simple while doing interpretations after calculation of

IRR.

In fact managers can easily estimate required rate of return and comfortably take the

decisions.

It covers all the relevant internal and external factors of the budgeting method to calculate

the internal rate of return with the help of discounting rate and present value of the

discounting rate (Financial Management and Risk, MSc, 2017).

It is not easy to practically apply this method because of their complex nature and broad

concept as well as due to absence of accuracy.

One of the major limitation of this method is that it ignores the size of the project while

evaluating the projects.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.