Financial Management Report: Dividend Policy & Investment Appraisal

VerifiedAdded on 2020/12/09

|13

|4312

|81

Report

AI Summary

This report provides a comprehensive analysis of financial management, focusing on dividend policy and investment appraisal techniques. It begins with an examination of dividend policy, calculating the fair price of Planet's shares using the Dividend Growth Model and addressing the model's limitations. The report then delves into investment appraisal techniques, evaluating the feasibility of purchasing a new machine for Lovewell Limited using methods such as Payback Period, Accounting Rate of Return (ARR), Net Present Value (NPV), and Internal Rate of Return (IRR). It includes detailed calculations, recommendations, and a critical evaluation of the appraisal techniques, offering a practical understanding of financial decision-making processes.

FINANCIAL

MANAGEMENT

MANAGEMENT

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

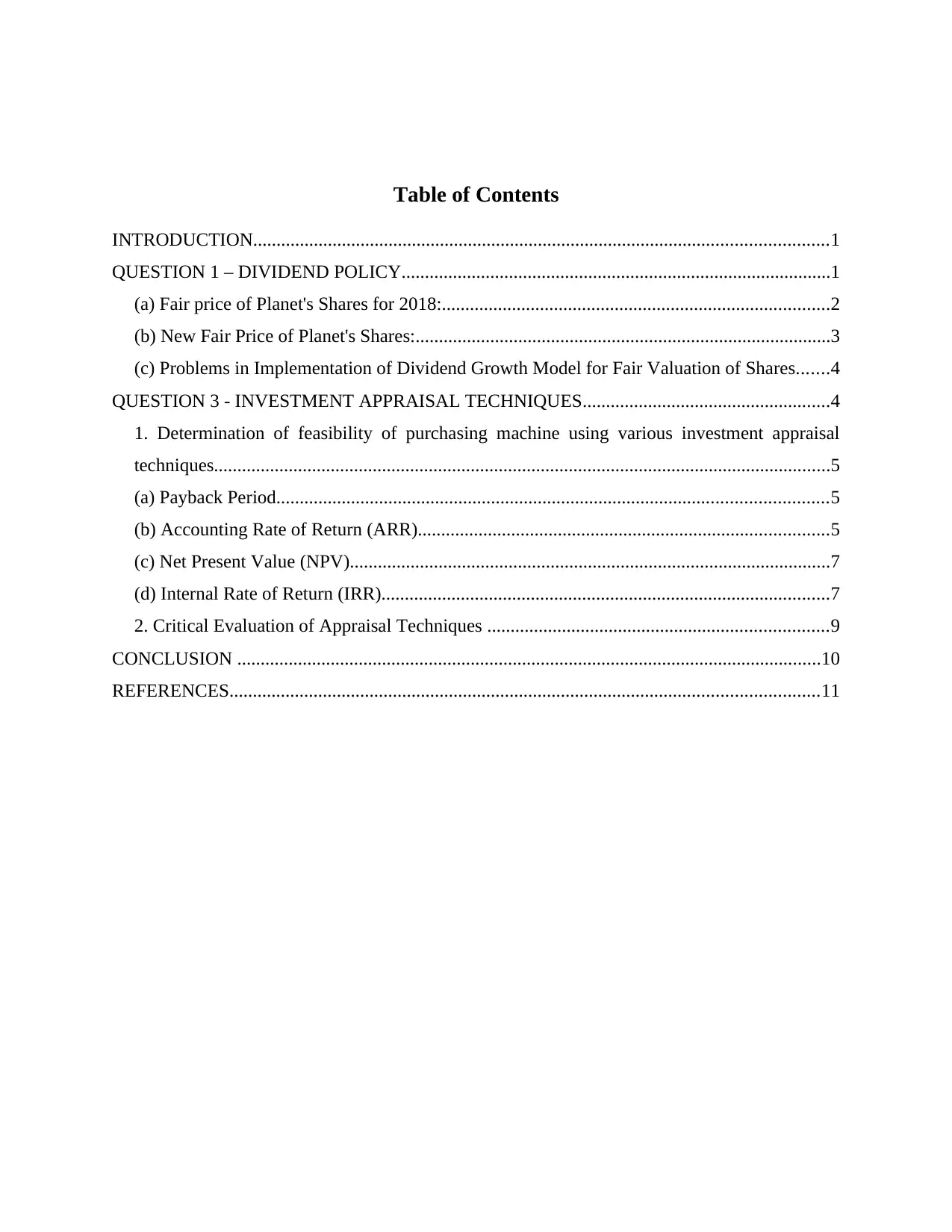

Table of Contents

INTRODUCTION...........................................................................................................................1

QUESTION 1 – DIVIDEND POLICY............................................................................................1

(a) Fair price of Planet's Shares for 2018:...................................................................................2

(b) New Fair Price of Planet's Shares:.........................................................................................3

(c) Problems in Implementation of Dividend Growth Model for Fair Valuation of Shares.......4

QUESTION 3 - INVESTMENT APPRAISAL TECHNIQUES.....................................................4

1. Determination of feasibility of purchasing machine using various investment appraisal

techniques....................................................................................................................................5

(a) Payback Period......................................................................................................................5

(b) Accounting Rate of Return (ARR)........................................................................................5

(c) Net Present Value (NPV).......................................................................................................7

(d) Internal Rate of Return (IRR)................................................................................................7

2. Critical Evaluation of Appraisal Techniques .........................................................................9

CONCLUSION .............................................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION...........................................................................................................................1

QUESTION 1 – DIVIDEND POLICY............................................................................................1

(a) Fair price of Planet's Shares for 2018:...................................................................................2

(b) New Fair Price of Planet's Shares:.........................................................................................3

(c) Problems in Implementation of Dividend Growth Model for Fair Valuation of Shares.......4

QUESTION 3 - INVESTMENT APPRAISAL TECHNIQUES.....................................................4

1. Determination of feasibility of purchasing machine using various investment appraisal

techniques....................................................................................................................................5

(a) Payback Period......................................................................................................................5

(b) Accounting Rate of Return (ARR)........................................................................................5

(c) Net Present Value (NPV).......................................................................................................7

(d) Internal Rate of Return (IRR)................................................................................................7

2. Critical Evaluation of Appraisal Techniques .........................................................................9

CONCLUSION .............................................................................................................................10

REFERENCES..............................................................................................................................11

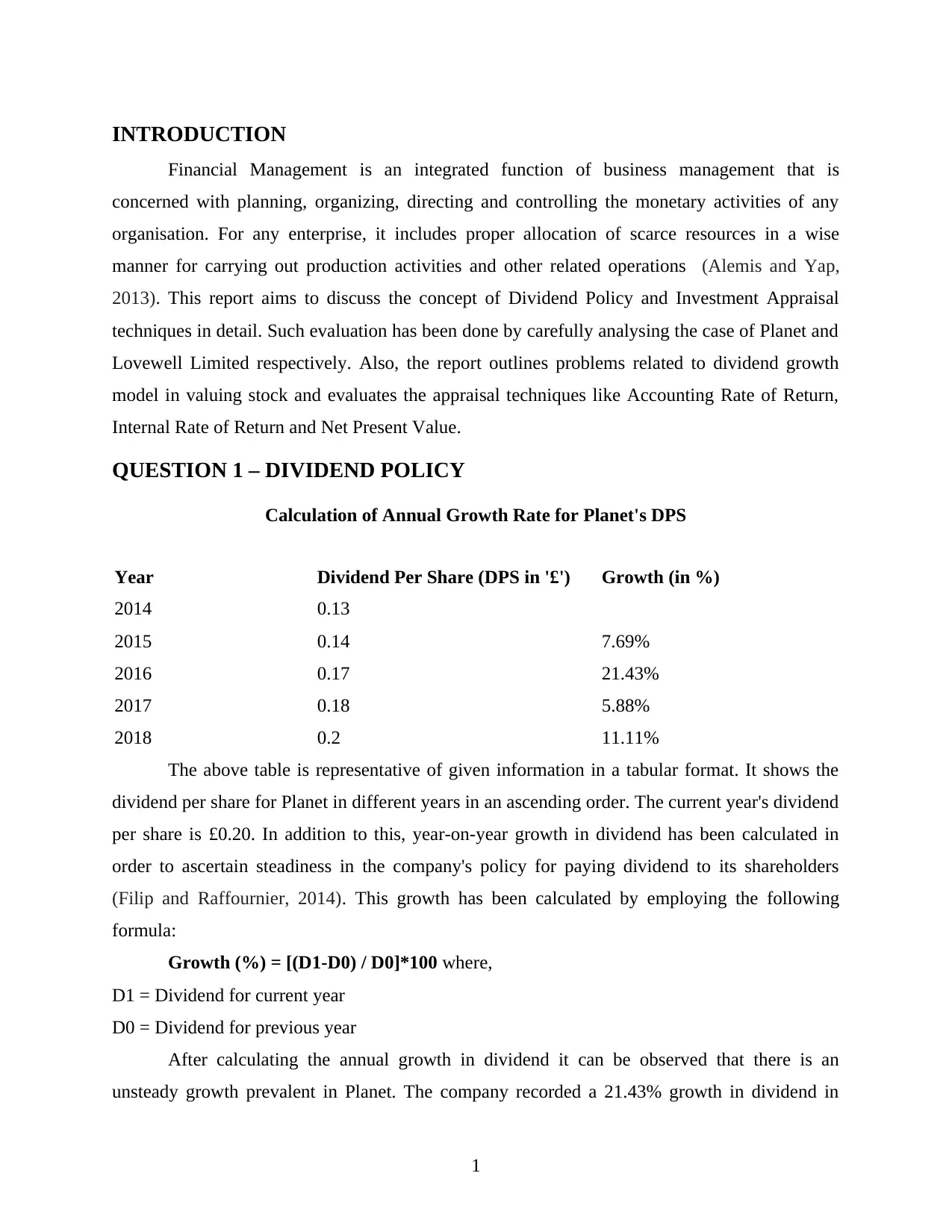

INTRODUCTION

Financial Management is an integrated function of business management that is

concerned with planning, organizing, directing and controlling the monetary activities of any

organisation. For any enterprise, it includes proper allocation of scarce resources in a wise

manner for carrying out production activities and other related operations (Alemis and Yap,

2013). This report aims to discuss the concept of Dividend Policy and Investment Appraisal

techniques in detail. Such evaluation has been done by carefully analysing the case of Planet and

Lovewell Limited respectively. Also, the report outlines problems related to dividend growth

model in valuing stock and evaluates the appraisal techniques like Accounting Rate of Return,

Internal Rate of Return and Net Present Value.

QUESTION 1 – DIVIDEND POLICY

Calculation of Annual Growth Rate for Planet's DPS

Year Dividend Per Share (DPS in '£') Growth (in %)

2014 0.13

2015 0.14 7.69%

2016 0.17 21.43%

2017 0.18 5.88%

2018 0.2 11.11%

The above table is representative of given information in a tabular format. It shows the

dividend per share for Planet in different years in an ascending order. The current year's dividend

per share is £0.20. In addition to this, year-on-year growth in dividend has been calculated in

order to ascertain steadiness in the company's policy for paying dividend to its shareholders

(Filip and Raffournier, 2014). This growth has been calculated by employing the following

formula:

Growth (%) = [(D1-D0) / D0]*100 where,

D1 = Dividend for current year

D0 = Dividend for previous year

After calculating the annual growth in dividend it can be observed that there is an

unsteady growth prevalent in Planet. The company recorded a 21.43% growth in dividend in

1

Financial Management is an integrated function of business management that is

concerned with planning, organizing, directing and controlling the monetary activities of any

organisation. For any enterprise, it includes proper allocation of scarce resources in a wise

manner for carrying out production activities and other related operations (Alemis and Yap,

2013). This report aims to discuss the concept of Dividend Policy and Investment Appraisal

techniques in detail. Such evaluation has been done by carefully analysing the case of Planet and

Lovewell Limited respectively. Also, the report outlines problems related to dividend growth

model in valuing stock and evaluates the appraisal techniques like Accounting Rate of Return,

Internal Rate of Return and Net Present Value.

QUESTION 1 – DIVIDEND POLICY

Calculation of Annual Growth Rate for Planet's DPS

Year Dividend Per Share (DPS in '£') Growth (in %)

2014 0.13

2015 0.14 7.69%

2016 0.17 21.43%

2017 0.18 5.88%

2018 0.2 11.11%

The above table is representative of given information in a tabular format. It shows the

dividend per share for Planet in different years in an ascending order. The current year's dividend

per share is £0.20. In addition to this, year-on-year growth in dividend has been calculated in

order to ascertain steadiness in the company's policy for paying dividend to its shareholders

(Filip and Raffournier, 2014). This growth has been calculated by employing the following

formula:

Growth (%) = [(D1-D0) / D0]*100 where,

D1 = Dividend for current year

D0 = Dividend for previous year

After calculating the annual growth in dividend it can be observed that there is an

unsteady growth prevalent in Planet. The company recorded a 21.43% growth in dividend in

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

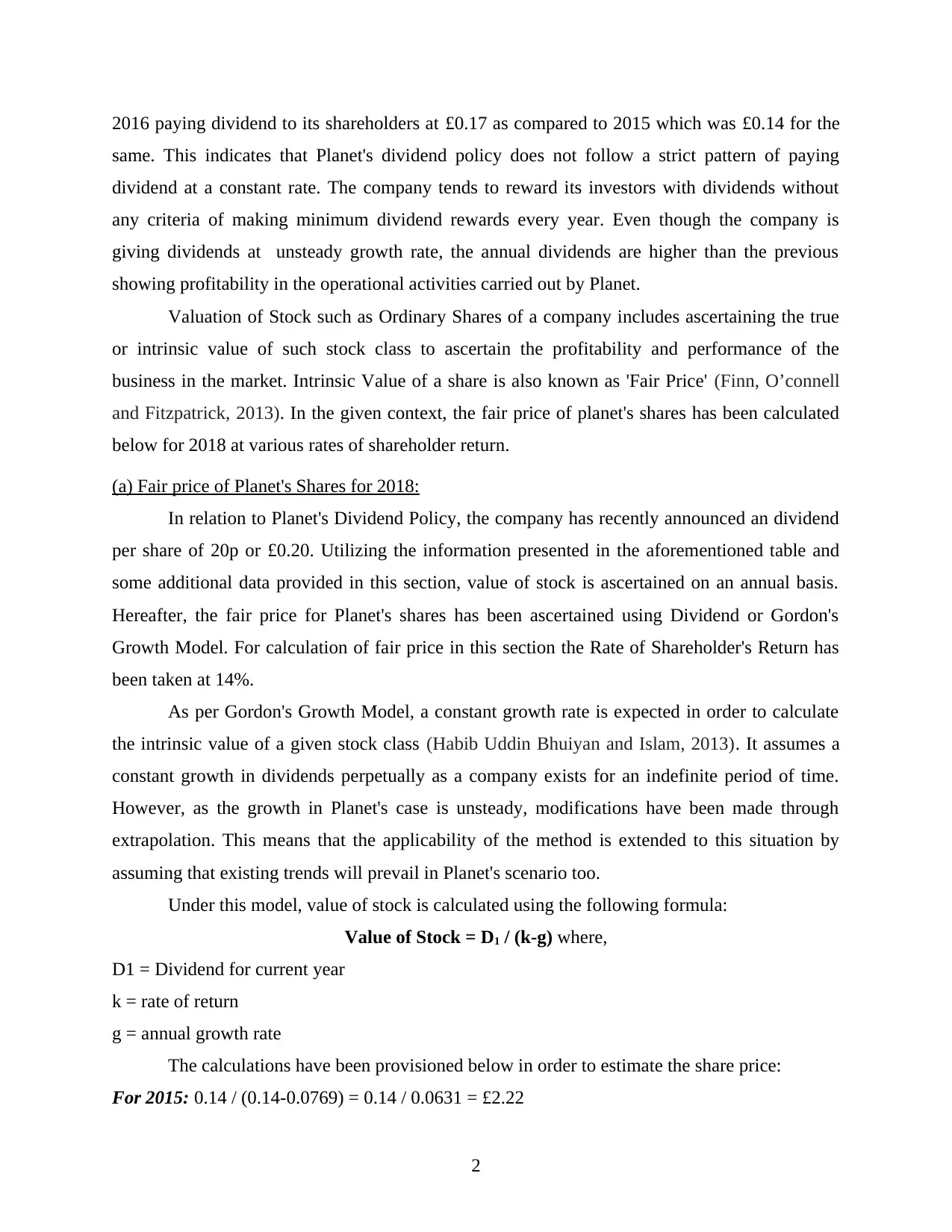

2016 paying dividend to its shareholders at £0.17 as compared to 2015 which was £0.14 for the

same. This indicates that Planet's dividend policy does not follow a strict pattern of paying

dividend at a constant rate. The company tends to reward its investors with dividends without

any criteria of making minimum dividend rewards every year. Even though the company is

giving dividends at unsteady growth rate, the annual dividends are higher than the previous

showing profitability in the operational activities carried out by Planet.

Valuation of Stock such as Ordinary Shares of a company includes ascertaining the true

or intrinsic value of such stock class to ascertain the profitability and performance of the

business in the market. Intrinsic Value of a share is also known as 'Fair Price' (Finn, O’connell

and Fitzpatrick, 2013). In the given context, the fair price of planet's shares has been calculated

below for 2018 at various rates of shareholder return.

(a) Fair price of Planet's Shares for 2018:

In relation to Planet's Dividend Policy, the company has recently announced an dividend

per share of 20p or £0.20. Utilizing the information presented in the aforementioned table and

some additional data provided in this section, value of stock is ascertained on an annual basis.

Hereafter, the fair price for Planet's shares has been ascertained using Dividend or Gordon's

Growth Model. For calculation of fair price in this section the Rate of Shareholder's Return has

been taken at 14%.

As per Gordon's Growth Model, a constant growth rate is expected in order to calculate

the intrinsic value of a given stock class (Habib Uddin Bhuiyan and Islam, 2013). It assumes a

constant growth in dividends perpetually as a company exists for an indefinite period of time.

However, as the growth in Planet's case is unsteady, modifications have been made through

extrapolation. This means that the applicability of the method is extended to this situation by

assuming that existing trends will prevail in Planet's scenario too.

Under this model, value of stock is calculated using the following formula:

Value of Stock = D1 / (k-g) where,

D1 = Dividend for current year

k = rate of return

g = annual growth rate

The calculations have been provisioned below in order to estimate the share price:

For 2015: 0.14 / (0.14-0.0769) = 0.14 / 0.0631 = £2.22

2

same. This indicates that Planet's dividend policy does not follow a strict pattern of paying

dividend at a constant rate. The company tends to reward its investors with dividends without

any criteria of making minimum dividend rewards every year. Even though the company is

giving dividends at unsteady growth rate, the annual dividends are higher than the previous

showing profitability in the operational activities carried out by Planet.

Valuation of Stock such as Ordinary Shares of a company includes ascertaining the true

or intrinsic value of such stock class to ascertain the profitability and performance of the

business in the market. Intrinsic Value of a share is also known as 'Fair Price' (Finn, O’connell

and Fitzpatrick, 2013). In the given context, the fair price of planet's shares has been calculated

below for 2018 at various rates of shareholder return.

(a) Fair price of Planet's Shares for 2018:

In relation to Planet's Dividend Policy, the company has recently announced an dividend

per share of 20p or £0.20. Utilizing the information presented in the aforementioned table and

some additional data provided in this section, value of stock is ascertained on an annual basis.

Hereafter, the fair price for Planet's shares has been ascertained using Dividend or Gordon's

Growth Model. For calculation of fair price in this section the Rate of Shareholder's Return has

been taken at 14%.

As per Gordon's Growth Model, a constant growth rate is expected in order to calculate

the intrinsic value of a given stock class (Habib Uddin Bhuiyan and Islam, 2013). It assumes a

constant growth in dividends perpetually as a company exists for an indefinite period of time.

However, as the growth in Planet's case is unsteady, modifications have been made through

extrapolation. This means that the applicability of the method is extended to this situation by

assuming that existing trends will prevail in Planet's scenario too.

Under this model, value of stock is calculated using the following formula:

Value of Stock = D1 / (k-g) where,

D1 = Dividend for current year

k = rate of return

g = annual growth rate

The calculations have been provisioned below in order to estimate the share price:

For 2015: 0.14 / (0.14-0.0769) = 0.14 / 0.0631 = £2.22

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

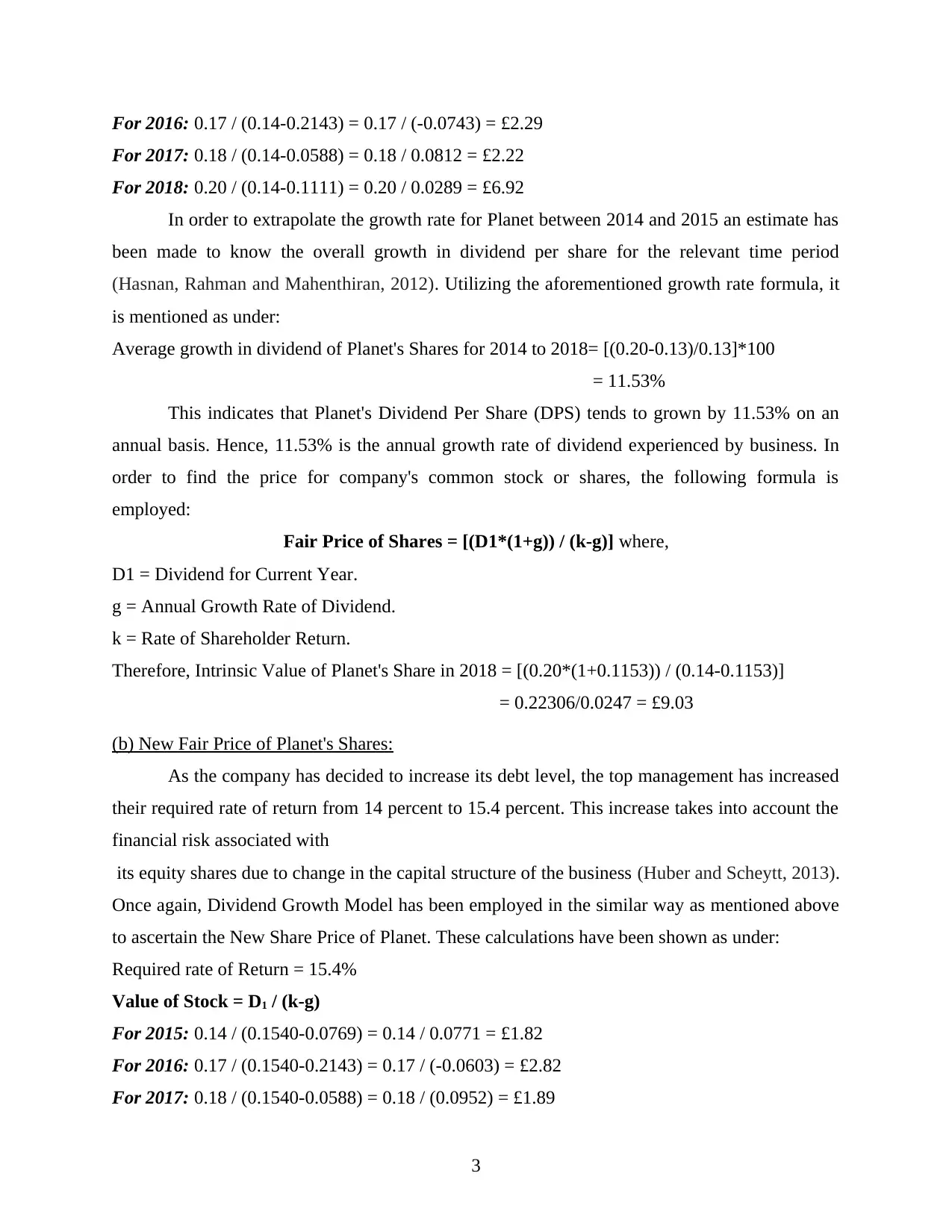

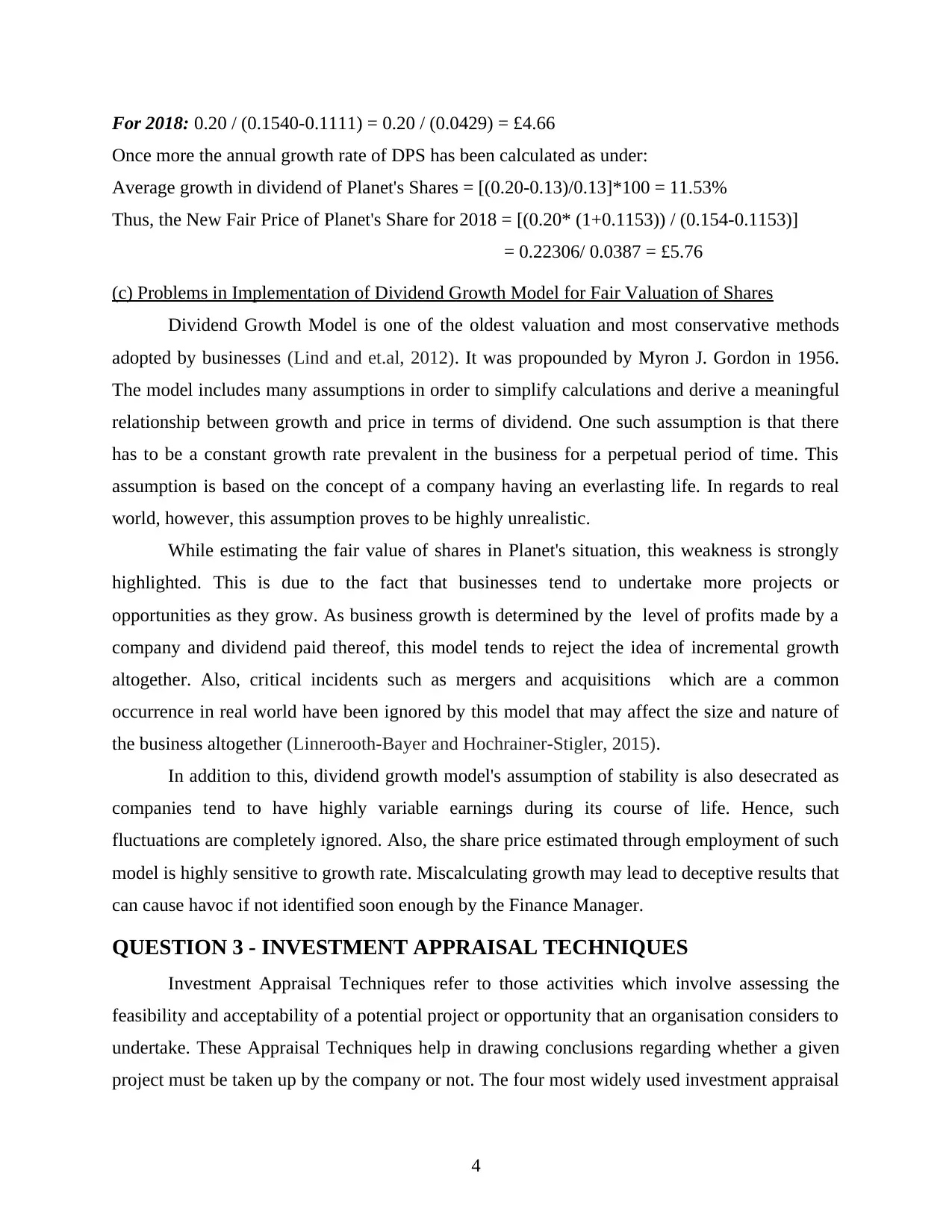

For 2016: 0.17 / (0.14-0.2143) = 0.17 / (-0.0743) = £2.29

For 2017: 0.18 / (0.14-0.0588) = 0.18 / 0.0812 = £2.22

For 2018: 0.20 / (0.14-0.1111) = 0.20 / 0.0289 = £6.92

In order to extrapolate the growth rate for Planet between 2014 and 2015 an estimate has

been made to know the overall growth in dividend per share for the relevant time period

(Hasnan, Rahman and Mahenthiran, 2012). Utilizing the aforementioned growth rate formula, it

is mentioned as under:

Average growth in dividend of Planet's Shares for 2014 to 2018= [(0.20-0.13)/0.13]*100

= 11.53%

This indicates that Planet's Dividend Per Share (DPS) tends to grown by 11.53% on an

annual basis. Hence, 11.53% is the annual growth rate of dividend experienced by business. In

order to find the price for company's common stock or shares, the following formula is

employed:

Fair Price of Shares = [(D1*(1+g)) / (k-g)] where,

D1 = Dividend for Current Year.

g = Annual Growth Rate of Dividend.

k = Rate of Shareholder Return.

Therefore, Intrinsic Value of Planet's Share in 2018 = [(0.20*(1+0.1153)) / (0.14-0.1153)]

= 0.22306/0.0247 = £9.03

(b) New Fair Price of Planet's Shares:

As the company has decided to increase its debt level, the top management has increased

their required rate of return from 14 percent to 15.4 percent. This increase takes into account the

financial risk associated with

its equity shares due to change in the capital structure of the business (Huber and Scheytt, 2013).

Once again, Dividend Growth Model has been employed in the similar way as mentioned above

to ascertain the New Share Price of Planet. These calculations have been shown as under:

Required rate of Return = 15.4%

Value of Stock = D1 / (k-g)

For 2015: 0.14 / (0.1540-0.0769) = 0.14 / 0.0771 = £1.82

For 2016: 0.17 / (0.1540-0.2143) = 0.17 / (-0.0603) = £2.82

For 2017: 0.18 / (0.1540-0.0588) = 0.18 / (0.0952) = £1.89

3

For 2017: 0.18 / (0.14-0.0588) = 0.18 / 0.0812 = £2.22

For 2018: 0.20 / (0.14-0.1111) = 0.20 / 0.0289 = £6.92

In order to extrapolate the growth rate for Planet between 2014 and 2015 an estimate has

been made to know the overall growth in dividend per share for the relevant time period

(Hasnan, Rahman and Mahenthiran, 2012). Utilizing the aforementioned growth rate formula, it

is mentioned as under:

Average growth in dividend of Planet's Shares for 2014 to 2018= [(0.20-0.13)/0.13]*100

= 11.53%

This indicates that Planet's Dividend Per Share (DPS) tends to grown by 11.53% on an

annual basis. Hence, 11.53% is the annual growth rate of dividend experienced by business. In

order to find the price for company's common stock or shares, the following formula is

employed:

Fair Price of Shares = [(D1*(1+g)) / (k-g)] where,

D1 = Dividend for Current Year.

g = Annual Growth Rate of Dividend.

k = Rate of Shareholder Return.

Therefore, Intrinsic Value of Planet's Share in 2018 = [(0.20*(1+0.1153)) / (0.14-0.1153)]

= 0.22306/0.0247 = £9.03

(b) New Fair Price of Planet's Shares:

As the company has decided to increase its debt level, the top management has increased

their required rate of return from 14 percent to 15.4 percent. This increase takes into account the

financial risk associated with

its equity shares due to change in the capital structure of the business (Huber and Scheytt, 2013).

Once again, Dividend Growth Model has been employed in the similar way as mentioned above

to ascertain the New Share Price of Planet. These calculations have been shown as under:

Required rate of Return = 15.4%

Value of Stock = D1 / (k-g)

For 2015: 0.14 / (0.1540-0.0769) = 0.14 / 0.0771 = £1.82

For 2016: 0.17 / (0.1540-0.2143) = 0.17 / (-0.0603) = £2.82

For 2017: 0.18 / (0.1540-0.0588) = 0.18 / (0.0952) = £1.89

3

For 2018: 0.20 / (0.1540-0.1111) = 0.20 / (0.0429) = £4.66

Once more the annual growth rate of DPS has been calculated as under:

Average growth in dividend of Planet's Shares = [(0.20-0.13)/0.13]*100 = 11.53%

Thus, the New Fair Price of Planet's Share for 2018 = [(0.20* (1+0.1153)) / (0.154-0.1153)]

= 0.22306/ 0.0387 = £5.76

(c) Problems in Implementation of Dividend Growth Model for Fair Valuation of Shares

Dividend Growth Model is one of the oldest valuation and most conservative methods

adopted by businesses (Lind and et.al, 2012). It was propounded by Myron J. Gordon in 1956.

The model includes many assumptions in order to simplify calculations and derive a meaningful

relationship between growth and price in terms of dividend. One such assumption is that there

has to be a constant growth rate prevalent in the business for a perpetual period of time. This

assumption is based on the concept of a company having an everlasting life. In regards to real

world, however, this assumption proves to be highly unrealistic.

While estimating the fair value of shares in Planet's situation, this weakness is strongly

highlighted. This is due to the fact that businesses tend to undertake more projects or

opportunities as they grow. As business growth is determined by the level of profits made by a

company and dividend paid thereof, this model tends to reject the idea of incremental growth

altogether. Also, critical incidents such as mergers and acquisitions which are a common

occurrence in real world have been ignored by this model that may affect the size and nature of

the business altogether (Linnerooth-Bayer and Hochrainer-Stigler, 2015).

In addition to this, dividend growth model's assumption of stability is also desecrated as

companies tend to have highly variable earnings during its course of life. Hence, such

fluctuations are completely ignored. Also, the share price estimated through employment of such

model is highly sensitive to growth rate. Miscalculating growth may lead to deceptive results that

can cause havoc if not identified soon enough by the Finance Manager.

QUESTION 3 - INVESTMENT APPRAISAL TECHNIQUES

Investment Appraisal Techniques refer to those activities which involve assessing the

feasibility and acceptability of a potential project or opportunity that an organisation considers to

undertake. These Appraisal Techniques help in drawing conclusions regarding whether a given

project must be taken up by the company or not. The four most widely used investment appraisal

4

Once more the annual growth rate of DPS has been calculated as under:

Average growth in dividend of Planet's Shares = [(0.20-0.13)/0.13]*100 = 11.53%

Thus, the New Fair Price of Planet's Share for 2018 = [(0.20* (1+0.1153)) / (0.154-0.1153)]

= 0.22306/ 0.0387 = £5.76

(c) Problems in Implementation of Dividend Growth Model for Fair Valuation of Shares

Dividend Growth Model is one of the oldest valuation and most conservative methods

adopted by businesses (Lind and et.al, 2012). It was propounded by Myron J. Gordon in 1956.

The model includes many assumptions in order to simplify calculations and derive a meaningful

relationship between growth and price in terms of dividend. One such assumption is that there

has to be a constant growth rate prevalent in the business for a perpetual period of time. This

assumption is based on the concept of a company having an everlasting life. In regards to real

world, however, this assumption proves to be highly unrealistic.

While estimating the fair value of shares in Planet's situation, this weakness is strongly

highlighted. This is due to the fact that businesses tend to undertake more projects or

opportunities as they grow. As business growth is determined by the level of profits made by a

company and dividend paid thereof, this model tends to reject the idea of incremental growth

altogether. Also, critical incidents such as mergers and acquisitions which are a common

occurrence in real world have been ignored by this model that may affect the size and nature of

the business altogether (Linnerooth-Bayer and Hochrainer-Stigler, 2015).

In addition to this, dividend growth model's assumption of stability is also desecrated as

companies tend to have highly variable earnings during its course of life. Hence, such

fluctuations are completely ignored. Also, the share price estimated through employment of such

model is highly sensitive to growth rate. Miscalculating growth may lead to deceptive results that

can cause havoc if not identified soon enough by the Finance Manager.

QUESTION 3 - INVESTMENT APPRAISAL TECHNIQUES

Investment Appraisal Techniques refer to those activities which involve assessing the

feasibility and acceptability of a potential project or opportunity that an organisation considers to

undertake. These Appraisal Techniques help in drawing conclusions regarding whether a given

project must be taken up by the company or not. The four most widely used investment appraisal

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

techniques include Payback Period, Accounting Rate of Return (ARR), Net Present Value (NPV)

and Internal Rate of Return (IRR). These have been discussed at length below in the context of

Lovewell Limited.

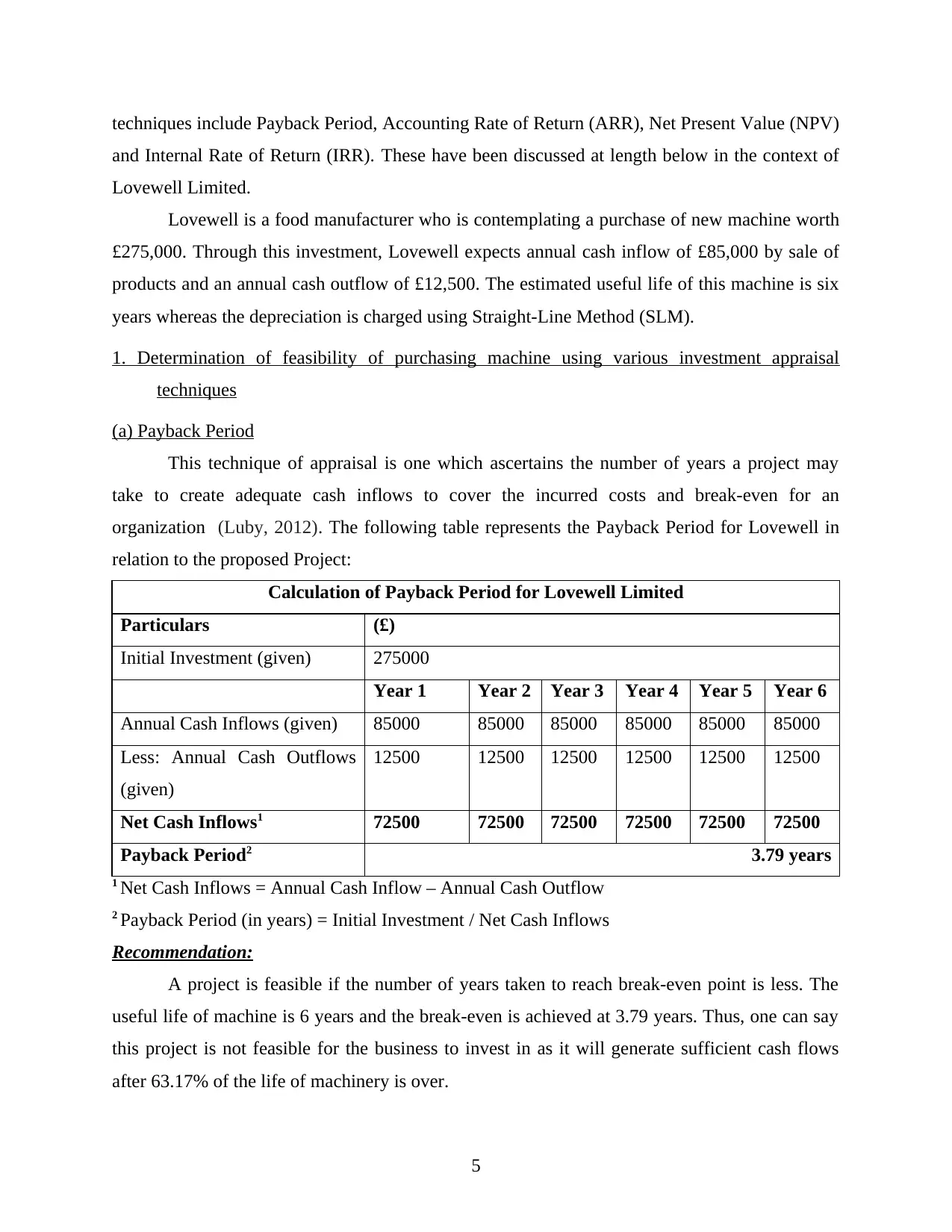

Lovewell is a food manufacturer who is contemplating a purchase of new machine worth

£275,000. Through this investment, Lovewell expects annual cash inflow of £85,000 by sale of

products and an annual cash outflow of £12,500. The estimated useful life of this machine is six

years whereas the depreciation is charged using Straight-Line Method (SLM).

1. Determination of feasibility of purchasing machine using various investment appraisal

techniques

(a) Payback Period

This technique of appraisal is one which ascertains the number of years a project may

take to create adequate cash inflows to cover the incurred costs and break-even for an

organization (Luby, 2012). The following table represents the Payback Period for Lovewell in

relation to the proposed Project:

Calculation of Payback Period for Lovewell Limited

Particulars (£)

Initial Investment (given) 275000

Year 1 Year 2 Year 3 Year 4 Year 5 Year 6

Annual Cash Inflows (given) 85000 85000 85000 85000 85000 85000

Less: Annual Cash Outflows

(given)

12500 12500 12500 12500 12500 12500

Net Cash Inflows1 72500 72500 72500 72500 72500 72500

Payback Period2 3.79 years

1 Net Cash Inflows = Annual Cash Inflow – Annual Cash Outflow

2 Payback Period (in years) = Initial Investment / Net Cash Inflows

Recommendation:

A project is feasible if the number of years taken to reach break-even point is less. The

useful life of machine is 6 years and the break-even is achieved at 3.79 years. Thus, one can say

this project is not feasible for the business to invest in as it will generate sufficient cash flows

after 63.17% of the life of machinery is over.

5

and Internal Rate of Return (IRR). These have been discussed at length below in the context of

Lovewell Limited.

Lovewell is a food manufacturer who is contemplating a purchase of new machine worth

£275,000. Through this investment, Lovewell expects annual cash inflow of £85,000 by sale of

products and an annual cash outflow of £12,500. The estimated useful life of this machine is six

years whereas the depreciation is charged using Straight-Line Method (SLM).

1. Determination of feasibility of purchasing machine using various investment appraisal

techniques

(a) Payback Period

This technique of appraisal is one which ascertains the number of years a project may

take to create adequate cash inflows to cover the incurred costs and break-even for an

organization (Luby, 2012). The following table represents the Payback Period for Lovewell in

relation to the proposed Project:

Calculation of Payback Period for Lovewell Limited

Particulars (£)

Initial Investment (given) 275000

Year 1 Year 2 Year 3 Year 4 Year 5 Year 6

Annual Cash Inflows (given) 85000 85000 85000 85000 85000 85000

Less: Annual Cash Outflows

(given)

12500 12500 12500 12500 12500 12500

Net Cash Inflows1 72500 72500 72500 72500 72500 72500

Payback Period2 3.79 years

1 Net Cash Inflows = Annual Cash Inflow – Annual Cash Outflow

2 Payback Period (in years) = Initial Investment / Net Cash Inflows

Recommendation:

A project is feasible if the number of years taken to reach break-even point is less. The

useful life of machine is 6 years and the break-even is achieved at 3.79 years. Thus, one can say

this project is not feasible for the business to invest in as it will generate sufficient cash flows

after 63.17% of the life of machinery is over.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

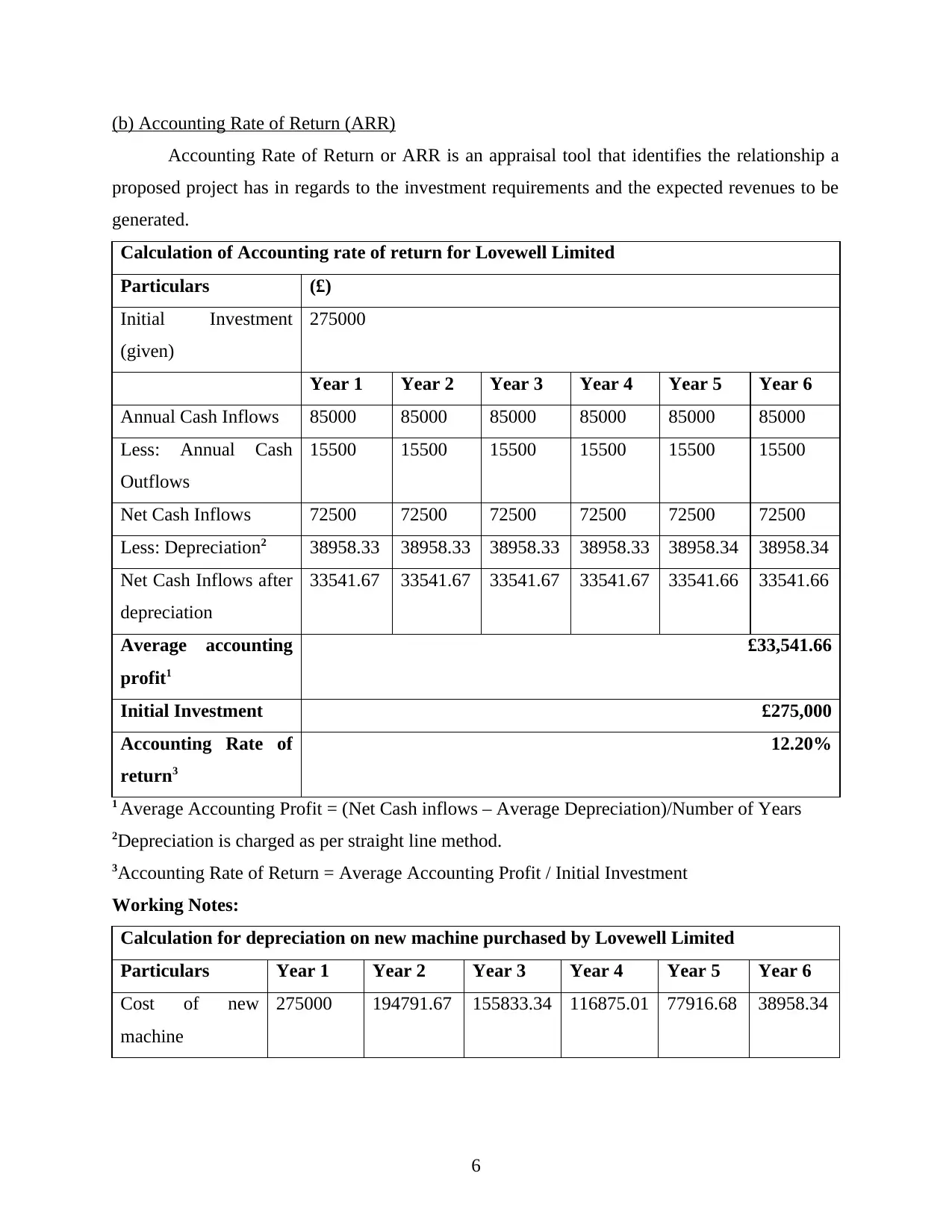

(b) Accounting Rate of Return (ARR)

Accounting Rate of Return or ARR is an appraisal tool that identifies the relationship a

proposed project has in regards to the investment requirements and the expected revenues to be

generated.

Calculation of Accounting rate of return for Lovewell Limited

Particulars (£)

Initial Investment

(given)

275000

Year 1 Year 2 Year 3 Year 4 Year 5 Year 6

Annual Cash Inflows 85000 85000 85000 85000 85000 85000

Less: Annual Cash

Outflows

15500 15500 15500 15500 15500 15500

Net Cash Inflows 72500 72500 72500 72500 72500 72500

Less: Depreciation2 38958.33 38958.33 38958.33 38958.33 38958.34 38958.34

Net Cash Inflows after

depreciation

33541.67 33541.67 33541.67 33541.67 33541.66 33541.66

Average accounting

profit1

£33,541.66

Initial Investment £275,000

Accounting Rate of

return3

12.20%

1 Average Accounting Profit = (Net Cash inflows – Average Depreciation)/Number of Years

2Depreciation is charged as per straight line method.

3Accounting Rate of Return = Average Accounting Profit / Initial Investment

Working Notes:

Calculation for depreciation on new machine purchased by Lovewell Limited

Particulars Year 1 Year 2 Year 3 Year 4 Year 5 Year 6

Cost of new

machine

275000 194791.67 155833.34 116875.01 77916.68 38958.34

6

Accounting Rate of Return or ARR is an appraisal tool that identifies the relationship a

proposed project has in regards to the investment requirements and the expected revenues to be

generated.

Calculation of Accounting rate of return for Lovewell Limited

Particulars (£)

Initial Investment

(given)

275000

Year 1 Year 2 Year 3 Year 4 Year 5 Year 6

Annual Cash Inflows 85000 85000 85000 85000 85000 85000

Less: Annual Cash

Outflows

15500 15500 15500 15500 15500 15500

Net Cash Inflows 72500 72500 72500 72500 72500 72500

Less: Depreciation2 38958.33 38958.33 38958.33 38958.33 38958.34 38958.34

Net Cash Inflows after

depreciation

33541.67 33541.67 33541.67 33541.67 33541.66 33541.66

Average accounting

profit1

£33,541.66

Initial Investment £275,000

Accounting Rate of

return3

12.20%

1 Average Accounting Profit = (Net Cash inflows – Average Depreciation)/Number of Years

2Depreciation is charged as per straight line method.

3Accounting Rate of Return = Average Accounting Profit / Initial Investment

Working Notes:

Calculation for depreciation on new machine purchased by Lovewell Limited

Particulars Year 1 Year 2 Year 3 Year 4 Year 5 Year 6

Cost of new

machine

275000 194791.67 155833.34 116875.01 77916.68 38958.34

6

Less: Salvage

Value

41250 0 0 0 0 0

Net cost of new

machine

233750 194791.67 155833.34 116875.01 77916.68 38958.34

Less:

Depreciation

38958.33 38958.33 38958.33 38958.33 38958.34 38958.34

Carried forward

balance as cost of

machinery

194791.67 155833.34 116875.01 77916.68 38958.34 0

Average

Depreciation of

new machinery4

£38,958.33

4 Average Depreciation of New Machinery is equal to the depreciation charged per year as the

amount of depreciation is same across the useful life of machinery under straight-line method.

Recommendation:

As per this model, higher rate of ARR would be more favourable to the company. Since

this project furnishes a rate of 12.20% as ARR, it is feasible to undertake such purchase on part

of Lovewell.

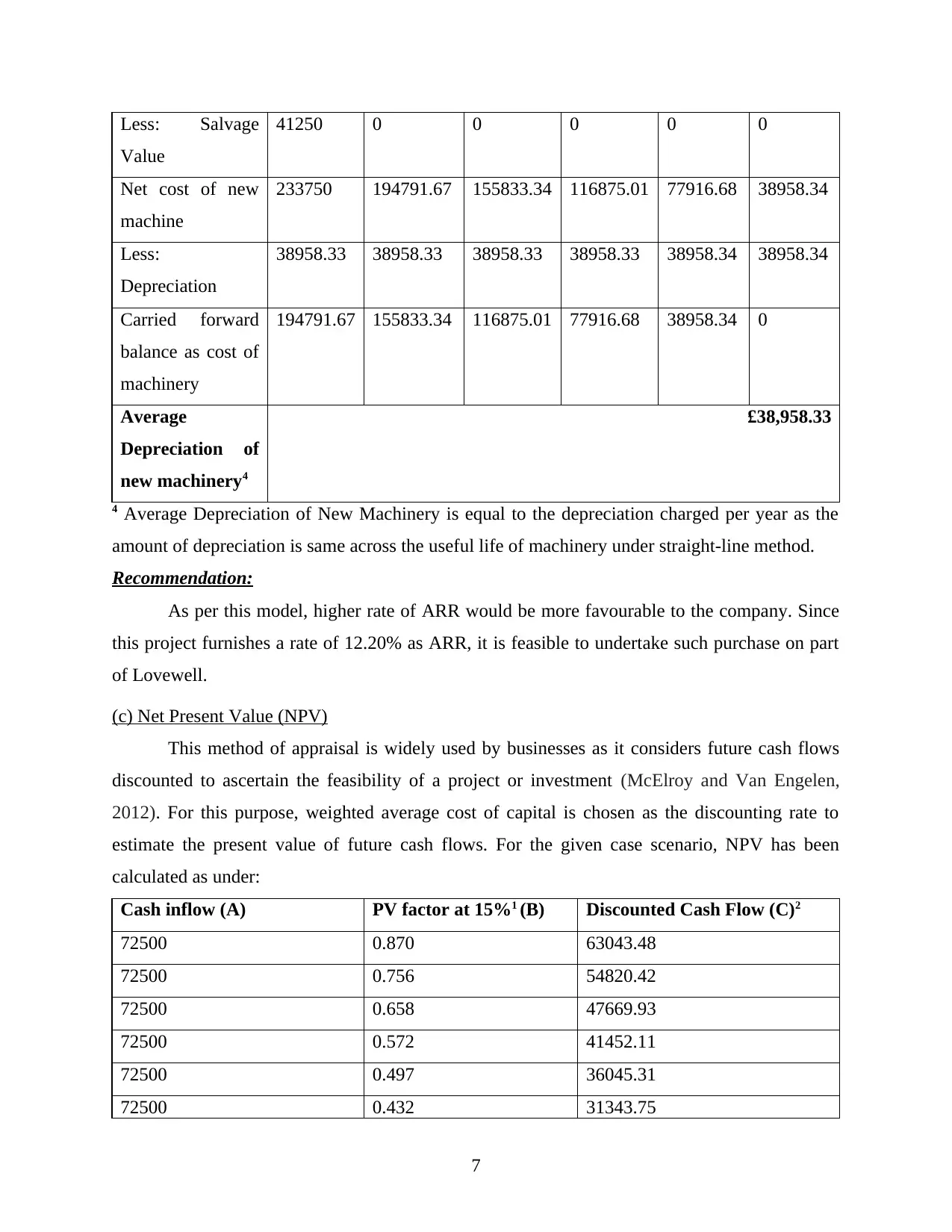

(c) Net Present Value (NPV)

This method of appraisal is widely used by businesses as it considers future cash flows

discounted to ascertain the feasibility of a project or investment (McElroy and Van Engelen,

2012). For this purpose, weighted average cost of capital is chosen as the discounting rate to

estimate the present value of future cash flows. For the given case scenario, NPV has been

calculated as under:

Cash inflow (A) PV factor at 15%1 (B) Discounted Cash Flow (C)2

72500 0.870 63043.48

72500 0.756 54820.42

72500 0.658 47669.93

72500 0.572 41452.11

72500 0.497 36045.31

72500 0.432 31343.75

7

Value

41250 0 0 0 0 0

Net cost of new

machine

233750 194791.67 155833.34 116875.01 77916.68 38958.34

Less:

Depreciation

38958.33 38958.33 38958.33 38958.33 38958.34 38958.34

Carried forward

balance as cost of

machinery

194791.67 155833.34 116875.01 77916.68 38958.34 0

Average

Depreciation of

new machinery4

£38,958.33

4 Average Depreciation of New Machinery is equal to the depreciation charged per year as the

amount of depreciation is same across the useful life of machinery under straight-line method.

Recommendation:

As per this model, higher rate of ARR would be more favourable to the company. Since

this project furnishes a rate of 12.20% as ARR, it is feasible to undertake such purchase on part

of Lovewell.

(c) Net Present Value (NPV)

This method of appraisal is widely used by businesses as it considers future cash flows

discounted to ascertain the feasibility of a project or investment (McElroy and Van Engelen,

2012). For this purpose, weighted average cost of capital is chosen as the discounting rate to

estimate the present value of future cash flows. For the given case scenario, NPV has been

calculated as under:

Cash inflow (A) PV factor at 15%1 (B) Discounted Cash Flow (C)2

72500 0.870 63043.48

72500 0.756 54820.42

72500 0.658 47669.93

72500 0.572 41452.11

72500 0.497 36045.31

72500 0.432 31343.75

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

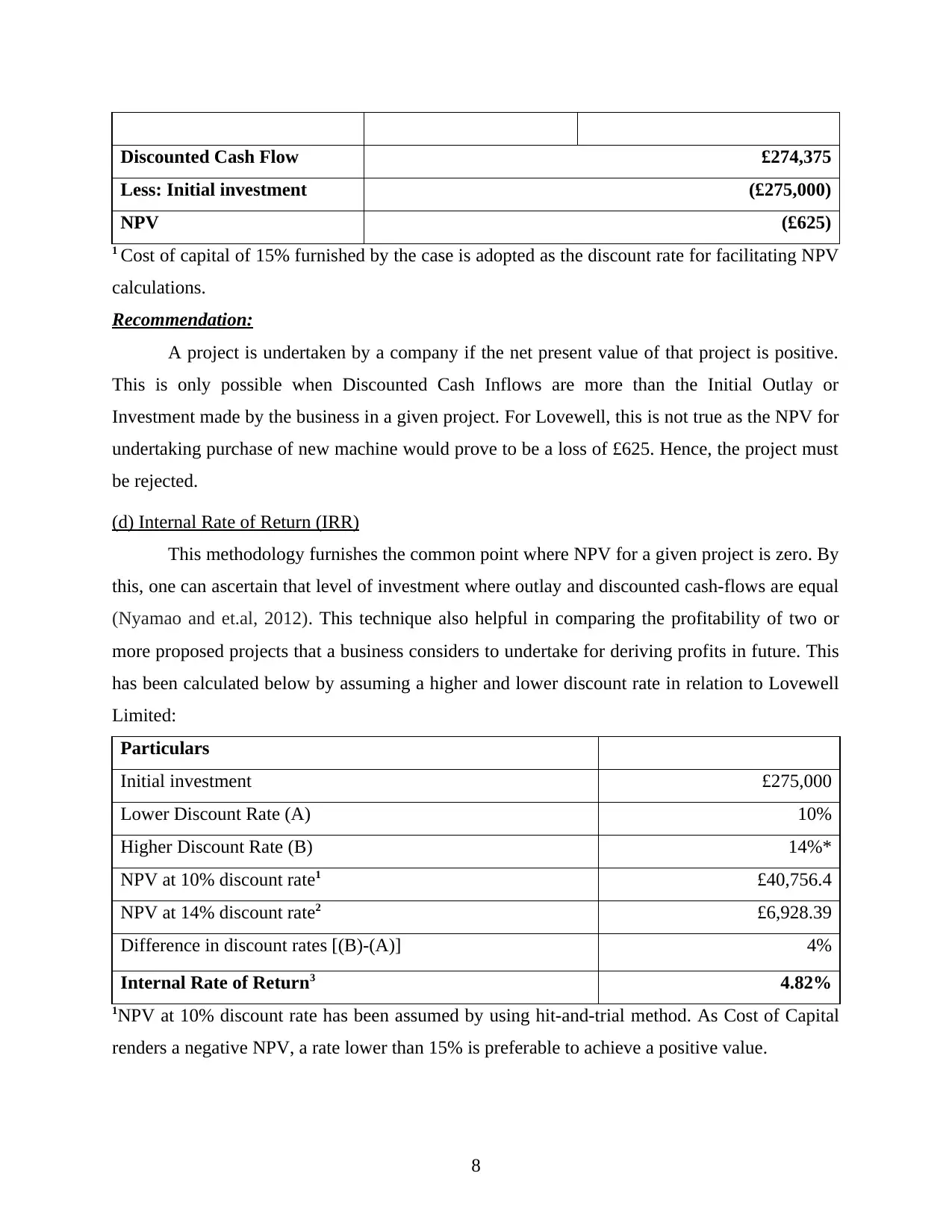

Discounted Cash Flow £274,375

Less: Initial investment (£275,000)

NPV (£625)

1 Cost of capital of 15% furnished by the case is adopted as the discount rate for facilitating NPV

calculations.

Recommendation:

A project is undertaken by a company if the net present value of that project is positive.

This is only possible when Discounted Cash Inflows are more than the Initial Outlay or

Investment made by the business in a given project. For Lovewell, this is not true as the NPV for

undertaking purchase of new machine would prove to be a loss of £625. Hence, the project must

be rejected.

(d) Internal Rate of Return (IRR)

This methodology furnishes the common point where NPV for a given project is zero. By

this, one can ascertain that level of investment where outlay and discounted cash-flows are equal

(Nyamao and et.al, 2012). This technique also helpful in comparing the profitability of two or

more proposed projects that a business considers to undertake for deriving profits in future. This

has been calculated below by assuming a higher and lower discount rate in relation to Lovewell

Limited:

Particulars

Initial investment £275,000

Lower Discount Rate (A) 10%

Higher Discount Rate (B) 14%*

NPV at 10% discount rate1 £40,756.4

NPV at 14% discount rate2 £6,928.39

Difference in discount rates [(B)-(A)] 4%

Internal Rate of Return3 4.82%

1NPV at 10% discount rate has been assumed by using hit-and-trial method. As Cost of Capital

renders a negative NPV, a rate lower than 15% is preferable to achieve a positive value.

8

Less: Initial investment (£275,000)

NPV (£625)

1 Cost of capital of 15% furnished by the case is adopted as the discount rate for facilitating NPV

calculations.

Recommendation:

A project is undertaken by a company if the net present value of that project is positive.

This is only possible when Discounted Cash Inflows are more than the Initial Outlay or

Investment made by the business in a given project. For Lovewell, this is not true as the NPV for

undertaking purchase of new machine would prove to be a loss of £625. Hence, the project must

be rejected.

(d) Internal Rate of Return (IRR)

This methodology furnishes the common point where NPV for a given project is zero. By

this, one can ascertain that level of investment where outlay and discounted cash-flows are equal

(Nyamao and et.al, 2012). This technique also helpful in comparing the profitability of two or

more proposed projects that a business considers to undertake for deriving profits in future. This

has been calculated below by assuming a higher and lower discount rate in relation to Lovewell

Limited:

Particulars

Initial investment £275,000

Lower Discount Rate (A) 10%

Higher Discount Rate (B) 14%*

NPV at 10% discount rate1 £40,756.4

NPV at 14% discount rate2 £6,928.39

Difference in discount rates [(B)-(A)] 4%

Internal Rate of Return3 4.82%

1NPV at 10% discount rate has been assumed by using hit-and-trial method. As Cost of Capital

renders a negative NPV, a rate lower than 15% is preferable to achieve a positive value.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

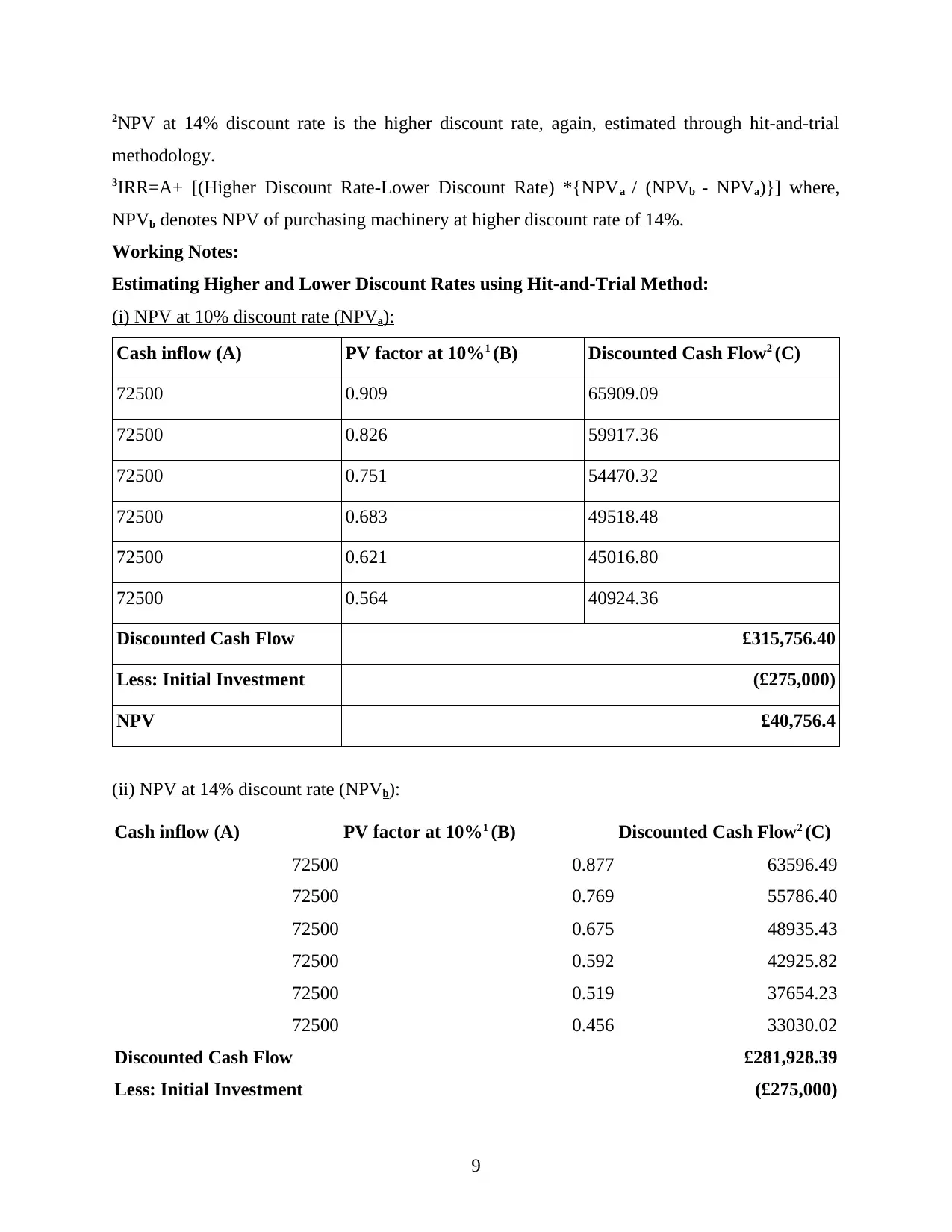

2NPV at 14% discount rate is the higher discount rate, again, estimated through hit-and-trial

methodology.

3IRR=A+ [(Higher Discount Rate-Lower Discount Rate) *{NPVa / (NPVb - NPVa)}] where,

NPVb denotes NPV of purchasing machinery at higher discount rate of 14%.

Working Notes:

Estimating Higher and Lower Discount Rates using Hit-and-Trial Method:

(i) NPV at 10% discount rate (NPVa):

Cash inflow (A) PV factor at 10%1 (B) Discounted Cash Flow2 (C)

72500 0.909 65909.09

72500 0.826 59917.36

72500 0.751 54470.32

72500 0.683 49518.48

72500 0.621 45016.80

72500 0.564 40924.36

Discounted Cash Flow £315,756.40

Less: Initial Investment (£275,000)

NPV £40,756.4

(ii) NPV at 14% discount rate (NPVb):

Cash inflow (A) PV factor at 10%1 (B) Discounted Cash Flow2 (C)

72500 0.877 63596.49

72500 0.769 55786.40

72500 0.675 48935.43

72500 0.592 42925.82

72500 0.519 37654.23

72500 0.456 33030.02

Discounted Cash Flow £281,928.39

Less: Initial Investment (£275,000)

9

methodology.

3IRR=A+ [(Higher Discount Rate-Lower Discount Rate) *{NPVa / (NPVb - NPVa)}] where,

NPVb denotes NPV of purchasing machinery at higher discount rate of 14%.

Working Notes:

Estimating Higher and Lower Discount Rates using Hit-and-Trial Method:

(i) NPV at 10% discount rate (NPVa):

Cash inflow (A) PV factor at 10%1 (B) Discounted Cash Flow2 (C)

72500 0.909 65909.09

72500 0.826 59917.36

72500 0.751 54470.32

72500 0.683 49518.48

72500 0.621 45016.80

72500 0.564 40924.36

Discounted Cash Flow £315,756.40

Less: Initial Investment (£275,000)

NPV £40,756.4

(ii) NPV at 14% discount rate (NPVb):

Cash inflow (A) PV factor at 10%1 (B) Discounted Cash Flow2 (C)

72500 0.877 63596.49

72500 0.769 55786.40

72500 0.675 48935.43

72500 0.592 42925.82

72500 0.519 37654.23

72500 0.456 33030.02

Discounted Cash Flow £281,928.39

Less: Initial Investment (£275,000)

9

NPV £6928.39

Recommendation:

As the NPV is negative, a rate of 15% is not feasible to be applied for this project. Hence

a rate of 10% and 14% is calculated to get a better understanding of the project. As the company

is able to achieve positive NPV at 14% rather than cost of capital, it is recommended to not

undertake the project.

2. Critical Evaluation of Appraisal Techniques

(a) Payback period: Benefits – Payback period method helps in revealing the payback period of an

investment. It is famous choice among the managers and the concept is highly simple to

understand and calculate. It can easily calculate without using a calculator or electronic

spreadsheet. The analysis helps in focus on risk to quickly money can be returned from

an investments (Swarbrooke and Page, 2012).

Limitations – The limitation of this method that ignores the time value of money because

cash flows received during the early years of a project get a higher weight than cash

flows received in later years. It is ignoring cash flows received after payback period and

does not consider a project's return on investment.

(b) Accounting rate of return: Benefits – The accounting rate of return easy to calculate and simple to understand like

pay back period. There are considering profits or savings over the entire period of

economic life of the project. With the help of this method recognise the concept of net

earnings.

Limitations – A true rate of return can not be evaluated on the basis of ARR and it is dis-

certain of the management. Many time this method neglect time factor which is primary

weakness of the average return method.

(c) Net Present Value: Benefits – The most important feature of the net present value method is that it is based

on the idea and NPV provides importance of time value of money. In the calculation of

NPV, both after cash flow and before cash flow over the life span of the project are

considered.

10

Recommendation:

As the NPV is negative, a rate of 15% is not feasible to be applied for this project. Hence

a rate of 10% and 14% is calculated to get a better understanding of the project. As the company

is able to achieve positive NPV at 14% rather than cost of capital, it is recommended to not

undertake the project.

2. Critical Evaluation of Appraisal Techniques

(a) Payback period: Benefits – Payback period method helps in revealing the payback period of an

investment. It is famous choice among the managers and the concept is highly simple to

understand and calculate. It can easily calculate without using a calculator or electronic

spreadsheet. The analysis helps in focus on risk to quickly money can be returned from

an investments (Swarbrooke and Page, 2012).

Limitations – The limitation of this method that ignores the time value of money because

cash flows received during the early years of a project get a higher weight than cash

flows received in later years. It is ignoring cash flows received after payback period and

does not consider a project's return on investment.

(b) Accounting rate of return: Benefits – The accounting rate of return easy to calculate and simple to understand like

pay back period. There are considering profits or savings over the entire period of

economic life of the project. With the help of this method recognise the concept of net

earnings.

Limitations – A true rate of return can not be evaluated on the basis of ARR and it is dis-

certain of the management. Many time this method neglect time factor which is primary

weakness of the average return method.

(c) Net Present Value: Benefits – The most important feature of the net present value method is that it is based

on the idea and NPV provides importance of time value of money. In the calculation of

NPV, both after cash flow and before cash flow over the life span of the project are

considered.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.