Financial Management: Cost of Capital & Investment Appraisal - APC308

VerifiedAdded on 2023/06/11

|17

|4873

|287

Report

AI Summary

This report delves into financial management, focusing on cost of capital and investment appraisal methods. It calculates market and book values, computes the weighted average cost of capital (WACC), and re-evaluates it considering changes in capital structure. The report critically examines the relationship between IRR and WACC in investment decisions and assesses the economic viability of investment projects using various appraisal techniques. It also discusses the advantages and limitations of different investment appraisal methods, providing a comprehensive analysis of financial decision-making in Faith PLC. Desklib offers more solved assignments and past papers for students.

Financial

Management

Management

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

TASK...............................................................................................................................................3

a) Calculate the market value and book value. Compute cost of capital................................3

b) Recomputed cost of capital of organisation which would reflect changes........................6

c) Critically examine that weather it is sympathize that the firms would be capable to reduce

the weighted average cost of capital.......................................................................................8

d) Critically analyse the connection between the Internal rate of return IRR and weighted

average cost of capital WACC on the purpose of investment................................................8

2. Investment appraisal method............................................................................................10

a. Compute the investment appraisal method and suggest the economic viability of the

assessment............................................................................................................................10

b. Critically measure the strategy of financial director of PM limited.................................13

c. Describe the advantages and limitations of investment appraisal methods......................13

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................16

INTRODUCTION...........................................................................................................................3

TASK...............................................................................................................................................3

a) Calculate the market value and book value. Compute cost of capital................................3

b) Recomputed cost of capital of organisation which would reflect changes........................6

c) Critically examine that weather it is sympathize that the firms would be capable to reduce

the weighted average cost of capital.......................................................................................8

d) Critically analyse the connection between the Internal rate of return IRR and weighted

average cost of capital WACC on the purpose of investment................................................8

2. Investment appraisal method............................................................................................10

a. Compute the investment appraisal method and suggest the economic viability of the

assessment............................................................................................................................10

b. Critically measure the strategy of financial director of PM limited.................................13

c. Describe the advantages and limitations of investment appraisal methods......................13

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................16

INTRODUCTION

Financial Management is a business function that deals with managing the funds available in

the business organisation. The proper utilisation of finances leads to success of the business

which is calculated by determining the return on investment of the business concern. In the

following report it states about the financial management which is used as a technique of

utilising the funds on project which yields maximum profits. It provides organised approach

towards dealing with the available data. It is process of classification, preparation, controlling

and providing guidance. It also uses and provides a coordinated approach that will help to

accomplish functional work in a fair, equitable, skilled and workable manner. The report further

covers different inquiry arrangements, which will help monitor the reserves collected so far.

Organizations selected to implement specific equipment and procedures that Trust plc is adapting

and using to examine the value of elements. The models in use can be understood as, for

example, price-to-profit ratio techniques, profit development models, and limited-revenue

strategies. The report further aids in generating ideas and recommendations that will aid in

understanding which model is ultimately best for different accessible models (Hao, Prevost and

Wongchoti, 2018).

TASK

a) Calculate the market value and book value. Compute cost of capital.

It reflects the amount of cash that an association invests resources into to find improved

results with the help of specific equipment, known as the cost of capital. For example: If an

individual spends a specific amount of cash to build another machine in his separate business to

achieve the goals and objectives set in the organization, that cost will be remembered because

hardware should be capital, not conducive to needing some return to Supported use of the

business.

WACC describes typical capital expenditures for setting up a large business that will be

paid to its partners or investors. Typically, weighted typical capital expenditures may be assets to

invest in associations that need to expand and grow in the organization, if required by the

organization. It further emphasizes the provision of common stock or securities to individuals so

that they can buy and subsidize businesses. For example: if an association asks for support, then

they should publicly offer specific shares and the organization will then make substantial normal

Financial Management is a business function that deals with managing the funds available in

the business organisation. The proper utilisation of finances leads to success of the business

which is calculated by determining the return on investment of the business concern. In the

following report it states about the financial management which is used as a technique of

utilising the funds on project which yields maximum profits. It provides organised approach

towards dealing with the available data. It is process of classification, preparation, controlling

and providing guidance. It also uses and provides a coordinated approach that will help to

accomplish functional work in a fair, equitable, skilled and workable manner. The report further

covers different inquiry arrangements, which will help monitor the reserves collected so far.

Organizations selected to implement specific equipment and procedures that Trust plc is adapting

and using to examine the value of elements. The models in use can be understood as, for

example, price-to-profit ratio techniques, profit development models, and limited-revenue

strategies. The report further aids in generating ideas and recommendations that will aid in

understanding which model is ultimately best for different accessible models (Hao, Prevost and

Wongchoti, 2018).

TASK

a) Calculate the market value and book value. Compute cost of capital.

It reflects the amount of cash that an association invests resources into to find improved

results with the help of specific equipment, known as the cost of capital. For example: If an

individual spends a specific amount of cash to build another machine in his separate business to

achieve the goals and objectives set in the organization, that cost will be remembered because

hardware should be capital, not conducive to needing some return to Supported use of the

business.

WACC describes typical capital expenditures for setting up a large business that will be

paid to its partners or investors. Typically, weighted typical capital expenditures may be assets to

invest in associations that need to expand and grow in the organization, if required by the

organization. It further emphasizes the provision of common stock or securities to individuals so

that they can buy and subsidize businesses. For example: if an association asks for support, then

they should publicly offer specific shares and the organization will then make substantial normal

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

capital expenditures and provide some normal returns to the association's associated financial

backers (Idward, Majid and Mediyati, 2018).

Variant of this approach in context of equity has been discussed earlier in the chapter of

Security Valuation. Simply speaking, if the present value arrived post application of the discount

rate is more than the current cost of investment, the valuation of the enterprise is attractive to

both stakeholders as well as externally interested parties (like stock analysts).

Market value of WACC: If an organisation computes its expected cost of capital then the

weighted average cost of capital would be formulating with the help of market value of different

elements which are not in their book value. Market value can be explained as a rate at which an

asset can be exported and implemented on basis such as who bids the highest auction amount

among different competitors available. Market value can also be referred as market price. Market

value also require the section of special figure, it then further states that they are accessible

among two associates in which they would be able to create fair value of higher transactions.

Book value of WACC: It reflects the amount of cash that an association invests in a

specific resource to learn to improve outcomes with the help of specific equipment and is known

as the cost of capital. For example: If an individual spends a certain portion of cash on building

another machine in his separate business to achieve goals and objectives set in the organization,

that cost will be remembered as hardware should be capital and against needing some return to

The business of legalizing consumption.

In this method the value of business is calculated by capitalization of company’s

expected annual maintainable profit using appropriate required rate of return or yield or

discounting rate. Annual expected maintainable profit can be calculated using weighted average

of previous years’ profits after adjusting synergy benefits or economy of scales in the same profit

(Kazakova and Sivkova, 2019).

Though the main advantage of using this method is that it is forward looking approach

however the disadvantages are estimation of expected future profit and difference in treatment of

extra ordinary and exceptional items.

The DCF is indeed a revolutionary model for valuation as FCFs truly represent the

intrinsic value of an entity. However, the whole calculation gravitates heavily on the WACC and

the TV. In fact, in many cases the TV is found to be a significant portion in final value arrived by

backers (Idward, Majid and Mediyati, 2018).

Variant of this approach in context of equity has been discussed earlier in the chapter of

Security Valuation. Simply speaking, if the present value arrived post application of the discount

rate is more than the current cost of investment, the valuation of the enterprise is attractive to

both stakeholders as well as externally interested parties (like stock analysts).

Market value of WACC: If an organisation computes its expected cost of capital then the

weighted average cost of capital would be formulating with the help of market value of different

elements which are not in their book value. Market value can be explained as a rate at which an

asset can be exported and implemented on basis such as who bids the highest auction amount

among different competitors available. Market value can also be referred as market price. Market

value also require the section of special figure, it then further states that they are accessible

among two associates in which they would be able to create fair value of higher transactions.

Book value of WACC: It reflects the amount of cash that an association invests in a

specific resource to learn to improve outcomes with the help of specific equipment and is known

as the cost of capital. For example: If an individual spends a certain portion of cash on building

another machine in his separate business to achieve goals and objectives set in the organization,

that cost will be remembered as hardware should be capital and against needing some return to

The business of legalizing consumption.

In this method the value of business is calculated by capitalization of company’s

expected annual maintainable profit using appropriate required rate of return or yield or

discounting rate. Annual expected maintainable profit can be calculated using weighted average

of previous years’ profits after adjusting synergy benefits or economy of scales in the same profit

(Kazakova and Sivkova, 2019).

Though the main advantage of using this method is that it is forward looking approach

however the disadvantages are estimation of expected future profit and difference in treatment of

extra ordinary and exceptional items.

The DCF is indeed a revolutionary model for valuation as FCFs truly represent the

intrinsic value of an entity. However, the whole calculation gravitates heavily on the WACC and

the TV. In fact, in many cases the TV is found to be a significant portion in final value arrived by

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

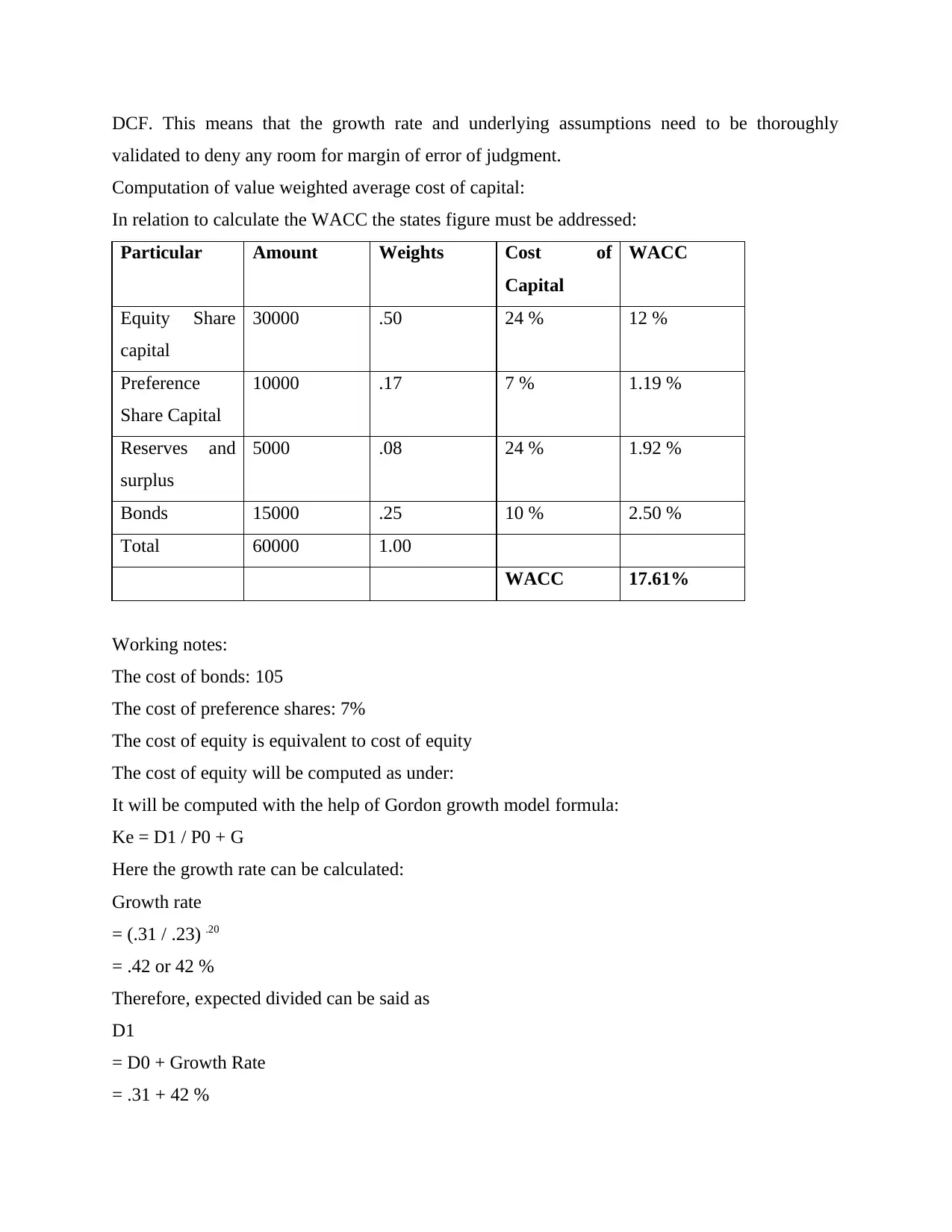

DCF. This means that the growth rate and underlying assumptions need to be thoroughly

validated to deny any room for margin of error of judgment.

Computation of value weighted average cost of capital:

In relation to calculate the WACC the states figure must be addressed:

Particular Amount Weights Cost of

Capital

WACC

Equity Share

capital

30000 .50 24 % 12 %

Preference

Share Capital

10000 .17 7 % 1.19 %

Reserves and

surplus

5000 .08 24 % 1.92 %

Bonds 15000 .25 10 % 2.50 %

Total 60000 1.00

WACC 17.61%

Working notes:

The cost of bonds: 105

The cost of preference shares: 7%

The cost of equity is equivalent to cost of equity

The cost of equity will be computed as under:

It will be computed with the help of Gordon growth model formula:

Ke = D1 / P0 + G

Here the growth rate can be calculated:

Growth rate

= (.31 / .23) .20

= .42 or 42 %

Therefore, expected divided can be said as

D1

= D0 + Growth Rate

= .31 + 42 %

validated to deny any room for margin of error of judgment.

Computation of value weighted average cost of capital:

In relation to calculate the WACC the states figure must be addressed:

Particular Amount Weights Cost of

Capital

WACC

Equity Share

capital

30000 .50 24 % 12 %

Preference

Share Capital

10000 .17 7 % 1.19 %

Reserves and

surplus

5000 .08 24 % 1.92 %

Bonds 15000 .25 10 % 2.50 %

Total 60000 1.00

WACC 17.61%

Working notes:

The cost of bonds: 105

The cost of preference shares: 7%

The cost of equity is equivalent to cost of equity

The cost of equity will be computed as under:

It will be computed with the help of Gordon growth model formula:

Ke = D1 / P0 + G

Here the growth rate can be calculated:

Growth rate

= (.31 / .23) .20

= .42 or 42 %

Therefore, expected divided can be said as

D1

= D0 + Growth Rate

= .31 + 42 %

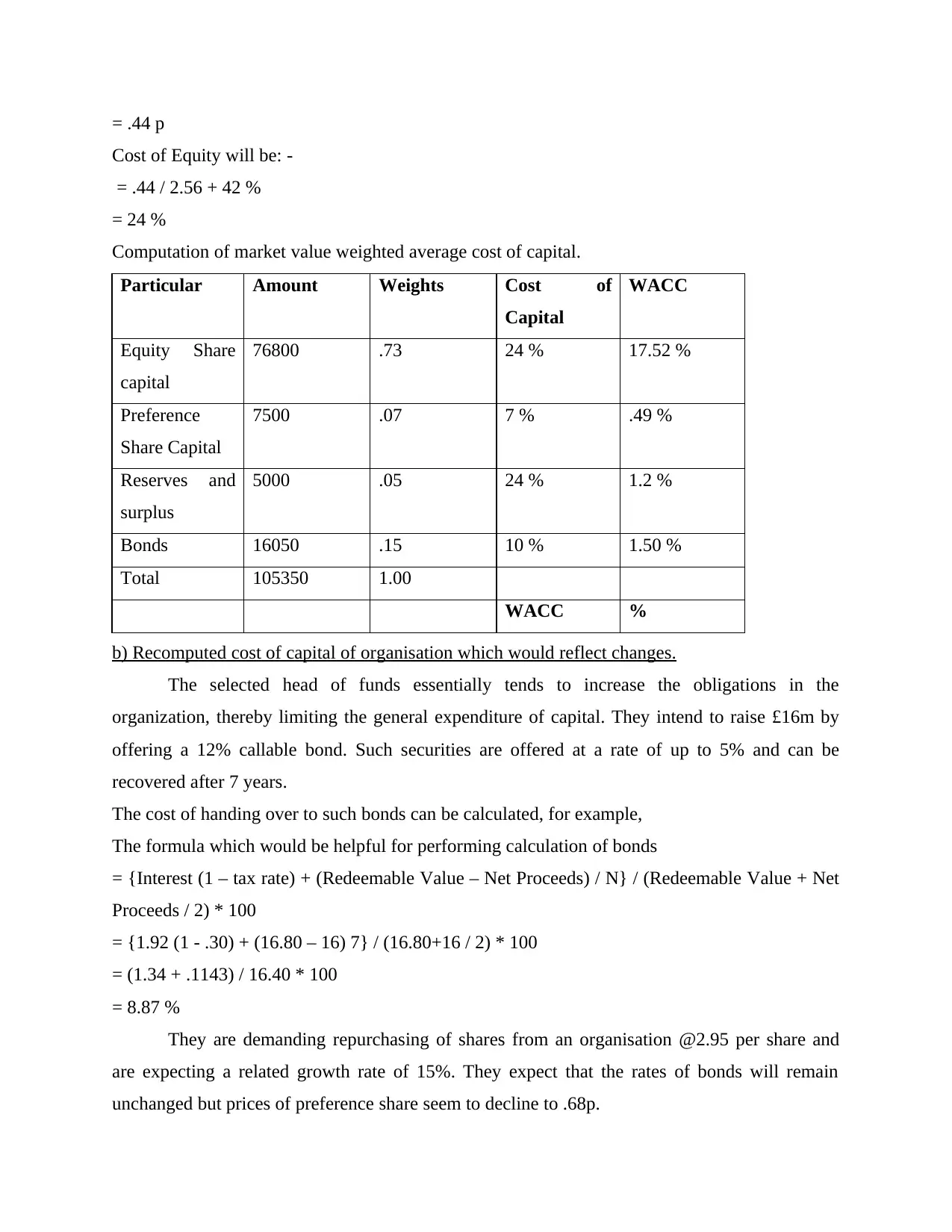

= .44 p

Cost of Equity will be: -

= .44 / 2.56 + 42 %

= 24 %

Computation of market value weighted average cost of capital.

Particular Amount Weights Cost of

Capital

WACC

Equity Share

capital

76800 .73 24 % 17.52 %

Preference

Share Capital

7500 .07 7 % .49 %

Reserves and

surplus

5000 .05 24 % 1.2 %

Bonds 16050 .15 10 % 1.50 %

Total 105350 1.00

WACC %

b) Recomputed cost of capital of organisation which would reflect changes.

The selected head of funds essentially tends to increase the obligations in the

organization, thereby limiting the general expenditure of capital. They intend to raise £16m by

offering a 12% callable bond. Such securities are offered at a rate of up to 5% and can be

recovered after 7 years.

The cost of handing over to such bonds can be calculated, for example,

The formula which would be helpful for performing calculation of bonds

= {Interest (1 – tax rate) + (Redeemable Value – Net Proceeds) / N} / (Redeemable Value + Net

Proceeds / 2) * 100

= {1.92 (1 - .30) + (16.80 – 16) 7} / (16.80+16 / 2) * 100

= (1.34 + .1143) / 16.40 * 100

= 8.87 %

They are demanding repurchasing of shares from an organisation @2.95 per share and

are expecting a related growth rate of 15%. They expect that the rates of bonds will remain

unchanged but prices of preference share seem to decline to .68p.

Cost of Equity will be: -

= .44 / 2.56 + 42 %

= 24 %

Computation of market value weighted average cost of capital.

Particular Amount Weights Cost of

Capital

WACC

Equity Share

capital

76800 .73 24 % 17.52 %

Preference

Share Capital

7500 .07 7 % .49 %

Reserves and

surplus

5000 .05 24 % 1.2 %

Bonds 16050 .15 10 % 1.50 %

Total 105350 1.00

WACC %

b) Recomputed cost of capital of organisation which would reflect changes.

The selected head of funds essentially tends to increase the obligations in the

organization, thereby limiting the general expenditure of capital. They intend to raise £16m by

offering a 12% callable bond. Such securities are offered at a rate of up to 5% and can be

recovered after 7 years.

The cost of handing over to such bonds can be calculated, for example,

The formula which would be helpful for performing calculation of bonds

= {Interest (1 – tax rate) + (Redeemable Value – Net Proceeds) / N} / (Redeemable Value + Net

Proceeds / 2) * 100

= {1.92 (1 - .30) + (16.80 – 16) 7} / (16.80+16 / 2) * 100

= (1.34 + .1143) / 16.40 * 100

= 8.87 %

They are demanding repurchasing of shares from an organisation @2.95 per share and

are expecting a related growth rate of 15%. They expect that the rates of bonds will remain

unchanged but prices of preference share seem to decline to .68p.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

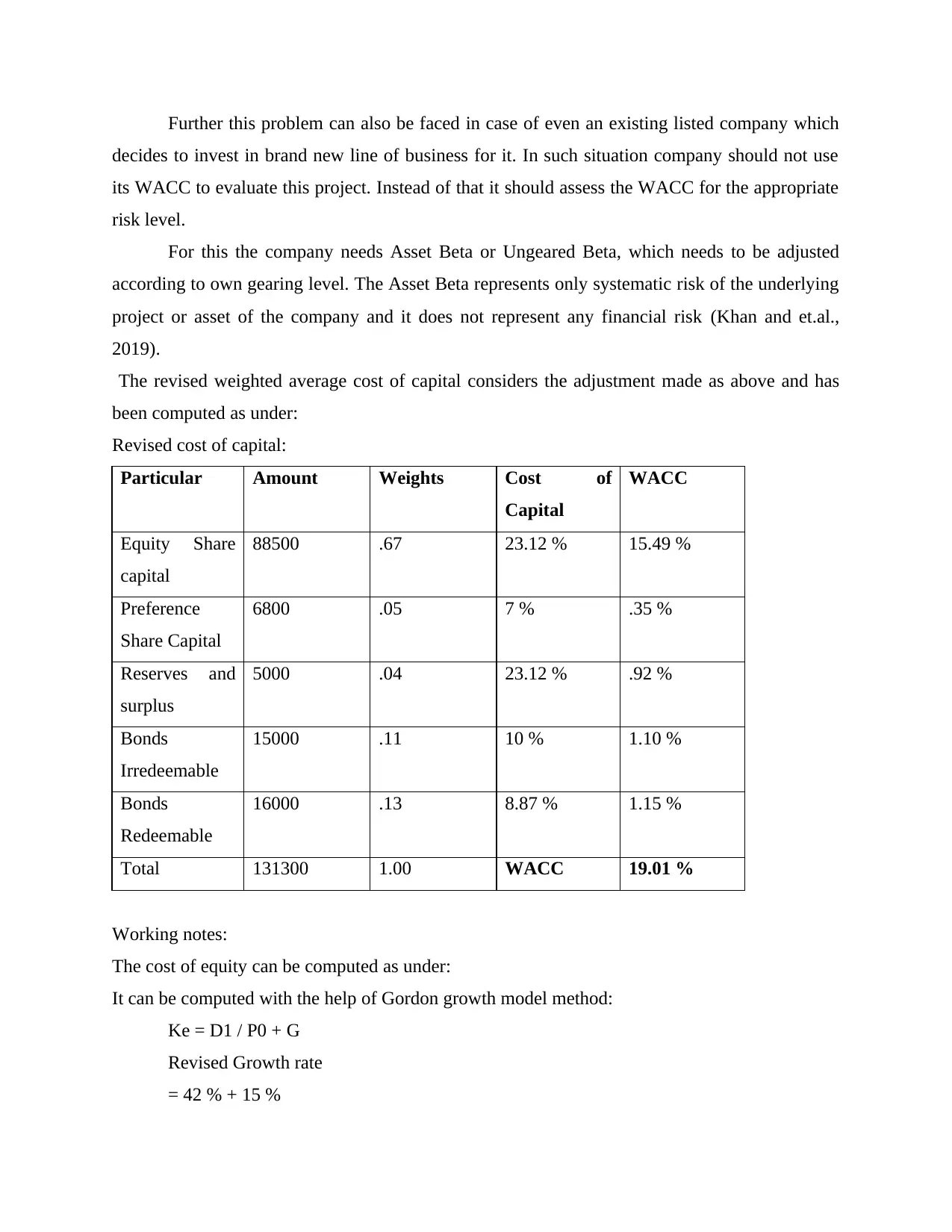

Further this problem can also be faced in case of even an existing listed company which

decides to invest in brand new line of business for it. In such situation company should not use

its WACC to evaluate this project. Instead of that it should assess the WACC for the appropriate

risk level.

For this the company needs Asset Beta or Ungeared Beta, which needs to be adjusted

according to own gearing level. The Asset Beta represents only systematic risk of the underlying

project or asset of the company and it does not represent any financial risk (Khan and et.al.,

2019).

The revised weighted average cost of capital considers the adjustment made as above and has

been computed as under:

Revised cost of capital:

Particular Amount Weights Cost of

Capital

WACC

Equity Share

capital

88500 .67 23.12 % 15.49 %

Preference

Share Capital

6800 .05 7 % .35 %

Reserves and

surplus

5000 .04 23.12 % .92 %

Bonds

Irredeemable

15000 .11 10 % 1.10 %

Bonds

Redeemable

16000 .13 8.87 % 1.15 %

Total 131300 1.00 WACC 19.01 %

Working notes:

The cost of equity can be computed as under:

It can be computed with the help of Gordon growth model method:

Ke = D1 / P0 + G

Revised Growth rate

= 42 % + 15 %

decides to invest in brand new line of business for it. In such situation company should not use

its WACC to evaluate this project. Instead of that it should assess the WACC for the appropriate

risk level.

For this the company needs Asset Beta or Ungeared Beta, which needs to be adjusted

according to own gearing level. The Asset Beta represents only systematic risk of the underlying

project or asset of the company and it does not represent any financial risk (Khan and et.al.,

2019).

The revised weighted average cost of capital considers the adjustment made as above and has

been computed as under:

Revised cost of capital:

Particular Amount Weights Cost of

Capital

WACC

Equity Share

capital

88500 .67 23.12 % 15.49 %

Preference

Share Capital

6800 .05 7 % .35 %

Reserves and

surplus

5000 .04 23.12 % .92 %

Bonds

Irredeemable

15000 .11 10 % 1.10 %

Bonds

Redeemable

16000 .13 8.87 % 1.15 %

Total 131300 1.00 WACC 19.01 %

Working notes:

The cost of equity can be computed as under:

It can be computed with the help of Gordon growth model method:

Ke = D1 / P0 + G

Revised Growth rate

= 42 % + 15 %

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

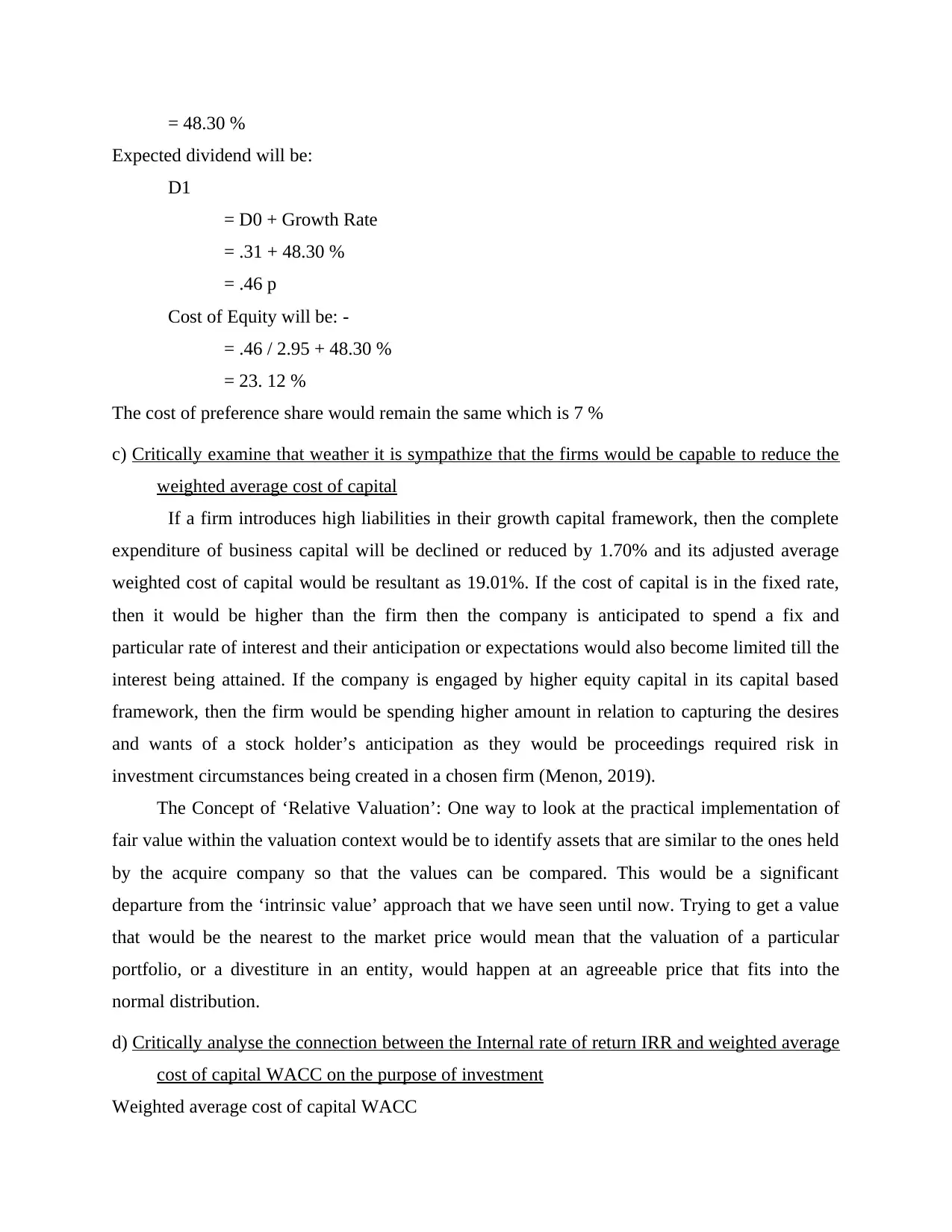

= 48.30 %

Expected dividend will be:

D1

= D0 + Growth Rate

= .31 + 48.30 %

= .46 p

Cost of Equity will be: -

= .46 / 2.95 + 48.30 %

= 23. 12 %

The cost of preference share would remain the same which is 7 %

c) Critically examine that weather it is sympathize that the firms would be capable to reduce the

weighted average cost of capital

If a firm introduces high liabilities in their growth capital framework, then the complete

expenditure of business capital will be declined or reduced by 1.70% and its adjusted average

weighted cost of capital would be resultant as 19.01%. If the cost of capital is in the fixed rate,

then it would be higher than the firm then the company is anticipated to spend a fix and

particular rate of interest and their anticipation or expectations would also become limited till the

interest being attained. If the company is engaged by higher equity capital in its capital based

framework, then the firm would be spending higher amount in relation to capturing the desires

and wants of a stock holder’s anticipation as they would be proceedings required risk in

investment circumstances being created in a chosen firm (Menon, 2019).

The Concept of ‘Relative Valuation’: One way to look at the practical implementation of

fair value within the valuation context would be to identify assets that are similar to the ones held

by the acquire company so that the values can be compared. This would be a significant

departure from the ‘intrinsic value’ approach that we have seen until now. Trying to get a value

that would be the nearest to the market price would mean that the valuation of a particular

portfolio, or a divestiture in an entity, would happen at an agreeable price that fits into the

normal distribution.

d) Critically analyse the connection between the Internal rate of return IRR and weighted average

cost of capital WACC on the purpose of investment

Weighted average cost of capital WACC

Expected dividend will be:

D1

= D0 + Growth Rate

= .31 + 48.30 %

= .46 p

Cost of Equity will be: -

= .46 / 2.95 + 48.30 %

= 23. 12 %

The cost of preference share would remain the same which is 7 %

c) Critically examine that weather it is sympathize that the firms would be capable to reduce the

weighted average cost of capital

If a firm introduces high liabilities in their growth capital framework, then the complete

expenditure of business capital will be declined or reduced by 1.70% and its adjusted average

weighted cost of capital would be resultant as 19.01%. If the cost of capital is in the fixed rate,

then it would be higher than the firm then the company is anticipated to spend a fix and

particular rate of interest and their anticipation or expectations would also become limited till the

interest being attained. If the company is engaged by higher equity capital in its capital based

framework, then the firm would be spending higher amount in relation to capturing the desires

and wants of a stock holder’s anticipation as they would be proceedings required risk in

investment circumstances being created in a chosen firm (Menon, 2019).

The Concept of ‘Relative Valuation’: One way to look at the practical implementation of

fair value within the valuation context would be to identify assets that are similar to the ones held

by the acquire company so that the values can be compared. This would be a significant

departure from the ‘intrinsic value’ approach that we have seen until now. Trying to get a value

that would be the nearest to the market price would mean that the valuation of a particular

portfolio, or a divestiture in an entity, would happen at an agreeable price that fits into the

normal distribution.

d) Critically analyse the connection between the Internal rate of return IRR and weighted average

cost of capital WACC on the purpose of investment

Weighted average cost of capital WACC

It would be very helpful for the company to create a collection of average cost of capital

in such a manner that the company would be capable to spend their returns against the investing

task being transferred out by the stockholders of the company. It includes some another

circumstances firm must issue shares when it need resources in it firm for the development and

expansion purpose. After such problems fascinated investors can spend its part of investment in

the firm.

Internal rate of return IRR

This method would be very useful when a firm desire to analyse its financial steadiness of firm

and analyse the profitable conditions frequently in a company over a given time period. It helps

the investor in terms of investing a related firm would prove to be advantageous and good or not.

There is one formula to compute the internal rate of return of a company.

IRR = Cash flow / (1+r)i

In this report it can explain the relation of IRR and WACC:

The final connection among them is IRR < WACC which shows that the internal rate of return

would be lower than the weighted average cost of capital. In general represent about the

dependent finance investment related tasks or activities which is upward from the anticipated

positivity of market competitors or in another part the investment task might also perform to be

more conservative if the purchaser is capable to spend for fixing the targets.

Also in other relationship between the IRR > WACC the weighted average cost of capital

and internal rate of return would be higher than the WACC. Basically it represent that the

investment in finance activity would be performed in a several firm it would be involved in

collaboration of several purchasers or investing the tasks performance to be highly positive then

the buying of product would be transferred out on a negotiated amount.

At this point it shows the IRR = WACC would basically mean that weighted average cost

of capital and internal rate of return they both perform to be similar as it mentions that the

investment based tasks are completed by investors in financial task working and it would grow

anticipation in the participation of market and would be reflecting the buying quantity which is

similar to the fair value of obtained company.

From an entity’s point of view, the most significant use of ROI would be to calculate the

returns generated by each individual / incremental investment on a project or different projects.

Thus, a company that has initiated a couple of projects during the year towards new business

in such a manner that the company would be capable to spend their returns against the investing

task being transferred out by the stockholders of the company. It includes some another

circumstances firm must issue shares when it need resources in it firm for the development and

expansion purpose. After such problems fascinated investors can spend its part of investment in

the firm.

Internal rate of return IRR

This method would be very useful when a firm desire to analyse its financial steadiness of firm

and analyse the profitable conditions frequently in a company over a given time period. It helps

the investor in terms of investing a related firm would prove to be advantageous and good or not.

There is one formula to compute the internal rate of return of a company.

IRR = Cash flow / (1+r)i

In this report it can explain the relation of IRR and WACC:

The final connection among them is IRR < WACC which shows that the internal rate of return

would be lower than the weighted average cost of capital. In general represent about the

dependent finance investment related tasks or activities which is upward from the anticipated

positivity of market competitors or in another part the investment task might also perform to be

more conservative if the purchaser is capable to spend for fixing the targets.

Also in other relationship between the IRR > WACC the weighted average cost of capital

and internal rate of return would be higher than the WACC. Basically it represent that the

investment in finance activity would be performed in a several firm it would be involved in

collaboration of several purchasers or investing the tasks performance to be highly positive then

the buying of product would be transferred out on a negotiated amount.

At this point it shows the IRR = WACC would basically mean that weighted average cost

of capital and internal rate of return they both perform to be similar as it mentions that the

investment based tasks are completed by investors in financial task working and it would grow

anticipation in the participation of market and would be reflecting the buying quantity which is

similar to the fair value of obtained company.

From an entity’s point of view, the most significant use of ROI would be to calculate the

returns generated by each individual / incremental investment on a project or different projects.

Thus, a company that has initiated a couple of projects during the year towards new business

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

lines can implement the ROI concept to calculate the returns on the investment and take further

decisions based on the same. Note that ROI is a historical ratio, so naturally the decision can

either only be a course corrective action, or channelling further investments into the more

successful business line (Mestry, 2018).

2. Investment appraisal method

a. Compute the investment appraisal method and suggest the economic viability of the

assessment

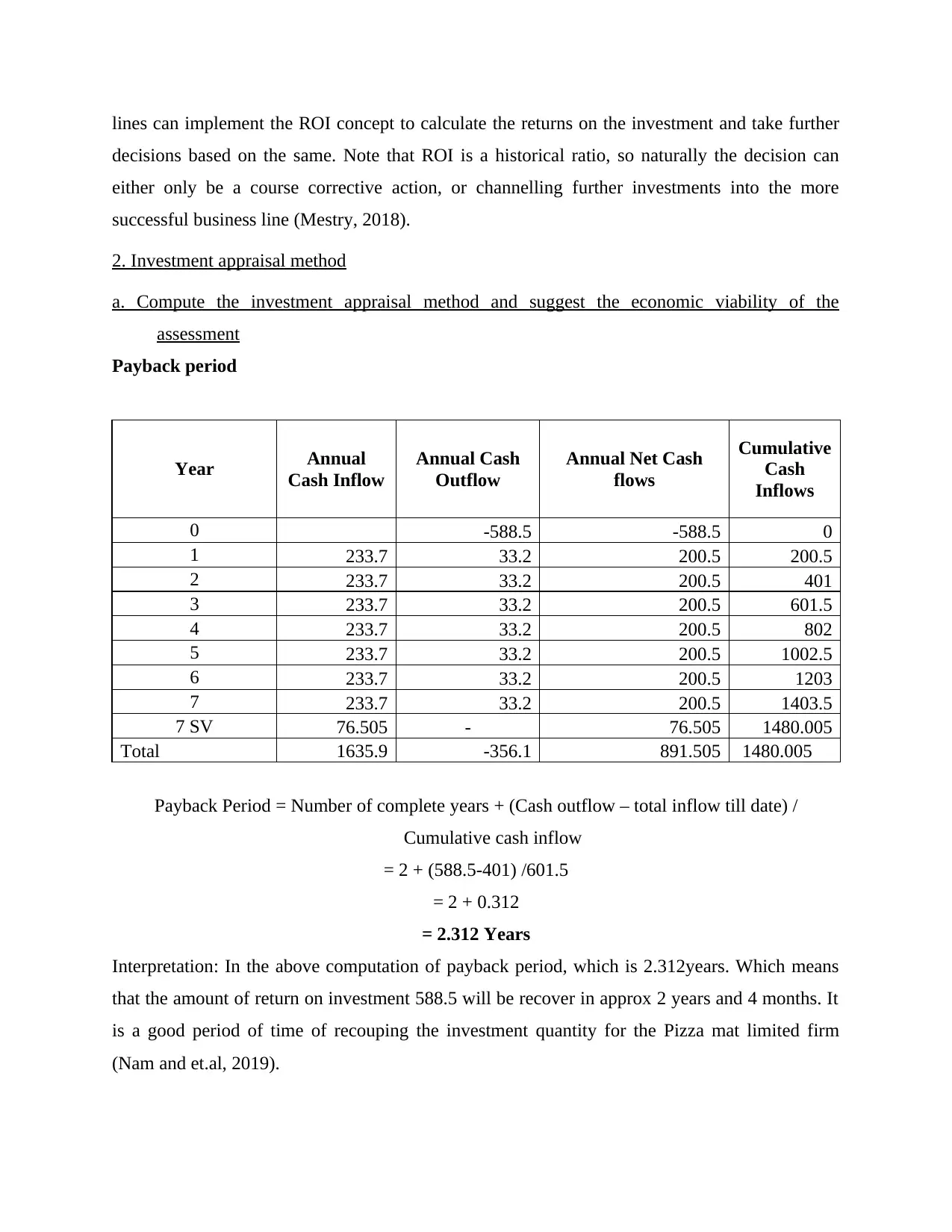

Payback period

Year Annual

Cash Inflow

Annual Cash

Outflow

Annual Net Cash

flows

Cumulative

Cash

Inflows

0 -588.5 -588.5 0

1 233.7 33.2 200.5 200.5

2 233.7 33.2 200.5 401

3 233.7 33.2 200.5 601.5

4 233.7 33.2 200.5 802

5 233.7 33.2 200.5 1002.5

6 233.7 33.2 200.5 1203

7 233.7 33.2 200.5 1403.5

7 SV 76.505 - 76.505 1480.005

Total 1635.9 -356.1 891.505 1480.005

Payback Period = Number of complete years + (Cash outflow – total inflow till date) /

Cumulative cash inflow

= 2 + (588.5-401) /601.5

= 2 + 0.312

= 2.312 Years

Interpretation: In the above computation of payback period, which is 2.312years. Which means

that the amount of return on investment 588.5 will be recover in approx 2 years and 4 months. It

is a good period of time of recouping the investment quantity for the Pizza mat limited firm

(Nam and et.al, 2019).

decisions based on the same. Note that ROI is a historical ratio, so naturally the decision can

either only be a course corrective action, or channelling further investments into the more

successful business line (Mestry, 2018).

2. Investment appraisal method

a. Compute the investment appraisal method and suggest the economic viability of the

assessment

Payback period

Year Annual

Cash Inflow

Annual Cash

Outflow

Annual Net Cash

flows

Cumulative

Cash

Inflows

0 -588.5 -588.5 0

1 233.7 33.2 200.5 200.5

2 233.7 33.2 200.5 401

3 233.7 33.2 200.5 601.5

4 233.7 33.2 200.5 802

5 233.7 33.2 200.5 1002.5

6 233.7 33.2 200.5 1203

7 233.7 33.2 200.5 1403.5

7 SV 76.505 - 76.505 1480.005

Total 1635.9 -356.1 891.505 1480.005

Payback Period = Number of complete years + (Cash outflow – total inflow till date) /

Cumulative cash inflow

= 2 + (588.5-401) /601.5

= 2 + 0.312

= 2.312 Years

Interpretation: In the above computation of payback period, which is 2.312years. Which means

that the amount of return on investment 588.5 will be recover in approx 2 years and 4 months. It

is a good period of time of recouping the investment quantity for the Pizza mat limited firm

(Nam and et.al, 2019).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

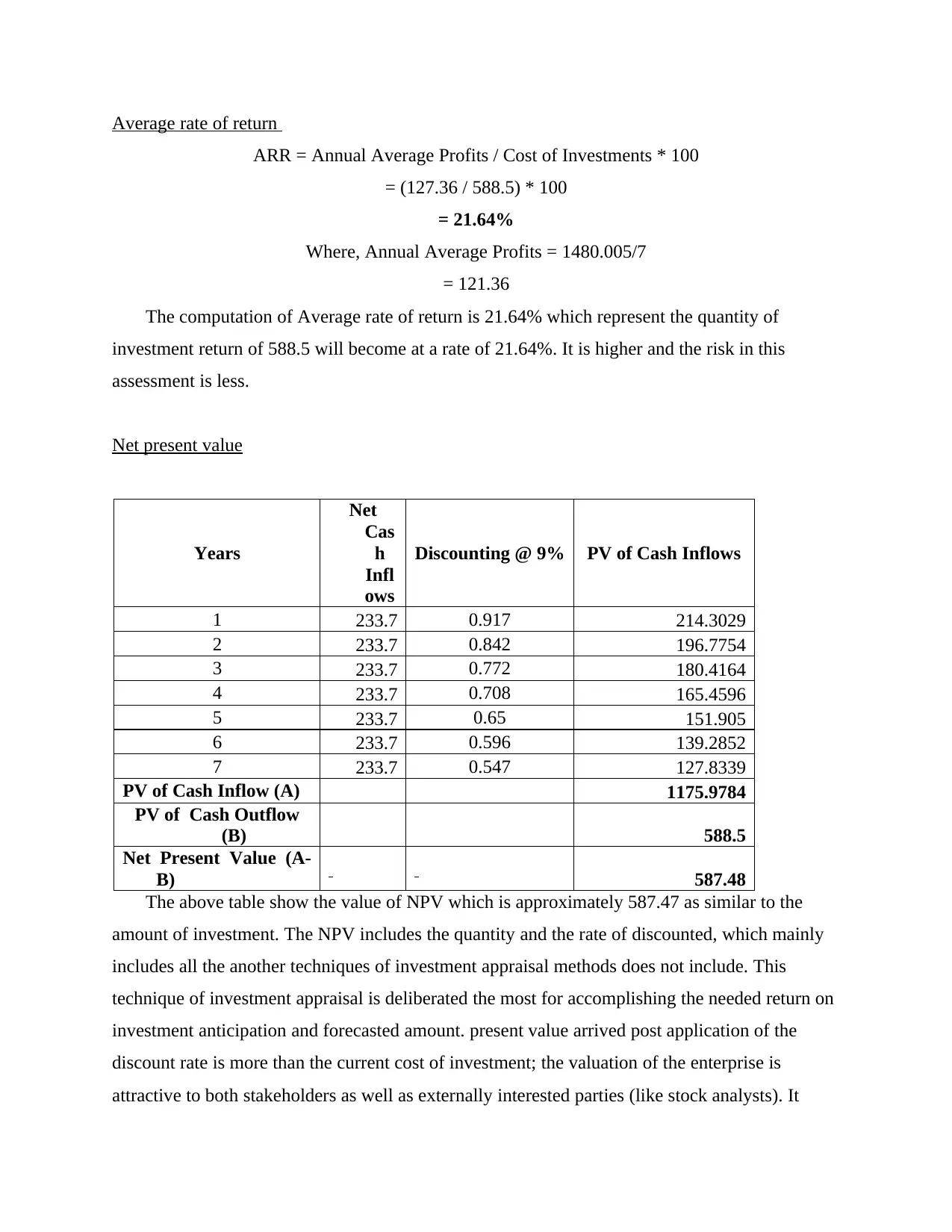

Average rate of return

ARR = Annual Average Profits / Cost of Investments * 100

= (127.36 / 588.5) * 100

= 21.64%

Where, Annual Average Profits = 1480.005/7

= 121.36

The computation of Average rate of return is 21.64% which represent the quantity of

investment return of 588.5 will become at a rate of 21.64%. It is higher and the risk in this

assessment is less.

Net present value

Years

Net

Cas

h

Infl

ows

Discounting @ 9% PV of Cash Inflows

1 233.7 0.917 214.3029

2 233.7 0.842 196.7754

3 233.7 0.772 180.4164

4 233.7 0.708 165.4596

5 233.7 0.65 151.905

6 233.7 0.596 139.2852

7 233.7 0.547 127.8339

PV of Cash Inflow (A) 1175.9784

PV of Cash Outflow

(B) 588.5

Net Present Value (A-

B) 587.48

The above table show the value of NPV which is approximately 587.47 as similar to the

amount of investment. The NPV includes the quantity and the rate of discounted, which mainly

includes all the another techniques of investment appraisal methods does not include. This

technique of investment appraisal is deliberated the most for accomplishing the needed return on

investment anticipation and forecasted amount. present value arrived post application of the

discount rate is more than the current cost of investment; the valuation of the enterprise is

attractive to both stakeholders as well as externally interested parties (like stock analysts). It

ARR = Annual Average Profits / Cost of Investments * 100

= (127.36 / 588.5) * 100

= 21.64%

Where, Annual Average Profits = 1480.005/7

= 121.36

The computation of Average rate of return is 21.64% which represent the quantity of

investment return of 588.5 will become at a rate of 21.64%. It is higher and the risk in this

assessment is less.

Net present value

Years

Net

Cas

h

Infl

ows

Discounting @ 9% PV of Cash Inflows

1 233.7 0.917 214.3029

2 233.7 0.842 196.7754

3 233.7 0.772 180.4164

4 233.7 0.708 165.4596

5 233.7 0.65 151.905

6 233.7 0.596 139.2852

7 233.7 0.547 127.8339

PV of Cash Inflow (A) 1175.9784

PV of Cash Outflow

(B) 588.5

Net Present Value (A-

B) 587.48

The above table show the value of NPV which is approximately 587.47 as similar to the

amount of investment. The NPV includes the quantity and the rate of discounted, which mainly

includes all the another techniques of investment appraisal methods does not include. This

technique of investment appraisal is deliberated the most for accomplishing the needed return on

investment anticipation and forecasted amount. present value arrived post application of the

discount rate is more than the current cost of investment; the valuation of the enterprise is

attractive to both stakeholders as well as externally interested parties (like stock analysts). It

attempts to overcome the problem of over- reliance on historical data as seen in both the previous

methods.

Internal Rate of Return:

Years

Cash

inflows

Discounting

Factor 9%

PV value of cash

inflow

1 233.7 0.917 214.3029

2 233.7 0.842 196.7754

3 233.7 0.772 180.4164

4 233.7 0.708 165.4596

5 233.7 0.65 151.905

6 233.7 0.596 139.2852

7 233.7 0.547 127.8339

Total Cash inflow 1175.9784

Total Cash outflow 588.5

NPV (A-B) 587.4784

Years

Cash

inflows

Discounting

Factor 20%

PV value of cash

inflow

1 233.7 0.833 194.6721

2 233.7 0.694 162.1878

3 233.7 0.579 135.3123

4 233.7 0.482 112.6434

5 233.7 0.402 93.9474

6 233.7 0.335 78.2895

7 233.7 0.279 65.2023

Total Cash inflow 842.2548

Total Cash outflow 588.5

NPV (A-B) 253.7548

IRR = Lower rate + Lower Rate NPV/ (Lower Rate NPV – Higher Rate NPV) * Diff. in Rates

= 9% + (587.48 / 587.48 - 253.75) * (20 – 9)

= 9% + (587.48 / 333.73) * 11

= 9% + (1.76) * 11

= 9% + 19.36

= 28.36%

Interpretation: The above calculation of internal rate of return is mainly used for anticipating

the profitable condition of the projected investment. If the Internal rate of return is computed for

methods.

Internal Rate of Return:

Years

Cash

inflows

Discounting

Factor 9%

PV value of cash

inflow

1 233.7 0.917 214.3029

2 233.7 0.842 196.7754

3 233.7 0.772 180.4164

4 233.7 0.708 165.4596

5 233.7 0.65 151.905

6 233.7 0.596 139.2852

7 233.7 0.547 127.8339

Total Cash inflow 1175.9784

Total Cash outflow 588.5

NPV (A-B) 587.4784

Years

Cash

inflows

Discounting

Factor 20%

PV value of cash

inflow

1 233.7 0.833 194.6721

2 233.7 0.694 162.1878

3 233.7 0.579 135.3123

4 233.7 0.482 112.6434

5 233.7 0.402 93.9474

6 233.7 0.335 78.2895

7 233.7 0.279 65.2023

Total Cash inflow 842.2548

Total Cash outflow 588.5

NPV (A-B) 253.7548

IRR = Lower rate + Lower Rate NPV/ (Lower Rate NPV – Higher Rate NPV) * Diff. in Rates

= 9% + (587.48 / 587.48 - 253.75) * (20 – 9)

= 9% + (587.48 / 333.73) * 11

= 9% + (1.76) * 11

= 9% + 19.36

= 28.36%

Interpretation: The above calculation of internal rate of return is mainly used for anticipating

the profitable condition of the projected investment. If the Internal rate of return is computed for

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.