Importance of Financial Management: Concept, Statements, Ratios, and Case Study Analysis

VerifiedAdded on 2023/06/14

|13

|2919

|270

AI Summary

This report covers the concept and importance of financial management, main financial statements, and the use of ratios in financial management. It also includes a case study analysis of a company's profitability, liquidity, and efficiency ratios. The report suggests improvements for the company's financial performance.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Importance of

Financial

Management

Financial

Management

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Contents

INTRODUCTION...........................................................................................................................3

SECTION 1.....................................................................................................................................3

Concept and importance of financial management.....................................................................3

SECTION 2.....................................................................................................................................4

Description of main financial statements and explanation of the use of ratios in financial

management.................................................................................................................................4

SECTION 3.....................................................................................................................................5

Completing the Information on the ‘Business Review Template................................................5

SECTION 4.....................................................................................................................................9

Using examples from the case study describing and discussing the processes this business

might use to improve their financial performance.......................................................................9

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION...........................................................................................................................3

SECTION 1.....................................................................................................................................3

Concept and importance of financial management.....................................................................3

SECTION 2.....................................................................................................................................4

Description of main financial statements and explanation of the use of ratios in financial

management.................................................................................................................................4

SECTION 3.....................................................................................................................................5

Completing the Information on the ‘Business Review Template................................................5

SECTION 4.....................................................................................................................................9

Using examples from the case study describing and discussing the processes this business

might use to improve their financial performance.......................................................................9

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION

Financial management is regarded as one of the most critical areas of corporate operations. It

engages in a variety of fund-related operations, such as raising funds, distributing funds within

the organisation, and so on. These functions aid in the smooth operation of corporate

organisations (Pomering, and Kammerer, 2019). This report covers the idea of financial

management, as well as its relevance, a description of the key financial statements, and the use of

ratios in financial management. Furthermore, it includes a brief discussion of various ratios, such

as profitability, liquidity, and efficiency ratio, using an example from the income statement and

balance sheet of the case study. This report also includes a business performance evaluation for

the aim of analysing the financial performance of the company. It includes the tactics that are

necessary to increase a company's success.

SECTION 1

Concept and importance of financial management

Financial management is described as the process of planning, organising, directing, and

controlling financial activities of a company. Essentially, it refers to the application of general

management ideas to a company's financial resources. It is critical to an organization's success

since it assists management in making vital decisions such as investment, financial, and dividend

decisions.

Importance of financial management:

Financial planning: The function of financial management in the financial planning process is

critical. It is responsible for determining the financial requirements of the corporate entity. It is

vital for a company organisation to arrange its finances in accordance with its requirements

(Brooks, and Schopohl, 2020). It has been shown that a company's financial planning has a

significant impact on its performance.

Safeguarding/Protecting Funds: One of the most important aspects of financial management is

the ability to save money in order to meet the organization's goals and objectives. It ensures the

seamless execution of all corporate processes. Overspending on a single project has resulted in a

lack of financial resources.

Allocation of funds: Another important aspect of financial management is the proper allocation

of cash. When the allotted funds are correctly devoted to the assets, the operational competency

Financial management is regarded as one of the most critical areas of corporate operations. It

engages in a variety of fund-related operations, such as raising funds, distributing funds within

the organisation, and so on. These functions aid in the smooth operation of corporate

organisations (Pomering, and Kammerer, 2019). This report covers the idea of financial

management, as well as its relevance, a description of the key financial statements, and the use of

ratios in financial management. Furthermore, it includes a brief discussion of various ratios, such

as profitability, liquidity, and efficiency ratio, using an example from the income statement and

balance sheet of the case study. This report also includes a business performance evaluation for

the aim of analysing the financial performance of the company. It includes the tactics that are

necessary to increase a company's success.

SECTION 1

Concept and importance of financial management

Financial management is described as the process of planning, organising, directing, and

controlling financial activities of a company. Essentially, it refers to the application of general

management ideas to a company's financial resources. It is critical to an organization's success

since it assists management in making vital decisions such as investment, financial, and dividend

decisions.

Importance of financial management:

Financial planning: The function of financial management in the financial planning process is

critical. It is responsible for determining the financial requirements of the corporate entity. It is

vital for a company organisation to arrange its finances in accordance with its requirements

(Brooks, and Schopohl, 2020). It has been shown that a company's financial planning has a

significant impact on its performance.

Safeguarding/Protecting Funds: One of the most important aspects of financial management is

the ability to save money in order to meet the organization's goals and objectives. It ensures the

seamless execution of all corporate processes. Overspending on a single project has resulted in a

lack of financial resources.

Allocation of funds: Another important aspect of financial management is the proper allocation

of cash. When the allotted funds are correctly devoted to the assets, the operational competency

of a corporate organisation is improved. Furthermore, allocating money results in a decrease in

business expenditures as well as an increase in capital estimation.

Investment opportunity: If a corporate organisation does a good job managing its money and

savings, it may create prospects for investment. Investment opportunities play a critical part in

generating money, which will aid the organisation in overcoming a period of deficit.

SECTION 2

Description of main financial statements and explanation of the use of ratios in financial

management

Financial statements are all of the books that are kept for the purpose of recording all of the

business transactions. The financial statement is the site where all monetary transactions are

recorded, as well as the financial statistics and fiscal health of the organisation (Radwan, Drissi,

and Secinaro, 2021). It is the financial manager's obligation to keep track of all transactions and

guarantee that they are properly audited. It verifies the accuracy of the assertions made by the

corporate organisation. The following are the most important financial statements:

Profit and loss statement: This is the book that contains the income, expenses, and revenue for

the financial period, as well as any accrued or outstanding income or costs. It includes all

transactions that take place during a given time frame, as well as the expenditures incurred by the

company in making sales. The net profit of a financial year may be estimated by removing the

business's costs and wages.

Statement of financial performance: It is regarded as the most essential financial affirmation

within a business organisation since it provides clients with a wide perspective of the company's

financial information. This statement shows the assets and liabilities that the company has agreed

to pay in the future. The major goal of this statement is to keep track of monetary transactions.

Cash flow statement: The cash flow statement is a financial statement that shows the net amount

of cash intake and outflow from a firm over a certain period of time. It essentially depicts the

changes in a business's cash, which include operating, investing, and financing operations

(Habib, and Hasan, 2019). The operational operations have represented changes in current

resources and current liabilities. The input and outflow of funds through shareholder capital

issues, dividend payments, debentures, and other financing exercises are only a few examples.

Ratios and their applications in financial management:

business expenditures as well as an increase in capital estimation.

Investment opportunity: If a corporate organisation does a good job managing its money and

savings, it may create prospects for investment. Investment opportunities play a critical part in

generating money, which will aid the organisation in overcoming a period of deficit.

SECTION 2

Description of main financial statements and explanation of the use of ratios in financial

management

Financial statements are all of the books that are kept for the purpose of recording all of the

business transactions. The financial statement is the site where all monetary transactions are

recorded, as well as the financial statistics and fiscal health of the organisation (Radwan, Drissi,

and Secinaro, 2021). It is the financial manager's obligation to keep track of all transactions and

guarantee that they are properly audited. It verifies the accuracy of the assertions made by the

corporate organisation. The following are the most important financial statements:

Profit and loss statement: This is the book that contains the income, expenses, and revenue for

the financial period, as well as any accrued or outstanding income or costs. It includes all

transactions that take place during a given time frame, as well as the expenditures incurred by the

company in making sales. The net profit of a financial year may be estimated by removing the

business's costs and wages.

Statement of financial performance: It is regarded as the most essential financial affirmation

within a business organisation since it provides clients with a wide perspective of the company's

financial information. This statement shows the assets and liabilities that the company has agreed

to pay in the future. The major goal of this statement is to keep track of monetary transactions.

Cash flow statement: The cash flow statement is a financial statement that shows the net amount

of cash intake and outflow from a firm over a certain period of time. It essentially depicts the

changes in a business's cash, which include operating, investing, and financing operations

(Habib, and Hasan, 2019). The operational operations have represented changes in current

resources and current liabilities. The input and outflow of funds through shareholder capital

issues, dividend payments, debentures, and other financing exercises are only a few examples.

Ratios and their applications in financial management:

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Comparisons: The most common application of ratio analysis is to analyse the financial

performance of firms in the same industry in order to determine a company's market position. It

is critical in identifying market gaps, as well as competitive advantages, strengths, and

weaknesses. The management of a business organisation uses this information to make decisions

that improve the company's market position.

Trend line: Ratios are used by a number of businesses to analyse the trend in their financial

performance. These businesses acquire important information from financial statements over a

long period of time (Kučera, 2019). The pattern that has been studied can be utilised by

businesses to forecast future financial performance directions.

Operational efficiency: It has also been discovered that financial ratio analysis is used by

businesses to determine the degree of efficiency in the management of obligations and assets.

Financial ratios are used to examine the over- and under-utilization of financial resources.

SECTION 3

Completing the Information on the ‘Business Review Template

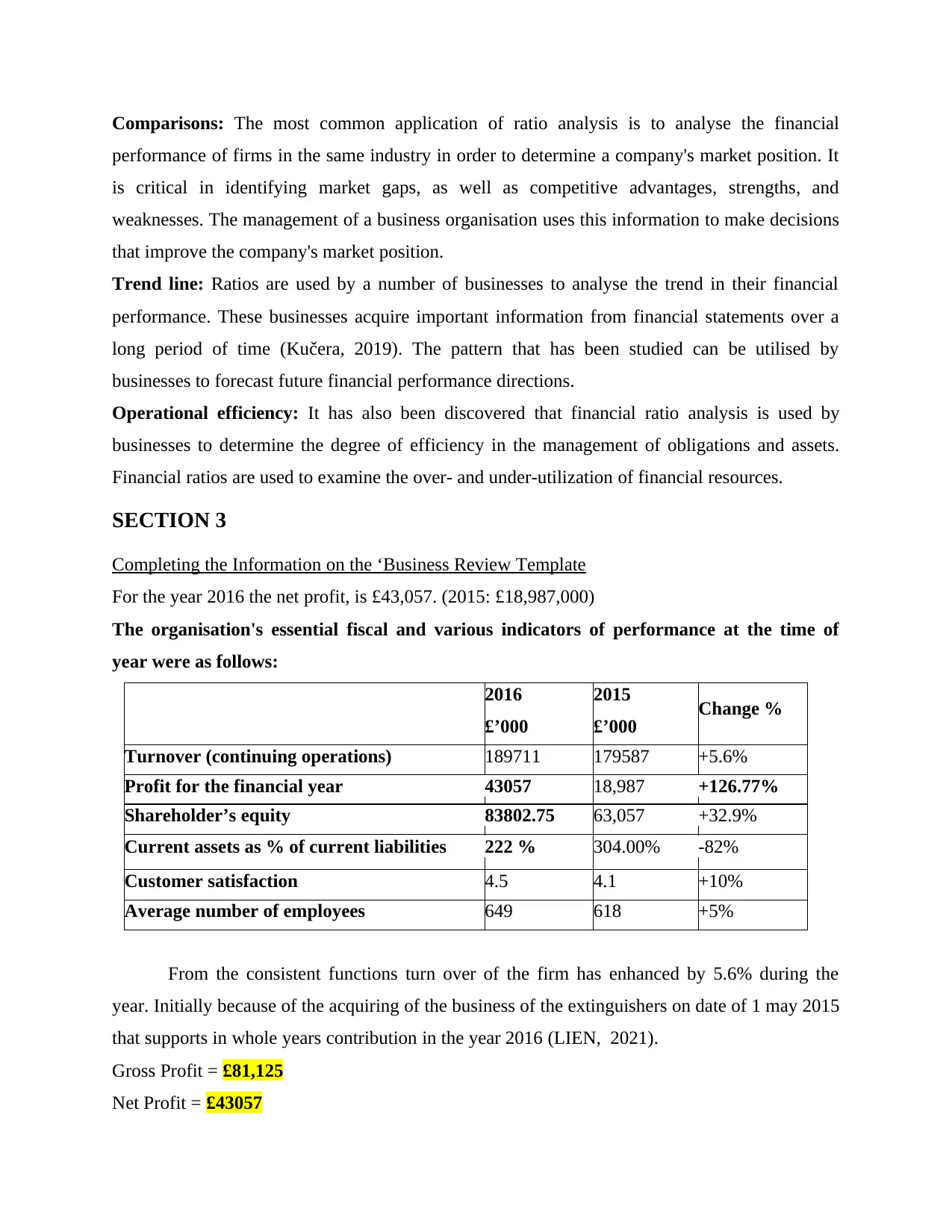

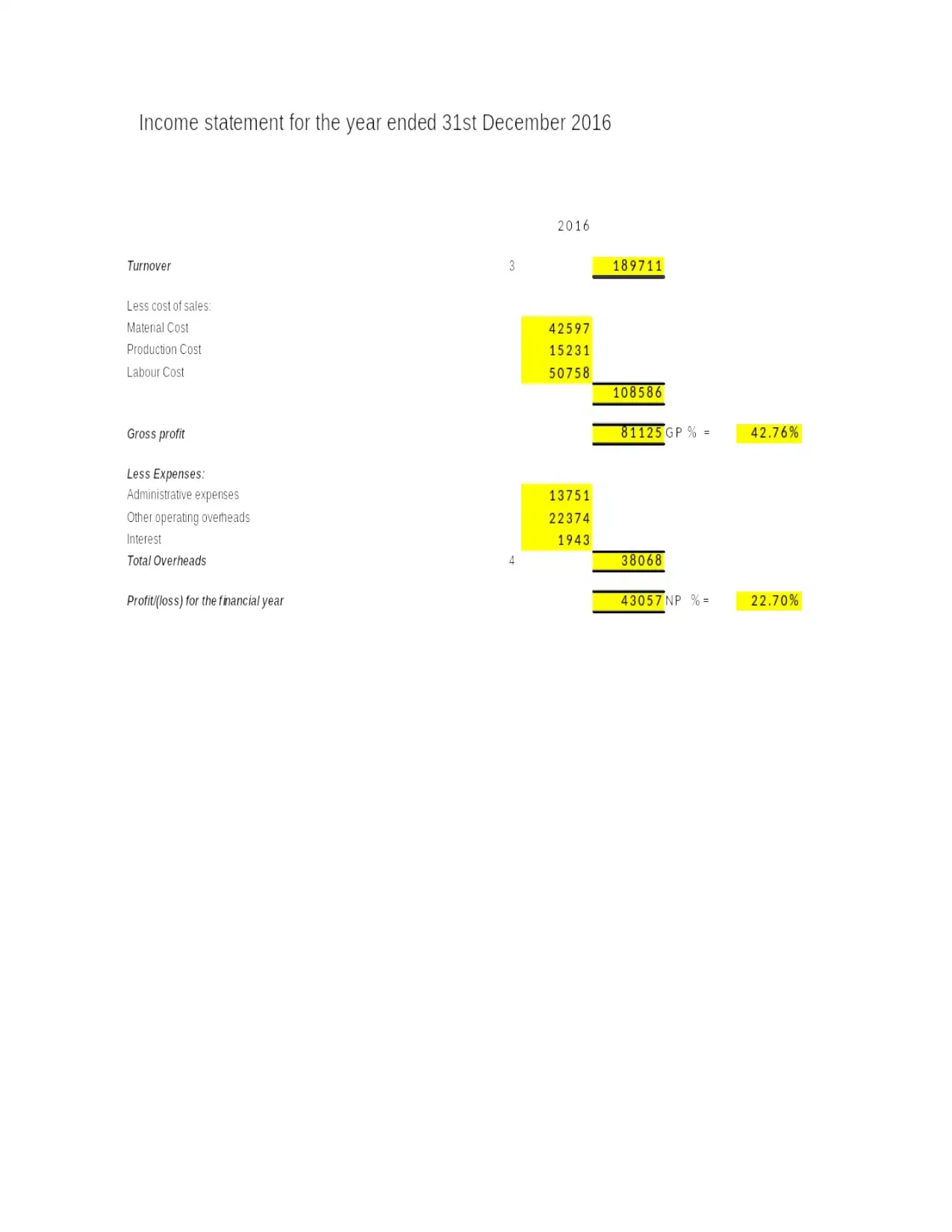

For the year 2016 the net profit, is £43,057. (2015: £18,987,000)

The organisation's essential fiscal and various indicators of performance at the time of

year were as follows:

2016

£’000

2015

£’000 Change %

Turnover (continuing operations) 189711 179587 +5.6%

Profit for the financial year 43057 18,987 +126.77%

Shareholder’s equity 83802.75 63,057 +32.9%

Current assets as % of current liabilities 222 % 304.00% -82%

Customer satisfaction 4.5 4.1 +10%

Average number of employees 649 618 +5%

From the consistent functions turn over of the firm has enhanced by 5.6% during the

year. Initially because of the acquiring of the business of the extinguishers on date of 1 may 2015

that supports in whole years contribution in the year 2016 (LIEN, 2021).

Gross Profit = £81,125

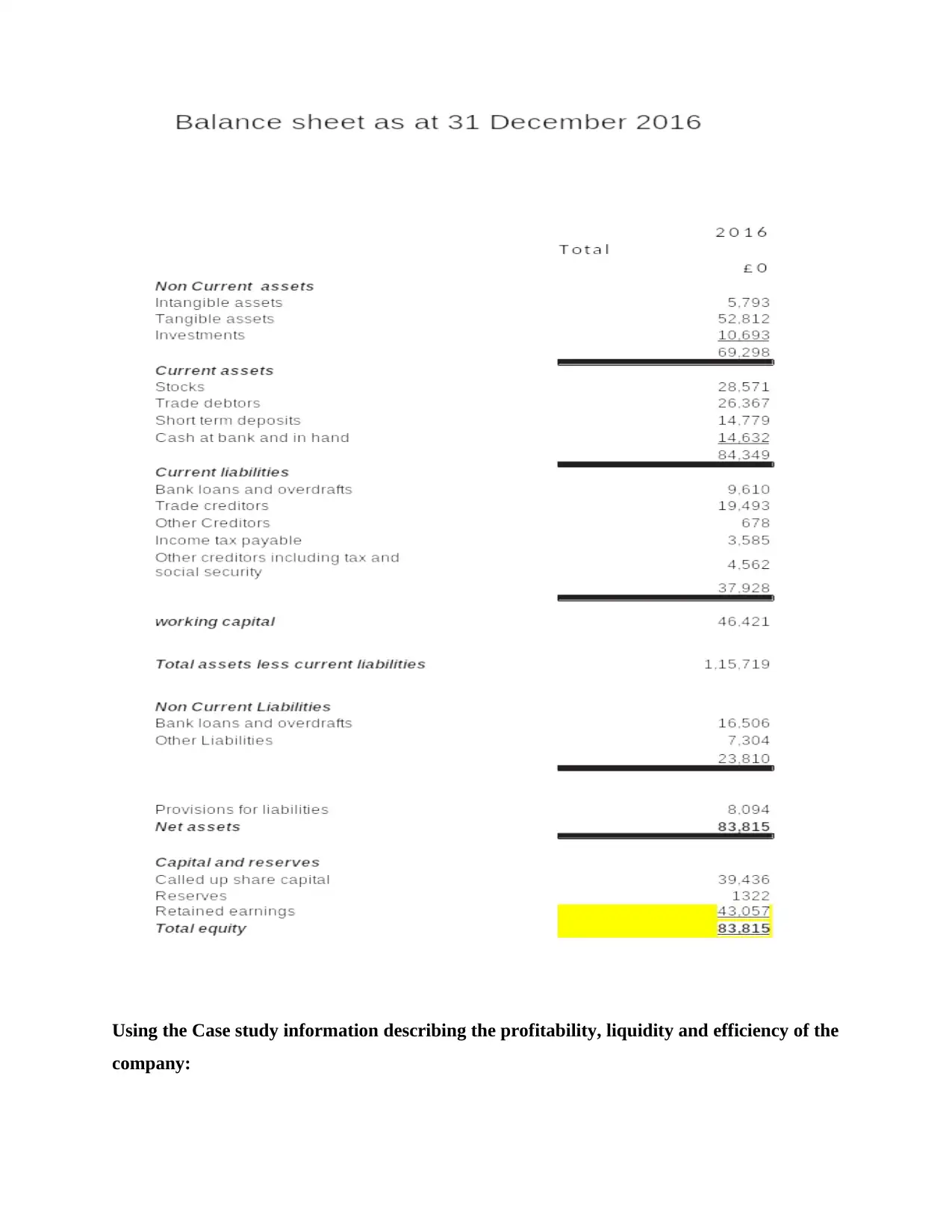

Net Profit = £43057

performance of firms in the same industry in order to determine a company's market position. It

is critical in identifying market gaps, as well as competitive advantages, strengths, and

weaknesses. The management of a business organisation uses this information to make decisions

that improve the company's market position.

Trend line: Ratios are used by a number of businesses to analyse the trend in their financial

performance. These businesses acquire important information from financial statements over a

long period of time (Kučera, 2019). The pattern that has been studied can be utilised by

businesses to forecast future financial performance directions.

Operational efficiency: It has also been discovered that financial ratio analysis is used by

businesses to determine the degree of efficiency in the management of obligations and assets.

Financial ratios are used to examine the over- and under-utilization of financial resources.

SECTION 3

Completing the Information on the ‘Business Review Template

For the year 2016 the net profit, is £43,057. (2015: £18,987,000)

The organisation's essential fiscal and various indicators of performance at the time of

year were as follows:

2016

£’000

2015

£’000 Change %

Turnover (continuing operations) 189711 179587 +5.6%

Profit for the financial year 43057 18,987 +126.77%

Shareholder’s equity 83802.75 63,057 +32.9%

Current assets as % of current liabilities 222 % 304.00% -82%

Customer satisfaction 4.5 4.1 +10%

Average number of employees 649 618 +5%

From the consistent functions turn over of the firm has enhanced by 5.6% during the

year. Initially because of the acquiring of the business of the extinguishers on date of 1 may 2015

that supports in whole years contribution in the year 2016 (LIEN, 2021).

Gross Profit = £81,125

Net Profit = £43057

Net Profit has been enhanced in the year 2016 by 126.77%.

Equity of shareholders has been enhanced by 32.9% by £20,745.75.

Quick ratio of the organisation (Current Assets without inventory divided by the current

liabilities) is 1,47:1

Current ratio of the company is 2.22: 1 (Current assets divided by current liabilities)

(The calculation are shown in appendix)

Using Excel producing an Income Statement for the Sample Organisation

This is included within appendix

Using Excel completing the Balance Sheet

Using the Case study information describing the profitability, liquidity and efficiency of the

company:

Using the Case study information describing the profitability, liquidity and efficiency of the

company:

Using the Case study information describing the profitability, liquidity and efficiency of the

company:

Equity of shareholders has been enhanced by 32.9% by £20,745.75.

Quick ratio of the organisation (Current Assets without inventory divided by the current

liabilities) is 1,47:1

Current ratio of the company is 2.22: 1 (Current assets divided by current liabilities)

(The calculation are shown in appendix)

Using Excel producing an Income Statement for the Sample Organisation

This is included within appendix

Using Excel completing the Balance Sheet

Using the Case study information describing the profitability, liquidity and efficiency of the

company:

Using the Case study information describing the profitability, liquidity and efficiency of the

company:

Using the Case study information describing the profitability, liquidity and efficiency of the

company:

Using the Case study information describing the profitability, liquidity and efficiency of the

company:

company:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Profitability Ratio - It is a type of financial boundary that is used to assess a company's

potential to earn money over time in relation to several components of the balance sheet and

income statements of the financial year, as well as the firm's productivity (Atrill, and Lindley,

2019.). The following are a few of the most important profitability ratios:

Gross Profit Margin= (Revenue – cost of Sales) / Revenue * 100

= (189,711 – 108,586) / 189,711 * 100 = 42.76%

Net Profit Margin = (Net profit/ Revenue) *100

= (43,057/189,711) * 100 = 22.70%

Interpretation: By combining non-operating and operating expenditures, the above-mentioned

ratios show the profit percentage in relation to the total revenue. The gross profit margin is

the dimension of the remaining capital firm's income, whereas the net profit margin is the

percentage of retained income after revenue from cost. The net income and gross profit

margins are 22.7 and 42.76 percent, respectively, indicating a 20 percent fall in profit

margins. The company has to lower its overhead expenditures, which is preventing them

from increasing their net earnings. This is necessary for potential investors to compare the

firm's earnings to those of other participants in the same industry in order to assess the firm's

actual position in the sector.

Efficiency Ratio – It assesses how effectively an organization's liabilities and assets are utilised.

This assesses how successfully the company collects money from customers and how long it will

take to repay the debt, as well as the turnover equity and assets (Jakobsen, Mitchell, Nørreklit,

and Trenca, 2019). Stock turnover, asset turnover, account payable turnover ratio, and receivable

turnover ratio are all important ratios.

Asset turnover Ratio= Total Sales/ Total assets = 189,711/153,647 = 1.23

Stock Turnover Ratio = Cost of Sales/ Stock = (108,586/28,571) = 3.8

Accounts receivable Days = 365/ Debtors Turnover Ratio

=365/ 7.19 = 50.77 days

Accounts Payable Days = 365/ Creditors Turnover Ratio

= 365/7.04 = 51.84 days

Interpretation: On average, it takes 51 days for a customer to return their loan. Furthermore,

creditors must wait 52 days to get their money. As a result, the company receives and pays

potential to earn money over time in relation to several components of the balance sheet and

income statements of the financial year, as well as the firm's productivity (Atrill, and Lindley,

2019.). The following are a few of the most important profitability ratios:

Gross Profit Margin= (Revenue – cost of Sales) / Revenue * 100

= (189,711 – 108,586) / 189,711 * 100 = 42.76%

Net Profit Margin = (Net profit/ Revenue) *100

= (43,057/189,711) * 100 = 22.70%

Interpretation: By combining non-operating and operating expenditures, the above-mentioned

ratios show the profit percentage in relation to the total revenue. The gross profit margin is

the dimension of the remaining capital firm's income, whereas the net profit margin is the

percentage of retained income after revenue from cost. The net income and gross profit

margins are 22.7 and 42.76 percent, respectively, indicating a 20 percent fall in profit

margins. The company has to lower its overhead expenditures, which is preventing them

from increasing their net earnings. This is necessary for potential investors to compare the

firm's earnings to those of other participants in the same industry in order to assess the firm's

actual position in the sector.

Efficiency Ratio – It assesses how effectively an organization's liabilities and assets are utilised.

This assesses how successfully the company collects money from customers and how long it will

take to repay the debt, as well as the turnover equity and assets (Jakobsen, Mitchell, Nørreklit,

and Trenca, 2019). Stock turnover, asset turnover, account payable turnover ratio, and receivable

turnover ratio are all important ratios.

Asset turnover Ratio= Total Sales/ Total assets = 189,711/153,647 = 1.23

Stock Turnover Ratio = Cost of Sales/ Stock = (108,586/28,571) = 3.8

Accounts receivable Days = 365/ Debtors Turnover Ratio

=365/ 7.19 = 50.77 days

Accounts Payable Days = 365/ Creditors Turnover Ratio

= 365/7.04 = 51.84 days

Interpretation: On average, it takes 51 days for a customer to return their loan. Furthermore,

creditors must wait 52 days to get their money. As a result, the company receives and pays

payments as well as obligations at the same time. It is also a disadvantage since, because there

are various differences in the time of days, it may be a concern for the company on the day of

receivable decrease. Inventory turnover is roughly 3.8, which refers to the whole investment of

the stock that flows four times a year, or three times a year. The turnover ratio of total assets is

1.23, indicating that the firm is operating efficiently and profitably.

Liquidity Ratio: This has an impact on the firm's ability to meet its debt obligations and on

public perceptions of the firm's solvency (Ahmadi, and Bouri, 2018). These ratios are based on

current liabilities, current assets, and inventories, among other things. The most important ratios

are fast and current ratios.

Current Ratio = Current Assets/ Current Liabilities

= 84,349/ 37,928 = 2.22:1

Quick Ratio = (Current Assets- Stock)/ Current Liabilities

= (84,349 - 28571)/ 37,928 = 1.47:1

Interpretation: The relevant ratio indicates the company's liquidation position. The abstract ratio

is 2:1, and the quick ratio is 1:1, indicating that the current assets to liabilities ratio is 2.22,

indicating that the company is solvent.

SECTION 4

Using examples from the case study describing and discussing the processes this business might

use to improve their financial performance.

Financial performance is a company's lifelong feature, since investors focus on investing in the

firm owing to the firm's view of its activities (Madanizadeh, Karimirad, and Rahmati, 2019). As

a result, it is critical to make the necessary budgetary considerations while substantiating the

financing decision. The following conclusions may be drawn from the above calculations:

• The current assets to current liabilities ratio has reduced by 82 percent in comparison to the

previous year. It claims that cash leakage is increasing and the company is losing liquidity.

• The net income increased by 126.77 percent due to lower non-operating expenses such as

management costs and lower interest rates.

• Consumer satisfaction indicates that the operation is spending more and assisting the business's

growth since the worker retention ratio has also improved.

are various differences in the time of days, it may be a concern for the company on the day of

receivable decrease. Inventory turnover is roughly 3.8, which refers to the whole investment of

the stock that flows four times a year, or three times a year. The turnover ratio of total assets is

1.23, indicating that the firm is operating efficiently and profitably.

Liquidity Ratio: This has an impact on the firm's ability to meet its debt obligations and on

public perceptions of the firm's solvency (Ahmadi, and Bouri, 2018). These ratios are based on

current liabilities, current assets, and inventories, among other things. The most important ratios

are fast and current ratios.

Current Ratio = Current Assets/ Current Liabilities

= 84,349/ 37,928 = 2.22:1

Quick Ratio = (Current Assets- Stock)/ Current Liabilities

= (84,349 - 28571)/ 37,928 = 1.47:1

Interpretation: The relevant ratio indicates the company's liquidation position. The abstract ratio

is 2:1, and the quick ratio is 1:1, indicating that the current assets to liabilities ratio is 2.22,

indicating that the company is solvent.

SECTION 4

Using examples from the case study describing and discussing the processes this business might

use to improve their financial performance.

Financial performance is a company's lifelong feature, since investors focus on investing in the

firm owing to the firm's view of its activities (Madanizadeh, Karimirad, and Rahmati, 2019). As

a result, it is critical to make the necessary budgetary considerations while substantiating the

financing decision. The following conclusions may be drawn from the above calculations:

• The current assets to current liabilities ratio has reduced by 82 percent in comparison to the

previous year. It claims that cash leakage is increasing and the company is losing liquidity.

• The net income increased by 126.77 percent due to lower non-operating expenses such as

management costs and lower interest rates.

• Consumer satisfaction indicates that the operation is spending more and assisting the business's

growth since the worker retention ratio has also improved.

• Measuring shareholder equity is increasing, resulting in a maximum in stock sales, a decrease

in operating costs, and an increase in revenue.

The following are some improvements that can be made:

• Effective and effective use of resources, resulting in lower costs and higher rates, as well as a

return on investment.

• It will help with working capital demands by reducing inventories and increasing stock

turnover.

CONCLUSION

The aforementioned analysis concludes that fiscal management plays a critical part in the

organization's operations. It allocates money, makes proper business decisions, and demonstrates

the firm' profitability, solvency, and economic stability. The financial accounts provide a quick

overview of the company. These are required for all employees in otfrr to manage and have them

audited by the appropriate individuals both externally and internally. It includes information on

obligations, assets, shareholder equity, earnings, and cash input and outflow. Financial ratios can

be used to assess a company's solvency and efficiency.

in operating costs, and an increase in revenue.

The following are some improvements that can be made:

• Effective and effective use of resources, resulting in lower costs and higher rates, as well as a

return on investment.

• It will help with working capital demands by reducing inventories and increasing stock

turnover.

CONCLUSION

The aforementioned analysis concludes that fiscal management plays a critical part in the

organization's operations. It allocates money, makes proper business decisions, and demonstrates

the firm' profitability, solvency, and economic stability. The financial accounts provide a quick

overview of the company. These are required for all employees in otfrr to manage and have them

audited by the appropriate individuals both externally and internally. It includes information on

obligations, assets, shareholder equity, earnings, and cash input and outflow. Financial ratios can

be used to assess a company's solvency and efficiency.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

REFERENCES

Books and Journals

Pomering, R. and Kammerer, L., 2019. Outsourced finance and accounting services can be a

growth area. The CPA Journal, 89(5), pp.15-16.

Brooks, C. and Schopohl, L., 2020. Green accounting and finance: Advancing research on

environmental disclosure, value impacts and management control systems. British

Accounting Review, Forthcoming.

Radwan, M., Drissi, S. and Secinaro, S., 2021. Machine learning in the fields of accounting,

economics and finance The emergence of new strategies. In The Essentials of Machine

Learning in Finance and Accounting (pp. 181-198). Routledge.

Habib, A. and Hasan, M.M., 2019. Corporate life cycle research in accounting, finance and

corporate governance: A survey, and directions for future research. International

Review of Financial Analysis, 61, pp.188-201.

Kučera, M., 2019, May. Analysis of student profile in terms of success in accounting study.

In Annual Conference on Finance and Accounting (pp. 343-350). Springer, Cham.

Atrill, P. and Lindley, L. eds., 2019. Issues in Accounting and Finance. Routledge.

Madanizadeh, S.A., Karimirad, A. and Rahmati, M.H., 2019. Business cycle accounting of trade

barriers in a small open economy. The Quarterly Review of Economics and Finance, 71,

pp.67-78.

Jakobsen, M., Mitchell, F., Nørreklit, H. and Trenca, M., 2019. Educating management

accountants as business partners: Pragmatic constructivism as an alternative

pedagogical paradigm for teaching management accounting at master’s

level. Qualitative Research in Accounting & Management.

Ahmadi, A. and Bouri, A., 2018. The accounting value relevance of earnings and book value:

Tunisian banks and financial institutions. International Journal of Law and

Management.

Books and Journals

Pomering, R. and Kammerer, L., 2019. Outsourced finance and accounting services can be a

growth area. The CPA Journal, 89(5), pp.15-16.

Brooks, C. and Schopohl, L., 2020. Green accounting and finance: Advancing research on

environmental disclosure, value impacts and management control systems. British

Accounting Review, Forthcoming.

Radwan, M., Drissi, S. and Secinaro, S., 2021. Machine learning in the fields of accounting,

economics and finance The emergence of new strategies. In The Essentials of Machine

Learning in Finance and Accounting (pp. 181-198). Routledge.

Habib, A. and Hasan, M.M., 2019. Corporate life cycle research in accounting, finance and

corporate governance: A survey, and directions for future research. International

Review of Financial Analysis, 61, pp.188-201.

Kučera, M., 2019, May. Analysis of student profile in terms of success in accounting study.

In Annual Conference on Finance and Accounting (pp. 343-350). Springer, Cham.

Atrill, P. and Lindley, L. eds., 2019. Issues in Accounting and Finance. Routledge.

Madanizadeh, S.A., Karimirad, A. and Rahmati, M.H., 2019. Business cycle accounting of trade

barriers in a small open economy. The Quarterly Review of Economics and Finance, 71,

pp.67-78.

Jakobsen, M., Mitchell, F., Nørreklit, H. and Trenca, M., 2019. Educating management

accountants as business partners: Pragmatic constructivism as an alternative

pedagogical paradigm for teaching management accounting at master’s

level. Qualitative Research in Accounting & Management.

Ahmadi, A. and Bouri, A., 2018. The accounting value relevance of earnings and book value:

Tunisian banks and financial institutions. International Journal of Law and

Management.

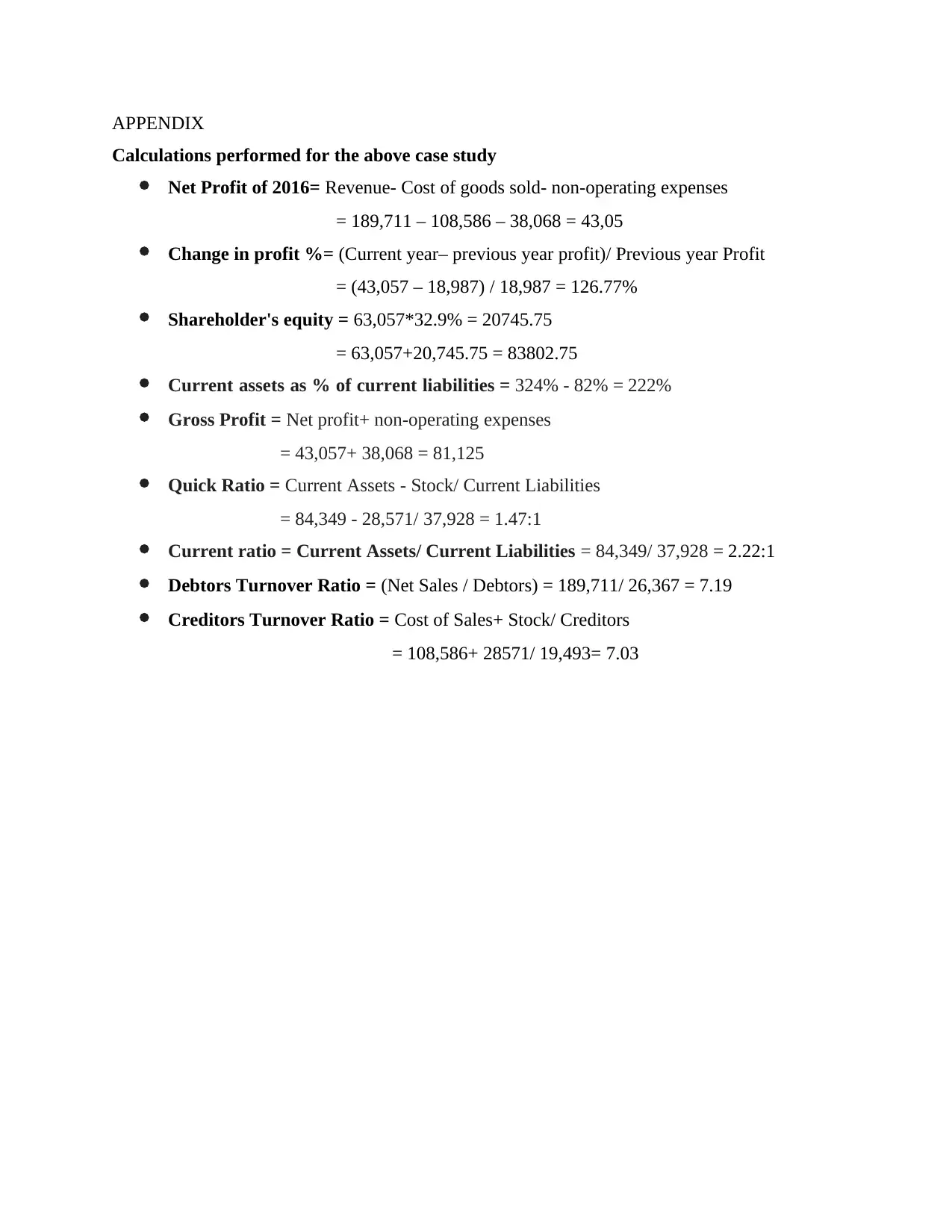

APPENDIX

Calculations performed for the above case study

Net Profit of 2016= Revenue- Cost of goods sold- non-operating expenses

= 189,711 – 108,586 – 38,068 = 43,05

Change in profit %= (Current year– previous year profit)/ Previous year Profit

= (43,057 – 18,987) / 18,987 = 126.77%

Shareholder's equity = 63,057*32.9% = 20745.75

= 63,057+20,745.75 = 83802.75

Current assets as % of current liabilities = 324% - 82% = 222%

Gross Profit = Net profit+ non-operating expenses

= 43,057+ 38,068 = 81,125

Quick Ratio = Current Assets - Stock/ Current Liabilities

= 84,349 - 28,571/ 37,928 = 1.47:1

Current ratio = Current Assets/ Current Liabilities = 84,349/ 37,928 = 2.22:1

Debtors Turnover Ratio = (Net Sales / Debtors) = 189,711/ 26,367 = 7.19

Creditors Turnover Ratio = Cost of Sales+ Stock/ Creditors

= 108,586+ 28571/ 19,493= 7.03

Calculations performed for the above case study

Net Profit of 2016= Revenue- Cost of goods sold- non-operating expenses

= 189,711 – 108,586 – 38,068 = 43,05

Change in profit %= (Current year– previous year profit)/ Previous year Profit

= (43,057 – 18,987) / 18,987 = 126.77%

Shareholder's equity = 63,057*32.9% = 20745.75

= 63,057+20,745.75 = 83802.75

Current assets as % of current liabilities = 324% - 82% = 222%

Gross Profit = Net profit+ non-operating expenses

= 43,057+ 38,068 = 81,125

Quick Ratio = Current Assets - Stock/ Current Liabilities

= 84,349 - 28,571/ 37,928 = 1.47:1

Current ratio = Current Assets/ Current Liabilities = 84,349/ 37,928 = 2.22:1

Debtors Turnover Ratio = (Net Sales / Debtors) = 189,711/ 26,367 = 7.19

Creditors Turnover Ratio = Cost of Sales+ Stock/ Creditors

= 108,586+ 28571/ 19,493= 7.03

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.