BMP5006 - Financial Management & Decision Making: Exam 2021/22

VerifiedAdded on 2023/06/07

|11

|1724

|65

Homework Assignment

AI Summary

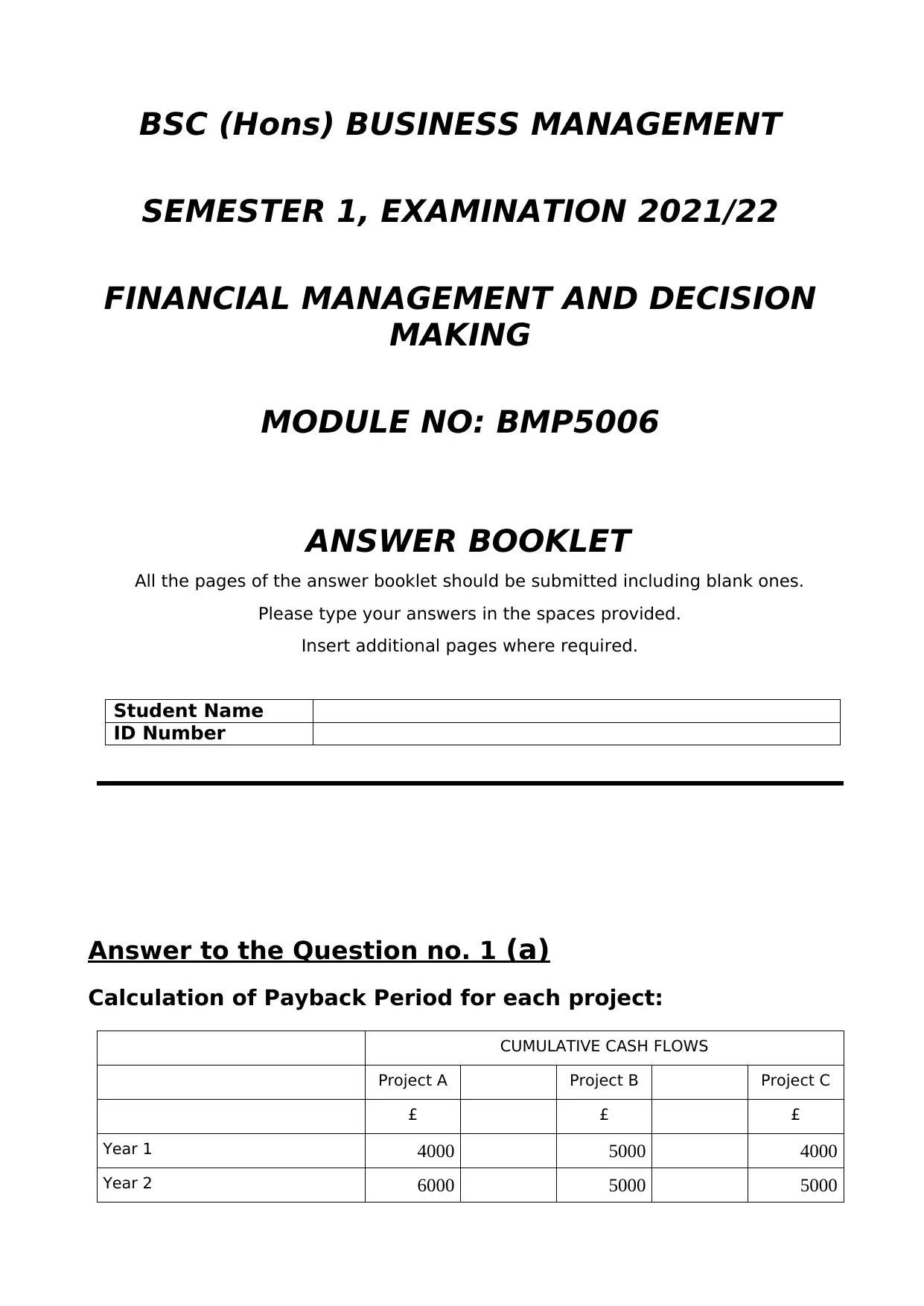

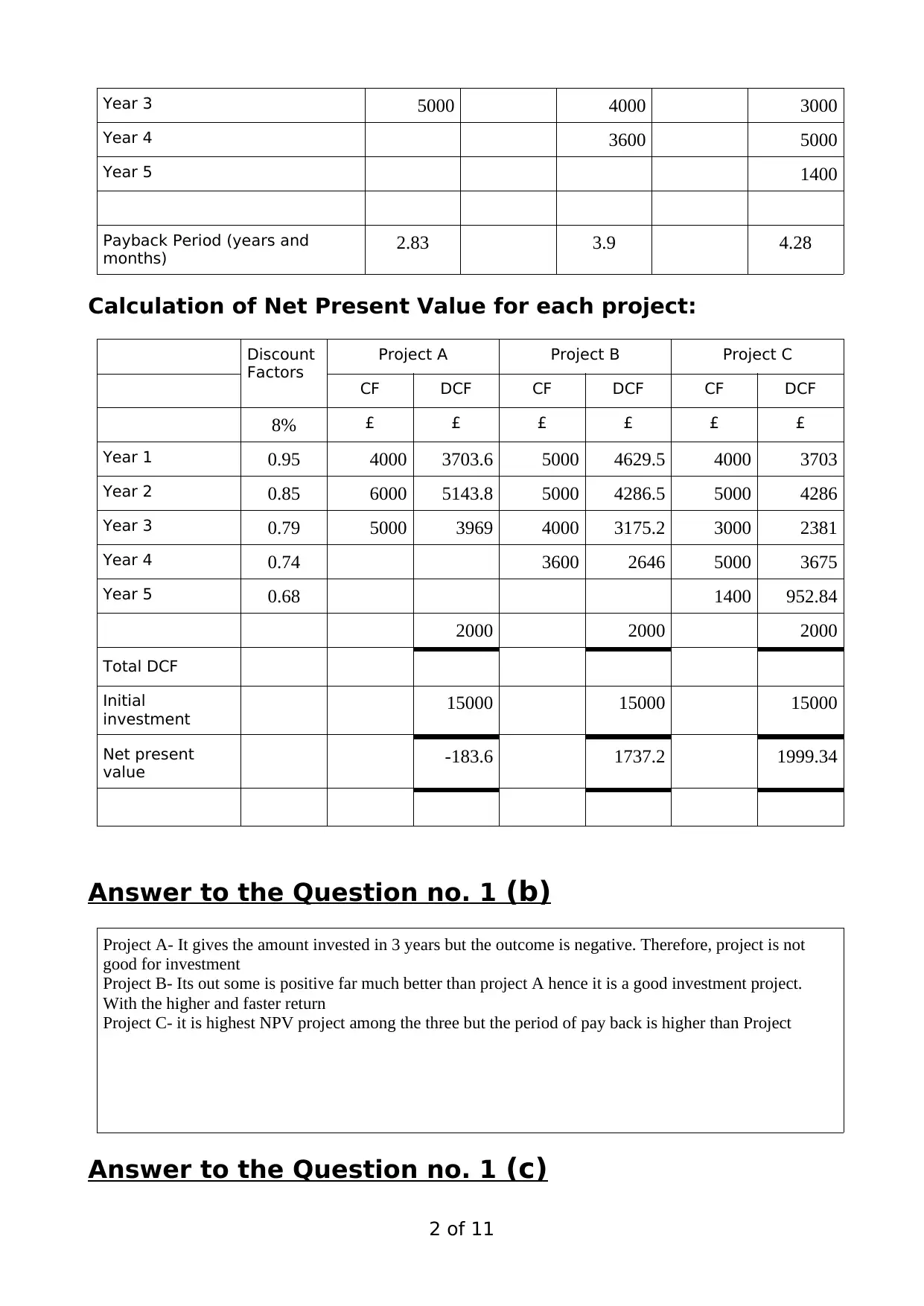

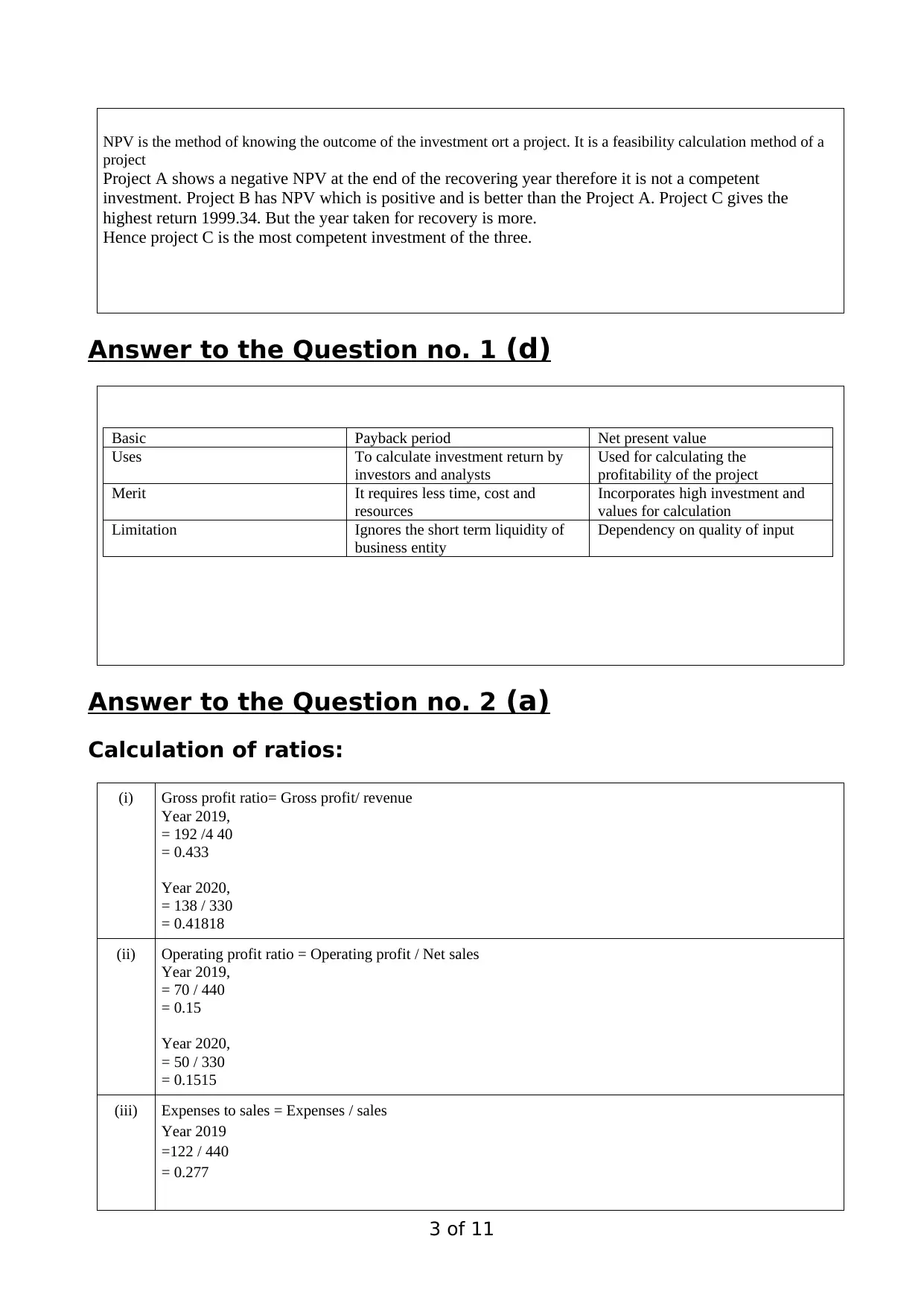

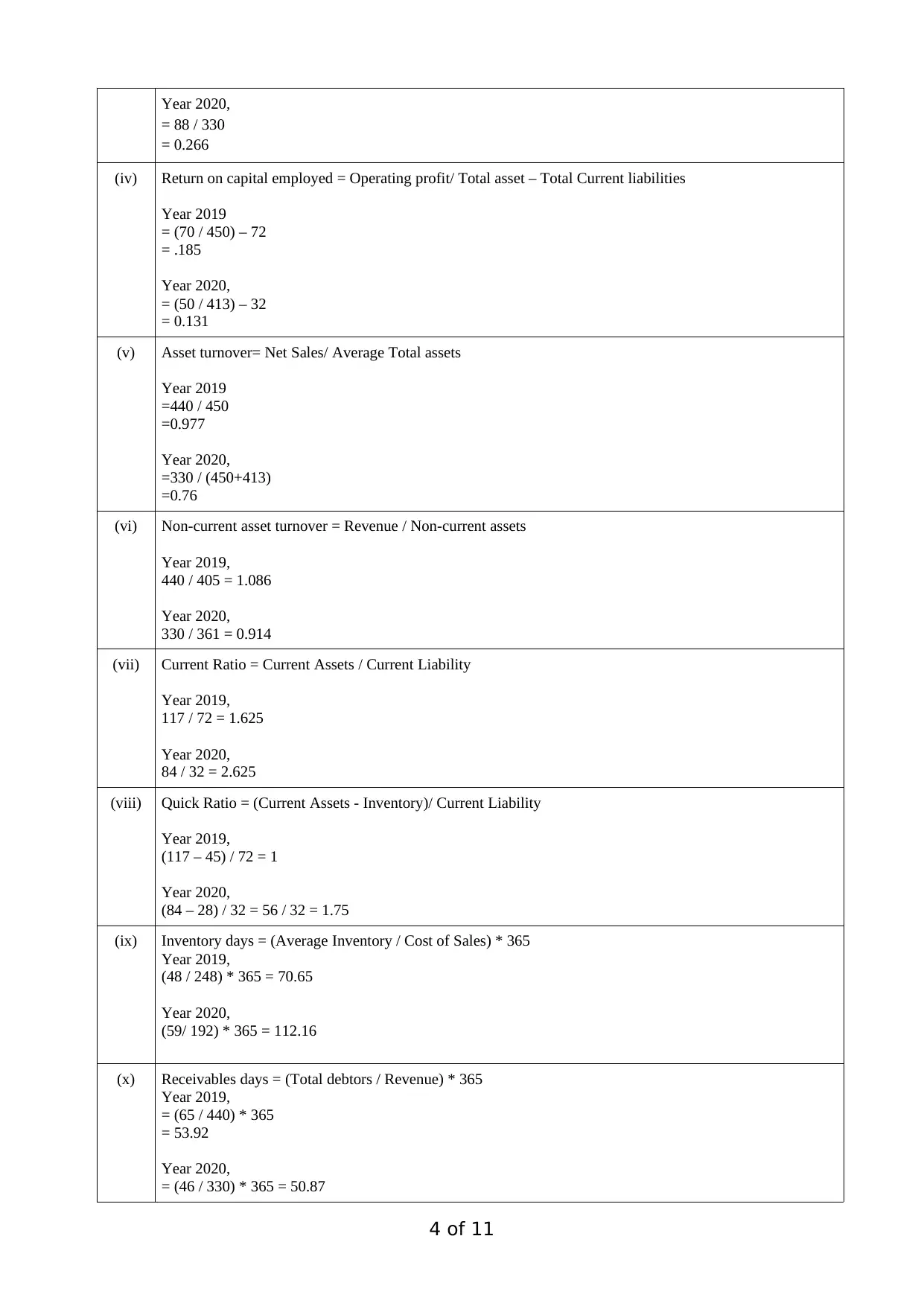

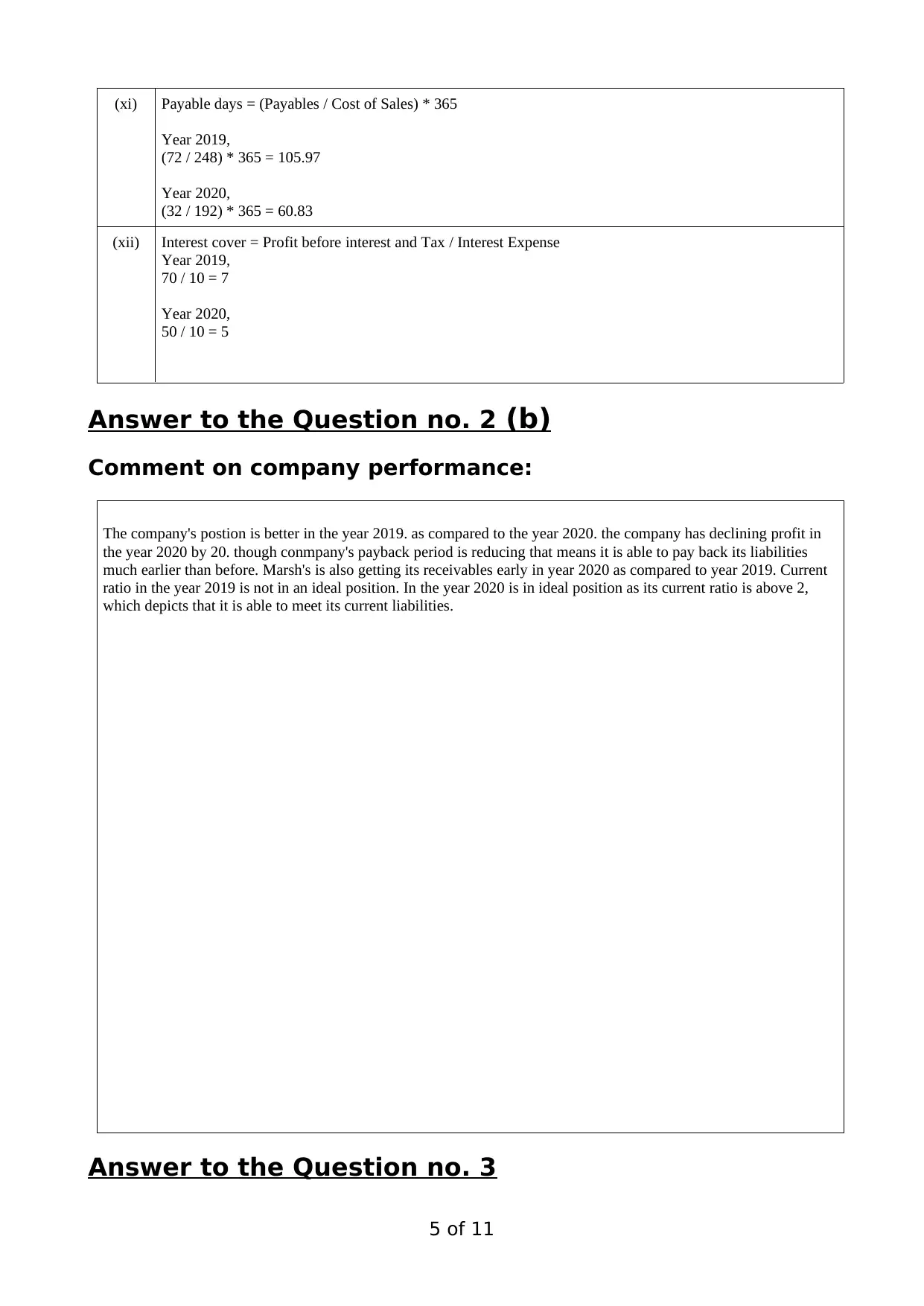

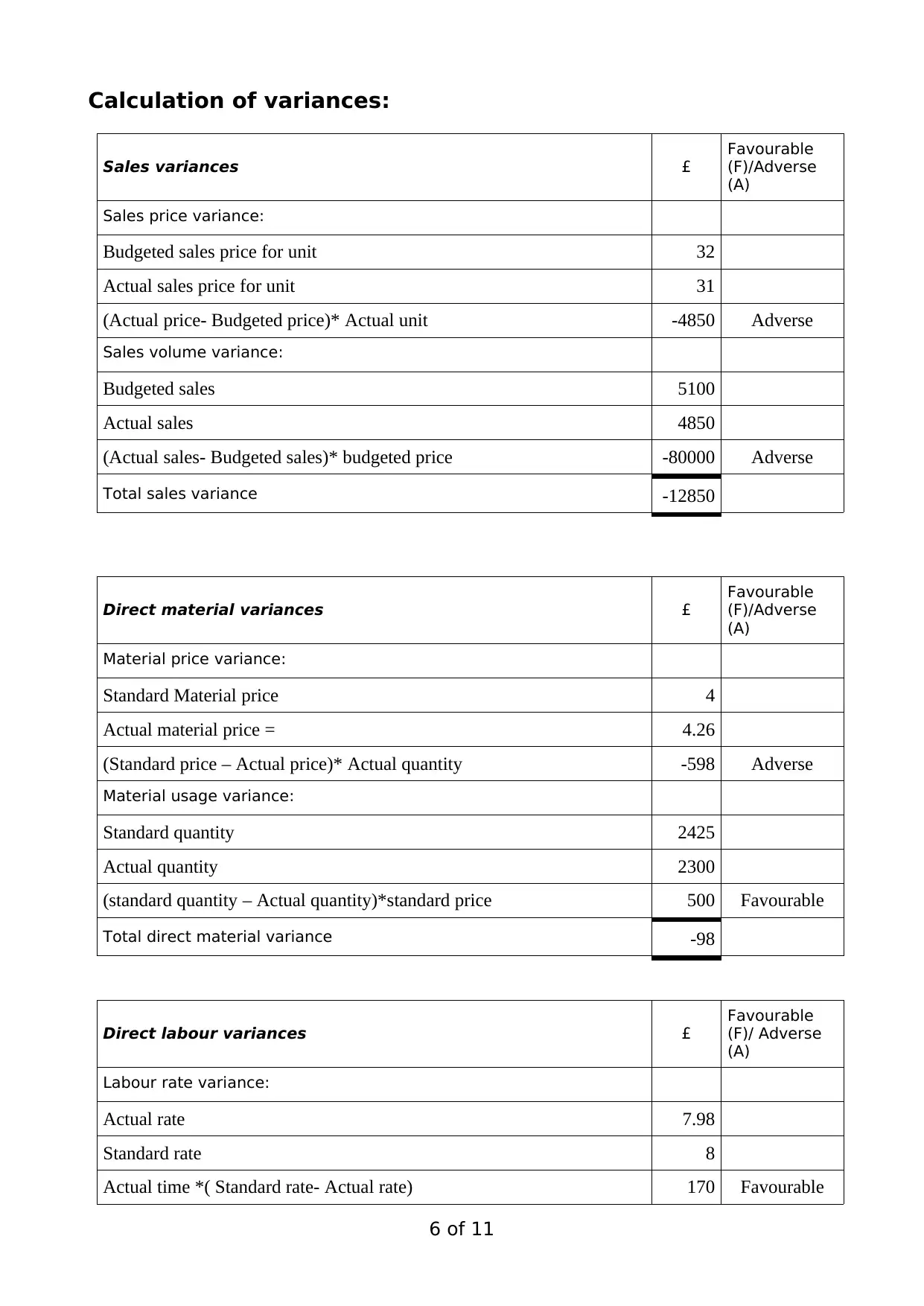

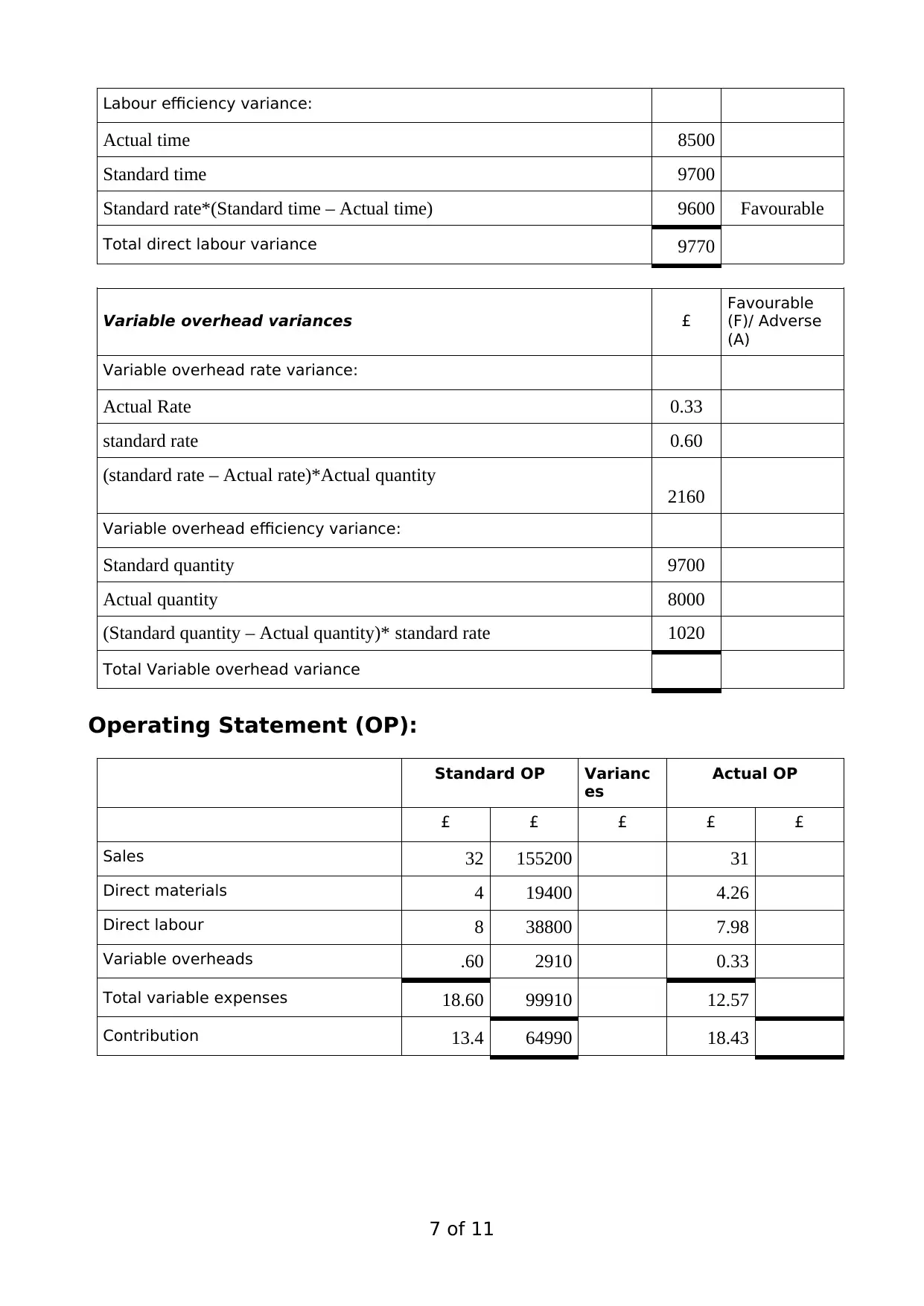

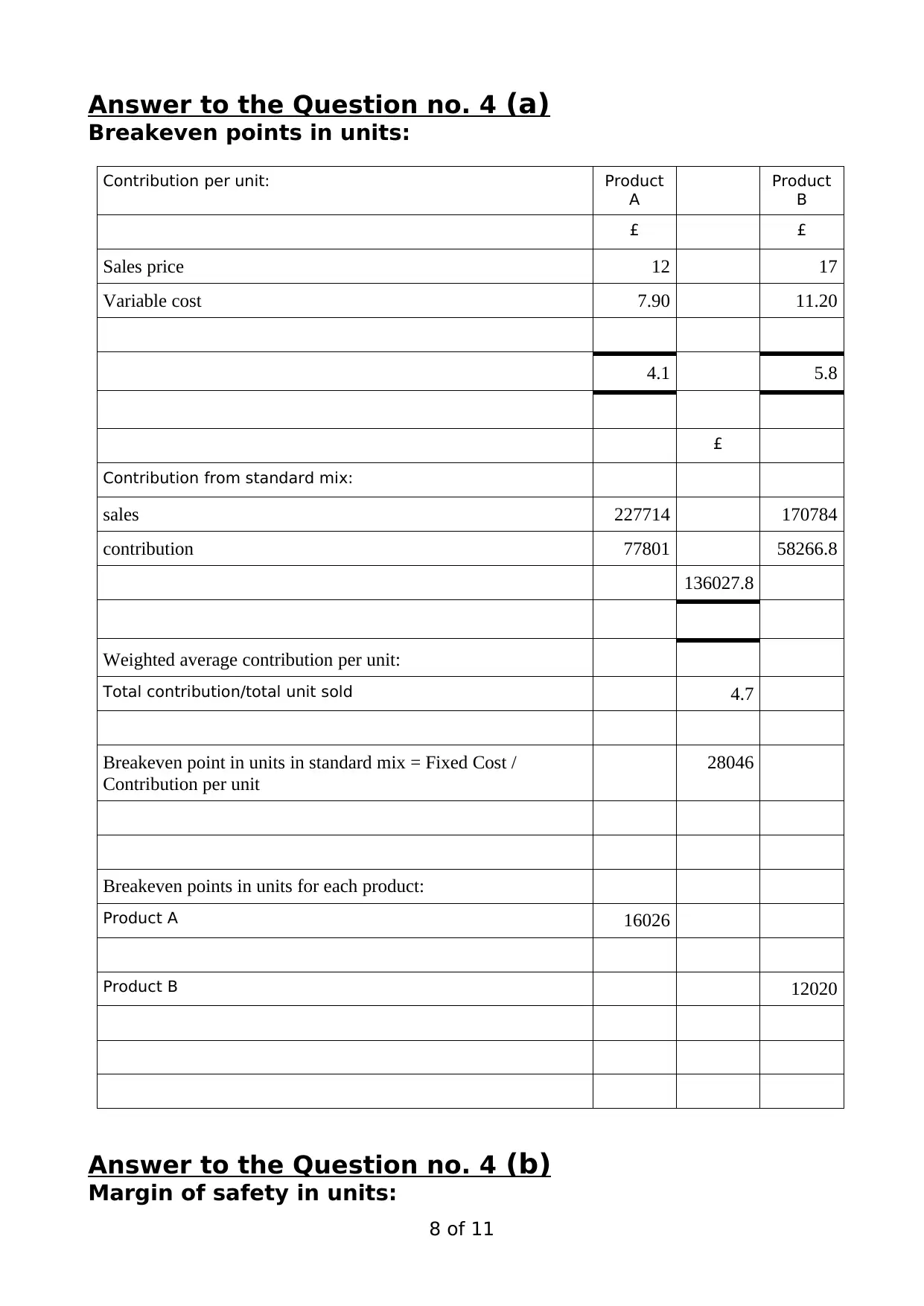

This document provides solutions to a financial management assignment covering key areas such as investment appraisal, ratio analysis, and variance analysis. Investment appraisal involves calculating the payback period and net present value (NPV) for different projects to determine the most viable investment. Ratio analysis assesses a company's financial performance by examining gross profit ratio, operating profit ratio, expenses to sales, return on capital employed, asset turnover, current ratio, quick ratio, inventory days, receivables days, payable days, and interest cover. Variance analysis calculates sales price variance, sales volume variance, material price variance, material usage variance, labor rate variance, labor efficiency variance, and variable overhead variances to evaluate operational efficiency. The assignment also addresses break-even analysis, including calculating break-even points in units and sales, margin of safety, and the relevance of break-even analysis in modern manufacturing. Finally, it outlines the significant steps in setting a financial/cost-controlling budget in a large organization. Desklib provides access to this and many other solved assignments.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.