Comprehensive Report on Financial Management & Decision Making

VerifiedAdded on 2023/06/18

|8

|2027

|473

Report

AI Summary

This report provides a detailed analysis of financial management and decision-making processes within businesses, covering key concepts such as activity-based costing (ABC), cost-volume-profit (CVP) analysis, and capital asset pricing model (CAPM). It explores the importance of budgeting as a control and performance management tool, contrasting traditional budgeting methods with more flexible approaches like beyond budgeting. The report also discusses principal means of finance for SMEs without stock market listing, including long-term loans, debentures, personal savings, and retained earnings. Furthermore, it emphasizes the need for a stakeholder approach in business, highlighting the importance of satisfying stakeholders to ensure the overall success and effective working of the company. The report concludes by referencing relevant books and journals to support its analysis and findings.

Financial management and

decision making

decision making

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

QUESTION 1...................................................................................................................................3

A..................................................................................................................................................3

B..................................................................................................................................................3

QUESTION 2...................................................................................................................................4

A..................................................................................................................................................4

B..................................................................................................................................................4

C..................................................................................................................................................4

QUESTION 3...................................................................................................................................5

A..................................................................................................................................................5

B..................................................................................................................................................5

QUESTION 4...................................................................................................................................6

Principal means of finance without stock market listing............................................................6

QUESTION 5...................................................................................................................................6

Need for stakeholder approach and related factors.....................................................................6

REFERENCES................................................................................................................................8

QUESTION 1...................................................................................................................................3

A..................................................................................................................................................3

B..................................................................................................................................................3

QUESTION 2...................................................................................................................................4

A..................................................................................................................................................4

B..................................................................................................................................................4

C..................................................................................................................................................4

QUESTION 3...................................................................................................................................5

A..................................................................................................................................................5

B..................................................................................................................................................5

QUESTION 4...................................................................................................................................6

Principal means of finance without stock market listing............................................................6

QUESTION 5...................................................................................................................................6

Need for stakeholder approach and related factors.....................................................................6

REFERENCES................................................................................................................................8

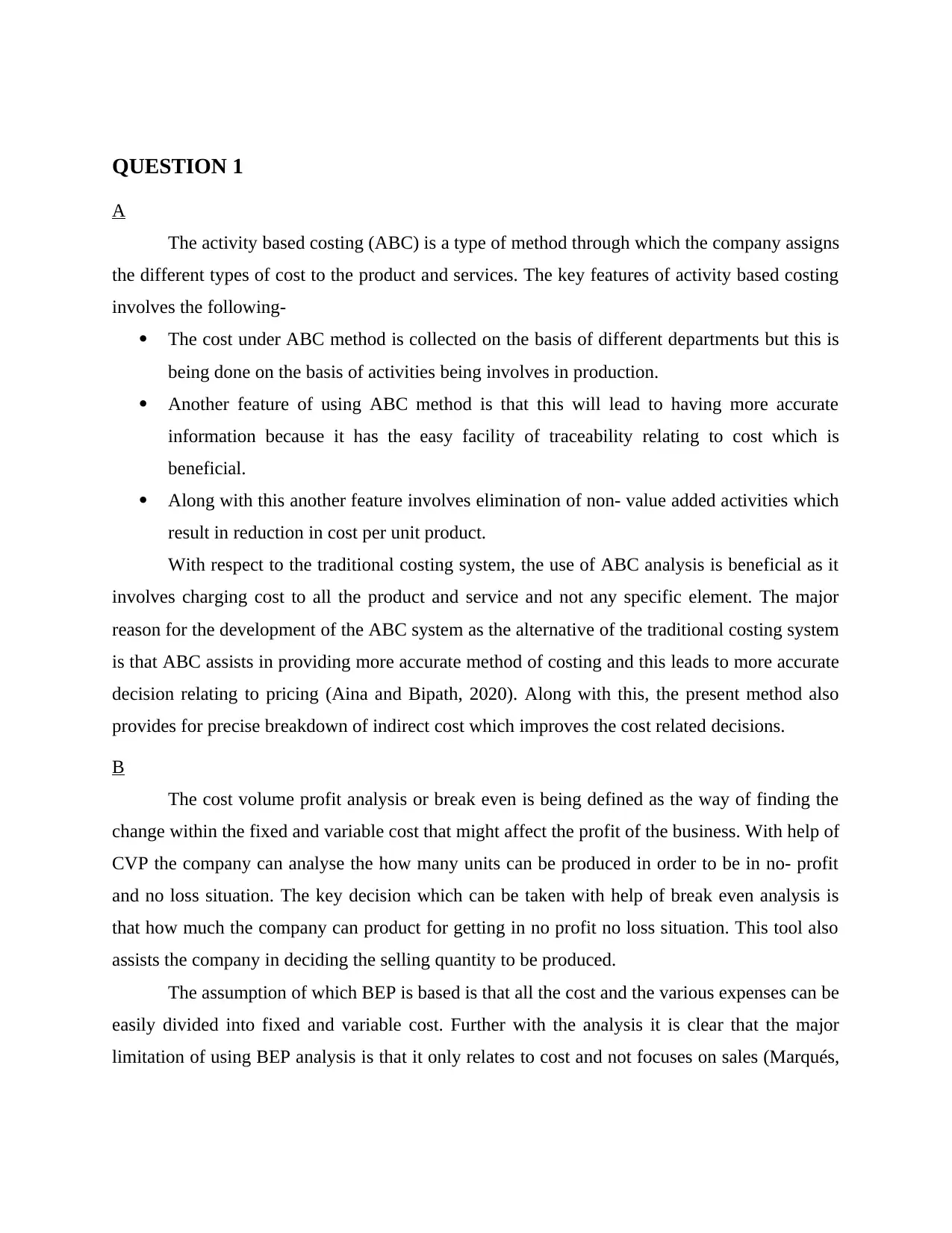

QUESTION 1

A

The activity based costing (ABC) is a type of method through which the company assigns

the different types of cost to the product and services. The key features of activity based costing

involves the following-

The cost under ABC method is collected on the basis of different departments but this is

being done on the basis of activities being involves in production.

Another feature of using ABC method is that this will lead to having more accurate

information because it has the easy facility of traceability relating to cost which is

beneficial.

Along with this another feature involves elimination of non- value added activities which

result in reduction in cost per unit product.

With respect to the traditional costing system, the use of ABC analysis is beneficial as it

involves charging cost to all the product and service and not any specific element. The major

reason for the development of the ABC system as the alternative of the traditional costing system

is that ABC assists in providing more accurate method of costing and this leads to more accurate

decision relating to pricing (Aina and Bipath, 2020). Along with this, the present method also

provides for precise breakdown of indirect cost which improves the cost related decisions.

B

The cost volume profit analysis or break even is being defined as the way of finding the

change within the fixed and variable cost that might affect the profit of the business. With help of

CVP the company can analyse the how many units can be produced in order to be in no- profit

and no loss situation. The key decision which can be taken with help of break even analysis is

that how much the company can product for getting in no profit no loss situation. This tool also

assists the company in deciding the selling quantity to be produced.

The assumption of which BEP is based is that all the cost and the various expenses can be

easily divided into fixed and variable cost. Further with the analysis it is clear that the major

limitation of using BEP analysis is that it only relates to cost and not focuses on sales (Marqués,

A

The activity based costing (ABC) is a type of method through which the company assigns

the different types of cost to the product and services. The key features of activity based costing

involves the following-

The cost under ABC method is collected on the basis of different departments but this is

being done on the basis of activities being involves in production.

Another feature of using ABC method is that this will lead to having more accurate

information because it has the easy facility of traceability relating to cost which is

beneficial.

Along with this another feature involves elimination of non- value added activities which

result in reduction in cost per unit product.

With respect to the traditional costing system, the use of ABC analysis is beneficial as it

involves charging cost to all the product and service and not any specific element. The major

reason for the development of the ABC system as the alternative of the traditional costing system

is that ABC assists in providing more accurate method of costing and this leads to more accurate

decision relating to pricing (Aina and Bipath, 2020). Along with this, the present method also

provides for precise breakdown of indirect cost which improves the cost related decisions.

B

The cost volume profit analysis or break even is being defined as the way of finding the

change within the fixed and variable cost that might affect the profit of the business. With help of

CVP the company can analyse the how many units can be produced in order to be in no- profit

and no loss situation. The key decision which can be taken with help of break even analysis is

that how much the company can product for getting in no profit no loss situation. This tool also

assists the company in deciding the selling quantity to be produced.

The assumption of which BEP is based is that all the cost and the various expenses can be

easily divided into fixed and variable cost. Further with the analysis it is clear that the major

limitation of using BEP analysis is that it only relates to cost and not focuses on sales (Marqués,

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

García and Sánchez, 2020). Along with this another limitation is that this method assumes that

fixed cost is always constant that is same at every level of production.

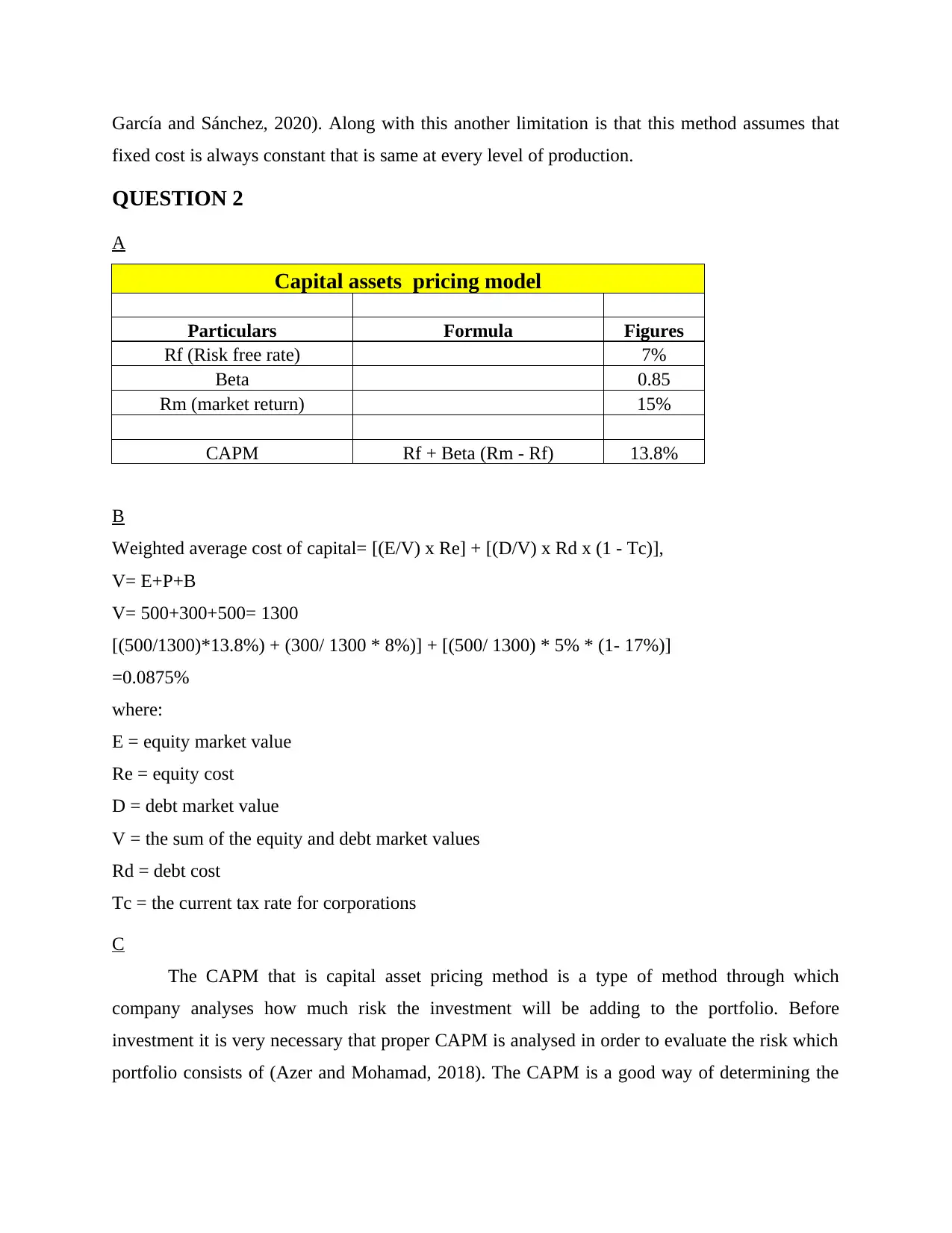

QUESTION 2

A

Capital assets pricing model

Particulars Formula Figures

Rf (Risk free rate) 7%

Beta 0.85

Rm (market return) 15%

CAPM Rf + Beta (Rm - Rf) 13.8%

B

Weighted average cost of capital= [(E/V) x Re] + [(D/V) x Rd x (1 - Tc)],

V= E+P+B

V= 500+300+500= 1300

[(500/1300)*13.8%) + (300/ 1300 * 8%)] + [(500/ 1300) * 5% * (1- 17%)]

=0.0875%

where:

E = equity market value

Re = equity cost

D = debt market value

V = the sum of the equity and debt market values

Rd = debt cost

Tc = the current tax rate for corporations

C

The CAPM that is capital asset pricing method is a type of method through which

company analyses how much risk the investment will be adding to the portfolio. Before

investment it is very necessary that proper CAPM is analysed in order to evaluate the risk which

portfolio consists of (Azer and Mohamad, 2018). The CAPM is a good way of determining the

fixed cost is always constant that is same at every level of production.

QUESTION 2

A

Capital assets pricing model

Particulars Formula Figures

Rf (Risk free rate) 7%

Beta 0.85

Rm (market return) 15%

CAPM Rf + Beta (Rm - Rf) 13.8%

B

Weighted average cost of capital= [(E/V) x Re] + [(D/V) x Rd x (1 - Tc)],

V= E+P+B

V= 500+300+500= 1300

[(500/1300)*13.8%) + (300/ 1300 * 8%)] + [(500/ 1300) * 5% * (1- 17%)]

=0.0875%

where:

E = equity market value

Re = equity cost

D = debt market value

V = the sum of the equity and debt market values

Rd = debt cost

Tc = the current tax rate for corporations

C

The CAPM that is capital asset pricing method is a type of method through which

company analyses how much risk the investment will be adding to the portfolio. Before

investment it is very necessary that proper CAPM is analysed in order to evaluate the risk which

portfolio consists of (Azer and Mohamad, 2018). The CAPM is a good way of determining the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

cost of equity because it provides rate of return which the company pays to the equity investors.

Hence, it provides a proper cost of equity and this is beneficial for the company.

QUESTION 3

A

With the views of Humaidi and et.al., (2020) the budgeting can be used as a tool of

controlling and management of performance. The reason underlying this fact is that in case the

budgets are prepared then this provides for a better guidance to company that how they have to

manage the working. Thus, this provides as a guidance note to the employees that they have to

perform within the provided limit only.

Moreover in support of this Lichtenberg and et.al., (2018) articulates that budgeting as a

tool assist the company in forecasting the working in better manner. Hence, as a result of this the

working of the business will be improved. Also the target being set will motivate the people in

working in better manner so that the targets can be attained. In addition to this, the budgeting is

also an important tool of working because of the reason that it will help company in improving

the performance in better and effective manner.

Also, this budgeting assists the business in keeping the track of the finance in proper

manner. The reason behind this fact is that in case the finance will be properly managed then this

will improve the working efficiency of the business. Moreover, the clear communication of the

budget will assist in proper sharing of information which will help in better working.

B

The traditional budgeting may be stated as preparation of budget by keeping the past data

as the base. The various limitation of traditional budgeting system involves the following-

The major limitation of traditional budgeting is that it consumes a lot of time and

resources. This is because of the reason that first it analyses past data and then predict the future.

Along with this another limitation is that there is low change responsiveness of the

budget being prepared. This is because of the reason that fewer reviews are made and latest

things can be missed within the budget.

Along with this, the new concept of beyond budgeting that is flexible budgeting is getting

popular. Under this method of budgeting it is flexible and not fixed and depends on the changes

being taking place in external environment (Ross III and Coambs, 2018). The feature of beyond

Hence, it provides a proper cost of equity and this is beneficial for the company.

QUESTION 3

A

With the views of Humaidi and et.al., (2020) the budgeting can be used as a tool of

controlling and management of performance. The reason underlying this fact is that in case the

budgets are prepared then this provides for a better guidance to company that how they have to

manage the working. Thus, this provides as a guidance note to the employees that they have to

perform within the provided limit only.

Moreover in support of this Lichtenberg and et.al., (2018) articulates that budgeting as a

tool assist the company in forecasting the working in better manner. Hence, as a result of this the

working of the business will be improved. Also the target being set will motivate the people in

working in better manner so that the targets can be attained. In addition to this, the budgeting is

also an important tool of working because of the reason that it will help company in improving

the performance in better and effective manner.

Also, this budgeting assists the business in keeping the track of the finance in proper

manner. The reason behind this fact is that in case the finance will be properly managed then this

will improve the working efficiency of the business. Moreover, the clear communication of the

budget will assist in proper sharing of information which will help in better working.

B

The traditional budgeting may be stated as preparation of budget by keeping the past data

as the base. The various limitation of traditional budgeting system involves the following-

The major limitation of traditional budgeting is that it consumes a lot of time and

resources. This is because of the reason that first it analyses past data and then predict the future.

Along with this another limitation is that there is low change responsiveness of the

budget being prepared. This is because of the reason that fewer reviews are made and latest

things can be missed within the budget.

Along with this, the new concept of beyond budgeting that is flexible budgeting is getting

popular. Under this method of budgeting it is flexible and not fixed and depends on the changes

being taking place in external environment (Ross III and Coambs, 2018). The feature of beyond

budgeting involves the fact that is includes all the changes being taking place in the external

environment. Along with this another feature is that this type of budget can be prepared for

managing obstacles of change.

QUESTION 4

Principal means of finance without stock market listing

The finance is the most essential element for any of the company to operate and

especially for the SME. The reason underlying this fact is that SME operates at small level and it

is not necessary that it have proper finance (Musah, Gakpetor and Pomaa, 2018). The source of

finance other than listing involves the following-

Long Term loan- this is a source of finance wherein the company can borrow the money

from banks or other financial institution. Under this source of finance both the company

can borrow money and against it they have to pay some interest.

Debenture- this is another way through which both the companies can arrange finance

without listing. This is type of debt instrument which does not require any collateral and

money can be arranged without giving any ownership to the provider of money.

Personal savings- this is yet another source of finance wherein both the company can

arrange for the finance of the business. Under this method both the companies can use

their own personal saving and other money which they have with them.

Retained earnings- this is a source of finance in which the company can use the

accumulated profit of the business which they have kept aside for future use. This money

is being kept aside by the company and is being used for dealing with the future

contingencies.

QUESTION 5

Need for stakeholder approach and related factors

For the business it is very important that there is a focus on the stakeholder approach and

other factors affecting. The reason behind this fact is that in case the stakeholders will not be

satisfied then this will be affecting the working capability of the business. The stakeholders

involve each and every person who is interested in the betterment and development of the

business (Al Ahbabi and Nobanee, 2019). For the company to be successful it is necessary

stakeholder are satisfied and happy with the performance. The stakeholder approach is very

environment. Along with this another feature is that this type of budget can be prepared for

managing obstacles of change.

QUESTION 4

Principal means of finance without stock market listing

The finance is the most essential element for any of the company to operate and

especially for the SME. The reason underlying this fact is that SME operates at small level and it

is not necessary that it have proper finance (Musah, Gakpetor and Pomaa, 2018). The source of

finance other than listing involves the following-

Long Term loan- this is a source of finance wherein the company can borrow the money

from banks or other financial institution. Under this source of finance both the company

can borrow money and against it they have to pay some interest.

Debenture- this is another way through which both the companies can arrange finance

without listing. This is type of debt instrument which does not require any collateral and

money can be arranged without giving any ownership to the provider of money.

Personal savings- this is yet another source of finance wherein both the company can

arrange for the finance of the business. Under this method both the companies can use

their own personal saving and other money which they have with them.

Retained earnings- this is a source of finance in which the company can use the

accumulated profit of the business which they have kept aside for future use. This money

is being kept aside by the company and is being used for dealing with the future

contingencies.

QUESTION 5

Need for stakeholder approach and related factors

For the business it is very important that there is a focus on the stakeholder approach and

other factors affecting. The reason behind this fact is that in case the stakeholders will not be

satisfied then this will be affecting the working capability of the business. The stakeholders

involve each and every person who is interested in the betterment and development of the

business (Al Ahbabi and Nobanee, 2019). For the company to be successful it is necessary

stakeholder are satisfied and happy with the performance. The stakeholder approach is very

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

useful for the business as this will assist in complete development of the business in better and

effective manner. Along with this, another need of doing stakeholder approach is that in case any

of the stakeholders will not be happy then this will be affecting the working of the company. For

instance, in case employees are not satisfied then this will be affecting the working of the

business to a great extent (Brigham and Houston, 2021). When the employee will not be satisfied

then they will not be performing well and as a result of this overall working will be affected.

Hence, for implementing any of the strategy or any other element it is necessary for the company

that they effectively implement the stakeholder approach and not just focus on shareholder rather

emphasize on stakeholder.

effective manner. Along with this, another need of doing stakeholder approach is that in case any

of the stakeholders will not be happy then this will be affecting the working of the company. For

instance, in case employees are not satisfied then this will be affecting the working of the

business to a great extent (Brigham and Houston, 2021). When the employee will not be satisfied

then they will not be performing well and as a result of this overall working will be affected.

Hence, for implementing any of the strategy or any other element it is necessary for the company

that they effectively implement the stakeholder approach and not just focus on shareholder rather

emphasize on stakeholder.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals

Aina, A. Y. and Bipath, K., 2020. School financial management: Insights for decision making in

public primary schools. South African Journal of Education. 40(4).

Al Ahbabi, A. R. and Nobanee, H., 2019. Conceptual building of sustainable financial

management & sustainable financial growth. Available at SSRN 3472313.

Azer, I. and Mohamad, S. A., 2018. Exploring financial management practices and problems

among students. Int. J. Acad. Res. Bus. Soc. Sci. 8. pp.2472-2477.

Brigham, E. F. and Houston, J. F., 2021. Fundamentals of financial management. Cengage

Learning.

Humaidi, A., and et.al., 2020. The Effect of Financial Technology, Demography, and Financial

Literacy on Financial Management Behavior of Productive Age in Surabaya,

Indonesia. International Journal of Advances in Scientific Research and

Engineering. 6(01). pp.77-81.

Lichtenberg, P. A., and et.al., 2018. Conceptual and empirical approaches to financial decision-

making by older adults: Results from a financial decision-making rating scale. Clinical

gerontologist. 41(1). pp.42-65.

Marqués, A. I., García, V. and Sánchez, J. S., 2020. Ranking-based MCDM models in financial

management applications: analysis and emerging challenges. Progress in Artificial

Intelligence. 9. pp.171-193.

Musah, A., Gakpetor, E. D. and Pomaa, P., 2018. Financial management practices, firm growth

and profitability of small and medium scale enterprises (SMEs). Information

management and business review. 10(3). pp.25-37.

Ross III, D. B. and Coambs, E., 2018. The impact of psychological trauma on finance: narrative

financial therapy considerations in exploring complex trauma and impaired financial

decision making. Journal of Financial Therapy. 9(2). p.4.

Books and Journals

Aina, A. Y. and Bipath, K., 2020. School financial management: Insights for decision making in

public primary schools. South African Journal of Education. 40(4).

Al Ahbabi, A. R. and Nobanee, H., 2019. Conceptual building of sustainable financial

management & sustainable financial growth. Available at SSRN 3472313.

Azer, I. and Mohamad, S. A., 2018. Exploring financial management practices and problems

among students. Int. J. Acad. Res. Bus. Soc. Sci. 8. pp.2472-2477.

Brigham, E. F. and Houston, J. F., 2021. Fundamentals of financial management. Cengage

Learning.

Humaidi, A., and et.al., 2020. The Effect of Financial Technology, Demography, and Financial

Literacy on Financial Management Behavior of Productive Age in Surabaya,

Indonesia. International Journal of Advances in Scientific Research and

Engineering. 6(01). pp.77-81.

Lichtenberg, P. A., and et.al., 2018. Conceptual and empirical approaches to financial decision-

making by older adults: Results from a financial decision-making rating scale. Clinical

gerontologist. 41(1). pp.42-65.

Marqués, A. I., García, V. and Sánchez, J. S., 2020. Ranking-based MCDM models in financial

management applications: analysis and emerging challenges. Progress in Artificial

Intelligence. 9. pp.171-193.

Musah, A., Gakpetor, E. D. and Pomaa, P., 2018. Financial management practices, firm growth

and profitability of small and medium scale enterprises (SMEs). Information

management and business review. 10(3). pp.25-37.

Ross III, D. B. and Coambs, E., 2018. The impact of psychological trauma on finance: narrative

financial therapy considerations in exploring complex trauma and impaired financial

decision making. Journal of Financial Therapy. 9(2). p.4.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.