Detailed Financial Analysis: Viability of a Chocolate Retail Business

VerifiedAdded on 2023/06/03

|30

|8007

|477

Case Study

AI Summary

This case study provides a comprehensive financial analysis of a proposed chocolate retail business in Norway. It includes an assessment of initial investment requirements, assumptions, breakeven analysis, forecasted income statement, balance sheet, and cash flow statement. Furthermore, a discounted cash flow analysis and sensitivity analysis are performed to evaluate the project's financial viability. The analysis helps determine whether the business plan is feasible and provides recommendations for Uncle Benjamin to proceed, considering factors such as import costs, sales volume, and market conditions. The report aims to equip the business owner with the necessary insights to make informed decisions regarding the financial sustainability of the chocolate retail venture.

Running head: FINANCIAL MANAGEMENT

Financial Management

Name of the Student:

Name of the University:

Author’s Note

Financial Management

Name of the Student:

Name of the University:

Author’s Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

FINANCIAL MANAGEMENT

Executive Summary

The main purpose of this assessment is to analyze the case study which is provided stating a plan

to open a Chocolate retail business in Norway. The assessment shows detail analysis of the

various estimations which are considered in this assessment along with other statements which

are prepared. The assessment shows analysis of investment capabilities of the owner along with

evaluation of income statement, balance sheet and cash flow statement. In addition to this, a

discounted cash flow statement and Sensitivity analysis is also included in the discussion part of

the report. The assessment aims to establish whether the owner should proceed with the plan and

also establish the financial viability of the project.

FINANCIAL MANAGEMENT

Executive Summary

The main purpose of this assessment is to analyze the case study which is provided stating a plan

to open a Chocolate retail business in Norway. The assessment shows detail analysis of the

various estimations which are considered in this assessment along with other statements which

are prepared. The assessment shows analysis of investment capabilities of the owner along with

evaluation of income statement, balance sheet and cash flow statement. In addition to this, a

discounted cash flow statement and Sensitivity analysis is also included in the discussion part of

the report. The assessment aims to establish whether the owner should proceed with the plan and

also establish the financial viability of the project.

2

FINANCIAL MANAGEMENT

Table of Contents

Introduction......................................................................................................................................3

Discussion........................................................................................................................................4

Initial Investment Requirement...................................................................................................4

Assumptions................................................................................................................................5

Breakeven Analysis.....................................................................................................................7

Income Statement Analysis for the Period..................................................................................9

Balance Sheet for the Period......................................................................................................11

Cash Flow Statement Analysis of the Business.........................................................................14

Discounted Cash Flow Analysis for the Proposed Business.....................................................15

Capital Requirement of the Proposed Business.........................................................................17

Sensitivity Analysis for the Proposed Business.........................................................................18

Conclusion and Recommendation.................................................................................................20

Bibliography..................................................................................................................................22

Appendix..........................................................................................................................................0

FINANCIAL MANAGEMENT

Table of Contents

Introduction......................................................................................................................................3

Discussion........................................................................................................................................4

Initial Investment Requirement...................................................................................................4

Assumptions................................................................................................................................5

Breakeven Analysis.....................................................................................................................7

Income Statement Analysis for the Period..................................................................................9

Balance Sheet for the Period......................................................................................................11

Cash Flow Statement Analysis of the Business.........................................................................14

Discounted Cash Flow Analysis for the Proposed Business.....................................................15

Capital Requirement of the Proposed Business.........................................................................17

Sensitivity Analysis for the Proposed Business.........................................................................18

Conclusion and Recommendation.................................................................................................20

Bibliography..................................................................................................................................22

Appendix..........................................................................................................................................0

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

FINANCIAL MANAGEMENT

Introduction

The main purpose of this assessment is to analyze the viability of a business plan which

as per the case study which is provided. As per the case study provided, Uncle Benjamin who

wants to open a chocolate retail store which would be supplying gourmet chocolates for which

the financial viability would be checked. The business would be getting supplies of chocolates

from Zurich and also Switzerland. The business aims to get trading license from Zurich for a

period of five years and also get trade license from Switzerland. The analysis for viability of the

project would be including breakeven analysis which would be estimating the minimum sales

which the business needs to achieve in order to continue operations of the business (King 2013).

The analysis is conducted for the purpose of helping Uncle Benjamin in estimating the sales and

profit which can be generated from the retail business (Hammond and Berman 2013). The

owners of the business also anticipate that the importing of Chocolate materials from

Switzerland would also allow certain portion of discount to the business which will further

reduce the overall costs of the business.

In addition to Breakeven analysis, a forecasted financial statement of the business is to be

prepared and analyzed in order to identify the performance areas and the capacity of the business

to generate profits. The report would also be showing various assumptions and justifications

which are considered by the business in the analysis of the viability of the project and would also

help in the decision-making process of the business (Jary and Wileman 2016). The analysis also

includes Sensitivity analysis which would allow Uncle Benjamin to compare between different

scenarios. In addition to this, time value of the estimated profitability of the business will be

evaluated with the help of Discounted Cash Flow Model.

FINANCIAL MANAGEMENT

Introduction

The main purpose of this assessment is to analyze the viability of a business plan which

as per the case study which is provided. As per the case study provided, Uncle Benjamin who

wants to open a chocolate retail store which would be supplying gourmet chocolates for which

the financial viability would be checked. The business would be getting supplies of chocolates

from Zurich and also Switzerland. The business aims to get trading license from Zurich for a

period of five years and also get trade license from Switzerland. The analysis for viability of the

project would be including breakeven analysis which would be estimating the minimum sales

which the business needs to achieve in order to continue operations of the business (King 2013).

The analysis is conducted for the purpose of helping Uncle Benjamin in estimating the sales and

profit which can be generated from the retail business (Hammond and Berman 2013). The

owners of the business also anticipate that the importing of Chocolate materials from

Switzerland would also allow certain portion of discount to the business which will further

reduce the overall costs of the business.

In addition to Breakeven analysis, a forecasted financial statement of the business is to be

prepared and analyzed in order to identify the performance areas and the capacity of the business

to generate profits. The report would also be showing various assumptions and justifications

which are considered by the business in the analysis of the viability of the project and would also

help in the decision-making process of the business (Jary and Wileman 2016). The analysis also

includes Sensitivity analysis which would allow Uncle Benjamin to compare between different

scenarios. In addition to this, time value of the estimated profitability of the business will be

evaluated with the help of Discounted Cash Flow Model.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

FINANCIAL MANAGEMENT

Discussion

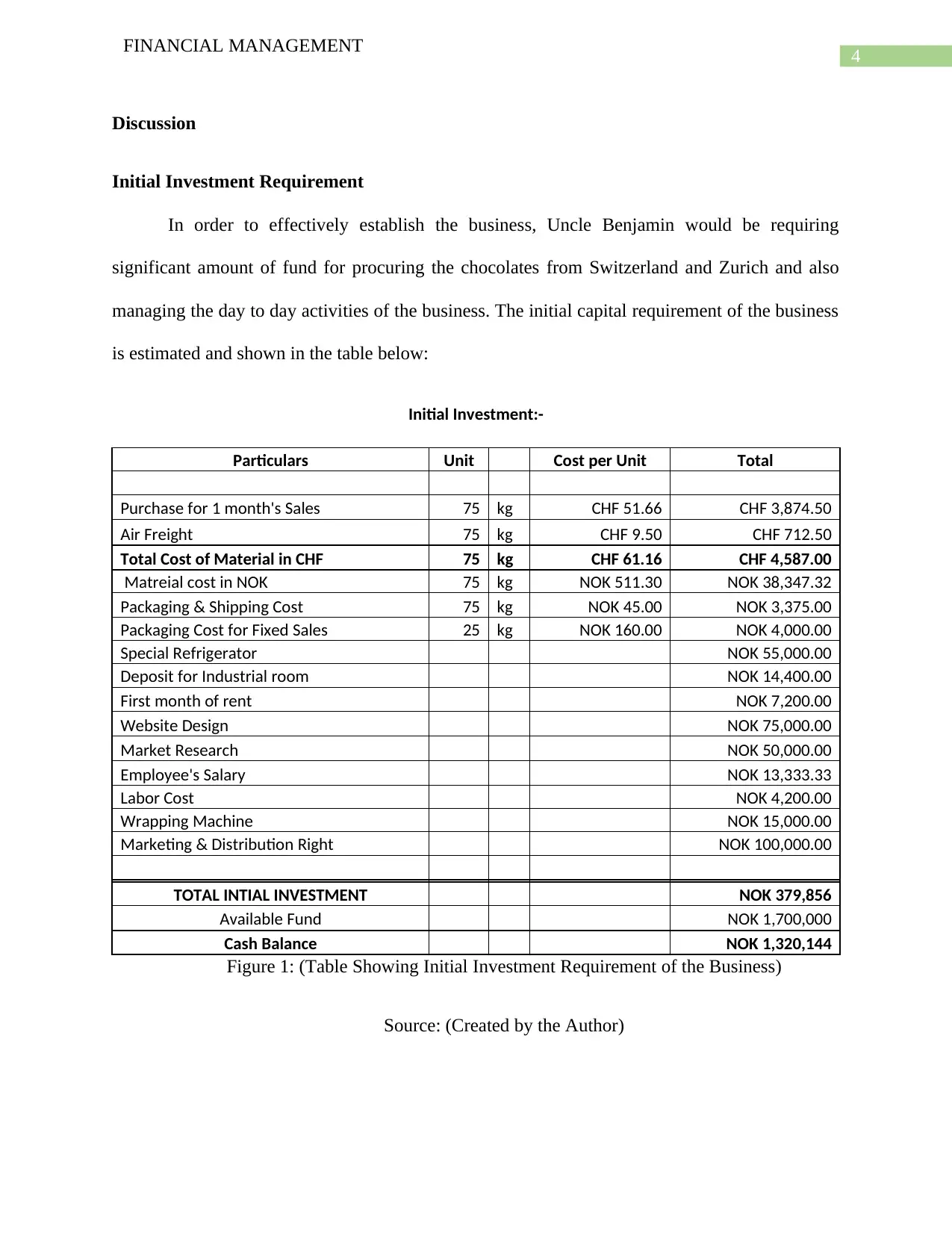

Initial Investment Requirement

In order to effectively establish the business, Uncle Benjamin would be requiring

significant amount of fund for procuring the chocolates from Switzerland and Zurich and also

managing the day to day activities of the business. The initial capital requirement of the business

is estimated and shown in the table below:

Initial Investment:-

Particulars Unit Cost per Unit Total

Purchase for 1 month's Sales 75 kg CHF 51.66 CHF 3,874.50

Air Freight 75 kg CHF 9.50 CHF 712.50

Total Cost of Material in CHF 75 kg CHF 61.16 CHF 4,587.00

Matreial cost in NOK 75 kg NOK 511.30 NOK 38,347.32

Packaging & Shipping Cost 75 kg NOK 45.00 NOK 3,375.00

Packaging Cost for Fixed Sales 25 kg NOK 160.00 NOK 4,000.00

Special Refrigerator NOK 55,000.00

Deposit for Industrial room NOK 14,400.00

First month of rent NOK 7,200.00

Website Design NOK 75,000.00

Market Research NOK 50,000.00

Employee's Salary NOK 13,333.33

Labor Cost NOK 4,200.00

Wrapping Machine NOK 15,000.00

Marketing & Distribution Right NOK 100,000.00

TOTAL INTIAL INVESTMENT NOK 379,856

Available Fund NOK 1,700,000

Cash Balance NOK 1,320,144

Figure 1: (Table Showing Initial Investment Requirement of the Business)

Source: (Created by the Author)

FINANCIAL MANAGEMENT

Discussion

Initial Investment Requirement

In order to effectively establish the business, Uncle Benjamin would be requiring

significant amount of fund for procuring the chocolates from Switzerland and Zurich and also

managing the day to day activities of the business. The initial capital requirement of the business

is estimated and shown in the table below:

Initial Investment:-

Particulars Unit Cost per Unit Total

Purchase for 1 month's Sales 75 kg CHF 51.66 CHF 3,874.50

Air Freight 75 kg CHF 9.50 CHF 712.50

Total Cost of Material in CHF 75 kg CHF 61.16 CHF 4,587.00

Matreial cost in NOK 75 kg NOK 511.30 NOK 38,347.32

Packaging & Shipping Cost 75 kg NOK 45.00 NOK 3,375.00

Packaging Cost for Fixed Sales 25 kg NOK 160.00 NOK 4,000.00

Special Refrigerator NOK 55,000.00

Deposit for Industrial room NOK 14,400.00

First month of rent NOK 7,200.00

Website Design NOK 75,000.00

Market Research NOK 50,000.00

Employee's Salary NOK 13,333.33

Labor Cost NOK 4,200.00

Wrapping Machine NOK 15,000.00

Marketing & Distribution Right NOK 100,000.00

TOTAL INTIAL INVESTMENT NOK 379,856

Available Fund NOK 1,700,000

Cash Balance NOK 1,320,144

Figure 1: (Table Showing Initial Investment Requirement of the Business)

Source: (Created by the Author)

5

FINANCIAL MANAGEMENT

The above table shows the initial investment which is estimated by the owner of the

business. The main selling products which is chocolate gourmet are being imported from

Switzerland and Zurich therefore the business needs to incur air fare for importing the

chocolates. In addition to this, the initial supply advance also needs to be paid by the owner of

the business. In addition to this, the business also needs to incur the following costs which are

shown in the table above in order to make the product of the business marketable (Popov and

Roosenboom 2013). There are certain assumptions which are considered while arriving at the

total initial investment which is required by the business. The marketing and distribution rights

for the products are assumed to be NOK 100,000 and the same is shown in the table above. The

initial requirement as per the table which is shown above is estimated to be NOK 3,79,856

considering all the initial expenses and maintenance requirements of the business. Uncle

Benjamin has the option of taking a loan for financing the initial expenses and meeting the initial

investment requirement of the business. However, the owner does not require to do so as it is

anticipated that all the initial investment would be met effectively with the lumpsum payment

which Uncle Benjamin received from retirement. This would enable the management of the

business to effectively finance all activities of the business smoothly (Laffy and Walters 2016).

The table which is shown above demonstrates that the business has appropriate funds to meet the

initial investment of the business and also would be left with a closing cash balance of NOK

1,320,144 which can be further invested in the activities of the business.

Assumptions

In order to estimate the profitability and breakeven analysis of the business, various

assumptions are considered for the analysis. The initial investment of the business shows the

marketing and distribution rights of the products is considered on an assumption basis judging

FINANCIAL MANAGEMENT

The above table shows the initial investment which is estimated by the owner of the

business. The main selling products which is chocolate gourmet are being imported from

Switzerland and Zurich therefore the business needs to incur air fare for importing the

chocolates. In addition to this, the initial supply advance also needs to be paid by the owner of

the business. In addition to this, the business also needs to incur the following costs which are

shown in the table above in order to make the product of the business marketable (Popov and

Roosenboom 2013). There are certain assumptions which are considered while arriving at the

total initial investment which is required by the business. The marketing and distribution rights

for the products are assumed to be NOK 100,000 and the same is shown in the table above. The

initial requirement as per the table which is shown above is estimated to be NOK 3,79,856

considering all the initial expenses and maintenance requirements of the business. Uncle

Benjamin has the option of taking a loan for financing the initial expenses and meeting the initial

investment requirement of the business. However, the owner does not require to do so as it is

anticipated that all the initial investment would be met effectively with the lumpsum payment

which Uncle Benjamin received from retirement. This would enable the management of the

business to effectively finance all activities of the business smoothly (Laffy and Walters 2016).

The table which is shown above demonstrates that the business has appropriate funds to meet the

initial investment of the business and also would be left with a closing cash balance of NOK

1,320,144 which can be further invested in the activities of the business.

Assumptions

In order to estimate the profitability and breakeven analysis of the business, various

assumptions are considered for the analysis. The initial investment of the business shows the

marketing and distribution rights of the products is considered on an assumption basis judging

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

FINANCIAL MANAGEMENT

from the tenure of such rights and the quantity of order placed per consignment. In addition to

this, assumptions have been made regarding the exchange rate of currency. As the business is

importing chocolate products from Zurich and Switzerland, the business would have to pay such

expenses in foreign currency and therefore conversion of domestic currency must be done to

foreign currency. In breakeven analysis, the business needs to consider the prevailing conversion

rate and the same is considered to be 8.36 which is the conversion rate prevailing on the date

when the analysis is undertaken by the owners. The conversion rate can change and such needs

to be considered appropriately by Uncle Benjamin. In the estimation of the sales volume which

can be achieved by the business in terms of variable sales is also considered on estimation basis

considering the local chocolate retail competitors (Coleman, Cotei and Farhat 2013). The sales

volume of the business is shown to increase which suggest that the management anticipates

growth which suggest that the product would be popular in the market.

The machinery and assets of the business is shown to have a useful life of 5 years and the

same is shown in the income statement which is prepared on estimation basis. The depreciation

and amortization expenses which is shown in the income statement is done on the basis of the

assumption which is undertaken by the owner of the business. In addition to this, the salary of

the employees who will be managing the stores of the business is also done on an estimation

basis. The labour costs and salary of the employees would be dependent on the number of

employees and support staff which is to be employed in the business (Wu et al. 2016). The

discount rate which is considered in the discounted cash flow computation on the interest rate

which is based on the interest rate on loans which is available from financial institutions and the

sane is considered to be 7%. In addition to this, the computation of Discounted cash flow also

considers that the sales of the business would grow in the initial three years and then there would

FINANCIAL MANAGEMENT

from the tenure of such rights and the quantity of order placed per consignment. In addition to

this, assumptions have been made regarding the exchange rate of currency. As the business is

importing chocolate products from Zurich and Switzerland, the business would have to pay such

expenses in foreign currency and therefore conversion of domestic currency must be done to

foreign currency. In breakeven analysis, the business needs to consider the prevailing conversion

rate and the same is considered to be 8.36 which is the conversion rate prevailing on the date

when the analysis is undertaken by the owners. The conversion rate can change and such needs

to be considered appropriately by Uncle Benjamin. In the estimation of the sales volume which

can be achieved by the business in terms of variable sales is also considered on estimation basis

considering the local chocolate retail competitors (Coleman, Cotei and Farhat 2013). The sales

volume of the business is shown to increase which suggest that the management anticipates

growth which suggest that the product would be popular in the market.

The machinery and assets of the business is shown to have a useful life of 5 years and the

same is shown in the income statement which is prepared on estimation basis. The depreciation

and amortization expenses which is shown in the income statement is done on the basis of the

assumption which is undertaken by the owner of the business. In addition to this, the salary of

the employees who will be managing the stores of the business is also done on an estimation

basis. The labour costs and salary of the employees would be dependent on the number of

employees and support staff which is to be employed in the business (Wu et al. 2016). The

discount rate which is considered in the discounted cash flow computation on the interest rate

which is based on the interest rate on loans which is available from financial institutions and the

sane is considered to be 7%. In addition to this, the computation of Discounted cash flow also

considers that the sales of the business would grow in the initial three years and then there would

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

FINANCIAL MANAGEMENT

a decline in sales. This is considered after evaluating the retail markets for chocolate gourmets in

Norway.

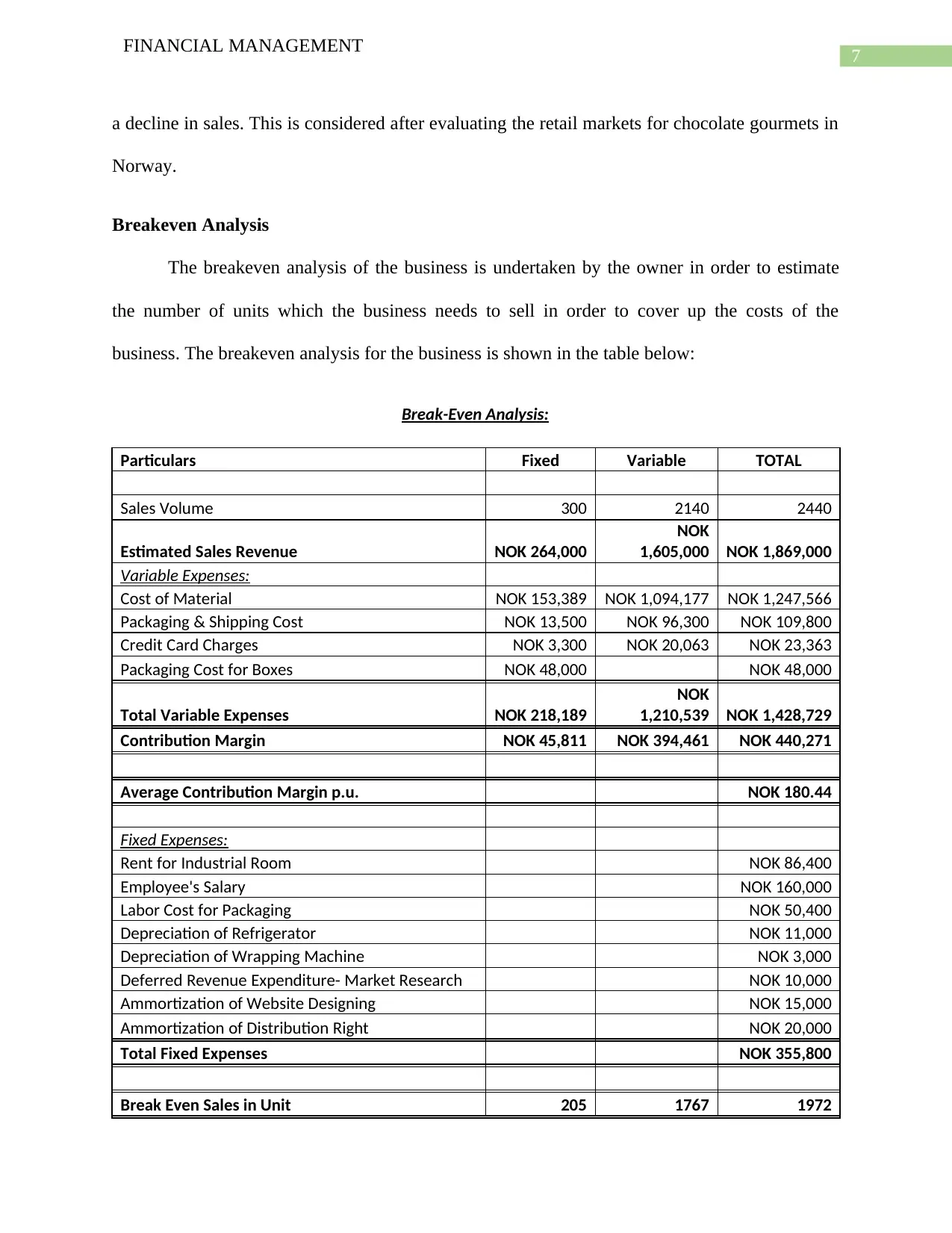

Breakeven Analysis

The breakeven analysis of the business is undertaken by the owner in order to estimate

the number of units which the business needs to sell in order to cover up the costs of the

business. The breakeven analysis for the business is shown in the table below:

Break-Even Analysis:

Particulars Fixed Variable TOTAL

Sales Volume 300 2140 2440

Estimated Sales Revenue NOK 264,000

NOK

1,605,000 NOK 1,869,000

Variable Expenses:

Cost of Material NOK 153,389 NOK 1,094,177 NOK 1,247,566

Packaging & Shipping Cost NOK 13,500 NOK 96,300 NOK 109,800

Credit Card Charges NOK 3,300 NOK 20,063 NOK 23,363

Packaging Cost for Boxes NOK 48,000 NOK 48,000

Total Variable Expenses NOK 218,189

NOK

1,210,539 NOK 1,428,729

Contribution Margin NOK 45,811 NOK 394,461 NOK 440,271

Average Contribution Margin p.u. NOK 180.44

Fixed Expenses:

Rent for Industrial Room NOK 86,400

Employee's Salary NOK 160,000

Labor Cost for Packaging NOK 50,400

Depreciation of Refrigerator NOK 11,000

Depreciation of Wrapping Machine NOK 3,000

Deferred Revenue Expenditure- Market Research NOK 10,000

Ammortization of Website Designing NOK 15,000

Ammortization of Distribution Right NOK 20,000

Total Fixed Expenses NOK 355,800

Break Even Sales in Unit 205 1767 1972

FINANCIAL MANAGEMENT

a decline in sales. This is considered after evaluating the retail markets for chocolate gourmets in

Norway.

Breakeven Analysis

The breakeven analysis of the business is undertaken by the owner in order to estimate

the number of units which the business needs to sell in order to cover up the costs of the

business. The breakeven analysis for the business is shown in the table below:

Break-Even Analysis:

Particulars Fixed Variable TOTAL

Sales Volume 300 2140 2440

Estimated Sales Revenue NOK 264,000

NOK

1,605,000 NOK 1,869,000

Variable Expenses:

Cost of Material NOK 153,389 NOK 1,094,177 NOK 1,247,566

Packaging & Shipping Cost NOK 13,500 NOK 96,300 NOK 109,800

Credit Card Charges NOK 3,300 NOK 20,063 NOK 23,363

Packaging Cost for Boxes NOK 48,000 NOK 48,000

Total Variable Expenses NOK 218,189

NOK

1,210,539 NOK 1,428,729

Contribution Margin NOK 45,811 NOK 394,461 NOK 440,271

Average Contribution Margin p.u. NOK 180.44

Fixed Expenses:

Rent for Industrial Room NOK 86,400

Employee's Salary NOK 160,000

Labor Cost for Packaging NOK 50,400

Depreciation of Refrigerator NOK 11,000

Depreciation of Wrapping Machine NOK 3,000

Deferred Revenue Expenditure- Market Research NOK 10,000

Ammortization of Website Designing NOK 15,000

Ammortization of Distribution Right NOK 20,000

Total Fixed Expenses NOK 355,800

Break Even Sales in Unit 205 1767 1972

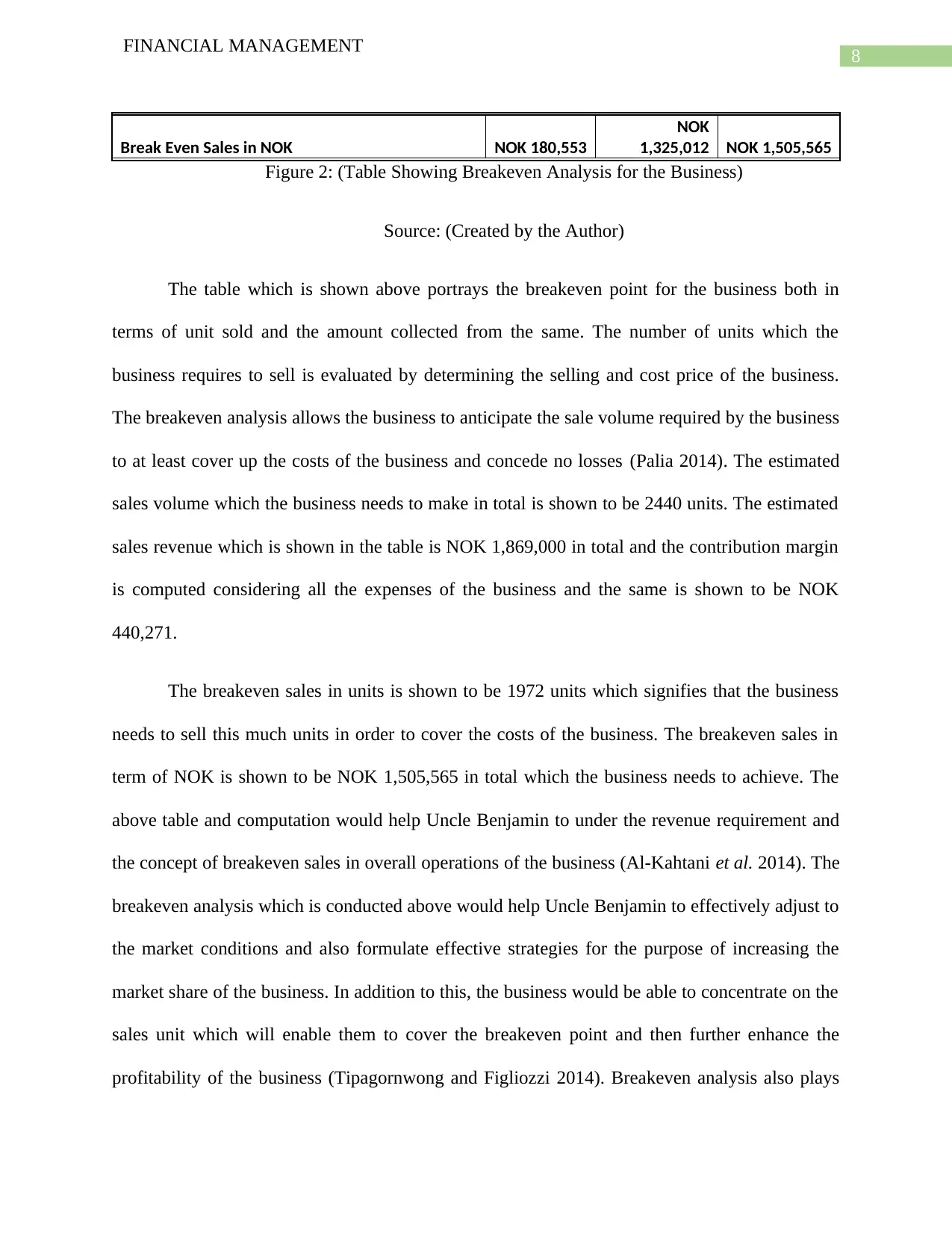

8

FINANCIAL MANAGEMENT

Break Even Sales in NOK NOK 180,553

NOK

1,325,012 NOK 1,505,565

Figure 2: (Table Showing Breakeven Analysis for the Business)

Source: (Created by the Author)

The table which is shown above portrays the breakeven point for the business both in

terms of unit sold and the amount collected from the same. The number of units which the

business requires to sell is evaluated by determining the selling and cost price of the business.

The breakeven analysis allows the business to anticipate the sale volume required by the business

to at least cover up the costs of the business and concede no losses (Palia 2014). The estimated

sales volume which the business needs to make in total is shown to be 2440 units. The estimated

sales revenue which is shown in the table is NOK 1,869,000 in total and the contribution margin

is computed considering all the expenses of the business and the same is shown to be NOK

440,271.

The breakeven sales in units is shown to be 1972 units which signifies that the business

needs to sell this much units in order to cover the costs of the business. The breakeven sales in

term of NOK is shown to be NOK 1,505,565 in total which the business needs to achieve. The

above table and computation would help Uncle Benjamin to under the revenue requirement and

the concept of breakeven sales in overall operations of the business (Al-Kahtani et al. 2014). The

breakeven analysis which is conducted above would help Uncle Benjamin to effectively adjust to

the market conditions and also formulate effective strategies for the purpose of increasing the

market share of the business. In addition to this, the business would be able to concentrate on the

sales unit which will enable them to cover the breakeven point and then further enhance the

profitability of the business (Tipagornwong and Figliozzi 2014). Breakeven analysis also plays

FINANCIAL MANAGEMENT

Break Even Sales in NOK NOK 180,553

NOK

1,325,012 NOK 1,505,565

Figure 2: (Table Showing Breakeven Analysis for the Business)

Source: (Created by the Author)

The table which is shown above portrays the breakeven point for the business both in

terms of unit sold and the amount collected from the same. The number of units which the

business requires to sell is evaluated by determining the selling and cost price of the business.

The breakeven analysis allows the business to anticipate the sale volume required by the business

to at least cover up the costs of the business and concede no losses (Palia 2014). The estimated

sales volume which the business needs to make in total is shown to be 2440 units. The estimated

sales revenue which is shown in the table is NOK 1,869,000 in total and the contribution margin

is computed considering all the expenses of the business and the same is shown to be NOK

440,271.

The breakeven sales in units is shown to be 1972 units which signifies that the business

needs to sell this much units in order to cover the costs of the business. The breakeven sales in

term of NOK is shown to be NOK 1,505,565 in total which the business needs to achieve. The

above table and computation would help Uncle Benjamin to under the revenue requirement and

the concept of breakeven sales in overall operations of the business (Al-Kahtani et al. 2014). The

breakeven analysis which is conducted above would help Uncle Benjamin to effectively adjust to

the market conditions and also formulate effective strategies for the purpose of increasing the

market share of the business. In addition to this, the business would be able to concentrate on the

sales unit which will enable them to cover the breakeven point and then further enhance the

profitability of the business (Tipagornwong and Figliozzi 2014). Breakeven analysis also plays

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

FINANCIAL MANAGEMENT

an important role in enhancing the market shares of the business and also determine the

appropriate number of units which is to be produced by the business. This will also help the

business in formulating an appropriate pricing strategy would help the business to become more

profitable in nature. In addition to this, the liquidity and growth perspective in the business

would help the owner to make future growth strategy and continuity for the same.

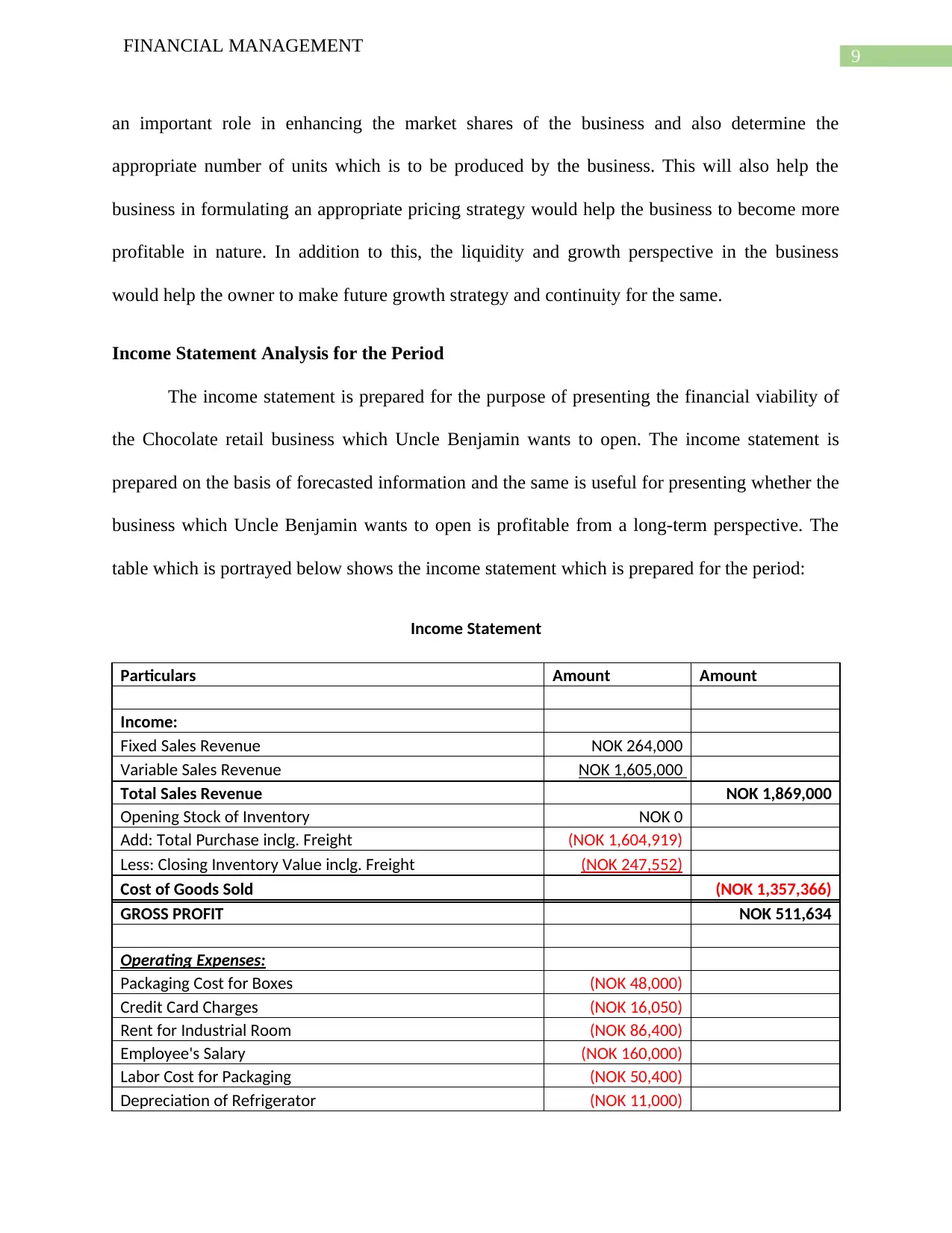

Income Statement Analysis for the Period

The income statement is prepared for the purpose of presenting the financial viability of

the Chocolate retail business which Uncle Benjamin wants to open. The income statement is

prepared on the basis of forecasted information and the same is useful for presenting whether the

business which Uncle Benjamin wants to open is profitable from a long-term perspective. The

table which is portrayed below shows the income statement which is prepared for the period:

Income Statement

Particulars Amount Amount

Income:

Fixed Sales Revenue NOK 264,000

Variable Sales Revenue NOK 1,605,000

Total Sales Revenue NOK 1,869,000

Opening Stock of Inventory NOK 0

Add: Total Purchase inclg. Freight (NOK 1,604,919)

Less: Closing Inventory Value inclg. Freight (NOK 247,552)

Cost of Goods Sold (NOK 1,357,366)

GROSS PROFIT NOK 511,634

Operating Expenses:

Packaging Cost for Boxes (NOK 48,000)

Credit Card Charges (NOK 16,050)

Rent for Industrial Room (NOK 86,400)

Employee's Salary (NOK 160,000)

Labor Cost for Packaging (NOK 50,400)

Depreciation of Refrigerator (NOK 11,000)

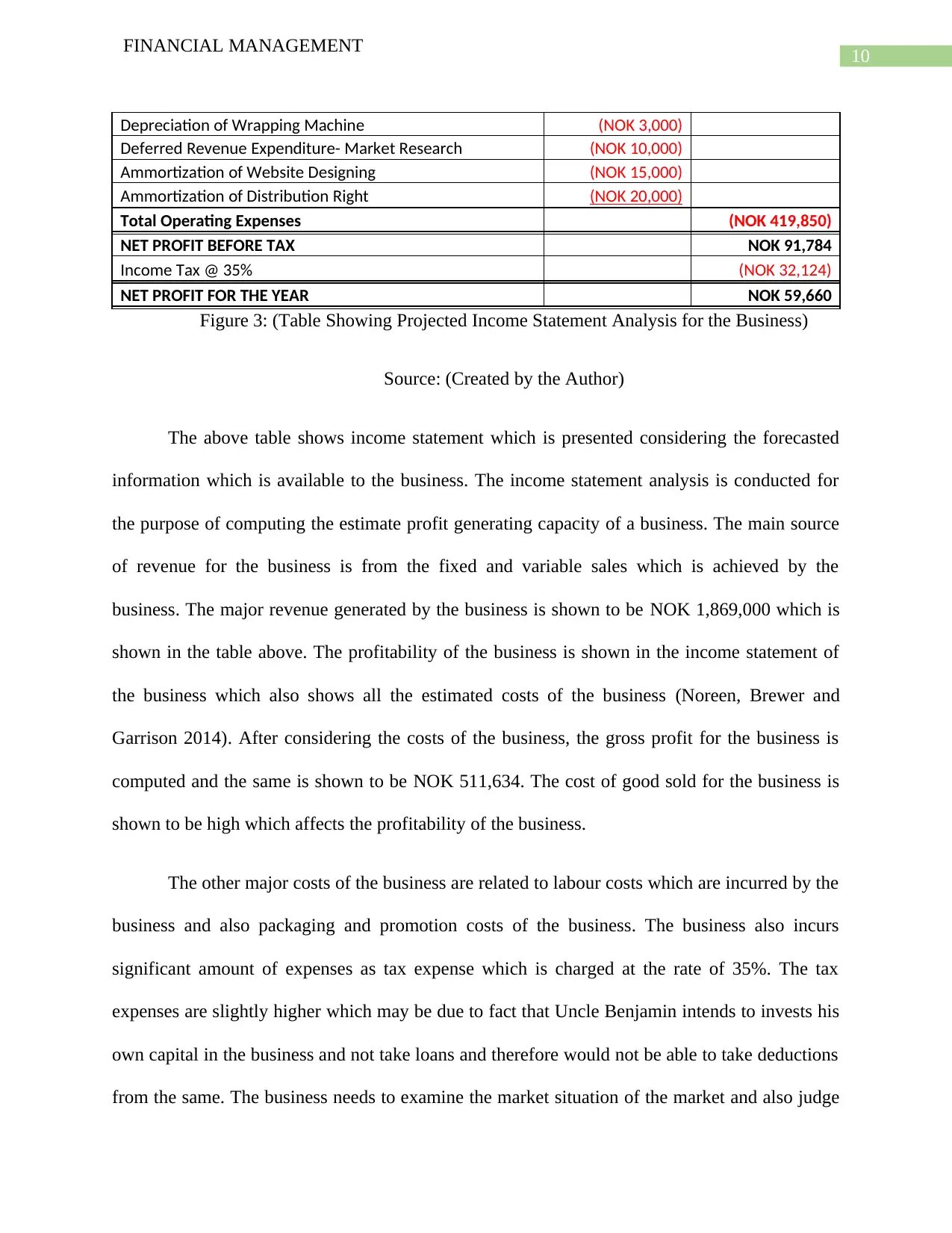

FINANCIAL MANAGEMENT

an important role in enhancing the market shares of the business and also determine the

appropriate number of units which is to be produced by the business. This will also help the

business in formulating an appropriate pricing strategy would help the business to become more

profitable in nature. In addition to this, the liquidity and growth perspective in the business

would help the owner to make future growth strategy and continuity for the same.

Income Statement Analysis for the Period

The income statement is prepared for the purpose of presenting the financial viability of

the Chocolate retail business which Uncle Benjamin wants to open. The income statement is

prepared on the basis of forecasted information and the same is useful for presenting whether the

business which Uncle Benjamin wants to open is profitable from a long-term perspective. The

table which is portrayed below shows the income statement which is prepared for the period:

Income Statement

Particulars Amount Amount

Income:

Fixed Sales Revenue NOK 264,000

Variable Sales Revenue NOK 1,605,000

Total Sales Revenue NOK 1,869,000

Opening Stock of Inventory NOK 0

Add: Total Purchase inclg. Freight (NOK 1,604,919)

Less: Closing Inventory Value inclg. Freight (NOK 247,552)

Cost of Goods Sold (NOK 1,357,366)

GROSS PROFIT NOK 511,634

Operating Expenses:

Packaging Cost for Boxes (NOK 48,000)

Credit Card Charges (NOK 16,050)

Rent for Industrial Room (NOK 86,400)

Employee's Salary (NOK 160,000)

Labor Cost for Packaging (NOK 50,400)

Depreciation of Refrigerator (NOK 11,000)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

FINANCIAL MANAGEMENT

Depreciation of Wrapping Machine (NOK 3,000)

Deferred Revenue Expenditure- Market Research (NOK 10,000)

Ammortization of Website Designing (NOK 15,000)

Ammortization of Distribution Right (NOK 20,000)

Total Operating Expenses (NOK 419,850)

NET PROFIT BEFORE TAX NOK 91,784

Income Tax @ 35% (NOK 32,124)

NET PROFIT FOR THE YEAR NOK 59,660

Figure 3: (Table Showing Projected Income Statement Analysis for the Business)

Source: (Created by the Author)

The above table shows income statement which is presented considering the forecasted

information which is available to the business. The income statement analysis is conducted for

the purpose of computing the estimate profit generating capacity of a business. The main source

of revenue for the business is from the fixed and variable sales which is achieved by the

business. The major revenue generated by the business is shown to be NOK 1,869,000 which is

shown in the table above. The profitability of the business is shown in the income statement of

the business which also shows all the estimated costs of the business (Noreen, Brewer and

Garrison 2014). After considering the costs of the business, the gross profit for the business is

computed and the same is shown to be NOK 511,634. The cost of good sold for the business is

shown to be high which affects the profitability of the business.

The other major costs of the business are related to labour costs which are incurred by the

business and also packaging and promotion costs of the business. The business also incurs

significant amount of expenses as tax expense which is charged at the rate of 35%. The tax

expenses are slightly higher which may be due to fact that Uncle Benjamin intends to invests his

own capital in the business and not take loans and therefore would not be able to take deductions

from the same. The business needs to examine the market situation of the market and also judge

FINANCIAL MANAGEMENT

Depreciation of Wrapping Machine (NOK 3,000)

Deferred Revenue Expenditure- Market Research (NOK 10,000)

Ammortization of Website Designing (NOK 15,000)

Ammortization of Distribution Right (NOK 20,000)

Total Operating Expenses (NOK 419,850)

NET PROFIT BEFORE TAX NOK 91,784

Income Tax @ 35% (NOK 32,124)

NET PROFIT FOR THE YEAR NOK 59,660

Figure 3: (Table Showing Projected Income Statement Analysis for the Business)

Source: (Created by the Author)

The above table shows income statement which is presented considering the forecasted

information which is available to the business. The income statement analysis is conducted for

the purpose of computing the estimate profit generating capacity of a business. The main source

of revenue for the business is from the fixed and variable sales which is achieved by the

business. The major revenue generated by the business is shown to be NOK 1,869,000 which is

shown in the table above. The profitability of the business is shown in the income statement of

the business which also shows all the estimated costs of the business (Noreen, Brewer and

Garrison 2014). After considering the costs of the business, the gross profit for the business is

computed and the same is shown to be NOK 511,634. The cost of good sold for the business is

shown to be high which affects the profitability of the business.

The other major costs of the business are related to labour costs which are incurred by the

business and also packaging and promotion costs of the business. The business also incurs

significant amount of expenses as tax expense which is charged at the rate of 35%. The tax

expenses are slightly higher which may be due to fact that Uncle Benjamin intends to invests his

own capital in the business and not take loans and therefore would not be able to take deductions

from the same. The business needs to examine the market situation of the market and also judge

11

FINANCIAL MANAGEMENT

the preference pattern of the consumers in order to understand their taste and preferences. Uncle

Benjamin also needs to consider the market which might be economic crisis. The profit

generating ability of the business depends on the investment made by the business.

The income statement allows Uncle Benjamin to estimate the profit generating capacity

of the venture. However, before estimating the profit, the owner needs to invest significantly on

promoting the product with the help of an appropriate advertisement program (Hofmann and

Lampe 2013). However, in order to achieve better results the costs of production needs to be

reduced so that the business can offer better price to the customers. This will be further

enhancing the demand for the product in the market and also contribute to profitability of the

business.

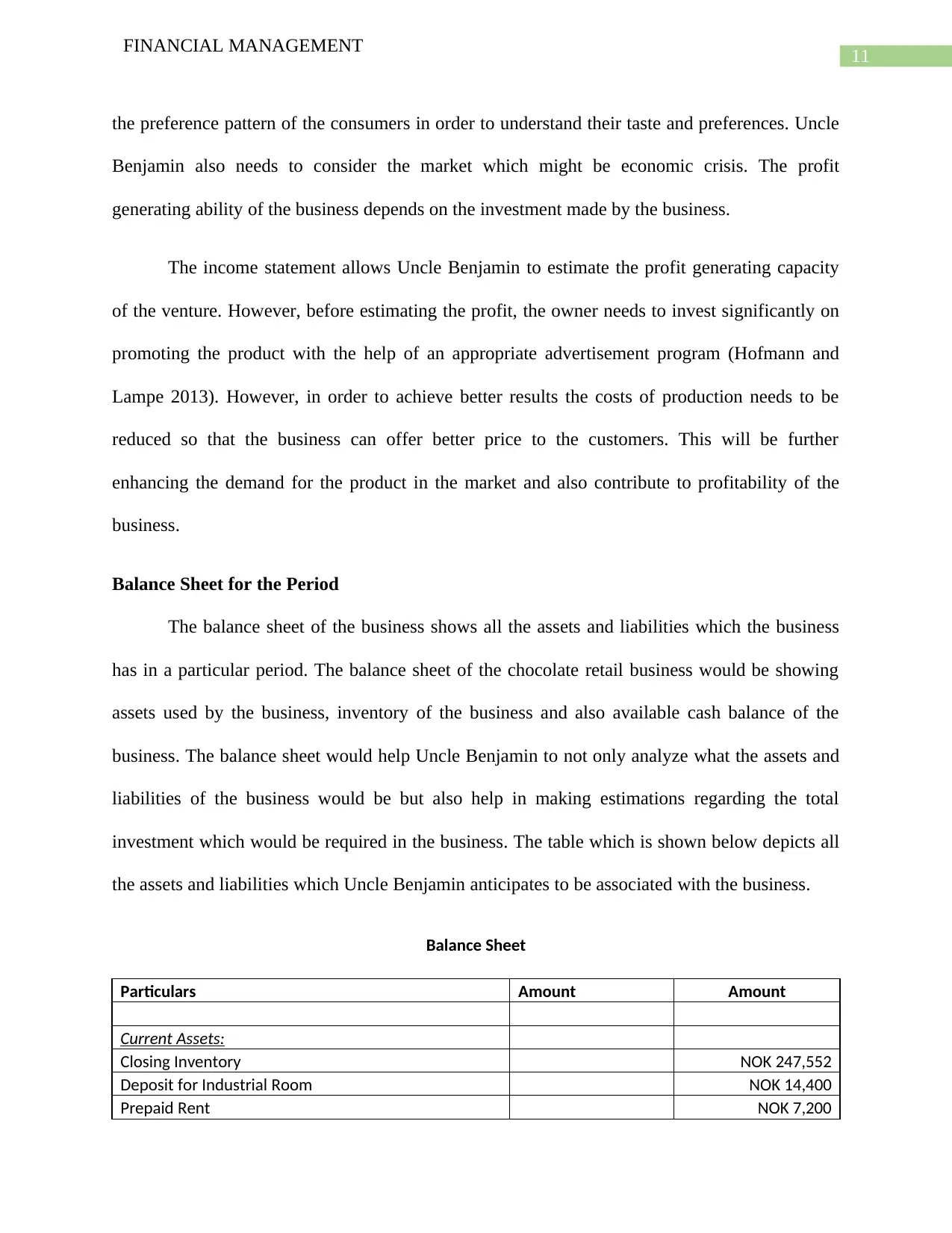

Balance Sheet for the Period

The balance sheet of the business shows all the assets and liabilities which the business

has in a particular period. The balance sheet of the chocolate retail business would be showing

assets used by the business, inventory of the business and also available cash balance of the

business. The balance sheet would help Uncle Benjamin to not only analyze what the assets and

liabilities of the business would be but also help in making estimations regarding the total

investment which would be required in the business. The table which is shown below depicts all

the assets and liabilities which Uncle Benjamin anticipates to be associated with the business.

Balance Sheet

Particulars Amount Amount

Current Assets:

Closing Inventory NOK 247,552

Deposit for Industrial Room NOK 14,400

Prepaid Rent NOK 7,200

FINANCIAL MANAGEMENT

the preference pattern of the consumers in order to understand their taste and preferences. Uncle

Benjamin also needs to consider the market which might be economic crisis. The profit

generating ability of the business depends on the investment made by the business.

The income statement allows Uncle Benjamin to estimate the profit generating capacity

of the venture. However, before estimating the profit, the owner needs to invest significantly on

promoting the product with the help of an appropriate advertisement program (Hofmann and

Lampe 2013). However, in order to achieve better results the costs of production needs to be

reduced so that the business can offer better price to the customers. This will be further

enhancing the demand for the product in the market and also contribute to profitability of the

business.

Balance Sheet for the Period

The balance sheet of the business shows all the assets and liabilities which the business

has in a particular period. The balance sheet of the chocolate retail business would be showing

assets used by the business, inventory of the business and also available cash balance of the

business. The balance sheet would help Uncle Benjamin to not only analyze what the assets and

liabilities of the business would be but also help in making estimations regarding the total

investment which would be required in the business. The table which is shown below depicts all

the assets and liabilities which Uncle Benjamin anticipates to be associated with the business.

Balance Sheet

Particulars Amount Amount

Current Assets:

Closing Inventory NOK 247,552

Deposit for Industrial Room NOK 14,400

Prepaid Rent NOK 7,200

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 30

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.