APC308 Financial Management Project: Valuation & Investment

VerifiedAdded on 2023/01/12

|13

|3071

|61

Project

AI Summary

This project addresses two key problems in financial management, focusing on merger & takeover scenarios and investment appraisal techniques. The solution begins with an introduction to financial management, highlighting its role in coordinating and regulating financial operations. Question 2 delves into valuation techniques, specifically analyzing Price Earnings Ratio (P/E), Dividend Valuation Model (DDM), and Discounted Cash Flow (DCF) methods. The analysis includes the advantages and disadvantages of each technique, with a recommendation to use the P/E ratio for share valuation. Question 3 focuses on investment appraisal, calculating and interpreting Payback Period, Accounting Rate of Return (ARR), Net Present Value (NPV), and Internal Rate of Return (IRR) to assess the viability of a machine investment. The project concludes with recommendations based on the financial analysis, suggesting the investment is beneficial due to a positive NPV and a good IRR.

Financial Management

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2

INTRODUCTION

Financial management includes the scheduling, coordination, monitoring and regulation of

financial operations, such as the acquisition and use of the company's funds. It implies adapting

the general management principles to the company's financial capital (Hoque, 2017). In this

assessment, we have to address two problems and it is based on merger & takeover and

investment appraisal techniques. There are several functions which are used for different purpose

such as estimation of capital requirement, capital composition, source of funds, investment of

funds etc.

MAIN BODY

Question 2

a. Price Earnings Ratio

Price earnings ratio: It is the connection between the share price of a company and the

earnings per share (EPS). It is a common ratio which gives shareholders a better understanding

of the firm's value. The P / E ratio reflects market expectations and is the price that is expected to

pay per amount of current earnings.

Aztec PE ratio = Share price / EPS

= 3.89 / 0.21 = 18.52

Trojan Plc = 40.4 / 147

= 27.48

Share price of Trojan Plc = 18.52 * 27.48

= 5.08

Total market value = 147 * 5.08

= 746.76

Here it is assumed that the market expects Aztec to produce a return on Trojan's assets on its

own assets comparable to that on.

Dividend valuation model: Dividend discount model (DDM) is a way of valuing an

organization's stock price based on the assumption that its stock is worth all the effort of all its

future dividend payout, compared to its value (Hashim and Piatti-Fünfkirchen, 2018). To put it

another way, securities are used to calculate based on the capital cost of the future distributions.

To calculate of dividend require the dividend model values for both g and r such as:

3

Financial management includes the scheduling, coordination, monitoring and regulation of

financial operations, such as the acquisition and use of the company's funds. It implies adapting

the general management principles to the company's financial capital (Hoque, 2017). In this

assessment, we have to address two problems and it is based on merger & takeover and

investment appraisal techniques. There are several functions which are used for different purpose

such as estimation of capital requirement, capital composition, source of funds, investment of

funds etc.

MAIN BODY

Question 2

a. Price Earnings Ratio

Price earnings ratio: It is the connection between the share price of a company and the

earnings per share (EPS). It is a common ratio which gives shareholders a better understanding

of the firm's value. The P / E ratio reflects market expectations and is the price that is expected to

pay per amount of current earnings.

Aztec PE ratio = Share price / EPS

= 3.89 / 0.21 = 18.52

Trojan Plc = 40.4 / 147

= 27.48

Share price of Trojan Plc = 18.52 * 27.48

= 5.08

Total market value = 147 * 5.08

= 746.76

Here it is assumed that the market expects Aztec to produce a return on Trojan's assets on its

own assets comparable to that on.

Dividend valuation model: Dividend discount model (DDM) is a way of valuing an

organization's stock price based on the assumption that its stock is worth all the effort of all its

future dividend payout, compared to its value (Hashim and Piatti-Fünfkirchen, 2018). To put it

another way, securities are used to calculate based on the capital cost of the future distributions.

To calculate of dividend require the dividend model values for both g and r such as:

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

G = (13 / 10) = 1.14 %

Alternatively

g = 4 √ (13 / 10) = 1.14%

The cost of equity using CAPM

Ke = 5 + (1.10 * (11 – 5)) = 11.60%

Po = 0.116 – 0.114 = 0.002

Total market value = 147 * 0.002 = 294m

Discount cash flow method Discounted cash flow (DCF) is a valuation instrument used to

calculate the value of an investment based on its expected cash flows. The DCF evaluation

attempts to quantify the worth of modern spending based on forecasts of how much income it

would produce in the present. This applies both to monetary donations from creditors as well as

to company owners wanting to make changes to their companies, such as purchasing new

appliances.

Discount cash flow method by using WACC of Aztec

Present value of earnings = 40.4 * 1.02 / (0.09 – 0.02)

= 588.68

Present value of assets sale = 21 million / 1.09

= 19.27

Present value of synergy = 5 / 0.09

= 55.56

Total present value of Trojan Plc = 588.68 + 19.27 + 55.56

= 663.51

b. Critically discuss the problems associated with valuation techniques and recommend the

board of Aztec to use

It is critically analyzed that to solving these problems required to analysis of different

advantage and disadvantages of these techniques such as:

Price earnings ratio

Advantage: P / E analyses a future growth prospects by taking into account the firm's

circumstances and contrasting them to past results. This also dictates what the investors are

created for. PE ratios help shareholders assess the potential for growth before investing in the

business. The ratios indicate businesses that can be impacted by drastic price change. High PE

4

Alternatively

g = 4 √ (13 / 10) = 1.14%

The cost of equity using CAPM

Ke = 5 + (1.10 * (11 – 5)) = 11.60%

Po = 0.116 – 0.114 = 0.002

Total market value = 147 * 0.002 = 294m

Discount cash flow method Discounted cash flow (DCF) is a valuation instrument used to

calculate the value of an investment based on its expected cash flows. The DCF evaluation

attempts to quantify the worth of modern spending based on forecasts of how much income it

would produce in the present. This applies both to monetary donations from creditors as well as

to company owners wanting to make changes to their companies, such as purchasing new

appliances.

Discount cash flow method by using WACC of Aztec

Present value of earnings = 40.4 * 1.02 / (0.09 – 0.02)

= 588.68

Present value of assets sale = 21 million / 1.09

= 19.27

Present value of synergy = 5 / 0.09

= 55.56

Total present value of Trojan Plc = 588.68 + 19.27 + 55.56

= 663.51

b. Critically discuss the problems associated with valuation techniques and recommend the

board of Aztec to use

It is critically analyzed that to solving these problems required to analysis of different

advantage and disadvantages of these techniques such as:

Price earnings ratio

Advantage: P / E analyses a future growth prospects by taking into account the firm's

circumstances and contrasting them to past results. This also dictates what the investors are

created for. PE ratios help shareholders assess the potential for growth before investing in the

business. The ratios indicate businesses that can be impacted by drastic price change. High PE

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

contributes to the company's selloff while low PE shows the company's continued production.

Enable shareholders to know how much they want to pay for the stock in exchange for every

dollar. We may rely on this knowledge to classify undervalued inventories.

Disadvantages: Price-earnings may not take into account debt / financial arrangement

when measuring the financial reports. Specific accounting practices hinder PE similarities

between different businesses and various countries (Mitchell and Calabrese, 2019. Such

measures include the approaches used for depreciation, amortization, and taxation. Competitive

nature of shares makes it hard to know what price earnings we will sell to render P / E in fact

subjective. The speeding up or stock buy-backs will raise the company's profits but this can lead

to higher risk cost for doing it. The loss-making businesses cannot use the PE ratio because it

cannot assess losses at the early stages of business growth.

Discounted cash flow model

Advantage: The discounted cash flow model has a major benefit as it decreases

expenditure to a single figure. When the net present value is favourable, it is assumed the

investment will be a source of profit; if it is unfavourable, the investment will be a sucker. This

helps decisions about individual investments to be up-to-down (Dwiastanti, 2017). Additionally,

the approach helps you to make choices between substantially different investments. Investment

decisions are the most precise and reliable tool. Assuming that the measurement calculations are

somewhat correct, no other approach does the job of determining which investments yield

optimum value.

Disadvantages: DCF's most significant limitation is the fact that it needs a number of

assumptions to be made. Cash flows in the near future may depend on different factors, such as

demand for the economy, business dynamics, unexpected problems and much more. Measuring

unrealistic potential cash flows may lead to making decisions about an investment that does not

pay off later, destroying earnings. Earning money flows too low, that can bring in lost chances of

making an investment look high priced. Deciding on a rate of return for your version can be a

gamble, and your version may need to be adequately predicted for compensation.

Dividend valuation model:

Advantage: The dividend valuation model will not allow a wealth creation assumption

for development. The rate of dividend growth for the stocks being measured cannot be greater

than the rate of return, or else the equation could not work. It means they are using this model to

5

Enable shareholders to know how much they want to pay for the stock in exchange for every

dollar. We may rely on this knowledge to classify undervalued inventories.

Disadvantages: Price-earnings may not take into account debt / financial arrangement

when measuring the financial reports. Specific accounting practices hinder PE similarities

between different businesses and various countries (Mitchell and Calabrese, 2019. Such

measures include the approaches used for depreciation, amortization, and taxation. Competitive

nature of shares makes it hard to know what price earnings we will sell to render P / E in fact

subjective. The speeding up or stock buy-backs will raise the company's profits but this can lead

to higher risk cost for doing it. The loss-making businesses cannot use the PE ratio because it

cannot assess losses at the early stages of business growth.

Discounted cash flow model

Advantage: The discounted cash flow model has a major benefit as it decreases

expenditure to a single figure. When the net present value is favourable, it is assumed the

investment will be a source of profit; if it is unfavourable, the investment will be a sucker. This

helps decisions about individual investments to be up-to-down (Dwiastanti, 2017). Additionally,

the approach helps you to make choices between substantially different investments. Investment

decisions are the most precise and reliable tool. Assuming that the measurement calculations are

somewhat correct, no other approach does the job of determining which investments yield

optimum value.

Disadvantages: DCF's most significant limitation is the fact that it needs a number of

assumptions to be made. Cash flows in the near future may depend on different factors, such as

demand for the economy, business dynamics, unexpected problems and much more. Measuring

unrealistic potential cash flows may lead to making decisions about an investment that does not

pay off later, destroying earnings. Earning money flows too low, that can bring in lost chances of

making an investment look high priced. Deciding on a rate of return for your version can be a

gamble, and your version may need to be adequately predicted for compensation.

Dividend valuation model:

Advantage: The dividend valuation model will not allow a wealth creation assumption

for development. The rate of dividend growth for the stocks being measured cannot be greater

than the rate of return, or else the equation could not work. It means they are using this model to

5

forecast what potential dividends will be, depending on what appears to be the present dividend.

While using this valuation model, choosing a way to invest is simpler, because you will be able

to retain the investment value) (Siminica, Motoi and Dumitru, 2017). At the same time, you can

gain income from the dividends you receive, which helps you to increase your portfolio's total

value, particularly if you've invested in several dividend stocks from a variety of industries.

Disadvantages: By comparing small-cap shares to large-cap securities, it is the smaller

companies that have done better across long periods of time. Many small companies aren't in a

position to afford a dividend, which ensures that their worth cannot be calculated using this

valuation model. This can be used on the dividend paid stocks. If shareholders were only focused

on this particular model, they could miss a number of chances to create value to their portfolio.

There are a number of variables that can affect a stock's price over time. Consumer satisfaction,

brand loyalty and even the possession of intangible assets all have the ability to improve the

company's worth. Unless the growth rate of the dividend is constant and established, those non-

dividend variables will potentially affect the company's value. That means the valuation

approach cannot yield desired results, even when measured correctly.

From the above analysis, it is recommended that company should follow P/E ratio for the

valuation of their shares. It helps the management to make their strategic decisions in order to

enhance organizational productivity or profitability.

Question 3

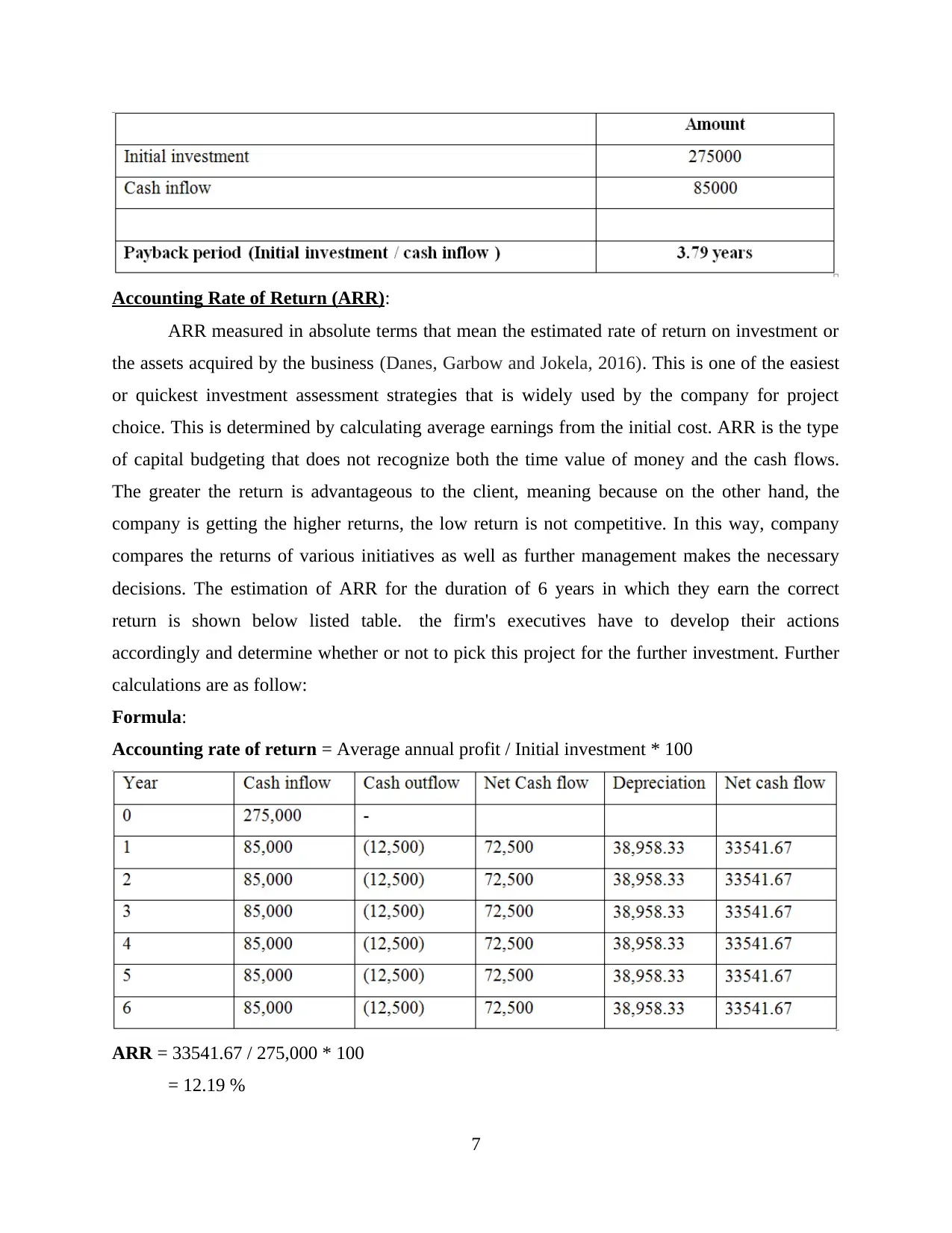

Payback period:

It is the capital budgeting approach that is used to determine further expenditure and to

enable the client to understand or select the best choice. Payback period is the duration during

which the company is able to retrieve the amount paid (Skimmyhorn, 2016). Low payback

period is advantageous to the company because it helps to restore initial investment and also to

start making returns on it. With the guidance of the company's inveterate assessment strategy

managers who can make informed decisions about potential investments. Measuring the overall

project risk is very critical for the organisations, so managers choose the project that involves

lower risk compared with other projects. Calculation of payback period for the machine is as

follow:

Formula:

Payback period = Initial investment / cash inflow

6

While using this valuation model, choosing a way to invest is simpler, because you will be able

to retain the investment value) (Siminica, Motoi and Dumitru, 2017). At the same time, you can

gain income from the dividends you receive, which helps you to increase your portfolio's total

value, particularly if you've invested in several dividend stocks from a variety of industries.

Disadvantages: By comparing small-cap shares to large-cap securities, it is the smaller

companies that have done better across long periods of time. Many small companies aren't in a

position to afford a dividend, which ensures that their worth cannot be calculated using this

valuation model. This can be used on the dividend paid stocks. If shareholders were only focused

on this particular model, they could miss a number of chances to create value to their portfolio.

There are a number of variables that can affect a stock's price over time. Consumer satisfaction,

brand loyalty and even the possession of intangible assets all have the ability to improve the

company's worth. Unless the growth rate of the dividend is constant and established, those non-

dividend variables will potentially affect the company's value. That means the valuation

approach cannot yield desired results, even when measured correctly.

From the above analysis, it is recommended that company should follow P/E ratio for the

valuation of their shares. It helps the management to make their strategic decisions in order to

enhance organizational productivity or profitability.

Question 3

Payback period:

It is the capital budgeting approach that is used to determine further expenditure and to

enable the client to understand or select the best choice. Payback period is the duration during

which the company is able to retrieve the amount paid (Skimmyhorn, 2016). Low payback

period is advantageous to the company because it helps to restore initial investment and also to

start making returns on it. With the guidance of the company's inveterate assessment strategy

managers who can make informed decisions about potential investments. Measuring the overall

project risk is very critical for the organisations, so managers choose the project that involves

lower risk compared with other projects. Calculation of payback period for the machine is as

follow:

Formula:

Payback period = Initial investment / cash inflow

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Accounting Rate of Return (ARR):

ARR measured in absolute terms that mean the estimated rate of return on investment or

the assets acquired by the business (Danes, Garbow and Jokela, 2016). This is one of the easiest

or quickest investment assessment strategies that is widely used by the company for project

choice. This is determined by calculating average earnings from the initial cost. ARR is the type

of capital budgeting that does not recognize both the time value of money and the cash flows.

The greater the return is advantageous to the client, meaning because on the other hand, the

company is getting the higher returns, the low return is not competitive. In this way, company

compares the returns of various initiatives as well as further management makes the necessary

decisions. The estimation of ARR for the duration of 6 years in which they earn the correct

return is shown below listed table. the firm's executives have to develop their actions

accordingly and determine whether or not to pick this project for the further investment. Further

calculations are as follow:

Formula:

Accounting rate of return = Average annual profit / Initial investment * 100

ARR = 33541.67 / 275,000 * 100

= 12.19 %

7

ARR measured in absolute terms that mean the estimated rate of return on investment or

the assets acquired by the business (Danes, Garbow and Jokela, 2016). This is one of the easiest

or quickest investment assessment strategies that is widely used by the company for project

choice. This is determined by calculating average earnings from the initial cost. ARR is the type

of capital budgeting that does not recognize both the time value of money and the cash flows.

The greater the return is advantageous to the client, meaning because on the other hand, the

company is getting the higher returns, the low return is not competitive. In this way, company

compares the returns of various initiatives as well as further management makes the necessary

decisions. The estimation of ARR for the duration of 6 years in which they earn the correct

return is shown below listed table. the firm's executives have to develop their actions

accordingly and determine whether or not to pick this project for the further investment. Further

calculations are as follow:

Formula:

Accounting rate of return = Average annual profit / Initial investment * 100

ARR = 33541.67 / 275,000 * 100

= 12.19 %

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

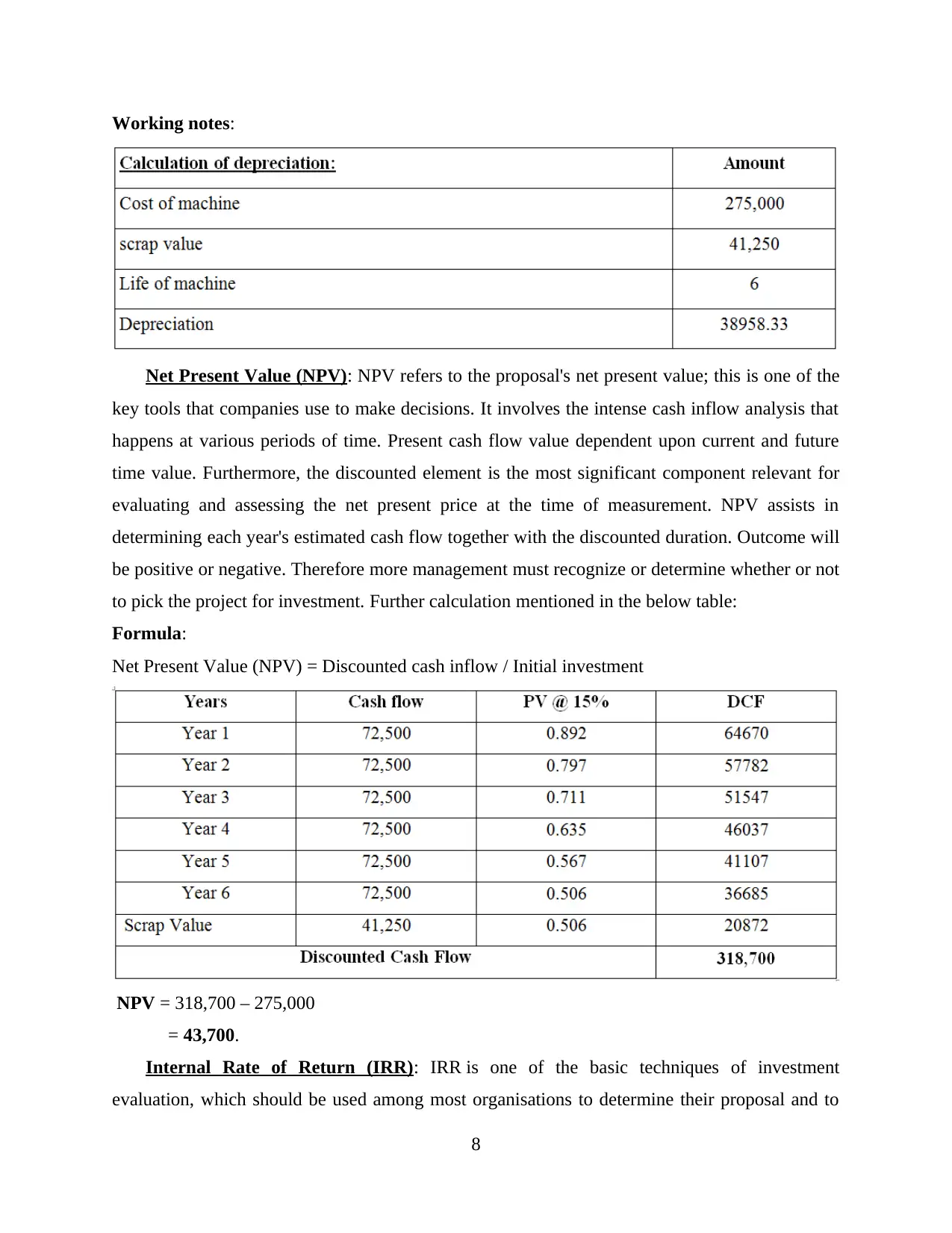

Working notes:

Net Present Value (NPV): NPV refers to the proposal's net present value; this is one of the

key tools that companies use to make decisions. It involves the intense cash inflow analysis that

happens at various periods of time. Present cash flow value dependent upon current and future

time value. Furthermore, the discounted element is the most significant component relevant for

evaluating and assessing the net present price at the time of measurement. NPV assists in

determining each year's estimated cash flow together with the discounted duration. Outcome will

be positive or negative. Therefore more management must recognize or determine whether or not

to pick the project for investment. Further calculation mentioned in the below table:

Formula:

Net Present Value (NPV) = Discounted cash inflow / Initial investment

NPV = 318,700 – 275,000

= 43,700.

Internal Rate of Return (IRR): IRR is one of the basic techniques of investment

evaluation, which should be used among most organisations to determine their proposal and to

8

Net Present Value (NPV): NPV refers to the proposal's net present value; this is one of the

key tools that companies use to make decisions. It involves the intense cash inflow analysis that

happens at various periods of time. Present cash flow value dependent upon current and future

time value. Furthermore, the discounted element is the most significant component relevant for

evaluating and assessing the net present price at the time of measurement. NPV assists in

determining each year's estimated cash flow together with the discounted duration. Outcome will

be positive or negative. Therefore more management must recognize or determine whether or not

to pick the project for investment. Further calculation mentioned in the below table:

Formula:

Net Present Value (NPV) = Discounted cash inflow / Initial investment

NPV = 318,700 – 275,000

= 43,700.

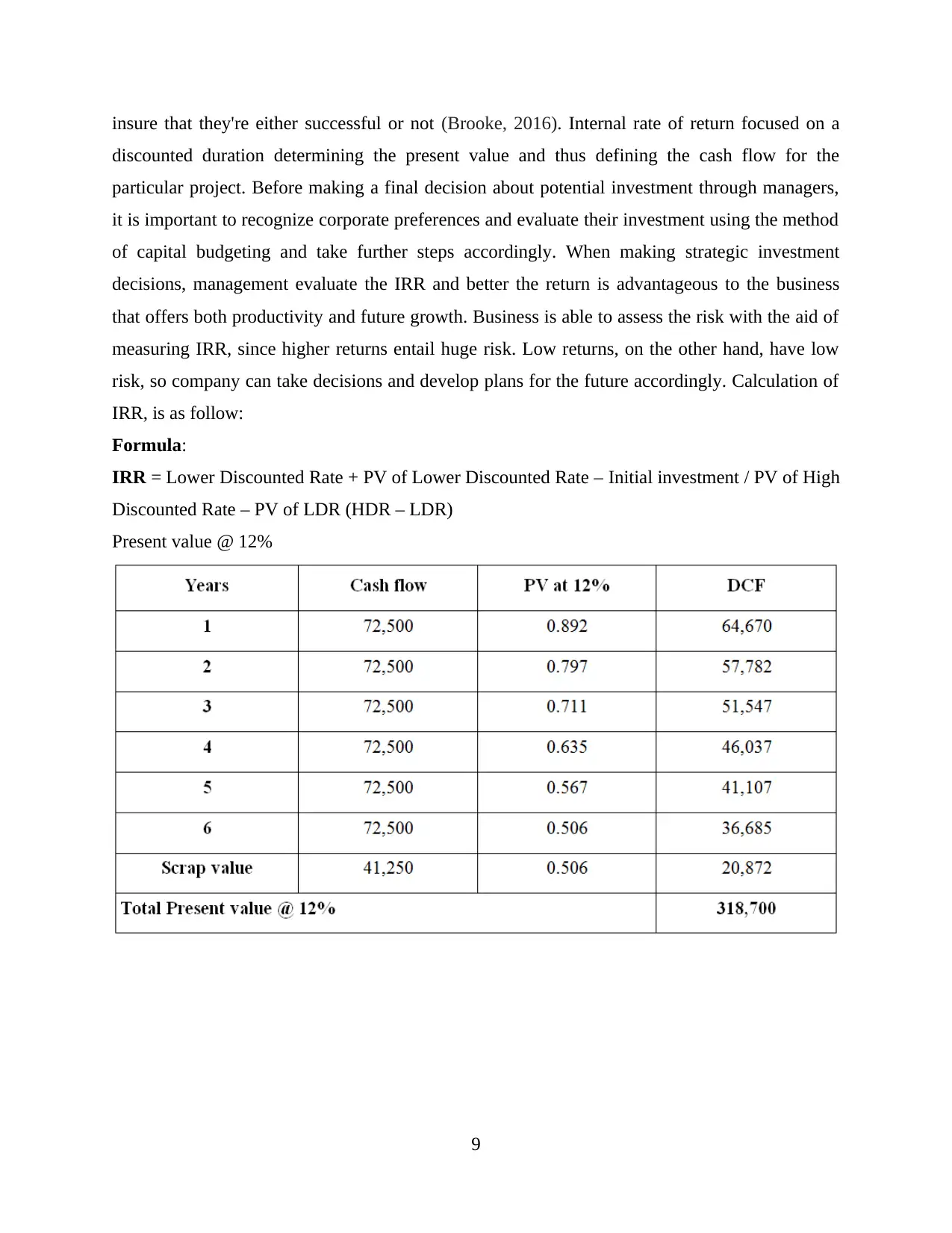

Internal Rate of Return (IRR): IRR is one of the basic techniques of investment

evaluation, which should be used among most organisations to determine their proposal and to

8

insure that they're either successful or not (Brooke, 2016). Internal rate of return focused on a

discounted duration determining the present value and thus defining the cash flow for the

particular project. Before making a final decision about potential investment through managers,

it is important to recognize corporate preferences and evaluate their investment using the method

of capital budgeting and take further steps accordingly. When making strategic investment

decisions, management evaluate the IRR and better the return is advantageous to the business

that offers both productivity and future growth. Business is able to assess the risk with the aid of

measuring IRR, since higher returns entail huge risk. Low returns, on the other hand, have low

risk, so company can take decisions and develop plans for the future accordingly. Calculation of

IRR, is as follow:

Formula:

IRR = Lower Discounted Rate + PV of Lower Discounted Rate – Initial investment / PV of High

Discounted Rate – PV of LDR (HDR – LDR)

Present value @ 12%

9

discounted duration determining the present value and thus defining the cash flow for the

particular project. Before making a final decision about potential investment through managers,

it is important to recognize corporate preferences and evaluate their investment using the method

of capital budgeting and take further steps accordingly. When making strategic investment

decisions, management evaluate the IRR and better the return is advantageous to the business

that offers both productivity and future growth. Business is able to assess the risk with the aid of

measuring IRR, since higher returns entail huge risk. Low returns, on the other hand, have low

risk, so company can take decisions and develop plans for the future accordingly. Calculation of

IRR, is as follow:

Formula:

IRR = Lower Discounted Rate + PV of Lower Discounted Rate – Initial investment / PV of High

Discounted Rate – PV of LDR (HDR – LDR)

Present value @ 12%

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

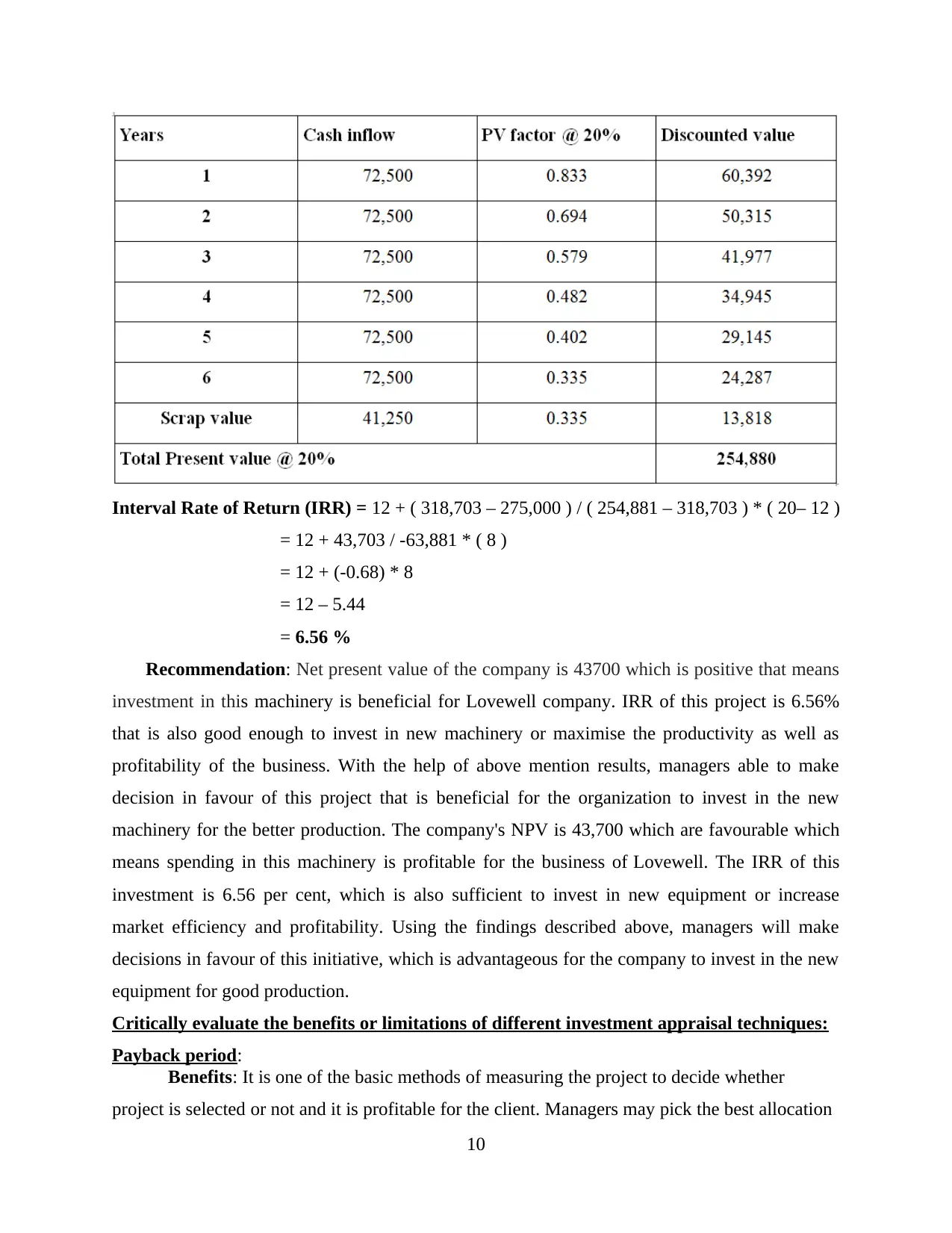

Interval Rate of Return (IRR) = 12 + ( 318,703 – 275,000 ) / ( 254,881 – 318,703 ) * ( 20– 12 )

= 12 + 43,703 / -63,881 * ( 8 )

= 12 + (-0.68) * 8

= 12 – 5.44

= 6.56 %

Recommendation: Net present value of the company is 43700 which is positive that means

investment in this machinery is beneficial for Lovewell company. IRR of this project is 6.56%

that is also good enough to invest in new machinery or maximise the productivity as well as

profitability of the business. With the help of above mention results, managers able to make

decision in favour of this project that is beneficial for the organization to invest in the new

machinery for the better production. The company's NPV is 43,700 which are favourable which

means spending in this machinery is profitable for the business of Lovewell. The IRR of this

investment is 6.56 per cent, which is also sufficient to invest in new equipment or increase

market efficiency and profitability. Using the findings described above, managers will make

decisions in favour of this initiative, which is advantageous for the company to invest in the new

equipment for good production.

Critically evaluate the benefits or limitations of different investment appraisal techniques:

Payback period:

Benefits: It is one of the basic methods of measuring the project to decide whether

project is selected or not and it is profitable for the client. Managers may pick the best allocation

10

= 12 + 43,703 / -63,881 * ( 8 )

= 12 + (-0.68) * 8

= 12 – 5.44

= 6.56 %

Recommendation: Net present value of the company is 43700 which is positive that means

investment in this machinery is beneficial for Lovewell company. IRR of this project is 6.56%

that is also good enough to invest in new machinery or maximise the productivity as well as

profitability of the business. With the help of above mention results, managers able to make

decision in favour of this project that is beneficial for the organization to invest in the new

machinery for the better production. The company's NPV is 43,700 which are favourable which

means spending in this machinery is profitable for the business of Lovewell. The IRR of this

investment is 6.56 per cent, which is also sufficient to invest in new equipment or increase

market efficiency and profitability. Using the findings described above, managers will make

decisions in favour of this initiative, which is advantageous for the company to invest in the new

equipment for good production.

Critically evaluate the benefits or limitations of different investment appraisal techniques:

Payback period:

Benefits: It is one of the basic methods of measuring the project to decide whether

project is selected or not and it is profitable for the client. Managers may pick the best allocation

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

to invest, with the aid of this tool. Such as a short recovery time would be selected because it

helps the business recover more quickly from the original investment.

Limitations: Managers should ignore unfavourable NPV while making important

decisions, as it won't be beneficial at all. This approach does not recognize time value of money

and would instead be based on minimal turnaround time whether any project will have the same

cash flow as other decisions.

Accounting rate of return:

Benefits: ARR lets the businesses make their investment options. High returns are good for

the business and competitive (Baños-Caballero, García-Teruel and Martínez-Solano, 2016).

Before reaching any decisions, management determines project ARR by choosing the most

appropriate one. This approach recognizes accounting importance that is frequently found in

proposal-making process by administrators.

Limitation: Average return rates disregard portfolio cash flow that is focused on reported

income and also calculate using average profit. It will further affect different activities needed to

be handled. Time value of money is ignored in this investment assessment techniques the affect

as well as the entire outcome or profitability of the project.

Net Present Value (NPV):

Benefits: The majority of companies use NPV to determine their investment and decide

whether or not the corporation will spend in this project. Favourable value of selected and

negative NPV will be refused as it is not profitable for the organization to continue in such

project. This investment assessment methodology takes into account time value of capital and

creates more prospects in front of corporations. For managers it is important to make their

choices based on the NPV interest.

Limitations: Managers may use this tool to assess their feasibility or to compete with other

plans, but cannot be only if all project cash capital flows were the same. If the initial outlay is

different, then there is no reason to evaluate or make assumptions because it does not yield exact

results. Net present value impacted by discounted rate when it changed and it excludes economic

factors such as inflation.

Internal Rate of Return (IRR):

Benefits: IRR used only to define the returns that company receives after spending in

particular ventures, and then to make additional decisions appropriately. It will ease management

11

helps the business recover more quickly from the original investment.

Limitations: Managers should ignore unfavourable NPV while making important

decisions, as it won't be beneficial at all. This approach does not recognize time value of money

and would instead be based on minimal turnaround time whether any project will have the same

cash flow as other decisions.

Accounting rate of return:

Benefits: ARR lets the businesses make their investment options. High returns are good for

the business and competitive (Baños-Caballero, García-Teruel and Martínez-Solano, 2016).

Before reaching any decisions, management determines project ARR by choosing the most

appropriate one. This approach recognizes accounting importance that is frequently found in

proposal-making process by administrators.

Limitation: Average return rates disregard portfolio cash flow that is focused on reported

income and also calculate using average profit. It will further affect different activities needed to

be handled. Time value of money is ignored in this investment assessment techniques the affect

as well as the entire outcome or profitability of the project.

Net Present Value (NPV):

Benefits: The majority of companies use NPV to determine their investment and decide

whether or not the corporation will spend in this project. Favourable value of selected and

negative NPV will be refused as it is not profitable for the organization to continue in such

project. This investment assessment methodology takes into account time value of capital and

creates more prospects in front of corporations. For managers it is important to make their

choices based on the NPV interest.

Limitations: Managers may use this tool to assess their feasibility or to compete with other

plans, but cannot be only if all project cash capital flows were the same. If the initial outlay is

different, then there is no reason to evaluate or make assumptions because it does not yield exact

results. Net present value impacted by discounted rate when it changed and it excludes economic

factors such as inflation.

Internal Rate of Return (IRR):

Benefits: IRR used only to define the returns that company receives after spending in

particular ventures, and then to make additional decisions appropriately. It will ease management

11

decision making to choose the company's most profitable project (Antonopoulos and Hall, 2018).

Managers make high-return choices, and they determine what project helps companies optimize

their earnings.

Limitations: IRR will not recognize economies of scale that influence the outcomes. It is

measured using hit & check method that does not yield reliable results. This also impacts

executive’s decision-making processes. Additionally, there is no such disparity between loans or

borrowings. Due to the shift in reduced rate, each project may have varying returns, and it is

difficult for executives to take investment decisions.

CONCLUSION

From the above analysis, It had been stated that financial management is really important to

the organisation's financial position. It is the structure that focuses on the enterprise and any

element or operation of the enterprise. Management develop strategy by emphasizing company

and functional efficiency. Company adopts the investment appraisal approach in order to make

financial decisions, that they quantify the various factors for the assessment. It includes, payback

time, rate of return accounting, IRR, NPV etc. Those are the capital budgeting approaches that

help management to make their decisions about future expenditure for the company's growth.

12

Managers make high-return choices, and they determine what project helps companies optimize

their earnings.

Limitations: IRR will not recognize economies of scale that influence the outcomes. It is

measured using hit & check method that does not yield reliable results. This also impacts

executive’s decision-making processes. Additionally, there is no such disparity between loans or

borrowings. Due to the shift in reduced rate, each project may have varying returns, and it is

difficult for executives to take investment decisions.

CONCLUSION

From the above analysis, It had been stated that financial management is really important to

the organisation's financial position. It is the structure that focuses on the enterprise and any

element or operation of the enterprise. Management develop strategy by emphasizing company

and functional efficiency. Company adopts the investment appraisal approach in order to make

financial decisions, that they quantify the various factors for the assessment. It includes, payback

time, rate of return accounting, IRR, NPV etc. Those are the capital budgeting approaches that

help management to make their decisions about future expenditure for the company's growth.

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.