Financial Management Report: CBA Performance Analysis (2018-2019)

VerifiedAdded on 2023/01/07

|18

|4171

|37

Report

AI Summary

This report presents a comprehensive financial analysis of the Commonwealth Bank of Australia (CBA), examining its financial performance from 2018 to 2019. The analysis includes an overview of the bank's background and business, followed by an examination of its financial statements and current economic outlook. The core of the report focuses on a detailed ratio analysis, covering profitability ratios (e.g., return on assets, net profit margin), efficiency ratios (e.g., asset turnover, cash return on assets), liquidity ratios (e.g., current ratio, quick ratio), and gearing ratios. Each ratio is calculated, presented, and discussed, comparing the bank's performance to industry averages. The report concludes with recommendations and an overall assessment of CBA's financial health, supported by calculations in the appendices. The report fulfills the requirements of a FINA600 Financial Management assignment.

Financial Management

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Executive summary.........................................................................................................................3

1. Introduction..................................................................................................................................4

1.1 Background and business......................................................................................................4

2. Company Analysis.......................................................................................................................4

2.1 Financial statements, Current financial performance, economic outlook.............................4

3. Ratio Analysis..............................................................................................................................5

3.1 Profitability ratios..................................................................................................................5

3.2 Efficiency ratios.....................................................................................................................7

3.3 Liquidity ratios.......................................................................................................................9

3.4 Gearing ratios.......................................................................................................................10

4. Recommendations and overall assessment................................................................................12

References......................................................................................................................................13

Appendices....................................................................................................................................14

Executive summary.........................................................................................................................3

1. Introduction..................................................................................................................................4

1.1 Background and business......................................................................................................4

2. Company Analysis.......................................................................................................................4

2.1 Financial statements, Current financial performance, economic outlook.............................4

3. Ratio Analysis..............................................................................................................................5

3.1 Profitability ratios..................................................................................................................5

3.2 Efficiency ratios.....................................................................................................................7

3.3 Liquidity ratios.......................................................................................................................9

3.4 Gearing ratios.......................................................................................................................10

4. Recommendations and overall assessment................................................................................12

References......................................................................................................................................13

Appendices....................................................................................................................................14

Executive summary

This project report is based on the analyses of Common wealth bank of Australia; the ASX name

is CBA. In this report; financial analysis of 2 years from 2018 to 2019 has been done and support

the analysis with interpretation. The final conclusion has been made in the form of

recommendation and assessment at the end.

This project report is based on the analyses of Common wealth bank of Australia; the ASX name

is CBA. In this report; financial analysis of 2 years from 2018 to 2019 has been done and support

the analysis with interpretation. The final conclusion has been made in the form of

recommendation and assessment at the end.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1. Introduction

1.1 Background and business

Commonwealth Bank was established under the Commonwealth Banking Act in 1911 and began

operating in 1912, engaged in the management of investment funds and the financial sector in

general. The Commonwealth Bank of Australia (CBA), or CommBank, is an Australian world

that holds money from organizations in New Zealand, Asia, the United States and the United

Kingdom. It provides a range of budget administrations, including retail, commercial and

institutional administrations, executives, retirement age, protection, profitability and brokerage

administrations. Commonwealth Bank is Australia's largest agency registered on the Australian

Securities Exchange since August 2015 with brands including Bankwest, Colonial First State

Investments, ASB Bank (New Zealand), Securities Commonwealth (CommSec) and

Commonwealth Insurance (CommInsure).

The bank's vision of becoming Australia's best money management association by going beyond

CBA support and a CBA approach is to see crucial open doors within its portfolio activities to

further motivate its customers, individuals and partners. In 1998 this bank was considered an

open group. The bank is headquartered in Sydney and, according to the latest reports, has more

than 1000 branches. In addition to Australia, this bank has supporters in New Zealand and parts

of Asian countries such as Indonesia, Hong Kong and Fiji.

2. Company Analysis

2.1 Financial statements, Current financial performance, economic outlook

Commonwealth Bank has revealed a net profit from operations for the 2020 Financial Year of

$7.3 billion, which indicates the proceeding with strong performance of the Group. Digital

banking is presently more ordinary than any time in recent memory, with new information

demonstrating $1.2 billion is executed through the CommBank App each and every day. Money

NPAT diminished 5% mirroring a kept testing working condition, however business essentials

stayed solid. The diminishing was driven by a 2% decrease altogether working salary, a 2%

1.1 Background and business

Commonwealth Bank was established under the Commonwealth Banking Act in 1911 and began

operating in 1912, engaged in the management of investment funds and the financial sector in

general. The Commonwealth Bank of Australia (CBA), or CommBank, is an Australian world

that holds money from organizations in New Zealand, Asia, the United States and the United

Kingdom. It provides a range of budget administrations, including retail, commercial and

institutional administrations, executives, retirement age, protection, profitability and brokerage

administrations. Commonwealth Bank is Australia's largest agency registered on the Australian

Securities Exchange since August 2015 with brands including Bankwest, Colonial First State

Investments, ASB Bank (New Zealand), Securities Commonwealth (CommSec) and

Commonwealth Insurance (CommInsure).

The bank's vision of becoming Australia's best money management association by going beyond

CBA support and a CBA approach is to see crucial open doors within its portfolio activities to

further motivate its customers, individuals and partners. In 1998 this bank was considered an

open group. The bank is headquartered in Sydney and, according to the latest reports, has more

than 1000 branches. In addition to Australia, this bank has supporters in New Zealand and parts

of Asian countries such as Indonesia, Hong Kong and Fiji.

2. Company Analysis

2.1 Financial statements, Current financial performance, economic outlook

Commonwealth Bank has revealed a net profit from operations for the 2020 Financial Year of

$7.3 billion, which indicates the proceeding with strong performance of the Group. Digital

banking is presently more ordinary than any time in recent memory, with new information

demonstrating $1.2 billion is executed through the CommBank App each and every day. Money

NPAT diminished 5% mirroring a kept testing working condition, however business essentials

stayed solid. The diminishing was driven by a 2% decrease altogether working salary, a 2%

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

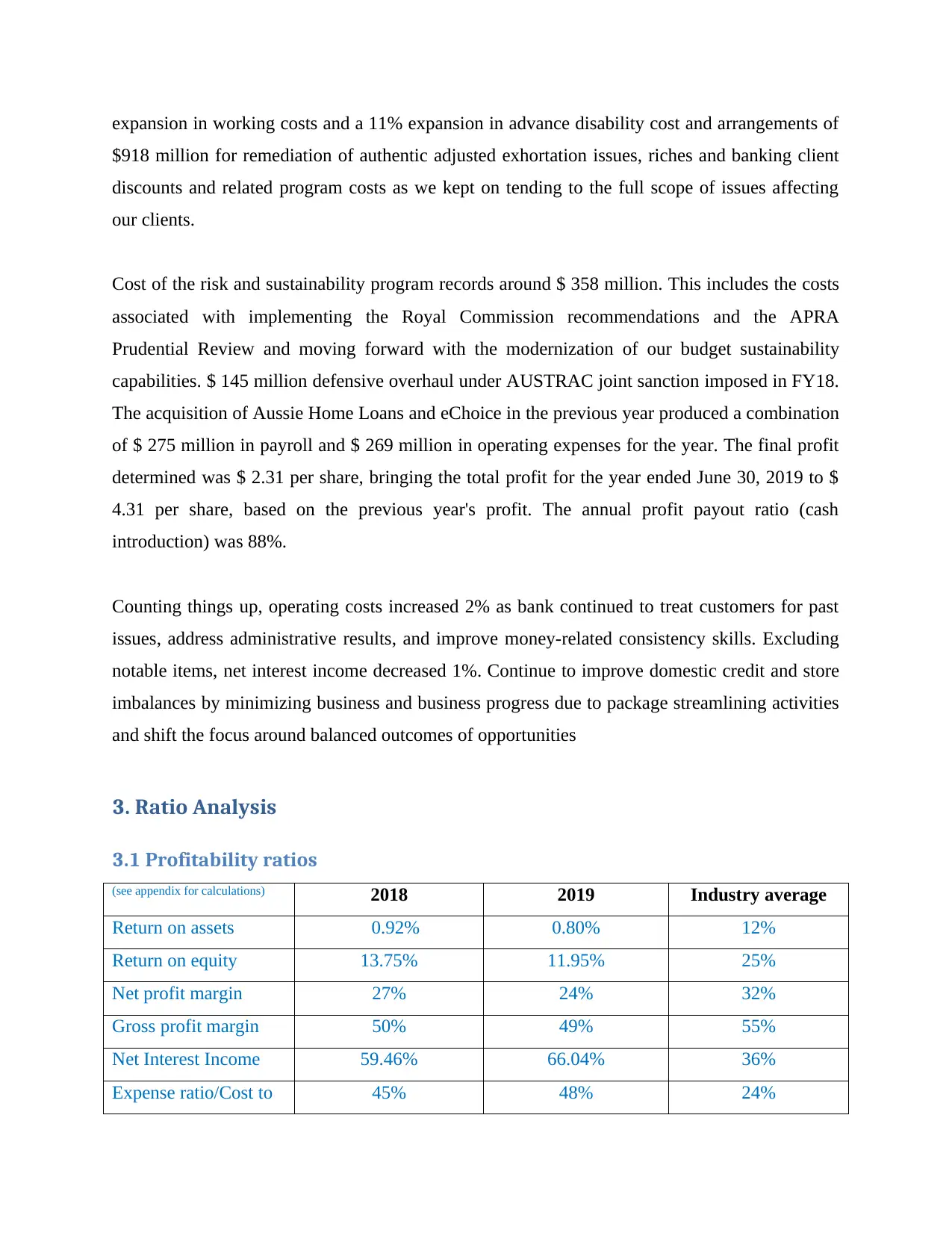

expansion in working costs and a 11% expansion in advance disability cost and arrangements of

$918 million for remediation of authentic adjusted exhortation issues, riches and banking client

discounts and related program costs as we kept on tending to the full scope of issues affecting

our clients.

Cost of the risk and sustainability program records around $ 358 million. This includes the costs

associated with implementing the Royal Commission recommendations and the APRA

Prudential Review and moving forward with the modernization of our budget sustainability

capabilities. $ 145 million defensive overhaul under AUSTRAC joint sanction imposed in FY18.

The acquisition of Aussie Home Loans and eChoice in the previous year produced a combination

of $ 275 million in payroll and $ 269 million in operating expenses for the year. The final profit

determined was $ 2.31 per share, bringing the total profit for the year ended June 30, 2019 to $

4.31 per share, based on the previous year's profit. The annual profit payout ratio (cash

introduction) was 88%.

Counting things up, operating costs increased 2% as bank continued to treat customers for past

issues, address administrative results, and improve money-related consistency skills. Excluding

notable items, net interest income decreased 1%. Continue to improve domestic credit and store

imbalances by minimizing business and business progress due to package streamlining activities

and shift the focus around balanced outcomes of opportunities

3. Ratio Analysis

3.1 Profitability ratios

(see appendix for calculations) 2018 2019 Industry average

Return on assets 0.92% 0.80% 12%

Return on equity 13.75% 11.95% 25%

Net profit margin 27% 24% 32%

Gross profit margin 50% 49% 55%

Net Interest Income 59.46% 66.04% 36%

Expense ratio/Cost to 45% 48% 24%

$918 million for remediation of authentic adjusted exhortation issues, riches and banking client

discounts and related program costs as we kept on tending to the full scope of issues affecting

our clients.

Cost of the risk and sustainability program records around $ 358 million. This includes the costs

associated with implementing the Royal Commission recommendations and the APRA

Prudential Review and moving forward with the modernization of our budget sustainability

capabilities. $ 145 million defensive overhaul under AUSTRAC joint sanction imposed in FY18.

The acquisition of Aussie Home Loans and eChoice in the previous year produced a combination

of $ 275 million in payroll and $ 269 million in operating expenses for the year. The final profit

determined was $ 2.31 per share, bringing the total profit for the year ended June 30, 2019 to $

4.31 per share, based on the previous year's profit. The annual profit payout ratio (cash

introduction) was 88%.

Counting things up, operating costs increased 2% as bank continued to treat customers for past

issues, address administrative results, and improve money-related consistency skills. Excluding

notable items, net interest income decreased 1%. Continue to improve domestic credit and store

imbalances by minimizing business and business progress due to package streamlining activities

and shift the focus around balanced outcomes of opportunities

3. Ratio Analysis

3.1 Profitability ratios

(see appendix for calculations) 2018 2019 Industry average

Return on assets 0.92% 0.80% 12%

Return on equity 13.75% 11.95% 25%

Net profit margin 27% 24% 32%

Gross profit margin 50% 49% 55%

Net Interest Income 59.46% 66.04% 36%

Expense ratio/Cost to 45% 48% 24%

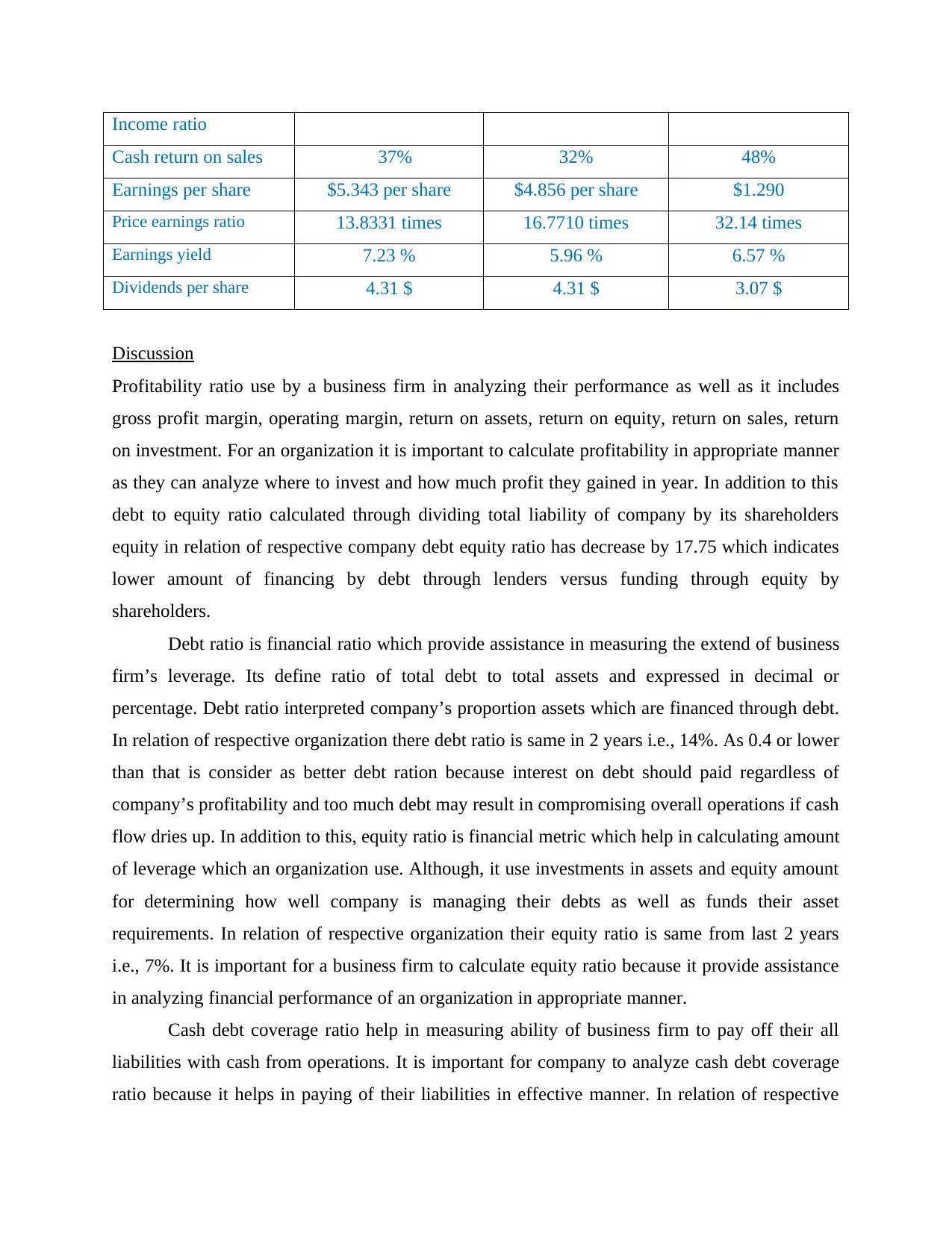

Income ratio

Cash return on sales 37% 32% 48%

Earnings per share $5.343 per share $4.856 per share $1.290

Price earnings ratio 13.8331 times 16.7710 times 32.14 times

Earnings yield 7.23 % 5.96 % 6.57 %

Dividends per share 4.31 $ 4.31 $ 3.07 $

Discussion

Profitability ratio use by a business firm in analyzing their performance as well as it includes

gross profit margin, operating margin, return on assets, return on equity, return on sales, return

on investment. For an organization it is important to calculate profitability in appropriate manner

as they can analyze where to invest and how much profit they gained in year. In addition to this

debt to equity ratio calculated through dividing total liability of company by its shareholders

equity in relation of respective company debt equity ratio has decrease by 17.75 which indicates

lower amount of financing by debt through lenders versus funding through equity by

shareholders.

Debt ratio is financial ratio which provide assistance in measuring the extend of business

firm’s leverage. Its define ratio of total debt to total assets and expressed in decimal or

percentage. Debt ratio interpreted company’s proportion assets which are financed through debt.

In relation of respective organization there debt ratio is same in 2 years i.e., 14%. As 0.4 or lower

than that is consider as better debt ration because interest on debt should paid regardless of

company’s profitability and too much debt may result in compromising overall operations if cash

flow dries up. In addition to this, equity ratio is financial metric which help in calculating amount

of leverage which an organization use. Although, it use investments in assets and equity amount

for determining how well company is managing their debts as well as funds their asset

requirements. In relation of respective organization their equity ratio is same from last 2 years

i.e., 7%. It is important for a business firm to calculate equity ratio because it provide assistance

in analyzing financial performance of an organization in appropriate manner.

Cash debt coverage ratio help in measuring ability of business firm to pay off their all

liabilities with cash from operations. It is important for company to analyze cash debt coverage

ratio because it helps in paying of their liabilities in effective manner. In relation of respective

Cash return on sales 37% 32% 48%

Earnings per share $5.343 per share $4.856 per share $1.290

Price earnings ratio 13.8331 times 16.7710 times 32.14 times

Earnings yield 7.23 % 5.96 % 6.57 %

Dividends per share 4.31 $ 4.31 $ 3.07 $

Discussion

Profitability ratio use by a business firm in analyzing their performance as well as it includes

gross profit margin, operating margin, return on assets, return on equity, return on sales, return

on investment. For an organization it is important to calculate profitability in appropriate manner

as they can analyze where to invest and how much profit they gained in year. In addition to this

debt to equity ratio calculated through dividing total liability of company by its shareholders

equity in relation of respective company debt equity ratio has decrease by 17.75 which indicates

lower amount of financing by debt through lenders versus funding through equity by

shareholders.

Debt ratio is financial ratio which provide assistance in measuring the extend of business

firm’s leverage. Its define ratio of total debt to total assets and expressed in decimal or

percentage. Debt ratio interpreted company’s proportion assets which are financed through debt.

In relation of respective organization there debt ratio is same in 2 years i.e., 14%. As 0.4 or lower

than that is consider as better debt ration because interest on debt should paid regardless of

company’s profitability and too much debt may result in compromising overall operations if cash

flow dries up. In addition to this, equity ratio is financial metric which help in calculating amount

of leverage which an organization use. Although, it use investments in assets and equity amount

for determining how well company is managing their debts as well as funds their asset

requirements. In relation of respective organization their equity ratio is same from last 2 years

i.e., 7%. It is important for a business firm to calculate equity ratio because it provide assistance

in analyzing financial performance of an organization in appropriate manner.

Cash debt coverage ratio help in measuring ability of business firm to pay off their all

liabilities with cash from operations. It is important for company to analyze cash debt coverage

ratio because it helps in paying of their liabilities in effective manner. In relation of respective

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

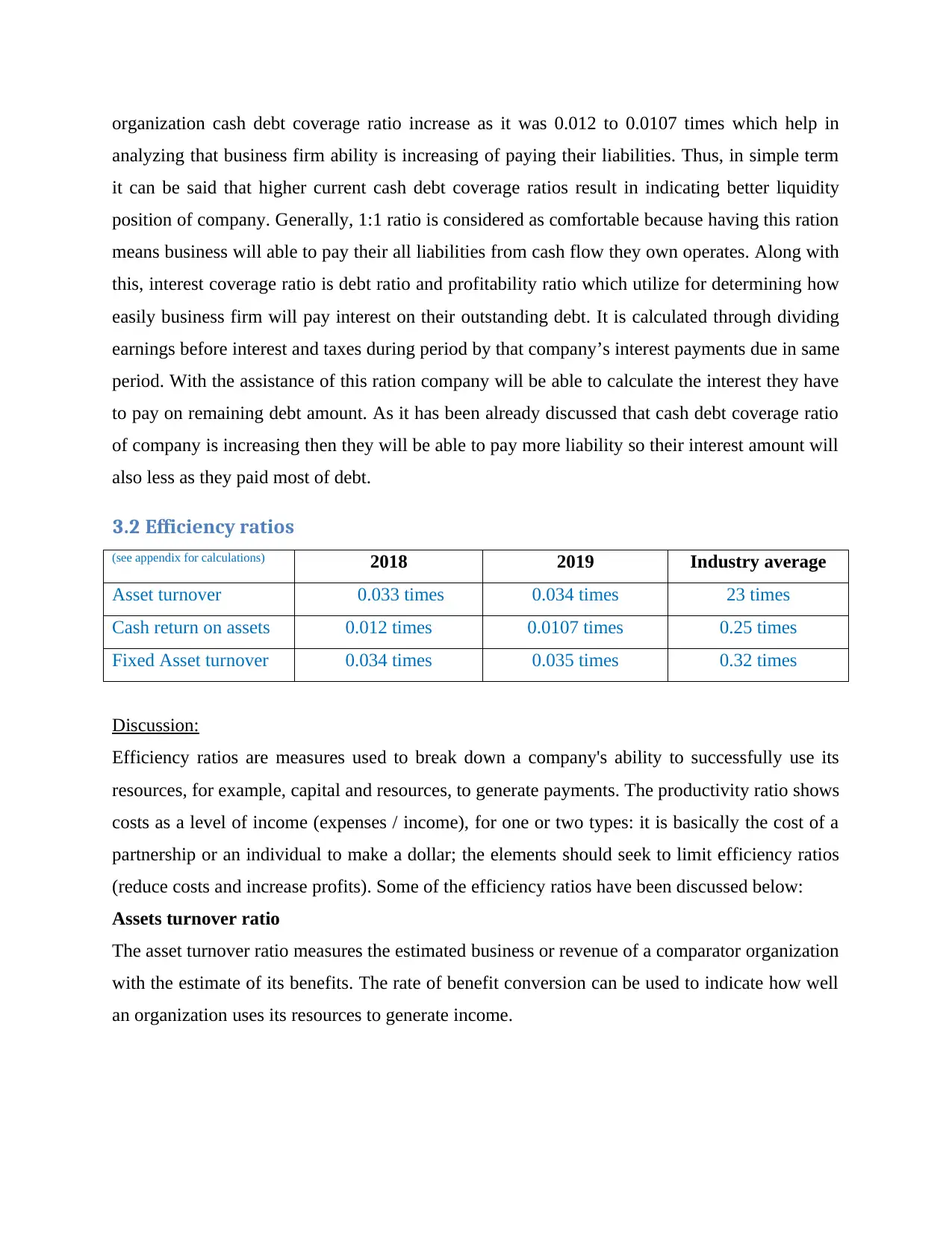

organization cash debt coverage ratio increase as it was 0.012 to 0.0107 times which help in

analyzing that business firm ability is increasing of paying their liabilities. Thus, in simple term

it can be said that higher current cash debt coverage ratios result in indicating better liquidity

position of company. Generally, 1:1 ratio is considered as comfortable because having this ration

means business will able to pay their all liabilities from cash flow they own operates. Along with

this, interest coverage ratio is debt ratio and profitability ratio which utilize for determining how

easily business firm will pay interest on their outstanding debt. It is calculated through dividing

earnings before interest and taxes during period by that company’s interest payments due in same

period. With the assistance of this ration company will be able to calculate the interest they have

to pay on remaining debt amount. As it has been already discussed that cash debt coverage ratio

of company is increasing then they will be able to pay more liability so their interest amount will

also less as they paid most of debt.

3.2 Efficiency ratios

(see appendix for calculations) 2018 2019 Industry average

Asset turnover 0.033 times 0.034 times 23 times

Cash return on assets 0.012 times 0.0107 times 0.25 times

Fixed Asset turnover 0.034 times 0.035 times 0.32 times

Discussion:

Efficiency ratios are measures used to break down a company's ability to successfully use its

resources, for example, capital and resources, to generate payments. The productivity ratio shows

costs as a level of income (expenses / income), for one or two types: it is basically the cost of a

partnership or an individual to make a dollar; the elements should seek to limit efficiency ratios

(reduce costs and increase profits). Some of the efficiency ratios have been discussed below:

Assets turnover ratio

The asset turnover ratio measures the estimated business or revenue of a comparator organization

with the estimate of its benefits. The rate of benefit conversion can be used to indicate how well

an organization uses its resources to generate income.

analyzing that business firm ability is increasing of paying their liabilities. Thus, in simple term

it can be said that higher current cash debt coverage ratios result in indicating better liquidity

position of company. Generally, 1:1 ratio is considered as comfortable because having this ration

means business will able to pay their all liabilities from cash flow they own operates. Along with

this, interest coverage ratio is debt ratio and profitability ratio which utilize for determining how

easily business firm will pay interest on their outstanding debt. It is calculated through dividing

earnings before interest and taxes during period by that company’s interest payments due in same

period. With the assistance of this ration company will be able to calculate the interest they have

to pay on remaining debt amount. As it has been already discussed that cash debt coverage ratio

of company is increasing then they will be able to pay more liability so their interest amount will

also less as they paid most of debt.

3.2 Efficiency ratios

(see appendix for calculations) 2018 2019 Industry average

Asset turnover 0.033 times 0.034 times 23 times

Cash return on assets 0.012 times 0.0107 times 0.25 times

Fixed Asset turnover 0.034 times 0.035 times 0.32 times

Discussion:

Efficiency ratios are measures used to break down a company's ability to successfully use its

resources, for example, capital and resources, to generate payments. The productivity ratio shows

costs as a level of income (expenses / income), for one or two types: it is basically the cost of a

partnership or an individual to make a dollar; the elements should seek to limit efficiency ratios

(reduce costs and increase profits). Some of the efficiency ratios have been discussed below:

Assets turnover ratio

The asset turnover ratio measures the estimated business or revenue of a comparator organization

with the estimate of its benefits. The rate of benefit conversion can be used to indicate how well

an organization uses its resources to generate income.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

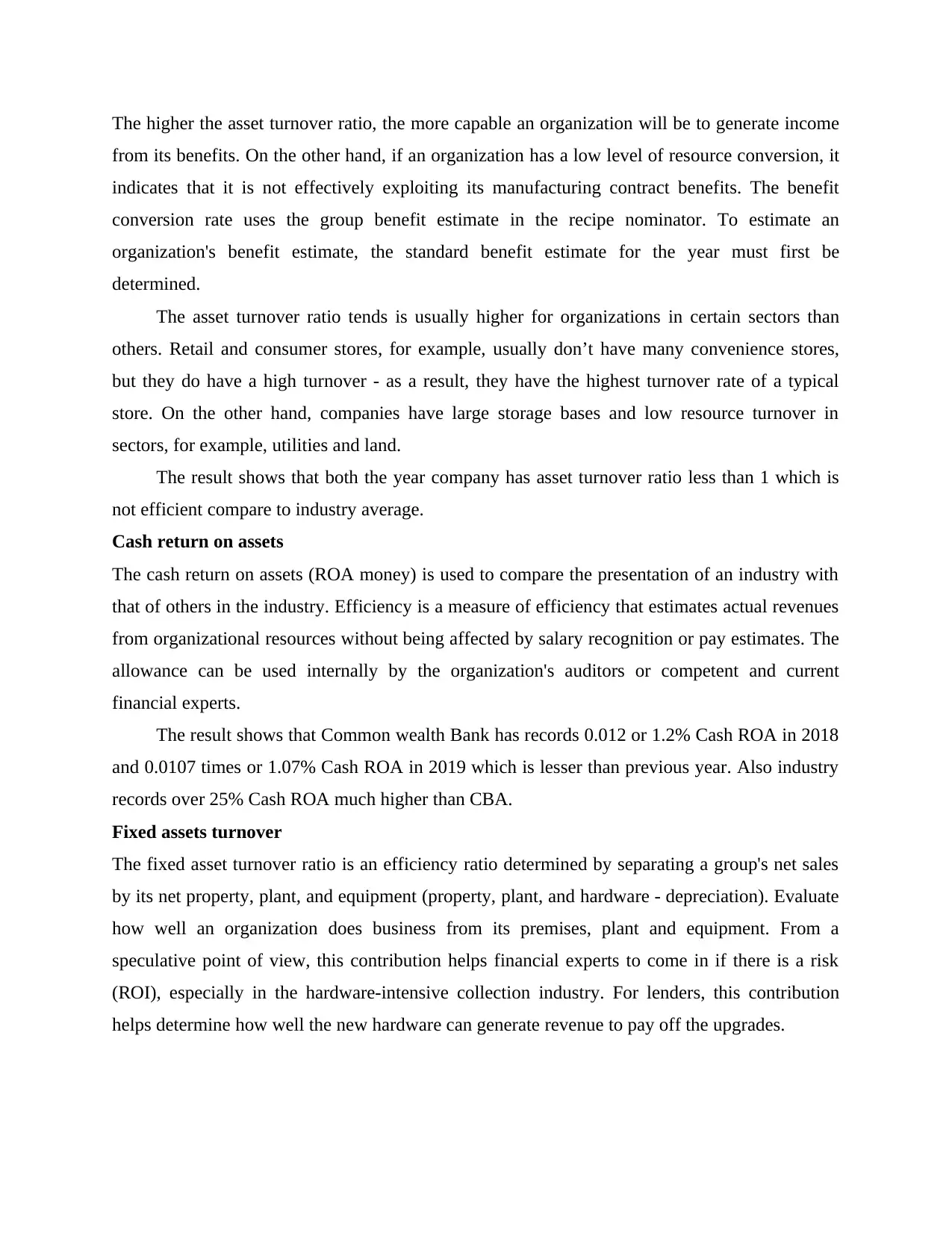

The higher the asset turnover ratio, the more capable an organization will be to generate income

from its benefits. On the other hand, if an organization has a low level of resource conversion, it

indicates that it is not effectively exploiting its manufacturing contract benefits. The benefit

conversion rate uses the group benefit estimate in the recipe nominator. To estimate an

organization's benefit estimate, the standard benefit estimate for the year must first be

determined.

The asset turnover ratio tends is usually higher for organizations in certain sectors than

others. Retail and consumer stores, for example, usually don’t have many convenience stores,

but they do have a high turnover - as a result, they have the highest turnover rate of a typical

store. On the other hand, companies have large storage bases and low resource turnover in

sectors, for example, utilities and land.

The result shows that both the year company has asset turnover ratio less than 1 which is

not efficient compare to industry average.

Cash return on assets

The cash return on assets (ROA money) is used to compare the presentation of an industry with

that of others in the industry. Efficiency is a measure of efficiency that estimates actual revenues

from organizational resources without being affected by salary recognition or pay estimates. The

allowance can be used internally by the organization's auditors or competent and current

financial experts.

The result shows that Common wealth Bank has records 0.012 or 1.2% Cash ROA in 2018

and 0.0107 times or 1.07% Cash ROA in 2019 which is lesser than previous year. Also industry

records over 25% Cash ROA much higher than CBA.

Fixed assets turnover

The fixed asset turnover ratio is an efficiency ratio determined by separating a group's net sales

by its net property, plant, and equipment (property, plant, and hardware - depreciation). Evaluate

how well an organization does business from its premises, plant and equipment. From a

speculative point of view, this contribution helps financial experts to come in if there is a risk

(ROI), especially in the hardware-intensive collection industry. For lenders, this contribution

helps determine how well the new hardware can generate revenue to pay off the upgrades.

from its benefits. On the other hand, if an organization has a low level of resource conversion, it

indicates that it is not effectively exploiting its manufacturing contract benefits. The benefit

conversion rate uses the group benefit estimate in the recipe nominator. To estimate an

organization's benefit estimate, the standard benefit estimate for the year must first be

determined.

The asset turnover ratio tends is usually higher for organizations in certain sectors than

others. Retail and consumer stores, for example, usually don’t have many convenience stores,

but they do have a high turnover - as a result, they have the highest turnover rate of a typical

store. On the other hand, companies have large storage bases and low resource turnover in

sectors, for example, utilities and land.

The result shows that both the year company has asset turnover ratio less than 1 which is

not efficient compare to industry average.

Cash return on assets

The cash return on assets (ROA money) is used to compare the presentation of an industry with

that of others in the industry. Efficiency is a measure of efficiency that estimates actual revenues

from organizational resources without being affected by salary recognition or pay estimates. The

allowance can be used internally by the organization's auditors or competent and current

financial experts.

The result shows that Common wealth Bank has records 0.012 or 1.2% Cash ROA in 2018

and 0.0107 times or 1.07% Cash ROA in 2019 which is lesser than previous year. Also industry

records over 25% Cash ROA much higher than CBA.

Fixed assets turnover

The fixed asset turnover ratio is an efficiency ratio determined by separating a group's net sales

by its net property, plant, and equipment (property, plant, and hardware - depreciation). Evaluate

how well an organization does business from its premises, plant and equipment. From a

speculative point of view, this contribution helps financial experts to come in if there is a risk

(ROI), especially in the hardware-intensive collection industry. For lenders, this contribution

helps determine how well the new hardware can generate revenue to pay off the upgrades.

A consistently fixed asset turnover ratio indicates that a company is using its profits

appropriately and productively to generate revenue. The low turnover rate of fixed assets for the

most part shows the opposite: a company does not use its profits successfully or to the maximum

extent of its revenue generating potential. Allowances alone do not guarantee the success of an

organization’s use of its established resources. Combined with several tests, it can distance you

from activities, performance, and benefits advice.

Thus, the result shows that in 2018; company records 3.4% and 3.5% Fixed assets turnover

ratio in 2019. This indicates, CBA has efficiently utilizes its resources in 2019, but not as much

efficiently as industry does.

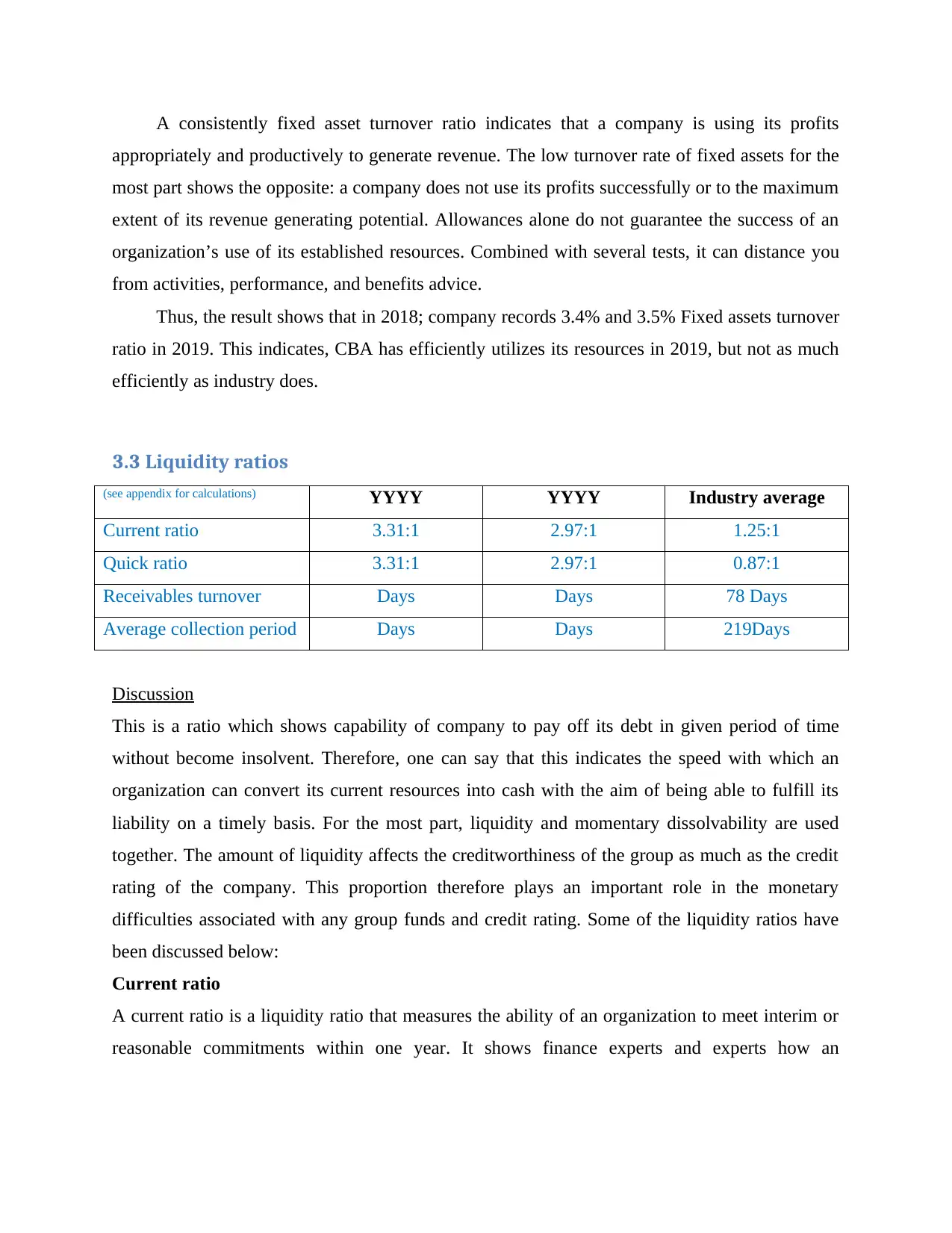

3.3 Liquidity ratios

(see appendix for calculations) YYYY YYYY Industry average

Current ratio 3.31:1 2.97:1 1.25:1

Quick ratio 3.31:1 2.97:1 0.87:1

Receivables turnover Days Days 78 Days

Average collection period Days Days 219Days

Discussion

This is a ratio which shows capability of company to pay off its debt in given period of time

without become insolvent. Therefore, one can say that this indicates the speed with which an

organization can convert its current resources into cash with the aim of being able to fulfill its

liability on a timely basis. For the most part, liquidity and momentary dissolvability are used

together. The amount of liquidity affects the creditworthiness of the group as much as the credit

rating of the company. This proportion therefore plays an important role in the monetary

difficulties associated with any group funds and credit rating. Some of the liquidity ratios have

been discussed below:

Current ratio

A current ratio is a liquidity ratio that measures the ability of an organization to meet interim or

reasonable commitments within one year. It shows finance experts and experts how an

appropriately and productively to generate revenue. The low turnover rate of fixed assets for the

most part shows the opposite: a company does not use its profits successfully or to the maximum

extent of its revenue generating potential. Allowances alone do not guarantee the success of an

organization’s use of its established resources. Combined with several tests, it can distance you

from activities, performance, and benefits advice.

Thus, the result shows that in 2018; company records 3.4% and 3.5% Fixed assets turnover

ratio in 2019. This indicates, CBA has efficiently utilizes its resources in 2019, but not as much

efficiently as industry does.

3.3 Liquidity ratios

(see appendix for calculations) YYYY YYYY Industry average

Current ratio 3.31:1 2.97:1 1.25:1

Quick ratio 3.31:1 2.97:1 0.87:1

Receivables turnover Days Days 78 Days

Average collection period Days Days 219Days

Discussion

This is a ratio which shows capability of company to pay off its debt in given period of time

without become insolvent. Therefore, one can say that this indicates the speed with which an

organization can convert its current resources into cash with the aim of being able to fulfill its

liability on a timely basis. For the most part, liquidity and momentary dissolvability are used

together. The amount of liquidity affects the creditworthiness of the group as much as the credit

rating of the company. This proportion therefore plays an important role in the monetary

difficulties associated with any group funds and credit rating. Some of the liquidity ratios have

been discussed below:

Current ratio

A current ratio is a liquidity ratio that measures the ability of an organization to meet interim or

reasonable commitments within one year. It shows finance experts and experts how an

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

organization can expand the existing resources of its asset relationship to meet its current

responsibilities and various debts.

Both the year have current ratio more than ideal one which is 2:1; which indicates

inefficiency of bank to utilize its short-term cash in proper way.

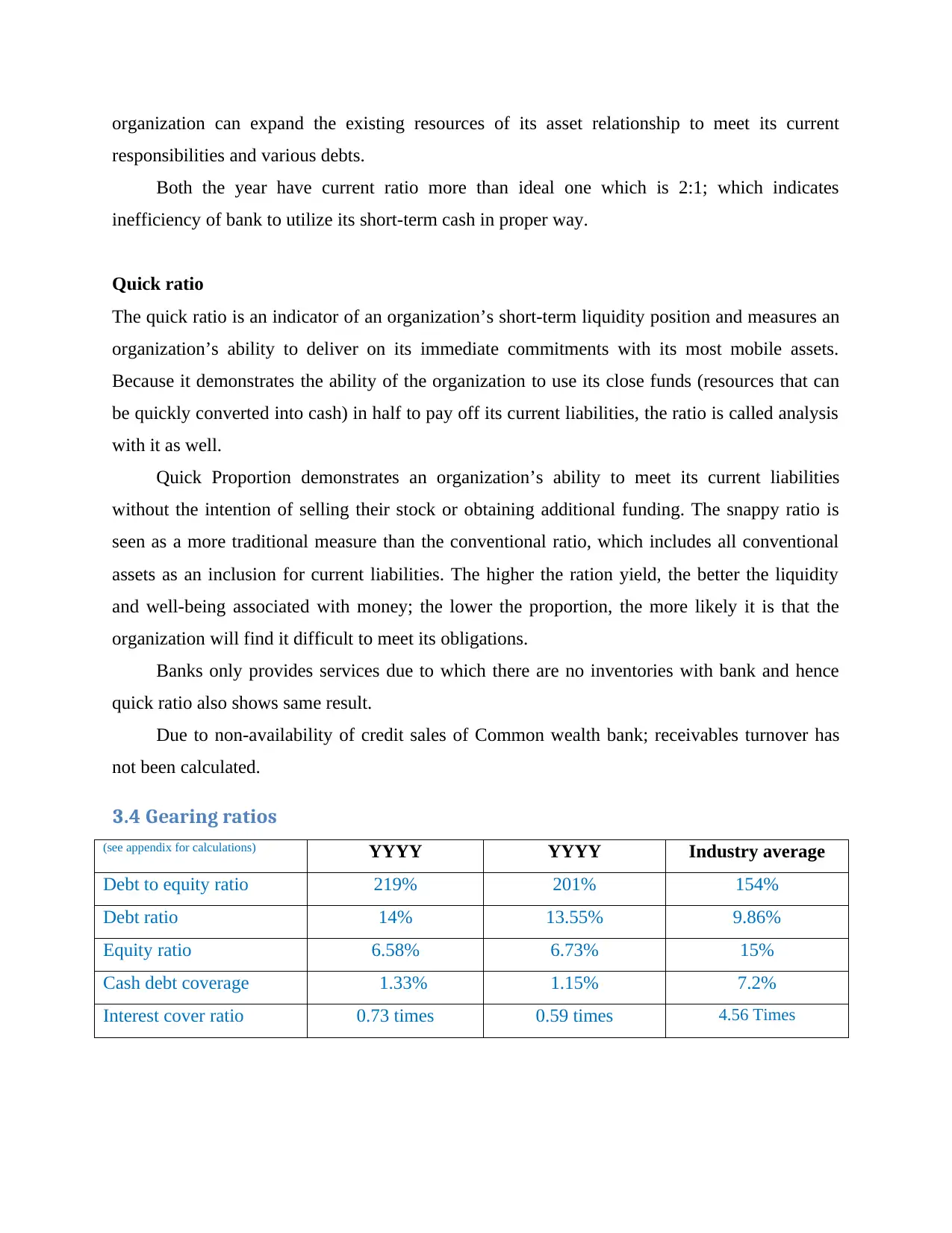

Quick ratio

The quick ratio is an indicator of an organization’s short-term liquidity position and measures an

organization’s ability to deliver on its immediate commitments with its most mobile assets.

Because it demonstrates the ability of the organization to use its close funds (resources that can

be quickly converted into cash) in half to pay off its current liabilities, the ratio is called analysis

with it as well.

Quick Proportion demonstrates an organization’s ability to meet its current liabilities

without the intention of selling their stock or obtaining additional funding. The snappy ratio is

seen as a more traditional measure than the conventional ratio, which includes all conventional

assets as an inclusion for current liabilities. The higher the ration yield, the better the liquidity

and well-being associated with money; the lower the proportion, the more likely it is that the

organization will find it difficult to meet its obligations.

Banks only provides services due to which there are no inventories with bank and hence

quick ratio also shows same result.

Due to non-availability of credit sales of Common wealth bank; receivables turnover has

not been calculated.

3.4 Gearing ratios

(see appendix for calculations) YYYY YYYY Industry average

Debt to equity ratio 219% 201% 154%

Debt ratio 14% 13.55% 9.86%

Equity ratio 6.58% 6.73% 15%

Cash debt coverage 1.33% 1.15% 7.2%

Interest cover ratio 0.73 times 0.59 times 4.56 Times

responsibilities and various debts.

Both the year have current ratio more than ideal one which is 2:1; which indicates

inefficiency of bank to utilize its short-term cash in proper way.

Quick ratio

The quick ratio is an indicator of an organization’s short-term liquidity position and measures an

organization’s ability to deliver on its immediate commitments with its most mobile assets.

Because it demonstrates the ability of the organization to use its close funds (resources that can

be quickly converted into cash) in half to pay off its current liabilities, the ratio is called analysis

with it as well.

Quick Proportion demonstrates an organization’s ability to meet its current liabilities

without the intention of selling their stock or obtaining additional funding. The snappy ratio is

seen as a more traditional measure than the conventional ratio, which includes all conventional

assets as an inclusion for current liabilities. The higher the ration yield, the better the liquidity

and well-being associated with money; the lower the proportion, the more likely it is that the

organization will find it difficult to meet its obligations.

Banks only provides services due to which there are no inventories with bank and hence

quick ratio also shows same result.

Due to non-availability of credit sales of Common wealth bank; receivables turnover has

not been calculated.

3.4 Gearing ratios

(see appendix for calculations) YYYY YYYY Industry average

Debt to equity ratio 219% 201% 154%

Debt ratio 14% 13.55% 9.86%

Equity ratio 6.58% 6.73% 15%

Cash debt coverage 1.33% 1.15% 7.2%

Interest cover ratio 0.73 times 0.59 times 4.56 Times

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

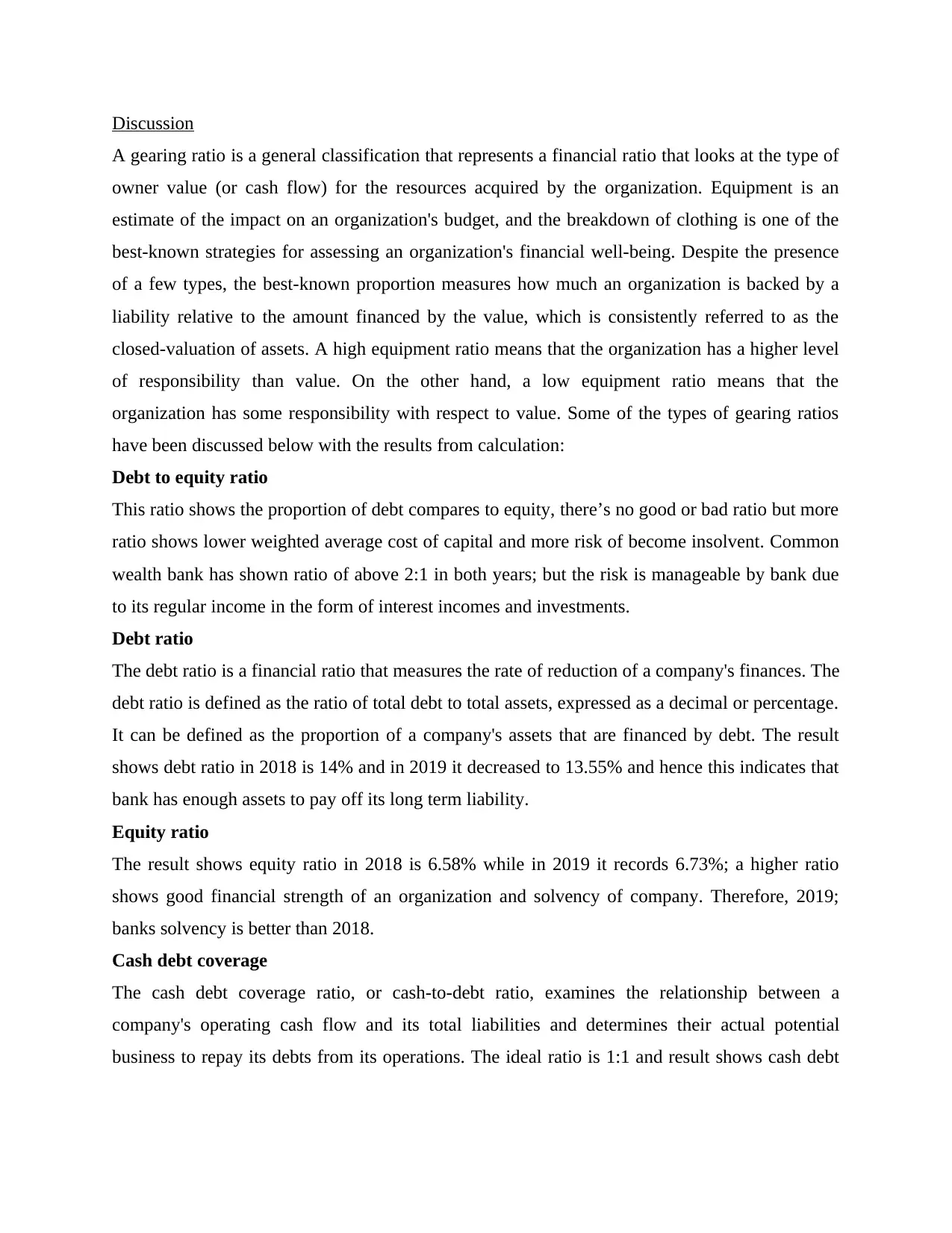

Discussion

A gearing ratio is a general classification that represents a financial ratio that looks at the type of

owner value (or cash flow) for the resources acquired by the organization. Equipment is an

estimate of the impact on an organization's budget, and the breakdown of clothing is one of the

best-known strategies for assessing an organization's financial well-being. Despite the presence

of a few types, the best-known proportion measures how much an organization is backed by a

liability relative to the amount financed by the value, which is consistently referred to as the

closed-valuation of assets. A high equipment ratio means that the organization has a higher level

of responsibility than value. On the other hand, a low equipment ratio means that the

organization has some responsibility with respect to value. Some of the types of gearing ratios

have been discussed below with the results from calculation:

Debt to equity ratio

This ratio shows the proportion of debt compares to equity, there’s no good or bad ratio but more

ratio shows lower weighted average cost of capital and more risk of become insolvent. Common

wealth bank has shown ratio of above 2:1 in both years; but the risk is manageable by bank due

to its regular income in the form of interest incomes and investments.

Debt ratio

The debt ratio is a financial ratio that measures the rate of reduction of a company's finances. The

debt ratio is defined as the ratio of total debt to total assets, expressed as a decimal or percentage.

It can be defined as the proportion of a company's assets that are financed by debt. The result

shows debt ratio in 2018 is 14% and in 2019 it decreased to 13.55% and hence this indicates that

bank has enough assets to pay off its long term liability.

Equity ratio

The result shows equity ratio in 2018 is 6.58% while in 2019 it records 6.73%; a higher ratio

shows good financial strength of an organization and solvency of company. Therefore, 2019;

banks solvency is better than 2018.

Cash debt coverage

The cash debt coverage ratio, or cash-to-debt ratio, examines the relationship between a

company's operating cash flow and its total liabilities and determines their actual potential

business to repay its debts from its operations. The ideal ratio is 1:1 and result shows cash debt

A gearing ratio is a general classification that represents a financial ratio that looks at the type of

owner value (or cash flow) for the resources acquired by the organization. Equipment is an

estimate of the impact on an organization's budget, and the breakdown of clothing is one of the

best-known strategies for assessing an organization's financial well-being. Despite the presence

of a few types, the best-known proportion measures how much an organization is backed by a

liability relative to the amount financed by the value, which is consistently referred to as the

closed-valuation of assets. A high equipment ratio means that the organization has a higher level

of responsibility than value. On the other hand, a low equipment ratio means that the

organization has some responsibility with respect to value. Some of the types of gearing ratios

have been discussed below with the results from calculation:

Debt to equity ratio

This ratio shows the proportion of debt compares to equity, there’s no good or bad ratio but more

ratio shows lower weighted average cost of capital and more risk of become insolvent. Common

wealth bank has shown ratio of above 2:1 in both years; but the risk is manageable by bank due

to its regular income in the form of interest incomes and investments.

Debt ratio

The debt ratio is a financial ratio that measures the rate of reduction of a company's finances. The

debt ratio is defined as the ratio of total debt to total assets, expressed as a decimal or percentage.

It can be defined as the proportion of a company's assets that are financed by debt. The result

shows debt ratio in 2018 is 14% and in 2019 it decreased to 13.55% and hence this indicates that

bank has enough assets to pay off its long term liability.

Equity ratio

The result shows equity ratio in 2018 is 6.58% while in 2019 it records 6.73%; a higher ratio

shows good financial strength of an organization and solvency of company. Therefore, 2019;

banks solvency is better than 2018.

Cash debt coverage

The cash debt coverage ratio, or cash-to-debt ratio, examines the relationship between a

company's operating cash flow and its total liabilities and determines their actual potential

business to repay its debts from its operations. The ideal ratio is 1:1 and result shows cash debt

ratio of only 0.0133 in 2018 and 0.0115 in 2019 which is much less than ideal merits and

indicates high risk to the company.

4. Recommendations and overall assessment

After analyzing all facts and figures of two years financial statement of Common wealth bank of

Australia from 2018 to 2019; following assessments has been made:

Has year 1 been better than year 2 for the company?

Yes, year 2018 has performed better than year 2019 of the bank. As different ratios like

profitability, efficiency and liquidity results indicates poor performance records in the year 2019

as compared to previous year.

Will the bank succeed in the future?

It’s a question mark whether it will perform well in the future or not but estimates say that; bank

has plan to launch its new digital services in the market to increase its customer base. But the

financial analyses report reflects opposite results.

The ethical considerations if the organization becomes insolvent

If the organization become insolvent than thousands of shareholders will face a loss in millions

and other money lender banks of Australia who owes money to Common wealth bank will also

loss their big portion of Assets into it.

Recommendation to bank

Based on above analysis; it is suggested that bank should minimize its debts and focus on

increasing its sources of income from investment in new ventures and blue chips company

shares. It is also recommended to minimize banks interest expenses on loans to other banks.

Should investment be done in this bank?

Well, it’s risky to invest in buying the shares of CBA because of higher risk and fewer returns. It

is better to invest in bonds rather to purchase CBA’s shares.

indicates high risk to the company.

4. Recommendations and overall assessment

After analyzing all facts and figures of two years financial statement of Common wealth bank of

Australia from 2018 to 2019; following assessments has been made:

Has year 1 been better than year 2 for the company?

Yes, year 2018 has performed better than year 2019 of the bank. As different ratios like

profitability, efficiency and liquidity results indicates poor performance records in the year 2019

as compared to previous year.

Will the bank succeed in the future?

It’s a question mark whether it will perform well in the future or not but estimates say that; bank

has plan to launch its new digital services in the market to increase its customer base. But the

financial analyses report reflects opposite results.

The ethical considerations if the organization becomes insolvent

If the organization become insolvent than thousands of shareholders will face a loss in millions

and other money lender banks of Australia who owes money to Common wealth bank will also

loss their big portion of Assets into it.

Recommendation to bank

Based on above analysis; it is suggested that bank should minimize its debts and focus on

increasing its sources of income from investment in new ventures and blue chips company

shares. It is also recommended to minimize banks interest expenses on loans to other banks.

Should investment be done in this bank?

Well, it’s risky to invest in buying the shares of CBA because of higher risk and fewer returns. It

is better to invest in bonds rather to purchase CBA’s shares.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.