Financial Management Report: Decision Making, Ratios, and Fraud

VerifiedAdded on 2023/01/11

|17

|5310

|61

Report

AI Summary

This report provides a comprehensive overview of financial management, focusing on its crucial role in business organizations for achieving sustainable growth. It explores various decision-making approaches, techniques, and factors that contribute to effective outcomes, including formal and informal decision-making processes, brainstorming, and cost-benefit analysis. The report delves into stakeholder management, addressing conflicting objectives and the importance of maintaining good relationships with internal and external stakeholders. It also examines the value of management accounting techniques like budgetary control and standard costing. Furthermore, the report discusses techniques for fraud detection and prevention, emphasizing the importance of identifying potential fraud areas, timely audits, and communicating implemented systems to staff. The report includes a financial ratio analysis of Morrison Supermarkets PLC, providing insights into its financial position and performance. It concludes with recommendations for improving financial sustainability. This report is a valuable resource for students studying financial management, offering insights into key concepts and practical applications.

Financial Management

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION......................................................................................................................3

Scenario A..................................................................................................................................3

1. Range of approaches, techniques and factor contributing to effective decision making...3

2. Stakeholder management and conflicting objective of different stakeholder....................4

3. Value of management accounting techniques....................................................................5

4. Techniques for fraud detection and prevention and approach to ethical decision making 5

5. Reflection...........................................................................................................................6

Scenario B..................................................................................................................................6

Financial ratios analysis of Morrison Supermarkets PLC for the year 2020, 2019 & 2018. .6

Application of data obtained in decision making.................................................................13

Outcomes of investment appraisal techniques utilized in taking actions to maximise ROI 14

Value of the techniques that is used in informed decision making......................................15

Long term sustainability through financial decision making...............................................15

Recommendations to improve financial sustainability........................................................15

CONCLUSION........................................................................................................................16

REFERENCES.........................................................................................................................17

INTRODUCTION......................................................................................................................3

Scenario A..................................................................................................................................3

1. Range of approaches, techniques and factor contributing to effective decision making...3

2. Stakeholder management and conflicting objective of different stakeholder....................4

3. Value of management accounting techniques....................................................................5

4. Techniques for fraud detection and prevention and approach to ethical decision making 5

5. Reflection...........................................................................................................................6

Scenario B..................................................................................................................................6

Financial ratios analysis of Morrison Supermarkets PLC for the year 2020, 2019 & 2018. .6

Application of data obtained in decision making.................................................................13

Outcomes of investment appraisal techniques utilized in taking actions to maximise ROI 14

Value of the techniques that is used in informed decision making......................................15

Long term sustainability through financial decision making...............................................15

Recommendations to improve financial sustainability........................................................15

CONCLUSION........................................................................................................................16

REFERENCES.........................................................................................................................17

INTRODUCTION

Financial management is the main function of every business organization. It refers to

the implementation of various principles of management for effectively managing the

financial resources of the company. In this report, the various aspects of financial

management are discussed in respect to decision making which helps in attaining sustainable

growth. The ratio analysis of Morrisons plc is carried out to know its financial position and

performance.

Scenario A

1. Range of approaches, techniques and factor contributing to effective decision making

There are many different types of approaches, techniques and factor which used to

contribute very adversely in making variety of the different type of the decision in the

organization. Some of the techniques approaches and factors of decision making are as

follows:

Approaches of Decision making

Formal Decision making: It is the type of decision making approach which is

generally followed by the company in taking variety of the decision in the organization. This

is the type of the decision making process in which all the responsible authority and allotted

with different responsibility and on the basis of the same different decision are being taken in

the organization. This approach generally follows a chain of process before making any

decision in the organization (Finkler, Smith and Calabrese, 2018).

Informal Decision making: This is the type of the decision making approach in firm,

in which there is no change of the process which are being followed in the organization to

make any of the decision at workplace. Different decisions are generally taken in the

organization in the participatory manner, in which generally all employees are involved in

decision making.

Different Technique of Decision making

Brainstorming: This is a type of the technique in which different decision in the

organization are taken on the basis of brainstorming management team to make variety of

different decision in an organization. It is technique of decision making in which all the

employee generally used to sit together and discuss variety of the decision in the organization

and finalize variety of the decision in company.

Cost Benefit Analysis: Cost benefit is another technique of decision making in which

company generally used to consider cost behind making variety of the decision and also used

to look at the benefit of making decision. On the basis of the same different decision are

being made at workplace. In this cost of implementing the decision and looking at the future

benefit of the decision are compared and on the basis of the same it used to decide whether

the decision which organization is looking to make is viable or not for the organization.

Different Factors contributing toward decision making

Financial management is the main function of every business organization. It refers to

the implementation of various principles of management for effectively managing the

financial resources of the company. In this report, the various aspects of financial

management are discussed in respect to decision making which helps in attaining sustainable

growth. The ratio analysis of Morrisons plc is carried out to know its financial position and

performance.

Scenario A

1. Range of approaches, techniques and factor contributing to effective decision making

There are many different types of approaches, techniques and factor which used to

contribute very adversely in making variety of the different type of the decision in the

organization. Some of the techniques approaches and factors of decision making are as

follows:

Approaches of Decision making

Formal Decision making: It is the type of decision making approach which is

generally followed by the company in taking variety of the decision in the organization. This

is the type of the decision making process in which all the responsible authority and allotted

with different responsibility and on the basis of the same different decision are being taken in

the organization. This approach generally follows a chain of process before making any

decision in the organization (Finkler, Smith and Calabrese, 2018).

Informal Decision making: This is the type of the decision making approach in firm,

in which there is no change of the process which are being followed in the organization to

make any of the decision at workplace. Different decisions are generally taken in the

organization in the participatory manner, in which generally all employees are involved in

decision making.

Different Technique of Decision making

Brainstorming: This is a type of the technique in which different decision in the

organization are taken on the basis of brainstorming management team to make variety of

different decision in an organization. It is technique of decision making in which all the

employee generally used to sit together and discuss variety of the decision in the organization

and finalize variety of the decision in company.

Cost Benefit Analysis: Cost benefit is another technique of decision making in which

company generally used to consider cost behind making variety of the decision and also used

to look at the benefit of making decision. On the basis of the same different decision are

being made at workplace. In this cost of implementing the decision and looking at the future

benefit of the decision are compared and on the basis of the same it used to decide whether

the decision which organization is looking to make is viable or not for the organization.

Different Factors contributing toward decision making

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Perception issue: It is the first factor which is consider by the organization, this

factor generally used to impact the process of decision making in the organization. As all the

people in the nation used to has different perception, thinking power and all the individual

used to has different ability to carry out different performance. As a result these is certainly

consider by all the organization before making any decision in the organization (Chandra,

2017).

Policies and Procedure: It is another important factor which is generally consider by

different firms at the time of making different decision in the organization. As all

organization generally used to look at the process which is simple in the nature, as

organization generally find it hard to make a rigid decision that easily in the organization.

Hence, different procedures which are followed in the organization used to impact efficiency

of variety of the different decision which is being taken in the organization.

2. Stakeholder management and conflicting objective of different stakeholder

Stakeholder management is the process in the organization in which organization used

to look to manage the good sort of the relationship with the variety of stakeholder of the

company. This process generally looks to involve the systematic review of different need and

requirement of different stakeholder and organization look to meet the different need of the

stakeholder in efficient ways in the organization. Stakeholder are generally defines as a

different parties in the organization who generally used to has a good sort of the interest in

the variety of the different operation of the business which are being carried out in the

organization (Candee and et.al., 2018). Generally all the stakeholder in the organization used

to has the different need and preference in the organization. As a result all the organization

used to take the different decision so that the need of different stakeholder can be maintain

very easily in the market. Main reason behind the same is identified that as company grows in

the size need and preference of different stakeholder are automatically fulfilled in the market.

So, it generally means that good stakeholder management system in the organization used to

help the stakeholder of the company to make different interested parties happy and satisfied

in the market. There are many different type of stakeholder which generally used to dealt in

the organization. There are two category of stakeholder i.e. internal stakeholder and external

stakeholder in organization. Internal stakeholder are the one in the organization who used to

operate from internal management of the organization i.e. senior management, employee and

management team. At the same time external stakeholder are the one in the organization who

used to operate from external environment, example are competitor and consumer in the

market.

All the stakeholder generally used to has a different sort of the interest in the

operation, these eventually used to create the situation in the organization to understand the

need of the different stakeholder and on the basis of the same different stakeholder plan are

generally made in the organization and on the basis of the same different organization used to

plan variety of different activity in the organization (Barr, and McClellan, 2018). Conflict

objective of different organization used to create many type of complicacies in the

organization. As a result organization generally used to focuses on different goals of the

business in the long run. To manage the objective of all the stakeholder in the organization,

all the organization generally look to present their objective in front of different stakeholder

in the way that they used to find the decision of the organization in a good manner these

generally help the company in getting the support of stakeholder and also help the company

in managing the interest of all the stakeholder in the long run (Alam, 2018).

factor generally used to impact the process of decision making in the organization. As all the

people in the nation used to has different perception, thinking power and all the individual

used to has different ability to carry out different performance. As a result these is certainly

consider by all the organization before making any decision in the organization (Chandra,

2017).

Policies and Procedure: It is another important factor which is generally consider by

different firms at the time of making different decision in the organization. As all

organization generally used to look at the process which is simple in the nature, as

organization generally find it hard to make a rigid decision that easily in the organization.

Hence, different procedures which are followed in the organization used to impact efficiency

of variety of the different decision which is being taken in the organization.

2. Stakeholder management and conflicting objective of different stakeholder

Stakeholder management is the process in the organization in which organization used

to look to manage the good sort of the relationship with the variety of stakeholder of the

company. This process generally looks to involve the systematic review of different need and

requirement of different stakeholder and organization look to meet the different need of the

stakeholder in efficient ways in the organization. Stakeholder are generally defines as a

different parties in the organization who generally used to has a good sort of the interest in

the variety of the different operation of the business which are being carried out in the

organization (Candee and et.al., 2018). Generally all the stakeholder in the organization used

to has the different need and preference in the organization. As a result all the organization

used to take the different decision so that the need of different stakeholder can be maintain

very easily in the market. Main reason behind the same is identified that as company grows in

the size need and preference of different stakeholder are automatically fulfilled in the market.

So, it generally means that good stakeholder management system in the organization used to

help the stakeholder of the company to make different interested parties happy and satisfied

in the market. There are many different type of stakeholder which generally used to dealt in

the organization. There are two category of stakeholder i.e. internal stakeholder and external

stakeholder in organization. Internal stakeholder are the one in the organization who used to

operate from internal management of the organization i.e. senior management, employee and

management team. At the same time external stakeholder are the one in the organization who

used to operate from external environment, example are competitor and consumer in the

market.

All the stakeholder generally used to has a different sort of the interest in the

operation, these eventually used to create the situation in the organization to understand the

need of the different stakeholder and on the basis of the same different stakeholder plan are

generally made in the organization and on the basis of the same different organization used to

plan variety of different activity in the organization (Barr, and McClellan, 2018). Conflict

objective of different organization used to create many type of complicacies in the

organization. As a result organization generally used to focuses on different goals of the

business in the long run. To manage the objective of all the stakeholder in the organization,

all the organization generally look to present their objective in front of different stakeholder

in the way that they used to find the decision of the organization in a good manner these

generally help the company in getting the support of stakeholder and also help the company

in managing the interest of all the stakeholder in the long run (Alam, 2018).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

3. Value of management accounting techniques

There are two kinds of guidelines which can be utilized for cost control, that is,

internal and external measures. The external standard measures are predominantly utilized for

comparing the performance of the organization with regard to different firms within the

industry with the help of financial ratios. As opposed to it, internal standards are utilized for

assessing the infra firm cost components, for example, material, labour and so on. Some of

the internal management accounting techniques are stated below.

Budgetary control

It is gotten from the financial plan as it utilizes budget plan for executing the

budgetary control as a method for arranging and controlling the different kinds of business

exercises. It builds up the pre-determined goals which is additionally utilized as a reason to

measure the performance of the business (Pradhan, Swain and Dash, 2018). Under budgetary

control, actual result is compared with the planned targets and in case if any deviation is

there, reasons for the same is identified and furthermore remedial moves is made to correct

the errors. The budgetary control helps in amplifying the use of constrained assets in a

effective manner and builds up appropriate coordination among the individuals. This aides in

viable profit planning and whenever executed effectively will result into increment in benefits

which will prompt increment in the investors' worth.

Standard costing

It is the most broadly utilized framework for practicing the cost control. Under this

method, the point is to set up the standards of performance along with the set target costs

which the organization is required to accomplish by remaining in the set working conditions.

It is fundamentally the pre-decided cost that decides the what every item would cost under

the given arrangement of conditions. It starts with the future estimate of the item regarding its

expense in a future period then standard expenses are set by collecting all the important

information from the various sources. This method sets up the measuring standard dependent

on which the presentation of the organization is estimated that helps in practicing the control

which implies for cost reduction and is thus prompts increment in benefits prompting

increment in the investors value which is valuable for both the organization and the investors.

4. Techniques for fraud detection and prevention and approach to ethical decision making

Fraud can be caused in light of tricks or fudging the money related reports or robbery

the own boss. The organizations and government offices across the world have suffered the

loss of several billions in lost or the abused assets due to unethical works practices causing an

irreversible harm to the organization's reputation and influencing the client trust. At the point

when the issue deteriorates, it forces associations to reduce its staff and reduce the spending

as well (Halbouni, Obeid and Garbou, 2016). The focus has been moving to internal review

divisions who are currently required to execute the misrepresentation anticipation and

identification measures. Some of the key strategies that can be utilized by the associations for

preventing and recognizing misrepresentation are described below.

Identifying the potential areas of fraud

This is the most important aspect in which the organization is required to list down

the crucial areas where there is higher chance of fraud along with the level of it. Then

There are two kinds of guidelines which can be utilized for cost control, that is,

internal and external measures. The external standard measures are predominantly utilized for

comparing the performance of the organization with regard to different firms within the

industry with the help of financial ratios. As opposed to it, internal standards are utilized for

assessing the infra firm cost components, for example, material, labour and so on. Some of

the internal management accounting techniques are stated below.

Budgetary control

It is gotten from the financial plan as it utilizes budget plan for executing the

budgetary control as a method for arranging and controlling the different kinds of business

exercises. It builds up the pre-determined goals which is additionally utilized as a reason to

measure the performance of the business (Pradhan, Swain and Dash, 2018). Under budgetary

control, actual result is compared with the planned targets and in case if any deviation is

there, reasons for the same is identified and furthermore remedial moves is made to correct

the errors. The budgetary control helps in amplifying the use of constrained assets in a

effective manner and builds up appropriate coordination among the individuals. This aides in

viable profit planning and whenever executed effectively will result into increment in benefits

which will prompt increment in the investors' worth.

Standard costing

It is the most broadly utilized framework for practicing the cost control. Under this

method, the point is to set up the standards of performance along with the set target costs

which the organization is required to accomplish by remaining in the set working conditions.

It is fundamentally the pre-decided cost that decides the what every item would cost under

the given arrangement of conditions. It starts with the future estimate of the item regarding its

expense in a future period then standard expenses are set by collecting all the important

information from the various sources. This method sets up the measuring standard dependent

on which the presentation of the organization is estimated that helps in practicing the control

which implies for cost reduction and is thus prompts increment in benefits prompting

increment in the investors value which is valuable for both the organization and the investors.

4. Techniques for fraud detection and prevention and approach to ethical decision making

Fraud can be caused in light of tricks or fudging the money related reports or robbery

the own boss. The organizations and government offices across the world have suffered the

loss of several billions in lost or the abused assets due to unethical works practices causing an

irreversible harm to the organization's reputation and influencing the client trust. At the point

when the issue deteriorates, it forces associations to reduce its staff and reduce the spending

as well (Halbouni, Obeid and Garbou, 2016). The focus has been moving to internal review

divisions who are currently required to execute the misrepresentation anticipation and

identification measures. Some of the key strategies that can be utilized by the associations for

preventing and recognizing misrepresentation are described below.

Identifying the potential areas of fraud

This is the most important aspect in which the organization is required to list down

the crucial areas where there is higher chance of fraud along with the level of it. Then

evaluate the impact of the risk on the business functioning. Also, the organization needs to

determine the risk which has a direct relation with its shareholders.

Timely audit and monitoring

By implementing timely audit and review system in the organization will help in

accuracy and validity of the business transactions. Also, the company can set up the script

which will run in the system for monitoring huge volume of data with the objective of

identifying anomalies. This will improve the quality of fraud detection.

Communicating the system implemented to the staff

For preventing fraud, the company can communicate with its employees about the

system implemented in the organization which will make them aware of it and if they tried to

do any fraud they can be easily caught. This will help in reducing the breaching the control

system and is the best way of prevention.

5. Reflection

Subsequent to evaluation all the 4 above stated questions, I can say that management

accounting is significant from the business point of view. The wide scope of methods and

instruments it has will help the business association in effective decision making. These

techniques are structured so that it will meet the different business prerequisites. Considering

different perspectives before taking decisions, for example, monetary and non-monetary

related viewpoints. The role of stakeholders in a business association is very essential and, in

this manner, appropriate management of them is exceptionally fundamental for the

association. There are two sorts of partners internal and external each having their own points

and objective and on the opposite side is organization which is having its own mission and

vision. Also, the organization is required to meet the needs of its stakeholders in order to run

the business smoothly. Additionally, decisions are taken by understanding the effect of it on

the organization's shareholders else it will influence the investors value. The different

strategies that can be utilized to deal with the expense and increasing the investors' worth

which is helpful for the organization. Misrepresentation and fraud which is the serious issue

that each association is confronting can be decreased or moderated by the application of

different procedures and approaches and furthermore it will help in identifying and detecting

that would have caused it.

Scenario B

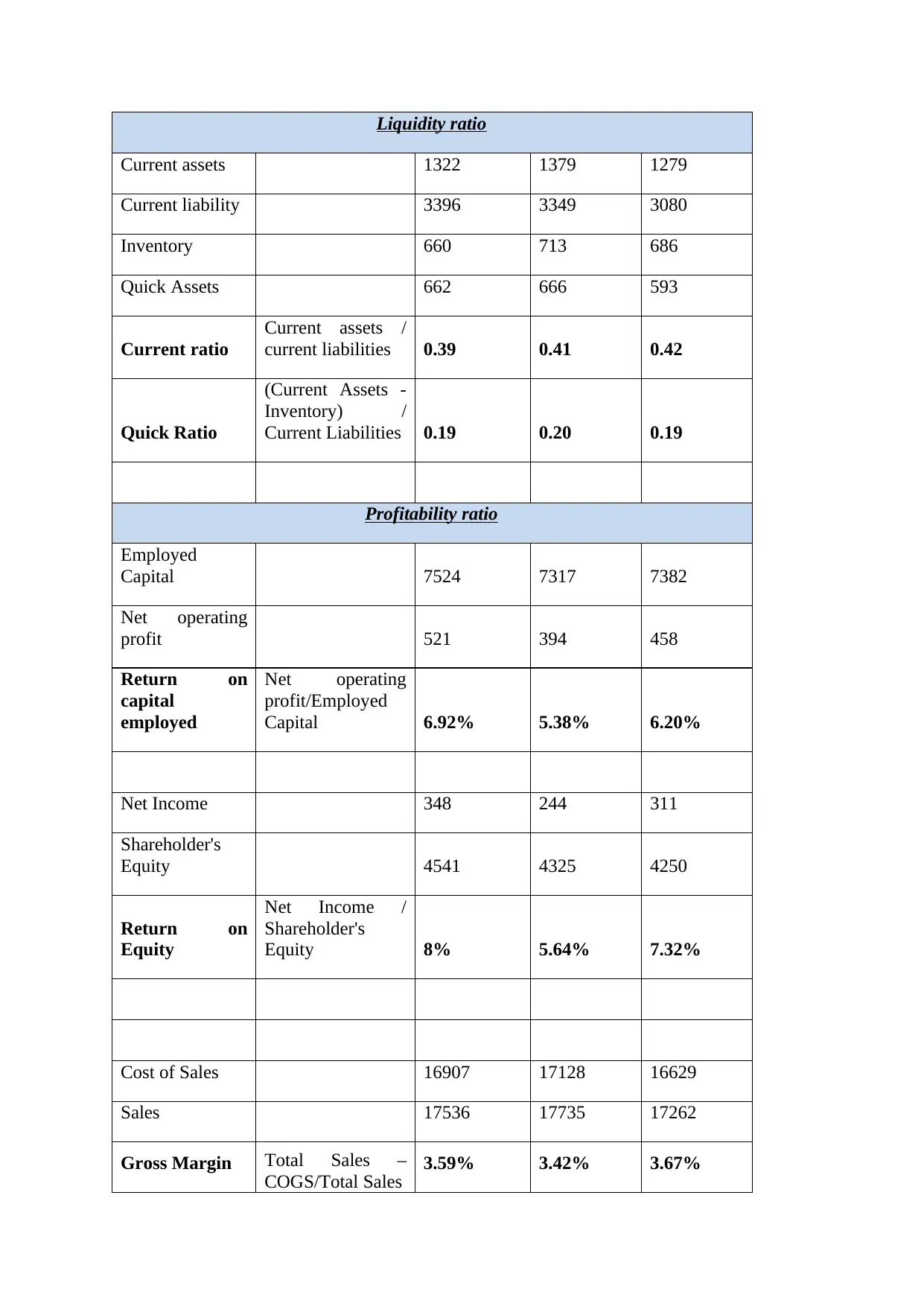

Financial ratios analysis of Morrison Supermarkets PLC for the year 2020, 2019 & 2018

Morrisons

2020 2019 2018

determine the risk which has a direct relation with its shareholders.

Timely audit and monitoring

By implementing timely audit and review system in the organization will help in

accuracy and validity of the business transactions. Also, the company can set up the script

which will run in the system for monitoring huge volume of data with the objective of

identifying anomalies. This will improve the quality of fraud detection.

Communicating the system implemented to the staff

For preventing fraud, the company can communicate with its employees about the

system implemented in the organization which will make them aware of it and if they tried to

do any fraud they can be easily caught. This will help in reducing the breaching the control

system and is the best way of prevention.

5. Reflection

Subsequent to evaluation all the 4 above stated questions, I can say that management

accounting is significant from the business point of view. The wide scope of methods and

instruments it has will help the business association in effective decision making. These

techniques are structured so that it will meet the different business prerequisites. Considering

different perspectives before taking decisions, for example, monetary and non-monetary

related viewpoints. The role of stakeholders in a business association is very essential and, in

this manner, appropriate management of them is exceptionally fundamental for the

association. There are two sorts of partners internal and external each having their own points

and objective and on the opposite side is organization which is having its own mission and

vision. Also, the organization is required to meet the needs of its stakeholders in order to run

the business smoothly. Additionally, decisions are taken by understanding the effect of it on

the organization's shareholders else it will influence the investors value. The different

strategies that can be utilized to deal with the expense and increasing the investors' worth

which is helpful for the organization. Misrepresentation and fraud which is the serious issue

that each association is confronting can be decreased or moderated by the application of

different procedures and approaches and furthermore it will help in identifying and detecting

that would have caused it.

Scenario B

Financial ratios analysis of Morrison Supermarkets PLC for the year 2020, 2019 & 2018

Morrisons

2020 2019 2018

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Liquidity ratio

Current assets 1322 1379 1279

Current liability 3396 3349 3080

Inventory 660 713 686

Quick Assets 662 666 593

Current ratio

Current assets /

current liabilities 0.39 0.41 0.42

Quick Ratio

(Current Assets -

Inventory) /

Current Liabilities 0.19 0.20 0.19

Profitability ratio

Employed

Capital 7524 7317 7382

Net operating

profit 521 394 458

Return on

capital

employed

Net operating

profit/Employed

Capital 6.92% 5.38% 6.20%

Net Income 348 244 311

Shareholder's

Equity 4541 4325 4250

Return on

Equity

Net Income /

Shareholder's

Equity 8% 5.64% 7.32%

Cost of Sales 16907 17128 16629

Sales 17536 17735 17262

Gross Margin Total Sales –

COGS/Total Sales 3.59% 3.42% 3.67%

Current assets 1322 1379 1279

Current liability 3396 3349 3080

Inventory 660 713 686

Quick Assets 662 666 593

Current ratio

Current assets /

current liabilities 0.39 0.41 0.42

Quick Ratio

(Current Assets -

Inventory) /

Current Liabilities 0.19 0.20 0.19

Profitability ratio

Employed

Capital 7524 7317 7382

Net operating

profit 521 394 458

Return on

capital

employed

Net operating

profit/Employed

Capital 6.92% 5.38% 6.20%

Net Income 348 244 311

Shareholder's

Equity 4541 4325 4250

Return on

Equity

Net Income /

Shareholder's

Equity 8% 5.64% 7.32%

Cost of Sales 16907 17128 16629

Sales 17536 17735 17262

Gross Margin Total Sales –

COGS/Total Sales 3.59% 3.42% 3.67%

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

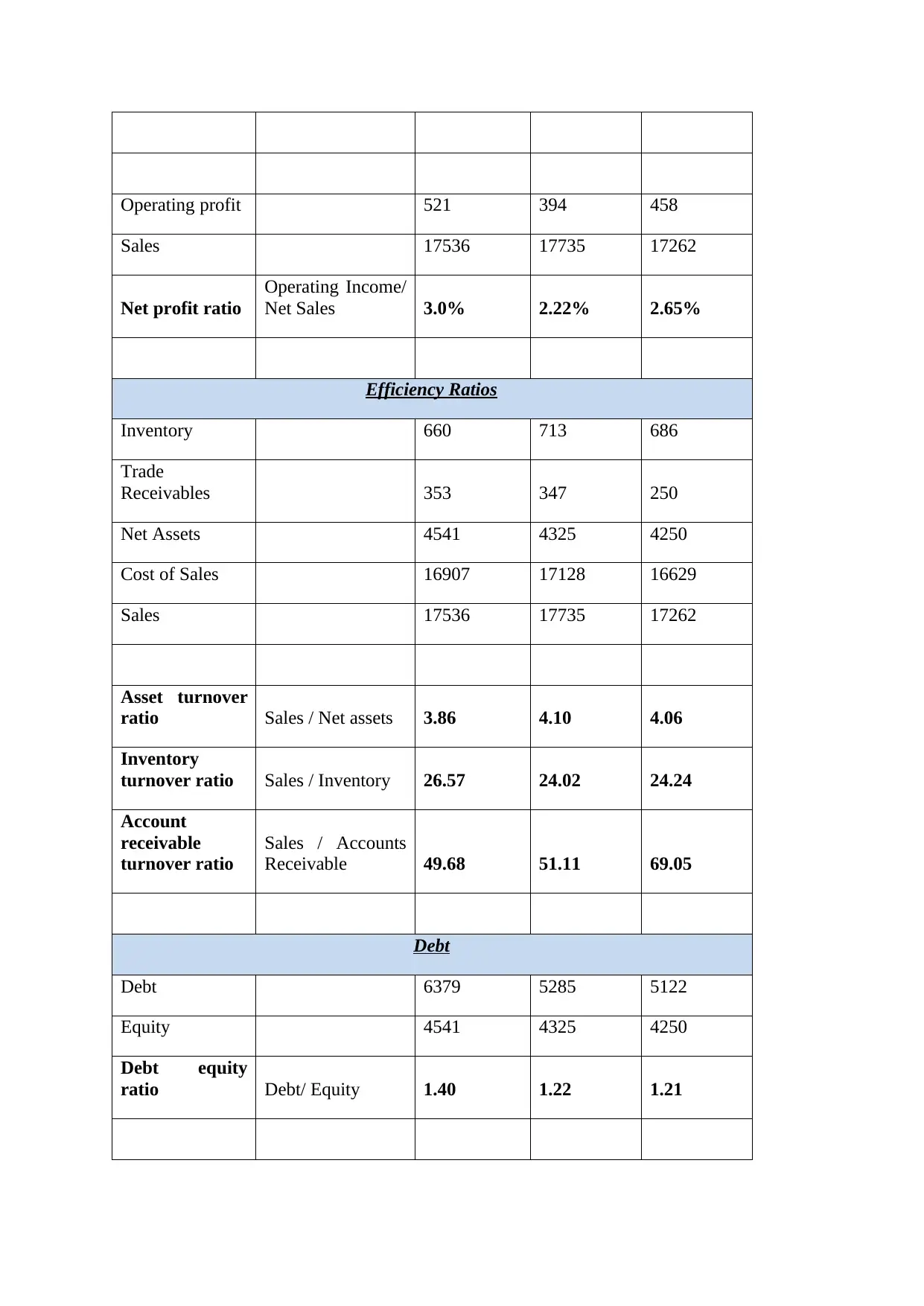

Operating profit 521 394 458

Sales 17536 17735 17262

Net profit ratio

Operating Income/

Net Sales 3.0% 2.22% 2.65%

Efficiency Ratios

Inventory 660 713 686

Trade

Receivables 353 347 250

Net Assets 4541 4325 4250

Cost of Sales 16907 17128 16629

Sales 17536 17735 17262

Asset turnover

ratio Sales / Net assets 3.86 4.10 4.06

Inventory

turnover ratio Sales / Inventory 26.57 24.02 24.24

Account

receivable

turnover ratio

Sales / Accounts

Receivable 49.68 51.11 69.05

Debt

Debt 6379 5285 5122

Equity 4541 4325 4250

Debt equity

ratio Debt/ Equity 1.40 1.22 1.21

Sales 17536 17735 17262

Net profit ratio

Operating Income/

Net Sales 3.0% 2.22% 2.65%

Efficiency Ratios

Inventory 660 713 686

Trade

Receivables 353 347 250

Net Assets 4541 4325 4250

Cost of Sales 16907 17128 16629

Sales 17536 17735 17262

Asset turnover

ratio Sales / Net assets 3.86 4.10 4.06

Inventory

turnover ratio Sales / Inventory 26.57 24.02 24.24

Account

receivable

turnover ratio

Sales / Accounts

Receivable 49.68 51.11 69.05

Debt

Debt 6379 5285 5122

Equity 4541 4325 4250

Debt equity

ratio Debt/ Equity 1.40 1.22 1.21

Analysis and interpretation:

Liquidity ratio

The current ratio of Morrison indicates its ability to meet its short-term liabilities

against the current assets available with the company (Williams and Dobelman, 2017). The

current ratio of Morrison is standing at the 0.42 times in the year 2018 and has further

reduced in 2019 and 2020 to 0.41 and 0.39 times respectively. This depicts that the liquidity

position of the company is not good which is a point of concern for the company as it is

lower than 1.

2018 2019 2020

0.05

0.1

0.15

0.2

0.25

0.3

0.35

0.4

0.19 0.2 0.19

Quick ratio

Quick ratio

The quick ratio takes into account the more liquid assets and excludes inventory and

prepaid expenses. In case of Morrisons the quick ratio has remained more or less the same in

2018 2019 2020

0.15

0.2

0.25

0.3

0.35

0.4

0.45

0.5

0.55

0.42 0.41 0.39

Current ratio

Current ratio

Liquidity ratio

The current ratio of Morrison indicates its ability to meet its short-term liabilities

against the current assets available with the company (Williams and Dobelman, 2017). The

current ratio of Morrison is standing at the 0.42 times in the year 2018 and has further

reduced in 2019 and 2020 to 0.41 and 0.39 times respectively. This depicts that the liquidity

position of the company is not good which is a point of concern for the company as it is

lower than 1.

2018 2019 2020

0.05

0.1

0.15

0.2

0.25

0.3

0.35

0.4

0.19 0.2 0.19

Quick ratio

Quick ratio

The quick ratio takes into account the more liquid assets and excludes inventory and

prepaid expenses. In case of Morrisons the quick ratio has remained more or less the same in

2018 2019 2020

0.15

0.2

0.25

0.3

0.35

0.4

0.45

0.5

0.55

0.42 0.41 0.39

Current ratio

Current ratio

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

these three years and is currently at 0.19 times. It is favourable to have higher ratio which

means that the Morrisons is at the worst situation and is required to manage its current assets

and liabilities effectively.

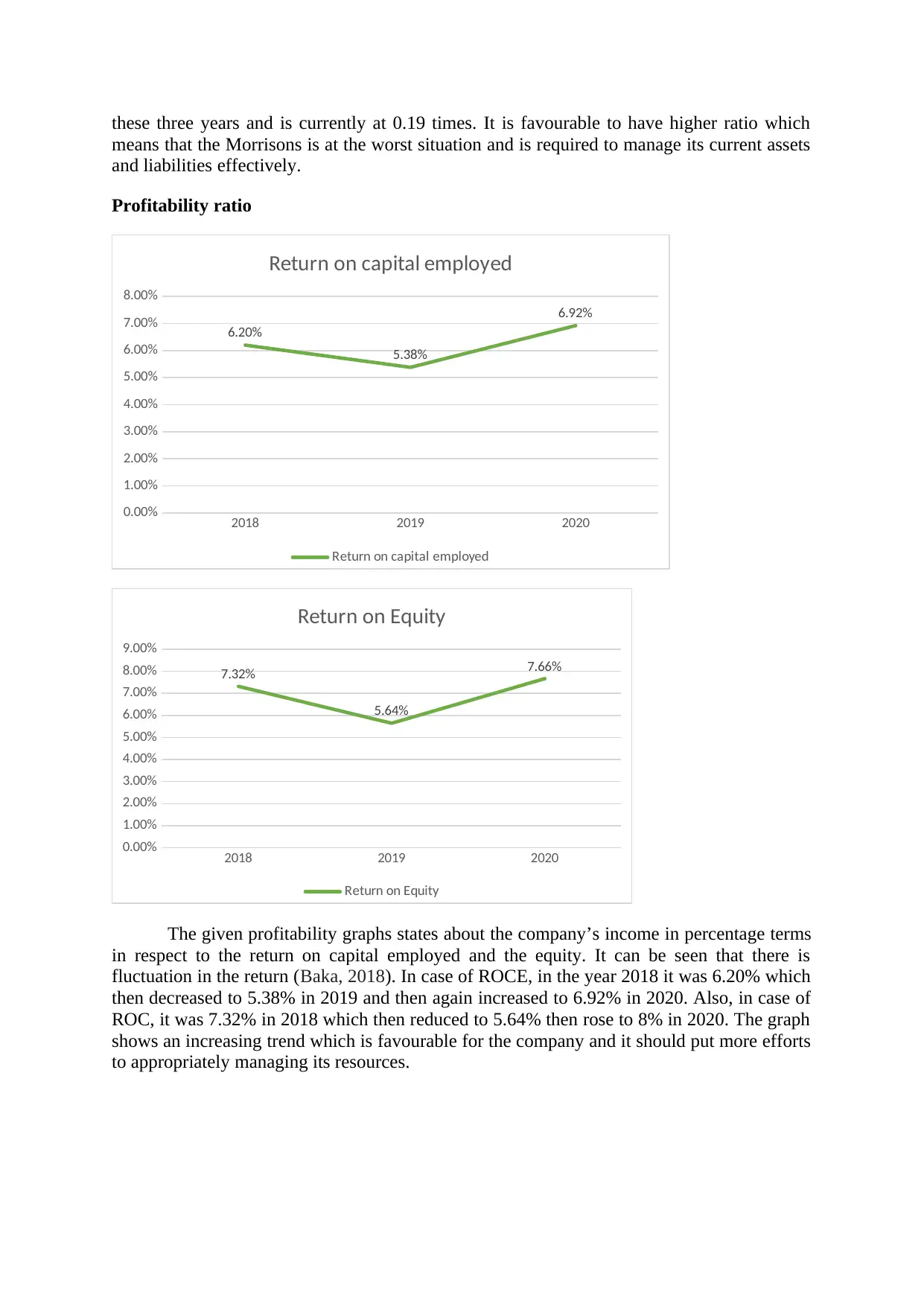

Profitability ratio

2018 2019 2020

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

7.00%

8.00%

6.20%

5.38%

6.92%

Return on capital employed

Return on capital employed

2018 2019 2020

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

7.00%

8.00%

9.00%

7.32%

5.64%

7.66%

Return on Equity

Return on Equity

The given profitability graphs states about the company’s income in percentage terms

in respect to the return on capital employed and the equity. It can be seen that there is

fluctuation in the return (Baka, 2018). In case of ROCE, in the year 2018 it was 6.20% which

then decreased to 5.38% in 2019 and then again increased to 6.92% in 2020. Also, in case of

ROC, it was 7.32% in 2018 which then reduced to 5.64% then rose to 8% in 2020. The graph

shows an increasing trend which is favourable for the company and it should put more efforts

to appropriately managing its resources.

means that the Morrisons is at the worst situation and is required to manage its current assets

and liabilities effectively.

Profitability ratio

2018 2019 2020

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

7.00%

8.00%

6.20%

5.38%

6.92%

Return on capital employed

Return on capital employed

2018 2019 2020

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

7.00%

8.00%

9.00%

7.32%

5.64%

7.66%

Return on Equity

Return on Equity

The given profitability graphs states about the company’s income in percentage terms

in respect to the return on capital employed and the equity. It can be seen that there is

fluctuation in the return (Baka, 2018). In case of ROCE, in the year 2018 it was 6.20% which

then decreased to 5.38% in 2019 and then again increased to 6.92% in 2020. Also, in case of

ROC, it was 7.32% in 2018 which then reduced to 5.64% then rose to 8% in 2020. The graph

shows an increasing trend which is favourable for the company and it should put more efforts

to appropriately managing its resources.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2018 2019 2020

2.50%

2.70%

2.90%

3.10%

3.30%

3.50%

3.70%

3.90%

3.67%

3.42%

3.59%

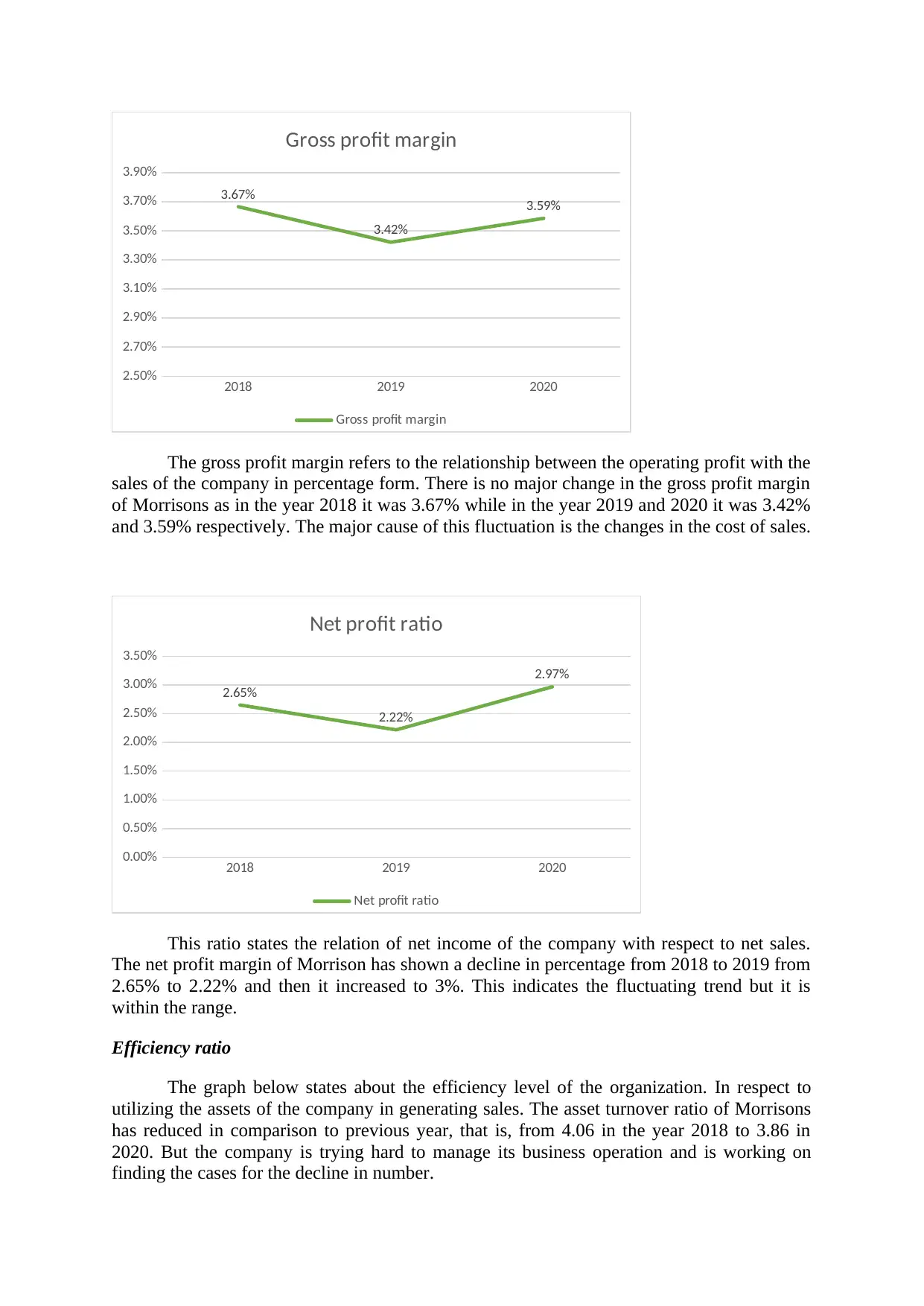

Gross profit margin

Gross profit margin

The gross profit margin refers to the relationship between the operating profit with the

sales of the company in percentage form. There is no major change in the gross profit margin

of Morrisons as in the year 2018 it was 3.67% while in the year 2019 and 2020 it was 3.42%

and 3.59% respectively. The major cause of this fluctuation is the changes in the cost of sales.

2018 2019 2020

0.00%

0.50%

1.00%

1.50%

2.00%

2.50%

3.00%

3.50%

2.65%

2.22%

2.97%

Net profit ratio

Net profit ratio

This ratio states the relation of net income of the company with respect to net sales.

The net profit margin of Morrison has shown a decline in percentage from 2018 to 2019 from

2.65% to 2.22% and then it increased to 3%. This indicates the fluctuating trend but it is

within the range.

Efficiency ratio

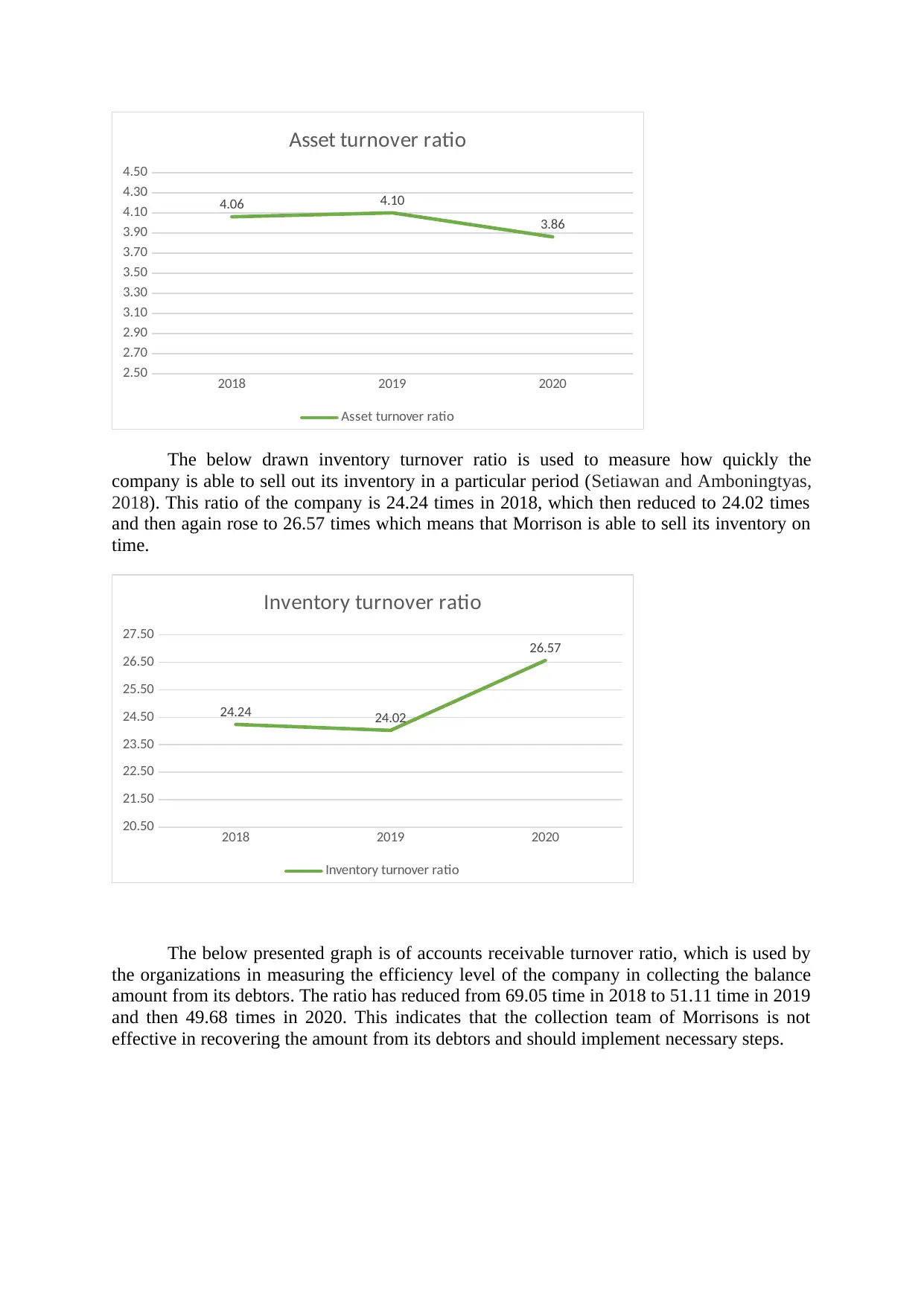

The graph below states about the efficiency level of the organization. In respect to

utilizing the assets of the company in generating sales. The asset turnover ratio of Morrisons

has reduced in comparison to previous year, that is, from 4.06 in the year 2018 to 3.86 in

2020. But the company is trying hard to manage its business operation and is working on

finding the cases for the decline in number.

2.50%

2.70%

2.90%

3.10%

3.30%

3.50%

3.70%

3.90%

3.67%

3.42%

3.59%

Gross profit margin

Gross profit margin

The gross profit margin refers to the relationship between the operating profit with the

sales of the company in percentage form. There is no major change in the gross profit margin

of Morrisons as in the year 2018 it was 3.67% while in the year 2019 and 2020 it was 3.42%

and 3.59% respectively. The major cause of this fluctuation is the changes in the cost of sales.

2018 2019 2020

0.00%

0.50%

1.00%

1.50%

2.00%

2.50%

3.00%

3.50%

2.65%

2.22%

2.97%

Net profit ratio

Net profit ratio

This ratio states the relation of net income of the company with respect to net sales.

The net profit margin of Morrison has shown a decline in percentage from 2018 to 2019 from

2.65% to 2.22% and then it increased to 3%. This indicates the fluctuating trend but it is

within the range.

Efficiency ratio

The graph below states about the efficiency level of the organization. In respect to

utilizing the assets of the company in generating sales. The asset turnover ratio of Morrisons

has reduced in comparison to previous year, that is, from 4.06 in the year 2018 to 3.86 in

2020. But the company is trying hard to manage its business operation and is working on

finding the cases for the decline in number.

2018 2019 2020

2.50

2.70

2.90

3.10

3.30

3.50

3.70

3.90

4.10

4.30

4.50

4.06 4.10

3.86

Asset turnover ratio

Asset turnover ratio

The below drawn inventory turnover ratio is used to measure how quickly the

company is able to sell out its inventory in a particular period (Setiawan and Amboningtyas,

2018). This ratio of the company is 24.24 times in 2018, which then reduced to 24.02 times

and then again rose to 26.57 times which means that Morrison is able to sell its inventory on

time.

2018 2019 2020

20.50

21.50

22.50

23.50

24.50

25.50

26.50

27.50

24.24 24.02

26.57

Inventory turnover ratio

Inventory turnover ratio

The below presented graph is of accounts receivable turnover ratio, which is used by

the organizations in measuring the efficiency level of the company in collecting the balance

amount from its debtors. The ratio has reduced from 69.05 time in 2018 to 51.11 time in 2019

and then 49.68 times in 2020. This indicates that the collection team of Morrisons is not

effective in recovering the amount from its debtors and should implement necessary steps.

2.50

2.70

2.90

3.10

3.30

3.50

3.70

3.90

4.10

4.30

4.50

4.06 4.10

3.86

Asset turnover ratio

Asset turnover ratio

The below drawn inventory turnover ratio is used to measure how quickly the

company is able to sell out its inventory in a particular period (Setiawan and Amboningtyas,

2018). This ratio of the company is 24.24 times in 2018, which then reduced to 24.02 times

and then again rose to 26.57 times which means that Morrison is able to sell its inventory on

time.

2018 2019 2020

20.50

21.50

22.50

23.50

24.50

25.50

26.50

27.50

24.24 24.02

26.57

Inventory turnover ratio

Inventory turnover ratio

The below presented graph is of accounts receivable turnover ratio, which is used by

the organizations in measuring the efficiency level of the company in collecting the balance

amount from its debtors. The ratio has reduced from 69.05 time in 2018 to 51.11 time in 2019

and then 49.68 times in 2020. This indicates that the collection team of Morrisons is not

effective in recovering the amount from its debtors and should implement necessary steps.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.