Analyzing Investment Appraisal Methods & Dividend Policies at Carport

VerifiedAdded on 2023/06/10

|15

|3815

|137

Report

AI Summary

This report provides a detailed analysis of financial management concepts, focusing on investment appraisal methods such as Net Present Value (NPV), Accounting Rate of Return (ARR), and payback period. It includes computations and recommendations for venture choices based on these methods, highlighting the advantages and disadvantages of each. Furthermore, the report assesses Carport Plc's share price under different dividend strategies, including the current policy and an alternative payout strategy proposed by the executive director. The analysis incorporates the dividend discount model and the Gordon growth method to determine the intrinsic value of the company's shares, considering the impact of dividend payments on market rate. This document, contributed by a student, is available on Desklib, a platform offering study tools and resources for students.

Financial management

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

Contents...........................................................................................................................................2

INTRODUCTION...........................................................................................................................1

Question No 1:.................................................................................................................................1

a) Computation of the payback period, NPV, and ARR, as well as advice on venture choice:. .1

b) Each of the numerous evaluation methods has its own set of advantages and disadvantages:

.....................................................................................................................................................5

Question No 3..................................................................................................................................7

a) Computation of Carport Plc's share price if the firm's present dividend strategy is not

changed:.......................................................................................................................................7

b) If the executive director's planned payout strategy is taken into account, the corporation's

shares will be valued at:...............................................................................................................7

c) Rational review of several systems or hypotheses backing and opposing the institution's

dividend payout based on its market rate:...................................................................................8

CONCLUTION.............................................................................................................................10

REFERENCES..............................................................................................................................12

Contents...........................................................................................................................................2

INTRODUCTION...........................................................................................................................1

Question No 1:.................................................................................................................................1

a) Computation of the payback period, NPV, and ARR, as well as advice on venture choice:. .1

b) Each of the numerous evaluation methods has its own set of advantages and disadvantages:

.....................................................................................................................................................5

Question No 3..................................................................................................................................7

a) Computation of Carport Plc's share price if the firm's present dividend strategy is not

changed:.......................................................................................................................................7

b) If the executive director's planned payout strategy is taken into account, the corporation's

shares will be valued at:...............................................................................................................7

c) Rational review of several systems or hypotheses backing and opposing the institution's

dividend payout based on its market rate:...................................................................................8

CONCLUTION.............................................................................................................................10

REFERENCES..............................................................................................................................12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Finance administration is the organisational function concerned with the planning and

monitoring of a company's fiscal assets (Arifin, Kevin and Siswanto, 2017). In other words, it's

far concerned with purchasing, funding, and managing assets in order to achieve an

organization's overall goal (most notably, to maximise value of stockholders). In addition to

identifying the business, investing evaluation methodologies were used in this study. NPV, ARR,

and payback period are the methodologies which have been used. Following the use of all of

these aforementioned approaches, a suggestion was provided as to which way is most practical

for the business, as well as the proposal decision. Another topic discussed in the document is the

assessment of Carport Plc in light of the company's current payout strategy. The marketplace

value was also assessed from the perspective of the chief executive. At the conclusion of the

paper, the ideas were addressed in terms of the implications on marketplace rate whenever a

corporation pays or does not pay a premium.

Question No 1:

a) Computation of the payback period, NPV, and ARR, as well as advice on venture choice:

Payback Period: This technique illustrates how long it will take for the planned initiative to

recoup the company's beginning expenditure. This strategy aids in determining how long it

would take for the company to begin making earnings for its shareholders (Arsen and DeLuca,

2016). The choice is made depending on the program's duration, and the venture with the

shortest payback period is chosen. The following is the method for determining the payback

period:

Payback Period = Initial Investment / Cash flows per year

The following is a breakdown of the payback period calculations for Program A and Program B:

Project A: (Figures in £)

Years Cash Flows Cumulative Cash Flows

0 -190000 -190000

1 55000 -135000

2 40000 -95000

3 25000 -70000

4 10000 -60000

Finance administration is the organisational function concerned with the planning and

monitoring of a company's fiscal assets (Arifin, Kevin and Siswanto, 2017). In other words, it's

far concerned with purchasing, funding, and managing assets in order to achieve an

organization's overall goal (most notably, to maximise value of stockholders). In addition to

identifying the business, investing evaluation methodologies were used in this study. NPV, ARR,

and payback period are the methodologies which have been used. Following the use of all of

these aforementioned approaches, a suggestion was provided as to which way is most practical

for the business, as well as the proposal decision. Another topic discussed in the document is the

assessment of Carport Plc in light of the company's current payout strategy. The marketplace

value was also assessed from the perspective of the chief executive. At the conclusion of the

paper, the ideas were addressed in terms of the implications on marketplace rate whenever a

corporation pays or does not pay a premium.

Question No 1:

a) Computation of the payback period, NPV, and ARR, as well as advice on venture choice:

Payback Period: This technique illustrates how long it will take for the planned initiative to

recoup the company's beginning expenditure. This strategy aids in determining how long it

would take for the company to begin making earnings for its shareholders (Arsen and DeLuca,

2016). The choice is made depending on the program's duration, and the venture with the

shortest payback period is chosen. The following is the method for determining the payback

period:

Payback Period = Initial Investment / Cash flows per year

The following is a breakdown of the payback period calculations for Program A and Program B:

Project A: (Figures in £)

Years Cash Flows Cumulative Cash Flows

0 -190000 -190000

1 55000 -135000

2 40000 -95000

3 25000 -70000

4 10000 -60000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4 50000 -10000

The payback period for Project A is longer than 4 years, because the starting expenditure

is not entirely returned even at the conclusion of the fourth year.

Project B: (Figures in £)

Years Cash Flows Cumulative Cash Flows

0 -170000 -170000

1 15000 -155000

2 25000 -130000

3 45000 -85000

4 65000 -20000

4 20000 Nil

The payback period for Program B was 4 years, because the original outlay of 170000

was completely repaid at the conclusion of the fourth year, and no more revenue was given in

that year.

Recommendation: After using the Payback Period Technique, it was determined that

Program B is the better option for the firm because it generates cash flows at the conclusion of

the fourth year, but Program A does not recoup the entire investment until the fifth year. Only

188000 were found in the endeavour, with 10,000 still outstanding (Bastani and Bayati, 2020).

Net Present Value: Because it analyses the temporal worth of capital, the NPV approach

is among the finest in investing assessment approach and is strongly suggested. The business

would be chosen based on its greater NPV, as it is more profitable for the firm to engage in that

initiative alone. The accompanying data shows the NPV calculations for Projects A and B, as

well as the conclusions reached on their choice. The method for determining net present value is

as follows:

Net Present Value = (Present Value of Cash Inflows – Present Value of Cash Outflows)

Project A: (Figures in £)

Years Cash flows Discount Factor @

10 %

Present Value of

Cash Inflows

1 55000 .909 49995

2 40000 .826 33040

The payback period for Project A is longer than 4 years, because the starting expenditure

is not entirely returned even at the conclusion of the fourth year.

Project B: (Figures in £)

Years Cash Flows Cumulative Cash Flows

0 -170000 -170000

1 15000 -155000

2 25000 -130000

3 45000 -85000

4 65000 -20000

4 20000 Nil

The payback period for Program B was 4 years, because the original outlay of 170000

was completely repaid at the conclusion of the fourth year, and no more revenue was given in

that year.

Recommendation: After using the Payback Period Technique, it was determined that

Program B is the better option for the firm because it generates cash flows at the conclusion of

the fourth year, but Program A does not recoup the entire investment until the fifth year. Only

188000 were found in the endeavour, with 10,000 still outstanding (Bastani and Bayati, 2020).

Net Present Value: Because it analyses the temporal worth of capital, the NPV approach

is among the finest in investing assessment approach and is strongly suggested. The business

would be chosen based on its greater NPV, as it is more profitable for the firm to engage in that

initiative alone. The accompanying data shows the NPV calculations for Projects A and B, as

well as the conclusions reached on their choice. The method for determining net present value is

as follows:

Net Present Value = (Present Value of Cash Inflows – Present Value of Cash Outflows)

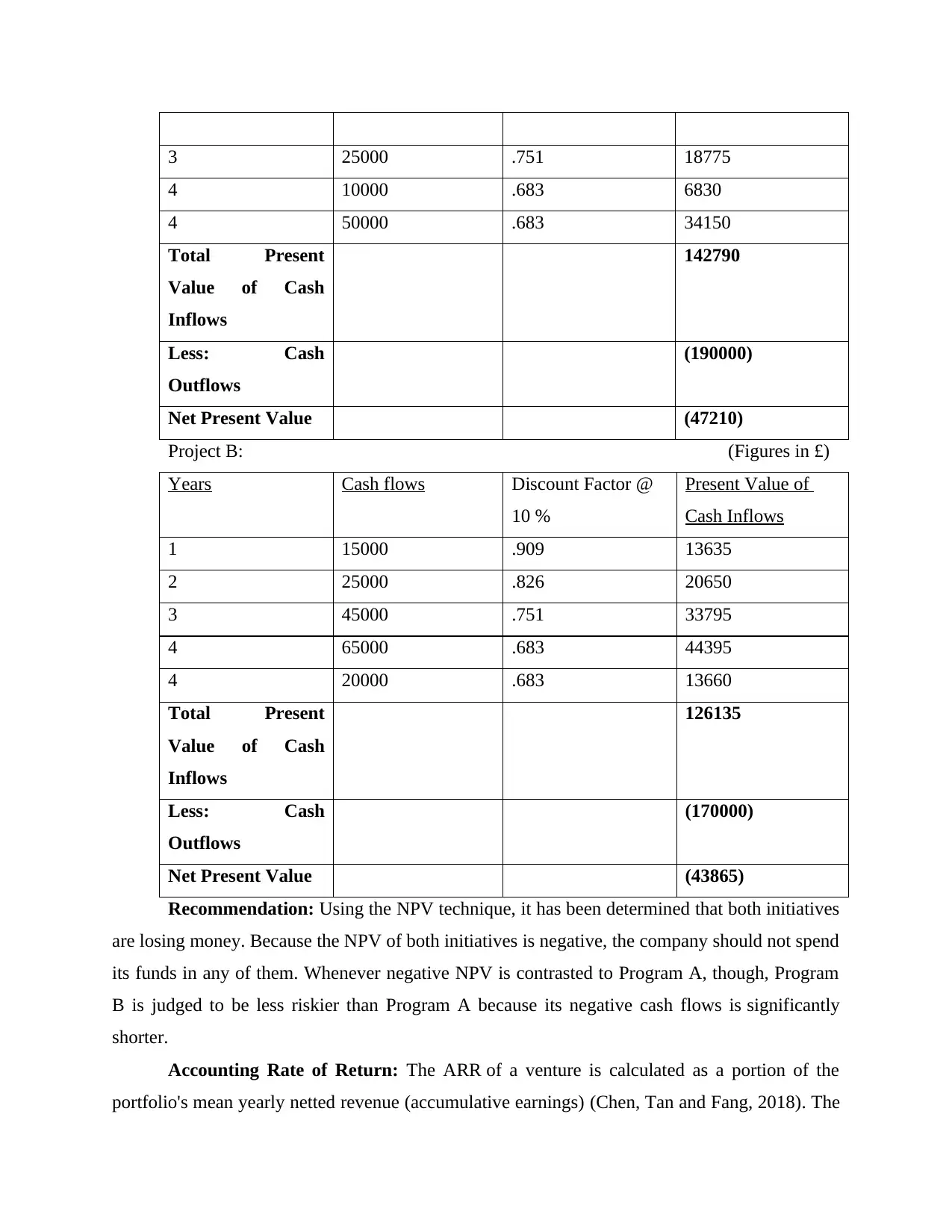

Project A: (Figures in £)

Years Cash flows Discount Factor @

10 %

Present Value of

Cash Inflows

1 55000 .909 49995

2 40000 .826 33040

3 25000 .751 18775

4 10000 .683 6830

4 50000 .683 34150

Total Present

Value of Cash

Inflows

142790

Less: Cash

Outflows

(190000)

Net Present Value (47210)

Project B: (Figures in £)

Years Cash flows Discount Factor @

10 %

Present Value of

Cash Inflows

1 15000 .909 13635

2 25000 .826 20650

3 45000 .751 33795

4 65000 .683 44395

4 20000 .683 13660

Total Present

Value of Cash

Inflows

126135

Less: Cash

Outflows

(170000)

Net Present Value (43865)

Recommendation: Using the NPV technique, it has been determined that both initiatives

are losing money. Because the NPV of both initiatives is negative, the company should not spend

its funds in any of them. Whenever negative NPV is contrasted to Program A, though, Program

B is judged to be less riskier than Program A because its negative cash flows is significantly

shorter.

Accounting Rate of Return: The ARR of a venture is calculated as a portion of the

portfolio's mean yearly netted revenue (accumulative earnings) (Chen, Tan and Fang, 2018). The

4 10000 .683 6830

4 50000 .683 34150

Total Present

Value of Cash

Inflows

142790

Less: Cash

Outflows

(190000)

Net Present Value (47210)

Project B: (Figures in £)

Years Cash flows Discount Factor @

10 %

Present Value of

Cash Inflows

1 15000 .909 13635

2 25000 .826 20650

3 45000 .751 33795

4 65000 .683 44395

4 20000 .683 13660

Total Present

Value of Cash

Inflows

126135

Less: Cash

Outflows

(170000)

Net Present Value (43865)

Recommendation: Using the NPV technique, it has been determined that both initiatives

are losing money. Because the NPV of both initiatives is negative, the company should not spend

its funds in any of them. Whenever negative NPV is contrasted to Program A, though, Program

B is judged to be less riskier than Program A because its negative cash flows is significantly

shorter.

Accounting Rate of Return: The ARR of a venture is calculated as a portion of the

portfolio's mean yearly netted revenue (accumulative earnings) (Chen, Tan and Fang, 2018). The

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

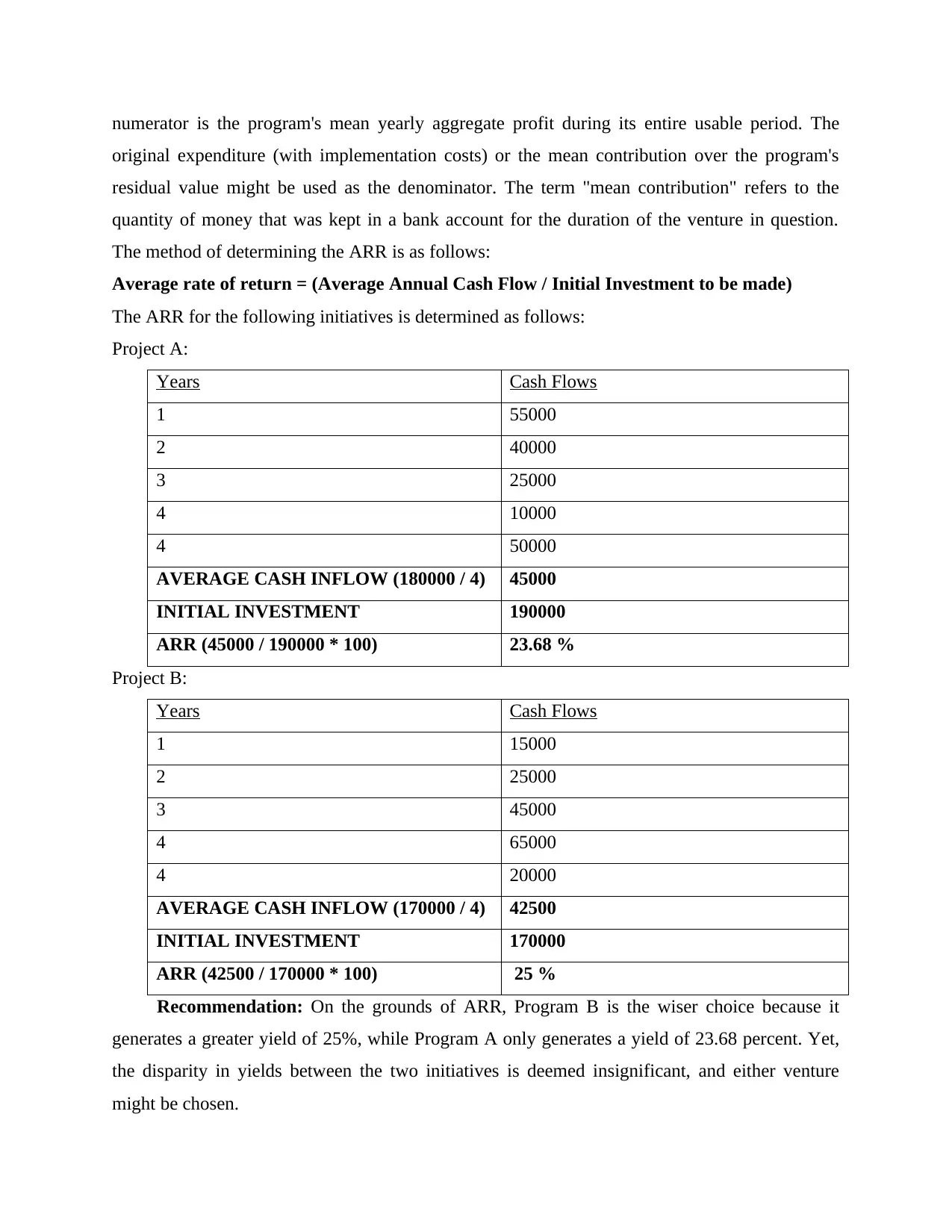

numerator is the program's mean yearly aggregate profit during its entire usable period. The

original expenditure (with implementation costs) or the mean contribution over the program's

residual value might be used as the denominator. The term "mean contribution" refers to the

quantity of money that was kept in a bank account for the duration of the venture in question.

The method of determining the ARR is as follows:

Average rate of return = (Average Annual Cash Flow / Initial Investment to be made)

The ARR for the following initiatives is determined as follows:

Project A:

Years Cash Flows

1 55000

2 40000

3 25000

4 10000

4 50000

AVERAGE CASH INFLOW (180000 / 4) 45000

INITIAL INVESTMENT 190000

ARR (45000 / 190000 * 100) 23.68 %

Project B:

Years Cash Flows

1 15000

2 25000

3 45000

4 65000

4 20000

AVERAGE CASH INFLOW (170000 / 4) 42500

INITIAL INVESTMENT 170000

ARR (42500 / 170000 * 100) 25 %

Recommendation: On the grounds of ARR, Program B is the wiser choice because it

generates a greater yield of 25%, while Program A only generates a yield of 23.68 percent. Yet,

the disparity in yields between the two initiatives is deemed insignificant, and either venture

might be chosen.

original expenditure (with implementation costs) or the mean contribution over the program's

residual value might be used as the denominator. The term "mean contribution" refers to the

quantity of money that was kept in a bank account for the duration of the venture in question.

The method of determining the ARR is as follows:

Average rate of return = (Average Annual Cash Flow / Initial Investment to be made)

The ARR for the following initiatives is determined as follows:

Project A:

Years Cash Flows

1 55000

2 40000

3 25000

4 10000

4 50000

AVERAGE CASH INFLOW (180000 / 4) 45000

INITIAL INVESTMENT 190000

ARR (45000 / 190000 * 100) 23.68 %

Project B:

Years Cash Flows

1 15000

2 25000

3 45000

4 65000

4 20000

AVERAGE CASH INFLOW (170000 / 4) 42500

INITIAL INVESTMENT 170000

ARR (42500 / 170000 * 100) 25 %

Recommendation: On the grounds of ARR, Program B is the wiser choice because it

generates a greater yield of 25%, while Program A only generates a yield of 23.68 percent. Yet,

the disparity in yields between the two initiatives is deemed insignificant, and either venture

might be chosen.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

b) Each of the numerous evaluation methods has its own set of advantages and disadvantages:

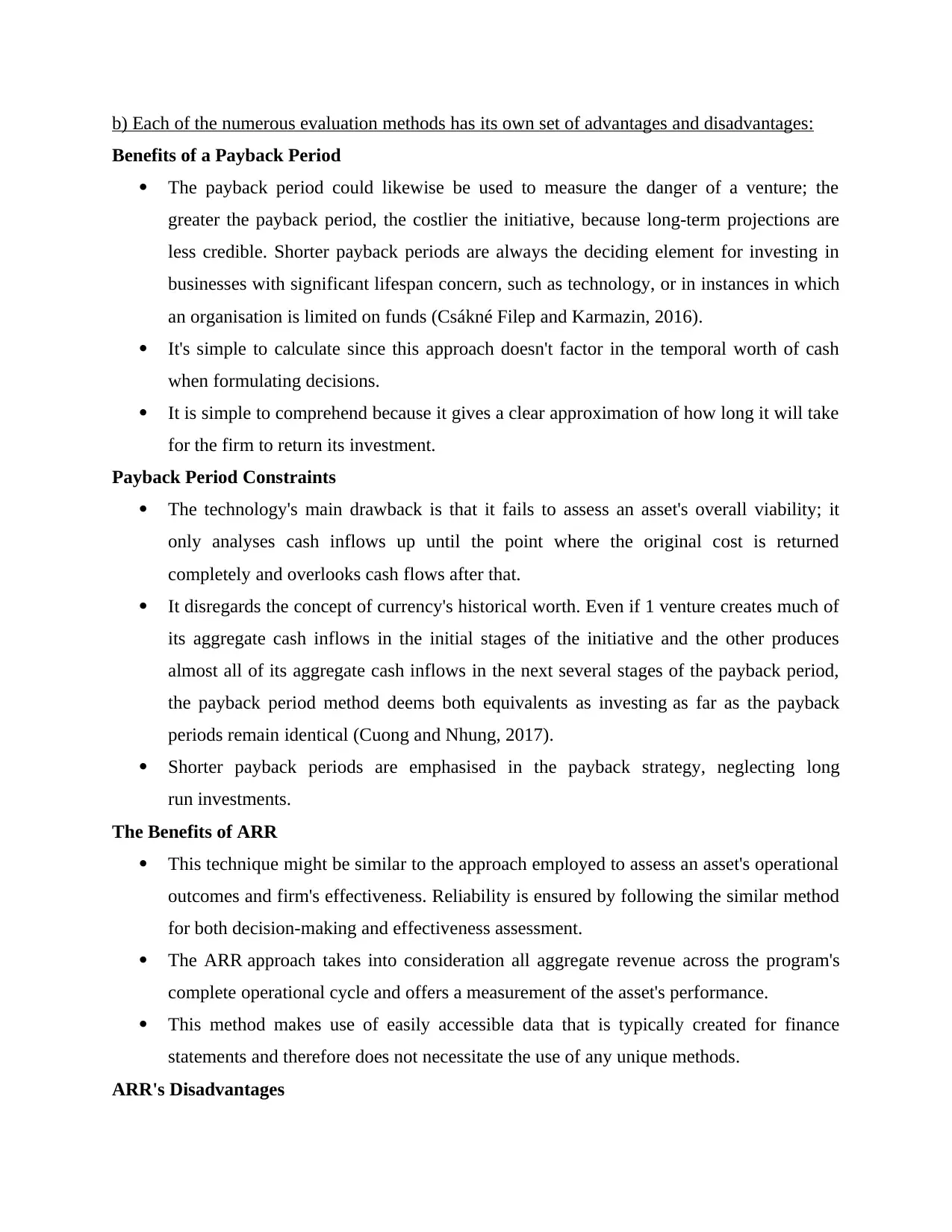

Benefits of a Payback Period

The payback period could likewise be used to measure the danger of a venture; the

greater the payback period, the costlier the initiative, because long-term projections are

less credible. Shorter payback periods are always the deciding element for investing in

businesses with significant lifespan concern, such as technology, or in instances in which

an organisation is limited on funds (Csákné Filep and Karmazin, 2016).

It's simple to calculate since this approach doesn't factor in the temporal worth of cash

when formulating decisions.

It is simple to comprehend because it gives a clear approximation of how long it will take

for the firm to return its investment.

Payback Period Constraints

The technology's main drawback is that it fails to assess an asset's overall viability; it

only analyses cash inflows up until the point where the original cost is returned

completely and overlooks cash flows after that.

It disregards the concept of currency's historical worth. Even if 1 venture creates much of

its aggregate cash inflows in the initial stages of the initiative and the other produces

almost all of its aggregate cash inflows in the next several stages of the payback period,

the payback period method deems both equivalents as investing as far as the payback

periods remain identical (Cuong and Nhung, 2017).

Shorter payback periods are emphasised in the payback strategy, neglecting long

run investments.

The Benefits of ARR

This technique might be similar to the approach employed to assess an asset's operational

outcomes and firm's effectiveness. Reliability is ensured by following the similar method

for both decision-making and effectiveness assessment.

The ARR approach takes into consideration all aggregate revenue across the program's

complete operational cycle and offers a measurement of the asset's performance.

This method makes use of easily accessible data that is typically created for finance

statements and therefore does not necessitate the use of any unique methods.

ARR's Disadvantages

Benefits of a Payback Period

The payback period could likewise be used to measure the danger of a venture; the

greater the payback period, the costlier the initiative, because long-term projections are

less credible. Shorter payback periods are always the deciding element for investing in

businesses with significant lifespan concern, such as technology, or in instances in which

an organisation is limited on funds (Csákné Filep and Karmazin, 2016).

It's simple to calculate since this approach doesn't factor in the temporal worth of cash

when formulating decisions.

It is simple to comprehend because it gives a clear approximation of how long it will take

for the firm to return its investment.

Payback Period Constraints

The technology's main drawback is that it fails to assess an asset's overall viability; it

only analyses cash inflows up until the point where the original cost is returned

completely and overlooks cash flows after that.

It disregards the concept of currency's historical worth. Even if 1 venture creates much of

its aggregate cash inflows in the initial stages of the initiative and the other produces

almost all of its aggregate cash inflows in the next several stages of the payback period,

the payback period method deems both equivalents as investing as far as the payback

periods remain identical (Cuong and Nhung, 2017).

Shorter payback periods are emphasised in the payback strategy, neglecting long

run investments.

The Benefits of ARR

This technique might be similar to the approach employed to assess an asset's operational

outcomes and firm's effectiveness. Reliability is ensured by following the similar method

for both decision-making and effectiveness assessment.

The ARR approach takes into consideration all aggregate revenue across the program's

complete operational cycle and offers a measurement of the asset's performance.

This method makes use of easily accessible data that is typically created for finance

statements and therefore does not necessitate the use of any unique methods.

ARR's Disadvantages

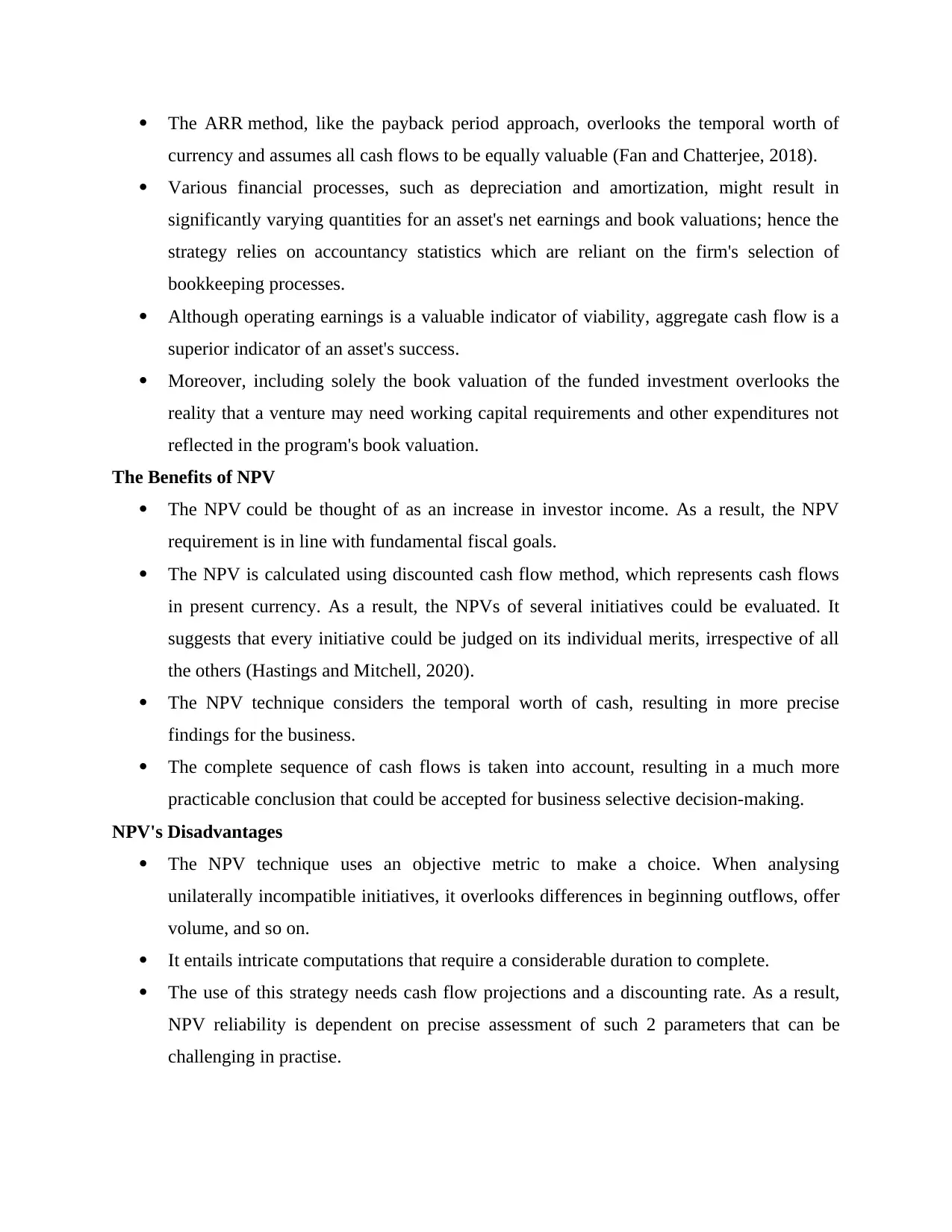

The ARR method, like the payback period approach, overlooks the temporal worth of

currency and assumes all cash flows to be equally valuable (Fan and Chatterjee, 2018).

Various financial processes, such as depreciation and amortization, might result in

significantly varying quantities for an asset's net earnings and book valuations; hence the

strategy relies on accountancy statistics which are reliant on the firm's selection of

bookkeeping processes.

Although operating earnings is a valuable indicator of viability, aggregate cash flow is a

superior indicator of an asset's success.

Moreover, including solely the book valuation of the funded investment overlooks the

reality that a venture may need working capital requirements and other expenditures not

reflected in the program's book valuation.

The Benefits of NPV

The NPV could be thought of as an increase in investor income. As a result, the NPV

requirement is in line with fundamental fiscal goals.

The NPV is calculated using discounted cash flow method, which represents cash flows

in present currency. As a result, the NPVs of several initiatives could be evaluated. It

suggests that every initiative could be judged on its individual merits, irrespective of all

the others (Hastings and Mitchell, 2020).

The NPV technique considers the temporal worth of cash, resulting in more precise

findings for the business.

The complete sequence of cash flows is taken into account, resulting in a much more

practicable conclusion that could be accepted for business selective decision-making.

NPV's Disadvantages

The NPV technique uses an objective metric to make a choice. When analysing

unilaterally incompatible initiatives, it overlooks differences in beginning outflows, offer

volume, and so on.

It entails intricate computations that require a considerable duration to complete.

The use of this strategy needs cash flow projections and a discounting rate. As a result,

NPV reliability is dependent on precise assessment of such 2 parameters that can be

challenging in practise.

currency and assumes all cash flows to be equally valuable (Fan and Chatterjee, 2018).

Various financial processes, such as depreciation and amortization, might result in

significantly varying quantities for an asset's net earnings and book valuations; hence the

strategy relies on accountancy statistics which are reliant on the firm's selection of

bookkeeping processes.

Although operating earnings is a valuable indicator of viability, aggregate cash flow is a

superior indicator of an asset's success.

Moreover, including solely the book valuation of the funded investment overlooks the

reality that a venture may need working capital requirements and other expenditures not

reflected in the program's book valuation.

The Benefits of NPV

The NPV could be thought of as an increase in investor income. As a result, the NPV

requirement is in line with fundamental fiscal goals.

The NPV is calculated using discounted cash flow method, which represents cash flows

in present currency. As a result, the NPVs of several initiatives could be evaluated. It

suggests that every initiative could be judged on its individual merits, irrespective of all

the others (Hastings and Mitchell, 2020).

The NPV technique considers the temporal worth of cash, resulting in more precise

findings for the business.

The complete sequence of cash flows is taken into account, resulting in a much more

practicable conclusion that could be accepted for business selective decision-making.

NPV's Disadvantages

The NPV technique uses an objective metric to make a choice. When analysing

unilaterally incompatible initiatives, it overlooks differences in beginning outflows, offer

volume, and so on.

It entails intricate computations that require a considerable duration to complete.

The use of this strategy needs cash flow projections and a discounting rate. As a result,

NPV reliability is dependent on precise assessment of such 2 parameters that can be

challenging in practise.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Question No 3

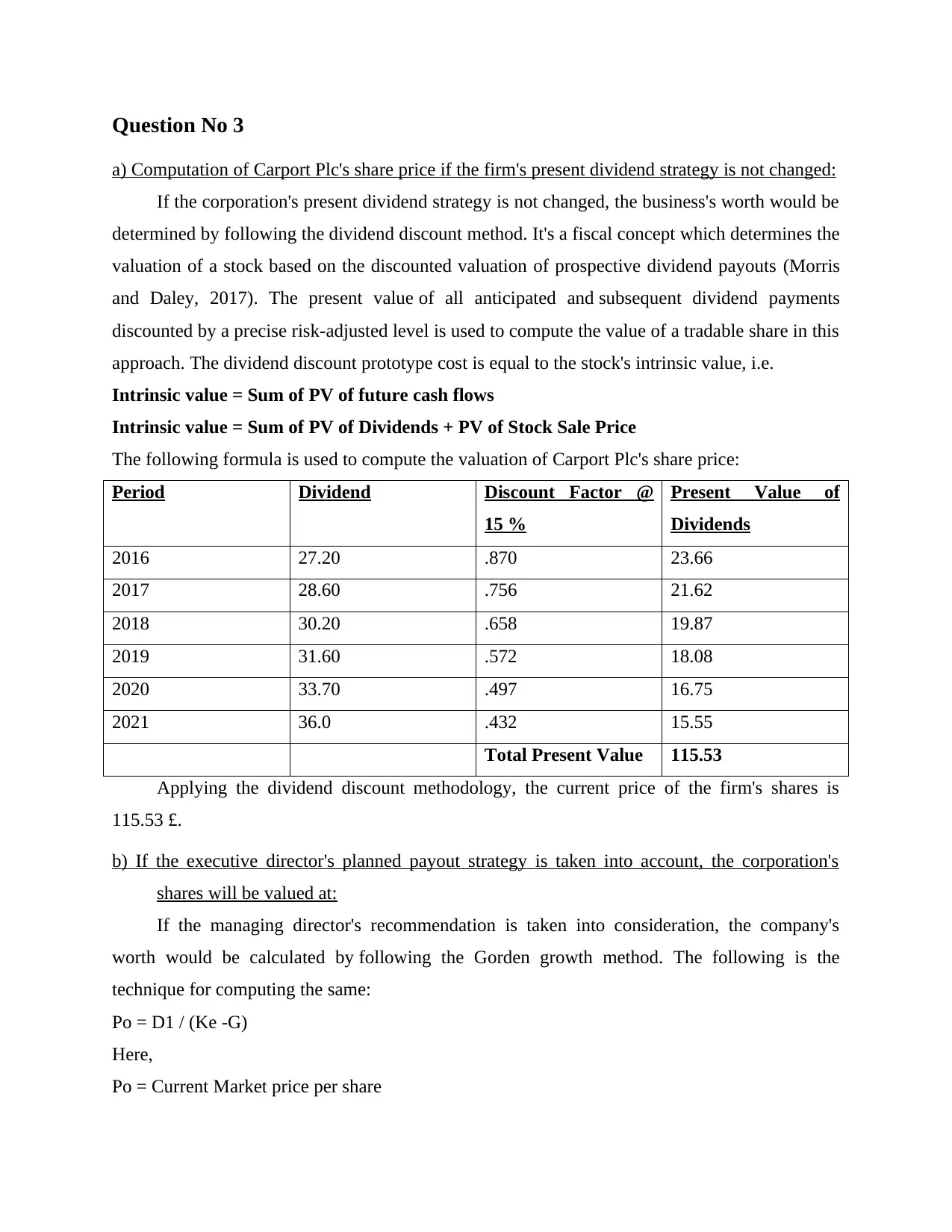

a) Computation of Carport Plc's share price if the firm's present dividend strategy is not changed:

If the corporation's present dividend strategy is not changed, the business's worth would be

determined by following the dividend discount method. It's a fiscal concept which determines the

valuation of a stock based on the discounted valuation of prospective dividend payouts (Morris

and Daley, 2017). The present value of all anticipated and subsequent dividend payments

discounted by a precise risk-adjusted level is used to compute the value of a tradable share in this

approach. The dividend discount prototype cost is equal to the stock's intrinsic value, i.e.

Intrinsic value = Sum of PV of future cash flows

Intrinsic value = Sum of PV of Dividends + PV of Stock Sale Price

The following formula is used to compute the valuation of Carport Plc's share price:

Period Dividend Discount Factor @

15 %

Present Value of

Dividends

2016 27.20 .870 23.66

2017 28.60 .756 21.62

2018 30.20 .658 19.87

2019 31.60 .572 18.08

2020 33.70 .497 16.75

2021 36.0 .432 15.55

Total Present Value 115.53

Applying the dividend discount methodology, the current price of the firm's shares is

115.53 £.

b) If the executive director's planned payout strategy is taken into account, the corporation's

shares will be valued at:

If the managing director's recommendation is taken into consideration, the company's

worth would be calculated by following the Gorden growth method. The following is the

technique for computing the same:

Po = D1 / (Ke -G)

Here,

Po = Current Market price per share

a) Computation of Carport Plc's share price if the firm's present dividend strategy is not changed:

If the corporation's present dividend strategy is not changed, the business's worth would be

determined by following the dividend discount method. It's a fiscal concept which determines the

valuation of a stock based on the discounted valuation of prospective dividend payouts (Morris

and Daley, 2017). The present value of all anticipated and subsequent dividend payments

discounted by a precise risk-adjusted level is used to compute the value of a tradable share in this

approach. The dividend discount prototype cost is equal to the stock's intrinsic value, i.e.

Intrinsic value = Sum of PV of future cash flows

Intrinsic value = Sum of PV of Dividends + PV of Stock Sale Price

The following formula is used to compute the valuation of Carport Plc's share price:

Period Dividend Discount Factor @

15 %

Present Value of

Dividends

2016 27.20 .870 23.66

2017 28.60 .756 21.62

2018 30.20 .658 19.87

2019 31.60 .572 18.08

2020 33.70 .497 16.75

2021 36.0 .432 15.55

Total Present Value 115.53

Applying the dividend discount methodology, the current price of the firm's shares is

115.53 £.

b) If the executive director's planned payout strategy is taken into account, the corporation's

shares will be valued at:

If the managing director's recommendation is taken into consideration, the company's

worth would be calculated by following the Gorden growth method. The following is the

technique for computing the same:

Po = D1 / (Ke -G)

Here,

Po = Current Market price per share

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

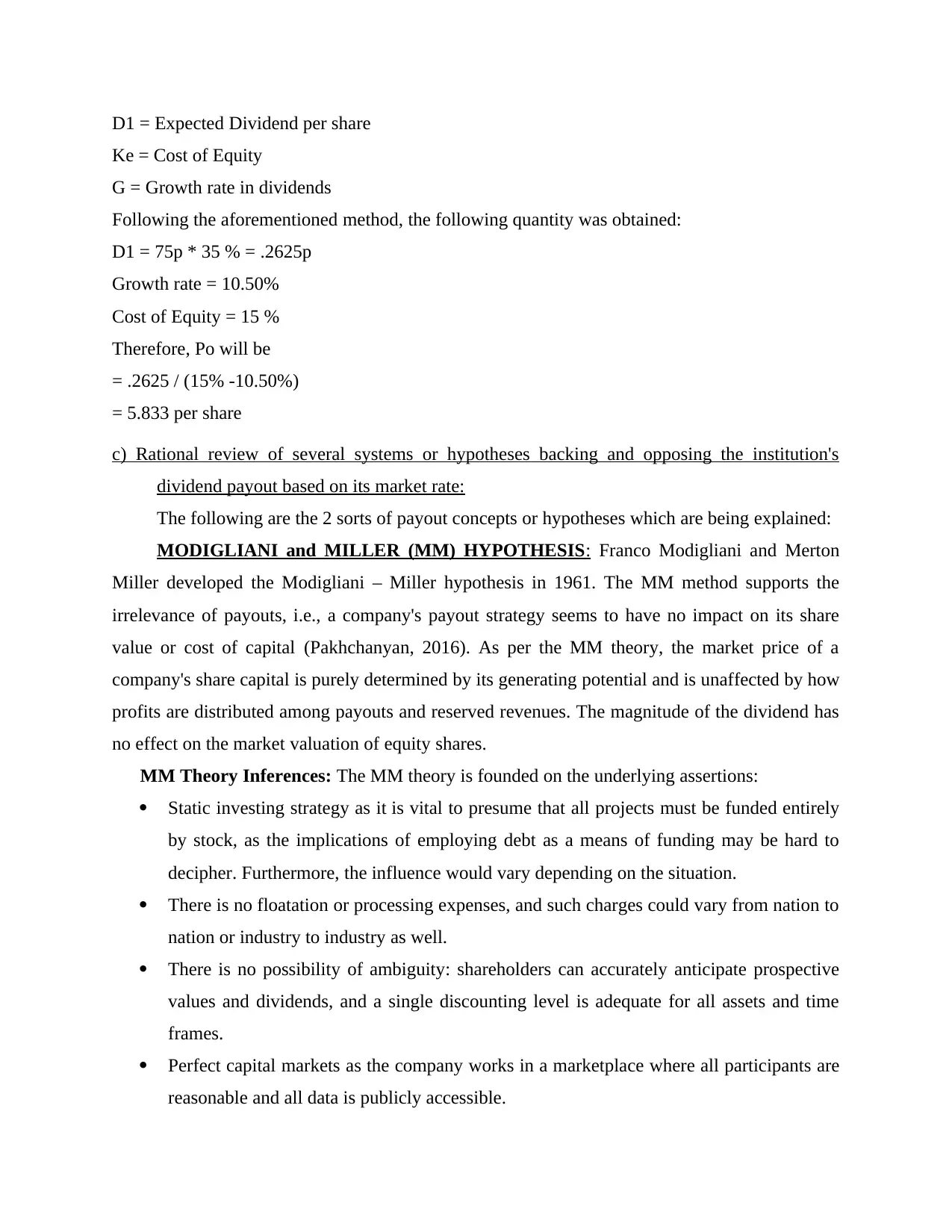

D1 = Expected Dividend per share

Ke = Cost of Equity

G = Growth rate in dividends

Following the aforementioned method, the following quantity was obtained:

D1 = 75p * 35 % = .2625p

Growth rate = 10.50%

Cost of Equity = 15 %

Therefore, Po will be

= .2625 / (15% -10.50%)

= 5.833 per share

c) Rational review of several systems or hypotheses backing and opposing the institution's

dividend payout based on its market rate:

The following are the 2 sorts of payout concepts or hypotheses which are being explained:

MODIGLIANI and MILLER (MM) HYPOTHESIS: Franco Modigliani and Merton

Miller developed the Modigliani – Miller hypothesis in 1961. The MM method supports the

irrelevance of payouts, i.e., a company's payout strategy seems to have no impact on its share

value or cost of capital (Pakhchanyan, 2016). As per the MM theory, the market price of a

company's share capital is purely determined by its generating potential and is unaffected by how

profits are distributed among payouts and reserved revenues. The magnitude of the dividend has

no effect on the market valuation of equity shares.

MM Theory Inferences: The MM theory is founded on the underlying assertions:

Static investing strategy as it is vital to presume that all projects must be funded entirely

by stock, as the implications of employing debt as a means of funding may be hard to

decipher. Furthermore, the influence would vary depending on the situation.

There is no floatation or processing expenses, and such charges could vary from nation to

nation or industry to industry as well.

There is no possibility of ambiguity: shareholders can accurately anticipate prospective

values and dividends, and a single discounting level is adequate for all assets and time

frames.

Perfect capital markets as the company works in a marketplace where all participants are

reasonable and all data is publicly accessible.

Ke = Cost of Equity

G = Growth rate in dividends

Following the aforementioned method, the following quantity was obtained:

D1 = 75p * 35 % = .2625p

Growth rate = 10.50%

Cost of Equity = 15 %

Therefore, Po will be

= .2625 / (15% -10.50%)

= 5.833 per share

c) Rational review of several systems or hypotheses backing and opposing the institution's

dividend payout based on its market rate:

The following are the 2 sorts of payout concepts or hypotheses which are being explained:

MODIGLIANI and MILLER (MM) HYPOTHESIS: Franco Modigliani and Merton

Miller developed the Modigliani – Miller hypothesis in 1961. The MM method supports the

irrelevance of payouts, i.e., a company's payout strategy seems to have no impact on its share

value or cost of capital (Pakhchanyan, 2016). As per the MM theory, the market price of a

company's share capital is purely determined by its generating potential and is unaffected by how

profits are distributed among payouts and reserved revenues. The magnitude of the dividend has

no effect on the market valuation of equity shares.

MM Theory Inferences: The MM theory is founded on the underlying assertions:

Static investing strategy as it is vital to presume that all projects must be funded entirely

by stock, as the implications of employing debt as a means of funding may be hard to

decipher. Furthermore, the influence would vary depending on the situation.

There is no floatation or processing expenses, and such charges could vary from nation to

nation or industry to industry as well.

There is no possibility of ambiguity: shareholders can accurately anticipate prospective

values and dividends, and a single discounting level is adequate for all assets and time

frames.

Perfect capital markets as the company works in a marketplace where all participants are

reasonable and all data is publicly accessible.

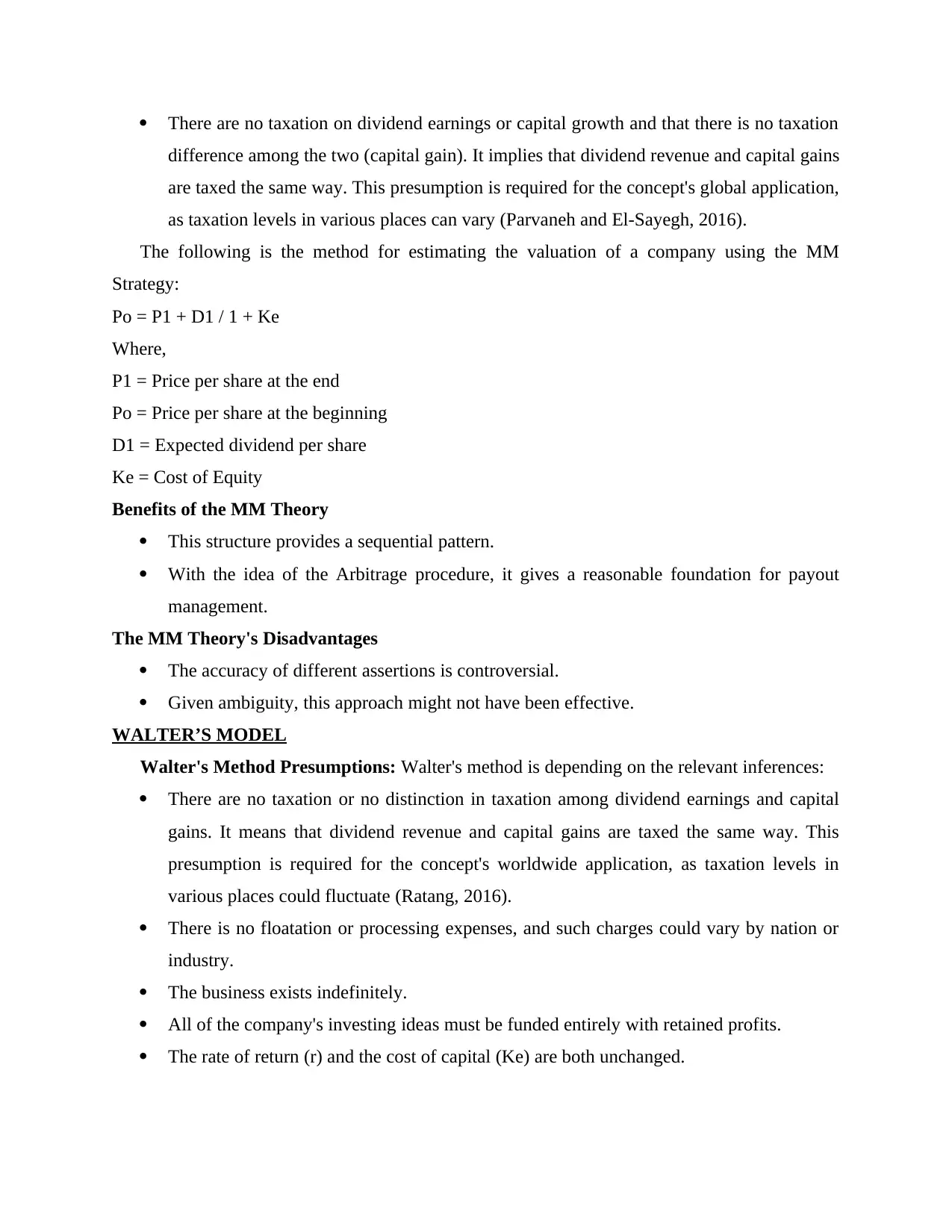

There are no taxation on dividend earnings or capital growth and that there is no taxation

difference among the two (capital gain). It implies that dividend revenue and capital gains

are taxed the same way. This presumption is required for the concept's global application,

as taxation levels in various places can vary (Parvaneh and El-Sayegh, 2016).

The following is the method for estimating the valuation of a company using the MM

Strategy:

Po = P1 + D1 / 1 + Ke

Where,

P1 = Price per share at the end

Po = Price per share at the beginning

D1 = Expected dividend per share

Ke = Cost of Equity

Benefits of the MM Theory

This structure provides a sequential pattern.

With the idea of the Arbitrage procedure, it gives a reasonable foundation for payout

management.

The MM Theory's Disadvantages

The accuracy of different assertions is controversial.

Given ambiguity, this approach might not have been effective.

WALTER’S MODEL

Walter's Method Presumptions: Walter's method is depending on the relevant inferences:

There are no taxation or no distinction in taxation among dividend earnings and capital

gains. It means that dividend revenue and capital gains are taxed the same way. This

presumption is required for the concept's worldwide application, as taxation levels in

various places could fluctuate (Ratang, 2016).

There is no floatation or processing expenses, and such charges could vary by nation or

industry.

The business exists indefinitely.

All of the company's investing ideas must be funded entirely with retained profits.

The rate of return (r) and the cost of capital (Ke) are both unchanged.

difference among the two (capital gain). It implies that dividend revenue and capital gains

are taxed the same way. This presumption is required for the concept's global application,

as taxation levels in various places can vary (Parvaneh and El-Sayegh, 2016).

The following is the method for estimating the valuation of a company using the MM

Strategy:

Po = P1 + D1 / 1 + Ke

Where,

P1 = Price per share at the end

Po = Price per share at the beginning

D1 = Expected dividend per share

Ke = Cost of Equity

Benefits of the MM Theory

This structure provides a sequential pattern.

With the idea of the Arbitrage procedure, it gives a reasonable foundation for payout

management.

The MM Theory's Disadvantages

The accuracy of different assertions is controversial.

Given ambiguity, this approach might not have been effective.

WALTER’S MODEL

Walter's Method Presumptions: Walter's method is depending on the relevant inferences:

There are no taxation or no distinction in taxation among dividend earnings and capital

gains. It means that dividend revenue and capital gains are taxed the same way. This

presumption is required for the concept's worldwide application, as taxation levels in

various places could fluctuate (Ratang, 2016).

There is no floatation or processing expenses, and such charges could vary by nation or

industry.

The business exists indefinitely.

All of the company's investing ideas must be funded entirely with retained profits.

The rate of return (r) and the cost of capital (Ke) are both unchanged.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.