Financial Management: Evaluating Valuation and Investment Appraisal

VerifiedAdded on 2023/01/06

|15

|4016

|96

Report

AI Summary

This report delves into financial management, focusing on valuation and investment appraisal techniques. It examines the Price Earnings Ratio (PER), Dividend Valuation Method, and Discounted Cash Flow (DCF) method, critically discussing their associated problems. Furthermore, it presents and evaluates investment appraisal techniques such as Payback Period, Accounting Rate of Return (ARR), Net Present Value (NPV), and Internal Rate of Return (IRR), using a case study of Lovewell Ltd to illustrate their application in assessing the feasibility of investing in a new machine. The analysis concludes that while each method has its drawbacks, PER is a widely used and relatively less risky approach for valuation, and that investing in the new machine is a viable option for Lovewell Ltd based on the appraisal results.

Financial Management

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

QUESTION 2...................................................................................................................................1

a) Price earnings ratio (PER).......................................................................................................1

b) Dividend valuation method.....................................................................................................1

c) Discounted cash flow method (DCF)......................................................................................2

d) Critically discussing the problems associated with using the valuation techniques...............3

Question 3........................................................................................................................................5

1. Presenting investment appraisal techniques............................................................................5

2. Critically evaluating different investment appraisal techniques.............................................8

REFERENCES..............................................................................................................................12

QUESTION 2...................................................................................................................................1

a) Price earnings ratio (PER).......................................................................................................1

b) Dividend valuation method.....................................................................................................1

c) Discounted cash flow method (DCF)......................................................................................2

d) Critically discussing the problems associated with using the valuation techniques...............3

Question 3........................................................................................................................................5

1. Presenting investment appraisal techniques............................................................................5

2. Critically evaluating different investment appraisal techniques.............................................8

REFERENCES..............................................................................................................................12

QUESTION 2

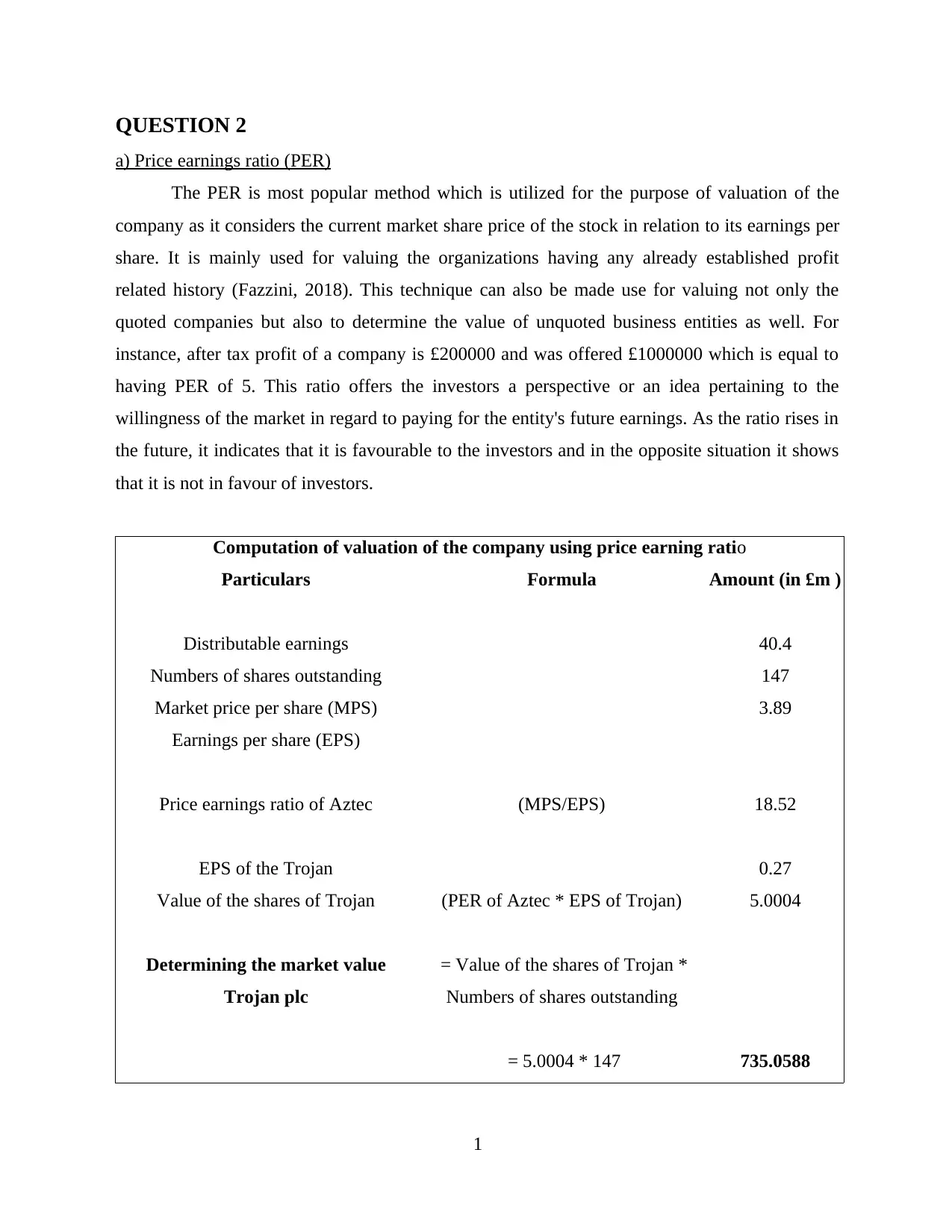

a) Price earnings ratio (PER)

The PER is most popular method which is utilized for the purpose of valuation of the

company as it considers the current market share price of the stock in relation to its earnings per

share. It is mainly used for valuing the organizations having any already established profit

related history (Fazzini, 2018). This technique can also be made use for valuing not only the

quoted companies but also to determine the value of unquoted business entities as well. For

instance, after tax profit of a company is £200000 and was offered £1000000 which is equal to

having PER of 5. This ratio offers the investors a perspective or an idea pertaining to the

willingness of the market in regard to paying for the entity's future earnings. As the ratio rises in

the future, it indicates that it is favourable to the investors and in the opposite situation it shows

that it is not in favour of investors.

Computation of valuation of the company using price earning ratio

Particulars Formula Amount (in £m )

Distributable earnings 40.4

Numbers of shares outstanding 147

Market price per share (MPS) 3.89

Earnings per share (EPS)

Price earnings ratio of Aztec (MPS/EPS) 18.52

EPS of the Trojan 0.27

Value of the shares of Trojan (PER of Aztec * EPS of Trojan) 5.0004

Determining the market value

Trojan plc

= Value of the shares of Trojan *

Numbers of shares outstanding

= 5.0004 * 147 735.0588

1

a) Price earnings ratio (PER)

The PER is most popular method which is utilized for the purpose of valuation of the

company as it considers the current market share price of the stock in relation to its earnings per

share. It is mainly used for valuing the organizations having any already established profit

related history (Fazzini, 2018). This technique can also be made use for valuing not only the

quoted companies but also to determine the value of unquoted business entities as well. For

instance, after tax profit of a company is £200000 and was offered £1000000 which is equal to

having PER of 5. This ratio offers the investors a perspective or an idea pertaining to the

willingness of the market in regard to paying for the entity's future earnings. As the ratio rises in

the future, it indicates that it is favourable to the investors and in the opposite situation it shows

that it is not in favour of investors.

Computation of valuation of the company using price earning ratio

Particulars Formula Amount (in £m )

Distributable earnings 40.4

Numbers of shares outstanding 147

Market price per share (MPS) 3.89

Earnings per share (EPS)

Price earnings ratio of Aztec (MPS/EPS) 18.52

EPS of the Trojan 0.27

Value of the shares of Trojan (PER of Aztec * EPS of Trojan) 5.0004

Determining the market value

Trojan plc

= Value of the shares of Trojan *

Numbers of shares outstanding

= 5.0004 * 147 735.0588

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

b) Dividend valuation method

The Gordon's dividend growth model (GGM) is another approach through which the

investor can identify the intrinsic value of the shares of the company on the basis of the constant

growth rate in respect to the dividend. This technique makes use of the dividend growth rate and

the entity's rate of return (ROR). It is based on the dividend discount model but it differs on

account of the fact that GGM assumes that dividend grows at the constant rate (Yu, Assad and

Fuller, 2016). The growth rate can be evaluated through making a multiplication of ROE with

the retention ratio. It provides assistance to the investors in determining whether it is viable to

make an investment in the respected company or not. It provides a clear relationship between the

return and the valuation. This technique is most suitable for business organization with the stable

earnings or the cash flows.

Computation of valuation of the company using Dividend valuation method

Particulars Formula Amount (in £m )

Information provided:

Latest dividend payment (Current

dividend) 0.13

Growth rate (GR)

= 0.10(1+g)^5 = 0.13

= 0.05 5.00%

Risk free rate (Rf) 5.00%

Beta (β) 1.10%

Number of shares 147

Return on market (Rm) 11.00%

For determining expected rate of return

(K), CAPM model will be used

According to CAPM, K is = Rf + (Rm-Rf)β

2

The Gordon's dividend growth model (GGM) is another approach through which the

investor can identify the intrinsic value of the shares of the company on the basis of the constant

growth rate in respect to the dividend. This technique makes use of the dividend growth rate and

the entity's rate of return (ROR). It is based on the dividend discount model but it differs on

account of the fact that GGM assumes that dividend grows at the constant rate (Yu, Assad and

Fuller, 2016). The growth rate can be evaluated through making a multiplication of ROE with

the retention ratio. It provides assistance to the investors in determining whether it is viable to

make an investment in the respected company or not. It provides a clear relationship between the

return and the valuation. This technique is most suitable for business organization with the stable

earnings or the cash flows.

Computation of valuation of the company using Dividend valuation method

Particulars Formula Amount (in £m )

Information provided:

Latest dividend payment (Current

dividend) 0.13

Growth rate (GR)

= 0.10(1+g)^5 = 0.13

= 0.05 5.00%

Risk free rate (Rf) 5.00%

Beta (β) 1.10%

Number of shares 147

Return on market (Rm) 11.00%

For determining expected rate of return

(K), CAPM model will be used

According to CAPM, K is = Rf + (Rm-Rf)β

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

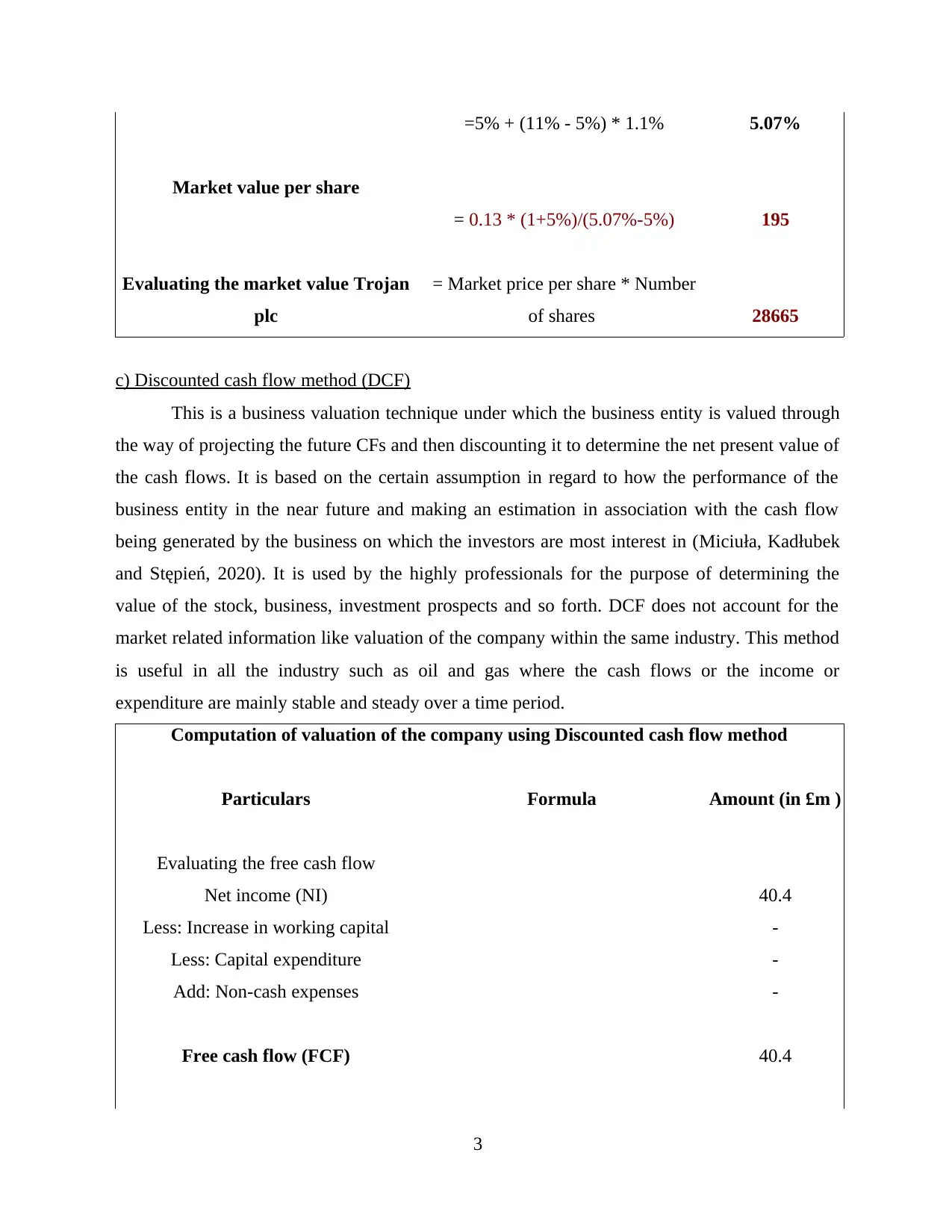

=5% + (11% - 5%) * 1.1% 5.07%

Market value per share

= 0.13 * (1+5%)/(5.07%-5%) 195

Evaluating the market value Trojan

plc

= Market price per share * Number

of shares 28665

c) Discounted cash flow method (DCF)

This is a business valuation technique under which the business entity is valued through

the way of projecting the future CFs and then discounting it to determine the net present value of

the cash flows. It is based on the certain assumption in regard to how the performance of the

business entity in the near future and making an estimation in association with the cash flow

being generated by the business on which the investors are most interest in (Miciuła, Kadłubek

and Stępień, 2020). It is used by the highly professionals for the purpose of determining the

value of the stock, business, investment prospects and so forth. DCF does not account for the

market related information like valuation of the company within the same industry. This method

is useful in all the industry such as oil and gas where the cash flows or the income or

expenditure are mainly stable and steady over a time period.

Computation of valuation of the company using Discounted cash flow method

Particulars Formula Amount (in £m )

Evaluating the free cash flow

Net income (NI) 40.4

Less: Increase in working capital -

Less: Capital expenditure -

Add: Non-cash expenses -

Free cash flow (FCF) 40.4

3

Market value per share

= 0.13 * (1+5%)/(5.07%-5%) 195

Evaluating the market value Trojan

plc

= Market price per share * Number

of shares 28665

c) Discounted cash flow method (DCF)

This is a business valuation technique under which the business entity is valued through

the way of projecting the future CFs and then discounting it to determine the net present value of

the cash flows. It is based on the certain assumption in regard to how the performance of the

business entity in the near future and making an estimation in association with the cash flow

being generated by the business on which the investors are most interest in (Miciuła, Kadłubek

and Stępień, 2020). It is used by the highly professionals for the purpose of determining the

value of the stock, business, investment prospects and so forth. DCF does not account for the

market related information like valuation of the company within the same industry. This method

is useful in all the industry such as oil and gas where the cash flows or the income or

expenditure are mainly stable and steady over a time period.

Computation of valuation of the company using Discounted cash flow method

Particulars Formula Amount (in £m )

Evaluating the free cash flow

Net income (NI) 40.4

Less: Increase in working capital -

Less: Capital expenditure -

Add: Non-cash expenses -

Free cash flow (FCF) 40.4

3

Discounting rate or WACC 9.00%

MPS = Free cash flow / Discounting rate 448.89

Market value of Trojan plc = MPS * Number of shares

= 448.89 * 147 65986.67

d) Critically discussing the problems associated with using the valuation techniques

The PER is one the popular and widely used method for valuing the company by there

are certain drawbacks of making use of this method. According to Dierks, Bruyère and Reginster

(2018), the earnings of the company can be easily distorted which indicates that the PER can be

distorted which is depended upon how the organization accounts for a specific item. An

important factor to considered is that it is distracted by the difference in the accounting standards

which vary from one country to another which creates problem in making comparison between

the two companies. The major drawback is the quality of the business earnings. There are times

when the earnings of the business entity is impacted by the unusual or the gains or the losses or

the time when the expenses have been recognized in the form of amortization even if the

organization has already accounted for the same. Another drawback is that PER does not

account for the increase in the EPS of the business entity. As defined by Mchawrab (2016), PER

cannot be dependent upon individually for making a decision in respect to whether to make an

investment or not as the earnings of the organization is published on a quarterly basis while the

EPS fluctuates every day. Therefore, the PER might not work in the same direction with the

company's performance.

As emphasized by O'Brien (2020), another useful method of valuation which is dividend

valuation method but every method is prone to certain level of drawbacks. The major issue

pertaining to it, is that it requires the dividend growth rate to be stable and constant which cannot

be an accurate assumption in the real life. Therefore, this creates problem for the newer

established companies as the constant GR is less common which is due to the fact of potential

fluctuations and volatility associated with their development process. Another important factor is

that it needs the rate of return to be greater than the GR or else, the model will provide negative

outcome. It does not take into consideration the external or the outside factor having an impact

over the value of the entity or its stock. As argued by Tripathi, Kashiramka and Jain (2018), this

4

MPS = Free cash flow / Discounting rate 448.89

Market value of Trojan plc = MPS * Number of shares

= 448.89 * 147 65986.67

d) Critically discussing the problems associated with using the valuation techniques

The PER is one the popular and widely used method for valuing the company by there

are certain drawbacks of making use of this method. According to Dierks, Bruyère and Reginster

(2018), the earnings of the company can be easily distorted which indicates that the PER can be

distorted which is depended upon how the organization accounts for a specific item. An

important factor to considered is that it is distracted by the difference in the accounting standards

which vary from one country to another which creates problem in making comparison between

the two companies. The major drawback is the quality of the business earnings. There are times

when the earnings of the business entity is impacted by the unusual or the gains or the losses or

the time when the expenses have been recognized in the form of amortization even if the

organization has already accounted for the same. Another drawback is that PER does not

account for the increase in the EPS of the business entity. As defined by Mchawrab (2016), PER

cannot be dependent upon individually for making a decision in respect to whether to make an

investment or not as the earnings of the organization is published on a quarterly basis while the

EPS fluctuates every day. Therefore, the PER might not work in the same direction with the

company's performance.

As emphasized by O'Brien (2020), another useful method of valuation which is dividend

valuation method but every method is prone to certain level of drawbacks. The major issue

pertaining to it, is that it requires the dividend growth rate to be stable and constant which cannot

be an accurate assumption in the real life. Therefore, this creates problem for the newer

established companies as the constant GR is less common which is due to the fact of potential

fluctuations and volatility associated with their development process. Another important factor is

that it needs the rate of return to be greater than the GR or else, the model will provide negative

outcome. It does not take into consideration the external or the outside factor having an impact

over the value of the entity or its stock. As argued by Tripathi, Kashiramka and Jain (2018), this

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

technique of value is mainly suitable for the corporates that pays dividend and not all the entities

make payment of the dividend and thus, this it limits the stock number in quantity and the

organizations for making use of this model in analysing the value of the business. Another

problem is that it is based upon the assumption that the firm develops or expands at the constant

rate and in actual it is not the same case as it is highly not likely or familiar that the businesses

will have their dividends growing at the constant rate. This model is very sensitive to the growth

rate and the discounting factor utilized.

The discounted cash flow is considered as the most rigorous but financially sound

approach for the purpose of valuation of the firm. According to Ardian and Kumral (2018), there

are 3 major pitfalls associated with DCF method of valuation. First is determining the DCF

value by estimating the operating cash flow forecasts. It incorporates various inherent problems

in association with the earnings and the CF forecasting. Further, stated by the author, that the

major issue is in respect to uncertainty on account of the CF projections in each year and this

model makes use of the min. 5 and maximum 10 years of future cash flows. Another issue is the

projection of the capital expenditure projections for each year and again in this case as well the

degree of uncertainty rises. Therefore, making an estimation pertaining to the capital expenditure

for the future years is a risky task. Even though, there are some techniques which can be used for

the same such as Fixed asset turnover ratio or the % revenue month. But, it is very important to

consider that even a small change or a minor variation in the assumptions would widely impact

the final outcome of the DCF valuation. Along with it, the assumption about the discounting rate

and GR also poses threat as analyst might use CAPM model or WACC as the discounting rate

but this approach is mostly theoretical.

Based on the critical analysis, it can be inferred that the PER is the most suitable method

for valuation purpose which is because even though it is prone to some drawbacks but it is not a

risky attempt and this approach is widely used by the associates or the businesses. Along with it,

it is very easy to compute and understand.

Question 3

1. Presenting investment appraisal techniques

Computation of cash inflows

Year Cash inflow Cash outflow Less: Gross Profit EBIT

5

make payment of the dividend and thus, this it limits the stock number in quantity and the

organizations for making use of this model in analysing the value of the business. Another

problem is that it is based upon the assumption that the firm develops or expands at the constant

rate and in actual it is not the same case as it is highly not likely or familiar that the businesses

will have their dividends growing at the constant rate. This model is very sensitive to the growth

rate and the discounting factor utilized.

The discounted cash flow is considered as the most rigorous but financially sound

approach for the purpose of valuation of the firm. According to Ardian and Kumral (2018), there

are 3 major pitfalls associated with DCF method of valuation. First is determining the DCF

value by estimating the operating cash flow forecasts. It incorporates various inherent problems

in association with the earnings and the CF forecasting. Further, stated by the author, that the

major issue is in respect to uncertainty on account of the CF projections in each year and this

model makes use of the min. 5 and maximum 10 years of future cash flows. Another issue is the

projection of the capital expenditure projections for each year and again in this case as well the

degree of uncertainty rises. Therefore, making an estimation pertaining to the capital expenditure

for the future years is a risky task. Even though, there are some techniques which can be used for

the same such as Fixed asset turnover ratio or the % revenue month. But, it is very important to

consider that even a small change or a minor variation in the assumptions would widely impact

the final outcome of the DCF valuation. Along with it, the assumption about the discounting rate

and GR also poses threat as analyst might use CAPM model or WACC as the discounting rate

but this approach is mostly theoretical.

Based on the critical analysis, it can be inferred that the PER is the most suitable method

for valuation purpose which is because even though it is prone to some drawbacks but it is not a

risky attempt and this approach is widely used by the associates or the businesses. Along with it,

it is very easy to compute and understand.

Question 3

1. Presenting investment appraisal techniques

Computation of cash inflows

Year Cash inflow Cash outflow Less: Gross Profit EBIT

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

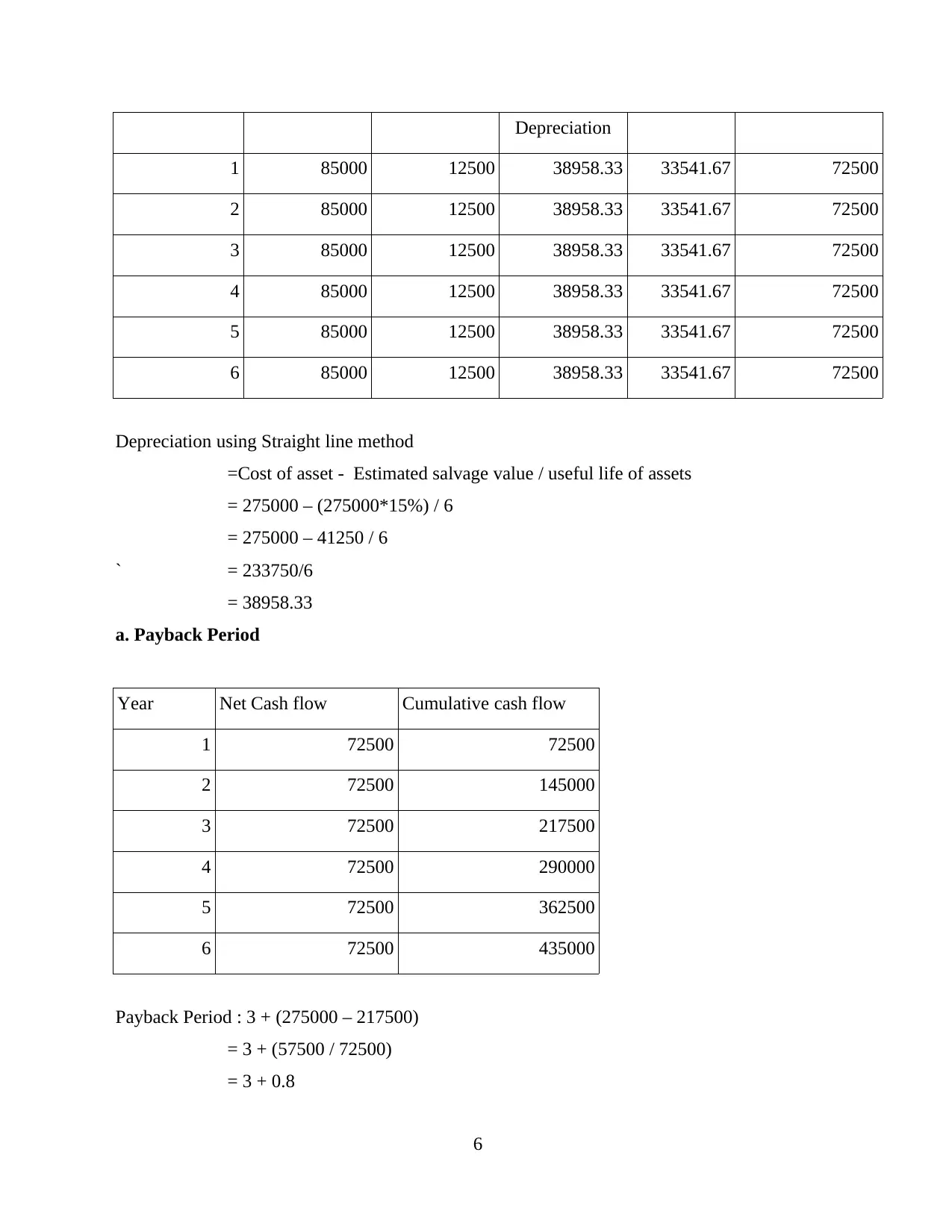

Depreciation

1 85000 12500 38958.33 33541.67 72500

2 85000 12500 38958.33 33541.67 72500

3 85000 12500 38958.33 33541.67 72500

4 85000 12500 38958.33 33541.67 72500

5 85000 12500 38958.33 33541.67 72500

6 85000 12500 38958.33 33541.67 72500

Depreciation using Straight line method

=Cost of asset - Estimated salvage value / useful life of assets

= 275000 – (275000*15%) / 6

= 275000 – 41250 / 6

` = 233750/6

= 38958.33

a. Payback Period

Year Net Cash flow Cumulative cash flow

1 72500 72500

2 72500 145000

3 72500 217500

4 72500 290000

5 72500 362500

6 72500 435000

Payback Period : 3 + (275000 – 217500)

= 3 + (57500 / 72500)

= 3 + 0.8

6

1 85000 12500 38958.33 33541.67 72500

2 85000 12500 38958.33 33541.67 72500

3 85000 12500 38958.33 33541.67 72500

4 85000 12500 38958.33 33541.67 72500

5 85000 12500 38958.33 33541.67 72500

6 85000 12500 38958.33 33541.67 72500

Depreciation using Straight line method

=Cost of asset - Estimated salvage value / useful life of assets

= 275000 – (275000*15%) / 6

= 275000 – 41250 / 6

` = 233750/6

= 38958.33

a. Payback Period

Year Net Cash flow Cumulative cash flow

1 72500 72500

2 72500 145000

3 72500 217500

4 72500 290000

5 72500 362500

6 72500 435000

Payback Period : 3 + (275000 – 217500)

= 3 + (57500 / 72500)

= 3 + 0.8

6

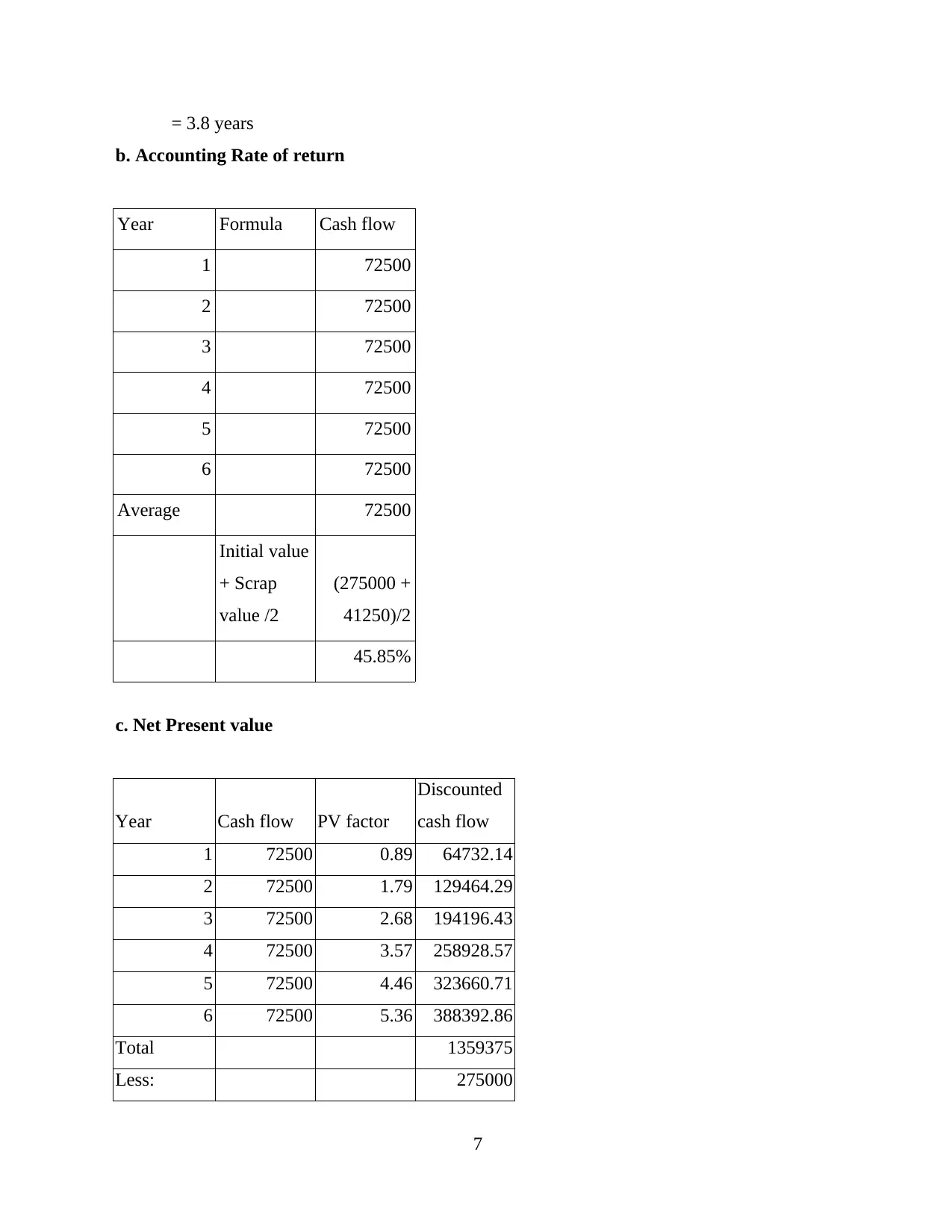

= 3.8 years

b. Accounting Rate of return

Year Formula Cash flow

1 72500

2 72500

3 72500

4 72500

5 72500

6 72500

Average 72500

Initial value

+ Scrap

value /2

(275000 +

41250)/2

45.85%

c. Net Present value

Year Cash flow PV factor

Discounted

cash flow

1 72500 0.89 64732.14

2 72500 1.79 129464.29

3 72500 2.68 194196.43

4 72500 3.57 258928.57

5 72500 4.46 323660.71

6 72500 5.36 388392.86

Total 1359375

Less: 275000

7

b. Accounting Rate of return

Year Formula Cash flow

1 72500

2 72500

3 72500

4 72500

5 72500

6 72500

Average 72500

Initial value

+ Scrap

value /2

(275000 +

41250)/2

45.85%

c. Net Present value

Year Cash flow PV factor

Discounted

cash flow

1 72500 0.89 64732.14

2 72500 1.79 129464.29

3 72500 2.68 194196.43

4 72500 3.57 258928.57

5 72500 4.46 323660.71

6 72500 5.36 388392.86

Total 1359375

Less: 275000

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

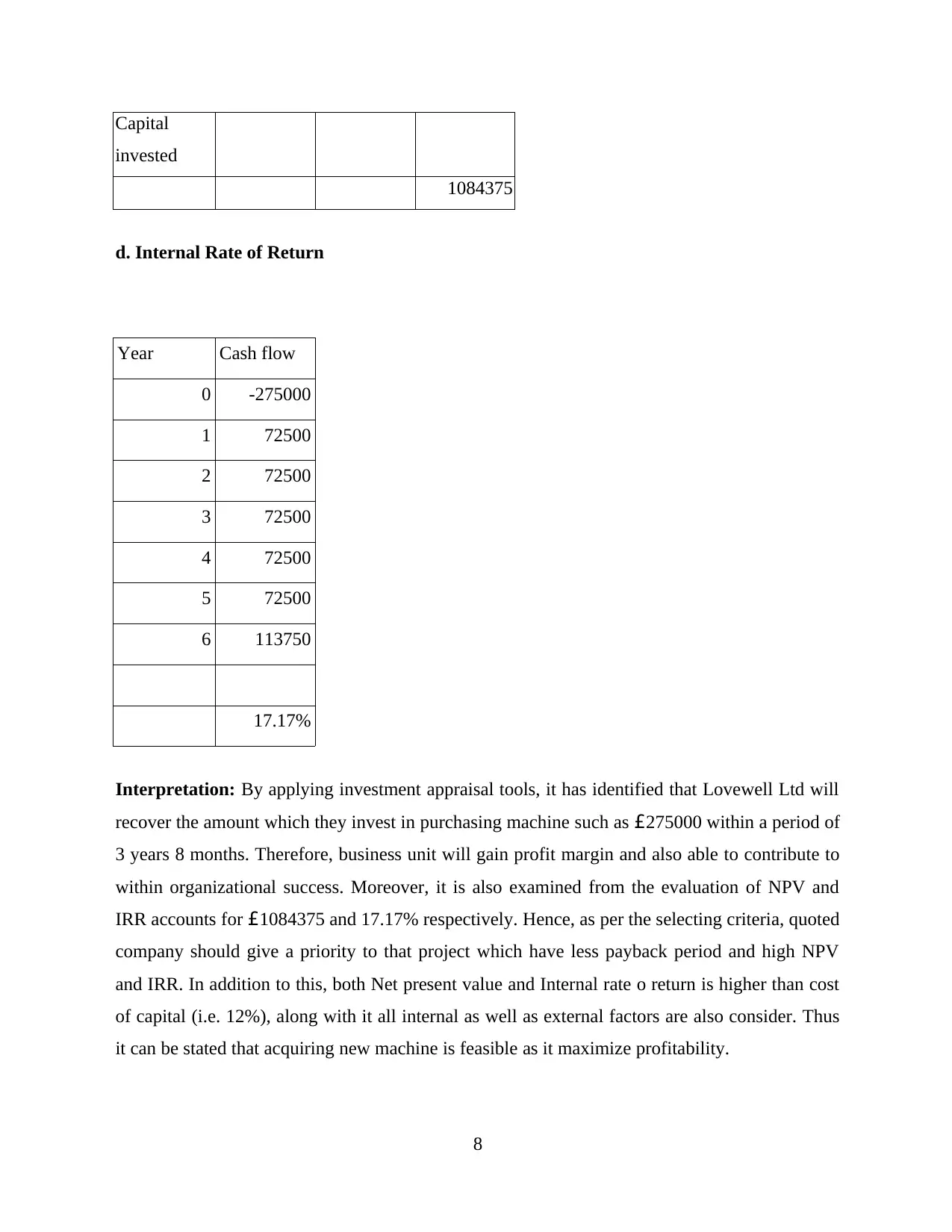

Capital

invested

1084375

d. Internal Rate of Return

Year Cash flow

0 -275000

1 72500

2 72500

3 72500

4 72500

5 72500

6 113750

17.17%

Interpretation: By applying investment appraisal tools, it has identified that Lovewell Ltd will

recover the amount which they invest in purchasing machine such as £275000 within a period of

3 years 8 months. Therefore, business unit will gain profit margin and also able to contribute to

within organizational success. Moreover, it is also examined from the evaluation of NPV and

IRR accounts for £1084375 and 17.17% respectively. Hence, as per the selecting criteria, quoted

company should give a priority to that project which have less payback period and high NPV

and IRR. In addition to this, both Net present value and Internal rate o return is higher than cost

of capital (i.e. 12%), along with it all internal as well as external factors are also consider. Thus

it can be stated that acquiring new machine is feasible as it maximize profitability.

8

invested

1084375

d. Internal Rate of Return

Year Cash flow

0 -275000

1 72500

2 72500

3 72500

4 72500

5 72500

6 113750

17.17%

Interpretation: By applying investment appraisal tools, it has identified that Lovewell Ltd will

recover the amount which they invest in purchasing machine such as £275000 within a period of

3 years 8 months. Therefore, business unit will gain profit margin and also able to contribute to

within organizational success. Moreover, it is also examined from the evaluation of NPV and

IRR accounts for £1084375 and 17.17% respectively. Hence, as per the selecting criteria, quoted

company should give a priority to that project which have less payback period and high NPV

and IRR. In addition to this, both Net present value and Internal rate o return is higher than cost

of capital (i.e. 12%), along with it all internal as well as external factors are also consider. Thus

it can be stated that acquiring new machine is feasible as it maximize profitability.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

So, in the context of current evaluation, it can be entailed that investing in new machine

will help company in attaining the set aim and objectives because ARR is higher which clearly

reflected that company earn profit.

2. Critically evaluating different investment appraisal techniques

Payback Period (PBP):

It is refers to the amount of time which takes to recover the cost of an investment. Thus,

it is length of the time, in which an investment reaches to a break even point. In this technique,

the shorter payback are considered more attractive investment rather than larger one (Gorshkov,

Murgul and Oliynyk, 2016). Payback period also ignores the concept of time value of money,

but is used in combination with other techniques of capital budgeting. Also, the main purpose of

using this tool is to compare similar investment and identify which is more beneficial for a

business.

Advantages:

Payback Period method is simple to use and easy to understand among all others. It is so

because only project's initial cost and annual cash flows are calculating.

It assist to generate quick solution because it needs fewer inputs and this in turn assist to

those companies who have limited resources.

Also provide crucial information which no other capital budgeting method reveals. The method is more suitable in those industries who have to cope up with rapid

technological changes. Therefore, it aid to reduce the chances of loss through

obsolescence.

Disadvantages:

It ignore time value of money which is quite important for business concept. As a result,

PBP distorting the true value of cash flows (Siecker, Kusakana and Numbi, 2018).

The method is consider cash flows till investment is recovered. Also, it is simple to use

but not realistic, that is why, normal business do not consider the same. There is no surety that project with shorter PBP will be profitable. It is so because it

neglects project's Return on investment (ROI).

Accounting rate of return (ARR):

9

will help company in attaining the set aim and objectives because ARR is higher which clearly

reflected that company earn profit.

2. Critically evaluating different investment appraisal techniques

Payback Period (PBP):

It is refers to the amount of time which takes to recover the cost of an investment. Thus,

it is length of the time, in which an investment reaches to a break even point. In this technique,

the shorter payback are considered more attractive investment rather than larger one (Gorshkov,

Murgul and Oliynyk, 2016). Payback period also ignores the concept of time value of money,

but is used in combination with other techniques of capital budgeting. Also, the main purpose of

using this tool is to compare similar investment and identify which is more beneficial for a

business.

Advantages:

Payback Period method is simple to use and easy to understand among all others. It is so

because only project's initial cost and annual cash flows are calculating.

It assist to generate quick solution because it needs fewer inputs and this in turn assist to

those companies who have limited resources.

Also provide crucial information which no other capital budgeting method reveals. The method is more suitable in those industries who have to cope up with rapid

technological changes. Therefore, it aid to reduce the chances of loss through

obsolescence.

Disadvantages:

It ignore time value of money which is quite important for business concept. As a result,

PBP distorting the true value of cash flows (Siecker, Kusakana and Numbi, 2018).

The method is consider cash flows till investment is recovered. Also, it is simple to use

but not realistic, that is why, normal business do not consider the same. There is no surety that project with shorter PBP will be profitable. It is so because it

neglects project's Return on investment (ROI).

Accounting rate of return (ARR):

9

It reflects the percentage rate of return which a business expected on an investment as

compared to initial investment's cost. ARR is considered as one of the most important

investment appraisal tools because it helps investor to examine the risk involved in making an

investment and also determine whether the risk is high or not (Psacharopoulos and Teixeira,

2019). Hence, it is a way of comparing profitability of different projects over the expected life of

an investment. The standard criteria o selection project is such that if the asset's expected ARR is

greater than or equal to management's desired rate of return then it is accepted, otherwise not.

Advantages:

ARR assist in comparing a new project with another one by generating best results.

Provides clear view of profitability and easy to calculate as well.

It is also used when trying to measure the present performance of a firm. The method is completely relied upon accounting information while other reports are not

(Accounting Rate of Return Method. Advantages & Disadvantage, 2020).

Disadvantages:

This method ignore the time factor and some external factors.

Investors faces difficulties in decision making, if the results of ROI and ARR are

different.

The calculation are done on the basis of profit earned by project but in the same time it

also ignores cash flows which is quite important factor for every business.

It do not helps the project to appraise where installment of an investment have been

made more than two times. This technique can be calculated in different ways and that is why, it leads to different

outcomes as well.

Net Present Value (NPV):

It is the difference between present value of cash inflow and outflows over a specific

time period. This methods is actually used to analyze the profitability of a project by considering

its define formula. Thus, a positive NPV indicates that project earnings are generated by a

project and vice versa. This method is more reliable as it uses a reinvestment rate close to the

investment cost, while other do not.

Advantages:

10

compared to initial investment's cost. ARR is considered as one of the most important

investment appraisal tools because it helps investor to examine the risk involved in making an

investment and also determine whether the risk is high or not (Psacharopoulos and Teixeira,

2019). Hence, it is a way of comparing profitability of different projects over the expected life of

an investment. The standard criteria o selection project is such that if the asset's expected ARR is

greater than or equal to management's desired rate of return then it is accepted, otherwise not.

Advantages:

ARR assist in comparing a new project with another one by generating best results.

Provides clear view of profitability and easy to calculate as well.

It is also used when trying to measure the present performance of a firm. The method is completely relied upon accounting information while other reports are not

(Accounting Rate of Return Method. Advantages & Disadvantage, 2020).

Disadvantages:

This method ignore the time factor and some external factors.

Investors faces difficulties in decision making, if the results of ROI and ARR are

different.

The calculation are done on the basis of profit earned by project but in the same time it

also ignores cash flows which is quite important factor for every business.

It do not helps the project to appraise where installment of an investment have been

made more than two times. This technique can be calculated in different ways and that is why, it leads to different

outcomes as well.

Net Present Value (NPV):

It is the difference between present value of cash inflow and outflows over a specific

time period. This methods is actually used to analyze the profitability of a project by considering

its define formula. Thus, a positive NPV indicates that project earnings are generated by a

project and vice versa. This method is more reliable as it uses a reinvestment rate close to the

investment cost, while other do not.

Advantages:

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.