Financial Management Project: Analyzing Unilever Group Plc's Finances

VerifiedAdded on 2023/01/13

|16

|2636

|55

Project

AI Summary

This project delves into the financial management of Unilever Group Plc, employing a comprehensive financial model to assess its performance. It begins with an introduction to financial management and its significance, followed by the construction of a detailed financial model incorporating pro forma financial statements (income statement, balance sheet, and cash flow statement) from 2017 to 2019. The model includes various inputs and assumptions, such as sales growth, interest rates, and payout ratios. The project then calculates amortization, projects cash flows, analyzes debt structures, and considers different scenarios to evaluate the company's financial health. Key financial management concepts, including the weighted average cost of capital (WACC), net present value (NPV), internal rate of return (IRR), and payback period are applied to assess investment viability. The analysis also includes the valuation of the company using the Free Cash Flow to Equity (FCFE) model and a discussion of financial analysis techniques. The project concludes with an overview of the findings and their implications for Unilever's financial strategy.

FINANCIAL MANAGEMENT

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

FINANCIAL MODEL.....................................................................................................................1

Proforma......................................................................................................................................1

Inputs............................................................................................................................................4

Amortisation................................................................................................................................5

Projection of Cash Flows.............................................................................................................5

Debt..............................................................................................................................................6

Cash Flows ..................................................................................................................................7

Scenarios......................................................................................................................................9

Financial Management...............................................................................................................11

CONCLUSION..............................................................................................................................14

INTRODUCTION...........................................................................................................................1

FINANCIAL MODEL.....................................................................................................................1

Proforma......................................................................................................................................1

Inputs............................................................................................................................................4

Amortisation................................................................................................................................5

Projection of Cash Flows.............................................................................................................5

Debt..............................................................................................................................................6

Cash Flows ..................................................................................................................................7

Scenarios......................................................................................................................................9

Financial Management...............................................................................................................11

CONCLUSION..............................................................................................................................14

INTRODUCTION

Financial management in a organization, is a critical operation. To accomplish strategic

targets and goals, this is the mechanism of planning coordinating, managing and tracking

financial assets and resources. This is an effective procedure for managing an organisation's

financial operations like fund acquisition, fund management, reporting, risk evaluation and

everything else connected to funds. Financial management relates to use of common

management concepts to a firm's financial resources. Commonly companies have a specific

division which takes care of the business's concerns. Finance manager is appointed within a

corporation to handle financing and control its capital. All relevant decisions relating to finance

are made in this role. This also involve use of some practical and numerical data to support

decisions taken by finance managers. This study-assessment cover practical aspects of financial

management like valuation of company, computation of cash flow, free-cash flows, optimum

capital structure and risk-assessment applying multiple approaches in context of Unilever Group

Plc

FINANCIAL MODEL

In the present case Unilever Group plc has been taken for applying the financial model.

The potential cash flows, FCF, capital structure and profitability of the investments are identified

using different techniques and tools used in financial management. Future calculations are made

on the basis of assumptions analysing the trend of company over previous years.

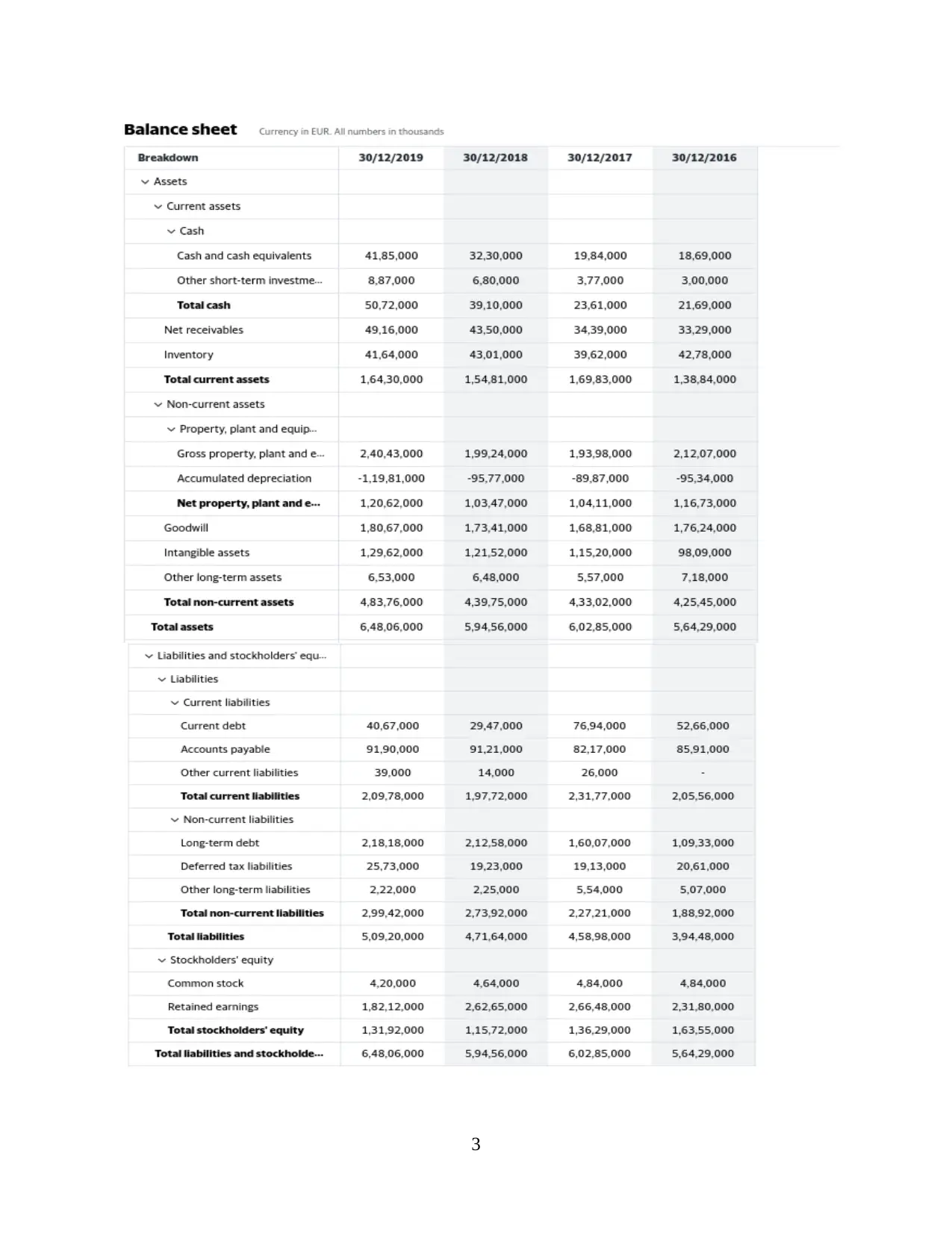

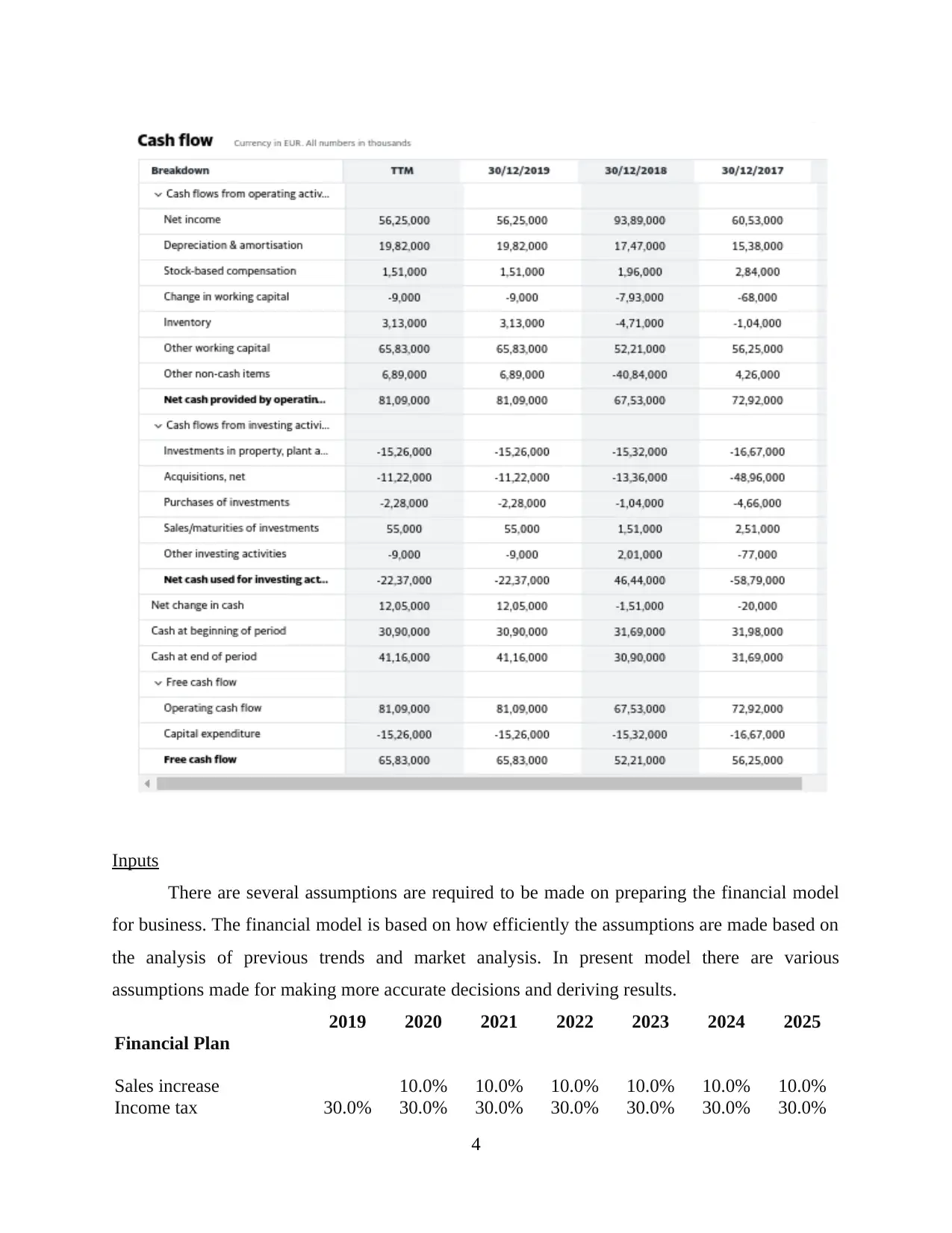

Proforma

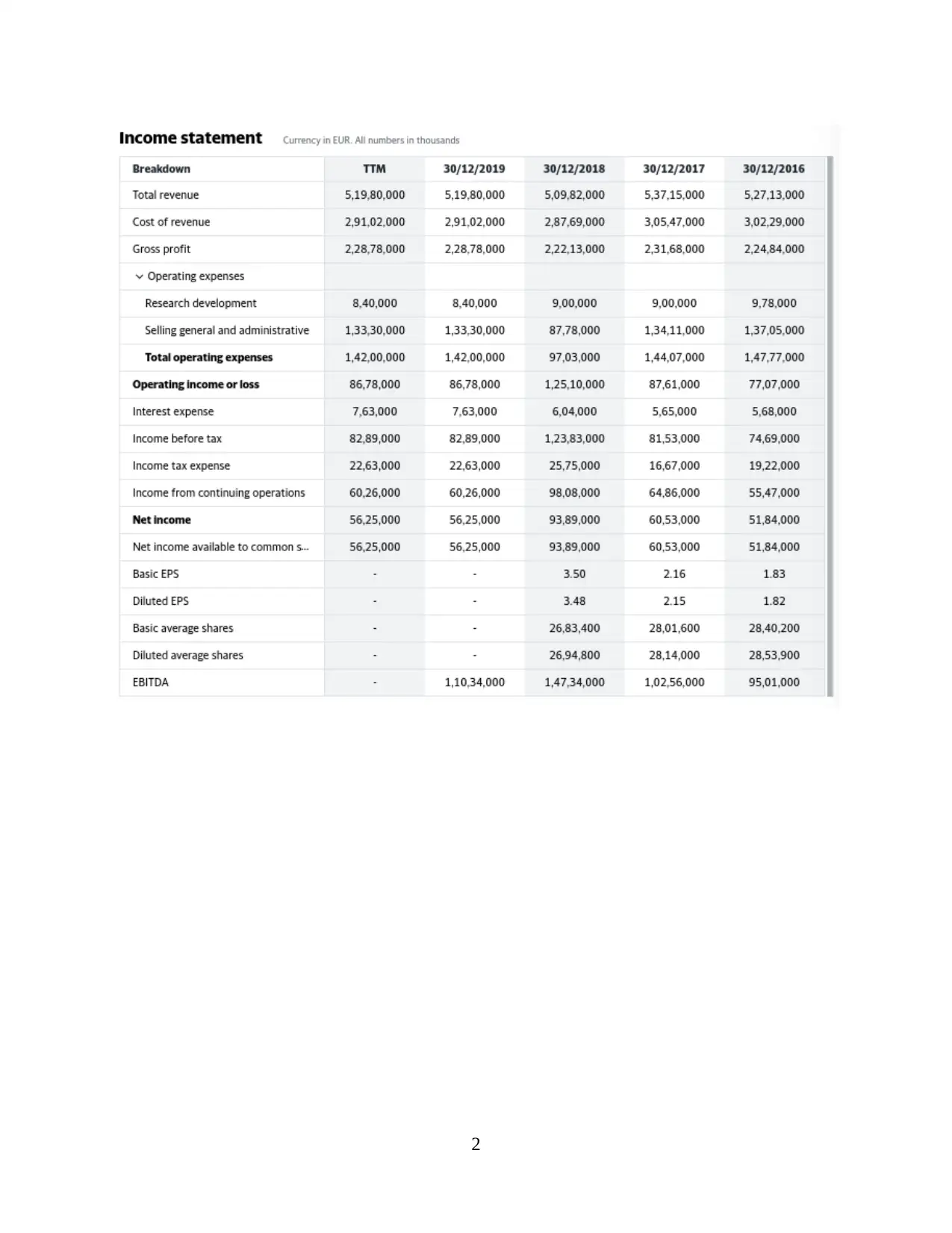

3 year's financial statement of the Unilever Group plc from 2017 to 2019 that are income

statement, balance sheet and cash flow statement.

Financial Statements of Unilever Group plc

1

Financial management in a organization, is a critical operation. To accomplish strategic

targets and goals, this is the mechanism of planning coordinating, managing and tracking

financial assets and resources. This is an effective procedure for managing an organisation's

financial operations like fund acquisition, fund management, reporting, risk evaluation and

everything else connected to funds. Financial management relates to use of common

management concepts to a firm's financial resources. Commonly companies have a specific

division which takes care of the business's concerns. Finance manager is appointed within a

corporation to handle financing and control its capital. All relevant decisions relating to finance

are made in this role. This also involve use of some practical and numerical data to support

decisions taken by finance managers. This study-assessment cover practical aspects of financial

management like valuation of company, computation of cash flow, free-cash flows, optimum

capital structure and risk-assessment applying multiple approaches in context of Unilever Group

Plc

FINANCIAL MODEL

In the present case Unilever Group plc has been taken for applying the financial model.

The potential cash flows, FCF, capital structure and profitability of the investments are identified

using different techniques and tools used in financial management. Future calculations are made

on the basis of assumptions analysing the trend of company over previous years.

Proforma

3 year's financial statement of the Unilever Group plc from 2017 to 2019 that are income

statement, balance sheet and cash flow statement.

Financial Statements of Unilever Group plc

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

3

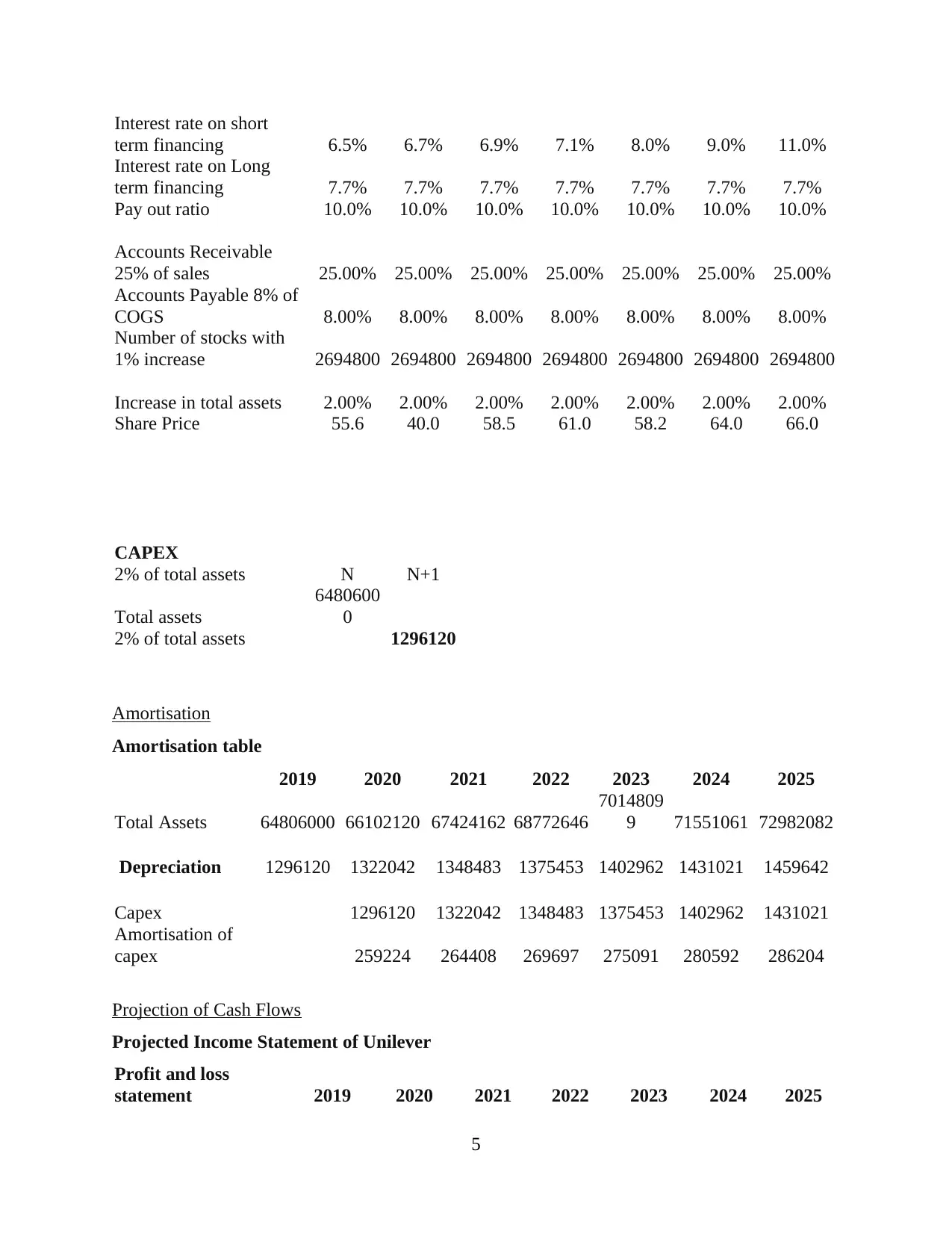

Inputs

There are several assumptions are required to be made on preparing the financial model

for business. The financial model is based on how efficiently the assumptions are made based on

the analysis of previous trends and market analysis. In present model there are various

assumptions made for making more accurate decisions and deriving results.

2019 2020 2021 2022 2023 2024 2025

Financial Plan

Sales increase 10.0% 10.0% 10.0% 10.0% 10.0% 10.0%

Income tax 30.0% 30.0% 30.0% 30.0% 30.0% 30.0% 30.0%

4

There are several assumptions are required to be made on preparing the financial model

for business. The financial model is based on how efficiently the assumptions are made based on

the analysis of previous trends and market analysis. In present model there are various

assumptions made for making more accurate decisions and deriving results.

2019 2020 2021 2022 2023 2024 2025

Financial Plan

Sales increase 10.0% 10.0% 10.0% 10.0% 10.0% 10.0%

Income tax 30.0% 30.0% 30.0% 30.0% 30.0% 30.0% 30.0%

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Interest rate on short

term financing 6.5% 6.7% 6.9% 7.1% 8.0% 9.0% 11.0%

Interest rate on Long

term financing 7.7% 7.7% 7.7% 7.7% 7.7% 7.7% 7.7%

Pay out ratio 10.0% 10.0% 10.0% 10.0% 10.0% 10.0% 10.0%

Accounts Receivable

25% of sales 25.00% 25.00% 25.00% 25.00% 25.00% 25.00% 25.00%

Accounts Payable 8% of

COGS 8.00% 8.00% 8.00% 8.00% 8.00% 8.00% 8.00%

Number of stocks with

1% increase 2694800 2694800 2694800 2694800 2694800 2694800 2694800

Increase in total assets 2.00% 2.00% 2.00% 2.00% 2.00% 2.00% 2.00%

Share Price 55.6 40.0 58.5 61.0 58.2 64.0 66.0

CAPEX

2% of total assets N N+1

Total assets

6480600

0

2% of total assets 1296120

Amortisation

Amortisation table

2019 2020 2021 2022 2023 2024 2025

Total Assets 64806000 66102120 67424162 68772646

7014809

9 71551061 72982082

Depreciation 1296120 1322042 1348483 1375453 1402962 1431021 1459642

Capex 1296120 1322042 1348483 1375453 1402962 1431021

Amortisation of

capex 259224 264408 269697 275091 280592 286204

Projection of Cash Flows

Projected Income Statement of Unilever

Profit and loss

statement 2019 2020 2021 2022 2023 2024 2025

5

term financing 6.5% 6.7% 6.9% 7.1% 8.0% 9.0% 11.0%

Interest rate on Long

term financing 7.7% 7.7% 7.7% 7.7% 7.7% 7.7% 7.7%

Pay out ratio 10.0% 10.0% 10.0% 10.0% 10.0% 10.0% 10.0%

Accounts Receivable

25% of sales 25.00% 25.00% 25.00% 25.00% 25.00% 25.00% 25.00%

Accounts Payable 8% of

COGS 8.00% 8.00% 8.00% 8.00% 8.00% 8.00% 8.00%

Number of stocks with

1% increase 2694800 2694800 2694800 2694800 2694800 2694800 2694800

Increase in total assets 2.00% 2.00% 2.00% 2.00% 2.00% 2.00% 2.00%

Share Price 55.6 40.0 58.5 61.0 58.2 64.0 66.0

CAPEX

2% of total assets N N+1

Total assets

6480600

0

2% of total assets 1296120

Amortisation

Amortisation table

2019 2020 2021 2022 2023 2024 2025

Total Assets 64806000 66102120 67424162 68772646

7014809

9 71551061 72982082

Depreciation 1296120 1322042 1348483 1375453 1402962 1431021 1459642

Capex 1296120 1322042 1348483 1375453 1402962 1431021

Amortisation of

capex 259224 264408 269697 275091 280592 286204

Projection of Cash Flows

Projected Income Statement of Unilever

Profit and loss

statement 2019 2020 2021 2022 2023 2024 2025

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Sales (increase of

10%) 51980000

5717800

0

6289580

0

6918538

0 76103918

8371431

0

9208574

1

COGS (70% of sales) 36386000

4002460

0

4402706

0

4842976

6 53272743

5860001

7

6446001

9

Gross earnings 15594000

1715340

0

1886874

0

2075561

4 22831175

2511429

3

2762572

2

General and

administrative costs

(10% of COGS) 3638600 4002460 4402706 4842977 5327274 5860002 6446002

Amortisation(2% of

total assets) 1296120 1322042 1348483 1375453 1402962 1431021 1459642

EBIT 2342480 2680418 3054223 3467524 3924312 4428980 4986360

Interests on Loan 82453 84248 85933 87651 89404 91193 93016

Income tax 678008 778851 890487 1013962 1150472 1301336 1468003

Net income/Loss 1582019 1817319 2077803 2365911 2684435 3036452 3425341

Number of stocks 2694800 2694800 2694800 2694800 2694800 2694800 2694800

EPS 0.587 0.674 0.771 0.878 0.996 1.127 1.271

EPS share

Dividends 158202 181732 207780 236591 268444 303645 342534

Retained earnings 2536598 2513068 2487020 2458209 2426356 2391155 2352266

DPS 0.059 0.067 0.077 0.088 0.100 0.113 0.127

Debt

A company on large or medium scale could not run effectively and efficiently without raising

funds from the market. It is responsibility of the financial managers to identify the most suitable

source of finance for raising fund whose cost of finance is lowest and give maximum benefits to

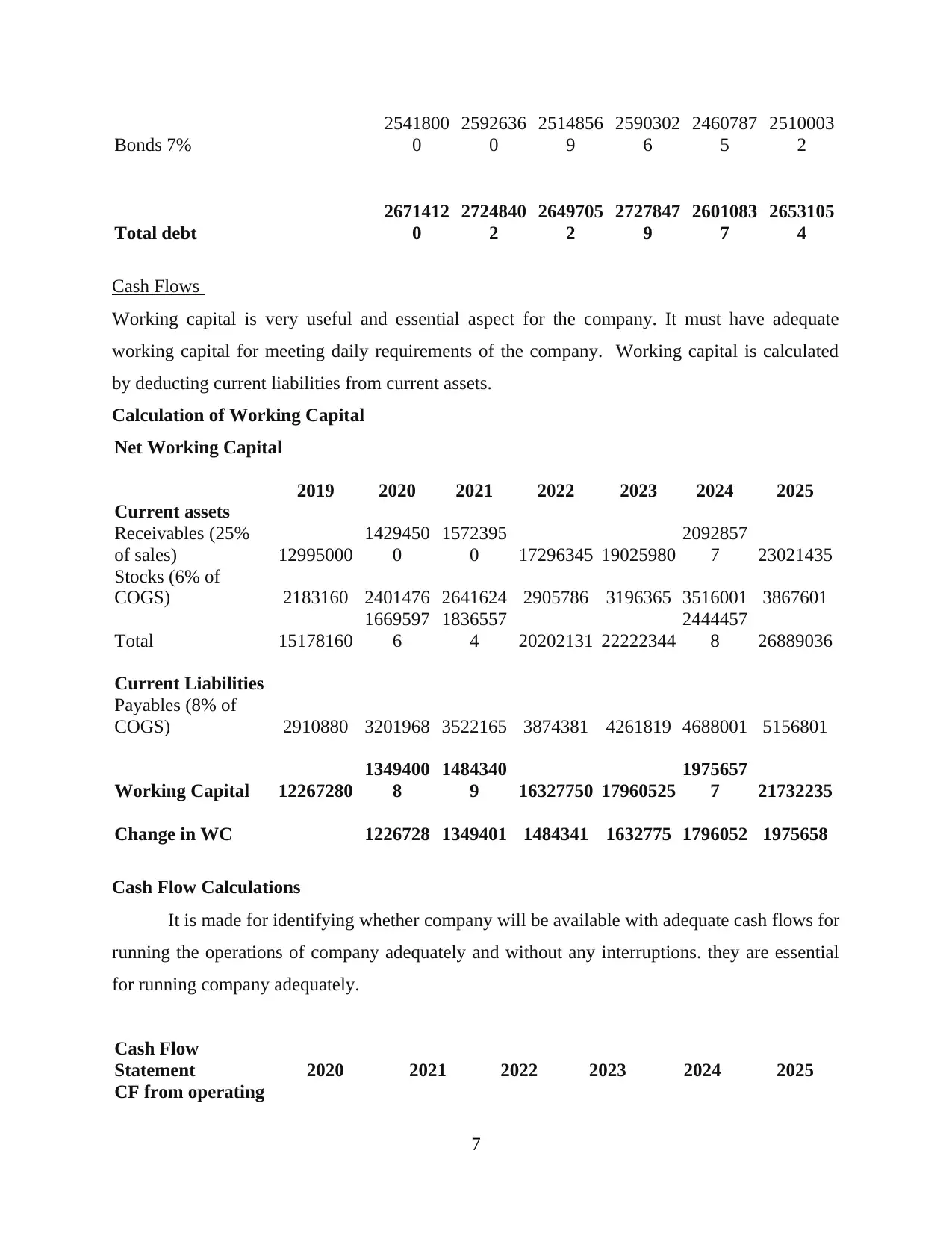

company. It has raised debt from both loan and bonds.

Debt 2019 2020 2021 2022 2023 2024 2025

Loan for Capex

Capex 1296120 1322042 1348483 1375453 1402962 1431021

Loan 1296120 1322042 1348483 1375453 1402962 1431021

Interest expense @

6.5% 82453 84248 85933 87651 89404 91193 93016

6

10%) 51980000

5717800

0

6289580

0

6918538

0 76103918

8371431

0

9208574

1

COGS (70% of sales) 36386000

4002460

0

4402706

0

4842976

6 53272743

5860001

7

6446001

9

Gross earnings 15594000

1715340

0

1886874

0

2075561

4 22831175

2511429

3

2762572

2

General and

administrative costs

(10% of COGS) 3638600 4002460 4402706 4842977 5327274 5860002 6446002

Amortisation(2% of

total assets) 1296120 1322042 1348483 1375453 1402962 1431021 1459642

EBIT 2342480 2680418 3054223 3467524 3924312 4428980 4986360

Interests on Loan 82453 84248 85933 87651 89404 91193 93016

Income tax 678008 778851 890487 1013962 1150472 1301336 1468003

Net income/Loss 1582019 1817319 2077803 2365911 2684435 3036452 3425341

Number of stocks 2694800 2694800 2694800 2694800 2694800 2694800 2694800

EPS 0.587 0.674 0.771 0.878 0.996 1.127 1.271

EPS share

Dividends 158202 181732 207780 236591 268444 303645 342534

Retained earnings 2536598 2513068 2487020 2458209 2426356 2391155 2352266

DPS 0.059 0.067 0.077 0.088 0.100 0.113 0.127

Debt

A company on large or medium scale could not run effectively and efficiently without raising

funds from the market. It is responsibility of the financial managers to identify the most suitable

source of finance for raising fund whose cost of finance is lowest and give maximum benefits to

company. It has raised debt from both loan and bonds.

Debt 2019 2020 2021 2022 2023 2024 2025

Loan for Capex

Capex 1296120 1322042 1348483 1375453 1402962 1431021

Loan 1296120 1322042 1348483 1375453 1402962 1431021

Interest expense @

6.5% 82453 84248 85933 87651 89404 91193 93016

6

Bonds 7%

2541800

0

2592636

0

2514856

9

2590302

6

2460787

5

2510003

2

Total debt

2671412

0

2724840

2

2649705

2

2727847

9

2601083

7

2653105

4

Cash Flows

Working capital is very useful and essential aspect for the company. It must have adequate

working capital for meeting daily requirements of the company. Working capital is calculated

by deducting current liabilities from current assets.

Calculation of Working Capital

Net Working Capital

2019 2020 2021 2022 2023 2024 2025

Current assets

Receivables (25%

of sales) 12995000

1429450

0

1572395

0 17296345 19025980

2092857

7 23021435

Stocks (6% of

COGS) 2183160 2401476 2641624 2905786 3196365 3516001 3867601

Total 15178160

1669597

6

1836557

4 20202131 22222344

2444457

8 26889036

Current Liabilities

Payables (8% of

COGS) 2910880 3201968 3522165 3874381 4261819 4688001 5156801

Working Capital 12267280

1349400

8

1484340

9 16327750 17960525

1975657

7 21732235

Change in WC 1226728 1349401 1484341 1632775 1796052 1975658

Cash Flow Calculations

It is made for identifying whether company will be available with adequate cash flows for

running the operations of company adequately and without any interruptions. they are essential

for running company adequately.

Cash Flow

Statement 2020 2021 2022 2023 2024 2025

CF from operating

7

2541800

0

2592636

0

2514856

9

2590302

6

2460787

5

2510003

2

Total debt

2671412

0

2724840

2

2649705

2

2727847

9

2601083

7

2653105

4

Cash Flows

Working capital is very useful and essential aspect for the company. It must have adequate

working capital for meeting daily requirements of the company. Working capital is calculated

by deducting current liabilities from current assets.

Calculation of Working Capital

Net Working Capital

2019 2020 2021 2022 2023 2024 2025

Current assets

Receivables (25%

of sales) 12995000

1429450

0

1572395

0 17296345 19025980

2092857

7 23021435

Stocks (6% of

COGS) 2183160 2401476 2641624 2905786 3196365 3516001 3867601

Total 15178160

1669597

6

1836557

4 20202131 22222344

2444457

8 26889036

Current Liabilities

Payables (8% of

COGS) 2910880 3201968 3522165 3874381 4261819 4688001 5156801

Working Capital 12267280

1349400

8

1484340

9 16327750 17960525

1975657

7 21732235

Change in WC 1226728 1349401 1484341 1632775 1796052 1975658

Cash Flow Calculations

It is made for identifying whether company will be available with adequate cash flows for

running the operations of company adequately and without any interruptions. they are essential

for running company adequately.

Cash Flow

Statement 2020 2021 2022 2023 2024 2025

CF from operating

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

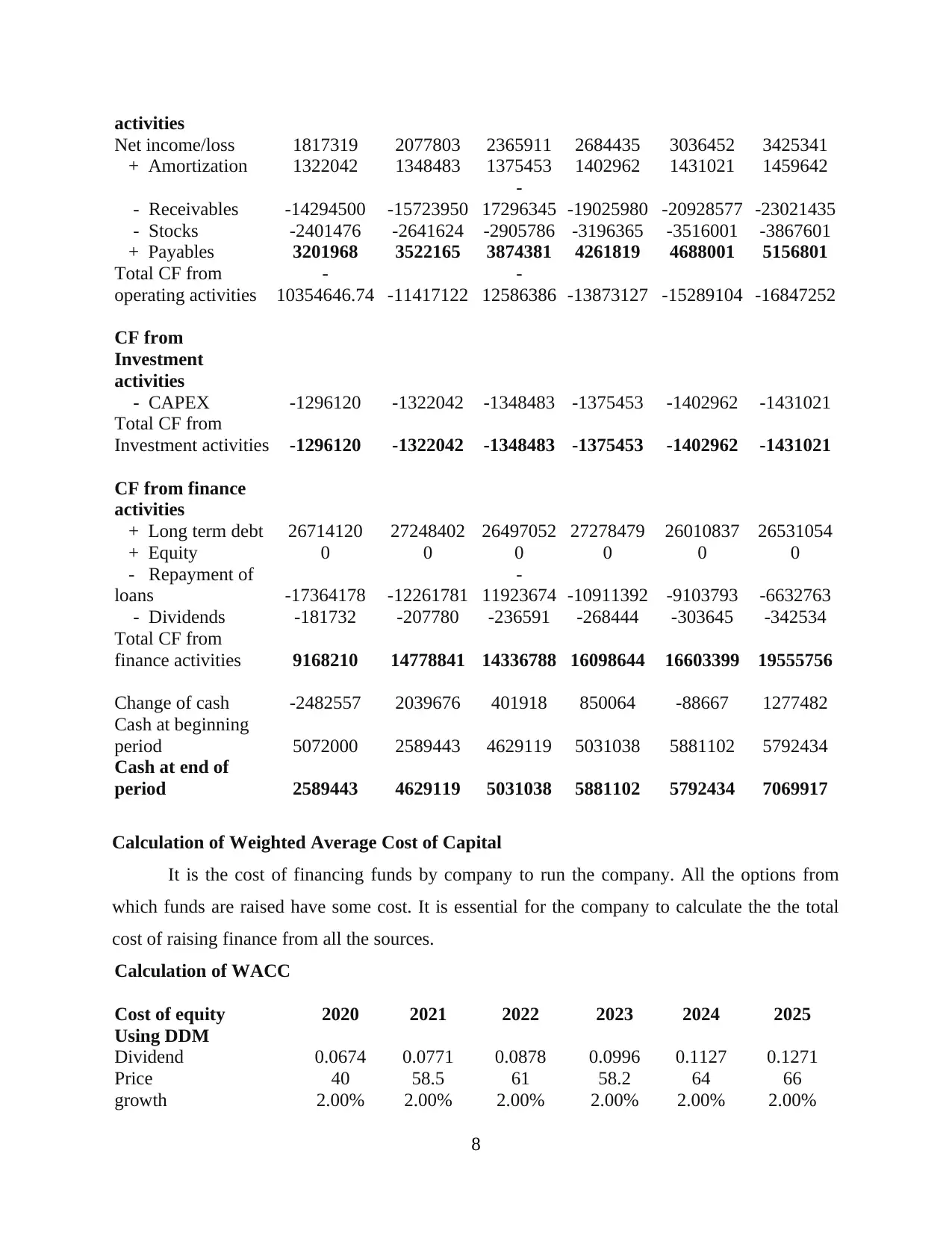

activities

Net income/loss 1817319 2077803 2365911 2684435 3036452 3425341

+ Amortization 1322042 1348483 1375453 1402962 1431021 1459642

- Receivables -14294500 -15723950

-

17296345 -19025980 -20928577 -23021435

- Stocks -2401476 -2641624 -2905786 -3196365 -3516001 -3867601

+ Payables 3201968 3522165 3874381 4261819 4688001 5156801

Total CF from

operating activities

-

10354646.74 -11417122

-

12586386 -13873127 -15289104 -16847252

CF from

Investment

activities

- CAPEX -1296120 -1322042 -1348483 -1375453 -1402962 -1431021

Total CF from

Investment activities -1296120 -1322042 -1348483 -1375453 -1402962 -1431021

CF from finance

activities

+ Long term debt 26714120 27248402 26497052 27278479 26010837 26531054

+ Equity 0 0 0 0 0 0

- Repayment of

loans -17364178 -12261781

-

11923674 -10911392 -9103793 -6632763

- Dividends -181732 -207780 -236591 -268444 -303645 -342534

Total CF from

finance activities 9168210 14778841 14336788 16098644 16603399 19555756

Change of cash -2482557 2039676 401918 850064 -88667 1277482

Cash at beginning

period 5072000 2589443 4629119 5031038 5881102 5792434

Cash at end of

period 2589443 4629119 5031038 5881102 5792434 7069917

Calculation of Weighted Average Cost of Capital

It is the cost of financing funds by company to run the company. All the options from

which funds are raised have some cost. It is essential for the company to calculate the the total

cost of raising finance from all the sources.

Calculation of WACC

Cost of equity 2020 2021 2022 2023 2024 2025

Using DDM

Dividend 0.0674 0.0771 0.0878 0.0996 0.1127 0.1271

Price 40 58.5 61 58.2 64 66

growth 2.00% 2.00% 2.00% 2.00% 2.00% 2.00%

8

Net income/loss 1817319 2077803 2365911 2684435 3036452 3425341

+ Amortization 1322042 1348483 1375453 1402962 1431021 1459642

- Receivables -14294500 -15723950

-

17296345 -19025980 -20928577 -23021435

- Stocks -2401476 -2641624 -2905786 -3196365 -3516001 -3867601

+ Payables 3201968 3522165 3874381 4261819 4688001 5156801

Total CF from

operating activities

-

10354646.74 -11417122

-

12586386 -13873127 -15289104 -16847252

CF from

Investment

activities

- CAPEX -1296120 -1322042 -1348483 -1375453 -1402962 -1431021

Total CF from

Investment activities -1296120 -1322042 -1348483 -1375453 -1402962 -1431021

CF from finance

activities

+ Long term debt 26714120 27248402 26497052 27278479 26010837 26531054

+ Equity 0 0 0 0 0 0

- Repayment of

loans -17364178 -12261781

-

11923674 -10911392 -9103793 -6632763

- Dividends -181732 -207780 -236591 -268444 -303645 -342534

Total CF from

finance activities 9168210 14778841 14336788 16098644 16603399 19555756

Change of cash -2482557 2039676 401918 850064 -88667 1277482

Cash at beginning

period 5072000 2589443 4629119 5031038 5881102 5792434

Cash at end of

period 2589443 4629119 5031038 5881102 5792434 7069917

Calculation of Weighted Average Cost of Capital

It is the cost of financing funds by company to run the company. All the options from

which funds are raised have some cost. It is essential for the company to calculate the the total

cost of raising finance from all the sources.

Calculation of WACC

Cost of equity 2020 2021 2022 2023 2024 2025

Using DDM

Dividend 0.0674 0.0771 0.0878 0.0996 0.1127 0.1271

Price 40 58.5 61 58.2 64 66

growth 2.00% 2.00% 2.00% 2.00% 2.00% 2.00%

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

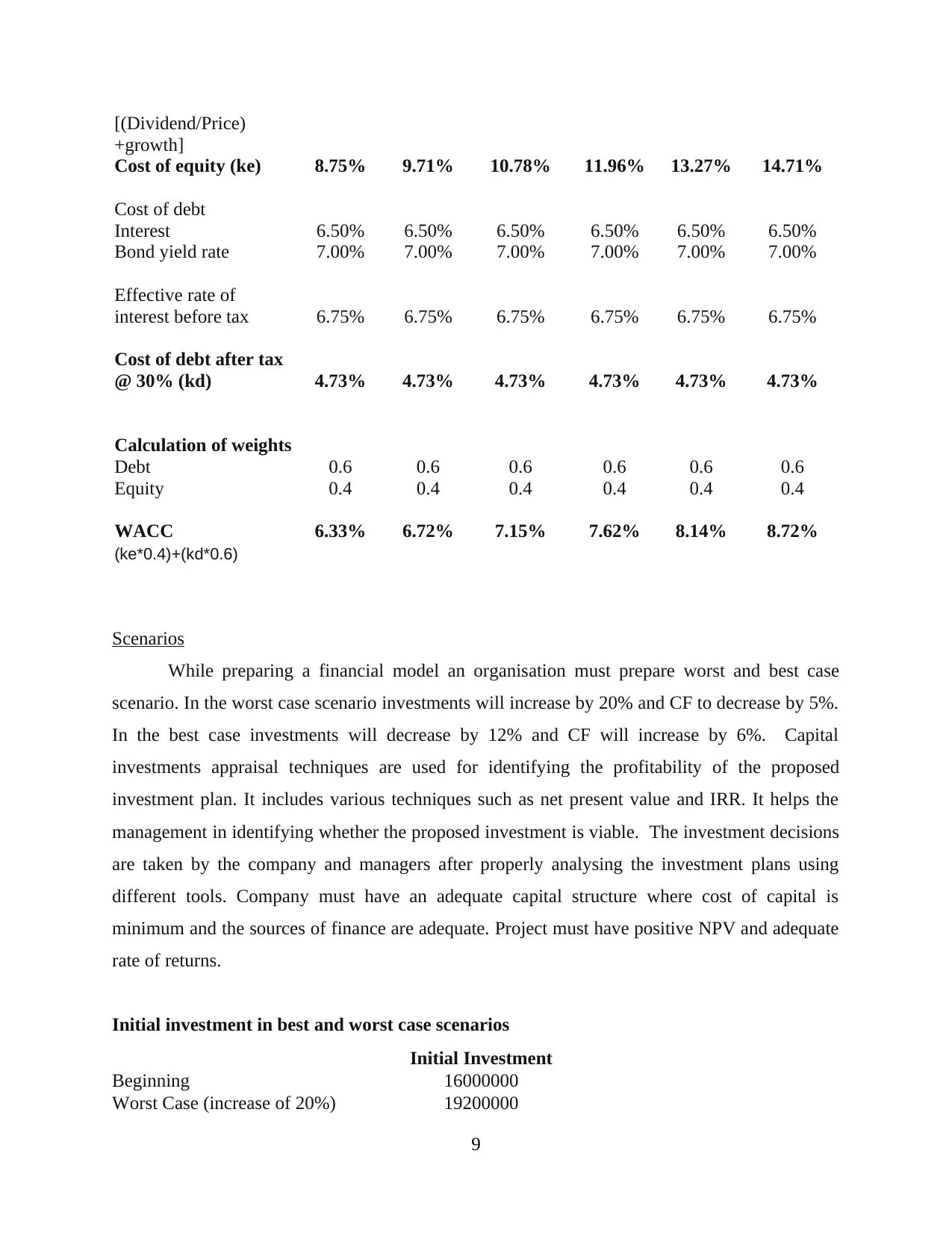

[(Dividend/Price)

+growth]

Cost of equity (ke) 8.75% 9.71% 10.78% 11.96% 13.27% 14.71%

Cost of debt

Interest 6.50% 6.50% 6.50% 6.50% 6.50% 6.50%

Bond yield rate 7.00% 7.00% 7.00% 7.00% 7.00% 7.00%

Effective rate of

interest before tax 6.75% 6.75% 6.75% 6.75% 6.75% 6.75%

Cost of debt after tax

@ 30% (kd) 4.73% 4.73% 4.73% 4.73% 4.73% 4.73%

Calculation of weights

Debt 0.6 0.6 0.6 0.6 0.6 0.6

Equity 0.4 0.4 0.4 0.4 0.4 0.4

WACC 6.33% 6.72% 7.15% 7.62% 8.14% 8.72%

(ke*0.4)+(kd*0.6)

Scenarios

While preparing a financial model an organisation must prepare worst and best case

scenario. In the worst case scenario investments will increase by 20% and CF to decrease by 5%.

In the best case investments will decrease by 12% and CF will increase by 6%. Capital

investments appraisal techniques are used for identifying the profitability of the proposed

investment plan. It includes various techniques such as net present value and IRR. It helps the

management in identifying whether the proposed investment is viable. The investment decisions

are taken by the company and managers after properly analysing the investment plans using

different tools. Company must have an adequate capital structure where cost of capital is

minimum and the sources of finance are adequate. Project must have positive NPV and adequate

rate of returns.

Initial investment in best and worst case scenarios

Initial Investment

Beginning 16000000

Worst Case (increase of 20%) 19200000

9

+growth]

Cost of equity (ke) 8.75% 9.71% 10.78% 11.96% 13.27% 14.71%

Cost of debt

Interest 6.50% 6.50% 6.50% 6.50% 6.50% 6.50%

Bond yield rate 7.00% 7.00% 7.00% 7.00% 7.00% 7.00%

Effective rate of

interest before tax 6.75% 6.75% 6.75% 6.75% 6.75% 6.75%

Cost of debt after tax

@ 30% (kd) 4.73% 4.73% 4.73% 4.73% 4.73% 4.73%

Calculation of weights

Debt 0.6 0.6 0.6 0.6 0.6 0.6

Equity 0.4 0.4 0.4 0.4 0.4 0.4

WACC 6.33% 6.72% 7.15% 7.62% 8.14% 8.72%

(ke*0.4)+(kd*0.6)

Scenarios

While preparing a financial model an organisation must prepare worst and best case

scenario. In the worst case scenario investments will increase by 20% and CF to decrease by 5%.

In the best case investments will decrease by 12% and CF will increase by 6%. Capital

investments appraisal techniques are used for identifying the profitability of the proposed

investment plan. It includes various techniques such as net present value and IRR. It helps the

management in identifying whether the proposed investment is viable. The investment decisions

are taken by the company and managers after properly analysing the investment plans using

different tools. Company must have an adequate capital structure where cost of capital is

minimum and the sources of finance are adequate. Project must have positive NPV and adequate

rate of returns.

Initial investment in best and worst case scenarios

Initial Investment

Beginning 16000000

Worst Case (increase of 20%) 19200000

9

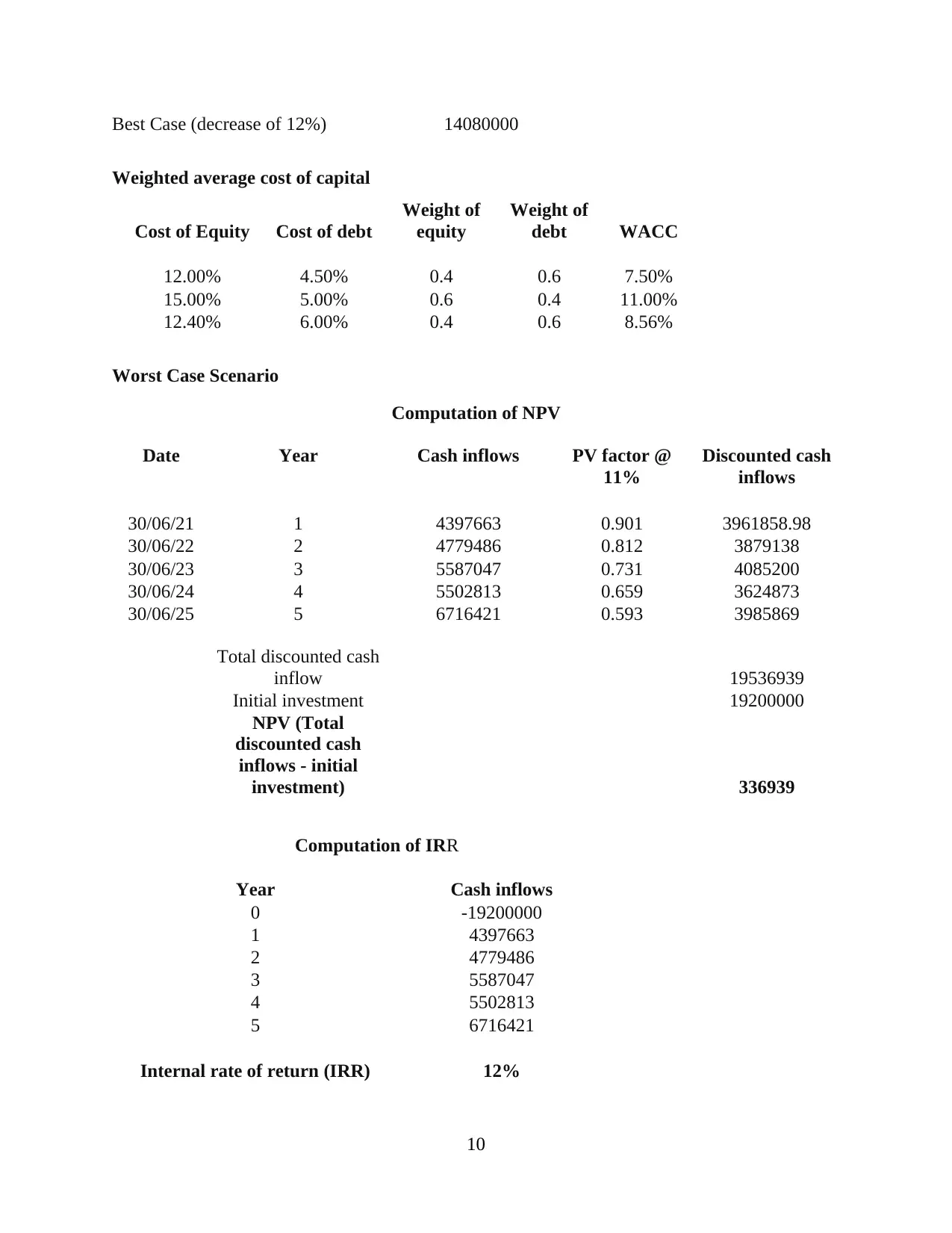

Best Case (decrease of 12%) 14080000

Weighted average cost of capital

Cost of Equity Cost of debt

Weight of

equity

Weight of

debt WACC

12.00% 4.50% 0.4 0.6 7.50%

15.00% 5.00% 0.6 0.4 11.00%

12.40% 6.00% 0.4 0.6 8.56%

Worst Case Scenario

Computation of NPV

Date Year Cash inflows PV factor @

11%

Discounted cash

inflows

30/06/21 1 4397663 0.901 3961858.98

30/06/22 2 4779486 0.812 3879138

30/06/23 3 5587047 0.731 4085200

30/06/24 4 5502813 0.659 3624873

30/06/25 5 6716421 0.593 3985869

Total discounted cash

inflow 19536939

Initial investment 19200000

NPV (Total

discounted cash

inflows - initial

investment) 336939

Computation of IRR

Year Cash inflows

0 -19200000

1 4397663

2 4779486

3 5587047

4 5502813

5 6716421

Internal rate of return (IRR) 12%

10

Weighted average cost of capital

Cost of Equity Cost of debt

Weight of

equity

Weight of

debt WACC

12.00% 4.50% 0.4 0.6 7.50%

15.00% 5.00% 0.6 0.4 11.00%

12.40% 6.00% 0.4 0.6 8.56%

Worst Case Scenario

Computation of NPV

Date Year Cash inflows PV factor @

11%

Discounted cash

inflows

30/06/21 1 4397663 0.901 3961858.98

30/06/22 2 4779486 0.812 3879138

30/06/23 3 5587047 0.731 4085200

30/06/24 4 5502813 0.659 3624873

30/06/25 5 6716421 0.593 3985869

Total discounted cash

inflow 19536939

Initial investment 19200000

NPV (Total

discounted cash

inflows - initial

investment) 336939

Computation of IRR

Year Cash inflows

0 -19200000

1 4397663

2 4779486

3 5587047

4 5502813

5 6716421

Internal rate of return (IRR) 12%

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.