In-depth Financial Management Report for MBA/MSC, KWI - 2019

VerifiedAdded on 2023/04/25

|20

|3338

|66

Report

AI Summary

This financial management report provides a comprehensive analysis of various financial concepts and techniques. It covers topics such as tax liability calculation, investment evaluation using risk and return analysis, and the importance of diversification in portfolio management. The report also delves into net funding requirements, ratio analysis for McDonald Corporation, and capital budgeting methods like payback period, accounting rate of return, net present value, and internal rate of return. Furthermore, it includes the preparation of financial statements for Winners Industries Ltd and discusses key financial axioms such as the risk-return trade-off, time value of money, and the agency problem. The analysis is supported by appendices containing detailed calculations and financial statements. Desklib offers similar solved assignments and study resources for students.

Running head: FINANCIAL MANAGEMENT

Financial Management

Name of the Student:

Name of the University:

Author’s Note:

Financial Management

Name of the Student:

Name of the University:

Author’s Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1FINANCIAL MANAGEMENT

Table of Contents

Question 1........................................................................................................................................2

Question 2........................................................................................................................................2

Question 3........................................................................................................................................3

Question 4........................................................................................................................................4

Question 5........................................................................................................................................6

Question 6........................................................................................................................................6

References......................................................................................................................................10

Appendix........................................................................................................................................12

1) Change in Net Assets..........................................................................................................12

1) Ratio Analysis.....................................................................................................................13

2) Capital Budgeting...............................................................................................................14

3) Accounts of Winners Industries..........................................................................................15

Table of Contents

Question 1........................................................................................................................................2

Question 2........................................................................................................................................2

Question 3........................................................................................................................................3

Question 4........................................................................................................................................4

Question 5........................................................................................................................................6

Question 6........................................................................................................................................6

References......................................................................................................................................10

Appendix........................................................................................................................................12

1) Change in Net Assets..........................................................................................................12

1) Ratio Analysis.....................................................................................................................13

2) Capital Budgeting...............................................................................................................14

3) Accounts of Winners Industries..........................................................................................15

2FINANCIAL MANAGEMENT

Question 1

a) The tax liability of the corporation can be calculated with the help of the given tax rate

where the corporation tax rate would be taken into consideration for determining the

taxable amount. The total tax liability that would be paid by the corporation would be

around $17,660.

b) The primary reason for the taxation is to raise revenue by the federal government in the

form of tax charged by the company for meeting the various goals and objectives of the

company. The same can be well explained with the help of the economic activities

undertaken by the government. However, there are various other social and economic

objectives that the company needs to undertake for an overall development and

sustainable growth of the economy (Babatunde, Ibukun and Oyeyemi 2017).

Question 2

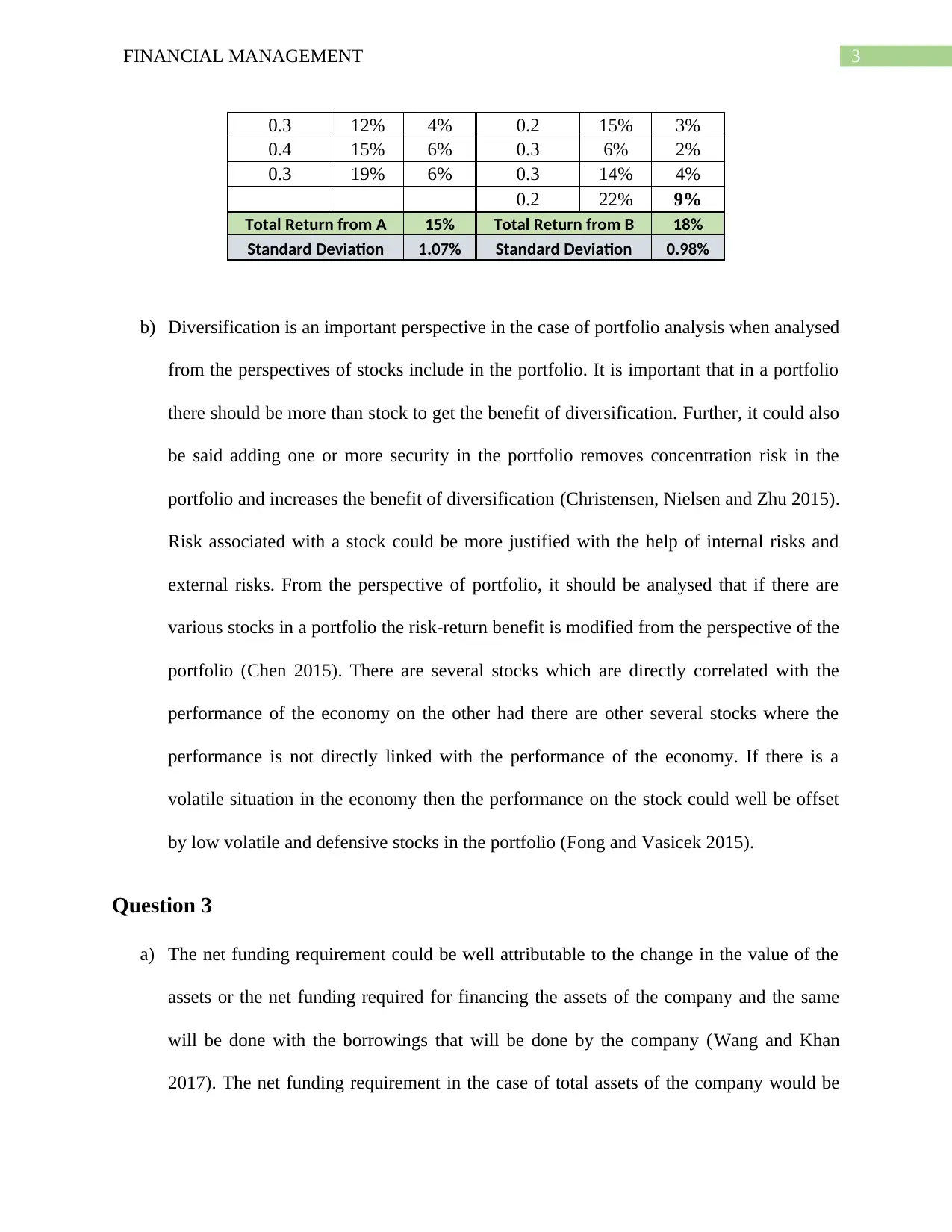

a) The investment evaluation by the Fair Incorporation should be done in accordance with

the return and risk generated by each of the stock. The return of the stock was calculated

by taking the probability figure of each of the stock and the correspondence return

generated. The return from the stock A generated was around 15% and the standard

deviation of the stock was around 1.07%. The return generated from stock B was around

18% while the standard deviation of the stock was calculated to be around 0.98%. On a

risk return basis, Stock A was assessed to be more consistent and efficient than other

Stock B (Kisman and Restiyanita 2015).

Common Stock A Total Common Stock B Total

Probabilit

y

Retur

n

Retur

n (%)

Probabilit

y

Retur

n

Retur

n (%)

Question 1

a) The tax liability of the corporation can be calculated with the help of the given tax rate

where the corporation tax rate would be taken into consideration for determining the

taxable amount. The total tax liability that would be paid by the corporation would be

around $17,660.

b) The primary reason for the taxation is to raise revenue by the federal government in the

form of tax charged by the company for meeting the various goals and objectives of the

company. The same can be well explained with the help of the economic activities

undertaken by the government. However, there are various other social and economic

objectives that the company needs to undertake for an overall development and

sustainable growth of the economy (Babatunde, Ibukun and Oyeyemi 2017).

Question 2

a) The investment evaluation by the Fair Incorporation should be done in accordance with

the return and risk generated by each of the stock. The return of the stock was calculated

by taking the probability figure of each of the stock and the correspondence return

generated. The return from the stock A generated was around 15% and the standard

deviation of the stock was around 1.07%. The return generated from stock B was around

18% while the standard deviation of the stock was calculated to be around 0.98%. On a

risk return basis, Stock A was assessed to be more consistent and efficient than other

Stock B (Kisman and Restiyanita 2015).

Common Stock A Total Common Stock B Total

Probabilit

y

Retur

n

Retur

n (%)

Probabilit

y

Retur

n

Retur

n (%)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3FINANCIAL MANAGEMENT

0.3 12% 4% 0.2 15% 3%

0.4 15% 6% 0.3 6% 2%

0.3 19% 6% 0.3 14% 4%

0.2 22% 9%

Total Return from A 15% Total Return from B 18%

Standard Deviation 1.07% Standard Deviation 0.98%

b) Diversification is an important perspective in the case of portfolio analysis when analysed

from the perspectives of stocks include in the portfolio. It is important that in a portfolio

there should be more than stock to get the benefit of diversification. Further, it could also

be said adding one or more security in the portfolio removes concentration risk in the

portfolio and increases the benefit of diversification (Christensen, Nielsen and Zhu 2015).

Risk associated with a stock could be more justified with the help of internal risks and

external risks. From the perspective of portfolio, it should be analysed that if there are

various stocks in a portfolio the risk-return benefit is modified from the perspective of the

portfolio (Chen 2015). There are several stocks which are directly correlated with the

performance of the economy on the other had there are other several stocks where the

performance is not directly linked with the performance of the economy. If there is a

volatile situation in the economy then the performance on the stock could well be offset

by low volatile and defensive stocks in the portfolio (Fong and Vasicek 2015).

Question 3

a) The net funding requirement could be well attributable to the change in the value of the

assets or the net funding required for financing the assets of the company and the same

will be done with the borrowings that will be done by the company (Wang and Khan

2017). The net funding requirement in the case of total assets of the company would be

0.3 12% 4% 0.2 15% 3%

0.4 15% 6% 0.3 6% 2%

0.3 19% 6% 0.3 14% 4%

0.2 22% 9%

Total Return from A 15% Total Return from B 18%

Standard Deviation 1.07% Standard Deviation 0.98%

b) Diversification is an important perspective in the case of portfolio analysis when analysed

from the perspectives of stocks include in the portfolio. It is important that in a portfolio

there should be more than stock to get the benefit of diversification. Further, it could also

be said adding one or more security in the portfolio removes concentration risk in the

portfolio and increases the benefit of diversification (Christensen, Nielsen and Zhu 2015).

Risk associated with a stock could be more justified with the help of internal risks and

external risks. From the perspective of portfolio, it should be analysed that if there are

various stocks in a portfolio the risk-return benefit is modified from the perspective of the

portfolio (Chen 2015). There are several stocks which are directly correlated with the

performance of the economy on the other had there are other several stocks where the

performance is not directly linked with the performance of the economy. If there is a

volatile situation in the economy then the performance on the stock could well be offset

by low volatile and defensive stocks in the portfolio (Fong and Vasicek 2015).

Question 3

a) The net funding requirement could be well attributable to the change in the value of the

assets or the net funding required for financing the assets of the company and the same

will be done with the borrowings that will be done by the company (Wang and Khan

2017). The net funding requirement in the case of total assets of the company would be

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4FINANCIAL MANAGEMENT

around $2,250,000 and the company for financing the assets in the year 2001 will borrow

the same (Appendix 1).

b) The additional fund required by Holy-Cross Enterprise would be around 1.5 million and

the same has been computed with the help of the change in the base figure that is the

revenue of the company. However, after taking account on both sides of the company that

is the liability and the assets of the company it was computed that a minimum of

$700,000 would be required for financing the net assets of the company. The same has

been done with the help of the change in the accounts payable of the company with a

change in the revenue of the company the accounts payable of the company will be

changing in the year 2001. The estimated profitability for the company in the year 2001

will be around $2 million and the same will be taken in the owner’s equity of the

company. The balance sheet and the estimated fund required by the enterprise was done

by including the factors and conditions given.

Question 4

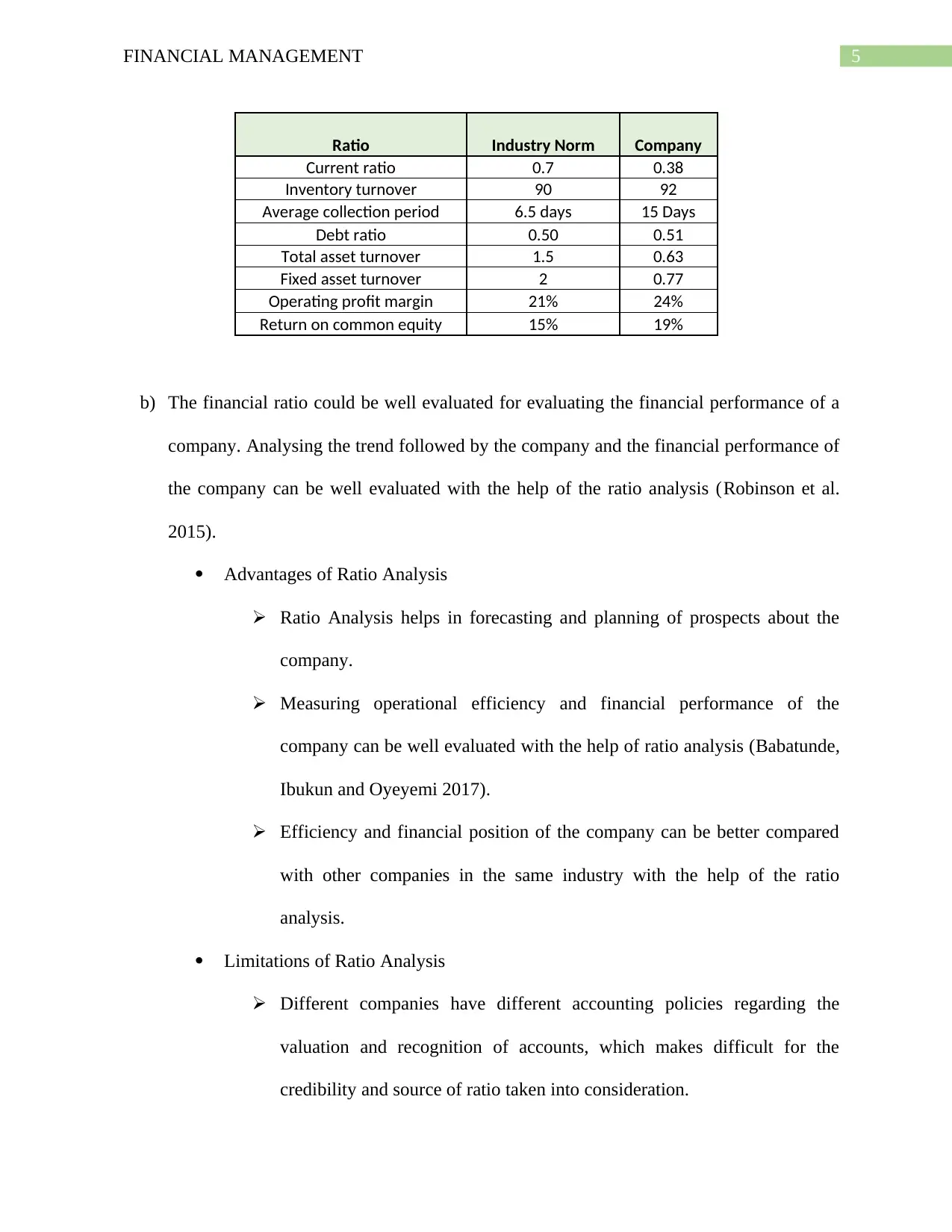

a) The ratio were calculated for the McDonald Corporation for the year ended 2016

covering the various aspects of the company. The liquidity, profitability and the activities

ratio were some of the key ratio’s that were performed for analysing the financial

condition of the company (Williams and Dobelman 2017). The ratio’s evaluated and

compared with industry standard for better understanding of the financial position of the

company (Appendix 2).

around $2,250,000 and the company for financing the assets in the year 2001 will borrow

the same (Appendix 1).

b) The additional fund required by Holy-Cross Enterprise would be around 1.5 million and

the same has been computed with the help of the change in the base figure that is the

revenue of the company. However, after taking account on both sides of the company that

is the liability and the assets of the company it was computed that a minimum of

$700,000 would be required for financing the net assets of the company. The same has

been done with the help of the change in the accounts payable of the company with a

change in the revenue of the company the accounts payable of the company will be

changing in the year 2001. The estimated profitability for the company in the year 2001

will be around $2 million and the same will be taken in the owner’s equity of the

company. The balance sheet and the estimated fund required by the enterprise was done

by including the factors and conditions given.

Question 4

a) The ratio were calculated for the McDonald Corporation for the year ended 2016

covering the various aspects of the company. The liquidity, profitability and the activities

ratio were some of the key ratio’s that were performed for analysing the financial

condition of the company (Williams and Dobelman 2017). The ratio’s evaluated and

compared with industry standard for better understanding of the financial position of the

company (Appendix 2).

5FINANCIAL MANAGEMENT

Ratio Industry Norm Company

Current ratio 0.7 0.38

Inventory turnover 90 92

Average collection period 6.5 days 15 Days

Debt ratio 0.50 0.51

Total asset turnover 1.5 0.63

Fixed asset turnover 2 0.77

Operating profit margin 21% 24%

Return on common equity 15% 19%

b) The financial ratio could be well evaluated for evaluating the financial performance of a

company. Analysing the trend followed by the company and the financial performance of

the company can be well evaluated with the help of the ratio analysis (Robinson et al.

2015).

Advantages of Ratio Analysis

Ratio Analysis helps in forecasting and planning of prospects about the

company.

Measuring operational efficiency and financial performance of the

company can be well evaluated with the help of ratio analysis (Babatunde,

Ibukun and Oyeyemi 2017).

Efficiency and financial position of the company can be better compared

with other companies in the same industry with the help of the ratio

analysis.

Limitations of Ratio Analysis

Different companies have different accounting policies regarding the

valuation and recognition of accounts, which makes difficult for the

credibility and source of ratio taken into consideration.

Ratio Industry Norm Company

Current ratio 0.7 0.38

Inventory turnover 90 92

Average collection period 6.5 days 15 Days

Debt ratio 0.50 0.51

Total asset turnover 1.5 0.63

Fixed asset turnover 2 0.77

Operating profit margin 21% 24%

Return on common equity 15% 19%

b) The financial ratio could be well evaluated for evaluating the financial performance of a

company. Analysing the trend followed by the company and the financial performance of

the company can be well evaluated with the help of the ratio analysis (Robinson et al.

2015).

Advantages of Ratio Analysis

Ratio Analysis helps in forecasting and planning of prospects about the

company.

Measuring operational efficiency and financial performance of the

company can be well evaluated with the help of ratio analysis (Babatunde,

Ibukun and Oyeyemi 2017).

Efficiency and financial position of the company can be better compared

with other companies in the same industry with the help of the ratio

analysis.

Limitations of Ratio Analysis

Different companies have different accounting policies regarding the

valuation and recognition of accounts, which makes difficult for the

credibility and source of ratio taken into consideration.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6FINANCIAL MANAGEMENT

Window Dressing is the common problem found in the accounts of a

company that makes difficult in identifying the actual worth of a company

in terms of the credible accounting source (Kisman and Restiyanita 2015).

Question 5

a) The analysis of the project was done with the help of Payback period, accounting rate of

return, Net present value and internal rate of return for the project (Appendix 3).

b) Capital Budgeting is formal process of a company for evaluating the various expenditures

and income that are taken by the company for taking the same into consideration thereby

analysing the financial performance of the company. The distinctive feature of the capital

budgeting is that there are various process and methods that can be applied thereby

including all the income and expenditure into account. The distinctive feature of the

capital budgeting is that the project taken into consideration is usually risky where the

financial viability of the same needs to be done by taking all the factors and condition

into account. Capital budgeting process like Net Present Value is concretive in nature,

which gives the result in the form of accepting or rejecting a project. The Internal rate of

project states the return generated from the project in the form of percentage wise, which

makes evaluation of the project easy when compare with the other available projects

(Hayward et al. 2017).

Question 6

a) Income statement and Balance Sheet for the Winners Industries Ltd were prepared by

taking the figures and analysis developed from the Trial Balance of the company.

b) Financial Axioms:

Window Dressing is the common problem found in the accounts of a

company that makes difficult in identifying the actual worth of a company

in terms of the credible accounting source (Kisman and Restiyanita 2015).

Question 5

a) The analysis of the project was done with the help of Payback period, accounting rate of

return, Net present value and internal rate of return for the project (Appendix 3).

b) Capital Budgeting is formal process of a company for evaluating the various expenditures

and income that are taken by the company for taking the same into consideration thereby

analysing the financial performance of the company. The distinctive feature of the capital

budgeting is that there are various process and methods that can be applied thereby

including all the income and expenditure into account. The distinctive feature of the

capital budgeting is that the project taken into consideration is usually risky where the

financial viability of the same needs to be done by taking all the factors and condition

into account. Capital budgeting process like Net Present Value is concretive in nature,

which gives the result in the form of accepting or rejecting a project. The Internal rate of

project states the return generated from the project in the form of percentage wise, which

makes evaluation of the project easy when compare with the other available projects

(Hayward et al. 2017).

Question 6

a) Income statement and Balance Sheet for the Winners Industries Ltd were prepared by

taking the figures and analysis developed from the Trial Balance of the company.

b) Financial Axioms:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7FINANCIAL MANAGEMENT

Risk Return Trade Off: The spectrum shows the relationship between the return

generated by a stock by undertaking the risk associated with a project. The trade-

off theory states the amount or potential return that can be generated by a stock by

undertaking the risk associated with the same (Neale et al. 2017).

Time Value of Money: The time value of money concepts shows the amount or

worth of receiving an amount today rather than on a later period. The principle

shows that the provided money can help in earning money in the form of interest

for the amount received today.

Cash is King: Cash is an integral part of an company which helps them in

maintaining liquidity in the company in the form of uninterrupted operations.

Cash is an integral part of the company helping them in making the operations of

the company efficient (Clubb 2015).

Incremental Cash Flows: The incremental cash flows shows the additional

revenue or the income that would be generated by a project and the same shows

the increased chances of a company in accepting the project.

Agency Problem: The agency problem reflects the conflict arising in an

organisation due to diversifying interest of the organisation. It is important that

both the stakeholders and the management of the company have a common goal

of interest in order to promote the growth and success of the company.

Taxes Biased Business Decision: There are several case when companies goes

ahead with initiating a transactions on the basis of the amount of tax shield the

company will be getting from the same. However, it is recommended that the

Risk Return Trade Off: The spectrum shows the relationship between the return

generated by a stock by undertaking the risk associated with a project. The trade-

off theory states the amount or potential return that can be generated by a stock by

undertaking the risk associated with the same (Neale et al. 2017).

Time Value of Money: The time value of money concepts shows the amount or

worth of receiving an amount today rather than on a later period. The principle

shows that the provided money can help in earning money in the form of interest

for the amount received today.

Cash is King: Cash is an integral part of an company which helps them in

maintaining liquidity in the company in the form of uninterrupted operations.

Cash is an integral part of the company helping them in making the operations of

the company efficient (Clubb 2015).

Incremental Cash Flows: The incremental cash flows shows the additional

revenue or the income that would be generated by a project and the same shows

the increased chances of a company in accepting the project.

Agency Problem: The agency problem reflects the conflict arising in an

organisation due to diversifying interest of the organisation. It is important that

both the stakeholders and the management of the company have a common goal

of interest in order to promote the growth and success of the company.

Taxes Biased Business Decision: There are several case when companies goes

ahead with initiating a transactions on the basis of the amount of tax shield the

company will be getting from the same. However, it is recommended that the

8FINANCIAL MANAGEMENT

long-term and important decisions be taken in the best interest of the stakeholders

of the company.

Risks: There are primarily two basic types of risks that affects a company and the

same could be classified as financial risks and business risks. Financial risk is the

risk associated due to high amount of debt or leverage in the overall capital

structure of the company. Business risk on the other hand is due to the changing

market conditions, business factors and various other internal factors of the

company that can significantly affect the operations of the company.

Ethical Guideline in Finance: Ethics play an important part in every industry

and organisations where the principles of ethics play an important role in guiding

the workings of the company and industry on an overall basis. There are several

regulatory bodies and institutions that lays down the principles and guidelines in a

organisation for better management of various activities and operations.

Curse of Competitive Market: The curse of the competitive market could well be

explained in the context of Oligopoly and Perfect Competition Market where the

level of competition is high. High level of competition often degrades the quality

of the product or exploit the customers if there is an absence of any regulatory

environment.

Efficient Capital Markets: Efficient Capital Market can be referred to market

where the informations and important financial data related to a stock is

incorporated quickly in the price of the assets. The reflected stock price in the

market shows the correct and full potential price of the stock determined by

taking the value of all available informations.

long-term and important decisions be taken in the best interest of the stakeholders

of the company.

Risks: There are primarily two basic types of risks that affects a company and the

same could be classified as financial risks and business risks. Financial risk is the

risk associated due to high amount of debt or leverage in the overall capital

structure of the company. Business risk on the other hand is due to the changing

market conditions, business factors and various other internal factors of the

company that can significantly affect the operations of the company.

Ethical Guideline in Finance: Ethics play an important part in every industry

and organisations where the principles of ethics play an important role in guiding

the workings of the company and industry on an overall basis. There are several

regulatory bodies and institutions that lays down the principles and guidelines in a

organisation for better management of various activities and operations.

Curse of Competitive Market: The curse of the competitive market could well be

explained in the context of Oligopoly and Perfect Competition Market where the

level of competition is high. High level of competition often degrades the quality

of the product or exploit the customers if there is an absence of any regulatory

environment.

Efficient Capital Markets: Efficient Capital Market can be referred to market

where the informations and important financial data related to a stock is

incorporated quickly in the price of the assets. The reflected stock price in the

market shows the correct and full potential price of the stock determined by

taking the value of all available informations.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9FINANCIAL MANAGEMENT

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10FINANCIAL MANAGEMENT

References

Andor, G., Mohanty, S.K. and Toth, T., 2015. Capital budgeting practices: A survey of Central

and Eastern European firms. Emerging Markets Review, 23, pp.148-172.

Babatunde, O.A., Ibukun, A.O. and Oyeyemi, O.G., 2017. Taxation revenue and economic

growth in Africa. Journal of Accounting and Taxation, 9(2), pp.11-22.

Boyas, E. and Teeter, R., 2017. Teaching Financial Ratio Analysis using XBRL. In

Developments in Business Simulation and Experiential Learning: Proceedings of the Annual

ABSEL conference (Vol. 44, No. 1).

Chen, M., 2015. Risk-return tradeoff in Chinese stock markets: some recent evidence.

International Journal of Emerging Markets, 10(3), pp.448-473.

Christensen, B.J., Nielsen, M.Ø. and Zhu, J., 2015. The impact of financial crises on the risk–

return tradeoff and the leverage effect. Economic Modelling, 49, pp.407-418.

Clubb, C., 2015. Information Content of Cash Flows. Wiley Encyclopedia of Management, pp.1-

6.

Fong, H.G. and Vasicek, O., 2015. The Tradeoff between Return and Risk in Immunized

Portfolios. Finance, Economics, and Mathematics, 39(5), p.203.

Hayward, M., Caldwell, A., Steen, J., Gow, D. and Liesch, P., 2017. Entrepreneurs’ capital

budgeting orientations and innovation outputs: Evidence from Australian biotechnology firms.

Long Range Planning, 50(2), pp.121-133.

References

Andor, G., Mohanty, S.K. and Toth, T., 2015. Capital budgeting practices: A survey of Central

and Eastern European firms. Emerging Markets Review, 23, pp.148-172.

Babatunde, O.A., Ibukun, A.O. and Oyeyemi, O.G., 2017. Taxation revenue and economic

growth in Africa. Journal of Accounting and Taxation, 9(2), pp.11-22.

Boyas, E. and Teeter, R., 2017. Teaching Financial Ratio Analysis using XBRL. In

Developments in Business Simulation and Experiential Learning: Proceedings of the Annual

ABSEL conference (Vol. 44, No. 1).

Chen, M., 2015. Risk-return tradeoff in Chinese stock markets: some recent evidence.

International Journal of Emerging Markets, 10(3), pp.448-473.

Christensen, B.J., Nielsen, M.Ø. and Zhu, J., 2015. The impact of financial crises on the risk–

return tradeoff and the leverage effect. Economic Modelling, 49, pp.407-418.

Clubb, C., 2015. Information Content of Cash Flows. Wiley Encyclopedia of Management, pp.1-

6.

Fong, H.G. and Vasicek, O., 2015. The Tradeoff between Return and Risk in Immunized

Portfolios. Finance, Economics, and Mathematics, 39(5), p.203.

Hayward, M., Caldwell, A., Steen, J., Gow, D. and Liesch, P., 2017. Entrepreneurs’ capital

budgeting orientations and innovation outputs: Evidence from Australian biotechnology firms.

Long Range Planning, 50(2), pp.121-133.

11FINANCIAL MANAGEMENT

Kisman, Z. and Restiyanita, S., 2015. M. The Validity of Capital Asset Pricing Model (CAPM)

and Arbitrage Pricing Theory (APT) in Predicting the Return of Stocks in Indonesia Stock

Exchange. American Journal of Economics, Finance and Management Vol, 1, pp.184-189.

Neale, J., Black, L., Getty, M., Hogan, C., Lennon, P., Lora, C., McDonald, R., Strang, J.,

Tompkins, C., Usher, J. and Villa, G., 2017. Paying participants in addiction research: Is cash

king?. Journal of Substance Use, 22(5), pp.531-533.

Robinson, T.R., Henry, E., Pirie, W.L. and Broihahn, M.A., 2015. International financial

statement analysis. John Wiley & Sons.

Wang, Z. and Khan, M.M., 2017. Market states and the risk-return tradeoff. The Quarterly

Review of Economics and Finance, 65, pp.314-327.

Williams, E.E. and Dobelman, J.A., 2017. Financial statement analysis. World Scientific Book

Chapters, pp.109-169.

Kisman, Z. and Restiyanita, S., 2015. M. The Validity of Capital Asset Pricing Model (CAPM)

and Arbitrage Pricing Theory (APT) in Predicting the Return of Stocks in Indonesia Stock

Exchange. American Journal of Economics, Finance and Management Vol, 1, pp.184-189.

Neale, J., Black, L., Getty, M., Hogan, C., Lennon, P., Lora, C., McDonald, R., Strang, J.,

Tompkins, C., Usher, J. and Villa, G., 2017. Paying participants in addiction research: Is cash

king?. Journal of Substance Use, 22(5), pp.531-533.

Robinson, T.R., Henry, E., Pirie, W.L. and Broihahn, M.A., 2015. International financial

statement analysis. John Wiley & Sons.

Wang, Z. and Khan, M.M., 2017. Market states and the risk-return tradeoff. The Quarterly

Review of Economics and Finance, 65, pp.314-327.

Williams, E.E. and Dobelman, J.A., 2017. Financial statement analysis. World Scientific Book

Chapters, pp.109-169.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.