Cash Budgets and Zero Based Budgeting

VerifiedAdded on 2023/01/18

|12

|2735

|30

AI Summary

This document provides an introduction to financial management and the importance of cash budgets for businesses. It also explains the concept of zero based budgeting and its advantages over traditional budgeting. The document includes a cash budget for a hotel for the year 2020 and discusses the process of zero based budgeting. It is relevant for students studying financial management or budgeting techniques.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

Cash Budgets for the year from January to December for the year 2020 of Hotel Haversons ...1

TASK 2............................................................................................................................................5

a) Zero Based Budgeting and its process.....................................................................................5

b) Assess advantages zero based budgeting is having over traditional budgeting......................6

C) Organisations introducing zero based budgeting technique in practical terms.......................8

CONCLUSION ...............................................................................................................................8

REFERENCES..............................................................................................................................10

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

Cash Budgets for the year from January to December for the year 2020 of Hotel Haversons ...1

TASK 2............................................................................................................................................5

a) Zero Based Budgeting and its process.....................................................................................5

b) Assess advantages zero based budgeting is having over traditional budgeting......................6

C) Organisations introducing zero based budgeting technique in practical terms.......................8

CONCLUSION ...............................................................................................................................8

REFERENCES..............................................................................................................................10

INTRODUCTION

Financial management refers to organising, planning, directing & controlling financial

activities like procuring and utilising the funds of enterprise. It refers to application of general

principles of management to financial resources of enterprise. Financial management is

undertaken ensuring regular & adequate supply of the funds . For ensuring that adequate returns

are available to the shareholders that depends on earning capacity, share's market prices and their

expectations (Financial Management, 2019). They enable the company to effectively utilise the

funds of company. Financial management involves various activities that are undertaken by the

management for effectively managing different operations of the business. Mostly companies

have separate department for managing the financial affairs of company (Mitchell and Calabrese,

2018). For financial management, financial managers are appointed by companies. It involves

various budgeting techniques like traditional budgeting, cash budgeting, zero based budgeting

and many more. The present report is about the Haverson Ltd that manages chain of hotels in

Europe and United Kingdom. One of its hotel of the group is situated in United Kingdom

Llantwit have identical 80 double rooms and 50 two bed rooms for which standard rate of 100

pound is charged per night. Report will give monthly cash budget for the hotel and understanding

about the zero based budgeting and its importance over traditional budgeting.

TASK 1

Cash Budgets

Cash budget could be defined as an estimation of cash flows for business over specific

time periods. The budget is generally used for assessing that company is having sufficient cash

for for its operations. Organisations uses sales & production forecasts for creating cash budgets,

with the assumptions associated with necessary spendings and the accounts receivable. If

company do not have required liquidity for its operations it should raise capital using through

issue of stocks or debts (Bratton,2018). Cash budget computes cash inflow and cash outflow for

given period. Budget allows company to forecast about the cash requirements for the year (Cash

Budgets, 2019).

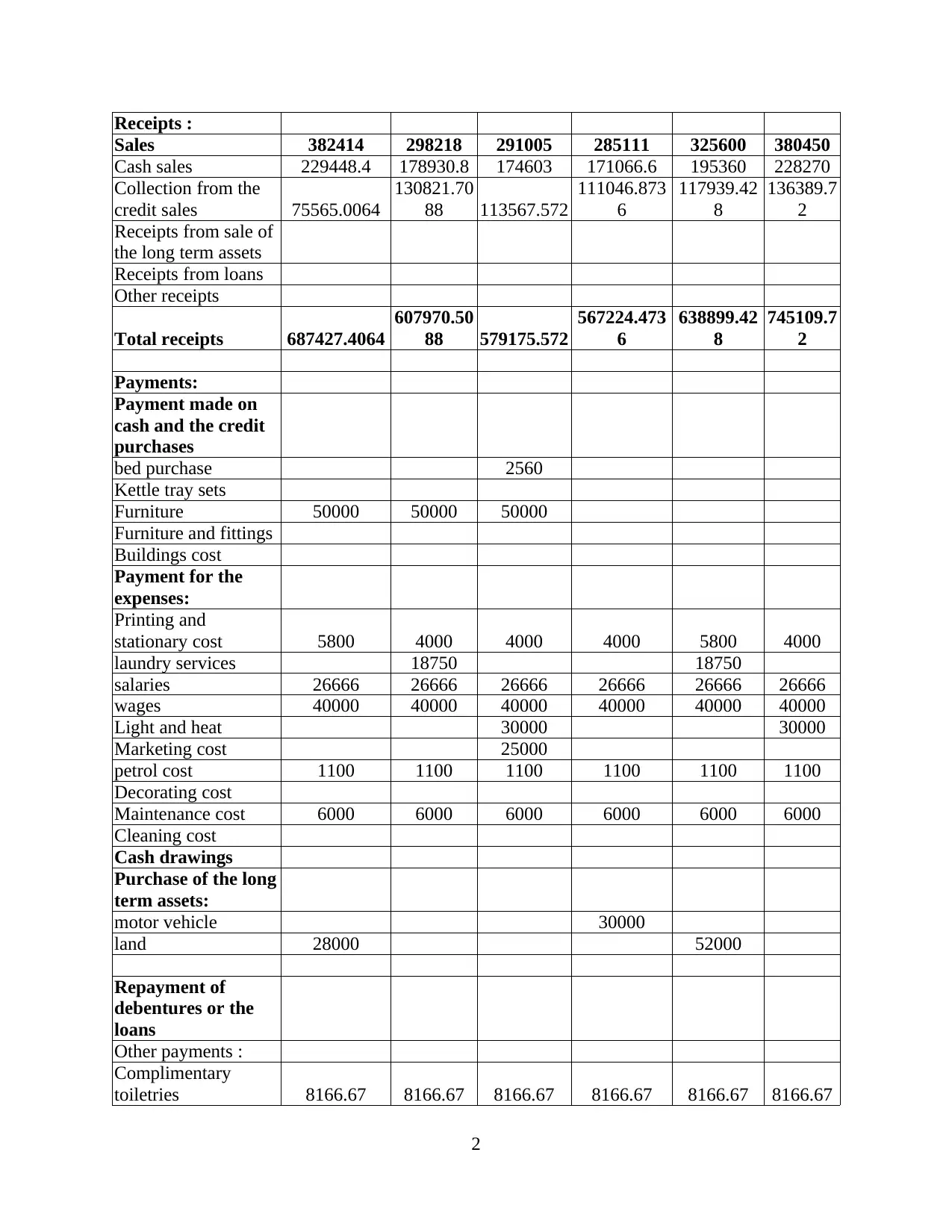

Cash Budgets for the year from January to December for the year 2020 of Hotel Haversons

Particulars January February March April May June

1

Financial management refers to organising, planning, directing & controlling financial

activities like procuring and utilising the funds of enterprise. It refers to application of general

principles of management to financial resources of enterprise. Financial management is

undertaken ensuring regular & adequate supply of the funds . For ensuring that adequate returns

are available to the shareholders that depends on earning capacity, share's market prices and their

expectations (Financial Management, 2019). They enable the company to effectively utilise the

funds of company. Financial management involves various activities that are undertaken by the

management for effectively managing different operations of the business. Mostly companies

have separate department for managing the financial affairs of company (Mitchell and Calabrese,

2018). For financial management, financial managers are appointed by companies. It involves

various budgeting techniques like traditional budgeting, cash budgeting, zero based budgeting

and many more. The present report is about the Haverson Ltd that manages chain of hotels in

Europe and United Kingdom. One of its hotel of the group is situated in United Kingdom

Llantwit have identical 80 double rooms and 50 two bed rooms for which standard rate of 100

pound is charged per night. Report will give monthly cash budget for the hotel and understanding

about the zero based budgeting and its importance over traditional budgeting.

TASK 1

Cash Budgets

Cash budget could be defined as an estimation of cash flows for business over specific

time periods. The budget is generally used for assessing that company is having sufficient cash

for for its operations. Organisations uses sales & production forecasts for creating cash budgets,

with the assumptions associated with necessary spendings and the accounts receivable. If

company do not have required liquidity for its operations it should raise capital using through

issue of stocks or debts (Bratton,2018). Cash budget computes cash inflow and cash outflow for

given period. Budget allows company to forecast about the cash requirements for the year (Cash

Budgets, 2019).

Cash Budgets for the year from January to December for the year 2020 of Hotel Haversons

Particulars January February March April May June

1

Receipts :

Sales 382414 298218 291005 285111 325600 380450

Cash sales 229448.4 178930.8 174603 171066.6 195360 228270

Collection from the

credit sales 75565.0064

130821.70

88 113567.572

111046.873

6

117939.42

8

136389.7

2

Receipts from sale of

the long term assets

Receipts from loans

Other receipts

Total receipts 687427.4064

607970.50

88 579175.572

567224.473

6

638899.42

8

745109.7

2

Payments:

Payment made on

cash and the credit

purchases

bed purchase 2560

Kettle tray sets

Furniture 50000 50000 50000

Furniture and fittings

Buildings cost

Payment for the

expenses:

Printing and

stationary cost 5800 4000 4000 4000 5800 4000

laundry services 18750 18750

salaries 26666 26666 26666 26666 26666 26666

wages 40000 40000 40000 40000 40000 40000

Light and heat 30000 30000

Marketing cost 25000

petrol cost 1100 1100 1100 1100 1100 1100

Decorating cost

Maintenance cost 6000 6000 6000 6000 6000 6000

Cleaning cost

Cash drawings

Purchase of the long

term assets:

motor vehicle 30000

land 28000 52000

Repayment of

debentures or the

loans

Other payments :

Complimentary

toiletries 8166.67 8166.67 8166.67 8166.67 8166.67 8166.67

2

Sales 382414 298218 291005 285111 325600 380450

Cash sales 229448.4 178930.8 174603 171066.6 195360 228270

Collection from the

credit sales 75565.0064

130821.70

88 113567.572

111046.873

6

117939.42

8

136389.7

2

Receipts from sale of

the long term assets

Receipts from loans

Other receipts

Total receipts 687427.4064

607970.50

88 579175.572

567224.473

6

638899.42

8

745109.7

2

Payments:

Payment made on

cash and the credit

purchases

bed purchase 2560

Kettle tray sets

Furniture 50000 50000 50000

Furniture and fittings

Buildings cost

Payment for the

expenses:

Printing and

stationary cost 5800 4000 4000 4000 5800 4000

laundry services 18750 18750

salaries 26666 26666 26666 26666 26666 26666

wages 40000 40000 40000 40000 40000 40000

Light and heat 30000 30000

Marketing cost 25000

petrol cost 1100 1100 1100 1100 1100 1100

Decorating cost

Maintenance cost 6000 6000 6000 6000 6000 6000

Cleaning cost

Cash drawings

Purchase of the long

term assets:

motor vehicle 30000

land 28000 52000

Repayment of

debentures or the

loans

Other payments :

Complimentary

toiletries 8166.67 8166.67 8166.67 8166.67 8166.67 8166.67

2

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

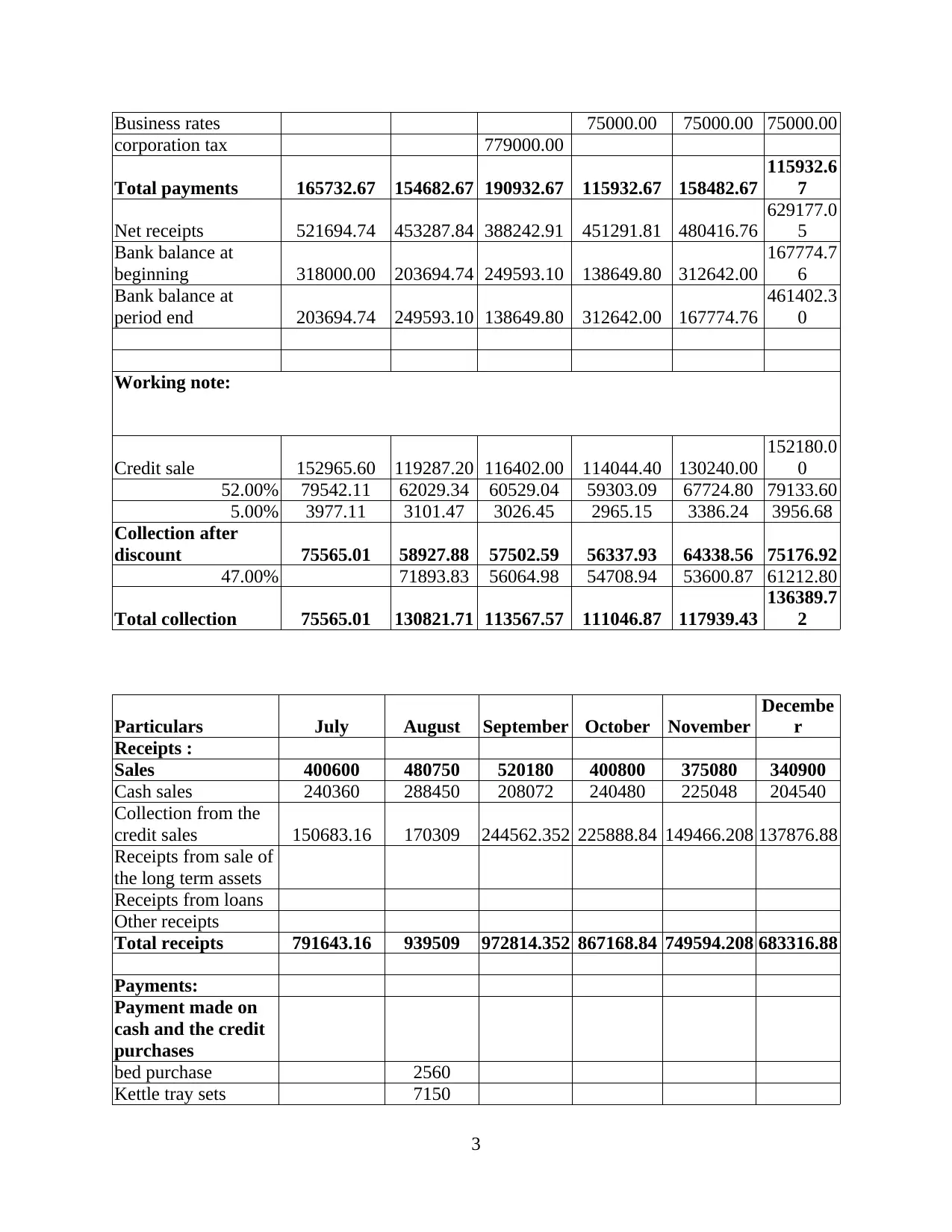

Business rates 75000.00 75000.00 75000.00

corporation tax 779000.00

Total payments 165732.67 154682.67 190932.67 115932.67 158482.67

115932.6

7

Net receipts 521694.74 453287.84 388242.91 451291.81 480416.76

629177.0

5

Bank balance at

beginning 318000.00 203694.74 249593.10 138649.80 312642.00

167774.7

6

Bank balance at

period end 203694.74 249593.10 138649.80 312642.00 167774.76

461402.3

0

Working note:

Credit sale 152965.60 119287.20 116402.00 114044.40 130240.00

152180.0

0

52.00% 79542.11 62029.34 60529.04 59303.09 67724.80 79133.60

5.00% 3977.11 3101.47 3026.45 2965.15 3386.24 3956.68

Collection after

discount 75565.01 58927.88 57502.59 56337.93 64338.56 75176.92

47.00% 71893.83 56064.98 54708.94 53600.87 61212.80

Total collection 75565.01 130821.71 113567.57 111046.87 117939.43

136389.7

2

Particulars July August September October November

Decembe

r

Receipts :

Sales 400600 480750 520180 400800 375080 340900

Cash sales 240360 288450 208072 240480 225048 204540

Collection from the

credit sales 150683.16 170309 244562.352 225888.84 149466.208 137876.88

Receipts from sale of

the long term assets

Receipts from loans

Other receipts

Total receipts 791643.16 939509 972814.352 867168.84 749594.208 683316.88

Payments:

Payment made on

cash and the credit

purchases

bed purchase 2560

Kettle tray sets 7150

3

corporation tax 779000.00

Total payments 165732.67 154682.67 190932.67 115932.67 158482.67

115932.6

7

Net receipts 521694.74 453287.84 388242.91 451291.81 480416.76

629177.0

5

Bank balance at

beginning 318000.00 203694.74 249593.10 138649.80 312642.00

167774.7

6

Bank balance at

period end 203694.74 249593.10 138649.80 312642.00 167774.76

461402.3

0

Working note:

Credit sale 152965.60 119287.20 116402.00 114044.40 130240.00

152180.0

0

52.00% 79542.11 62029.34 60529.04 59303.09 67724.80 79133.60

5.00% 3977.11 3101.47 3026.45 2965.15 3386.24 3956.68

Collection after

discount 75565.01 58927.88 57502.59 56337.93 64338.56 75176.92

47.00% 71893.83 56064.98 54708.94 53600.87 61212.80

Total collection 75565.01 130821.71 113567.57 111046.87 117939.43

136389.7

2

Particulars July August September October November

Decembe

r

Receipts :

Sales 400600 480750 520180 400800 375080 340900

Cash sales 240360 288450 208072 240480 225048 204540

Collection from the

credit sales 150683.16 170309 244562.352 225888.84 149466.208 137876.88

Receipts from sale of

the long term assets

Receipts from loans

Other receipts

Total receipts 791643.16 939509 972814.352 867168.84 749594.208 683316.88

Payments:

Payment made on

cash and the credit

purchases

bed purchase 2560

Kettle tray sets 7150

3

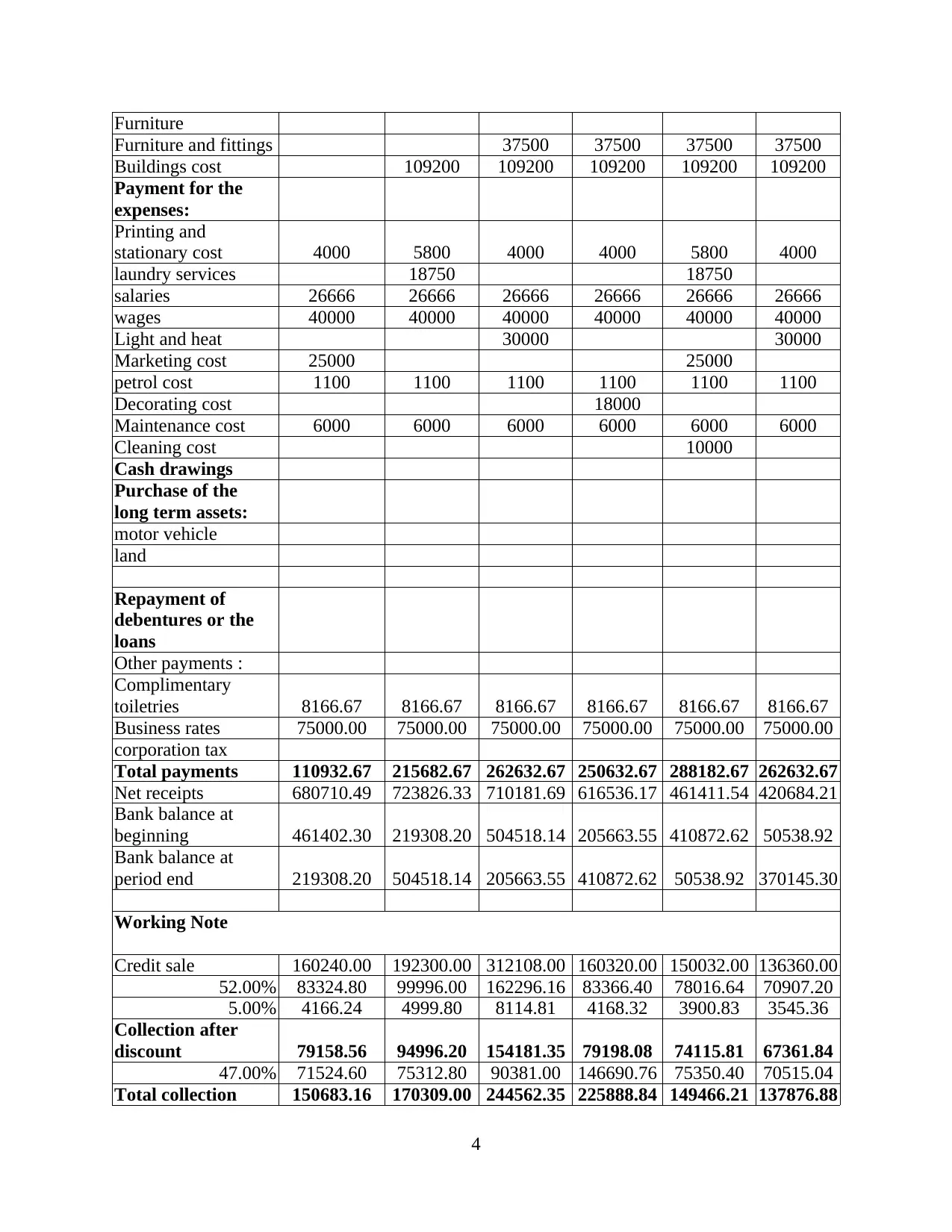

Furniture

Furniture and fittings 37500 37500 37500 37500

Buildings cost 109200 109200 109200 109200 109200

Payment for the

expenses:

Printing and

stationary cost 4000 5800 4000 4000 5800 4000

laundry services 18750 18750

salaries 26666 26666 26666 26666 26666 26666

wages 40000 40000 40000 40000 40000 40000

Light and heat 30000 30000

Marketing cost 25000 25000

petrol cost 1100 1100 1100 1100 1100 1100

Decorating cost 18000

Maintenance cost 6000 6000 6000 6000 6000 6000

Cleaning cost 10000

Cash drawings

Purchase of the

long term assets:

motor vehicle

land

Repayment of

debentures or the

loans

Other payments :

Complimentary

toiletries 8166.67 8166.67 8166.67 8166.67 8166.67 8166.67

Business rates 75000.00 75000.00 75000.00 75000.00 75000.00 75000.00

corporation tax

Total payments 110932.67 215682.67 262632.67 250632.67 288182.67 262632.67

Net receipts 680710.49 723826.33 710181.69 616536.17 461411.54 420684.21

Bank balance at

beginning 461402.30 219308.20 504518.14 205663.55 410872.62 50538.92

Bank balance at

period end 219308.20 504518.14 205663.55 410872.62 50538.92 370145.30

Working Note

Credit sale 160240.00 192300.00 312108.00 160320.00 150032.00 136360.00

52.00% 83324.80 99996.00 162296.16 83366.40 78016.64 70907.20

5.00% 4166.24 4999.80 8114.81 4168.32 3900.83 3545.36

Collection after

discount 79158.56 94996.20 154181.35 79198.08 74115.81 67361.84

47.00% 71524.60 75312.80 90381.00 146690.76 75350.40 70515.04

Total collection 150683.16 170309.00 244562.35 225888.84 149466.21 137876.88

4

Furniture and fittings 37500 37500 37500 37500

Buildings cost 109200 109200 109200 109200 109200

Payment for the

expenses:

Printing and

stationary cost 4000 5800 4000 4000 5800 4000

laundry services 18750 18750

salaries 26666 26666 26666 26666 26666 26666

wages 40000 40000 40000 40000 40000 40000

Light and heat 30000 30000

Marketing cost 25000 25000

petrol cost 1100 1100 1100 1100 1100 1100

Decorating cost 18000

Maintenance cost 6000 6000 6000 6000 6000 6000

Cleaning cost 10000

Cash drawings

Purchase of the

long term assets:

motor vehicle

land

Repayment of

debentures or the

loans

Other payments :

Complimentary

toiletries 8166.67 8166.67 8166.67 8166.67 8166.67 8166.67

Business rates 75000.00 75000.00 75000.00 75000.00 75000.00 75000.00

corporation tax

Total payments 110932.67 215682.67 262632.67 250632.67 288182.67 262632.67

Net receipts 680710.49 723826.33 710181.69 616536.17 461411.54 420684.21

Bank balance at

beginning 461402.30 219308.20 504518.14 205663.55 410872.62 50538.92

Bank balance at

period end 219308.20 504518.14 205663.55 410872.62 50538.92 370145.30

Working Note

Credit sale 160240.00 192300.00 312108.00 160320.00 150032.00 136360.00

52.00% 83324.80 99996.00 162296.16 83366.40 78016.64 70907.20

5.00% 4166.24 4999.80 8114.81 4168.32 3900.83 3545.36

Collection after

discount 79158.56 94996.20 154181.35 79198.08 74115.81 67361.84

47.00% 71524.60 75312.80 90381.00 146690.76 75350.40 70515.04

Total collection 150683.16 170309.00 244562.35 225888.84 149466.21 137876.88

4

TASK 2

a) Zero Based Budgeting and its process.

For staying on top of business expenses, companies are are required to plan and update

constantly the business budgets. When companies are using traditional budgeting method they

use previous budgets that might not be effective way of preparing a budget.

Zero Based Budgeting

Zero Based Budgeting is defined as the method that is used for preparing budget of

company for specific time periods under the consideration where the budgets of company are set

from the scratch after all activities of company are re-evaluated from starting.

ZBB allows companies to begin with zero as base for every item that is include in there

budgeting list. This eliminated the chances of all the errors by taking all the right factors into

consideration (Zero Based Budgeting, 2019).

This budgeting is beneficial as company is not required to depend over any reference

points for making estimations over budget of particular item. This process requires justification

for every dollar spend over the expense that is occurring on constant basis over the years.

Example – If company each year is spending around 10000 pounds for rent for the warehouse

building. , under process of zero based budgeting it is presumed as no rent was paid previously.

This causes that every activity of the warehouse should be justified, reviewed and needs to be

documented before it is given space in the budget. ZBB in comparison with other popular

budgeting techniques that focuses over incremental changes from current budget and current

expense (Menifield, 2017). In other terms, under typical processes of budgeting rent expense of

10000 pounds is accepted and focus is whether the rent for upcoming budgets are required to

have adjustment for inflation of around 300 pounds or related amounts.

While the ZBB would be much more time taking rather than focusing over incremental

changes related to the next budgets, it results in cost savings significantly. For example ;

Documentation and analysis of warehouse activities that are required by ZBB can lead effective

utilisation of the warehouse space, inventory management etc. If they are managed efficiently

than warehousing budgets may be dragged down to 6000.

5

a) Zero Based Budgeting and its process.

For staying on top of business expenses, companies are are required to plan and update

constantly the business budgets. When companies are using traditional budgeting method they

use previous budgets that might not be effective way of preparing a budget.

Zero Based Budgeting

Zero Based Budgeting is defined as the method that is used for preparing budget of

company for specific time periods under the consideration where the budgets of company are set

from the scratch after all activities of company are re-evaluated from starting.

ZBB allows companies to begin with zero as base for every item that is include in there

budgeting list. This eliminated the chances of all the errors by taking all the right factors into

consideration (Zero Based Budgeting, 2019).

This budgeting is beneficial as company is not required to depend over any reference

points for making estimations over budget of particular item. This process requires justification

for every dollar spend over the expense that is occurring on constant basis over the years.

Example – If company each year is spending around 10000 pounds for rent for the warehouse

building. , under process of zero based budgeting it is presumed as no rent was paid previously.

This causes that every activity of the warehouse should be justified, reviewed and needs to be

documented before it is given space in the budget. ZBB in comparison with other popular

budgeting techniques that focuses over incremental changes from current budget and current

expense (Menifield, 2017). In other terms, under typical processes of budgeting rent expense of

10000 pounds is accepted and focus is whether the rent for upcoming budgets are required to

have adjustment for inflation of around 300 pounds or related amounts.

While the ZBB would be much more time taking rather than focusing over incremental

changes related to the next budgets, it results in cost savings significantly. For example ;

Documentation and analysis of warehouse activities that are required by ZBB can lead effective

utilisation of the warehouse space, inventory management etc. If they are managed efficiently

than warehousing budgets may be dragged down to 6000.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Employees of the company could also be involved for creating ZBB. Employees can

provide for the expenses that will be incurred and where company could expenses of the

business.

It was mainly discussed in 1970's for governments and businesses. Today it is used by various

large organisations for significantly reducing their unneeded expenses.

Zero Based Budgeting Process

Before preparing Zero Based budgets few steps are to be kept in mind. The process follows some

basic steps

Identifying the business goals

Developing and analysing new ways of achieving goals

Discovering new ways for funding the business process

Prioritizing funds

Through these steps of zero based budgeting, company can determine about the expenses that

will go towards achievement of business goals which directly benefits the company. This helps

company in finding new ways for spending.

b) Assess advantages zero based budgeting is having over traditional budgeting.

Advantages of Zero Based Budgeting over traditional budgeting

Profit Centre - The budgeting technique gives priority to profits above the expenses. Therefore

the units or departments that are generating profits whether directly or indirectly are given more

preferences. As result funds are available to the business for generating profits and revenues.

Detailed - Details can help in saving the business. The approach reduces errors and helps

business in looking deeply in the business processes. Due to this inefficiencies are properly

handled and this helps in making the business very effective.

Strategic - As the aim of every business is of growing, to get more customers, and to serve more

clients. The budgeting techniques helps business to become strategic in its approach & only

6

provide for the expenses that will be incurred and where company could expenses of the

business.

It was mainly discussed in 1970's for governments and businesses. Today it is used by various

large organisations for significantly reducing their unneeded expenses.

Zero Based Budgeting Process

Before preparing Zero Based budgets few steps are to be kept in mind. The process follows some

basic steps

Identifying the business goals

Developing and analysing new ways of achieving goals

Discovering new ways for funding the business process

Prioritizing funds

Through these steps of zero based budgeting, company can determine about the expenses that

will go towards achievement of business goals which directly benefits the company. This helps

company in finding new ways for spending.

b) Assess advantages zero based budgeting is having over traditional budgeting.

Advantages of Zero Based Budgeting over traditional budgeting

Profit Centre - The budgeting technique gives priority to profits above the expenses. Therefore

the units or departments that are generating profits whether directly or indirectly are given more

preferences. As result funds are available to the business for generating profits and revenues.

Detailed - Details can help in saving the business. The approach reduces errors and helps

business in looking deeply in the business processes. Due to this inefficiencies are properly

handled and this helps in making the business very effective.

Strategic - As the aim of every business is of growing, to get more customers, and to serve more

clients. The budgeting techniques helps business to become strategic in its approach & only

6

those amounts are spent which are required for growth of business. This will give direction to the

spending of the business and this would become means for achieving something worthwhile.

Situational - ZBB does not encourage practitioners in following the rules and regulations. They

are done with mind of achieving and maximising the wealth of the organisation (Advantages of

ZBB, 2019).

Why Zero based Budgeting over traditional budgeting

Zero based budgets do not consider the budget made in the prior years unlike traditional

budgeting. Traditional budgets reviews budget prepared in previous year and adjust the budgets

of current year based on information given in previous budgets. Zero based budgeting is time

consuming process as compared with traditional budgeting as in this everything is to be started

from the beginning and to frame strategies which are essential for cutting the expenses. This

monitors the expense of every dollar. ZBB is useful in making departmental budgets. Funds

could be allocated to the managers of different department. ZBB cuts down every unnecessary

spending of the company.

Mandatory Systematic Analysis

Before identifying the unit or department that will be getting funds, the budgeting

techniques encourage analysing carefully requirements for funding. The manager should be able

to give appropriate reasons for getting the approvals for funding. Funds will not be given to

particular department that comes down over other reason to choose ZBB over the traditional

budgets.

Ensuring Cost Effectiveness

Major reason behind which the zero based budgets are used because it helps in saving

lots of upfront cost. For instance ; it is observed by manager that one department is not

performing well. Staff of accounting department is not performing well and work is not adding

value in generating profits for the company (Epper and Fehr-Duda, 2015). Two things could be

done in this scenario ; employees could be shifted to other job role that helps them in

appreciating their abilities and talent or the accounting work could be outsourced from the next

year.

7

spending of the business and this would become means for achieving something worthwhile.

Situational - ZBB does not encourage practitioners in following the rules and regulations. They

are done with mind of achieving and maximising the wealth of the organisation (Advantages of

ZBB, 2019).

Why Zero based Budgeting over traditional budgeting

Zero based budgets do not consider the budget made in the prior years unlike traditional

budgeting. Traditional budgets reviews budget prepared in previous year and adjust the budgets

of current year based on information given in previous budgets. Zero based budgeting is time

consuming process as compared with traditional budgeting as in this everything is to be started

from the beginning and to frame strategies which are essential for cutting the expenses. This

monitors the expense of every dollar. ZBB is useful in making departmental budgets. Funds

could be allocated to the managers of different department. ZBB cuts down every unnecessary

spending of the company.

Mandatory Systematic Analysis

Before identifying the unit or department that will be getting funds, the budgeting

techniques encourage analysing carefully requirements for funding. The manager should be able

to give appropriate reasons for getting the approvals for funding. Funds will not be given to

particular department that comes down over other reason to choose ZBB over the traditional

budgets.

Ensuring Cost Effectiveness

Major reason behind which the zero based budgets are used because it helps in saving

lots of upfront cost. For instance ; it is observed by manager that one department is not

performing well. Staff of accounting department is not performing well and work is not adding

value in generating profits for the company (Epper and Fehr-Duda, 2015). Two things could be

done in this scenario ; employees could be shifted to other job role that helps them in

appreciating their abilities and talent or the accounting work could be outsourced from the next

year.

7

Based over routine decisions

In zero based budgets decisions triumphs over the routine where the traditional budgets

almost activities are of routine. In ZBB every thing is questioned, analysis is done of the

approaches and things may also be redone. Because of this there is no space left for wasting

money, time and efforts. Management are also in control as the decisions matter more than the

routine (Han, Zhang and Luo, 2016).

C) Organisations introducing zero based budgeting technique in practical terms.

ZBB is an approach facilitating particular process that evaluated the programs of

company. It allows reductions in the budgets and and also permits re-allocation of resources that

range from low to high priority procedures & programs. It is used as cost analysis tool that helps

company in decision-making.

Companies could modify or develop their own separate approaches for ZBB and these

five will provide baseline for the implementation.

Start – Begin from the ground zero. Creating new annual budgets from the scratch without the

use of previous year's budgets as baseline

Evaluate – Evaluating every area of cost. Reducing and eliminating all the unnecessary services

or activities.

Justify – All components of budget should be accounted. To identify the areas which are

relevant, cost effective and help in driving cost savings.

Streamline – Determining which activities are required to be performed & how they are to be

performed. Standardizing and automating the processes where it is possible.

Execute – Rolling out execution process and comprehensive planning. Communicating the plans

clearly, and also the roles & responsibilities (Zero Based Budgeting, 2019).

CONCLUSION

Carrying out the above study it could be conclude that financial management play an important

role in the business. Financial management helps the organisation in making the strategies for

the business that will help in achievement of the financial goals. All the activities of business

requires funds to carry out its activities and financial management effectively allocates the fund

to different departments. There are various budgeting techniques that are used by organisation to

8

In zero based budgets decisions triumphs over the routine where the traditional budgets

almost activities are of routine. In ZBB every thing is questioned, analysis is done of the

approaches and things may also be redone. Because of this there is no space left for wasting

money, time and efforts. Management are also in control as the decisions matter more than the

routine (Han, Zhang and Luo, 2016).

C) Organisations introducing zero based budgeting technique in practical terms.

ZBB is an approach facilitating particular process that evaluated the programs of

company. It allows reductions in the budgets and and also permits re-allocation of resources that

range from low to high priority procedures & programs. It is used as cost analysis tool that helps

company in decision-making.

Companies could modify or develop their own separate approaches for ZBB and these

five will provide baseline for the implementation.

Start – Begin from the ground zero. Creating new annual budgets from the scratch without the

use of previous year's budgets as baseline

Evaluate – Evaluating every area of cost. Reducing and eliminating all the unnecessary services

or activities.

Justify – All components of budget should be accounted. To identify the areas which are

relevant, cost effective and help in driving cost savings.

Streamline – Determining which activities are required to be performed & how they are to be

performed. Standardizing and automating the processes where it is possible.

Execute – Rolling out execution process and comprehensive planning. Communicating the plans

clearly, and also the roles & responsibilities (Zero Based Budgeting, 2019).

CONCLUSION

Carrying out the above study it could be conclude that financial management play an important

role in the business. Financial management helps the organisation in making the strategies for

the business that will help in achievement of the financial goals. All the activities of business

requires funds to carry out its activities and financial management effectively allocates the fund

to different departments. There are various budgeting techniques that are used by organisation to

8

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

save their costs and eliminate the unnecessary spendings over unproductive activities. Cash

budget is essential as it helps company to track the outflow and inflow of cash. It can than

monitor and control the cash spendings over different activities. Zero based budgets are prepared

by organisations for allocating the resources efficiently to the activities and departments. They

are more preferred over the traditional budgeting as they are not made on e previous estimates

that may have error.

9

budget is essential as it helps company to track the outflow and inflow of cash. It can than

monitor and control the cash spendings over different activities. Zero based budgets are prepared

by organisations for allocating the resources efficiently to the activities and departments. They

are more preferred over the traditional budgeting as they are not made on e previous estimates

that may have error.

9

REFERENCES

Books and Journals

Mitchell, G.E. and Calabrese, T.D., 2018. Proverbs of nonprofit financial management. The

American Review of Public Administration. p.0275074018770458.

Bratton, A., 2018. Cash oriented budget accounting (Doctoral dissertation, Тернопіль: ТНЕУ).

Menifield, C.E., 2017. The basics of public budgeting and financial management: A handbook

for academics and practitioners. Rowman & Littlefield.

Epper, T. and Fehr-Duda, H., 2015. Risk preferences are not time preferences: balancing on a

budget line: comment. American Economic Review. 105(7). pp.2261-71.

Han, K., Zhang, C. and Luo, J., 2016. Taming the uncertainty: Budget limited robust

crowdsensing through online learning. IEEE/ACM Transactions on Networking

(TON). 24(3). pp.1462-1475.

Online

Cash Budgets. 2019. [Online]. Available through : <https://debitoor.com/dictionary/cash-

budget>.

Financial Management. 2019. [Online]. Available through :

<https://www.managementstudyguide.com/financial-management.htm>.

Zero Based Budgeting. 2019. [Online]. Available through :

<https://www.wallstreetmojo.com/zero-based-budgeting/>.

Advantages of ZBB. 2019. [Online]. Available through : <https://www.anaplan.com/blog/zbb-

zero-based-budgeting-guide/>.

10

Books and Journals

Mitchell, G.E. and Calabrese, T.D., 2018. Proverbs of nonprofit financial management. The

American Review of Public Administration. p.0275074018770458.

Bratton, A., 2018. Cash oriented budget accounting (Doctoral dissertation, Тернопіль: ТНЕУ).

Menifield, C.E., 2017. The basics of public budgeting and financial management: A handbook

for academics and practitioners. Rowman & Littlefield.

Epper, T. and Fehr-Duda, H., 2015. Risk preferences are not time preferences: balancing on a

budget line: comment. American Economic Review. 105(7). pp.2261-71.

Han, K., Zhang, C. and Luo, J., 2016. Taming the uncertainty: Budget limited robust

crowdsensing through online learning. IEEE/ACM Transactions on Networking

(TON). 24(3). pp.1462-1475.

Online

Cash Budgets. 2019. [Online]. Available through : <https://debitoor.com/dictionary/cash-

budget>.

Financial Management. 2019. [Online]. Available through :

<https://www.managementstudyguide.com/financial-management.htm>.

Zero Based Budgeting. 2019. [Online]. Available through :

<https://www.wallstreetmojo.com/zero-based-budgeting/>.

Advantages of ZBB. 2019. [Online]. Available through : <https://www.anaplan.com/blog/zbb-

zero-based-budgeting-guide/>.

10

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.